chikahisa sumi director, regional office for asia ... - mier · chikahisa sumi. director, regional...

TRANSCRIPT

Chikahisa SumiDirector, Regional Office for Asia and the Pacific

International Monetary Fund

A more gradual monetary policy normalization

Fiscal stance remains neutral

Moderate inflation in both AEs and EMDEs Oil baseline projection is raised from last year but

remains weak Upward revision for nonfuel commodities price

projections

0

2

4

6

8

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Real GDP Growth

Emerging Market and Developing EconomiesWorldAdvanced Economies

(percent YOY)

Risks to the Global Outlook

ASSUMPTIONS

Source: International Monetary Fund, World Economic Outlook, October 2017. 2

World AdvancedEconomies U.S. U.K. Japan Euro

Area Germany CanadaOther

Advanced Asia

2016 3.2 1.7 1.5 1.8 1.0 1.8 1.9 1.5 2.2

2017 3.6 2.2 2.2 1.7 1.5 2.1 2.0 3.0 2.6

Revision from Jul.

20170.1 0.2 0.1 0.0 0.2 0.2 0.2 0.5 0.3

Revision from Apr.

20170.1 0.2 -0.1 -0.3 0.3 0.4 0.4 1.1 0.3

2018 3.7 2.0 2.3 1.5 0.7 1.9 1.8 2.1 2.5

Revision from Jul.

20170.1 0.1 0.2 0.0 0.1 0.2 0.2 0.2 0.1

Revision from Apr.

20170.1 0.0 -0.2 0.0 0.1 0.3 0.3 0.1 0.1

Source: International Monetary Fund, World Economic Outlook, October 2017. 3

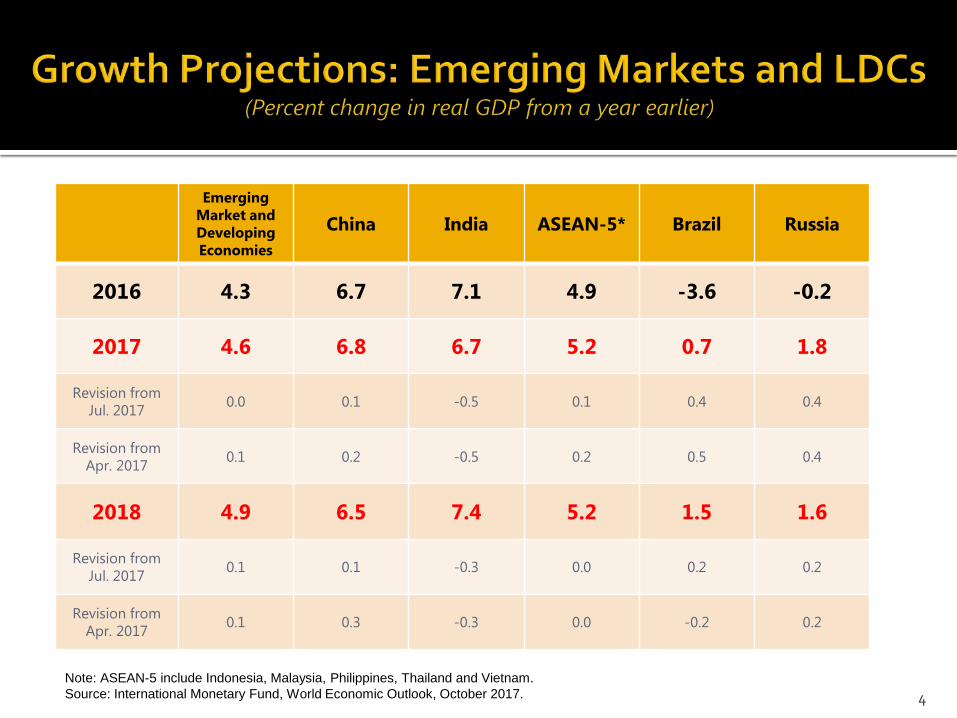

Emerging Market and Developing Economies

China India ASEAN-5* Brazil Russia

2016 4.3 6.7 7.1 4.9 -3.6 -0.2

2017 4.6 6.8 6.7 5.2 0.7 1.8

Revision from Jul. 2017 0.0 0.1 -0.5 0.1 0.4 0.4

Revision from Apr. 2017 0.1 0.2 -0.5 0.2 0.5 0.4

2018 4.9 6.5 7.4 5.2 1.5 1.6

Revision from Jul. 2017 0.1 0.1 -0.3 0.0 0.2 0.2

Revision from Apr. 2017 0.1 0.3 -0.3 0.0 -0.2 0.2

Note: ASEAN-5 include Indonesia, Malaysia, Philippines, Thailand and Vietnam. Source: International Monetary Fund, World Economic Outlook, October 2017. 4

0

1

2

3

4

5

6

7

8

9

Asia Euro area Latin America andthe Caribbean

Middle East andNorth Africa

United States

April 2017 WEO October 2017 WEO

2017 Inflation Forecast(Percent)

Source: IMF World Economic Outlook. 5

Global growth picked up further in 2017H1; outlook is for higher annual growth in 2017 and 2018

Advanced Economies: stronger cyclical recovery in near term, subdued potential growth in medium term

Emerging Market and Developing Economies: activity in stressed economies bottoming out, commodity importers generally projected to maintain high growth rates

Inflation remains subdued

Risks skewed to the downside in the medium term

Policy priorities: macroeconomic management needs vary; common goal is to boost potential growth

6

ADVANCED ECONOMIES

Cyclical rebound; varying degrees of post-crisis repair;

Demographic trends

EMERGING MARKET AND DEVELOPING ECONOMIES

Rebalancing in China Adjustment to lower commodity prices Geopolitical and political factors

Weak productivity growth

Ongoing forces…

…overlaid on…

7

• Asia is in a favorable position: growth is revised up.

• However, the sustainability of the pickup is still not clear.

• While Asia is more resilient, medium-term vulnerabilities have increased.

• The “window for reforms” is now.

Growth Projections: Selected Asia(Percent change from a year earlier)

World Asia China India Japan Korea

Australiaand New Zealand ASEAN

Small States

2016 3.2 5.4 6.7 7.1 1.0 2.8 2.6 4.8 3.2

2017 3.6 5.6 6.8 6.7 1.5 3.0 2.4 5.1 3.7

Revision fromApr. 2017

0.2 0.1 0.2 -0.5 0.3 0.3 -0.5 0.2 0.1

2018 3.7 5.5 6.5 7.4 0.7 3.0 2.9 5.1 4.4

Revision from Apr. 2017

0.1 0.1 0.3 -0.3 0.1 0.1 0.2 0.0 -0.2

9

5459 61

55 54

0

10

20

30

40

50

60

70

2014 2015 2016 2017 2018

Asia: Contribution to Global Growth(Percent, PPP)

Source: IMF World Economic Outlook.10

-20

-10

0

10

20

30

40

Jul-1

1Ma

r-12

Nov-

12Ju

l-13

Mar-1

4No

v-14

Jul-1

5Ma

r-16

Nov-

16Ju

l-17

Jul-1

1Ma

r-12

Nov-

12Ju

l-13

Mar-1

4No

v-14

Jul-1

5Ma

r-16

Nov-

16Ju

l-17

To the United States To Euro area To Japan To China

Selected Asia: Exports to Major Destinations(Year-over-year percent change)

Sources: Haver Analytics; CEIC Data Co. Ltd.; and IMF staff calculations.Note: Selected Asia includes China, Hong Kong SAR, Japan, Korea, Malaysia, Taiwan Province of China, Thailand, the Philippines, Singapore, and Vietnam. Indonesia is excluded due to data lags.

11

-2-10123456789

2016

2017

2018

2016

2017

2018

2016

2017

2018

2016

2017

2018

2016

2017

2018

2016

2017

2018

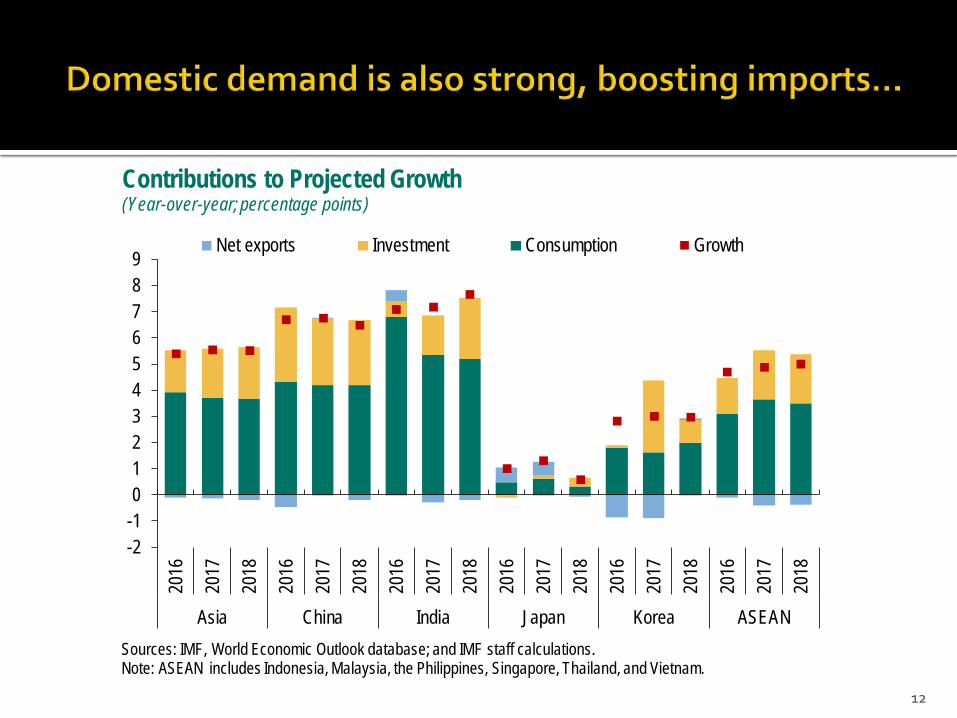

Asia China India Japan Korea ASEAN

Net exports Investment Consumption Growth

Contributions to Projected Growth(Year-over-year; percentage points)

Sources: IMF, World Economic Outlook database; and IMF staff calculations.Note: ASEAN includes Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam.

12

-2-1012345678

Asia China India Japan Korea ASEAN

2015 2016 2017 (Projection) 2018 (Projection)

Asia: Current Account Balances(Percent of GDP)

Sources: IMF, World Economic Outlook database; and IMF staff calculations and projections.Note: ASEAN includes Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam. 13

-40

-30

-20

-10

0

10

20

30

40

50

60

Aug 15 Dec 15 Apr 16 Aug 16 Dec 16 Apr 17 Aug 17

Africa & Middle East Emerging Europe Latin America Emerging Asia

Sources: National Sources; Bloomberg Finance L.P.; and Institute of International Finance.

Total Portfolio Flows(Billions of U.S. dollars)

14

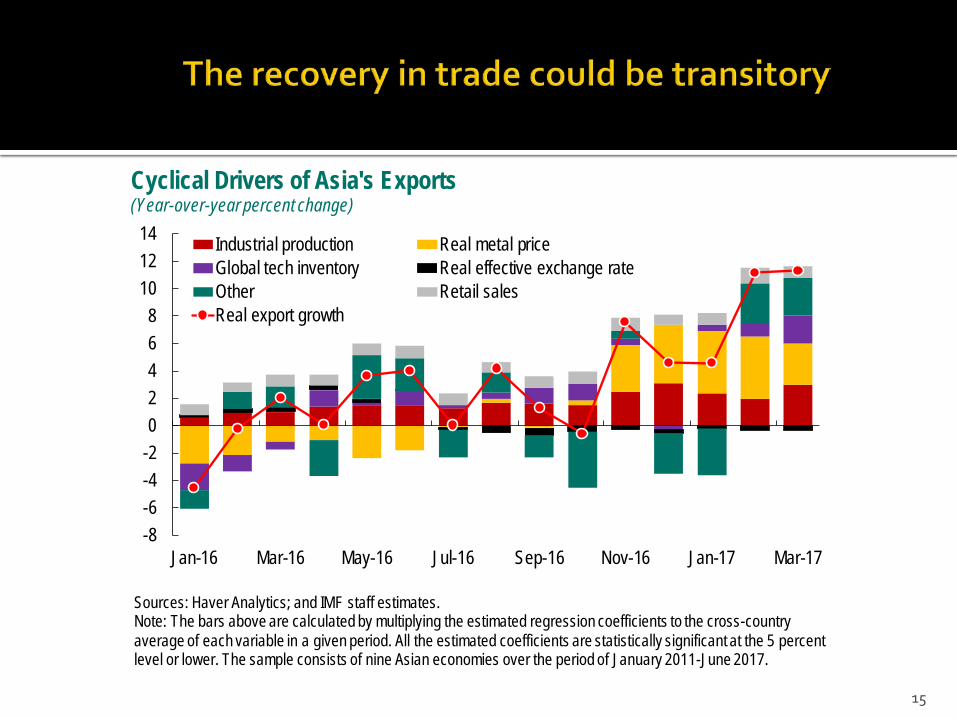

-8-6-4-202468

101214

Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17

Industrial production Real metal priceGlobal tech inventory Real effective exchange rateOther Retail salesReal export growth

Sources: Haver Analytics; and IMF staff estimates.Note: The bars above are calculated by multiplying the estimated regression coefficients to the cross-country average of each variable in a given period. All the estimated coefficients are statistically significant at the 5 percent level or lower. The sample consists of nine Asian economies over the period of January 2011-June 2017.

Cyclical Drivers of Asia's Exports (Year-over-year percent change)

15

•Tighter global financial conditions, amid high leverage.

• Geopolitical tensions.

• Inward looking policies.

• Sharp adjustment in China over the medium term.

• Climate change and natural disasters.

16

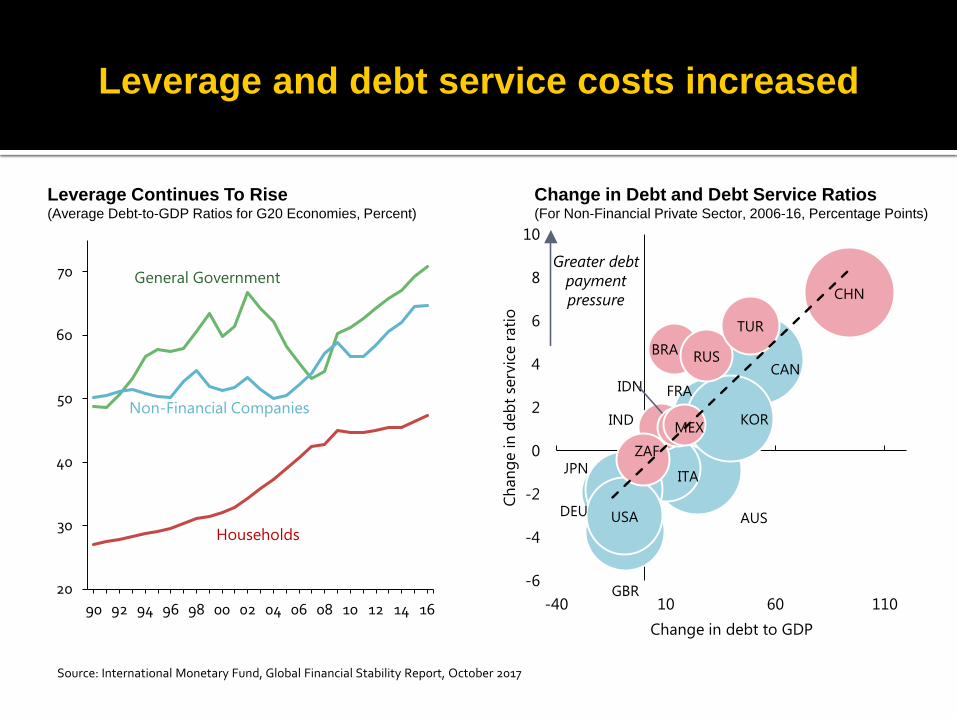

9

Leverage Continues To Rise(Average Debt-to-GDP Ratios for G20 Economies, Percent)

Leverage and debt service costs increased

Change in Debt and Debt Service Ratios(For Non-Financial Private Sector, 2006-16, Percentage Points)

20

30

40

50

60

70

90 92 94 96 98 00 02 04 06 08 10 12 14 16

General Government

Non-Financial Companies

HouseholdsAUS

CANFRA

DEU

ITAJPN

KOR

GBR

USA

BRA

CHN

IND

IDN

MEX

RUS

ZAF

TUR

-6

-4

-2

0

2

4

6

8

10

-40 10 60 110

Chan

ge in

deb

t ser

vice

ratio

Change in debt to GDP

Greater debtpaymentpressure

Source: International Monetary Fund, Global Financial Stability Report, October 2017

Credit above trend

-15

-10

-5

0

5

10

15

20

1996 1997 1998 2000 2001 2003 2004 2005 2007 2008 2010 2011 2013 2014 2015

EM Asia EMs AEs

Credit Gap(Percent, PPP weighted)

Source: Bank for International Settlements. 18

0

50

100

150

200

250

300

350

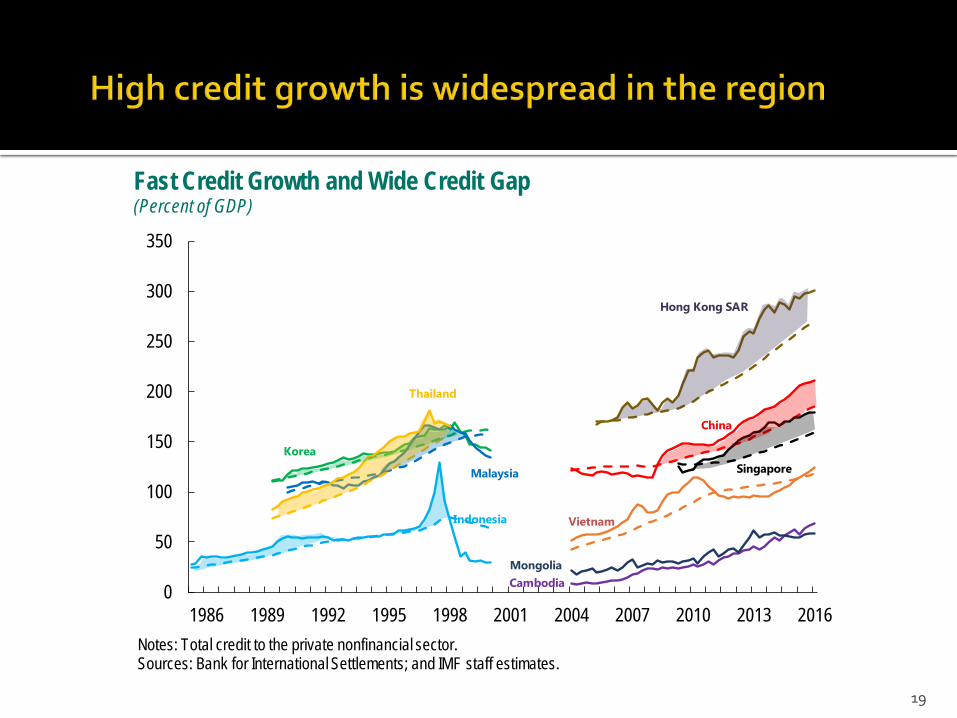

1986 1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

Fast Credit Growth and Wide Credit Gap (Percent of GDP)

Notes: Total credit to the private nonfinancial sector.Sources: Bank for International Settlements; and IMF staff estimates.

China

Hong Kong SAR

Indonesia

Korea

Thailand

Malaysia

Vietnam

MongoliaCambodia

Singapore

19

0

20

40

60

80

100

120

140

160

180

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Private Public

Selected Asia: Private and Public Debt(Percent of GDP)

Sources: Bank for International Settlements; IMF Wolrd Economic Outlook; and IMF staff calculations.Note: Selected Asia is PPPGDP weighted by Australia, China, Hong Kong SAR, Japan, Korea, India, Indonesia, Malaysia, New Zealand, Singapore, and Thailand.

20

0

20

40

60

80

100

120

140

Austr

alia

China

Hong

Kon

g SAR Ind

ia

Indon

esia

Japa

n

Kore

a

Malay

sia

New

Zeala

nd

Sing

apor

e

Thail

and

All c

ount

ries AE EMs

EM A

sia

1996 Q4 2016 Q4

Households Credit (Percent of GDP)

Note: For green bars: Advanced Economies, 1999Q4; Indonesia, 2001Q4; Malaysia, 2006Q1; China, 2006Q1; India, EM Asia, 2007Q2; EMs, All Countries, 2008Q1.Sources: Bank for International Settlements; and IMF staff calculations.

Adva

nced

Econ

omies

21

10

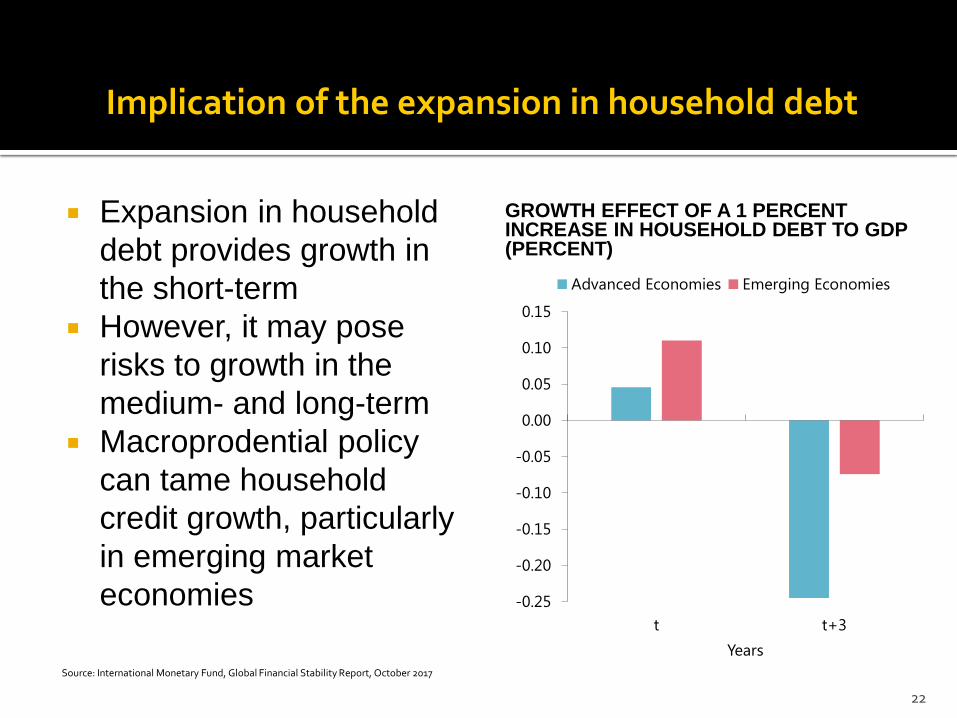

Implication of the expansion in household debt

Source: International Monetary Fund, Global Financial Stability Report, October 2017

GROWTH EFFECT OF A 1 PERCENT INCREASE IN HOUSEHOLD DEBT TO GDP(PERCENT)

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

t t+3Years

Advanced Economies Emerging Economies

Expansion in household debt provides growth in the short-term

However, it may pose risks to growth in the medium- and long-term

Macroprodential policy can tame household credit growth, particularly in emerging market economies

22

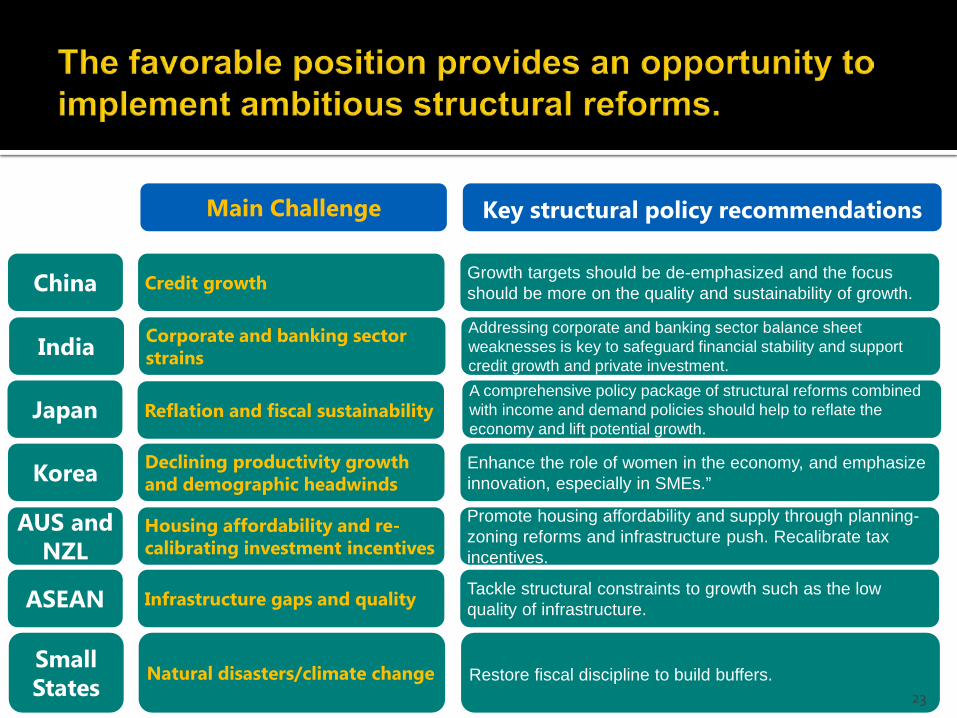

Key structural policy recommendationsMain Challenge

China Growth targets should be de-emphasized and the focus should be more on the quality and sustainability of growth. Credit growth

JapanA comprehensive policy package of structural reforms combined with income and demand policies should help to reflate the economy and lift potential growth.

Reflation and fiscal sustainability

IndiaAddressing corporate and banking sector balance sheet weaknesses is key to safeguard financial stability and support credit growth and private investment.

Corporate and banking sector strains

AUS and NZL

Promote housing affordability and supply through planning-zoning reforms and infrastructure push. Recalibrate tax incentives.

Housing affordability and re-calibrating investment incentives

ASEAN Tackle structural constraints to growth such as the low quality of infrastructure. Infrastructure gaps and quality

Korea Enhance the role of women in the economy, and emphasize innovation, especially in SMEs.”

Declining productivity growth and demographic headwinds

SmallStates Restore fiscal discipline to build buffers.Natural disasters/climate change

23

Malaysian Institute of Economic ResearchNational Economic Outlook Conference

November 21, 2017