chicago skyway - ferrovial.com · america, canada, australia, japan or any other jurisdiction where...

TRANSCRIPT

www.cintra.es Chicago Skyway 1

CHICAGO SKYWAYMadrid, 16 November 2004

www.cintra.es Chicago Skyway 2

Pursuant the existing publicity restrictions contained in the Initial Public Offer of the CINTRACONCESIONES DE INFRAESTRUCTURAS DE TRANSPORTE, S.A., shares, listed in the SpanishStock Exchanges since 27th October, 2004, please note the following:

The release of research or information on the Company and its distribution to investors is restricted untildecember 6th 2004. The receiver of this information expressely accepts, the obligation not to publish anyanalysis or report on the Company until such date.

The information contained herein is not for publication or distribution to persons in the United States ofAmerica, Canada, Australia, Japan or any other jurisdiction where the distribution of such information isrestricted by law, and does not constitute an offer to sell, or solicitation of an offer to buy, securities in theUnited States, Canada, Australia, Japan or in any other jurisdiction in which it is unlawful to make suchan offer or solicitation. The securities referred to herein have not been and will not be registered underthe US Securities Act of 1933, as amended. The securities may not be offered or sold in the UnitedStates absent registration or an exemption from registration under the U.S.. Securities Act of 1933, asamended, or in any other jurisdiction other than in compliance with the laws of that jurisdiction. There isno intention to register any portion of the Offering in the United States or to conduct a public offering ofsecurities in the United States. No money, securities or other consideration is being solicited, and, if sentin response to the information contained herein, will not be accepted.

Neither this document nor any copy of it may be taken or transmitted or published into the United States,Australia, Canada or Japan or distributed, directly or indirectly, to any resident thereof.

IMPORTANT LEGAL NOTICE

www.cintra.es Chicago Skyway 3

[ First incursion into the US—a strategic market in Cintra’s expansion plans

[ Advances in geographical diversification

[ Capacity to generate value:

- higher investment and a longer concession period

[ Growth capacity:

- can absorb traffic from saturated alternative routes- toll review- completion of rehabilitation work (6 lanes were restored)

[ The transaction is in line with strategic objectives:

- significant investment- the world’s economic powerhouse- long-term concession: 99 years - increases residual life- controlling stake

STRATEGIC TRANSACTION

www.cintra.es Chicago Skyway 4

STRATEGIC TRANSACTION

99 94

6150

36 32 29 27 26 25 20 20 19 13 11

42

Skyway

407 ETR

Radial

4

Ausol

II

Ausol

I

Madrid

-Leva

nte Autema

N4-N6

Norte L

itoral

Algarve M-45

Collipu

lli-Te

muco

Santia

go - T

alca

Temuc

o-Río

Bueno

Europis

tas

Talca

- Chil

lán

Weighted average of 73 years (*)

(*) based on Cintra's internal valuations

Spain26%

Portugal 5%

Canada23%

Ireland3%

USA24%

Chile19%

INVESTMENT BY REGION TOTAL: €1.7 BILLION

INCREASE IN RESIDUAL LIFE

Cintra manages 17 toll roads(Artxanda tunnel held through Europistas)

www.cintra.es Chicago Skyway 5

Toll roads portfolio by degree of development

8%

26%

27%

39%

Without Chicago Skyway With Chicago Skyway

11%

35%

36%

18%

Construction

Ramp-up

Growth

Maturity

www.cintra.es Chicago Skyway 6

STRATETIC TRANSACTION

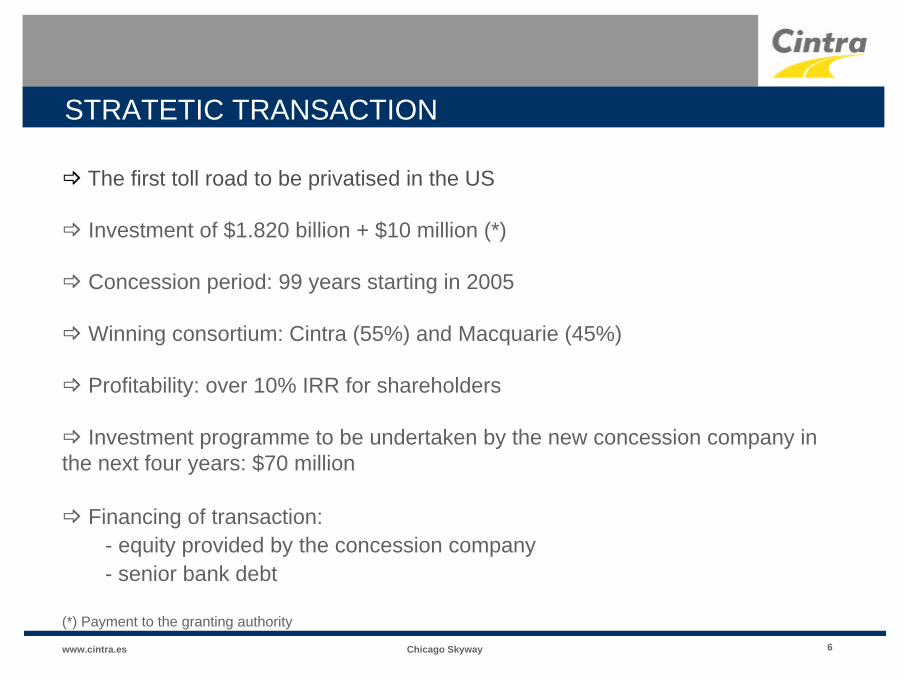

_ The first toll road to be privatised in the US

_ Investment of $1.820 billion + $10 million (*)

_ Concession period: 99 years starting in 2005

_ Winning consortium: Cintra (55%) and Macquarie (45%)

_ Profitability: over 10% IRR for shareholders

_ Investment programme to be undertaken by the new concession company inthe next four years: $70 million

_ Financing of transaction:- equity provided by the concession company- senior bank debt

(*) Payment to the granting authority

www.cintra.es Chicago Skyway 7

THE PROJECT

www.cintra.es Chicago Skyway 8

THE PROJECT

_Opened to traffic in 1959

_ A 12.5 km elevated tollway

_ 36% of elevated structures - bridge over the riverCalumet (main span: 216 metres)

_ 3 lanes each way

_ Traditional tolling, no transponders

_ Connects the Dan Ryan Expressway (southernaccess to Chicago) to the Indiana Toll Road (accessto Indiana, Michigan and the north-eastern states). Itis part of the I-90 that links Boston and Seattle.

_ An asset in “good condition” - intenserehabilitation in the last four years ($260 million)

www.cintra.es Chicago Skyway 9

KEY AGGREGATES

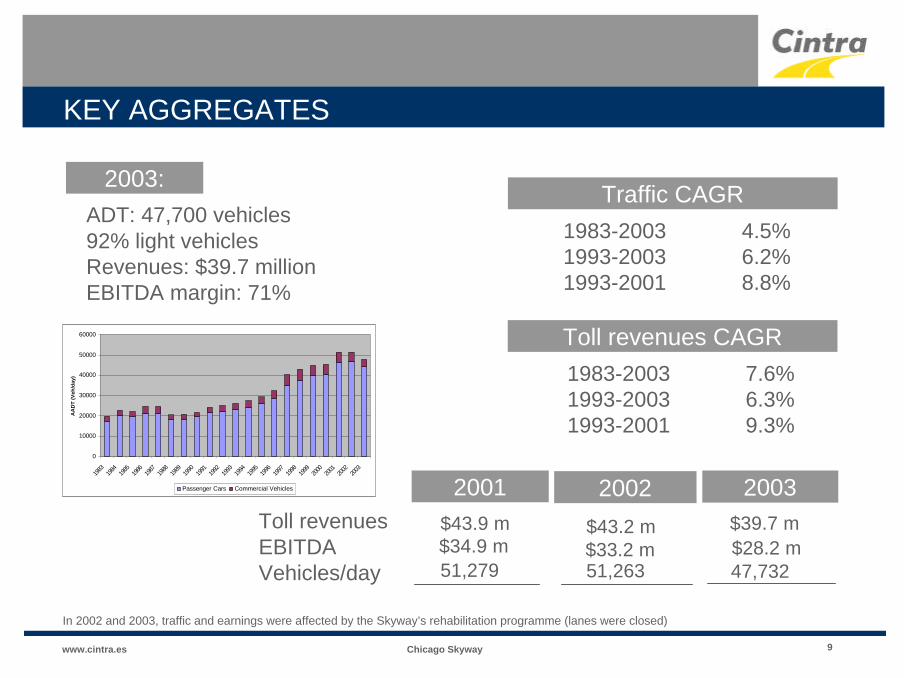

ADT: 47,700 vehicles92% light vehiclesRevenues: $39.7 millionEBITDA margin: 71%

In 2002 and 2003, traffic and earnings were affected by the Skyway’s rehabilitation programme (lanes were closed)

2001 2002 2003Toll revenues EBITDAVehicles/day

$34.9 m $33.2 m $28.2 m

Traffic CAGR 1983-2003 4.5% 1993-2003 6.2% 1993-2001 8.8%

Toll revenues CAGR1983-2003 7.6%1993-2003 6.3%1993-2001 9.3%

$39.7 m

47,732

$43.2 m$43.9 m

51,263 51,279

2003:

0

10000

20000

30000

40000

50000

60000

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

AA

DT

(V

eh/d

ay)

Passenger Cars Commercial Vehicles

www.cintra.es Chicago Skyway 10

TOLLS

_In the 2008-2017 period, the maximum toll applicable each year is the greater ofthe toll included in the above table or the maximum toll for the immediatelypreceding year adjusted for period inflation_As from 2018, tolls will increase by the greater of 2% per year, annual CPI, ornominal per capita GDP growth_Similarities between Chicago Skyway and 407 ETR (Canada): in both cases,maximum revenue tolls in the long term

$0,0

$1,0

$2,0

$3,0

$4,0

$5,0

$6,0

$7,0

$ p

or

viaj

e (t

arifa

máx

ima)

ligeros 2 2,5 2,5 2,5 3 3 3 3,5 3,5 4 4 4,5 4,5 5 5,1

pesados / eje DIA 1,2 1,7 1,7 1,7 2,6 2,6 2,6 3,4 3,4 4,2 4,2 5,1 5,1 5,9 6,1

pesados / eje NOCHE 1,2 1,2 1,2 1,2 1,8 1,8 1,8 2,4 2,4 3 3 3,6 3,6 4,2 4,3

2004 5 6 7 8 9 10 11 12 13 14 15 16 17 2018

www.cintra.es Chicago Skyway 11

TRAFFIC

] Higher growth capacity:- CAGR in the Skyway 1996-2001: 8.0%- CAGR in the corridor: 3.3%

] Absorption capacity: - captures 44% of the corridor’s traffic (upfrom 35% in 1996)

] Journey time reduced by 20-40 minutes inpeak hours with respect to the alternative route

] The only road in the corridor with sparecapacity

Reasons for travelling(light vehicles)

Business 30%

Home/work39%

Other31%

www.cintra.es Chicago Skyway 12

TRAFFIC

Spare capacity contrasts with growing congestion on alternative routes

ADT per lane in 2003

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Dan Ryan(N)

Dan Ryan(S)

BishopFord

BormanKingery

Skyway (6 lanes)

Indiana E-W

www.cintra.es Chicago Skyway 13

TRAFFIC

Skyway: shortens distances and reduces journey times

Skyway / Indiana East-West Toll

32 minutes +/-5 minutes30 miles

Alternative route54 minutes +/- 10 minutes36 miles

60% slower20% longer

www.cintra.es Chicago Skyway 14

CATCHMENT AREA

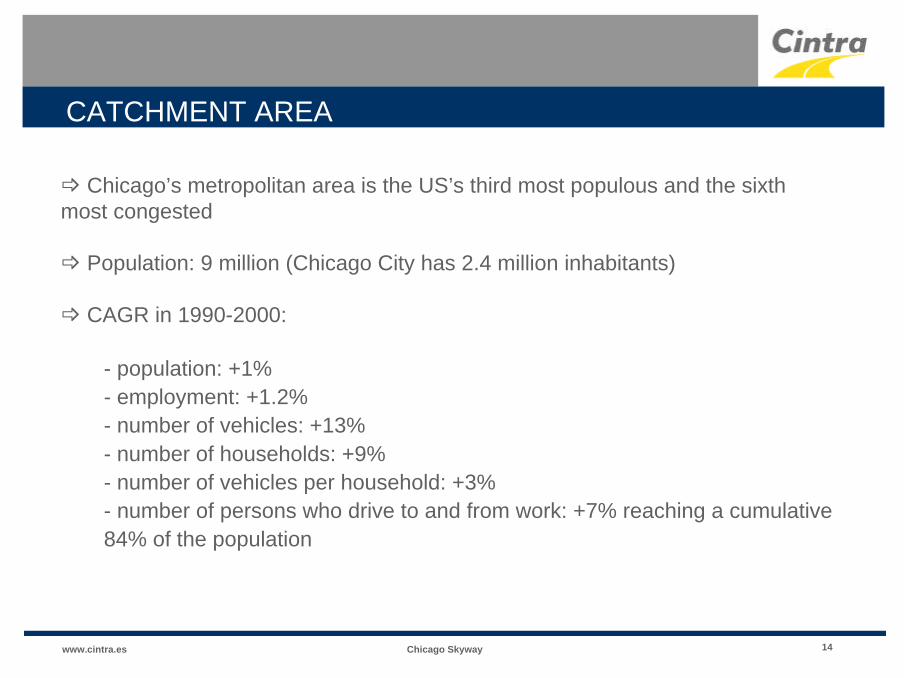

_ Chicago’s metropolitan area is the US’s third most populous and the sixthmost congested

_ Population: 9 million (Chicago City has 2.4 million inhabitants)

_ CAGR in 1990-2000:

- population: +1%- employment: +1.2%- number of vehicles: +13%- number of households: +9%- number of vehicles per household: +3%- number of persons who drive to and from work: +7% reaching a cumulative84% of the population

www.cintra.es Chicago Skyway 15

TRAFFIC ANALYSIS

_ Capacity: 150,000 vehicles/day, to be attained in 2050, beginning to take effect

in 2020 (extension of peak hours)

_Maximum revenue toll: attained in about 2035

_A road with spare capacity in a congested corridor: traffic on the Skyway did not

start to rise until alternative routes became congested in the late 1980s

_Sizeable weekend traffic (recreational uses, trips to Michigan and casinos)

_ Traffic risk is mitigated because: - traffic does not depend on future real estate or industrial development(they will provide only 1% additional traffic in 2020) - plans to develop competing roads and to expand existing roads have beenexamined with Illinois and Indiana road agencies and are limited by environment - rising home prices in Chicago are shifting the population outwards: LakeDistrict (east of the Skyway) is expanding rapidly

www.cintra.es Chicago Skyway 16FINANCING

www.cintra.es Chicago Skyway 17

FINANCIAL STRUCTURE

_ Financing: shareholder equity + senior bank debt

Cintra equity 500.5 Acquisition 1,820 + 10 Macquarie equity 409.5 Reserve account 37 Debt (tranche A) 1,020 Transaction costs 53 Total 1,920 Total 1,920

($million)

_Bank loan underwritten by SCH, CALYON, BBVA, and DEPFA- Use: acquisition (tranche A: $1,020Mn), liquidity facility (tranche B: $90Mn),2005-2008 investment programme (tranche C: $80Mn)- Maturity: 9 years

_Possible bond issue: refinancing of loan and partial reimbursement ofshareholders contribution

- Firm offers from monoline insurers- Preliminary investment grade rating from S&P and Moody’s- Period: up to a maximum of 40-45 years from 2005, in several stages

SOURCES OF FUNDS APPLICATIONS OF FUNDS

www.cintra.es Chicago Skyway 18BIDDING PROCESS

www.cintra.es Chicago Skyway 19

BIDDING PROCESS_ Sale calendar

Hito FechaMay 2004

Economic Disclosure Statemen (EDS) for affiliate companies 30 June

Non-binding indicative offer 8 July

Meeting with City / Site Visit 20 July

Due diligence July-AugustFinal comments on Concession Agreement 10 September

Receipt of offer forms and final concession contract 30 SeptemberIncorporation and registration of new companies andsubmission of new EDS

4 October

Final binding offer 14 October

Award 15 October

Signature of concession contract 27 October

Financial close End January

Transitory period (i.e. services provided by the City of Chicago) February-May

Pre-qualification

_No. of advisors/auditors managed: 18_No. of people involved: internal (15); external advisors (60)_Teams located in Madrid/Chicago/New York/Sydney_Bid budget for external advisors: $2.2 m

MILESTONE DATE

www.cintra.es Chicago Skyway 20

CONSULTANTS

- Maunsell (consortium advisor)- Halcrow (banks’ advisor)

- Cintra and MIG

- CTE, Consoer Townsend Envirodyne

- Halcrow (banks’ advisor)

- Ferrovial Agroman Engineering Dept.- Cintra + 407ETR Engineering Dept.

Extensive knowledge of the asset(official Skyway engineer for severalyears)

Extensive experience ininternational and US markets(407ETR traffic advisors)

World leaders in infrastructuremanagementExperience in concessions with tollincreases (sensitivity to tollincreases)

Broad international experience

Proven technical knowledge andexperience

TRAFFIC AND REVENUE ANALYSIS

TECHNICAL ANALYSIS

www.cintra.es Chicago Skyway 21MANAGEMENT AND CONTRACT

www.cintra.es Chicago Skyway 22

MANAGEMENT

_Financial close: payment to City of Chicago on 26 January 2005_4-month transitory period from financial close. In this period:

- All current Skyway employees which we request (whether they will form partof our workforce or not) will remain in their posts- All services provided by the City of Chicago to Skyway will remain active(winter maintenance, legal advice, etc.)- The Skyway will compensate the City of Chicago for these costs

_Selection of personnel: to be completed before year-end (no obligation to hireany of the current Skyway employees)_ Cintra majority on Board of Directors_ Senior management team with international experience:

- Cintra: 3 expatriates- MIG: 2 expatriates

_Strong support from Sponsors’ corporate departments in the initial start-upperiod - some of the team already in place

www.cintra.es Chicago Skyway 23

CONCESSION CONTRACT

_ The concession holder has the right to apply maximum tolls and:- Tolls which are lower than the maximum permitted- User discounts- Different tolls according to the time of day, season, congestion levels,occupancy levels, etc.-Special charges for implementing electronic tolling systems

_The City of Chicago is obliged to collaborate with the concession holder toenforce the electronic tolling system (where implemented)

_There are a number of improvements to be undertaken by the concession holderin the period 2005-2008, whose scope and deadline for completion are establishedin the contract

_Contract does not include any protection against the development of new routes,alternative modes of transport or the improvement of existing alternative routes

- But they’ve been analysed and are limited by envitonment

_No compensation for toll increases on the connecting toll road with Indiana (80%of Skyway traffic currently comes from this road) which may impact traffic, but

- Scope for increase subject to legal limitations- Sensitivity analysis developed reveals impact in traffic is limited

www.cintra.es Chicago Skyway 24

CONCESSION CONTRACT

_The concession holder must comply with the operation and maintenancecriteria established by the City of Chicago

_Concession holder default:

- Any breach not cured within 90 days, with a 60-day remedy period (30days in some cases and for disallowed share transactions)- Failure to comply with operation criteria is not cause for default exceptwhere it jeopardises safety or impedes the use of the Skyway as a transportinfrastructure- In the event of unremedied default by the concession holder, the contractwill be terminated with no right to compensation

www.cintra.es Chicago Skyway 25

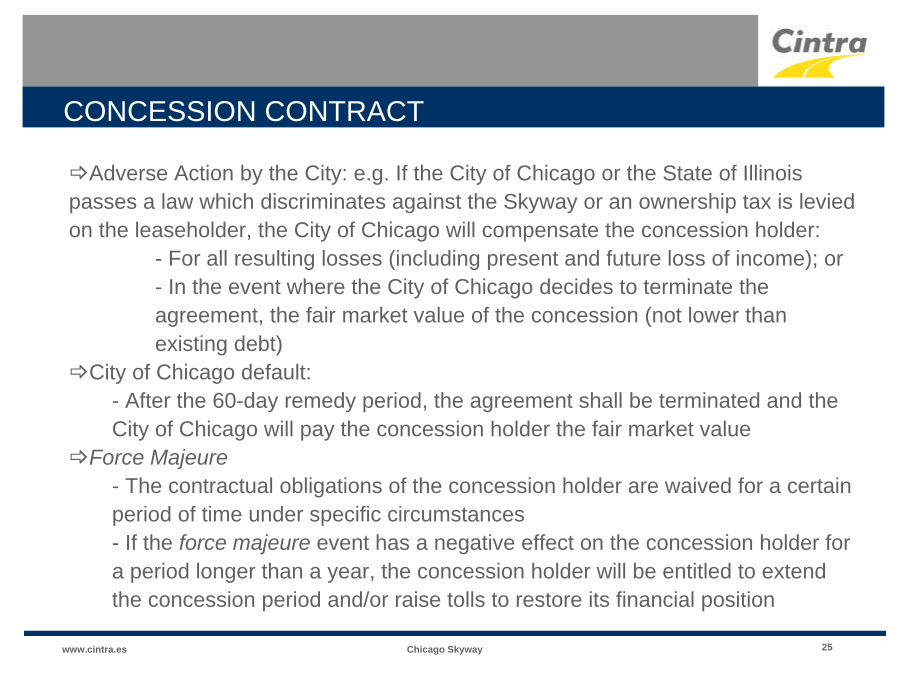

CONCESSION CONTRACT

_Adverse Action by the City: e.g. If the City of Chicago or the State of Illinoispasses a law which discriminates against the Skyway or an ownership tax is leviedon the leaseholder, the City of Chicago will compensate the concession holder:

- For all resulting losses (including present and future loss of income); or- In the event where the City of Chicago decides to terminate theagreement, the fair market value of the concession (not lower thanexisting debt)

_City of Chicago default:- After the 60-day remedy period, the agreement shall be terminated and theCity of Chicago will pay the concession holder the fair market value

_Force Majeure- The contractual obligations of the concession holder are waived for a certainperiod of time under specific circumstances- If the force majeure event has a negative effect on the concession holder fora period longer than a year, the concession holder will be entitled to extendthe concession period and/or raise tolls to restore its financial position

www.cintra.es Chicago Skyway 26ASSUMPTIONS AND THEIR IMPACT

www.cintra.es Chicago Skyway 27

BASIC ASSUMPTIONS

_Application of the maximum tolls envisaged in the concession contract

_∆ in CPI: 2.5% p.a. throughout the 99-year concession

_Nominal rise in GDP (from 2017): 4.5% p.a.

_Increase in US population (from 2017): 0.8% p.a.

- Increase in implicit nominal GDP per capita: approx. 3.7% p.a. (3.6%

assumed in model)

_The IRR calculation assumed no further releverage after the initial bond issue

_Traffic revenues: internal report (similar to bank audit reports)

_Investment programme for the first four years: $70 million

_Operation & Maintenance estimated by Cintra (based on projections by local

engineer CTE)

_EUR/USD exchange rate: 1.2272 (14/10/2004)

_Model developed for 99 years (no calculation of residual value)

www.cintra.es Chicago Skyway 28

CHICAGO SKYWAY