china distribution & trading - fung group issue 22 january 2005 china distribution & trading...

TRANSCRIPT

1Issue 22 January 2005

China Distribution & Trading Issue 22 January 2005

IN THIS ISSUE :

Li & Fung Research Centre

13/F, LiFung Centre

2 On Ping Street

Shatin, Hong Kong

Tel: (852) 2635 5563

Fax: (852) 2635 1598

E-mail: [email protected]

China’s Consumer Market and

The Market Profile on

Three Major City Clusters:

The Pearl River Delta,

the Yangtze River Delta, and

the “Beijing-Tianjin-Hebei” Region

China – a Huge but Not a Single UnifiedMarket

Given a population of 1.3 billion people, no doubt, China has a huge consumer market

with great potential. Over 1978 – 2003, GDP and total retail sales of consumer goods

rose at an average annual rate of 14.92% and 14.48% respectively. Such an expanding

consumer market, however, presents a fragmented picture. Incomes vary enormously

from region to region, and from urban to rural areas. Different regions are developing

at their own pace due to vast differences among cities and regions in terms of

geographical location, economic development, etc. Each provincial/city government

also wants to protect their local businesses, hence leading to barriers to enter the

markets. Overall, China is not a single unified market; instead, it is composed of many

fragmented, localized markets.

I. The Market Profile on Three Major CityClusters: The Pearl River Delta, the YangtzeRiver Delta, and the Beijing-Tianjin-HebeiRegion

1. The Pearl River Delta

The Pearl River Delta (PRD) Economic Zone locates in the central and southern part

of Guangdong province, an area immediately north of Hong Kong and Macao and

surrounding the Pearl River. The PRD Economic Zone covers 13 cities and counties

(districts), including 2 sub-provincial-level cities: Guangzhou and Shenzhen; 5

prefecture-level cities: Dongguan, Foshan, Zhuhai, Zhongshan, Jiangmen; urban

districts of Huizhou, Huidong County, Boluo County, urban districts of Zhaoqing,

Gaoyao County-level City and Sihui County-level City (See Exhibit 1). It has an area

of 41,698 square kilometers, about 0.43% of the total area of the whole country. Its

size of population is 23.99 million, 1.86% of the national total.

China – a Huge but Not

a Single Unified Market

I. The Market Profile on

Three Major City Clusters:

The Pearl River Delta, the

Yangtze River Delta, and the

“Beijing-Tianjin-Hebei” Region 1

1. The Pearl River Delta 1

2. The Yangtze River Delta 5

3. The “Beijing-Tianjin-Hebei”

Region 12

II. General Background on

China’s Consumer Market 15

1. The Two-tier Market:

Urban and Rural 15

2. Regional Disparity in

Wealth and Consumption 18

3. The Upgrading of

Consumption Structure 20

4. Fragmented Market:

Local Protectionism 23

2Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Exhibit 1: Map of the Pearl River Delta Region

Zhanjiang

Maoming Yangjiang

Yunfu

Jiangmen

Zhaoqing

Qingyuan

Shaoguan

HeyuanMeizhou

Zhongshan

Guangzhou

Chaozhou

ShantouJieyang

ShanweiHuizhou

Zhuhai

Shenzhen

DongguanFoshan

Hong Kong

Gaoyao

Zhaoqing

Sihui

Guangzhou

Foshan Dongguan

Jiangmen

Zhongshan

Zhuhai

Shenzhen

Boluo

Huizhou

Huidong

Hong Kong

The PRD has been China’s most economically dynamic

region since the onset of China’s reform and opening up in

1978. The GDP of the PRD grew from below 12 billion yuan

in 1980 to over 1,134 billion yuan in 2003. During the period,

the average annual growth rate of GDP in the PRD was

21.87%, well above that of Guangdong Province (13.6%)

and the country as a whole (9.6%). The per capita GDP of

the PRD amounted to USD 4,800 in 2003, which is 2.3

times that of Guangdong Province and 4.36 times that of

the whole country. The PRD has also been the economic

hub of Guangdong Province. The PRD region accounted

for 25% of Guangdong’s land area but contributed over 84%

of the province’s GDP in 2003. Within the PRD region,

Guangzhou, Shenzhen, Foshan and Dongguan are the

most prosperous cities, and the per capita GDP of each of

them was over 40,000 yuan (USD 4,830) in 2003.

The PRD has also increasingly become an attractive

consumer marketplace. Over the past two decades, the

retail sales of consumer goods in the PRD increased

dramatically from 7.07 billion yuan in 1980 to 397.66 billion

yuan in 2003. In 2003, the retail sales of consumer goods

grew by 11.81% year-on-year (yoy), and accounted for over

70% of the provincial total.

3Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

(1) Guangdong Province

Guangdong Province, where the PRD is located, is one of

the most economically developed provinces of China. In

2003, Guangdong’s GDP reached 1,345 billion yuan, up

by 13.6% yoy, which is the highest growth rate since 1996.

The value-added of the primary industry, the secondary

industry and the tertiary industry were 105.16 billion yuan

(up by 1.2% yoy), 704.81 billion yuan (up by 18.1% yoy)

and 535.03 billion yuan (up by 10.8% yoy), respectively.

a. Retail sales

Guangdong Province has been the largest consumer market

among all provinces in the country though its population

only ranks the fourth. The total retail sales of consumer

goods in Guangdong increased by 11.4% yoy to reach

501.36 billion yuan in 2003, accounting for 12.26% of the

national total. Of which, the retail sales of consumer goods

in urban areas grew by 11.6% yoy to reach 398.77 billion

yuan, and the retail sales of consumer goods in rural areas

grew by 12.35% yoy to reach 161.833 billion yuan. As shown

in Exhibit 2, the retail sales of consumer goods in

Guangdong mainly concentrated in the PRD (See Exhibit

2). Guangzhou, in particular, is the city with the biggest

consumer market in Guangzhou, with its retail sales of

consumer goods hitting 149.43 billion yuan in 2003.

Shenzhen ranked the second, with retail sales of consumer

goods amounting to 80.18 billion yuan (See Exhibit 3).

Exhibit 2: Retail sales of consumer goods in Guangdong Province in 2003

Zhanjiang

Maoming Yangjiang

Yunfu

Jiangmen

Zhaoqing

Qingyuan

Shaoguan

HeyuanMeizhou

Zhongshan

Guangzhou

Chaozhou

ShantouJieyang

ShanweiHuizhou

Zhuhai

Shenzhen

DongguanFoshan

Hong Kong

80 - 15040 - 7920 - 3910 - 19< 9

Retail sales of consumer goods (billion yuan)

Source: Guangdong Statistical Yearbook, 2004

4Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Exhibit 3: Living Standard of Local Residents in Major Cities of the PRD in 2003

(Year-on-year growth %)

Total Retail

Major City GDP Per Capita GDP Sales of Consumer Goods

(million yuan) (%) (yuan) (%) (million yuan) (%)

Guangzhou 349,687.87 (15.2%) 48,372 (14.2%) 149,427 (9.02%)

Shenzhen 289,540.70 (19.2%) 54,545 (9.3%) 80,177 (16.27%)

Zhuhai 47,327.42 (17.5%) 37,675 (16.3%) 15,918 (10.95%)

Foshan 138,159.51 (16.1%) 40,444 (14.7%) 47,319 (12.72%)

Jiangmen 73,008.25 (11.1%) 19,131 (10.9%) 27,784 (11.86%)

Dongguan 94,796.54 (19.5%) 60,158 (17.6%) 33,800 (50.26%)

Zhongshan 50,140.43 (18.6%) 28,645 (16.4%) 15,361 (14.35%)

Huizhou 59,097.72 (13.9%) 20,759 (12.7%) 18,167(12.84%)

Zhaoqing 46,639.14 (11.4%) 11,907 (10.9%) 17,120 (10.72%)

Source: Guangdong Statistical Yearbook, 2004

Looking at retail sales of consumer goods by sector, the retail sales of the Wholesale and Retail Trade Sector in Guangdong

reached 468.108 billion yuan in 2003, up by 28.65% over the previous year. The retail sales of Catering Services were 87.729

billion yuan in 2003, up by 5.74% yoy (See Exhibit 4).

Exhibit 4: Retail Sales of Consumer Goods in Guangdong, 2002-2003

2003 2002 2002-2003 Growth (%)

(billion yuan) (billion yuan)

Total retail sales of consumer goods 560.602 501.359 11.82%

By Location of Retailers:

City 398.77 357.31 11.6%

County and Under County Level 161.833 144.049 12.35%

By Sectors:

Wholesale and Retail Trade 468.108 363.851 28.65%

Catering Services 87.729 82.964 5.74%

Others 4.765 54.544 -91.26%

Source: Guangdong Statistical Yearbook, 2004

b. Income level

Incomes of both urban and rural residents in Guangdong Province increased steadily in 2003. The per capita annual disposable

income of urban residents in Guangdong in 2003 was 12,380.43 yuan, up by a real growth of 10.4% yoy. The per capita net

income of rural residents in Guangdong in 2003 was 4,054.58 yuan, up by a real growth of 3.4% yoy.

5Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

c. Price level

The general price level in Guangdong Province in 2003

increased by small margin in 2003. The Consumer Price

Index (CPI) of Guangdong recorded an annual growth of

0.6% in 2003. Of which, “Residence” grew by 3.1%; “Food”

by 2.3%; and “Health Cares and Personal Articles” by 0.4%.

The CPI of “Clothing”, “Household Facilities, Articles and

Services”, “Transportation and Communication”, and

“Recreation, Education and Cultural Articles” decreased

(See Exhibit 5).

Exhibit 5: Consumer Price Indices ofGuangzhou Province in 2003

Year-on-year

Item growth rate (%)

Consumer Price Index 0.6

Urban Areas 0.7

Rural Areas 0.4

Food 2.3

Of which: Grain 1.9

Clothing -2.3

Household Facilities, Articles

and Services -2.0

Health Cares & Personal Articles 0.4

Transportation and Communication -2.1

Recreation, Education and Cultural

Articles -2.0

Residence 3.1

Services 0.1

Source: National Bureau of Statistics, PRC

d. The development of the retail sector

Guangdong has one of the most developed retail sectors

in China. In addition to traditional department stores, various

forms of modern retail operations such as chain stores,

supermarkets, hypermarkets and convenience stores

flourish in the market. As a result of the shift of consumers

preference towards those new modes of retail operations,

the number of traditional department stores dropped by an

averaged rate of nearly 10% from 10,073 in 2000 to 7,511

in 2003 (See Exhibit 6).

Major foreign retail enterprises in Guangdong include Wal-

Mart from the U.S., Carrefour from France, Jusco from

Japan, Park’N shop from Hong Kong, and Trust-Mart from

Taiwan. It was reported that the four European giants, OBI,

Ikea, Metro and Decathlon, have also planned to open retail

outlets in Shenzhen. A host of franchised chain stores such

as U2, G2000, Baleno, Bossini, Fortei etc., and convenience

stores such as Circle K and 7-Eleven from Hong Kong have

also entered Guangdong. Many Hong Kong brands such

as A-Fontane, Airland, Saint Honore and Lion & Globe are

also on the list of famous brands existing in Guangdong.

Exhibit 6: Number of Retail Outlets inGuangdong Province in 2000and 2003

average

annual

growth

2003 2000 rate (%)

Total number of

outlets 66,086 49,897 9.82

By operating system

Detached Stores 41,083 36,315 4.20

General Chain stores 1,266 1,102 4.73

Branch Chain Stores 6,827 1,512 65.28

Others 16,910 10,968 15.52

By operating form

Department stores 7,511 10,073 -9.32

Supermarkets 1,287 1,135 4.28

Monopoly Stores 21,964 12,902 19.40

Others 35,324 25,787 11.06

Source: Guangdong statistical yearbook, 2001, 2004.

2. The Yangtze River Delta

The Yangtze River Delta (YRD) spans across 1 municipality

and 2 provinces. It has 16 cities, including 1 centrally-

administered municipality: Shanghai; 3 sub-provincial-level

cities: Nanjing, Hangzhou, Ningbo; 12 prefecture-level cities:

Suzhou, Wuxi, Changzhou, Zhenjiang, Nantong, Yangzhou,

6Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Taizhou of the southern Jiangsu Province, and Huzhou,

Jiaxing, Shaoxing, Zhoushan, and Taizhou of the northern

Zhejiang Province (See Exhibit 7). The YRD’s total

population stood at 75.6 million by the end of 2003,

accounting for about 6% of the national total.

Exhibit 7: Map of Shanghai Municipalityand 15 Cities of The YangtzeRiver Delta Region

Source: Hong Kong Trade Development Council

The development of the YRD has been extremely

impressive over the last decade. The growth of Shanghai

and its surrounding cities has created a new focal point of

China’s development. Although the YRD only covers an area

of 100,201 square kilometres, which is only 1% of the total

land area of China, its GDP reached 2,376.69 billion yuan

in 2003, accounting for one-fifth of the national economy.

The per capita GDP and disposable income of some YRD

cities are among the highest in China. For example,

Shanghai’s per capita GDP in 2003 exceeded US$5,600,

which was the highest among all municipalities, provinces

and autonomous regions in the Chinese mainland. In fact,

the YRD has become a very important economic

powerhouse of the Chinese mainland, with Shanghai being

China’s financial and logistics center, and Zhejiang and

Jiangsu being increasingly important world manufacturing

bases.

The YRD has one of the largest and most sophisticated

consumer markets in China. The relatively high income level

in the YRD, combined with a large inflow of tourists, resulted

in strong consumer demand. In 2003, the total retail sales

of consumer goods in the YRD reached 728.701 billion yuan,

up by 9.1% yoy.

The retail sector in the YRD is highly developed. Major

foreign-invested retail enterprises in the YRD include

Carrefour from France, Metro from Germany, Yaohan from

Japan, Park’N shop from Hong Kong, and Trust-Mart from

Taiwan. The retail distribution format in the YRD is also

changing rapidly. Apart from traditional department stores,

various forms of modern retail operation such as chain

stores, supermarkets, hypermarkets and convenience

stores are also flourishing. There are also many wholesale

markets within or very close to the YRD which are among

the largest in China or even the world, such as the wholesale

markets of small commodities in Yiwu, and textiles in

Shaoxing.

(1) Shanghai Municipality

Shanghai has been a commercial and financial center of

China historically. Its GDP amounted to 625.081 billion yuan

in 2003, contributing to 5.4% of the national GDP. Shanghai

ranked fourth in terms of utilized foreign direct investment

(FDI) (USD 5.16 billion) among all mainland cities,

accounting for 8.1% of China’s utilized FDI in 2003.

a. Retail sales

Shanghai’s total retail sales of consumer goods reached

222.06 billion yuan in 2003, up by 9.1% yoy, which

accounted for 4.8% of the national total. Of which, the retail

sales of consumer goods in urban areas grew by 9.5% yoy

to reach 190.59 billion yuan, and the retail sales of consumer

goods in rural areas grew by 6.8% yoy to reach 31.474

billion yuan.

Looking at total retail sales of consumer goods by sector,

the retail sales of the Wholesale and Retail Trade Sector in

Shanghai reached 175.927 billion yuan, up by 9.3% yoy.

The retail sales of Catering Services were 21.438 billion

yuan, up by 16.6% yoy (See Exhibit 8).

7Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Exhibit 8: Total Retail Sales of ConsumerGoods in Shanghai Provincein 2003

2003 2003-2003

(billion yuan) Growth (%)

Total retail sales of

consumer goods 222.064 9.1%

By Location of Retailers:

Urban 190.59 9.5%

Counties 31.474 6.8%

By Sectors:

Wholesale and Retail

Trade 175.927 9.3%

Catering Services 21.483 16.6%

Manufacturing 4.978 2.3%

Others 19.676 2.1%

Source: National Bureau of Statistics, PRC.

b. Income level

According to the National Bureau of Statistics, the per capita

disposable income of urban residents in Shanghai was

14,867 yuan in 2003, up by 12.2% yoy. The per capita net

income of rural residents in Shanghai was 6,658 yuan, up

by 7.2% yoy. With the rise in income and the upgrading of

consumption structure, the increase in demand for cars and

durable consumer goods among consumers in Shanghai

accelerated. In 2003, 78.4 thousand motor vehicles were

sold, up by 22.5%. Of which 71.1 thousand cars were sold,

up by 30%; 1.3 million mobile telephones, up by 110%; 41

thousand pick-up cameras , up by 35.4%; 5.77 million video

disc players , up by 32.3%; 8.07 million air conditioners,

up by 46.9%; and 2.89 million auto washing machine, up

by 28.1%.

c. Price level

The Consumer Price Index of Shanghai increased by 0.1%

yoy in 2003. Of which, the consumer prices of “Food”,

“Recreation, Education and Cultural Articles”, and

“Residence” increased. Consumer Price Index of “Health

Cares & Personal Articles” was the same as the previous

year. “Clothing”, “Household Facilities”, “Articles and

Services”, and “Transportation and Communication”

decreased (See Exhibit 9).

Exhibit 9: Consumer Price Indices ofShanghai in 2003

Year-on-year

Item growth rate (%)

Consumer Price Index 0.1

Food 1.3

Clothing -2.5

Household Facilities, Articles

and Services -1.6

Health Cares & Personal Articles 0.0

Transportation and Communication -3.7

Recreation, Education and

Cultural Articles 0.3

Residence 1.1

Source: National Bureau of Statistics, PRC.

d. Retail sector

Shanghai’s retail sector is one of the most developed in

China. Besides the traditional department stores, various

forms of modern operations flourish. The Shanghai

Chamber of Commerce has published the city’s first White

Paper, “White Paper — Shanghai’s Retail Development in

2003”. The White Paper identified 8 trends in Shanghai’s

retail business in the coming 3 to 5 years: (i) department

stores will be further reshuffled; (ii) the food and grocery

sector will continue its modernization process; (iii) industries

such as garment and accessories, and office equipments,

etc. will emerge as the major industries of the new retail

formats; (iv) the market will open further, drawing more retail

companies into the city; (v) a few large retailers will dominate

the market share; (vi) shopping malls will put greater

emphasis on innovation, management and optimization; (vii)

innovation, the application of managerial technology and

breakthroughs in supply chains will bring a new competitive

edge; (viii) and the growth of non-store retail, such as

automat, e-commerce and mail orders, will accelerate.

By the end of 2003, the number of chain stores which are

above designated size in Shanghai was 7,014. Of which

chain supermarkets reached 3,376, convenience stores

2,240. The retail sales of chain stores reached 80.04 billion

yuan in 2003, up by 27% yoy. Major foreign-invested retail

8Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

enterprises in Shanghai include Carrefour from France,

Metro from Germany, Isetan from Japan, Park’n Shop from

Hong Kong, and Pacific department store from Taiwan.

Dozens of franchised chain stores such as U2, G2000,

Baleno, Bossini, Giordano etc. from Hong Kong have also

entered Shanghai.

In addition, Shanghai consumers are also widely recognized

as trend-setters for fashion and other lifestyle products of

China. For example, lots of domestic merchandisers visit

Nanjing Road, one of Shanghai’s major shopping districts,

to take a look at the latest fashion trends in China. Likewise,

distributors from across the country visit Shanghai to

preview the latest fashion styles and designs, which are

expected to become popular in their own cities.

e. Major commercial districts

There are eight major commercial districts in Shanghai.

i. Nanjing East Road

It is a mid- to high-end commercial district where a number

of large department stores are located. Shanghai No. 1,

Hualian and New World together account for almost 50%

of the total sales on this road.

ii. Nanjing West Road

It is where the most prestigious shopping malls are located,

including CITIC Square, Plaza 66 and Westgate Mall.

According to statistics, about 80% of visitors at Plaza 66

would make purchases, with an average spending in the

range of 8,000 – 20,000 yuan. In 2001, the combined retail

sales of CITIC Square, Plaza 66 and Westgate Mall reached

1.35 billion yuan, up by 20% year-on-year.

iii. Huaihai Central Road

It is a mid- to high-end commercial district where a number

of department stores are located, including Shanghai

Department Store No. 2, Novel and New Hualian (clothing),

Parkson and Pacific (trendy merchandise), Orient Meisha

and Lady Fashion (Ladies’ clothing and accessories), and

Hongxing Optical (branded spectacles).

iv. Sichuan North Road

It is a low-end, mass-market commercial district. Large

department stores include Spring, Yuandong Electrical

Appliances Commercial Building, Shanghai No. 7, Hongji

Jiakou Plaza and Dongtai Plaza.

v. Xujiahui Commercial City

It is a mid- to high-end commercial district targeted at

young consumers. It covers Huashan Road, Hengshan

Road, Zhaojiabin Road and Tianyaoqiao Road. There are

nine large department stores and shopping malls,

including Shanghai Orient, Pacific, Shanghai Department

Store No. 6, Huijin, Huilian, Grand Gateway, Metro City

and Buynow.

vi. Yuyuan Tourist Mart

It is a low- to middle-end commercial district. It has been

traditionally a distribution hub for small commodities.

Nowadays gold jewellery, tourist souvenirs and antiques

dominate the district. “Gold jewellery” is the theme of all

major jewellers there, including Yayi, Yongsheng, Laomiao,

Pearl and jade Mart, Laofendxiang and Chenghuang.

vii. New Shanghai Square and Buyecheng

Centred around Zhangyang Road and a number of adjoining

streets, New Shanghai Square is a large shopping district

in Pudong. Shanghai No. 1 Yaohan Department Store

features the premier shopping centre in the district.

Buyecheng is a comprehensive commercial district featuring

shopping, commerce, dining and entertainment facilities.

viii. Xintiandi

It is a newly developed mid- to high-end commercial district

offering personal products and home decoration items with

an emphasis on lifestyle. Dining is still the main theme of

the district at the moment, but it is expected that Xintiandi

will become a posh shopping district selling upmarket, trendy

and personalised products in the near future. Foreigners

make up 80% of the consumers at Xintiandi.

9Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Exhibit 10: Major Economic Indicators of the Yangtze River Delta in 2003

Urban Per Capita Total Retail sales

Per Capita GDP Primary industry: Disposable Income of Consumer Goods

Municipality/ GDP (bn yuan) (yuan) (growth Secondary industry: (yuan) (growth (bn yuan) (growth

Tier Cities (growth rate % yoy) rate % yoy) Tertiary industry rate % yoy) rate % yoy)

1st-tier city Shanghai 625.1 (11.8%) 46,614 (14.5%) 1.5:50.1:48.4 14,867 (12.2%) 222.064 (9.1%)

2nd-tier cities Hangzhou 209.2 (15.0%) 32,700 (16.2%) 6.1:51.6:42.3 12,898 (9.5%) 58.752 (12.4%)

Ningbo 176.99 (15.3%) 28,220 (12.07%) 6.3:56.9:36.8 14,277 (10.1%) 52.15 (12.7%)

Suzhou 280.2 (18%) 47,700 (17%) 2.8%, 63.1%, 34.1% 12,350 (16.3%) 52.605 (16.5%)

Nanjing 157.62 (15.1%) 27,283 (13.1%) 4.1:51.1:44.8 10,195.56 (11.3%) 60.24 (14.4%)

Wuxi 190.1 (15.4%) 43,160 (14.5%) 3%, 57%, 40% 11,647 (16.6%) 48.71 (15.4%)

3rd-tier cities Shaoxing 108.8 (15%) 25,094 (14.9%) 7.8%, 59.2%, 33% 13,535 (11.6%) 29.2 (12.6%)

Jiaxing 85.563 (16.9%) 25,720 (16.7%) 7.72:59.31:32.97 12,954 (12.6%) 27.939 (12.1%)

Bantong 100.665 (13.4%) 12,923 (12.66%) 14:51.2:34.8 9,598 (11.1%) 33.128 (12.7%)

Changzhou 90.02 (18.4) 26,145 (19.5%) 5.2:57.2:37.1 11,307 (13.8%) 28.07 (12.8%)

Taizhou 99.278 (14.9%) 18,000 (14.5%) 9.3:58.2:32.5 13,609 (15.2%) 26.233 (13%)

4th-tier cities Zhoushan 17.18 (15.5%) 17,695.6 (36%) 19.1:40.3:40.6 12,213 (11.2%) 7.5 (12.1%)

Huzhou 48.897 (14.8%) 19,032 (14.8%) 11.3%, 33.9%, 54.8% 12607 (10.7%) 18.234 (11.7%)

Yangzhou 64.722 (13.4%) 14,300 (15.6%) 21:9:70 8,705 (11.1%) 19.796 (12.5%)

Zhenjiang 64.356 (14.1%) 24,089 (14%) 5.1:57.2:37.9 9,451 (15.2%) 16.82 (12.6%)

Taizhou 58.0 (13.4%) 11,492 (13.2%) 33.3:33.3:33.3 8,500 (9.1%) 17.26 (11.7%)

Source: Guide of 16 Major Cities in the YRD Region, Hong Kong Trade Development Council.

Key: Shanghai Municipality Jiangsu Province Zhejiang Province

a. Retail sales

Retail sales of the consumer market also witnessed a

relatively fast growth. In 2003, the retail sales of consumer

goods in Jiangsu reached 356.65 billion yuan, up by 13.7%,

1.6 percentage points higher than the previous year. The

retail sales of consumer goods in urban areas was 251.62

billion yuan, up by 14.6% yoy. The retail sales of consumer

goods in rural areas was 105.02 billion yuan, up by 11.5%

yoy (See Exhibit 11).

(2) Jiangsu Province

Jiangsu economy grew fast in 2003. The GDP reached

1,245.18 billion yuan in 2003, up by 13.5% yoy, 1.9

percentage point higher than the previous year. The value-

added of the primary industry was 110.66 billion yuan, which

was the same as last year. The value-added of the

secondary industry and the tertiary industry were 678.23

billion yuan (up by 17.2% yoy) and 456.27 billion yuan (up

by 11.7% yoy) respectively. The ratios of primary industry,

secondary industry and tertiary industry in 2003 was 8.9:

54.5: 36.6.

10Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Looking at total retail sales of consumer goods by sector,

the retail sales of the Wholesale and Retail Trade Sector in

Jiangsu reached 307.26 billion yuan in 2003, up by 13.0%

yoy. The retail sales of Catering Services were 43.45 billion

yuan, up by 20.2% yoy (See Exhibit 11).

Exhibit 11: To t a l R e t a i l S a l e s o fConsumer goods in JiangsuProvince in 2003

2003 2003-2003

(billion yuan) Growth (%)

Total retail sales

of consumer goods 356.65 13.7%

By Location of Retailers:

Urban 251.62 14.6%

Rural 105.02 11.5%

By Sectors:

Wholesale and Retail

Trade 307.26 13.0%

Catering Services 43.45 20.2%

Others 5.94 1.6%

Source: National Bureau of Statistics, PRC.

b. Income level

The per capita disposable income of urban residents in

Jiangsu was 9,262 yuan in 2003, up by 13.2% yoy. The per

capita living expenditure of urban residents was 6,708 yuan,

up by 11.0% yoy. The per capita net income of rural residents

in Jiangsu in 2003 was 4,239 yuan, up by 6.1% yoy. The

per capita living expenditure of rural residents was 2,704

yuan, up by 3.0% yoy.

c. Price level

The Consumer Price Index in Jiangsu in 2003 increased

by 1.0% yoy. Of which, the consumer prices of “Food”,

“Health Cares & Personal Articles”, “Recreation, Education

and Cultural Articles”, and “Residence” increased.

Consumer Price Indices of “Clothing”, “Household Facilities,

Articles and Services”, and “Transportation and

Communication” decreased (See Exhibit 12).

Exhibit 12: Consumer Price Indices ofJiangsu Province in 2003,Year-on-year growth rate (%)

Item Province

Urban Rural

Consumer Price Index 1.0 0.9 1.2

Food 3.3 3.7 2.6

Of which: Grain 2.1 2.7 1.2

Clothing -1.0 -1.1 -0.5

Household Facilities,

Articles and Services -3.4 -4.4 -1.7

Health Cares &

Personal Articles 0.3 -0.1 0.7

Transportation and

Communication -2.6 -4.6 -0.1

Recreation, Education

and Cultural Articles 2.5 1.6 3.6

Residence 1.0 1.4 0.6

Source: National Bureau of Statistics, PRC.

(3) Zhejiang Province

Zhejiang Province’s economy grew fast in 2003. The GDP

reached 939.5 billion yuan in 2003, up by 14% yoy. The

value-added of the primary industry, the secondary industry

and the tertiary industry were 72.2 billion yuan (up by 2.7%

yoy), 483.0 billion yuan (up by 16.6% yoy), and 364.8 billion

yuan (up by 13.2% yoy), respectively. The ratios of primary

industry, secondary industry and tertiary industry was

changed from 8.9 : 51.1 : 40.0 in 2002 to 7.8 : 52.5 : 39.7 in

2003.

a. Retail sales

Zhejiang Province is the fourth largest market of consumer

goods after Guangdong, Shandong, and Jiangsu. The total

retail sales of consumer goods in Zhejiang reached 315.71

billion yuan in 2003, up by a real growth of 11.5% yoy over

the previous year. Of which, the retail sales of consumer

goods in urban areas was 200.0 billion yuan, up by 11.5%

yoy. The retail sales of consumer goods in rural areas was

115.7 billion yuan, up by 9.8% yoy (See Exhibit 13). Looking

11Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

at the retail sales of consumer goods by sector, the retail

sales of the Wholesale and Retail Trade Sector in Zhejiang

reached 269.6 billion yuan in 2003, up by 10.1% yoy. The

retail sales of Catering Services were 35.89 billion yuan in

2003, up by 16.0% yoy.

Exhibit 13: To t a l R e t a i l S a l e s o fC o n s u m e r g o o d s i nZhejiang Province in 2003

2003 2003-2003

(billion yuan) Growth (%)

Total retail sales of

consumer goods 315.7 11.5%

By Location of Retailers:

Urban 200.0 11.5%

Rural 115.7 9.8%

By Sectors:

Wholesale and Retail

Trade 269.6 10.1%

Catering Services 35.89 16.0%

Others 10.18 14.4%

Source: National Bureau of Statistics, PRC.

b. Income level

The living standard of the residents in Zhejiang Province

has been improving considerably. The per capita disposable

income of urban residents in Zhejiang Province was 13,180

yuan in 2003, up by a real growth of 11.9% yoy. The per

capita net income of rural residents was 5,431 yuan, up by

a real growth of 7.8% yoy. The Engel Coefficient, a measure

of the proportion of food expenditure to the total living

expenditure, of urban households and rural households was

36.6% and 38.2%, dropped by 1.3 percentage point and

2.6 percentage points, respectively.

c. Price level

The Consumer Price Index in Zhejiang in 2003 increased

by 1.9% yoy. Of which, the growth figures were 0.5% for

Urban CPI and 2.9% for Rural CPI (See Exhibit 14).

Exhibit 14: Consumer Price Indices ofZhejiang Province in 2003,Year-on-year growth rate (%)

Item Province Urban Rural

Consumer Price Index 1.9 0.5 2.9

Food 2.8 2.2 3.4

Of which: Grain 3.2 3.3 3.1

Clothing -3.3 -3.4 -3.3

Household Facilities,

Articles and Services -3.1 -4.1 -1.8

Health Cares & Personal

Articles 0.1 -1.4 1.1

Transportation and

Communication -4.9 -3.4 -4.5

Recreation, Education

and Cultural Articles 11.2 3.7 17.4

Residence 12 2.0 0.4

Source: National Bureau of Statistics, PRC.

d. Retail sector

Hangzhou is the city with the largest economy, in terms of

GDP, in Zhejiang (See Exhibit 10). It has a robust retail

market. In 2003, Hangzhou’s retail sales of consumer goods

increased by 12.4% yoy to reach 58.75 billion yuan, ranking

the first among all cities in Zhejiang. Among various types

of retail outlets, chain stores have developed most quickly

in recent years. In 2002, sales at chain stores amounted to

6.1 billion yuan, an increase of 57% over the previous year,

and accounted for some 11% of Hangzhou’s total retail

sales. In the first half of 2003, sales of chain stores grew

further by 57.7% yoy. Major chain stores in Hangzhou

include Lianhua , Hualian , Hymart ,

Metro , and Lotus etc. Hangzhou is

also a key distribution center of consumer goods in the

region.

Ningbo has the second highest GDP among all cities in

Zhejiang (See Exhibit 10), and is also the second largest

retail market in the province. Ningbo’s retail sales of

consumer goods increased by 12.7% yoy to reach 52.15

billion yuan in 2003. The retail format in Ningbo is also

changing. Apart from traditional department stores, various

forms of modern operation such as chain stores,

supermarkets and specialty stores are developing fast.

12Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

3. The “Beijing-Tianjin-Hebei” Region

The “Beijing-Tianjin-Hebei” Region spans across 2

municipalities and 1 province. It includes 2 centrally-

administered municipalities: Beijing and Tianjin; and

prefecture-level cities such as Tangshan, Baoding, Langfang

Qinhuangdao, Zhangjiakou, Shijiazhuang, Chengde,

Cangzhou, Handan, etc. of Heibei province. It has an area

of 32,600 square kilometers, about 0.34% of the total area

of the whole country. Its size of population is 27.62 million,

2.15% of the national total. The “Beijing-Tianjin-Hebei”, with

a consumer group of around 100 million people, is one of

the largest consumer markets in China. Its GDP reached

1,309.42 billion yuan and retail sales of consumer goods

amounted to 516.87 billion yuan in 2003.

(1) Beijing Municipality

The GDP of Beijing reached 361.19 billion yuan in 2003,

up by 10.5%. The GDP has been at double-digit growth in

the past five years. The per capita GDP in Beijing was

31,613 yuan (USD 3,818) in 2003, up by 9.2% yoy.

a. Retail sales

The retail sales of consumer goods in Beijing increased by

a real growth of 16.6% yoy to 191.67 billion yuan in 2003,

accounting for 4.18% of the national total and ranked the

second among the four central ly administered

municipalities. The upgrading of consumption structure has

been the major factor driving up the consumption growth.

Real estate, automobiles and telecommunications services

remained the hot spots of consumption.

b. Income level

The per capita disposable income of urban residents in

Beijing in 2003 was 13,882.6 yuan, up by a real growth of

11.2% yoy. The Engel Coefficient of urban residents was

31.7%, down by 2.1 percentage points from the previous

year.

The per capita net income of rural households in Beijing in

2003 was 6,496.3 yuan, up by a real growth of 11.5% yoy.

The Engel Coefficient of rural residents was 31.7%, down

by 1.3 percentage point from the previous year.

c. Price level

The Consumer Price Index in Beijing in 2003 was mainly

driven up by the price of “Food” which was up by 3.2% yoy.

The Consumer Price Indices of “Health Cares & Personal

Articles” and “Residence” also increased, whereas the

Consumer Price Indices of “Clothing”, “Household Facilities,

A r t i c l es and Se rv i ces ” , “Transpo r ta t i on and

Communication”, and “Recreation, Education and Cultural

Articles” decreased (See Exhibit 15).

Exhibit 15: Consumer Price Indices ofBeijing in 2003

Year-on-year

Item growth rate (%)

Consumer Price Index 0.2

Food 3.2

Clothing -2.9

Household Facilities, Articles and

Services -2.3

Health Cares & Personal Articles 0.1

Transportation and Communication -2.2

Recreation, Education and Cultural

Articles -1.7

Residence 1.6

Source: National Bureau of Statistics, PRC.

d. Retail sector

Thanks to the huge size and potential of the consumer

market in Beijing, new department stores and shopping

centers developed rapidly in the past few years. There

are three well-known traditional shopping districts in

Beijing, namely Wangfujing ( ), Xidan ( ) and

Qianmen ( ). Many department stores such as Xidan

Shopp ing A rcade ( ) , Wang fu j i ng

Department Store ( ), Longfu Building (

), New Dong An Market ( ) and the

Friendship Store ( ) etc. have strong customer

f lows. In addi t ion, other reta i l out lets such as

supermarkets, convenient stores have also been growing

rapidly.

13Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Beijing was one of the first 11 pilot cities chosen by the

State Council to form Sino-foreign joint retail enterprises

with import-export rights. The first batch of Sino-foreign

joint retail enterprises formed in Beijing included the Beijing

Lufthansa Shopping Center ( ) and the

Scitech Plaza ( ). By end-2002, there were

already 15 Sino-foreign joint retail enterprises in Beijing.

In addition, a group of Sino-foreign chain stores such as

Carrefour, Makro and Ito Yokado have emerged in the

market in recent years. The growth of Sino-foreign joint

retail enterprises has also stimulated the development of

some local chain stores and supermarkets such as

Hualian, Wumei and Guomei.

(2) Tianjin Municipality

a. Retail sales

The retail sales of consumer goods in Tianjin reached

107.41 billion yuan in 2003, up by 14.1% yoy. Of which, the

retail sales of Wholesale and Retail Trade Sector reached

72.71 billion yuan, up by 12.5% yoy; and the retail sales of

Catering Service reached 10.991 billion yuan, up by 7.2%

yoy.

b. Income level

In 2003, the per capita disposable income of urban residents

in Tianjin was 10,312.91 yuan, up by 10.45% yoy. The Engel

Coefficient of urban residents was 38%, down by 2

percentage points from the previous year. The per capita

net income of rural households in Tianjin was 4,566.01 yuan,

up by a real growth of 6.71% yoy. The Engel Coefficient of

rural residents was 38%, which was the same as the

previous year.

c. Price level

Urban CPI of Tianjin increased by 1.0% yoy in 2003. The

growth was mainly driven by “Food” (which went up by 3.3%

yoy). The Urban CPI of “Clothing”, “Household Facilities,

Art icles and Services” and “Transportat ion and

Communication” went down by 11.9% yoy, 3.5% yoy, and

3.0% yoy respectively.

d. Retail sector

There has been fierce competition between foreign and local

retail enterprises in the retail sector in Tianjin. Famous

market players include Walmart ( ), Wankelong (

), Carrefour ( ), Daiei ( ), Family World

( ) and Quanye ( ).

(3) Hebei Province

a. Retail sales

The total retail sales of consumer goods in Hebei rose by

10.64% yoy to reach 217.79 billion yuan in 2003, ranking

the ninth among all provinces, municipalities and

autonomous regions in China (See Exhibit 16).

Exhibit 16: To t a l R e t a i l S a l e s o fConsumer goods in HebeiProvince in 2003

2003

(billion yuan)

Total retail sales of consumer goods 217.79

By Location of Retailers:

Urban 106.44

County 42.11

Under County Level 69.24

By Sectors:

Wholesale and Retail Trade 155.85

Catering Services 23.35

Manufacturing 16.99

Others 21.59

Source: National Bureau of Statistics, PRC.

b. Price level

The Consumer Price Index in Hebei in 2003 increased by

2.2% yoy in 2003 which was mainly driven by the price of

“Food” (up by 4.5% yoy). The Consumer Price Indices of

“Food”, “Health Cares & Personal Articles” and “Recreation,

Education and Cultural Articles”, “Residence” and “Services”

also increased, whereas the Consumer Price Indices of

“Clothing”, “Household Facilities, Articles and Services”, and

“Transportation and Communication”, decreased (See

Exhibit 17).

14Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Exhibit 17: Consumer Price Indices ofHebei Province in 2003 (yoygrowth rate %)

Item Province Urban Rural

Consumer Price Index 2.2 2.3 2.0

Food 4.5 4.8 4.1

Clothing -2.2 -2.9 -1.5

Household Facilities,

Articles and Services -3.0 -3.5 -2.1

Health Cares & Personal

Articles 6.0 2.9 8.7

Transportation and

Communication -1.9 -2.3 -1.5

Recreation, Education

and Cultural Articles 0.7 2.4 -0.8

Residence 4.5 7.2 2.6

Services 4.8 5.2 4.5

Source: National Bureau of Statistics, PRC.

c. Retail sector

Retail centres of the province are mainly located in

Shijiazhuang, Tangshan, Handan and Baoding. The

combined retail sales of these four cities amounted to 131.48

billion yuan in 2003, which accounted for 60.37% of the

provincial total (See Exhibit 18). Major department stores

and shopping centers in Hebei include Shijiazhuang Beiguo

Commercial City ( ), Shijiazhuang Renmin

Department Store ( ), Shijiazhuang

Dongfeng City Plaza ( ), Shijiazhuang

Ximei Department Store ( ), Tangshan

Department Store ( ), Qinhuangdao Hualian

Commercial Ci ty ( ) and Baoding

Department Store ( ), etc..

Exhibit 18 : Major Economic Indicators of Hebei, 2003 (yoy growth rate %)

Total Retail Sales of Per Capita Urban Per Capita Rural

GDP Consumer Goods Disposable Income Net Income

Region (billion yuan) (billion yuan) (yuan) (yuan)

Tangshan 1,295 (13.2%) 30.738 (10.8%) 8,068 (8.1%) 3,790 (4.5%)

Baoding 92.86 (12.6%) 31.62 (11.7%) 7,139 (7.1%) 2,921 (4.1%)

Langfang 52.85 (12.1%) 12.06 (11.7%) 8,404 (8.2%) 4,000 (4.0%)

Qinhuangdao 38.703(12.1%) 11.773 (11.2%) 7,870 (9.4%) 2,891 (5.4%)

Zhangjiakou 8.25 (10.3%) 2.835 (8.9%) 6,430 (6.8%) 1,863 (1.4%)

Shijiazhuang 137.79 (12.5%) 45.66 (11.0%) 7,741 (6.9%) 3,394 (4.6%)

Chengde 23.552 (12.1%) 9.17 (6.0%) 6,306.96 (9.1%) 1,696 (8.6%)

Cangzhou 62.886 (12.1%) 16.537 (9.8%) 6,728 (9.3%) 2,691 (5.6%)

Handan 76.26 (12.1%) 23.46 (11.3%) 6,842 910.1%) 2,900 (5.1%)

Source: National Bureau of Statistics, PRC.

15Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

II. General Background on China’s Consumer Market

1. The Two-tier Market: Urban and Rural

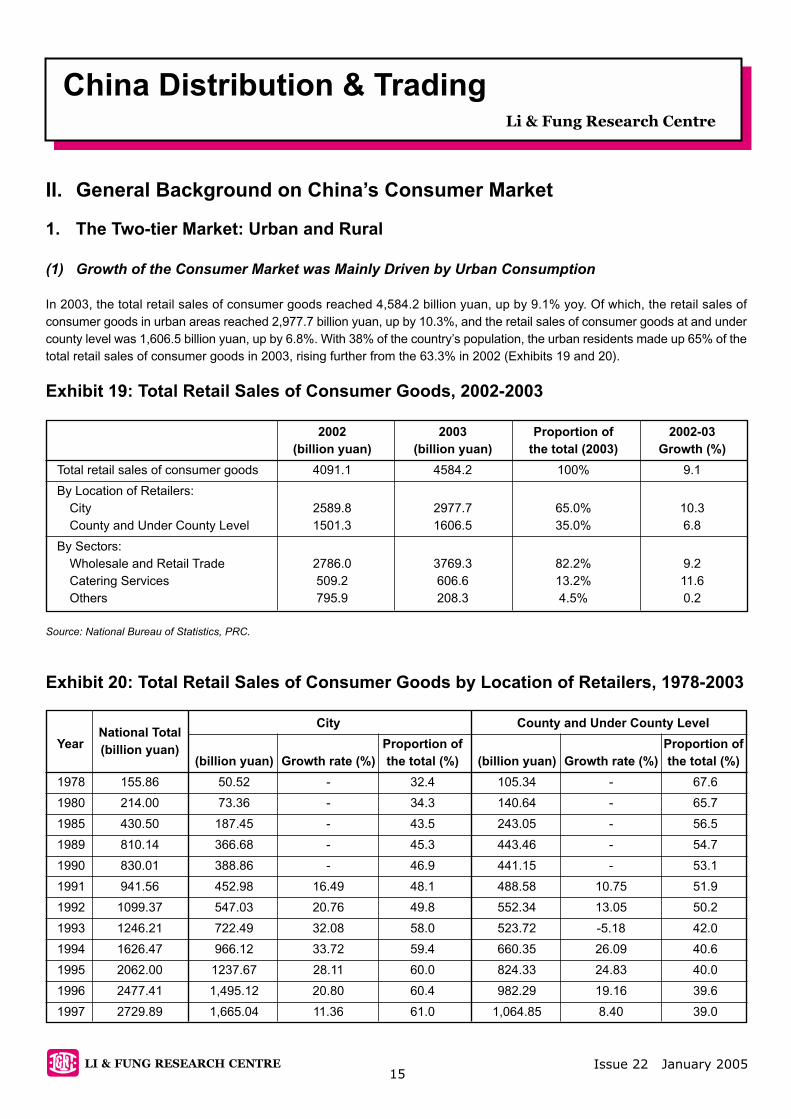

(1) Growth of the Consumer Market was Mainly Driven by Urban Consumption

In 2003, the total retail sales of consumer goods reached 4,584.2 billion yuan, up by 9.1% yoy. Of which, the retail sales of

consumer goods in urban areas reached 2,977.7 billion yuan, up by 10.3%, and the retail sales of consumer goods at and under

county level was 1,606.5 billion yuan, up by 6.8%. With 38% of the country’s population, the urban residents made up 65% of the

total retail sales of consumer goods in 2003, rising further from the 63.3% in 2002 (Exhibits 19 and 20).

Exhibit 19: Total Retail Sales of Consumer Goods, 2002-2003

2002 2003 Proportion of 2002-03

(billion yuan) (billion yuan) the total (2003) Growth (%)

Total retail sales of consumer goods 4091.1 4584.2 100% 9.1

By Location of Retailers:

City 2589.8 2977.7 65.0% 10.3

County and Under County Level 1501.3 1606.5 35.0% 6.8

By Sectors:

Wholesale and Retail Trade 2786.0 3769.3 82.2% 9.2

Catering Services 509.2 606.6 13.2% 11.6

Others 795.9 208.3 4.5% 0.2

Source: National Bureau of Statistics, PRC.

Exhibit 20: Total Retail Sales of Consumer Goods by Location of Retailers, 1978-2003

National TotalCity County and Under County Level

Year Proportion of Proportion of(billion yuan)

(billion yuan) Growth rate (%) the total (%) (billion yuan) Growth rate (%) the total (%)

1978 155.86 50.52 - 32.4 105.34 - 67.6

1980 214.00 73.36 - 34.3 140.64 - 65.7

1985 430.50 187.45 - 43.5 243.05 - 56.5

1989 810.14 366.68 - 45.3 443.46 - 54.7

1990 830.01 388.86 - 46.9 441.15 - 53.1

1991 941.56 452.98 16.49 48.1 488.58 10.75 51.9

1992 1099.37 547.03 20.76 49.8 552.34 13.05 50.2

1993 1246.21 722.49 32.08 58.0 523.72 -5.18 42.0

1994 1626.47 966.12 33.72 59.4 660.35 26.09 40.6

1995 2062.00 1237.67 28.11 60.0 824.33 24.83 40.0

1996 2477.41 1,495.12 20.80 60.4 982.29 19.16 39.6

1997 2729.89 1,665.04 11.36 61.0 1,064.85 8.40 39.0

16Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

National TotalCity County and Under County Level

Year Proportion of Proportion of(billion yuan)

(billion yuan) Growth rate (%) the total (%) (billion yuan) Growth rate (%) the total (%)

1998 2,915.25 1,782.52 7.06 61.1 1,132.73 6.37 38.9

1999 3,113.47 1,909.16 7.10 61.3 1,204.31 6.32 38.7

2000 3,415.26 2,111.03 10.57 61.8 1,304.23 8.30 38.2

2001 3,759.52 2,354.34 11.53 62.6 1,405.18 7.74 37.4

2002 4,091.05 2,589.76 10.00 63.3 1,501.29 6.84 36.7

2003 4,584.20 2,977.70 14.98 65.0 1,606.50 7.01 35.0

Source: National Bureau of Statistics, PRC.

Looking at the total retail sales of consumer goods by

location of retailers, since the growth rate of the retail sales

of consumer goods was higher in urban areas, the

proportion of urban retail sales of consumer goods to the

national total had been increasing. This results in the growth

of the consumer market mainly driven by urban consumption

(See Exhibit 20). This trend is expected to continue between

urban and rural areas.

(2) Income Disparity between Urban and Rural

Areas

Since the 1978 reform, both urban and different rural

incomes have witnessed impressive growth. Due to different

degrees of economic development between urban and rural

areas, however, income growth in the rural areas has been

lagging behind that in the urban areas (See Exhibit 21).

The result is a widening income gap between urban

households and rural households, as shown by the rising

“urban-to-rural” income ratio from 2.50 in 1980 to 3.23 in

2003 (See Exhibit 22). For example, in 2003, the per capita

annual disposable income of urban residents in Guangdong

was 12,380.43 yuan which was about three times the per

capita net income of rural households in Guangdong

(4,054.58) (See Exhibit 23).

Exhibit 21: Income Growth Rate ofUrban and Rural Residents,1990 - 2003

14 1311

3

19 18

36

29

23 22

13

95

8 7 912

610

0

5

10

15

20

25

30

35

40

grow

thra

te(%

)

year

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

growth rate of urban disposable income growth rate of rural net income

10

32

73 2 2

5 5

27

Source: National Bureau of Statistics, PRC.

Exhibit 22: Ratio of Per Capita Annual Disposable Income between Urban and RuralHouseholds, 1978 - 2003

2.57 2.5

1.84 1.86

2.282.2

2.42.58

2.8 2.862.71

2.51 2.47 2.512.65

2.792.9

3.113.23

3.5

3

2.5

2

1.5

1

0.5

01978 1980 1984 1985 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

urba

n-to

-rur

alra

tio

Source: National Bureau of Statistics, PRC.

17Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Exhibit 23: Annual Income and Engel Coefficient in Urban and Rural Areas by Region,2003

Urban Per Capita Rural Per

Annual Disposable Engel Capita Net Engel

Rank Region Income (yuan) Coefficient Rank Region Income (yuan) Coefficient

1 Shanghai 14,867.49 0.37 1 Shanghai 6,653.92 0.35

2 Beijing 13,882.62 0.32 2 Beijing 5,601.55 0.32

3 Zhejiang 13,179.53 0.37 3 Zhejiang 5,389.04 0.38

4 Guangdong 12,380.43 0.37 4 Tianjin 4,566.01 0.38

5 Tianjin 10,312.91 0.38 5 Jiangsu 4,239.26 0.41

6 Fujian 9,999.54 0.29 6 Guangdong 4,054.58 0.48

7 Jiangsu 9,262.46 0.38 7 Fujian 3,733.89 0.45

8 Tibet 8,765.45 4.42 8 Shangdong 3,150.49 0.42

9 Shandong 8,399.91 0.34 9 Liaoning 2,934.44 0.43

10 Chongqing 8,093.67 0.38 10 Hebei 2,853.38 0.40

11 Guangxi 7,785.04 0.40 11 Hainan 2,588.06 0.58

12 Hunan 7,674.20 0.36 12 Hubei 2,566.76 0.52

13 Yunnan 7,643.57 0.42 13 Hunan 2,532.87 0.52

14 Hubei 7,321.98 0.38 14 Jilin 2,530.41 0.44

15 Hainan 7,259.25 0.45 15 Heilongjiang 2,508.94 0.41

16 Liaoning 7,240.58 0.39 16 Jiangxi 2,457.53 0.52

17 Hebei 7,239.06 0.35 17 Shanxi 2,299.17 0.43

18 Xinjiang 7,173.54 0.36 18 Inner Mongolia 2,267.65 0.41

19 Sichuan 7,041.87 0.39 19 Henan 2,235.68 0.48

20 Inner Mongolia 7,012.90 0.31 20 Sichuan 2,229.86 0.54

21 Jilin 7,005.17 0.36 21 Chongqing 2,214.55 0.53

22 Shanxi 7,005.03 0.34 22 Anhui 2,127.48 0.46

23 Henan 6,926.12 0.34 23 Xinjiang 2,106.19 0.46

24 Jiangxi 6,901.42 0.40 24 Guangxi 2,094.51 0.51

25 Shaanxi 6,806.35 0.35 25 Ningxia 2,043.30 0.42

26 Anhui 6,778.03 0.44 26 Qinghai 1,794.13 0.50

27 Qinghai 6,745.32 0.37 27 Yunnan 1,697.12 0.53

28 Heilongjiang 6,678.90 0.36 28 Tibet 1,690.76 0.65

29 Gansu 6,657.24 0.36 29 Shaanxi 1,675.66 0.39

30 Guizhou 6,569.23 0.40 30 Gansu 1,673.05 0.44

31 Ningxia 6,530.48 0.36 31 Guizhou 1,564.66 0.57

Source: National Bureau of Statistics, PRC.

18Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

2. Regional Disparity in Wealth andConsumption

The widening income gap among different regions in China

is another major factor that explains the unbalanced

consumption levels in the country. Looking at the annual

income of urban and rural households by region on Exhibit

22, the 7 richest provincial-level administrative regions are

all located in the eastern, coastal areas. The lower ranking

regions tend to be those central and western regions. For

example, in 2003, the urban per capita disposable income

in Shanghai was 14,867.5 yuan, 2.28-times that in Ningxia

(6,530.5 yuan) (See Exhibit 23).

In fact, the eastern region, central region and western region

accounted for 60.57%, 26.33% and 16.9% respectively of

the total retail sales of consumer goods in 2003. The retail

sales of consumer goods were largely concentrated in the

six most prosperous cities/provinces, namely, Shanghai,

Beijing, Jiangsu, Guangdong, Shangdong and Zhejiang,

each with retail sales of consumer goods over 200 billion

yuan, altogether contributing more than 5 percentage points

to the growth rate of total retail sales of consumer goods in

2003. For example, Guangdong alone accounted for 12.2%

of the total retail sales of consumer goods, similar in size to

that of the whole western China (See Exhibit 24).

The combined retail sales of consumer goods of the first

10 rankings in 2003 accounted for 65.2% of the national

total, 0.3 percentage point higher than that in 2002. The

combined retail sales of consumer goods of the last 10

rankings in 2003 accounted for 8.87% of the national total,

0.43 percentage point lower than that in 2002. The growth

rate of the retail sales of consumer goods of the first 10

rankings and that of the last 10 rankings were 11.5% and

6.68% respectively. This implies that there is still an

enormous gap in terms of the size of the consumer market

in different regions of China. (For the rankings of the retail

sales of consumer goods and the growth rates by region,

see Exhibit 25)

Exhibit 24: Retail Sales of Consumer Goods by Region, 2003

Total Retail Per Capita

Sales of Retail Sales

Consumer Goods of Consumer Under Provincial

Region (billion yuan) Goods (yuan) City County County Level Growth (%)

National 4,584.2 3,547.40 2,977.73 524.78 1,081.69 9.1

Eastern Region

Beijing 191.67 1316.41 153.58 8.88 29.22 14.5

Tianjin 92.23 912.27 85.92 3.53 2.78 10.9

Hebei 217.79 321.75 106.44 42.11 69.24 10.6

Liaoning 233.08 553.66 196.37 11.2 25.52 12.3

Shanghai 222.06 1,297.84 190.59 1.76 29.71 9.1

Jiangsu 356.65 481.57 251.63 21.78 83.23 13.7

Zhejiang 315.71 674.59 199.99 32.95 82.77 10.9

Fujian 174.04 498.97 105.75 21.83 46.46 13.1

Shangdong 393.65 431.40 252.56 39.64 101.45 22.2

Guangdong 560.60 704.80 371.83 26.94 161.83 11.8

Hainan 19.16 236.25 12.81 1.66 4.69 10.9

19Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Total Retail Per Capita

Sales of Retail Sales

Consumer Goods of Consumer Under Provincial

Region (billion yuan) Goods (yuan) City County County Level Growth (%)

Central Region

Shanxi 72.93 220.07 47.13 13.52 12.28 13.7

Jilin 111.03 410.61 85.77 7.68 17.58 10.1

Heilongjiang 137.65 360.81 101.94 18.66 17.04 10.1

Anhui 133.12 207.68 66.66 28.56 37.9 9.8

Jiangxi 92.32 217.02 45.53 20.66 26.13 11.7

Henan 242.64 251.00 123.48 49.42 69.74 10.8

Hubei 235.87 392.99 160.33 22.29 53.25 10.8

Hunan 181.63 272.59 99.71 33.25 48.67 10.8

Western Region

Inner Mongolia 72.68 305.38 44.95 16.65 11.08 21.3

Chongqing 83.55 266.93 48.23 11.27 24.05 9.5

Sichuan 209.11 240.36 100.42 35.73 72.96 13

Guizhou 45.88 118.55 27.2 8.58 10.1 10.2

Yunnan 78.25 178.82 42.53 18.05 17.67 10

Tibet 5.83 215.93 2.61 0.25 0.72 9.2

Shaanxi 85.32 231.22 56.56 14.91 13.85 17.2

Gansu 47.46 182.33 30.8 7.62 9.04 9.5

Qinghai 10.27 192.32 6.61 2.47 1.18 11.5

Ningxia 12.08 208.28 8.15 2.08 1.85 15.1

Xinjiang 42.12 217.79 31.13 4.92 6.06 11.1

Guangxi 85.77 176.59 45.85 16.97 22.95 12.2

Source: National Bureau of Statistics, PRC.

Exhibit 25: Rankings of the Retail Sales of Consumer Goods and Growth by Region,2001 – 2003

Rank (Growth) Rank (Retail Sales)

Region 2003 2002 2001 2003 2002 2001

Beijing 5 22 11 11 11 11

Tianjin 16 1 2 18 17 18

Hebei 22 14 14 9 9 9

Shanxi 6 8 30 23 23 21

Inner Mongolia 2 2 7 24 24 24

Liaoning 10 10 16 7 7 5

Jilin 24 12 4 16 16 17

Heilongjiang 25 16 19 14 14 14

Shanghai 31 24 31 8 8 8

20Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Rank (Growth) Rank (Retail Sales)

Region 2003 2002 2001 2003 2002 2001

Jiangsu 7 5 15 3 3 2

Zhejiang 17 3 6 4 4 4

Anhui 27 31 28 15 15 15

Fujian 8 13 22 13 13 13

Jiangxi 13 25 29 17 18 19

Shangdong 1 4 5 2 2 3

Henan 19 15 9 5 5 6

Hubei 20 7 12 6 6 7

Hunan 21 9 10 12 12 12

Guangdong 12 11 8 1 1 1

Gansu 11 20 24 19 19 16

Hainan 18 27 26 28 28 28

Chongqing 28 26 25 21 20 20

Sichuan 9 17 13 10 10 10

Guizhou 23 18 18 26 26 27

Yunnan 26 29 3 22 22 23

Tibet 30 30 1 31 31 31

Shaanxi 3 23 21 20 21 22

Gansu 29 21 23 25 25 26

Qinghai 14 6 17 30 30 30

Ningxia 4 19 20 29 29 29

Xinjiang 15 28 27 27 27 25

Source: National Bureau of Statistics, PRC.

3. The Upgrading ofConsumption Structure

Accompanying the income growth is the upgrading of

consumption structures of both urban households and rural

households – the Engel Coefficient, a measure of the

proportion of food expenditure to the total living expenditure,

has dropped remarkably over the past two decades (See

Exhibits 26 and 27).

(1) The Urban Households

Consumption of traditional items such as “Food”, “Clothing”,

and “Household Facilities, Articles and Service” went down

from 76% of total consumption expenditure in 1985 to a

53.21% in 2003. The consumption of other items went up

considerably for urban households. The percentage share

of consumption of “Medicine and Medical Service”, and

“Transport, Post and Communication Services” in 2003 was

almost four times that in 1985. The consumption of

“Education, Cultural and Recreation Services” and

“Residence” in 2003 almost doubled that in 1985. “Clothing”

had long been the second largest item of expenditure of

urban residents after “Food”. However, in 2000, “Education,

Cultural and Recreation Services” had already surpassed

“Clothing” and became the second largest item of

expenditure (See Exhibit 26).

(2) The Rural Households

The importance of “Food”, “Clothing” and “Home Equipment

Articles for Use and Services” decreased lightly although

together they sti l l accounted for 55.46% in total

consumption, and the single “Food” item still took up 46%

of total consumption in 2003. In addition, the share of

“Medicine and Medical Service”, “Transport, Post and

Communication Services” and “Education, Cultural and

Recreation Services” has been growing considerably (See

Exhibit 27).

21Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Exhibit 26: Consumption Structure of Urban Households, 1985 - 2003

Per Capita Annual Living Composition of Per Capita Annual

Expenditures for Consumption (yuan) Living Expenditure for Consumption (%)

Items of Consumption 1985 1990 1995 2000 2003 1985 1990 1995 2000 2003

Per Capita Living

Expenditure 673.20 1278.89 3537.57 4998.00 6510.94 100 100 100 100 100

Food 351.72 693.77 1766.02 1958.31 2416.92 52.25 54.25 50.09 39.44 37.12

Clothing 98.04 170.90 479.2 500.46 637.72 14.56 13.36 13.55 10.01 9.79

Household Facilities,

Articles and Service 57.87 108.45 296.94 439.29 410.34 8.60 10.14 7.44 7.49 6.3

Medicine and

Medical Service 16.71 25.67 110.11 318.07 475.98 2.48 2.01 3.11 6.36 7.31

Transport, Post and

Communication Services 14.39 40.51 171.01 395.01 721.12 2.14 1.20 5.18 8.54 11.08

Education, Cultural and

Recreation Services 55.01 112.26 312.71 627.82 934.38 8.17 11.12 9.36 13.40 14.35

Residence 32.23 60.86 250.18 500.49 699.38 4.79 6.98 8.02 11.31 10.74

Miscellaneous Commodities

and Services 47.23 66.57 151.39 258.54 215.10 7.01 0.94 3.25 3.44 3.30

Source: National Bureau of Statistics, PRC.

Exhibit 27: Consumption Structure of Rural Households, 1985 - 2003

Annual Per Capita Composition of

Consumption Expenditures (yuan) Consumption Expenditure (%)

Items of Consumption 1985 1990 1995 2000 2003 1985 1990 1995 2000 2003

Per Capita Living

Expenditure 317.42 584.63 1310.36 1670.13 1943.3 100 100 100 100 100

Food 183.43 343.76 768.19 820.52 885.95 57.79 58.8 58.62 49.13 45.59

Clothing 30.86 45.44 89.79 95.95 110.09 9.72 7.77 6.85 5.75 5.67

Home Equipment Articles

for Use and Services 16.25 30.9 68.48 75.45 81.62 5.12 5.29 5.23 4.52 4.2

Medical Treatment and

Health Care 7.65 19.02 42.48 87.57 115.82 2.41 3.25 3.24 5.24 5.96

Transport and

Communication 5.48 8.42 33.76 93.13 162.46 1.72 1.44 2.58 5.58 8.36

Recreation, Education

and Cultural Services 12.45 31.38 102.39 186.72 235.72 3.92 5.37 7.81 11.18 12.13

Housing 57.9 101.37 182.21 258.34 308.4 18.24 17.34 13.91 15.47 15.87

Miscellaneous Commodities

and Services 3.4 4.34 23.06 52.46 42.95 1.07 0.74 1.76 3.14 2.21

Source: National Bureau of Statistics, PRC.

22Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

(3) Consumption structures of differentincome groups

Exhibits 28 and 29 display the composition of living

expenditures of urban households and rural households in

different income groups. It is found that urban households,

in general, spend proportionately less on food than rural

households. Households with higher income levels in both

urban areas and rural areas also tend to spend

proportionately less on food. On the other hand, urban

households in general, as well as the higher income groups,

spend more on items such as “Clothing”, “Transport and

Communications“, “Education, Cultural and Recreation

Services”, etc.

Exhibit 28: Composition of Living Expenditure of Urban Households by Income Groups,2003 (%)

Lower Upper

Low Middle Middle Middle High Highest

Lowest Income Income Income Income Income Income

Income Poor Households Households Households Households Households Households

Households Households (second (second (third (fourth (ninth (tenth

Item Average (first decile) (first 5%) decile) quintile) quintile) quintile) decile) decile)

Total Living

Expenditures

(%) 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00

Food 37.12 47.72 48.59 44.93 42.26 39.23 36.61 34.67 29.85

Clothing 9.79 7.75 7.02 9.27 10.01 10.56 10.49 9.82 8.79

Household

Facilities,

Articles and

Services 6.30 3.59 3.43 4.4 5.01 5.87 6.26 7.14 8.08

Medicine and

Medical

Services 7.31 6.86 6.48 6.67 7.13 7.10 7.43 7.87 7.37

Transport,

Post and

Communication

Services 11.08 6.80 6.15 8.47 9.39 10.23 10.95 11.49 14.34

Education –

Cultural and

Recreation

Services 14.35 12.79 13.10 12.81 13.29 13.88 14.61 15.40 15.22

Residence 10.74 12.06 12.83 10.93 10.08 10.07 10.33 10.03 12.36

Miscellaneous

Commodities

and Services 3.30 2.43 2.40 2.52 2.83 3.07 3.32 3.59 3.99

Source: National Bureau of Statistics, PRC.

23Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

Exhibit 29: Composition of Living Expenditure of Rural Households by Income Groups,2003 (%)

Lower Lower Middle Middle Upper Middle High

Income Income Income Income Income

Item Households Households Households Households Households

Living Expenditure 100.00 100.00 100.00 100.00 100.00

Food 54.06 51.84 48.53 45.64 38.05

Clothing 5.59 5.64 5.64 5.74 5.70

Residence 13.30 13.13 13.90 15.50 19.34

Household Facilities, Articles and

Services 3.70 3.74 3.83 4.14 4.84

Medicines and Medical Services 5.99 5.93 6.02 5.70 6.08

Transport, Post and

Telecommunications 5.34 6.10 7.44 8.37 10.99

Cultural, Educational and Recreational

Articles and Services 10.33 11.71 12.60 12.64 12.39

Other Commodities and Services 1.69 1.90 2.05 2.26 2.60

Source: National Bureau of Statistics, PRC.

4 . F r a g m e n t e d M a r k e t : L o c a lProtectionism

(1) Background

A very successful retail strategy in one region may not be

able to apply in other regions – an obstacle for retailers to

enter the fragmented market in China. One key reason for

this is local protectionism, which refers to the illicit and

irregular use of administrative controls by local governments

to interfere the inward trade of goods and services from

other parts of the country.

With the introduction of fiscal decentralization since the

economic reform in 1978, the central government has

allowed more management decisions to be made at lower

levels. This decentralization process has given cities and

counties authorities significant decision-making power, and

many state-owned enterprises have been mandated to local

governments.

Since the local governments are obsessed with local

economic growth and local GDP growth rate has become

the leading criteria for evaluating the performance of the

officials, local governments have been making full use of

their administrative rights to assist and protect local

enterprises. They rely on the businesses in their jurisdictions

for tax revenue and also care about local employment, which

is important for maintaining social stability. Local

governments thus often take administrative controls to

protect local businesses from competition from other parts

of China.

In general, local protectionism is caused by the following

reasons: a) protection of local industries and enterprises

by local government; b) the necessity for local government

to maintain the quality and security of products within its

territory; c) the maximization of local fiscal revenue due to

rising local fiscal expenditure; d) the necessity for local

government officials to show their performance; e) the close

relationship between the local government officials and the

local enterprises.

24Issue 22 January 2005

China Distribution & TradingLi & Fung Research Centre

(2) Government Policies in Regulating Local

Protectionism

The central government is taking a series of measures to

tackle the problem of local protectionism. It aims to break

through regional blockage that is obstructing the formation

of a nationally unified market.

Working teams formed jointly by the Ministry of Commerce,

the Ministry of Finance, the Ministry of Supervision, and

four other departments, are urging the local governments

to remove protective regulations. For example, on 12 and

15 September 2003, nine provinces around the Pearl River

Delta, namely, Fujian, Jiangxi, Hunan, Guangdong,

Guangxi, Hainan, Sichuan, Guizhou and Yunnan, signed

an agreement to remove protective regulations in the region.

© Copyright 2005 Li & Fung Research Centre. All rights reserved.

Though Li & Fung Research Centre endeavours to ensure the information discussed in this material is accurate and updated, no legal liability can be

attached as to the contents hereof. Reproduction or redistribution of this material without Li & Fung Research Centre’s prior written consent is prohibited.