chile japan business committee

TRANSCRIPT

CHILE‐JAPAN BUSINESS COMMITTEECHILE JAPAN BUSINESS COMMITTEECHILEAN COPPER MINING AND CODELCO CHALLENGES

Nelson Pizarro C

December 2nd, 2014

Nelson Pizarro C.CEO

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Chile: An attractive mining districtYear 2013

SHARE IN GLOBAL PRODUCTION SHARE IN GLOBAL RESERVES

32%Chile

28%Chile

Global Ranking: 1

Copper32%

68%Others

28%

72%Others

Molybdenum15%

85%

Chile

Others

21%

79%

Chile

OthersGlobal Ranking: 3

85% 79%

Natural Nitrates100%

Chile

100%

Chile

Global Ranking: 1

Lithium Carbonate39%

61%

Chile

Others

Chile

OthersGlobal Ranking: 158%

42%

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Source: Cochilco, Codelco, USGS.

58%

Codelco has a great future

CODELCO: WORLD LEADER IN COPPER RESERVES

Leadership in copper reserves Estimated mineral resources

Our mineral resources let us expect more than 70 years of exploitationCodelco

9%

Others

Others29%

Our mineral resources let us expect more than 70 years of exploitation

Mineral(million tonnes)

Copper grade

(%)

Copper content(million tonnes)

Share(%)

Chuquicamata 2,147 0.70 15.1 11.6Chile19%

AustraliaPeruRussia

4%

China4%

q

Radomiro Tomic 3,671 0.46 16.8 12.9

MH 936 0.95 8.9 6.8

Salvador 1,678 0.46 7.7 5.9

Andina 6,017 0.75 45.1 34.7Australia

13%Peru10%USA

6%Mexico

6%

4%

Source: U.S. Geological Survey, January 2014.

El Teniente 4,195 0.83 34.8 26.7

Gabriela Mistral 491 0.36 1.8 1.4

Codelco 19,136 0.68 130.2 100.0

*: Mineral resources include mineral stocks and broken material.

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Although, copper prices has shown a downward trend since 2011 …

475

500

900

1.000

Copper Pricec/lb

Stocks in Metal Exchanges ** ‘000 tonnes

425

450

700

800

350

375

400

400

500

600

C P i

275

300

325

100

200

300

Stocks in Metal

Copper Price

250

275

0

100

ene 2011 jul 2011 ene 2012 jul 2012 ene 2013 jul 2013 ene 2014 jul 2014

Stocks in Metal Exchanges

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

*: Year 2014: copper price and stocks until November 19th. **: LME, COMEX and SHFE.

Price prospects remain auspicious in the long‐termLong‐term copper price forecasts, c/lb, 2015 currency

400

FORECASTS EVOLUTION: BANKS AND ANALYSTS LATEST PROJECTIONS

334355

CRUWood Mackenzie

250

300

350

318320328339345345334

CIMB GroupBarclays Capital

BoA Merrill LynchIHS Economics

J.P. MorganAnalysts average

CRU

150

200

250

299299304304305317

UBSMacquarie

Credit SuisseGoldman Sachs

Commonwealth BankMorgan Stanley

p

1002002 2006 2009 2011 2013CRU Wood Mackenzie (Brook Hunt)Structural Fiscal Budget BarclaysMacquarie

301253269269279281285

B k & OthNumis

Wilson HTMInvestec

RBC Capital MarketsDeutsche Bank

Citigroup

q

305305301

0 100 200 300 400

Average without extremesAnalysts, Banks & Others average

Banks & Others average

Correlation between spot and long term forecast: 0.67

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Note: Structural Budget price is the average in the next ten years after the year of forecast.

Despite the trend towards more discipline in capital use and delays in projects, important investments are projected in the coming years

US$ billi 2014

Total Latin America: US$ 165 billion Total Rest of the World: US$ 127 billion

EXPECTED INVESTMENT IN COPPER PROJECTS* WITH STARTUP DURING THE PERIOD 2014‐2023

21

60

70

WORLD TOTAL: US$ 292 billion

US$ billion, 2014 currency

65

49

29 30

40

50

272

44

2024 16

7 6 11

15

10

20

30

22

1412 12 11 11

8 8 7 7

13

27

26 5 6 8 8

1 31214 7 6

11 11 6 6 11

-

PossibleMore probable

7 7

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

PossibleMore probable

Sources: Codelco and Wood Mackenzie (September 2014).*: Includes CAPEX of projects under construction, highly probable, probable and possible.

Major copper projects in Chile* with startup between 2014 and 2023(without Codelco)

Name Owner Status Startup year Production‘000 tonnes

Investment**US$ million

Caserones Pan Pacific Copper On commissioning 2014 174 4,080

Sierra Gorda KGHM On commissioning 2014 190 4,240

Antucoya Antofagasta Under construction 2015 76 1,900

Escondida OGP1 (Organic Growth Project 1)

BHP Billiton/ Rio Tinto Under construction 2015 107 4,199

REVISAR(Organic Growth Project 1) Rio Tinto

Encuentro Oxides Antofagasta On feasibility 2016 45 760

Los Pelambres Expansion Antofagasta On prefeasibility 2020 95 7,000

Lomas Bayas Sulphides Glencore On prefeasibility 2020 97 1,600

El Morro Goldcorp On prefeasibility 2021 127 3,900***

Quebrada Blanca Hypogene Teck Resources On feasibility 2021 205 5,590

Santo Domingo Sur Iris Capstone Mining On feasibility 2021 87 1,700

El Abra Mill Freeport On feasibility 2022 198 5,000

Relincho Teck Resources On feasibility 2022 174 4,500

Collahuasi Phase 3 Anglo American/ Glencore On prefeasibility 2023 294 6,500

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Sources: Codelco, SNL and Wood Mackenzie (3rd quarter 2014), companies’ reports and press releases.*: The list includes highly probable and probable projects. Average production of copper content in the first 10 years operating at capacity. **: CAPEX according to companies’ reports orother sources. ***: Currently under revision, as the company withdrew its EIA's in November 7, 2014.

Codelco’s target: around 2.5 million tonnes of annual copper production by 2025

MINING STRUCTURAL PROJECTS

2019 202320192018‐20192014 2019 2019

Feasibility completed and early worksUnder construction On feasibilityOn commissioning On prefeasibility

El Teniente New Mine Level432,000 tpy

AndinaExpansion343,000 tpy

ChuquicamataUnderground367,000 tpy

Radomiro Tomic Sulphides Phase II354,000 tpy

Ministro Hales176,000 tpy

Salvador Inca Open Pit196,000 tpy

AndinaTransfer161,000 tpy

Note: Projects production corresponds to the average of the first 10 years operating at design capacity.

US$ million, 2014 currency

Codelco faces an unprecedented investment challenge

Investment Program: history and future (PND* 2014)

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

*: PND: Business and Development Plan.

Production contribution of all the Structural Projects, PND 2014 (under construction and pending approval)

3,000

Ministro Hales, Radomiro Tomic Sulphides Phase II, Chuquicamata Underground, El Teniente New Mine Level,

Salvador Inca Open Pit, Andina Transfer, Andina Expansion

per

2,500

2,000

‘000

tonn

es of cop

p

1,500

1,000

500

New Mine Level Teniente Chuquicamata Underground Inca Pit El Salvador

New Andina Phase II Other Projects Andina Plan with Projects Plan without Projects

Ministro Hales Sulphides R. Tomic – P. II

Primary Crushing System Andina

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Note: Ministro Hales project commissioned included in production of Codelco with and without Projects. PND: Business and Development Plan of Codelco (with projects)

Codelco: the challenge of maintaining production in the short and medium term, despite the sharp drop in ore grades

GRADE AND TREATED MINERAL**

(‘000 fmt)

COPPER PRODUCTION*

Treated mineral Copper ore grade

1.600

1.800

2.000

1 00

1,05

1,10

270 000

315.000

360.000

(‘000 fmt) ‘000 dmtpp g

%

800

1.000

1.200

1.400

0,90

0,95

1,00

180.000

225.000

270.000

200

400

600

800

0,75

0,80

0,85

45.000

90.000

135.000

* I d ’ i l d C d l ’ k i El Ab d A l A i S

0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0,700

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

** U il 2010 d d F 2010 d i d

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

*: It doesn’t include Codelco’s stake in El Abra and Anglo American Sur. **: Until year 2010, treated ore grade. From year 2010 to date, mined ore grade.

Projected production PND* 2014 and critical success factors

• Robust mine plans.

Production‘000 fmt

Treated ore grade (%)

1,02.000

• Optimize the use of treatment capacity,reaching design capabilities.

• Increase concentrator recovery andsmelter yield.

0,7

0,8

0,9

1.400

1.600

1.800

y

• Higher rates of operational continuity.

• Increased own and third partiesproductivity.0,4

0,5

0,6

800

1.000

1.200

• Management alignment and leadershipin the administration of assets andproduction processes.

0,1

0,2

0,3

200

400

600

• Commitment of employees and theentire organization.0,00

2014 2015 2016 2017 2018

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Note: It doesn’t include Codelco’s stake in El Abra and Anglo American Sur. *: PND stands for Business and Development Plan.

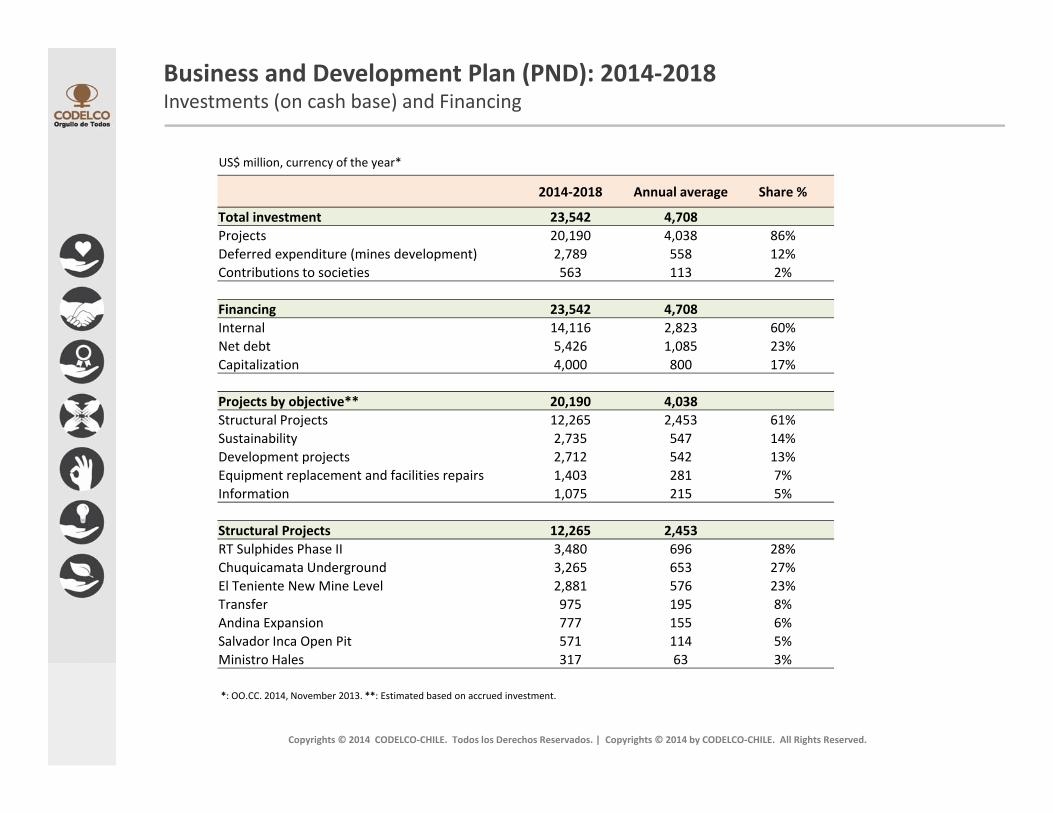

Business and Development Plan (PND): 2014‐2018Investments (on cash base) and Financing

2014‐2018 Annual average Share %

Total investment 23,542 4,708Projects 20,190 4,038 86%Deferred expenditure (mines development) 2 789 558 12%

US$ million, currency of the year*

Deferred expenditure (mines development) 2,789 558 12%Contributions to societies 563 113 2%

Financing 23,542 4,708Internal 14,116 2,823 60%Net debt 5,426 1,085 23%Capitalization 4,000 800 17%

Projects by objective** 20,190 4,038Structural Projects 12,265 2,453 61%Sustainability 2,735 547 14%Development projects 2 712 542 13%Development projects 2,712 542 13%Equipment replacement and facilities repairs 1,403 281 7%Information 1,075 215 5%

Structural Projects 12,265 2,453RT Sulphides Phase II 3,480 696 28%Chuquicamata Underground 3,265 653 27%El Teniente New Mine Level 2,881 576 23%Transfer 975 195 8%Andina Expansion 777 155 6%Salvador Inca Open Pit 571 114 5%Ministro Hales 317 63 3%

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Ministro Hales 317 63 3%

*: OO.CC. 2014, November 2013. **: Estimated based on accrued investment.

Codelco’s Investment: 2015PRELIMINARY FIGURES*

$ ll

INVESTMENTS BY DISTRICT PROJECTS INVESTMENT BY OBJECTIVES

US$ illiUS$ million

NORTH DISTRICT 1,707

CENTER SOUTH DISTRICT 1,782

STRUCTURAL PROJECTS 1,364

SUSTAINABILITY 847

US$ million

PROJECTS INVESTMENT 3,489

MINE DEVELOPMENT AND DEFERRED EXPENSES 800

SUSTAINABILITY 847

OTHER DEVELOPMENT PROJECTS 684

ENGINEERING STUDIES, DEFERRED EXPENSES

CONTRIBUTIONS TO SOCIETIES 113

GEOLOGICAL EXPLORATION AND RESEARCH

362

EQUIPMENT REPLACEMENT AND FACILITY REFURBISHMENT 233

GRAND TOTAL ACCRUED 4,402 PROJECTS INVESTMENT 3,489

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

*: 2015, preliminary budget.

Structural mining projects: major milestones 2014 ‐ 2015

• Chuquicamata Underground:– Taking investment decision and start construction, beyond the early works.

• Chuquicamata Underground:– Taking investment decision and start construction, beyond the early works.

• El Teniente NewMine Level:– Further progress in the development and construction of mining works.

• El Teniente NewMine Level:– Further progress in the development and construction of mining works.

• RT Sulphides Phase II:– Environmental approval.– Submit the First Stage of investment request.

• RT Sulphides Phase II:– Environmental approval.– Submit the First Stage of investment request.

• Andina Expansion:– Continue advancing for environmental approval in 2015.

• Andina Expansion:– Continue advancing for environmental approval in 2015.

• Salvador Inca Open Pit:– Completion of pre‐feasibility study.

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Cross challenge: detailed engineering of change in management models of the projects

The increase in costs has been a widespread trend in the industry

300

INDUSTRY AVERAGE COSTS

c/lb, currency of the year

240

260

280

300

Total Cathode Cost

160

180

200

220

Net Cathode Cost

80

100

120

140Cash Cost (C1)

0

20

40

60

1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

Source: Wood Mackenzie and Codelco.

After several years, during 2013, Codelco broke the upward trend in costs standing at the second quartile cut of the industry cost

200

DIRECT CASH COST (C1), CODELCO AND INDUSTRY QUARTILES

c/lb, currency of the year

160

180

200

3rd quartile cut

100

120

1402nd quartile cut

1st quartile cut

40

60

80

0

20

40

1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

CODELCO

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Source: Wood Mackenzie and Codelco.

Since 2013, Codelco is engaged in a systematic effort to increase productivity and reduce costs

Maximize copper production through: • Identify opportunities that provide fine copper other than those defined in budgetOptimize

PRODUCTIVITYPRODUCTIVITY

STRUCTURAL PROJECT OF PRODUCTIVITY AND COSTS (PEPC) MODEL:DETAIL BY LEVER

• Identify opportunities that provide fine copper, other than those defined in budget • Visibility and closing the gaps of bottlenecks • Project of Breaks in Management

Promote initiatives to improve productivity:• Project of Third Party Service Productivity (PPST)

Communica

performance in critical path

Services • FTE and Productivity Measurement • Relationship with APRIMIN, CCHC, AGEMA and Mining Council • Management model based on KPI and Back Office (PGST)

Optimize budget management corporately:• Salaries

ation plan and tr

productivity

• Energy, supplies, materials and equipment • Energy efficiency • Contracts, services and strategic supplies• Third Party Services

Through savings on discretionary items, install a transverse message of cost

ransfer of good

Budget Optimization

g g y , gcontainment, including:• Vehicles• Consultancies • Service commissions• Cellphones

practices

Hygienic Factors

COSTSCOSTS

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

Our challenge: to eradicate fatalitiesNumber of Fatalities and Rate, 2000 – 2014*

Number of fatalities Fatalities per million of hours‐worked0,1212

0,079

0,104

0,084 0,0850 08

0,10

8

10

0,076

0,054 0,053

0,06

0,08

6

8

0,038

0,0390,042

0,023

0,033

0,024

0 0170,02

0,04

2

4

0,0130,017

0,0002000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

FAT k FAT t t FAT t t l t

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

*: Year 2014 up to November 7.

FAT own workers FAT contractors FAT total rate

Environment and communities: PND 2014 goals and key success factors

50

SERIOUS AND VERY SERIOUS ENVIRONMENTAL INCIDENTS

GOALS

• Zero serious and very serious environmental incidents.

• Zero serious or very serious sanctions of EnvironmentSuperintendence.

• Zero community conflicts with impact on business continuity ori j t ti

20

30

40

50

in projects execution.

• Environmental and social approval of the Structural Projects.0

10

2008 2009 2010 2011 2012 2013 2014*

KEY SUCCESS FACTORS*: Year 2014 up to November 12.

2011 2014

ENVIRONMENTAL VULNERABILITIES • Closing gaps associated with the most critical environmentalvulnerabilities.

• Ensuring RCAs commitments.2011 2014

Total 92 40

More critical 55 14

• Environmental Risk System integrated to the operation.

• Application of standards and tools for community management:close linkage with more critical localities.

• Commitment of employees and the entire organization.

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.

CHILE‐JAPAN BUSINESS COMMITTEECHILE JAPAN BUSINESS COMMITTEECHILEAN COPPER MINING AND CODELCO CHALLENGES

Nelson Pizarro C

December 2nd, 2014

Nelson Pizarro C.CEO

Copyrights © 2014 CODELCO‐CHILE. Todos los Derechos Reservados. | Copyrights © 2014 by CODELCO‐CHILE. All Rights Reserved.