china taiping insurance holdings company limited 2016 ... · at 31 dec 2014 at 31 dec 2015 at 31...

TRANSCRIPT

23 March 2017

China Taiping Insurance

Holdings Company Limited

2016 Annual Results

Presentation

2

Forward-looking Statements

This presentation and subsequent discussions may contain certain forward-looking statements with respect to the financial condition, results of operations and businesses of the CTIH Group. These forward-looking statements represent the CTIH Group’s expectations or beliefs concerning future events and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements

3

Note (1):Ageas owns the remaining 24.9%, 20% and 20% equity interests in TPL, TPeC and TPAM, respectively. Note (2):PT Megah Putra Manunggal owns the remaining 45% equity interest in TP Indonesia. Note (3):TPSM and TPR (BJ) are wholly-owned subsidiaries of TPL. CTIH’s effective interest in TPSM and TPR (BJ) is 75.1%. Note (4):TPIH and TPL own 61% and 39% of the equity interests of TPR (SH), respectively. CTIH’s effective interest in TPR (SH) is 90.3%. Note (5):TPL, TPI and TPPM own 60%, 20% and 20% of the equity interests in TPR (Suzhou), respectively. CTIH’s effective interest in TPR (Suzhou) is 85.1%. Note (6):TPL and TPI own 80% and 20% of the equity interests in TPR (Nanning), respectively. CTIH’s effective interest in TPR (Nanning) is 80.1%. Note (7):Sinopec Group Company owns the remaining 50% equity interests in TSFL. Note (8):In addition to operating its own business lines, TPIH, TPSM and TPP also act as investment platforms in the asset management business. Note (9):The above structure was as of 31 Dec 2016.

Simplified Company Structure

Substantial Success in the “Boutique Strategy”, Significant Increase in

Business Value, Business Scale Continued to Grow Steadily

Total premium reached HK$149.3 billion, increased by 7.8% over the Last Year

Total assets were over HK$505.4 billion, increased by 3.6% over the last year-end

Profit attributable to owners was HK$4.774 billion, decreased by 24.7% over the Last Year, better than

industry average

Life insurance’s new business value was HK$9.115 billion, increased by 28.8% over the Last Year

(increased by 37.6% in terms of RMB);under the same assumption, life insurance’s new business

value increased by 49.9% over the Last Year (increased by 60.1% in terms of RMB)*

Group embedded value per share attributable to owners was HK$28.5, increased by 4.6% over the last

year-end figure of HK$27.3, while TPL’s embedded value increased by 5.3% over the end of Last Year

(increased by 12.4% in terms of RMB); under the same assumption, TPL’s embedded value increased by

11.7% over the last year-end (increased by 19.2% in terms of RMB)*

The Board recommended the payment of a final dividend of HK10 cents per share

The combined ratio of property and casualty insurance and reinsurance business remained stable,

continued in making underwriting profit

4 * Calculated in accordance with the C-Ross assessment standard

Highlights and Consolidated Results of Operations

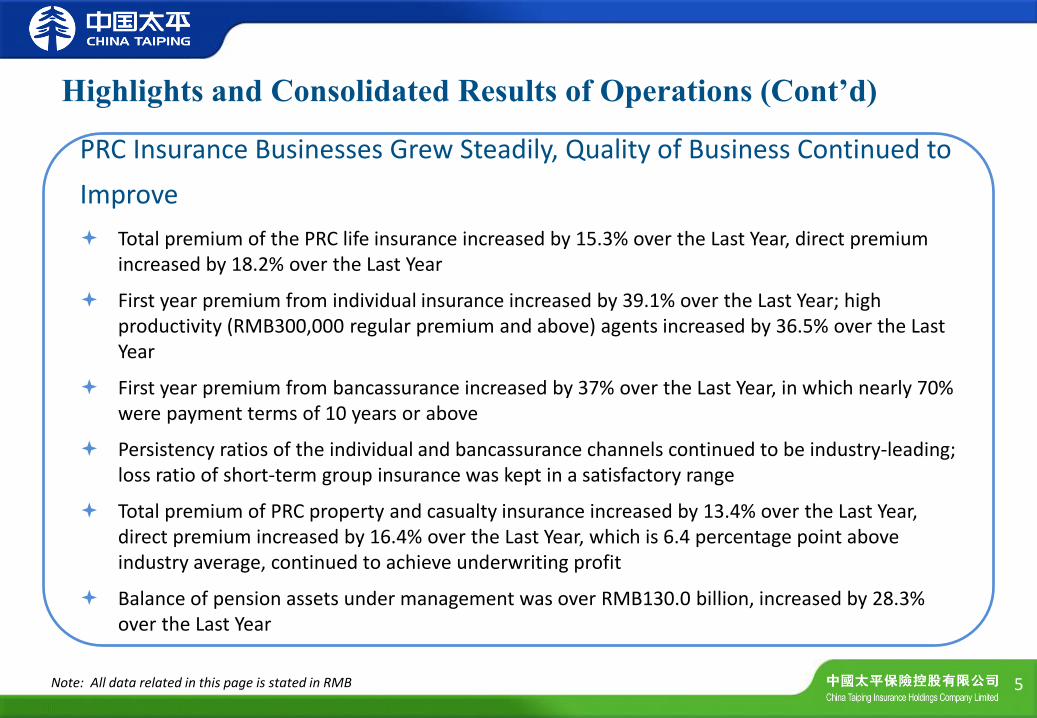

PRC Insurance Businesses Grew Steadily, Quality of Business Continued to

Improve

Total premium of the PRC life insurance increased by 15.3% over the Last Year, direct premium increased by 18.2% over the Last Year

First year premium from individual insurance increased by 39.1% over the Last Year; high productivity (RMB300,000 regular premium and above) agents increased by 36.5% over the Last Year

First year premium from bancassurance increased by 37% over the Last Year, in which nearly 70% were payment terms of 10 years or above

Persistency ratios of the individual and bancassurance channels continued to be industry-leading; loss ratio of short-term group insurance was kept in a satisfactory range

Total premium of PRC property and casualty insurance increased by 13.4% over the Last Year, direct premium increased by 16.4% over the Last Year, which is 6.4 percentage point above industry average, continued to achieve underwriting profit

Balance of pension assets under management was over RMB130.0 billion, increased by 28.3% over the Last Year

5 Note: All data related in this page is stated in RMB

Highlights and Consolidated Results of Operations (Cont’d)

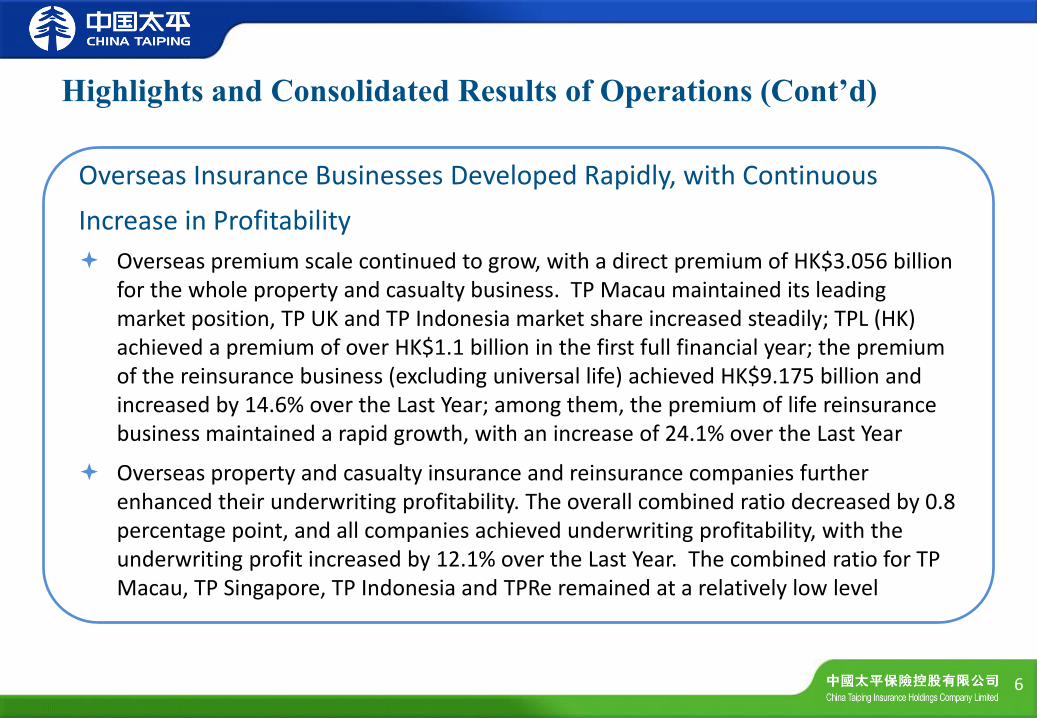

Overseas Insurance Businesses Developed Rapidly, with Continuous

Increase in Profitability

Overseas premium scale continued to grow, with a direct premium of HK$3.056 billion for the whole property and casualty business. TP Macau maintained its leading market position, TP UK and TP Indonesia market share increased steadily; TPL (HK) achieved a premium of over HK$1.1 billion in the first full financial year; the premium of the reinsurance business (excluding universal life) achieved HK$9.175 billion and increased by 14.6% over the Last Year; among them, the premium of life reinsurance business maintained a rapid growth, with an increase of 24.1% over the Last Year

Overseas property and casualty insurance and reinsurance companies further enhanced their underwriting profitability. The overall combined ratio decreased by 0.8 percentage point, and all companies achieved underwriting profitability, with the underwriting profit increased by 12.1% over the Last Year. The combined ratio for TP Macau, TP Singapore, TP Indonesia and TPRe remained at a relatively low level

6

Highlights and Consolidated Results of Operations (Cont’d)

Steady Development of the Investment Business

The asset scale grew steadily. At the end of 2016, the total investment assets of the Group is HK$425.2 billion, increased by 14.1% over the beginning of the Year; the third-party entrusted investment assets amounted to HK$296.0 billion, increased by 26.6% over the beginning of the Year

Reinforced investment income base. In 2016, the Group recorded an investment income of HK$20.018 billion and a net investment income of HK$17.656 billion, representing an increase of 13.1%, which indicates that the Group has well coped with the market fluctuations and laid the foundation for its income base

Traditional investments were prudent and active . As at the end of 2016, the allocation of equity securities and investment funds is 8.1%, 5.2 percentage point lower than the industrial average; domestic available for sale debt investments outperformed the Total Wealth Index of ChinaBond by 95 bp and the Wind Bond Fund Index by 185 bp; the Group’s assets credit risk screening shows sound risk management results

7

Highlights and Consolidated Results of Operations (Cont’d)

Effective Implementation of Strategic Cooperation and Cross-selling

Initiatives with Large Clients

In 2016, China Taiping signed Group Strategic Cooperation Agreements with 16 large clients, including China Everbright Group, Ant Financial and CRRC Group. As at the end of 2016, China Taiping had established strategic cooperation relationships with 68 large clients

Our cross-selling initiatives achieved HK$4.543 billion insurance sales, including HK$3.826 billion of property insurance sales through TPL, HK$0.620 billion of pension sales through TPL, and HK$97 million of property insurance sales through TPP

The Sinopec gas station project achieved rapid development, achieving HK$1.756 billion of insurance sales for the full year of 2016, increased by 51.4% over the Last Year. 5,160 outlets had been stationed by the end of 2016

8

Highlights and Consolidated Results of Operations (Cont’d)

HK$ million 2016 2015 Change

Life Insurance 4,843.41 6,697.77 -27.7%

PRC Property and Casualty Insurance 552.11 821.25 -32.8%

Overseas Property and Casualty Insurance and Reinsurance

920.79 888.41 +3.6%

Pension and Group Life Insurance 24.18 178.36 -86.4%

Others 1 (38.01) (417.55) +90.9%

Net Profit from operations 6,302.48 8,168.24 -22.8%

Non-controlling interests (1,528.23) (1,827.00) -16.4%

Net profit attributable to the owners 4,774.25 6,341.24 -24.7%

1 Others mainly include the operating results of the holding company, asset management, TPeC, TPIH, TPFH and consolidation adjustments. 9

Net Profit by Business Segment

As TPL (HK) is a newly established company in 2015 and its business is still in its initial state, the results under life insurance business for the Year of 2016 is still mainly contributed by TPL. The following figures are the results of TPL from its operations, before intra-group eliminations.

• TPL

• TPL (HK)

Life Insurance Business Review

Note: The Group holds 75.1% of the equity interest in TPL, and 100% in TPL (HK)

10

Direct Premiums Written

(HKD million)

Comprehensive Solvency Ratio

11

Note: 1.Direct Premium Written growth is 18.1% in terms of RMB

2.TPL redeemed all of its residual subordinated notes in 2016

110,395

2016 2015

+10.9% 251%

271%

At 31 Dec 2016 At 31 Dec 2015

C-Ross

99,538

Life Insurance: Premiums Maintained Steady Growth, with

Sufficient Solvency

C-Ross

2015 2016

2,268 2,578

43,295 43,632

53,975 64,185

Further Increase in Proportion of Individual Agency Business (HKD million,%)

Individual

Group and other channels*

Bancassurance

12 * Other channels is mainly telemarketing

2015 2016

54%

44%

2%

58%

40%

2%

Life Insurance: Structure of Gross Premiums – By Distribution

Channels

13

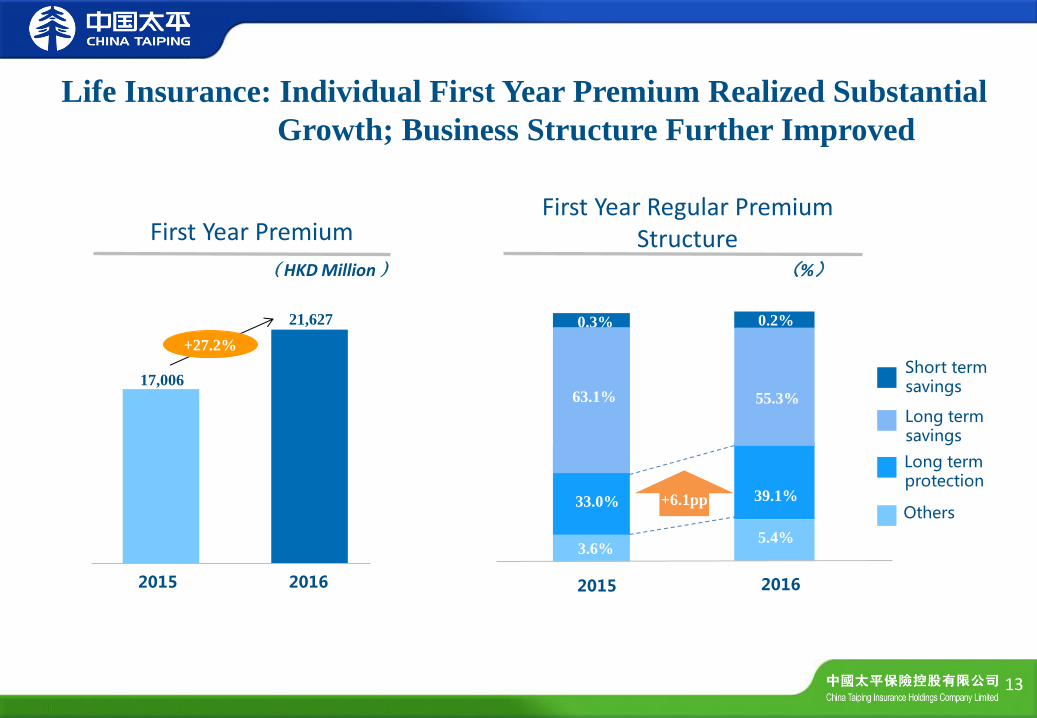

First Year Premium

(HKD Million)

21,627

17,006

2016 2015

+27.2%

Life Insurance: Individual First Year Premium Realized Substantial

Growth; Business Structure Further Improved

First Year Regular Premium Structure

(%)

2015 2016

3.6%

33.0%

0.3%

5.4%

39.1%

55.3%

0.2%

63.1%

Short term savings

Others +6.1pp

Long term savings

Long term protection

Life Insurance: Agency Force Realized Rapid Growth; High

Productivity Agents Grew Substantially

Number of Agents

14

(person)

261,922

231,766

+13.0%

* RMB300,000 regular premium above

10,066

7,373

+36.5%

Number of High Productivity Agents*

(person)

At 31 Dec 2016 At 31 Dec 2015 At 31 Dec 2016 At 31 Dec 2015

15

Note:1.Assumption Change: The annual investment return of 2016 is assumed to be adjusted from 5.5% to 5.0%, and the risk discount rate remained unchanged, and similarly hereinafter

2.NBV Margin=NBV/First Year Annualized Premium; First Year Annualized Premium=First Year Regular Premium + Single Premium/10 3.Year 2016*: result from the same valuation assumptions of 2015 unless otherwise specified, similarly hereinafter

Individual NBV Margin

Life Insurance: Individual NBV Margin Kept Growing

2016* C-Ross

2015 Solvency l

2015 C-Ross

2016 C-Ross

36.2%

43.6% 42.8%

48.2%

+7.4pp

+4.6pp -5.4pp

Standard Change

Business Growth

Assumption Change

First Year Regular Premium

16

(HKD million)

4,207

3,271

2016 2015

+28.6%

Life Insurance: Bancassurance Channel First Year Regular Premium

Grew substantially; Business Structure Kept Improving

Premium Structure

2015 2016

52.6%

39.8%

7.6%

49.8%

40.6%

9.6%

First year regular premium

(%)

Renewal regular premium

Single premium

91% 92%

94%

89% 87%

89%

第13个月之保费继续率

第25个月之保费继续率

93% 93%

95%

89% 88% 89%

第13个月之保费继续率

第25个月之保费继续率

Individual Bancassurance

Persistency ratio – 13th month

Persistency ratio – 25th month

At 31 Dec 2014 At 31 Dec 2015 At 31 Dec 2016 At 31 Dec 2014 At 31 Dec 2015 At 31 Dec 2016

Persistency ratio – 25th month

17

Note: According to communications with peers, TPL was No.1 in both Individual and Bancassurance Channels in terms of 13th month persistency ratio

Persistency ratio – 13th month

Life Insurance: Persistency Ratios Stood at the Forefront of the

Industry

81,862

87,422

92,049 97,610

41,351

40,511

45,511

41,911 53,480

44,130

47,919

44,130

18 ** YoY growth is 19.2% in terms of RMB

+6.8%

+11.7%** -5.7%

Adjusted Net

Worth

In-force Business

Value

+3.5%

+27.6% -10.4%

92,049

87,422

At 31 Dec 2016

+5.3%

At 31 Dec 2015

Embedded Value

Life Insurance: Embedded Value Realized Steady Growth

(HKD million)

2015 Solvency l

2015 C-Ross

2016* C-Ross

2016 C-Ross

Standard Change

Business Growth

Assumption Change

(HKD million)

Standard Change & Assumption Change Moving Analysis

C-Ross C-Ross

19

* Including differences between the actual experience and expected experience in terms of investment return, dividend, mortality, morbidity, lapses, expenses ,etc., as well as exchange rate impact arising from the exchange rate of the RMB

92,049

87,422

9,115

6,672

2,310

(7,015) (2,194)

(4,261)

Embedded Value as at the end of

2015

Expected Return on Embedded

Value

New Business

Value

Minimum Capital

Dispersion Effect

Assumption and Model

Change

Embedded Value as at the end of

2016

Experience Variance

and Others*

Capital Injection or Dividend to

Owners

(HKD million)

Life Insurance: Movement Analysis of Embedded Value

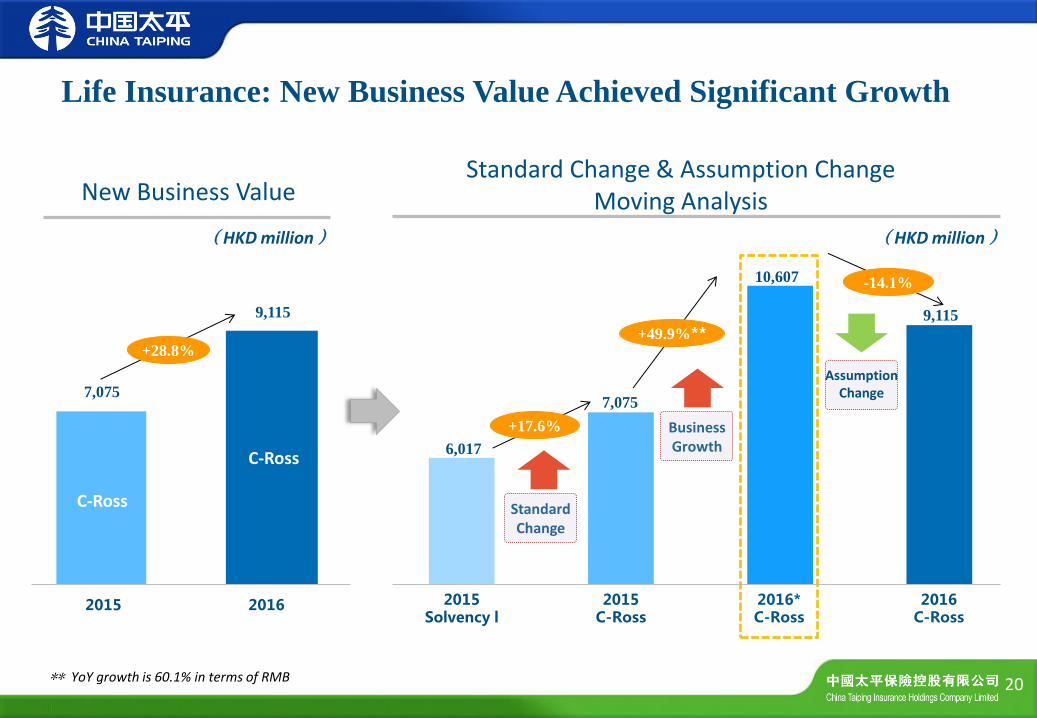

C-Ross C-Ross

7,075

6,017

9,115

10,607

20 ** YoY growth is 60.1% in terms of RMB

+17.6%

+49.9%**

-14.1%

2016 2015

7,075

9,115

+28.8%

New Business Value

Life Insurance: New Business Value Achieved Significant Growth

(HKD million)

Standard Change & Assumption Change Moving Analysis

(HKD million)

Standard Change

Business Growth

Assumption Change

2015 Solvency l

2015 C-Ross

2016* C-Ross

2016 C-Ross

C-Ross

C-Ross

21

NBV Margin

Life Insurance: NBV Margin Kept Improving

28.0%

32.9% 33.5%

39.0%

+4.9pp

+6.1pp -5.5pp

Standard Change

Business Growth

Assumption Change

2015 Solvency l

2015 C-Ross

2016* C-Ross

2016 C-Ross

• TPI

Mainland P&C Insurance

Business Review

Note:The Group holds the 100% equity interest of TPI

The following figures are the results of TPI from its operations, before intra-group eliminations. 22

Direct Premiums Written

(HKD million)

At 31 Dec 2016 At 31 Dec 2015

Comprehensive Solvency Ratio

23

21,269

19,447

2016 2015

+9.4%

206%

268% -62pp

Note: The decrease of solvency ratio is mainly due to premium growth, increase in the unlisted equity and trust plans, as well as adjustment to impenetrability of asset management products.

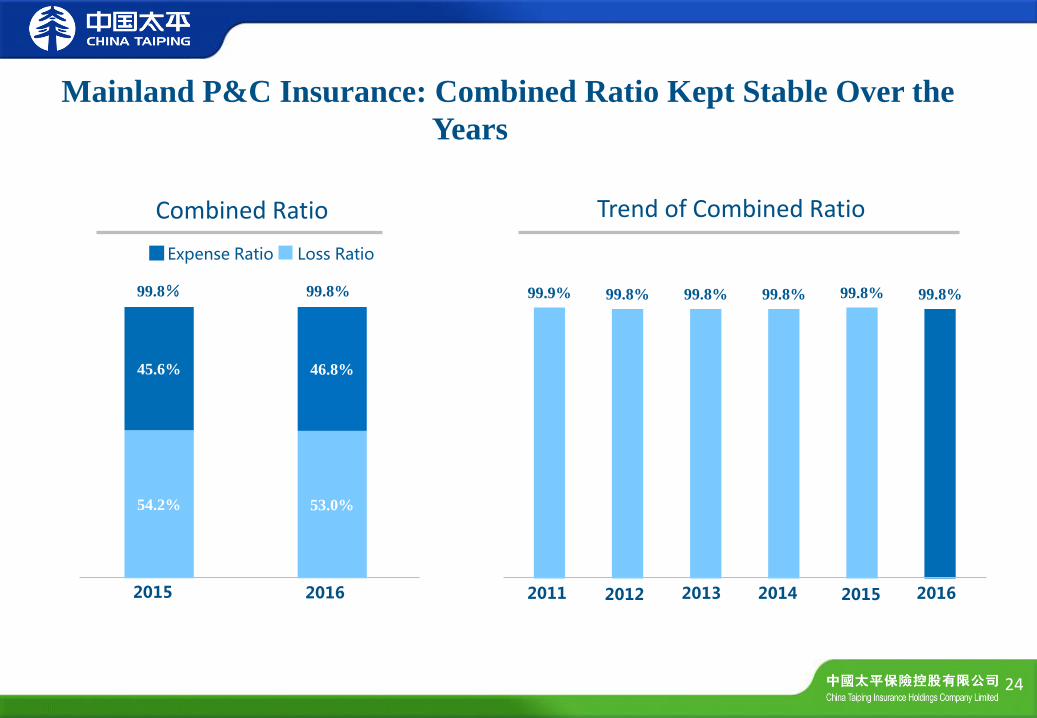

Mainland P&C Insurance: Premiums Kept Growing, with

Sufficient Solvency

C-Ross C-Ross

54.2% 53.0%

45.6% 46.8%

2015 2016

Combined Ratio Trend of Combined Ratio

24

Expense Ratio Loss Ratio

99.8% 99.8% 99.9% 99.8% 99.8% 99.8% 99.8% 99.8%

2016 2015 2014 2013 2012 2011

Mainland P&C Insurance: Combined Ratio Kept Stable Over the

Years

The following figures are the results of the respective companies from their respective operations,

before intra-group eliminations.

Overseas P&C Insurance and Reinsurance Businesses Review

HK & Macau

• CTPI (HK)

• TP Macau

Overseas

• TP Singapore

• TP UK

• TP Indonesia

Reinsurance

• TPRe

• TPRe (China)

25

Note:The Group holds 55% of the equity interest in TP Indonesia, and 100% in the other companies listed above

3,016

1,983

1,033

3,056

1,959

1,097

2015

2016

Overseas P&C Direct Premiums Written

Reinsurance Premiums Written**

( HKD million ) ( HKD million )

26

* Excluding innovative type of business; Premiums for Overseas P&C is HK$3.895 billion, and HK$2.862 billion for HK & Macau if including innovative type of business in 2015

Overseas P&C*

HK & Macau*

Other Overseas

3,404 4,224

4,601

4,951

2015 2016

-1.2%

+6.2%

+1.3%

+14.6% 8,005

9,175

** Including business of TPRe (China) and excluding universal insurance

Overseas P&C Insurance and Reinsurance: P&C Premiums Kept

Increasing; TPRe Life Reinsurance Continued to Achieve Breakthroughs

Life

Non-Life

94.3% 95.9%

92.3% 93.3% 93.5%

94.8% 92.6% 92.9%

* non-life reinsurance business

Combined Ratio

27

-1.1pp +0.3pp -0.4pp -0.8pp

Overseas P&C and Re

HK & Macau Other Overseas Reinsurance*

Overseas P&C Insurance and Reinsurance: Combined Ratios

Decreased, With Further Business Quality Improvement

2015

2016

The following figures are the results of TPP from its operations, before intra-group eliminations.

• TPP

Pension and Group Life Insurance Businesses Review

Note: The Group holds 100% of the equity interest in TPP

28

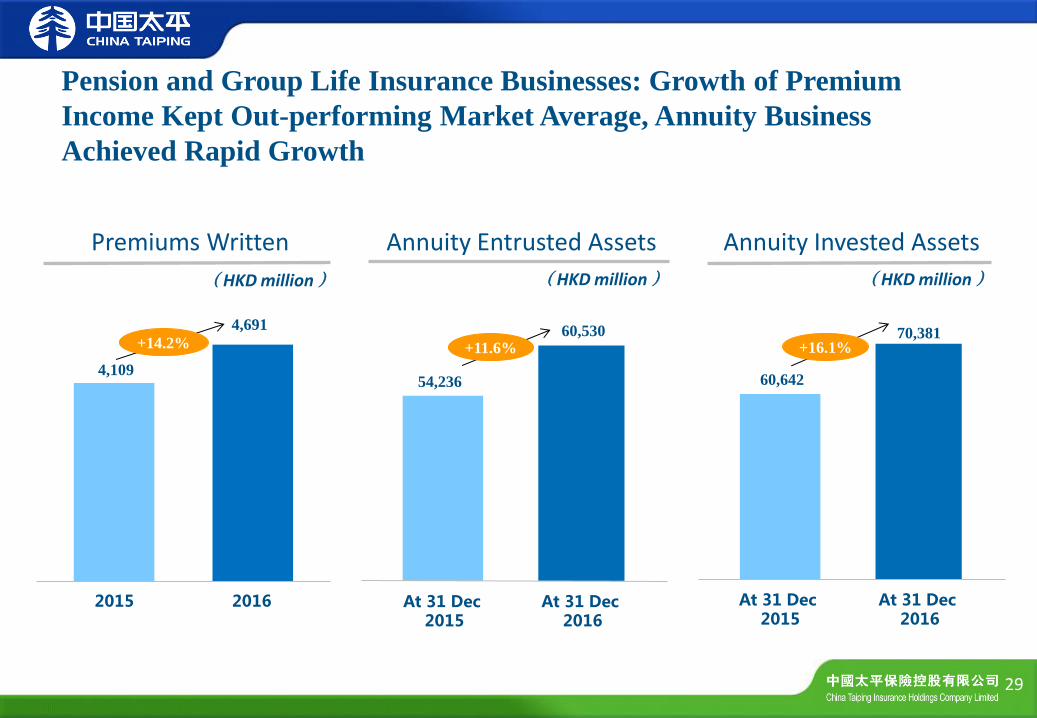

Pension and Group Life Insurance Businesses: Growth of Premium

Income Kept Out-performing Market Average, Annuity Business

Achieved Rapid Growth

(HKD million)

Annuity Entrusted Assets

At 31 Dec 2016

At 31 Dec 2015

Annuity Invested Assets

At 31 Dec 2016

At 31 Dec 2015

(HKD million) (HKD million)

29

60,530

54,236

+11.6% 70,381

60,642

+16.1%

Premiums Written

2016 2015

4,109

+14.2%

4,691

Investment

30

372,667

425,180

31

% of Total 2015 2016

Fixed income 72.8% 73.6%

Debt securities 38.8% 38.7%

Term deposits 9.2% 10.9%

Debt products 19.3% 17.6%

Other fixed income investments 5.5% 6.4%

Equity investments 14.4% 13.3%

Equity securities 7.0% 5.2%

Investment funds 3.4% 2.9%

Other equity investments 4.0% 5.2%

Investment properties 3.3% 4.6%

Cash, cash equivalents and others 9.3% 8.5%

Total 100.0% 100.0%

(HKD million)

Investment Assets

At 31 Dec 2015 At 31 Dec 2016

Note: Figures may not match totals due to rounding.

+14.1%

Allocation of Investment Assets of the Group

15,615 17,656

11,042

2,362

0

5,000

10,000

15,000

20,000

25,000

30,000

26,657

5.01% 7.97%

20,018

-24.9%

32

Note: 1.Including the income from the spread of investment securities, gain or loss on changes in fair value and impairment loss.

2.Including the interest income from deposit, interest income from bonds, dividends from equity investments, rental income from investment properties and deducting interest expense on securities sold under resale agreements.

3.In the calculation of total investment yield, as the denominator, the average investment assets takes into account the effect of securities purchase under resale agreements and securities sold under repurchase agreements.

(HKD million)

Total investment yield 3

Net Realized and unrealized investment gains 1

Net investment income 2

2016 2015

Investment Income

86.5% of the debt securities held by the Group were domestic bonds. 97.2% out of such domestic bonds were government bonds (GB) , financial policy bonds (FPB) with high credit ratings and corporate bonds rated AAA. Investment grade bonds with BBB ratings and above reached 100%

Foreign bonds accounted for the remaining 13.5%, of which 86.2% were investment grade with international ratings, while the remaining were issued by government and large corporations, with adequate credit enhancements.

33

Debt Investments: High Credit Ratings of Debt Asset

46.2%

33.1%

17.9%

1.8% 1.0% 0.0% 0.0%

Credit ratings of domestic bonds

AAA GBs FPBs AA+ A-1 AA- AA

Local Government Debt Financing

Within the local government debt investments, 72% were from provincial or sub-provincial platform, lower level platform projects are guaranteed by the banks

By sector, 63% of them were in the transport and municipal industries, in line with the insurance capital investment infrastructure construction policy guidance

By credit enhancements, 66% were guaranteed by commercial banks or its holding companies, projects exempted from guarantee were debtors of relatively strong repayment ability. The average yield was 5.8% or above, and the average maturity was 6.5 years

Real Estate Financial Investment Debt Products

Real estate financial investment debt products is approximately HK$14.5 billion, representing only 2.8% of the total assets

The credit ratings of the real estate financial investment debt products remained stable

Major projects were located in tier 1 or developed tier 2 cities

Purchased External Financial Products

In 2016, under the background of asset shortage, the Group has actively invested in external financial products and allocated HK$19.8 billion to purchased external alternative assets, with an average yield of 5.3%

Within the purchased external projects, 68% were trust schemes and real estate debt schemes, 82% were in real estate, financial and municipal industries, 76% were guaranteed by commercial banks or its holding companies

Note: including exposures to each other, which is not directly in the total

Alternative investments has been further diversified The proportion of alternative investments held by the Group to total investment assets was 27.7%, from which

"South-to-North Water Diversion" project accounted for HK$11.7 billion. If "South-to-North Water Diversion" project is excluded, the proportion of alternative investments to total investment assets was 25.0%.

Domestic financial investment debt products are mainly debt schemes, with the ratio of trust products and asset management products increased, reflecting the investments has been further diversified.

34

Alternative Investments

Alternative investments risk remained at a low level

Outlook

35

Continuously Advancing the “Boutique Strategy”, balanced expanding of Scale and Value In 2017 and the coming period, China Taiping will actively cope with changes from the macro economy and

market, stick to established strategies, adhere to the working policy of “Steady Growth, Innovation-driven, Lower Cost and Higher Efficency, Strictly Controlling Risks”, devote great attention to the development of core businesses, promote the establishment of investment platforms, optimise the structure of principal businesses, strengthen the innovation of products, business models, management and services, boost the strategic layout for its internationalisation, enhance the synergistic effect between insurance and investment, safeguard against financial risks, strengthen the operation model with its own characteristics by seeking balance between the development of insurance and investment, and thereby endeavor to create more value for shareholders, clients and the society

36

TPL TPL will further improve channel management, continuously optimise procedures and models, promote the

professional operation standards, ensure rapid and healthy development of core businesses, continue to strengthen our industry leading position in persistency ratios and build the professional features of Taiping

TPL will drive individual insurance by “products, agency force, institutions and projects”, improve the development layout of individual insurance, focus on both scale and value, aiming to achieve breakthroughs in various indicators; bancassurance will be value-driven, focus on expanding and strengthening its high value regular premium business

Outlook

TPI To speed up the establishment of professional channels for motor insurance, promote the

expansion of innovative business and strategic sectors, improve the institutional productivity as well as optimise the business structure, actively respond to the implementation and marketisation of the motor insurance rates, further strengthen the risk control and commit concrete efforts to reduce claims and losses, so as to enhance the business value and operating efficiency of the Company

TPP To strengthen, optimise and expand the core business of group insurance and the scale of

pension assets under management, and put great emphasis on the optimisation of business structure, operating model, operational services and profit structure, and accelerate the innovative development, so as to enhance the internal dynamics of the development of the Company

TPL (HK) To continuously grasp the development opportunities in the life insurance market in Hong Kong,

accelerate the business development and realise the objectives of “Creating unique product features, achieving outstanding sales results and establishing good service reputation”

37

Outlook (Cont’d)

Overseas Business Overseas Property and Casualty insurance companies will reinforce company infrastructure,

strengthen refine management, improve customer service, strengthen corporate comprehensive management, and further promote their business quality

CTPI (HK) and TP Macau will further explore the potential in local markets and improve the innovation of products and channels, so as to maintain their leading positions; TP Singapore, TP UK and TP Indonesia will continue to serve the national strategies of “Going Global” and “The Belt and Road”, actively provide risk coverage for overseas projects for Chinese enterprises, and continue rapid growth of their business

Reinsurance Business TPRe will maintain the synchronised growth between scale and efficiency, promote the overall

customer service ability, enhance market position, accelerate the global business layout and improve the international management capabilities

TPRe (China) will promote the development of the company and lay a solid foundation, strive to build up the company's core competitiveness and enhance its market position

38

Outlook (Cont’d)

Investment To build a complete investment segment. The Group will be dedicated to develop an

investment layout covering domestic and overseas, specialising comprehensive and professional fields, integrating traditional and alternative investments, and featuring prominent advantages, resources sharing, rational labor division and effective synergies

To thoroughly exhibit the concept of value investing. The Group will fully utilise the advantages of insurance funds on long term investments, and implement the idea of value investing in areas such as the strategic allocation of assets and the selection of investments

To capture investment priority in line with the state strategies. In view of the national industrial transformation and upgrading, the Group’s investment priority will focus on, among other things, strategic emerging industries, modern manufacturing industry and modern agriculture; in view of the "three state strategies", the Group’s investment priority will focus on, among other things, “The Belt and Road”, Beijing-Tianjin-Hebei Economic Belt and Yangtze River Economic Belt; the Group will also actively invest in major infrastructures and people livelihood projects through various innovative ways.

To serve the insurance business while emphasising on strategic synergies. The Group will improve its investments and efforts in areas that are conform to its principal business, such as pension, health, medical care and automobile industry chain

39

Outlook (Cont’d)

Questions and Answers

40