china passenger vehicle fuel consumption development

TRANSCRIPT

InnovationCenterforEnergyandTransportation(iCET)

December2017

ChinaPassengerVehicleFuelConsumptionDevelopmentAnnualReport2017

-1-

TheInnovationCenterforEnergyandTransportation(iCET)

Phone:+86.10.65857324|Fax:+86.10.65857394

Email:[email protected]|Website:www.icet.org.cn

Acknowledgements

WewishtothanktheEnergyFoundationforprovidinguswiththefinancialsupportrequiredfortheexecutionofthisreportandsubsequentresearchwork.Wewouldalsoliketoexpressoursincerethanksforthevaluableadviceandrecommendationsprovidedbythefollowingdistinguishedexpertsandcolleagues:Prof.WangHewu,Prof.OuXunmin,JinYongfuandXinYan.

ReportTitle

ChinaPassengerVehicleFuelConsumptionDevelopmentAnnualReport2017

ReportDate

December2017

AuthorsLipingKang,LanzhiQin,MayaBenDror,FengAn

-2-

CONTENT

EXECUTIVESUMMARY......................................................................................................................................................3

1. INTRODUCTION:THEDRIVINGFORCEBEHINDCHINA’SPASSANGERVEHICLEENERGYMANAGEMENT.....................................................................................................................................................................11

2. CHINA’SPASSENGERCARSFUELCONSUMPTIONSTANDARD.......................................................132.1PASSENGERCARSFUELCONSUMPTIONSTANDARDSYSTEM............................................................................132.2THEFOURTHPHASEOFCHINA’SFCSTANDARD.................................................................................................15

3. CHINA'SFUELCONSUMPTIONANDNEWENERGYVEHICLEDOUBLEINTEGRALMANAGEMENT.....................................................................................................................................................................163.2FUELCONSUMPTIONANDNEWENERGYVEHICLEINTEGRATEDACCOUNTING...........................................163.3CREDITSTRADINGMECHANISM...............................................................................................................................203.4CREDITSMANAGEMENT.............................................................................................................................................203.5DIFFICULTIESANDCHALLENGESONENERGYEFFICIENCYMANAGEMENT...................................................21

4. COMPARISONBETWEENCHINA’SNEVCREDITSANDCALIFORNIA’SZEVCREDITS........22

5. CURRENTSTATUSANDTRENDSFORPASSENGERCARFCINCHINA.......................................265.1REPORTEDFCVALUELARGELYUNCHANGED......................................................................................................265.22016CAFCCOMPLIANCESTATUS.........................................................................................................................285.3FUELCONSUMPTIONTRENDS...................................................................................................................................305.4BRANDFCPERFORMANCE........................................................................................................................................325.5IMPACTOFSUVANDMPVMARKETEXPANSIONONCHINA’SNATIONALFCPERFORMANCE................33

6. CHINACAFCNEV(SUPER-)CREDITSANDNEVCREDITS.................................................................366.1CORPORATECAFCNEVSUPER-CREDITS............................................................................................................366.2NEVCREDITS...............................................................................................................................................................386.3NEVCREDITSIMPACT:CONCLUDINGREMARKS..................................................................................................41

BIBLIOGRAPHY....................................................................................................................................................................44

-3-

ExecutiveSummary

China'stotaloilconsumption in2016reached556milliontonsrepresentingarateofoil import

dependenceashighas65.5%.Transportationaccountedformorethanhalfoftotaloilconsumption

lastyear,ofwhichpassengercarfuelconsumptioncontributed110milliontons,about90%oftotal

gasolineconsumption(andabout20%of totaloildemand).China’s fueleconomystandardsand

managementregulationwereapprovedasoneofthemosteffectiveeffortstoimprovefuelefficiency

and energymanagement regulation. The standardsweremeant to reduce oil consumption and

advanceChina’senergysecurity.

SinceChinaimplementedpassengervehiclefuelconsumptionstandardsin2005,itunderwentfourphases.Themostrecentone(PhaseIV)enteredintoeffectin2016.In2013,Chinaintroducedtheaverage corporate fuel consumption (CAFC) standard, as part of a series of flexibilitymechanismsthatwereintroducedin2017.Alsoin2017,ChinaannouncedtheformationofanNEVcreditssystemthatwilloperateundertheCAFCstandardregime,andenterintoeffectin2019.

TheInnovationCenterforEnergyandTransportation(iCET)hasbeeninvolvedinthedraftingofChina’sfuelstandardssinceitsfirstiterationandhasbeentrackingitsdevelopmentsince.Thisreport is the7th iCETAnnualReportevaluatingChina’sCAFCstandard implementationstatus with recommendations for policy. This year the report, although covering variousaspects of China’s corporate FC development, places considerable focus on the jointmanagementmechanism of China’s existing CAFC standard and the newly introducedNEVcreditssystem.

Thehighlightsofthisyear’sreportaregroupedaroundthreethemes:(I)fuelefficiencyandtheCAFCstandardregime,(II)NEVsuper-credits(flexibilitymechanism)andCAFCperformance,and,(III)thenewlyintroducedNEVcreditssystemandtheCAFCstandardregime.

I.FuelefficiencyandCAFC:

1. PhaseIVrequirementshaveincreasedinstringencyfrom2016to2020,andthenumberofcompaniesthatfailedtomeetthecorporateaveragefuelconsumptionrequirements

hasgrownin2016whentheflexibilitymechanismwasexcludedfromCAFCcalculations.

About30%ofdomesticmanufacturersand20%ofimportersfailedtomeetthestandard(the

latterisupfromamere4%in2015,thefinalyearofPhaseIII).Thesenon-compliantcompanies

cumulativelysoldover5.68millioncarsin2016,ledbyChangan(ChanaFord,ChanaAuto)and

GreatWall.

-4-

Note:Onlycorporationswithabove100,000unitperyearincluded;bubblesizeindicativeofproductionvolume; NEV

creditsexcludedfromCAFCcalculations.

Improvements intheFCratedecreased inpacesincePhaseIVwas implemented.Fordomestic independentmanufacturers, average FC even increased from2013 to 2016(when the flexibility mechanism was excluded from calculations). Based on FC datareportedbymanufacturersandpublishedbyMIIT,anannualaveragereductionof1.7%wasachieved during a decade of implementation, with importers, JVs, and independentmanufacturers reaching anannual average reduction rateof2.7%,2.2%,and less than1%,respectively.

Note:NEVcreditsexcludedfromCAFCcalculations.

2. Theincreaseofaveragevehicleweightisstymieingfurtherreductionsinpassengercarfuelconsumptionrates,whichtranslatestoFCincreaseof0.5-1L/100kmper100kg.Overthepastdecade,China’saveragefleetweighthasincreasedby13%(163kg).Domesticindependentmanufacturerssawanincreaseof22%overtheperiod(258kg).Independent

128%

132%

136%

140%

144%

148%

6.0 6.5 7.0 7.5 8.0 8.5 9.0

CAFC/Tcafc

CAFC,L/100km

MA IN AUTO MAKERS FA I LED CAFC REQU IRMENT

6.0

7.0

8.0

9.0

10.0

11.0

12.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

CAFC

(L/100km)

BY-COPORATETYPEAVERAGEANNUALCAFC

Domestic(JVs+Indp')JVsIndependentImporters

-5-

andimportersalsoexperiencedasignificantincreaseinaveragefleetweightoverthepastyear.

Note:NEVcreditsexcludedfromCAFCcalculations.

3. ThetrendofweightandenginesizeincreaseisevidentlydrivenbytheincreasingmarketshareofSUVSandlargemodels.In2016,SUVsandMPVstogetheraccountedfornearlyhalfofChina’spassengercarmarket,withSUVsmarketshareincreasingfrom15%in2012to40%in2016.TheaverageFCofSUVs is1.2L/100kmhigher thanthatof theaveragesedan.Itsweightis215kghigheranditsenginedisplacementis130mllarger.

BY-SEGMENT2016AVERAGECURB-WEIGHT,FC,DISPLACEMENTANDPOWER

1100

1300

1500

1700

1900

2009 2010 2011 2012 2013 2014 2015 2016

Cur

b W

eigh

t,kg

BY-COPORATETYPECAFCDEVELOPMENT

JVs Independent Importers

1,309

1,515

1,404

1,141

1000

1100

1200

1300

1400

1500

1600

CurbWeight�kg

car SUV MPV cross-typePV

1576

1709

1548

1286

1000

1100

1200

1300

1400

1500

1600

1700

1800

Displacement�ml

car SUV MPV cross-typePV

95

114

87

68

60

70

80

90

100

110

120

power�kw

car SUV MPV cross-typePV

6.18

7.44

7.06

6.55

5

5.5

6

6.5

7

7.5

8

AverageFC�L/100km

car SUV MPV cross-typePV

-6-

II.NewEnergyVehicle(NEV)supercreditsandCAFC:

4. Abouttwo-thirdsofChina’sFCreductioncomesfromtheincorporationofNEVsupercredits. China’s national average FC rate decreased from 7.04L/100km in 2015 to6.56L/100kmin2016,withfuelsavingtechnologiesaccountingfor33%(0.16L/100km)ofthisreductionandtherest(0.32/100km)fromflexibilitymechanismcalculationsofNEVproduction(eachEVisconsideredfivevehicleswith0L/100kminCAFCcalculations).

2015-2016FCREDUCTIONCOMPONENTS

5. In2016,theindustrygeneratedatotalof1.54millionCAFCcreditsdeficit,whileCAFCcreditssurpluswasseventimeslarger.Over7timesofCAFCsurpluswereproducesin2016andover2millionCAFCcreditssurpluswerecarriedfrom2013to2015bydomesticmanufacturers(nocreditswereforwardedbyimporters),thereforeitisnotaheavyburdenforcompaniestomeetCAFCcreditrequirement.

20157.04L/100km

ICEtechnologyimprovement0.16L/100km NEVpreferenceaward

0.32L/100km

20166.56L/100km

5.00

5.50

6.00

6.50

7.00

7.50

L/100km

33%

67%

397

632

10461117

99 125198

1117

-32 -27 -18-137

-200

0

200

400

600

800

1000

1200

2013 2014 2015 2016

CAFCcredits

,10k

CAFCCREDITSDEVELOPMENTFORDOMESTICPRODUDERS

creditsurplus-previousmethod creditsurplus-newmethod CAFCcreditdeficit

-7-

6. The flexibility mechanism introduced in Phase IV has dramatically reduced thedifficultyofmeetingtheCAFCstandard.WhilecompaniesmayalmostmeettheannualrequirementifCAFCisbasedontheirICEvehiclesalone(134%ofthe2020target),theyactuallyeasilymeet2016targetifNEVsupercreditsareincluded-achieving124%ofthe2020target!The2017targetof128%wasthereforealreadymetin2016,duetothefactthatcalculationsincludedNEVs.

7. LeadingNEVcompanies(e.g.BYD,BAIC,Geely,SAIC,GAC)benefittedgreatlyfromtheincorporationofNEVsupercreditsintoCAFCcaluclations(zeroFCand5timeforproductionforNEV).Evenautocompaniesthat failed tomeet theirCAFCrequirementachievedcompliancewiththehelpofNEVsupercredits(forexmapleJMCholdings).

30

70

85

41

0 0 0

41

-10.6-5.7 -3.2 -17.1

-20

0

20

40

60

80

100

2013 2014 2015 2016

CA

FC c

redi

ts,

10k

CAFC CREDITS DEVELOPMENT FOR IMPORTERS

credit surplus-previous method CAFC credit surplus-new method CAFC credit deficit

132% 131%

135%138%

132%

124%

130%

112%

127% 124%

100%

110%

120%

130%

140%

Domestic JVBrand IndependentBrand

Import NatioanlAverage

BY-CORPORATETYPE2016CAFCWITH/WITHOUTNEVSUPERCREDITS

CAFC/TCAFC(excludingNEV) CAFC/TCAFC(includingNEV)

-8-

8. BAICandBYDleadCAFCcreditssurplus(over950kpointseach),whileGreatWallandChangan,alsoSUVsdominators,leadincreditsdeficit(overminus200kpointseach).

TOPNEVCREDITSSURPLUSANDSHORTFALLHOLDERSOF2016

III.ThenewlyintroducedNEVcreditssystemandCAFC:

9. China’snewNEVcreditssystem,slatedtogointoeffectin2019,isrewardingPEVsandPHEVwithdoublethecreditsthesevehicleswouldhavebeengivenundertheCalifornian ZEV credits system. However, the practice of over-rewarding creditsdowngradestheimpactofboththenewNEVcreditsandtheCAFCstandardtowhichitislinked.

COMPARISONOFPEVANDPHEVCREDITSGENERATEDINTHECAANDINCHINA

0%

20%

40%

60%

80%

100%

120%

140%

160%

BYD-A

uto in

dustr

y

BYD-A

uto

BAIC

-Mot

or

Jiang

nan-

Motor

Geely-

Mot

or

SAIC

-Mot

orChe

ry JAC

Geely-

Dihao

Brillia

nce -

BMW

BY-COMPANY2016CAFCPERFROMANCEWITH/WOTHOUTNEVSUPERCREDITS

CAFC/Tcafc(including NEV) CAFC/Tcafc(exculding NEV)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

CAFCsu

rplus�

10k

-35.0

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

CAFCnegetivecredit�10k

-9-

10. TheintegrationofthenewNEVcreditssystemwiththeCAFCstandardregimeisverylikelytodrivecompaniestoabandontheir fuelsavinginvestmentin favorofnewenergyvehicleinvestments,andlikelynotintheformofdirectR&DbutratherthroughthemergingandacquisitionofexistingNEVmanufacturers.

11. In order to ensure that NEVs are making real contribution to China’s emissionreductiongoals,thefollowingissuggested:

(1) The NEV credit system should be a stand-alone mechanism in order to clarifycorporateresponsibilitiesandenablesound implementationandenforcement.EvenbeforetheNEVcreditspolicywasintroduced,theCAFCregimehasproventobetoocomplextomanagewell,givenChina’svastindustrialandinter-ministerialstructures.

(2) Longer term requirements and a predictable baseline of theNEV credits policyshouldbepresentedassoonaspossibletoenablepropermarketstrategicplanning,reduce market failure risks and promote steady investment streams, and soundgradualimprovementsofthequalityofNEVs.

(3) IntroducewellinformedandeffectivepenaltymechanismstoensuretheNEVcreditspolicyisaspowerfulasitcanbe.Thisincludesfeelevels,supplementarypenalties(for

5.28

3.82

5

3.812

2.72

5

2.6882.38 2.13

2.72.08 1.5

4

1.25

BYD-Qin BAIC-EU260 Denz JVC-IEV6s Lifan330EV ModelS CheryQQ3EV

ChinaNEVcredit CaliforniaZEVcredit

0.9250.675 0.6125 0.675

0.81 1.1

2 2 2 2 2 2 2

BYD-Tang RoweiRX5 Arrizo7e Roweie950 BYD-Song VELITE BMW-I3

CaliforniaZEVcredit ChinaNEVcredit

-10-

example,creditowedwillstillbeowedregardlessofpenaltiespaid),andefficientandtransparentpolicyscrutinyandpanelizingprocess.

(4) Considersimplificationofthepolicytoeaseitsmanagement.Forexample,eliminatethepracticeofforwardingcreditstocorporateactors.

-11-

1. INTRODUCTION:THEDRIVINGFORCEBEHINDCHINA’SPASSANGERVEHICLEENERGYMANAGEMENT

China's totaloil consumptionin2016reached556million tons, translating toanoil importdependencerateashighas65.5%,asdemonstratedinFigure1.Transportationaccountedformorethanhalfofthetotaloilconsumptionlastyear,ofwhichpassengercarfuelconsumptioncontributed110million tons,accounting forabout90%of totalgasolineconsumption(andabout 20% of total oil demand). As demonstrated in Figure 2, China’s car energy savingspotentialisstillverylarge.Therefore,China’svehicleenergymanagementismeanttoreduceoilconsumptionandimproveenergysecurity.

Figure1:China’soilimportsgrowthtrend

Source:ChinaPetroleumInstituteofEconomicsandTechnology.

Figure2:By-sourcesplitofChina’soilimportsin2016

54.3%55.9%

56.9% 57.5%59.4%

61.3%

65.5%

50%52%54%56%58%60%62%64%66%68%70%

0

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014 2015 2016

MillionTons

oilproductionvolume oilimportvolume oilimportpercetage

Chemicals20%

Indusrty10.3%

Building2%

Residential5.2%

Agri-Forest-Fishery 3.3%

Business3.5%

PassengerVehicles20%

CommercialVehicles21%

Meritime2.7%

Aviation5%

Other6.2%

Transportation55.5%

-12-

Source:iCETcompiledthefigurebasedondatasourcesfromCNOOCTechnologyResearchInstitute,ChinaAutomotive

TechnologyResearchCenterandNationalBureauofStatistics.

Inaddition,Chinaisthelargestautomobilemarketintheworldforeightconsecutiveyears.Over24millionpassengercarshavebeenproducedinChinaandanadditional1millionwereimportedoverthepastyear,asshowninFigure3.Althoughthemarketisalreadylarge,therateof carownershipper capita is still low(less than118 for1000people1). China’s StateCouncil,inits"MadeinChina2025"plan,hasputforwardanationalpassengervehicleaverageFCratetargetof5.0L/100kmby2020and4L/100kmby2025.

Inthe"ChinaMotorVehicleEnvironmentalManagementAnnualReport(2017),"releasedlastyearbyChina’sMinistryofEnvironmentalProtection(MEP),itisnotedthatmotorvehiclesaccountfor30%-40%of urban PM2.5pollutants in Beijing, Shanghai, Hangzhou, Guangzhou, Shenzhen andothermajorcities.Passengercarsinparticularareapredominantsourceofcarbonmonoxide(CO)andhydrocarbons(HC)pollutants,reaching49%and40%,respectively.

Figure3:2006-2016productionandimportvolumeofChinaPassengerCars

1 http://data.stats.gov.cn/easyquery.htm?cn=C01&zb=A0G0J&sj=2016

0

500

1000

1500

2000

2500

3000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Unit,10k

PassengerVehicleProduction

PasssengerVehicleImport

-13-

2. CHINA’SPASSENGERCARSFUELCONSUMPTIONSTANDARD

2.1PassengercarsfuelconsumptionstandardsystemAt the coreofChina's vehicleFC standard is the conceptof limitations and targets, energyconsumption labeling, and technical guidelines, as detailed in Table 1. It is a weight-binstandard(unliketheUS),measuredinL/100km(notbyCO2,asenactedintheEUandUS),anditisbasedontheNEDCtestcycle(yetthedevelopmentofanewChinacycleisunderway).SinceChinastartedtheimplementationofapassengervehicleFCstandardin2005,itunderwentfourphases, the lastoneentered intoeffect in2016.Thedevelopmentof thestandardregime isoutlinedinTable2.

Table1:China’sPassengerCarFuelEconomyStandards

Type TitleandYearissued Enforcementlevel

Testingstandards

Measurementmethodsoffuelconsumptionforlightdutyvehicles(GB/T19233-2008)

Voluntary

Testmethodsforenergyconsumptionoflight-dutyhybridelectricvehicles(GB/T19753-2013)

Voluntary

Labelstandard

Energyconsumptionlabelforlightvehicle–Partone:gasolineanddieselvehicles(GB22757.1-2017)

Mandatory

Energyconsumptionlabelforlightvehicle–Part2:electricitypoweredvehicles(GB22757.2-2017)

Mandatory

Mandatorystandards

Fuelconsumptionlimitsforpassengercars(GB19578-2014) MandatoryFuelconsumptionevaluationmethodsandtargetsforpassengercars(GB27999-2014)

Mandatory

EVsenergyconsumptionlimit* VoluntaryOthervoluntarystandards

Conversionmethodsforenergyconsumptionofhybridelectricvehicles*

Voluntary

Off-cycletechnology/deviceenergysavingeffectsevaluationmethodsforpassengercars*

Voluntary

*Standardsunderdevelopment.

Table2:China’sBy-PhaseFuelConsumptionStandards

Phase Timeframe Title Comments

PhaseI

2005.07-2008.01newmodelslimit2006.07-2009.01inproductionmodelslimit

GB19578-2004SinglevehicleFClimit(Importedvehiclesnotincluded)

PhaseII

2008.01-2012.07newmodelslimit2009.01-2012.07inproductionmodelslimit

GB19578-2004

-14-

PhaseIII

2012.07-2015.12limitsimilartoPhaseII2012.07-2015.12newCAFCintroduced

GB19578-2004GB27999-2011

SinglevehicleFClimitandcorporateaverageFCtarget;(Importedvehiclesincluded);Includingimportedvehicles.

PhaseIV

2016.01-2020.12newmodelslimit2018.01-2020.12inproductionmodelslimit

2016.01-2020.12 CAFC targetandlimit

GB19578-2014GB27999-2014

SinglevehicleFClimitandcorporateaverageFCtarget;(Importedvehiclesincluded);Includingimportedvehicles.

The standard requirement intensified with each phase. For example, the third standardrequirementwas20%morestringent thanthoseof thesecondphase,and the fourthphaserequirementsare30%-40%morestringentthanthoseofthethirdphase.

Figure4:China’sby-phaseCAFCstandarddevelopment

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

500 700 900 1100 1300 1500 1700 1900 2100 2300 2500

FuelConsumption(

L/100km)

CurbWeight(kg)

phaseIIIFClimitforMTphaseIIIFClimitforATphaseIIIFCtarget&phaseIVFClimitforMTphaseIIIFCtarget&phaseIVFClimitforATphaseIVFCtargetforseatrows<3phaseIVFCtargetforseatrows>=3

-15-

2.2ThefourthphaseofChina’sFCstandardThefourthphaseisaimedatachievinganationalaverageFCtargetof5L/100kmby2020.Thestandardisheavilyinvestedintheactualvalue(versusthetargetvaluegap)ofthecorporateaveragefuelconsumption(CAFC)rate,Itsaimistoachieveazerogapby2020,asshowninTable3.

Table3:CAFC/TCAFC-IVRequirementforCarProducersandImportersDuringPhaseIV

Year Requiredratio (CAFC/TCAFC-IV)

NationalFCtarget(L/100km)

2016 134% 6.7

2017 128% 6.4

2018 120% 6.0

2019 110% 5.5

2020 100% 5.0

NewEnergyVehicles(NEVs)wereincorporatedintoChina’sCAFCaccountingprocessaspartofthe

“flexibilitymechanism”designedtosupportanincreasedrateoftargetrealization.Accordingtothe

flexibilitymechanism,NEVsarecountedasseveralvehiclesofwith0L/100kmasdetailedinTable

4. Off-cycle technologies (e.g. idle start-stop devices, shift reminders, efficient air conditioning,

brakeenergyrecovery,etc.)arealsoeligibleforFCdiscountstypicallycountedas0.5L/100km.

Table:NewEnergyandEnergySavingVehicleProductionPrivilegeinCAFCCalculation(productionvolume

multiplier)

PEV FCV PHEV* ESV**

~2015 5 5 5 32016-2017 5 5 5 3.5

2018-2019 3 3 3 2.52020 2 2 2 1.5*Plug-inelectricvehicles(PHEVs)aredefinedascarswithelectricrangeofatleast50km.

**EnergySavingVehiclesaredefinedascarswithafuelconsumptionratelowerthan2.8L/100km.

China'spassengercarenergyefficiencystandardhasevolvedandmaturedoverthepastdecade.PhaseVofthestandardiscurrentlyunderway,aswellasthedevelopmentofaChinadrivingcycle,bytheleadautostandarddrafter-ChinaAutomotiveTechnologyandResearchCenter(CATARC).

-16-

3. CHINA'S FUEL CONSUMPTION AND NEW ENERGY VEHICLE DOUBLE INTEGRALMANAGEMENT

China'sCAFC regimemanagement relieson reportingandgovernmentverification,by-companyperformance release, production suspension, and set increasingly stringent CAFC/Tcafcperformancetarget(seetable3).Theambitioustargets--5.0L/100kmby2020and4.0L/100kmby2025–illustratestheseriousnesswithwhichthegovernmentintendstopursueimplementationand enforcement. This chapter reviews the CAFC system, including the newly announced NEVcredits,aswellasananalysisoftheprosandconsofthepolicy.

3.1Requirements

Eachmanufacturerexceeding2,000vehiclesperyearisrequiredtomeettheby-vehiclestandard

limit(weight-binbased)aswellasacorporateaverageFClimitandacertainpercentageoftheCAFC

target.Forthelatter,creditscanbeaccumulatedifsuccessful,or,ifpercentagetargetisn'tmet,the

manufacturercanpurchaseexcesscreditswithinthecomplianceyear.

Inordertoachievethesetargets,China’sMinistryofIndustryandInformationTechnology(MIIT)

enables more benefits from the shift to NEVs– not only the above explained NEV flexibility

mechanism(seeTable3andTable4),butalsoanewNEV-creditssystemhasbeenintegratedinthe

CAFCmanagementlastSeptember.2

Manufacturersofover30,000vehiclesperyeararerequiredtoproduce10%and12%newenergy

vehicles in 2019 and 2020, respectively.Manufacturers that fail tomeet theannual compliance

requirement are required to purchase credits from manufacturers with excess credits to

compensate.

3.2Fuelconsumptionandnewenergyvehicleintegratedaccounting

(1) CAFCactualvalueandtargetvalueaccounting

China’sCAFCusesvehiclemodel,year,andannualsalesdatatocalculateaweightedaverage

for FC based on theNewEuropeanDriving Cycle (NEDC). The CAFC target is based on

individualvehicleFCtargets,whichusethequantityofannualproductionforeachmodel

tocalculateaweightedaverage.BothCAFClimitsandtargetsarecalculatedasshowninthe

formulasbelow:

2 Corporate Average Fuel Consumption and New Energy Vehicles Credits Joint Management Method report released. http://www.icet.org.cn/english/admin/upload/2017102642532337.pdf

1

1

N

i iiN

i ii

FC VCAFC

V W

=

=

´=

´

å

å

N

i ii=1

N

ii=1

T V

VCAFCT

´=å

å

-17-

Whereas: N:thevehiclemodelnumberFCi:fuelconsumptionofthe“i”thmodelVi:annualproductionofthe“i”thmodel|Wi:productiontimesofthe“i”thmodel,if“i”thmodelisqualifiedNEVorESVTi:fuelconsumptiontargetofthe“i”thmodel

(2) CalculationoftheintegratedCAFCandNEVcredits

China’sCAFCPhase IV introducedan integrateddualmanagement thatenables theexchangeof

CAFCNEVsupercredits(differencebetweenthetargetandactualCAFC).

CCAFC=(a´TCAFC-CAFC)´TP

Where:CCAFC-passengercarcorporateaveragefuelconsumptioncredits; TCAFC-passengercarcorporateaveragefuelconsumptiontargetvalue;

CAFC-Passengercarcompanyaveragefuelconsumptionactualvalue; a—annualaveragecorporatefuelconsumptionrequirement(%); TP-passengercarproduction(excludingexports)orimports.

CAFC and NEV credits will be calculated independently. Corporate CAFC and NEV credits

performancewillalsobeevaluatedseparately.YetCAFCcanbeoffsetbyNEVcredits,asillustrated

inFigure5.Theratiooftradingis1:1.

Figure5:Dual-scheme–NEVsupercredits(CAFCcredits)andNEVcreditscalculationmethod

Companiesproducingorimportingover30,000passengercarsperyearareobligedtocomplywith

theNEVcreditsrequirement,anannualNEVversusICEproduction/importationratioof10%and

12%in2019and2020,respectively.The2021ratiotargetwillbedeterminedinthefuture.Credit

calculationsperdifferentvehicletechnologiesisspecifiedinTable5andpresentedFigure5,witha

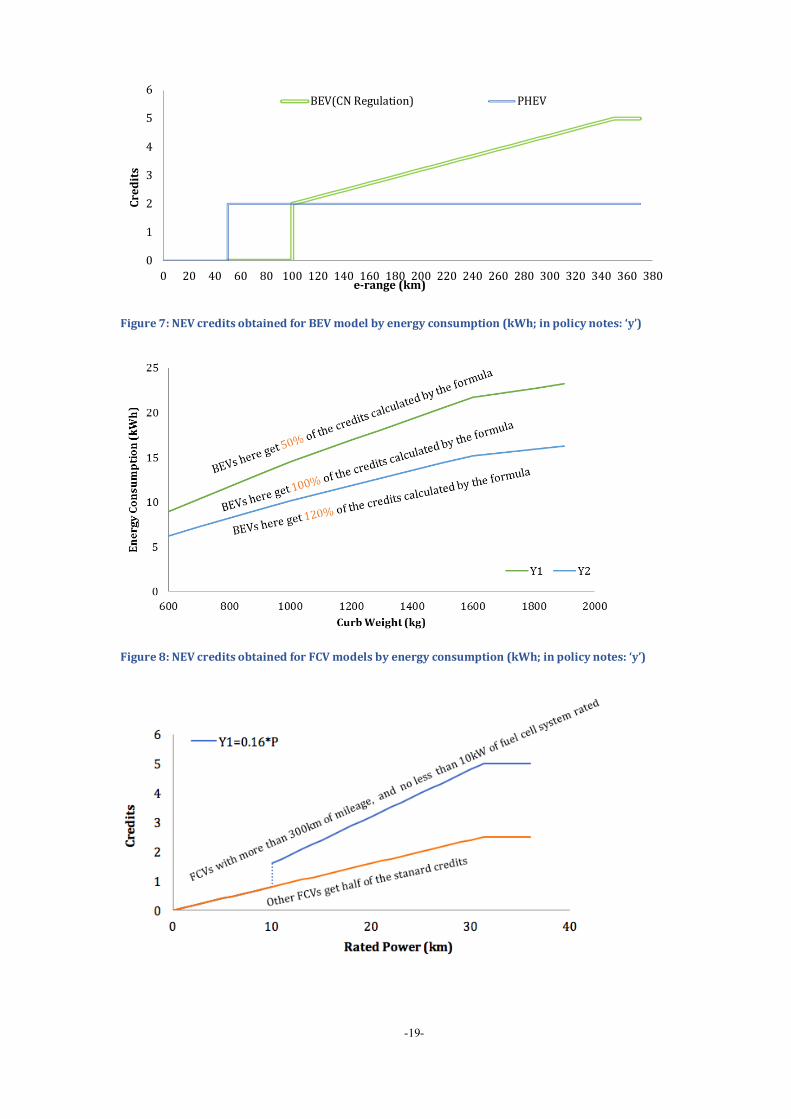

maximum of five credits per vehicle. The credit calculations are based on range and power

consumption,asexemplifiedforBEVsinFigure6,andforFCVsinFigure7.Pureelectricvehicles

CAFCcredit

NEVcredit

CAFC actualvalue

CAFC standardvalue� a� TCAFC target

value�

CAFCactualvalue

CAFC standardvalue� a� TCAFC target

value�

CAFC surplus=�a´TCAFC -CAFC�´TP

CAFC deficit=�a´TCAFC -CAFC�´TP

NEVcredit pervehicle

Productionof

traditionalcar

NEVProductionofthetype

Proportiontarget

�

�

� �NEV

creditactualvalue

� � NEVcredittargetvalue

Compare

NEV surplus=NEVactualvalue- targetvalue

+

-NEVdeficit=NEVtargetvalue- actualvalue

1:1offset

-18-

models,forexample,receivecreditsaccordingtoelectricenergyconsumption(kW-h)andvehicle

curbweight(referencebase),usingafactorof0.5,1,or1.2.FCVsreceivecreditsbasedontheirrated

powerusingafactorof0.5.

Table4:Creditscalculation

Passengervehicletype

Creditscalculationrequirement

Comments

BEV 0.012×R+0.8 (1) R is calculated according to the joint (urban andsuburban)drivingcycle(measuredbykm).(2)Pistheratedpowerofthefuelcellsystem,inkW (3)Theuppercreditslimitis5points.(4) Credit calculation results are rounded to twodecimalpoints.

PHEV (REEVincluded)

2

FCV 0.16×P

Technologicalspecificationsavailableinreferences.3

Figure6:PEVsandPHEVscreditsaccumulationgraph

3 Technologicalbenchmark:

(1)BEVs:Therequirementisfora30-minutesmaximumdrivespeedofnotlessthan100km/h,andpureelectric

modedrivingrangeofnotlessthan100km.

(2)Thecreditsenableddependontherelationshipsbetweenenergyconsumptionandthevehiclecurbweight(m)

in the followingmanner:ForY1, ifm≤1000kg,Y1≤0.014×m+0.5;if 1000<m≤1600kg,Y1≤0.012×m+2.5;if

m>1600kg,Y≤0.005×m+13.7.ForY2,ifm≤1000kg,Y2≤0.0098×m+0.35;if1000<m≤1600kg,Y2≤0.0084×m+1.75;

ifm>1600kg,Y2≤0.0035×m+9.59.Ofwhich,YstandsforenergyconsumptionandMstandsforthecurbweightof

BEVs.

(3)PHEVs:theminimaldrivingrangeforcrediteligibilityis50km;

PHEVs:whenminimalrangeis80kmorless,theenergyconsumption(GB19578)shouldbelessthan70%ofthe

standardlimit.Otherwisecreditswillbereducedto50%oftheformula.

CreditsfromPHEVsofmorethan80e-rangebutwithlowerenergyconsumptionthanthestandardlimitcannotbe

exchanged.

(4)FCVs:Therequirementtargetsfuelcellsystemratedpowertohavenotlessthan30%oftheratedpowerofthedrivemotor,andnotlessthan30kW.Failuretomeetthisrequirementenablesonly50%ofthecreditsanddisablescreditexchange(ownuseonly).

-19-

Figure7:NEVcreditsobtainedforBEVmodelbyenergyconsumption(kWh;inpolicynotes:‘y’)

Figure8:NEVcreditsobtainedforFCVmodelsbyenergyconsumption(kWh;inpolicynotes:‘y’)

0

1

2

3

4

5

6

0 20 40 60 80 100 120 140 160 180 200 220 240 260 280 300 320 340 360 380

Credits

e-range(km)

BEV(CNRegulation) PHEV

-20-

3.3Creditstradingmechanism CAFCandNEVnegativepointsmustbecompensatedforannually.AnexcessofCAFCcreditscanbe

carriedforwardthreeyears,whileNEVexcesscreditscannot(theycanbecarriedforwardoneyear

from2019,asagraceperiod).ThisisillustratedinFigure9.

Figure9:Creditsexchangemechanism,includingNEVSsupercredits(CAFCcredits)andNEVcredits

iCET believes thismechanism is threatening FC rate improvements for ICE vehicles. Given the

alreadylargeflexibilityofCAFCimplementationthroughsupercredits(25%),acombinationofthe

systemisnotuseful.iCEThasbeenanadvocatorforNEVcreditssystemsince2013,yetbelieves

suchasystemshouldbedirectlylinkedtocarbonemissionreductionsandmaintainindependence

fromothersystems.GiventhedifficultiesofmonitoringandenforcingtheCAFCsystemitisunwise

tofurthercomplicationthesystembyintegratingNEVcredits.

3.4CreditsmanagementMIIT,MinistryofFinance(MOF),MinistryofCommerce(MOFCOM),andGeneralAdministrationof

Customs,theStateAdministrationofQualitySupervision,Inspection,andQuarantine(AQSIQ)will

jointlyenforcethe“average fuelconsumptionofpassengercarsandnewenergyvehicle integral

management.”The first twowill oversee the enforcementof domesticmanufacturers,while the

lattertwowillsupportdocumentationsubmissionofimporterstotheformertwo.Thegoverning

entitiesandtheirresponsibilitiesarelistedinFigure10.

MIITwillestablishavehicleFCandNEVintegratedinformationmanagementplatform,including

thesummaryandpublicationofFCandNEVrelatedinformation.Automakersandimporterswill

promptlyreporttheirvehicleproductionandimportationvolumesaswellasvehicleFCtoMIIT–

CAFCcreditsystem

CAFC deficitNEVdeficit

NEVCreditsystem

CAFC surplus

CAFCpreviousyearscreditsurplus,bycompany

CAFCsurplusfromaffiliatedgroupcorp.

NEVsurplusproducedthisyear,bycompany

PurchasingNEV surplus

NEVsurplusBankingofcreditsfornextyearscommitment

Transferofcreditstoaffiliatedcorps(25%ownership)

NEVdependent market�freetrade�

Note�NEVsurpluscreditcan’tbebankedNote�CAFCsurpluscreditcanbebankedforthreeyears

AutoMakers

1:1offset

Purchasetooffset

Offset

Usefor

-21-

aslistedinAppendixIofRegulation.4 Thereportingwillincludeby-vehiclecalculationsperformed

bytheautomakersthemselves.

Figure10:NEVsupercredits(CAFCcredits)andNEVdualnetworkmanagement

Penaltiesincludetheseizureofvehicleproductionorimportationandtheissuingofapublicnotice

(“shaming”approach),summarizedinFigure11.Enforcementwillbepursuedinaccordancewith“Automobile Industry Development Policy” 5 and the “Mandatory Product Certification

ManagementRegulations.”6

Figure11:CACmanagementenforcementinstruments

3.5DifficultiesandChallengesonenergyefficiencymanagementAtpresent,therearenearly100passengercarmanufacturers inChinaandnearly30 importers.

Over2,900newmodelswereaddedtoMIIT’sFuelEconomywebsitein20167.Thehighvolumeof

4 http://zqyj.chinalaw.gov.cn/draftDetail?listType=2&DraftID=1894&1497592757400

5 http://www.miit.gov.cn/n1146295/n1146557/n1146624/c3554600/content.html

6 http://www.cnca.gov.cn/cnca/rdht/qzxcprz/flfg/193003.shtml

7 ChinaAutofuelConsumptionofficialwebsite(中国汽车燃料消耗量网站).http://chinaafc.miit.gov.cn/

CAFC

NEVcredit

Creditinstitutionalmanagement

Creditmanagementplatform

MIIT(Lead)

MOF

MOC

GACC

AQSIQ

VerifyPVimportvolume

Verifydomesticpassengervehicle(PV)producer,fuelconsumptionofPV,newenergyPVindex,andproductionvolumeofPV

VerifyPVimportingofsupplycompany

VerifyfuelconsumptionofimportPV,andimportnewenergyPVindex

Notification

��Notification��Publicannouncementofincompliantcompanies(‘shaming’)

Rectification

��Notifyrectificationprocesses,forconductingscrutinyofcompanyreporting

Suspension

��Suspendmanufacturing��suspendcertificationissuance

Otherpenalties

��Other(monetary)penaltiesmayapply

-22-

vehiclesandnewmodelscreatesenormousenforcementchallenges.Thedualmanagementscheme

governingbothCAFCand thenewNEVcreditssystem is increasing thepressuresongoverning

entities,asillustratedinFigure12.

Figure12:ComplexstructuretoChina’sautoregime

ThegoverninginstitutionalstructureofCAFCandNEVcreditsiscomplex.ItincludesseveralMIIT

departments, the National Development and Reform Commission, the Ministry of Finance, the

Ministry of Commerce, the General Administration of Customs, the General Administration of

QualitySupervision,InspectionandQuarantine,andothergovernmentagencies.Thiscomplexity

increasescoordinationchallengesandhindersprospectsforadequateenforcement.

Chinamadegreateffortstodevelopenergy-savingandnewenergyvehicles,andisinaperiodof

industrial restructuring. Based on iCET’s decade of analysis and research on fuel consumption

standardsandtheirdevelopmentandimplementationinChina,itisadvisedthat:

(1)Companiesbegivenaclearlong-termcomplianceplan,thatwouldsupportthedevelopmentof

competitiveproducts.

(2)Alleconomicmechanisms(penaltiesinparticular)beclear,significant,andenforced.

4. COMPARISONBETWEENCHINA’SNEVCREDITSANDCALIFORNIA’SZEVCREDITS

Inspired by the California’s 1990 ZEV regulation, which has beenmodified multiple times and

adoptedinnineotherUSstates,ChinareleaseditsownadjustedversioninSeptember2017,which

DomesticproducerA

DomesticproducerB

Shareholding≥25%

DomesticproducerA DomesticproducerB

DomesticthirdpartyShareholding

≥25%Shareholding≥25%

ImportsupplierA DomesticproducerB

Shareholding≥25%

OverseasproducerAuthorizing

CompanyA

CompanyB

CompanyC

Shareholding≥25%

Shareholding≥25%

-23-

enteredintoeffectin2018.8 TherearesignificantdifferencesbetweentheZEVcreditsystems,as

showninFigure13andFigure14.

Figure13:ComparisonbetweentheChinaandCaliforniaNECcreditsmanagementmechanisms

Figure14:ComparisonbetweentheChinaandCaliforniaNEVcreditpolicydesign

Figure15:BEVcreditcomparisonsbetweenthenewNEV-creditsdraftandZEVcreditregulationinCalifornia

8 Corporate Average Fuel Consumption and New Energy Vehicles Credits Joint Management Method Regulation http://www.icet.org.cn/english/admin/upload/2017101337455653.pdf

Goal

Scale

Requiremt

Trading

Credits

Penalty

Apost-subsidyregulatoryinstrumenttoforcethetechnologicaltransitiontoNEVs.

Economicinstrumentforadvancingtechnologicaltransitionaimedatcurbingcarbonemissions.

National IntroducedbyCalifornia,witheightotherstatesthatfollowed,enablingintra-statetransfer.

MinimalNEVpercentageproductionrequirementoftotalannualproduction.

MinimalNEVpercentagesales requirementoftotallocalsales.

Oncerequirementismet,excesscreditscanbeobtained. Oncerequirementismet,excesscreditscanbe

obtained.NEVcreditscanbesold(followingnon-transparentnegotiationbetweencompanies)orbanked.

NEVcreditscanbesold,butnottransferredorbanked.

Administrativemainly:productionsuspensionandpublicannouncement(“shaming”)ofnon-compliantcompanies.

Economic:non-compliantcompaniespaypenaltiesandtheircreditsshortageforwardedtothefollowingyear.

JointMngtwithCAFC

Yes No

China’sNEVcredits,partofCAFCregime California’sZEVcredits (independent) regulation

2019-10%,2020-12%,2020-andbeyondTBD. 2018-4.5%with2.5%percentpointsaddedannuallyto22%in2025.

Compliance

CompanySize

Creditstypes

Creditsexpiration

Creditstransfer

Basedonsameyearproductiondata. Averageofpastthreeyears(excludingthepreviousyear);

Productionvolumeof30,000carsormore. Productionexceeding4,500.

NEVcredits,comprisedofPEVs,FCVsandPHEVs.

ZEVcreditscomprisedofaminimumofZEVs(FCVs,PEVs)andgraduallydecreasingmaximumoftransitional-ZEVs(TZEVs);Creditscanonlybeusedinthesameyear,

cannotbebanked(excludingoneyeargraceperiodfor2019credits).

Creditscanbeforwardedandcompensatepartiallyforfuturerequirement;

Excesscreditscanbesoldorcarriedforward.Shortfallofcreditsneedstobecompensatedthroughfineandforwardyearcreditscompliance,orsameyearcreditscompliance.

ExcesscreditscanbetransferredtocompensateforCAFCrequirements.Shortfallmustbemetwithinthesameyear.

Creditsrequireme

nt

China’sNEVcredits,partofCAFCregime California’sZEVcredits (independent) regulation

-24-

Figure16:CombinedcyclecreditresultsforsevenBEVsmodelsunderNEV-creditsdraftandZEV-credits

systemcompared

Figure 17: PHEV credit comparisons between the new NEV-credits draft and ZEV credit regulation in

California

0

1

2

3

4

5

6

70 110 150 190 230 270 310 350 390 430 470 510 550 590

Credits

e-kmCNMIITRegulation US(California)Regulation

560

5.28

3.82

5

3.812

2.72

5

2.688

2.38 2.132.7

2.08 1.5

4

1.25

BYD-Qin BAIC-EU260 Denz JVC-IEV6s Lifan330EV ModelS CheryQQ3EV

ChinaNEVcredit CaliforniaZEVcredit

YNEV=0.012×X+0.8

YZEV=0.01× X /1.6+0.5

-25-

Figure18:ComparisonbetweencreditsfromsevenPHEVsmodelsunderNEV-creditdraftandZEV-credit

system

0

0.5

1

1.5

2

2.5

0 50 100 150 200

Credits

e-km

USPHEVs USPHEVs≥10milesofAERonUS06tetcycle CNPHEVs

0.93

0.68 0.61 0.680.80

1.001.10

2 2 2 2 2 2 2

BYDTang RoeweRX5 Arrizo7e Roewee950

BYDSong VELITE BMWi3

USRegulation CNRegulation

-26-

5. CURRENTSTATUSANDTRENDSFORPASSENGERCARFCINCHINA

5.1ReportedFCvaluelargelyunchangedAccordingtotheMIITin2016,theaverageFCrateofdomesticandimportedcarswas6.51L/100km

and 7.89L/100km, respectively. Comparedwith the 2015 average FC rate of 7.04L/100km, the

reportedannualaverageof6.56L/100kmin2016showsadecreaseof0.16L/100km(33%)thatcan

be attributed to vehicle energy efficiency improvement and 0.32L/100km (67%) that can be

attributedtoNEVsupercredits(theflexibilitymechanism).

Figure19:China'saverageFC-MIITreported,NEVandenergysavingtechnologiescontribution

AfterenteringtheFCstandardimplementationphaseIVin2016,therateofnon-complianceamong

domesticandimportingcarcompaniesreachedabout30%and50%respectively.In2015,thenon-

compliancerateforimporterswasamere4%,indicatingthefuelsavingapplicationinmanyauto

companiesdidnotcatchupwiththestringentstandardrequirements.

Figure20:Bycorporatetype-PhaseIVcompliance

20157.04L/100km

ICEtechnologyimprovement0.16L/100km NEVpreferenceaward

0.32L/100km

20166.56L/100km

5.00

5.50

6.00

6.50

7.00

7.50

L/100km

33%

67%

0102030405060708090100

DomesticManufacturers Importers

automakersnum

ber

-27-

Althoughmanyenterprisesdidnotmeetthestandard,theactualFCrateofthepassengervehicle

industry in 2016 had a value-to-target ratio of 132%, lower than the required ratio of 134%,

highlightedinFigure21.AfterincorporatingNEVreductionstoCAFC,theratiogoesevenlowerto126% -beatingthe2017value-to-target ratioof128%ratiooneyearearlier.This indicates the

standardiscurrentlynotstringentenough.

Figure21:2016companiesreportedversustargetvalue

In2016,asmanyas2,906new(M1class)domesticmodelswereaddedtotheMIIT’sfueleconomy

website, indicating there was huge opportunity for improvements in corporate fuel savings.

However, only 400models in 2016 reached the target, accounting for 15%of the totalmodels,

demonstratedinFigure22.Goingforward,thepolicyregimewillclearlyneedtoplayabiggerroleintheadoptionoffuelsavinginitiatives.

Figure22:ReportedFCof2016M1passengervehicles

132% 131%

135%138%

132%

124%

130%

112%

127% 124%

100%

110%

120%

130%

140%

Domestic JVBrand IndependentBrand

Import NationalAverage

CAFC/TCAFC(excludingNEV) CAFC/TCAFC(includingNEV)

3.04.05.06.07.08.09.010.011.012.013.014.0

500 700 900 1100 1300 1500 1700 1900 2100 2300 2500

L/100km

curbweight(kg)

PhaseIVMTPhaseIV-ATPhaseIVtarget<3RowsPhaseIV>3Rows2016models

-28-

Note:PhaseIVofCAFCofficiallyenteredimplementationin2016.

5.22016CAFCcompliancestatus Among the top 10 selling domestic automakers, GreatWall Motor, Chang'an Changan andChanganForddidnotmeetthevalue-to-targetrequirementratioof134%.FAW-Volkswagen,ontheotherhand,reached125%value-to-targetratio,wellaheadthe2017requirements(seeFigure22).NEVproducers,however,achievedasubstantiallylowerratio:asmanyassixsuchmanufacturers were able to reach the 2020 target in 2016. That said, most of thesemanufacturerswouldperformpoorlyifitwasn’tfortheuseoftheNEVflexibilitymechanism,e.g. JiangnanAutomobile, JAC(seeFigure24).Both independentand importerswouldhavefailedtomeetthetargetifitwasn’tfortheNEVsupercreditoption(seeFigure25).

Figure23:Top2016averageCAFCperformingdomesticmanufacturers

Note:Thesizeofthebubblerepresentscomparativeannualproductionvolume.

Figure24:Domestic2016CAFCincomparisontoChina’s2020target

116%

122%

128%

134%

140%

146%

6.0 7.0 8.0 9.0 10.0 11.0

CAFC/Tcafc

CAFC,L/100km

-29-

Note:Onlyautocompanieswithannualproductionexceeding100,000carsareincluded;Thesizeofthebubblerepresentscomparativeannualproductionvolume.

Figure25:By-corporatetypeCAFCcomparisonwith/withoutNEVcredits

The top 10 importing car companies’CAFCactual-to-target ratiowas relatively scattered; threecompanieshadaratiohigherthan140%,whilesomeachievedthe2017ratioaheadoftime(e.g.BMW,Porsche),asshowninFigure26.

Figure26:Importers’2016CAFCinrelationto2016and2017target

0%

20%

40%

60%

80%

100%

120%

140%

2.0 3.0 4.0 5.0 6.0 7.0 8.0

CAFC/Tcafc

CAFC,L/100km

0%20%40%60%80%100%120%140%160%

BYD-Autoindustry

BYD-Auto

BAIC-Motor

Jiangnan-Motor

Geely-Motor

SAIC-Motor

Chery JAC

Geely-Dihao

Brilliance-BMW

CAFC/Tcafc(includingNEV) CAFC/Tcafc(exculdingNEV)

-30-

Note:Thesizeofthebubblerepresentscomparativeannualproductionvolume.

5.3FuelconsumptiontrendsChina'sfuelconsumptionstandardssawanaverageannualdropof1.7%and2.7%from2006to2016throughoutthe implementationperiodof its three firstphases,respectively.From2012to2016,theaverageannualdeclineintheFCrateforimportedcarswas3.7%,significantlylowerthanthatofdomesticvehicles,whichsawanaveragedeclineof2.2%.Theannualaveragedeclineoverthesameperiodwas2%(seefigure27).JVsandindependentmanufacturersCAFCdecreasedby2.2%and1%from2006to2016,respectively(seefigure28).

Figure27:ImportersanddomesticCAFCdevelopment

Note:NEVflexibilitymechanismexcluded,onlyICEFCcalculationincluded.

Figure28:Importer2016CAFCinrelationto2016and2017target

120%

125%

130%

135%

140%

145%

6.0 6.5 7.0 7.5 8.0

CAFC/Tcafc

CAFC,L/100km

6.0

7.0

8.0

9.0

10.0

11.0

12.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

L/100km

DomesticManufacturers(JVs+Indp') Importers

-31-

Note:NEVflexibilitymechanismexcluded,onlyICEFCcalculationincluded.

ThereisampleevidencethatitistheincreaseinvehicleweightthatslowsFCreductions.Between2006and2016,domesticvehiclecarcurbweightincreasedby160kg(13%),ofwhichindependentcarsweight increasedbyasmuchas258kg(22%),asshowninFigure29.Becauseeach100kgincreaseincurbweightisequivalenttoaFCincreaseofabout0.3-0.6L,China’svehiclecurbweightincrease led to 0.5-1L/100kmFC increase. Domestic vehicle averageweight increase led toFCincrease of 0.7-1.5 L. Luckily, domestic car power and displacement also continued to increase(whilethatofimportedcarsstabilized),absorbingsomeoftheweight-basedFCincrease.

Figure29:By-corporatetypecurb-weight(kg)developmenttrend

Inaddition,theratedpowerofdomesticpassengercarscontinuestoincrease.Theratedpowerofjoint-ventureand independent brands between 2009 and 2016 increased from17kW to 33kW,respectively,asshowninFigure33.

Figure30:By-corporatetypepower(kw)developmenttrend

6.0

6.5

7.0

7.5

8.0

8.5

9.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

FuelConsumption,L/100km

JVs IndependentManufacturers

1100

1300

1500

1700

1900

2009 2010 2011 2012 2013 2014 2015 2016

CurbWeight,

kg

JVs Independent Importers

-32-

5.4BrandFCperformance SixautomakersthatachievedthesteepestCAFCdecline,reaching24%to39%,arelistedinfigure26.Amongthese,NEVswereaninstrumentalCAFCreductionpathwayforGeelyAutomobileandSAIC (Geely Zhidou and Dihao EV production reached 40,000, SAIC Roewe plug-in hybridproductionwas22,000).GAC,ontheotherhand,focusedonfuelsavingflagshipmodelproduction(Chuan Qi GS4 with 6.3-6.7L/100km, which reached 336,000 sales). Beijing Benz, GuangzhouAutomobile and Tianjin FAW Toyota also focused on fuel saving technology integration (e.g.lightweighttechnology,idlestop-start,superchargeddirectinjection,advancedtransmission).

Figure31:TopperformingcompaniesinCAFCreductionbetween2012and2016

Amongimportingbrands,PorscheandVolvosawthelargestFCdecreaseofover30%between2012and2016,asillustratedinFigure32.Porsche’scorporateFCratedroppedfrom9.12L/100kmin2015to7.71L/100kmin2015,down15.4%.Inpart,thisisaresultofhighimportationofPorscheCayenne,theflagshipofthecompany’ssmallandlowFCcapacities.GreatWallMotorandChanganAutomobile,aretheleadersofCAFCincreaseasillustratedinFigure33,likelyduetotheirstrategicfocusonlargeengineandSUVmarkets.

50.0

60.0

70.0

80.0

90.0

100.0

110.0

2009 2010 2011 2012 2013 2014 2015 2016

power,kw

JVs IndependentCooperation

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Geely

SAIC-Moter

GAC-Moter

BAIC-Benz

GAC-Toyota

FAW-Toyota-…

CAFC

,L/100km

2012 2013 2014 2015 2016

-33-

Figure32:TopperformingimportersinCAFCreductionbetween2012and2016

Figure33:GreatWallMotorsandChanaAutoCAFCtrends

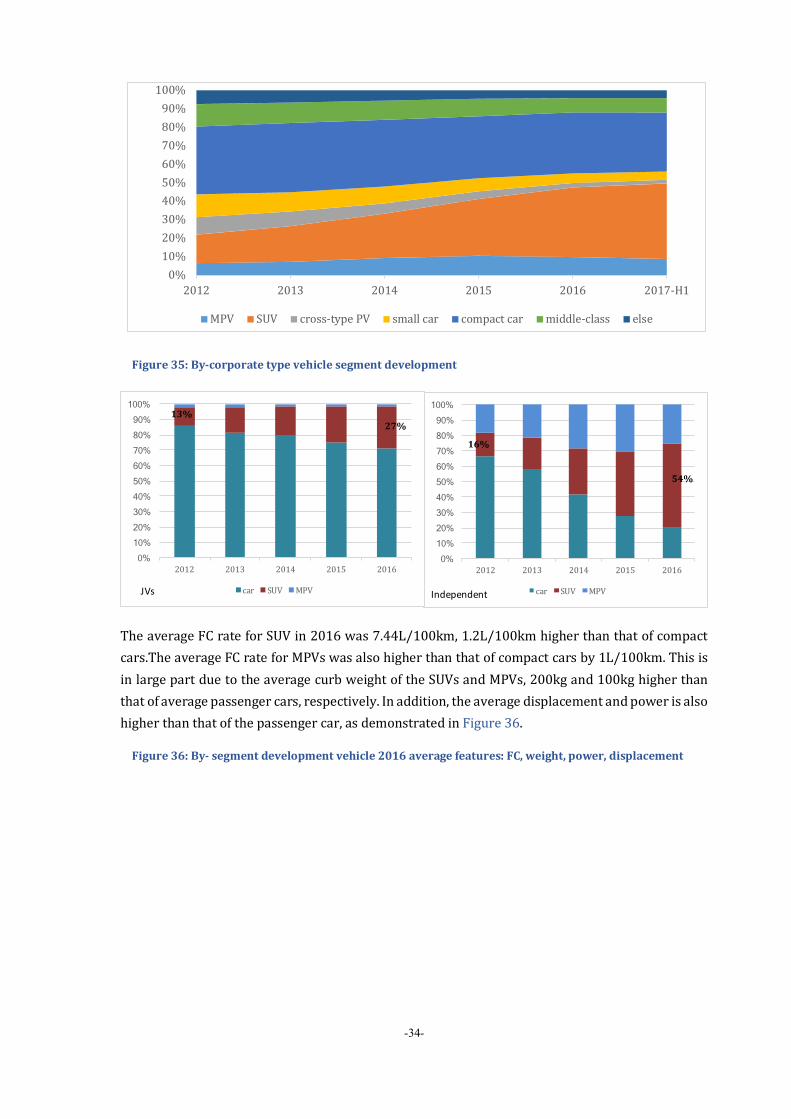

5.5ImpactofSUVandMPVmarketexpansiononChina’snationalFCperformance Whilecompactcarssawlessthan4%growthin2016,SUVandMPVsalesincreasedbyover40%and20%(respectively)forfourconsecutiveyears,erodingthemarketshareofsmallandcompactcar.In2016,SUVsandMPVsaccountedfornearlyone-halfoftheentirepassengercarmarket,asillustratedinFigure34.

SUVmarketshareincreasedfrom15%in2012toover40%in2016.MarketshareofindependentSUVsinparticular,increasedfrom16%to64%,whileJV’sSUVsmarketshareincreasedfrom13%to27%,duringthisperiod–asshowninFigure35.

Figure34:By-segmentmarketsharedevelopment

-32% -30% -19% -13% -13% -13%

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

Porsche Audi Volvo BMW Audi Nissan

CAFC(L/100km)

2012 2013 2014 2015 2016

7.12

6.83

7.11

7.67 7.64

6.58 6.56 6.66

7.017.21

6.0

6.4

6.8

7.2

7.6

8.0

2012 2013 2014 2015 2016

CAFC

,L/100km

GreatWallAuto ChanaAuto

-34-

Figure35:By-corporatetypevehiclesegmentdevelopment

TheaverageFCrateforSUVin2016was7.44L/100km,1.2L/100kmhigherthanthatofcompactcars.TheaverageFCrateforMPVswasalsohigherthanthatofcompactcarsby1L/100km.ThisisinlargepartduetotheaveragecurbweightoftheSUVsandMPVs,200kgand100kghigherthanthatofaveragepassengercars,respectively.Inaddition,theaveragedisplacementandpowerisalsohigherthanthatofthepassengercar,asdemonstratedinFigure36.

Figure36:By-segmentdevelopmentvehicle2016averagefeatures:FC,weight,power,displacement

0%10%20%30%40%50%60%70%80%90%100%

2012 2013 2014 2015 2016 2017-H1

MPV SUV cross-typePV smallcar compactcar middle-class else

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

2012 2013 2014 2015 2016

car SUV MPV

54%

16%

Independent

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

2012 2013 2014 2015 2016

car SUV MPV

27%13%

JVs

-35-

GivenhigherFCrateaswellastheincreaseinmarketshareforSUVsandMPVs,FCtargetshavebecomehardertoachievethantheywerebefore.IfthestructureofChina’scarmarketin2016wassimilartothatof2012,averagetotalFCwouldhavebeenabout20%lower,asshowninFigure37.

Figure37:SUV/MPVmarketshareincreasepushesaverageFCupward

Note:PredictedFCisbasedon2012autostructure;becauseSUVandMPVshareislikelytocontinuetoincrease,FCislikelytoincrease.

1,309

1,515

1,404

1,141

1000

1100

1200

1300

1400

1500

1600

CurbWeight�kg

car SUV MPV cross-typePV

1576

1709

1548

1286

1000

1100

1200

1300

1400

1500

1600

1700

1800

Displacement�ml

car SUV MPV cross-typePV

95

114

87

68

60

70

80

90

100

110

120

power�kw

car SUV MPV cross-typePV

6.18

7.44

7.06

6.55

5

5.5

6

6.5

7

7.5

8

AverageFC�L/100km

car SUV MPV cross-typePV

0.05

0.12

0.21

0.28

6.83

6.55

0.00

0.10

0.20

0.30

0.40

6

6.4

6.8

7.2

7.6

2012 2013 2014 2015 2016

L/100km

L/100km

FCgap FC predictedFC

-36-

6. CHINACAFCNEV(SUPER-)CREDITSANDNEVCREDITS

6.1CorporateCAFCNEVsuper-creditsAfter entering Phase IV, given themarket dominance of domestically produced cars and theirincreasedproductionofNEVs,overallCAFCcreditsmaintainedhighvolumeandmanufacturerscompliancepressures remained low–asdemonstrated inFigure38.GreatWallhad the largestshortageofCAFCcreditsin2016,andmaythereforepurchasecreditsfromYogoma,anEVcompanythatGreatWallbought25%of its shares.ChanganAutomobile, the second largestmanufacturerwith CAFCshortage, is likely to be reliant onChanganGroup's affiliatedenterprises for creditscompensation.

Figure38:By-segmentdevelopmentvehicle2016averages:FC,weight,power,displacement

Note: The 2013-15 credits are calculated according to the "AccountingMethod for Average FuelConsumptionofPassengerVehicleEnterprises",while2016creditsarecalculatedincludingflexibilitymechanism.9 If2016calculationswereperformedusing2013-15credits,creditsfortheseyearswouldhavebeensignificantlyreduced.Figure39:Top10surplusCAFCsupercreditsholders

9 Passenger car CAFC calculation method (乘用车企业平均燃料消耗量核算办法)http://chinaafc.miit.gov.cn/n2257/n2783/c86525/content.html

397

632

10461117

99 125198

1117

-32 -27 -18 -137

-200

0

200

400

600

800

1000

1200

2013 2014 2015 2016

CAFCcredits�10k

creditsurplus- previousmethod creditsurplus-newmethod CAFCcreditdeficit

Domestic(JVs+Independent)

1137 5202 10699 14812

37800

152172

16700

62608

4568

5284

0

50000

100000

150000

200000

250000

2010 2011 2012 2013 2014 2015

NEVvolu

me

PEV-domesticproduced PHEV-domesticproduced EVsimported

Imported

-37-

In 2016, as indicated in Figure 38, the top 10 CAFCcredit producerswereNEVmanufacturers(besides FAW-Volkswagen), the majority of which were JVs e.g. FAW-Volkswagen, ShanghaiVolkswagen, Changan Ford, BMW Brilliance, and Dongfeng Nissan. The greatest CAFC creditshortageswere fromSUV leadersGreatWallandChangan,witha totalof290,000and230,000negativepointsrespectively,asshowninFigure40.Thebulkofthe2016CAFCcreditdeficitwasproducedbytwomajorindependentbrandmanufacturers,GreatWallandChangan,withatotalof290,000and230,000negativecredits,respectively.CheetahandSAICalsohadanexcessofover100,000deficitofcredits.

Figure40:Top10deficitCAFCsupercreditsholders

Great Wall, the largest negative credit automanufacturer, has transferred as many as 40,000positivecredits forwardsince2013(only80%of thecreditscanbetransferredtothe followingyear))yetstillholds270,000negativecredits.Inordertocomply,GreatWallisprojectedtoinject25%ofthesharesofelectriccarmakerYogomointoitsaffiliatedcompanyinordertoachieveFCcompliance10.

10 长城入股御捷,新一轮新能源领域的合资合作即将开启.http://auto.sina.com.cn/news/qw/2017-08-30/detail-ifykpuuh9592164.shtml

0.0

20.0

40.0

60.0

80.0

100.0

120.0

BAIC-Motor

BYD-Auto

FAW-VW

BYD-AutoIndustry

Jiangnan-Motor

Geely-Motor

SAIC-Motor

Chery

Geely-Dihao

JAC

CAFCsurplus,

10k

-35.0

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

SoueastMoter

Brilliance-Jinbei

Chana-Ford

GAC-FCA

FAW-Toyota-Sichuan

Leopaard

SAIC-GM-BS

Chana-Motor

GWM

CAFCnegetivecredit,

10k

-38-

Changan Automobile, the second largest negative credits manufacturer, has relatively lowcompliancepressure. Some of itsnegativepoints can be carried forward usingpositive creditsproducedinpreviousyears–morethan100,000positivecreditsgeneratedin2013.In2016,thecompany generated about 21,000 new energy credits through its various affiliates companies(Changan Mazda, Changan Suzuki, Hefei Changan, etc.). Recently, Changan Automobile alsointroduced"Shangri-La,"anewenergybrandthatisprojectedtoincreaseinvestmentinnewenergyvehiclestocomply11.

ChanganFordperformedwellincorporateCAFCcomplianceinthepastfewyears,butgeneratedover70,000negativecreditsin2016.Thecompanymainlyproduceshigh-qualitysedansandSUVs.After entering Phase IV, the standard increased in stringency, and is becoming harder tomeetwithoutnewenergyvehiclesproduction.

Inrecentyears,GuangzhouAutomobileGroupproducednegative integrals.From2015to2016,energy-saving technologies were widely employed in the development of the GAIC GS seriesmodels,asGS4withlowFCgainsagoodsales.Inthisway,withouttheaidofnewenergyvehicles,thecompanymanagedtomaketheshiftfromanegativeCAFCtoapositivecreditsmanufacturer.

6.2NEVcreditsIn2016,thenumberofdomesticNEVcarsreached319,000,accountingfor1.35%ofChina’stotalpassengercars.Thismarkedanincreaseof48.5%fromthepreviousyear,asshowninFigure41.Also in this time,pureelectricvehicle (PEV)andplug-inhybridvehicle (PHEV)productionwas248,000and70,000,respectively.Importsofelectricpassengercarsreached16,600,doubledfromlastyear.NEVsgradually shifted fromcommercialandgovernmentprocurement to theprivatepassengercardomain.

Figure41:NEVsproductiondevelopment

11 2025年将全部停售燃油车?长安汽车发布“香格里拉”计划.http://auto.sina.com.cn/j_kandian.d.html?docid=fymzzpv7049586&subch=bauto

-39-

AccordingtotherecentlyintroducedintegratedCAFCsupercreditsandNEVcreditsmanagementsystem,allmanufacturersproducingover30,000vehiclesperyearwouldberequiredtoproduce10%NEVsin2019(about60domesticmanufacturersand10importers).Companiesrequiredtocomplymakeupover90%ofthemarket.In2016,atotalof954,000newenergypassengervehiclesweregenerated,ofwhich813,000werefromPEVsand141,000werefromPHEVs.Accordingtothecompliancerequirementsof2019,3millionNEVcreditsarerequired,equivalenttoabout1millionNEVs.BasedonNEVgrowththusfar–thistargetwillbeeasilymet.

In2016,therewerenineautomobileenterpriseswithanNEVoutputexceeding10,000,includingBYD,Beiqi,Geely,JiangnanAutomobile,SAIC,Chery,andJAC.Atotalof901,000NEVcreditsweregenerated,accountingfor94.4%ofthetotalcredits,asshowninTable6.

MostNEVcreditsareprojectedtobeproducedbyBYD,Beiqi,Geely,Jiangnan,andJMC.Inparticular,BYDgenerated250,000+NEVcreditsurplusthatcouldbeusedtooffsetnegativeCAFCcredits(ownorothers).

Table5:NEVpointsformajorChineseelectricvehiclemanufacturersin2016

Vehiclemanufacturer Mainmodels

NEVproductionvolume

NEVcredits

2019NEVcreditsrequirement(10%)*

Creditssurplus**

BYDindustry Tang/Denz/e6 46458 154784 9652 145132

152172

248283

62608

70463

5284

16595

0

50000

100000

150000

200000

250000

300000

350000

400000

2010 2011 2012 2013 2014 2015 2016

NEV

vol

ume

PEV-domestic produced PHEV-domestic produced EVs imported

-40-

BAICMotor EU200/EV200 42260 113745 29764 83981

BYDAuto Qin/e5 40186 130719 22927 107792

GeelyMotor DihaoEV/ZD 39449 133811 33003 100808

JiangnanMotor

Zotye100/E200/JiangnanTT 35899 104301 25834 78467

SAICMotor Roewee550/e950 22151 45896 29121 16775

Chery Arrizo7/eQ 20118 50415 41219 9196

JAC iEV5 18370 60632 30960 29672

JMC-Landwind E100/E200 17362 45558 7879 37679GeelyHaoqing

Motor ZD 7533 19493 49307 -29814

ChanaMotor EadoEV 5701 21880 99294 -77414

Dongfeng ER30 5298 19734 14583 5151

Note:*The10%NEVcreditsrequirementcalculationherefor2019isbasedon2016vehicleproductioninsteadofsame

yearproduction.

**Surplusiscalculatedincomparisontothe2016-basedgenerated2019NEVcreditsrequirementversus2016NEV

production.

Atpresent,theelectricvehiclemarketisdominatedbyvehiclesofClassAandbelow(about75%).FortheClassB(e.g.sedansorSUVs)vehiclesavailable,NEVsareprimarilyplug-inhybridvehicles.In2016, theaverage curbweightofelectricvehicleswas1480kg.PEVsaveraged1355kgwhilePHEVsaveraged1917kg,66kgheavierthan thatof conventionalvehicles.Althoughtheaverageweight increaseofelectricvehicleswasderived fromaddedbatteryweight, increases inPHEVsweightwasderivedfromlargervehiclemodels.ListedinTable6,PEVsaveragereportedmileagewas204km.

Table6:ComparisonbetweenICEandEVparametersin2016

Vehicleparameters

PureElectricVehicles(PEV)

Plug-inHybridVehicles(PHEV)

InternalCombustionEngine

(ICE)CarsVehiclesizegroup A00/A0/A A/B

All

Energyconsumption*

N/A N/A6.86L/100km

Weight,kg 1355 1917 1391

Power,kW 69 119 101

Displacement,ml

0 16891617

Range,km 204 N/A UnlimitedNote:Themodelparametersinthetablearecalculatedbasedontheaveragefeaturesofdomesticmodels(imported

modelsareexcluded).

*PEVsandPHEVspowerconsumptiondataisnoteasilyaccessible(amongotherreasons,becauseNEVsaretaxexempt

andthereforelessreportingisavailableonline).

-41-

In2016,asmanyastenPEVsexceeded10,000vehiclesales, includingtheBYDe5/e6,BAIC200EU200/EV200, ImperialEV,Zotyeun100,andCheryeQ.Their featureswereas follows:energyconsumptionranged10-20kwh/100km,e-ranged150-400km,andNEVcreditseligibilityranged1.33-5.28credits(averaging3.28credits),asdetailedinTable7.DetailsrelatedtothesefeaturesofmajorPHEVbrandsareavailableinTable8.

Table7:FeaturesofChina’s2016majorPEVbrands

Model Curbweight(kg)

e-range(km)

Energyconsumption(kwh/100km)

2016Annualsales

NEVcreditseligibility

BYDe6 2420 400 19.5 18917 5.00BAICEU200 1600 200 12 17892 3.84

JeelyDihaoEV 1570 300 N/A 16894 4.40Zotye100 1040 150 10 15314 2.60CheryeQ 1128 151 12 15136 2.61ZotyeE200 1080 160 N/A 13497 2.72 BYDe5 1845 256 N/A 12333 3.87

BAICEV200 1295 200 15 10509 3.84JMCE100 825 152 N/A 10005 2.62ZDD2 690 155 N/A 9178 2.66

Note:BecausePEVspowerconsumptiondataisnoteasilyaccessible,thecreditscalculationusesafactorof1forall

models.

Table8:FeaturesofChina’s2016majorPHEVbrands

ModelCurb

weight(kg)e-range(km)

Energyconsumption(kwh/100km)

2016Annualsales

NEVcreditseligibility

BYDTang 2280 80 2.0、N/A 24871 2BYDQin 1720 80 1.4、N/A 19493 2

Roewee550 1699 58 1.6、N/A 16253 2Arrizo7 1590 50 2.7、N/A 3660 2

Roewee950 1590 60 1.7、N/A 3900 2Note:BecausePHEVspowerconsumptiondataisnoteasilyaccessible,thetablestatesN/A(notapplicable).

6.3NEVcreditsimpact:concludingremarksChina’snewNEVcreditssystemisprojectedtodriveNEVproductionwhilelargelyavoidingenergysavingshiftsamongtraditionalandwellsellingICEmodels.Forexample,JMCHoldingsaverageFCrateisashighas9.76L/100km.Thecompany’sFCchallengeisledbyitsbestsellingSUVLandsatX7withFCashighas10.4L/100km.However,theproductionofitsA100E100electriccar(showninFigure24)droppedthecompany’saverageFCto4.71L/100km.Theissueistheresultedcarbonimpact.Werethe10,000E100producedsoldandusedwithinhighlypopulatedareasandthereforebroughtactuallocalcarbonandotheremissionreductionsorisitthe60,000highlypollutingX7swhicharenowthedominantsourceoflocalairquality?

Figure42:SelectedICEversusNEVmodel

-42-

Asmanyas12majorelectricvehiclecompanies(includingNEVandnon-NEV),wereabletoreducetheirICEvehiclebasedcorporateaverageFCby3%to68%,asshowninFigure43.TheaccumulatedNEVcreditsurpluscan,inturn,betransferredtoaffiliatedcompanies(definedasfigure13),orsoldto other companies, but not to save for use in future years. One approach adopted by largemanufacturersistheacquisitionofNEVmanufacturersandthecreationofstrategicJVs,addingtomarketnon-competitiveness,impedingthegoalsofthestandardregimeandfurthercomplicatingthemanagementofthestandard’simplementationandenforcement.

Figure43:NEVsupercreditimpactonCAFCofEVproducers

Intheshortterm,NEVmanufacturerswillbebenefitedbythenewNEVcreditstandardasitwillcreatearevenuestreamandenablefurtherinvestmentsinproductimprovement,aswasthecaseintheUSintheearlyyearsoftheZEV-creditspolicy.Forinstance,theGreatWallinvestmentsintheYogomo.

TosumupiCET’sviewsontheinfluenceofNEVcredits:

JMC-ICEFlagshipmodel–Landwind X7Production2016�approx. 60thousand�75%oftraditionalmodelsKerb mass�1775kgAveragedisplacement�2.0LAverage power�140kWCombinedfuelconsumption�10.4L/100km134%oftarget�7.9L/100km

JMC-EVFlagshipmodel-E100Production2016�approx.10thousand�60%ofelectricmodelsKerb mass�825kgAveragedisplacement�152kmAverage power�20kWCombinedelectricityconsumption�N/ANEV credit�2.62pervehicle

VS

0%10%20%30%40%50%60%70%80%

0.00

2.00

4.00

6.00

8.00

10.00

12.00

BYD-Autoindustry JM

C

BYD-Auto

BAIC-Motor

Jiangnan-Motor

Geely-Motor

SAIC-Motor JAC

Chery

DongfengMotor

Geely-Dihao

ChanaMotor

CAFCDecrease

CAFC

(L/100km

)

CAFC(excludingNEV) CAFC(includingNEV) CAFCdecrease

-43-

(1) NEVcreditswillplayakeyroleinthetransitionofChina’sautosectorintoagloballeaderinzerotailpipeemissionefforts,asitprovidesfinancialincentivestoadvanceinvestmentsinNEVs.

(2) GiventheNEVcreditsystem,investmentsinenergysavingpoliciesandprogramsisevenlessdesirable thanbefore. Since companieshavenotbeendelivering the improvementsneededformeetingthestandard,theshifttoNEVsmayfinallypresentanimplementableapproachtovehicleemissionsreductions.

(3) OverallemissionimpactsoftheNEVcreditshasyettounfold.Yetpoliciesgoverningenergyproductionshouldmoveaheadquicklyandeffectively,andoverallgainsareprojectedinthelongerrun.

InordertoensuretheNEVismakingactualcontributiontoChina’semissionreductiongoals,iCET’ssuggeststhefollowing:

(5) TheNEVcreditsystemshouldbeastand-alonemechanisminordertoclarifycorporateresponsibilitiesandenablegoodimplementationandenforcement.GivenChina’scomplexindustrialandinter-ministerialstructures,theCAFCregimehasproventobetoocomplextomanagewell,evenbeforetheNEVcreditpolicywasintroduced.

(6) Policydesignersshould introduce longertermrequirementsandpredictablebaselineoftheNEVcreditspolicyshouldbepresentedassoonaspossibletoenablestrategicmarketplanning, minimize market risks and promote steady investment streams, and soundgradualimprovementsofqualityNEVs.

(7) Policy makers should introduce well-informed and effectively implementable penaltymechanismtoensurethestrengthandeffectivenessoftheNEVcreditspolicy.Thisincludesfeelevels,supplementarypenalties(forexample,creditowedwillstillbeowedregardlessofpenaltiespaid),andefficientandtransparentpolicyscrutinyandpanelizingprocess.

(8) Policymakers should consider simplification of the policy to ease itsmanagement; forexample,eliminatethepracticeofforwardingcreditsamongcorporateactors.

-44-

BIBLIOGRAPHY 中国石油经济技术研究.2016年国内外油气行业发展报告.2017.01环保部.中国机动车环境管理年报 2017.2017.06http://www.zhb.gov.cn/gkml/hbb/qt/201706/W020170605537942778925.pdf汽车推荐性国家标准《电动汽车与插电式混合动力汽车能耗折算方法》征求意见的函 .http://www.catarc.org.cn/NewsDetails.aspx?ID=2707,2016年 7月 22日查询汽车推荐性国家标准《乘用车循环外技术/装置评价方法第 2部分怠速起停系统》征求意见的

函.http://www.catarc.org.cn/NewsDetails.aspx?ID=2664,2016年 7月 22日查询.汽车推荐性国家标准《乘用车循环外技术装置节能效果评价方法第 1部分节能驾驶指示装置》

征求意见的函.http://www.catarc.org.cn/NewsDetails.aspx?ID=2641,2016年 7月 22日查询.汽车推荐性国家标准《乘用车循环外技术装置节能效果评价方法第 3部分汽车空调》征求意

见的函 http://www.catarc.org.cn/NewsDetails.aspx?ID=2798,2017年 10月 30日查询.

汽车推荐性国家标准《电动汽车能量消耗率限值》征求意见的函.

http://www.catarc.org.cn/NewsDetails.aspx?ID=2882,2017年 10月 30日查询

工信部等五部委 . 乘用车企业平均燃料消耗量与新能源汽车积分并行管理办法

http://www.miit.gov.cn/n1146285/n1146352/n3054355/n3057585/n3057592/c5826834/content.html中国汽车燃料消耗量网站.http://chinaafc.miit.gov.cn/2017年 1月 30日查询工信部.公示 2016年度乘用车企业平均燃料消耗量情况.2017年 8月 31日查询

http://www.miit.gov.cn/n1146285/n1146352/n3054355/n3057585/n3057589/c5560565/content.html康利平,MayaBenDror,秦兰芝,安锋.《中国乘用车燃料消耗量发展年度报告 2016》.(2017-06-28)http://www.icet.org.cn/admin/upload/2016092350679321.pdf