chapters - ccul.orgmembers.ccul.org/publications/cudigest/digest_issues/2012/12_0809... · credit...

TRANSCRIPT

credit union

Feature Story on Page 12

IRR: CUs Reveal Their Game Plan | Page 6Shapiro Group Celebrates 20 Years | Page 8Don’t Ignore the Big Squeeze | Page 17An Open Letter to Community Bankers | Page 22

C H A P T E R S:ON THE FRONT L INES

Vol. 38 | No. 5 | August/September 2012Members First

Jeffrey Cu- Jeffrey Cu-faude faude Principal, Idea ArchitectsConvention Emcee

What’s It Take to Succeed Right Here, Right Now?Learn to thrive in today’s changing world with some of the brightest minds in business, new media, cross-disciplinary innovation, politics, and consumer behavior.

And much more, including: Follow-up sessions with Baer, Goldman, and Moore, and additional Breakout Sessions • PAC Golf Tournament • Networking Opportunities • Exhibit Area

Register at amc.ccul.org right now!

Scheduled events and speakers are subject to change.

Tucker CarlsonDailyCaller.com editor-in-chief, FOX News contributor

California and Nevada Credit Union Leagues 2012 Annual Meeting & ConventionNov. 12–14The Mirage Hotel & CasinoLas Vegas, NV

Dr. Neil GoldmanSenior Partner, Goldman Consulting & Strategy

John MooreMarketing Mastermind fromStarbucks and Whole Foods

Jay BaerRenowned social media consultant; author of The NOW Revolution

Frans JohanssonCEO, The Medici Group; au-thor of The Medici Effect and The Click Moment

Emceed by

Jeffrey Cufaude Principal, Idea Architects

3credit union digest | august/september 2012 | members first

Leader 2 Leader South Bay CU

News & Views IRR: CUs Reveal Their Game Plan

Shapiro Perspective Shapiro Group Celebrates 20 Years

Advocacy Congressman Highlights CU Difference

Legal Staff, Social Media, and Free Speech

FEATURE STORY Chapters: On The Front Lines

Economic Perspective Why Ag, High-Tech, and Europe Matter

Market Performance Don’t Ignore the Big Squeeze

Asked & Answered No Training Needed? Think Again

Research & Information Which Rule Applies in Garnishments?

CU Business Solutions Overdraft Provider May Put CU at Risk

CU Business Solutions Retail Channels Never Die

Closing Thoughts An Open Letter to Community Bankers

5

6

8

10

11

1216

17

18

19

20

21

22

August/September 2012 | Vol. 38 | No. 5

What's Inside

credit union

On The Cover: California State Senator Tony Strickland (front center) poses with leaders of the California Credit Union League’s San Fernando-Antelope Valley Chapter (L-R): Linda Walmsley, Director of Compliance for First Entertain-ment CU; Anabel Ortiz, Technical Trainer for Los Angeles FCU; Terry Mota, Operations Process Improvement Manager for L.A. Financial FCU; Tony Strickland; Marvel Ford, Chap-ter President and FVP/Risk Management Officer for Califor-nia CU; Jared Falk, Collections Manager for L.A. Financial FCU; Ron McDaniel, President and CEO of California CU, and California Credit Union League Government Relations Committee Chairman; and Abiy Fikreslassie, Lending and Service Center Representative for SchoolsFirst FCU

Credit Union Digest publishes six bi-monthly issues per year.

Remaining Issues:

October/November 2012 Issue DEADLINE: Aug. 23, 2012 The Road Less Traveled

December 2012/January 2013 Issue DEADLINE: Oct. 25, 2012 Small But Mighty

Themes subject to change. For more infor-mation, please contact Credit Union Digest Editor-in-Chief Carol Payne at 800.472.1702, ext. 6040, or at [email protected].

Please Welcome Our New Member

Congratulations to the following credit union that recently became a member of the California Credit Union League:

AFTRA-SAG FCU CEO Roger Runyan [email protected] Assets: $192 million Burbank, CA

Editiorial Deadline Schedule

credit union

Feature Story on Page 12

IRR: CUs Reveal Their Game Plan | Page 6Shapiro Group Celebrates 20 Years | Page 8Don’t Ignore the Big Squeeze | Page 17An Open Letter to Community Bankers | Page 22

C H A P T E R S:ON THE FRONT L INES

Vol. 38 | No. 5 | August/September 2012Members First

4 credit union digest | august/september 2012 | members first

Editor-in-ChiEfCarol E. Payne, Vice President, Communications and Marketing | [email protected]

ASSoCiAtE EditorMatt Wrye, Publications Specialist/Writer | [email protected]

ASSiStAnt EditorDavid Dudley, Marketing Specialist/Copywriter | [email protected]

ExECutivE StAffDiana R. Dykstra, President and Chief Executive OfficerMark Klinkert, Senior Vice President and Chief Operating OfficerBob Arnould, Senior Vice President Sylvia Fath, Senior Vice President Lucy Ito, Senior Vice President Cindy Cavanaugh, Vice President

GrAphiC dESiGnNatalie J. Moreno, Senior Graphic DesignerDanielle Price, Graphic Designer

ConCEptCarol Payne | Matt Wrye

EditoriAL ContributorSVictoria Allen | Melissa Ameluxen | Greg Badovinac | Chris Collver | David Creager | Donna Dyer | Jeremy Empol | Rita Fillingane | Dwight Johnston |Henry Kertman | Dianne Molvig | Arnold Ramirez | Tina Ramos-Ingold | Andrea Svoboda | Ashley Trujillo | Tonja Wheatley | Thomas H. Wolfe

photoGrAphyDavid Dudley | Natalie J. Moreno | Carol E. Payne | Matt Wrye

ContACt informAtionInternet address | www.ccul.orgMailing address | P.O. Box 51476, Ontario, CA 91761-0076Communications Department Fax | 909.390.3014

Credit Union Digest (ISSN#08921075) is published bi-monthly by the California and Nevada Credit Union Leagues, 2855 E. Guasti Road, Ste. 600, Ontario, CA 91761-1250; 1201 K Street, Suite 1050, Sacramento, CA 95814. Annual subscription rate: $48 members, $250 non-members. To subscribe, contact LaDonna Kohler at [email protected]. Periodicals postage paid at Ontario, CA and additional mailing offices.

AdvErtiSinGTraci Miller Olszowy, Director, Membership Development | [email protected]

poStmAStErSend address changes to Credit Union Digest, P.O. Box 51476, Ontario, CA 91761-0076. Single issues are available: Call 909.212.6044

The California and Nevada Credit Union Leagues reserve the right to edit letters to the editor and all submissions. The Leagues do not take responsibility for the return of unsolicited materials. For more information, contact Editor-in-Chief Carol Payne at 909.212.6040.

Credit Union Digest is printed on recycled paper.

©2012 California and Nevada Credit Union LeaguesUSPS 011-679

credit union

Providing Innovative Support and Services to Member Credit Unions Since 1933.

Winner:• 2012 CUNA/AACUL Pro and Blockbuster Honorable Mention• 2012 and 2011 Communicator Award of Distinction• 2011 CUNA/AACUL Pro and Blockbuster Award

CALiforniA LEAGuE offiCErS

President Diana R. Dykstra | 909.212.6001 | [email protected] Secretary Sharon Weber | 909.212.6003 | [email protected]

Treasurer Cindy Cavanaugh | 909.212.6006 | [email protected]

CALiforniA LEAGuE ExECutivE CommittEE

Chairman Teresa Halleck | 858.597.8690 | [email protected]

1st Vice Chairman Larry Palochik | 909.809.3608 | [email protected]

2nd Vice Chairman Teresa Freeborn | 310.607.2075 | [email protected]

Committee Member Jon Hernandez | 310.371.4242, ext. 217 | [email protected]

Committee Member Hank Barrett | 209.549.8511, ext. 3000 | [email protected]

Ex-Officio Eileen Rivera | 310.491.7601 | [email protected]

CALiforniA LEAGuE boArd of dirECtorS

At-Large Director Hank Barrett | 209.549.8511, ext. 3000 | [email protected]

At-Large Director Jim Updike | 310.217.8655 | [email protected]

At-Large Director Larry Palochik | 909.809.3608 | [email protected]

At-Large Director Eileen Rivera | 310.491.7500 | [email protected]

District 1 Director Ron Seaman | 916.979.7233 | [email protected]

District 2 Director Barry Nelson | 707.469.1678 | [email protected]

District 3 Director | Vacant

District 4 Director | Vacant

District 5 Director Teresa Freeborn | 310.607.2075 | [email protected]

District 6 Director Linda Walmsley | 888.800.3328 | [email protected]

District 7 Director Roger Ballard | 714.375.8001 | [email protected]

District 8 Director Charles Papenfus | 909.822.1810, ext. 215 | [email protected]

District 9 Director Marla Shepard | 858.636.4221 | [email protected]

Group A Director Chris Coursen | 714.641.5946, ext. 12 | [email protected]

Group B Director Jon Hernandez | 310.371.4242, ext. 217 | [email protected]

Group C Director Rick Hanan | 510.483.1300 | [email protected]

Group D Director Teresa Halleck | 858.597.8690 | [email protected]

CunA boArd mEmbErS

Jeff York* | 805.733.7640 | [email protected]

Brett Martinez* | 707.576.5101 | [email protected]

nEvAdA LEAGuE boArd of dirECtorS

Chairman Dennis Flannigan | 775.789.3108 | [email protected]

Vice Chairman Wayne Tew | 702.939.3020 | [email protected]

Secretary Wallace Murray | 775.882.2060 | [email protected]

Treasurer Douglas Schwartz | 702.397.6949 | [email protected]

Director Barbara Reuter | 775.945.2421, ext. 4013 | [email protected]

Director Eric Estes | 702.293.7772, ext. 183 | [email protected]

Director | Open

* Ex-Officio California League Board Member

5credit union digest | august/september 2012 | members first

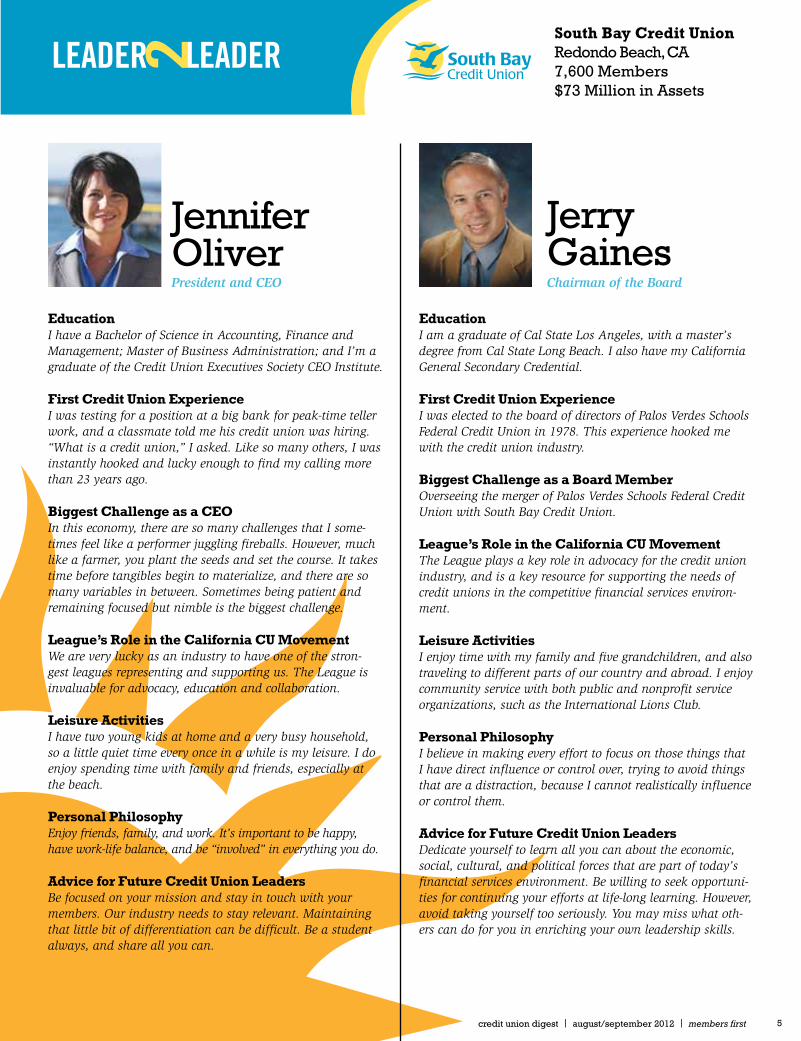

2 South bay Credit unionRedondo Beach, CA7,600 Members$73 Million in Assets

LEADER LEADER

EducationI am a graduate of Cal State Los Angeles, with a master’s degree from Cal State Long Beach. I also have my California General Secondary Credential.

first Credit union ExperienceI was elected to the board of directors of Palos Verdes Schools Federal Credit Union in 1978. This experience hooked me with the credit union industry.

biggest Challenge as a board memberOverseeing the merger of Palos Verdes Schools Federal Credit Union with South Bay Credit Union.

League’s role in the California Cu movementThe League plays a key role in advocacy for the credit union industry, and is a key resource for supporting the needs of credit unions in the competitive financial services environ-ment.

Leisure ActivitiesI enjoy time with my family and five grandchildren, and also traveling to different parts of our country and abroad. I enjoy community service with both public and nonprofit service organizations, such as the International Lions Club.

personal philosophyI believe in making every effort to focus on those things that I have direct influence or control over, trying to avoid things that are a distraction, because I cannot realistically influence or control them.

Advice for future Credit union LeadersDedicate yourself to learn all you can about the economic, social, cultural, and political forces that are part of today’s financial services environment. Be willing to seek opportuni-ties for continuing your efforts at life-long learning. However, avoid taking yourself too seriously. You may miss what oth-ers can do for you in enriching your own leadership skills.

President and CEO

JenniferOliver

Chairman of the Board

EducationI have a Bachelor of Science in Accounting, Finance and Management; Master of Business Administration; and I’m a graduate of the Credit Union Executives Society CEO Institute.

first Credit union ExperienceI was testing for a position at a big bank for peak-time teller work, and a classmate told me his credit union was hiring. “What is a credit union,” I asked. Like so many others, I was instantly hooked and lucky enough to find my calling more than 23 years ago.

biggest Challenge as a CEoIn this economy, there are so many challenges that I some-times feel like a performer juggling fireballs. However, much like a farmer, you plant the seeds and set the course. It takes time before tangibles begin to materialize, and there are so many variables in between. Sometimes being patient and remaining focused but nimble is the biggest challenge.

League’s role in the California Cu movementWe are very lucky as an industry to have one of the stron-gest leagues representing and supporting us. The League is invaluable for advocacy, education and collaboration.

Leisure ActivitiesI have two young kids at home and a very busy household, so a little quiet time every once in a while is my leisure. I do enjoy spending time with family and friends, especially at the beach.

personal philosophyEnjoy friends, family, and work. It’s important to be happy, have work-life balance, and be “involved” in everything you do.

Advice for future Credit union LeadersBe focused on your mission and stay in touch with your members. Our industry needs to stay relevant. Maintaining that little bit of differentiation can be difficult. Be a student always, and share all you can.

Jerry Gaines

6 credit union digest | august/september 2012 | members first

new

s &

vie

ws IRR: CUs Reveal Their

Game Plan how is your credit union complying with nCuA’s interest rate risk regulation?

By Sept. 30, almost half of all U.S. credit unions must have a “writ-ten policy on interest rate risk (IRR) management and a program to implement it effectively.” That’s according to the National Credit Union Administration’s finalized regulation, one that’s stirred controversy since inception.

Whether or not executives agree the rule is fair or proper strategy, the agency’s field examiners will soon be keeping tabs on this area of management, which has prompted many credit unions to act accord-ingly. While the Federal Reserve says it expects to keep rates “low” until

priority one CuCFO: Saeid RaadAssets: $158 millionMembers: 30,000Headquarters: South Pasadena, CA

I’m not bothered by the fact that NCUA is creating more work for us. They’re opening the door for us to have broader policy language in place to effectively deal with interest rate risk. They’re thinking ahead as opposed to reacting to a situation after it’s too late. The challenge is not with NCUA, it’s trying to manage uncertainty in the world we live in.

About 45 percent of our loan portfolio is composed of mortgages. We’re reviewing our policy and procedures, testing some shock scenarios and income simulations, and looking at what’s required in the actual regulation. This is probably what we as an industry should have done with regard to credit risk during 2004 through 2006.

It’s a welcome sign to see the regulators offering some leeway in terms of the kind of instruments we can use for hedging risk. They may eventually allow us to use derivatives, such as adjustable-rate mortgages from Fannie Mae or Freddie Mac or other investments. I’m interested to see how that’s going to play out in the credit union industry, which is by and large conservative when it comes to investing. If your credit union can effectively hedge, you may be just fine.

I don’t think there’s a credit union that’s not feeling weighed down by the pace and level of increased regulations, especially when the economy has required keen expense control and there is less money available to hire internal resources to implement expanding regulations.

That being said, I can also understand the regulator’s sense of urgency to avoid having a second “risk bubble” bursting when interest rates are bound to increase, especially on the heels of the credit risk crisis.

SESLOC has a good part of the requirements addressed in our existing IRR management policy. But with limited internal resources, we will have to rely on outsourcing with a third party, ALM First, to help us review our policy and ensure our modeling is meeting full compliance. We also will be working with our audit firm on the internal controls for our IRR program.

I know in the long run the credit union will be in better shape for strengthening our analysis and contingency planning, even though it is burdensome right now.

The National Credit Union Administration’s interest rate risk regulation affects federally insured credit unions with more than $50 million in assets, and those between $10-50 million holding a certain number of first mortgages and longer-term investments. The following resources may help credit unions as they write or update their policies:

• NCUA’sMay2012LettertoCUsandIRRExaminationQuestionnaire—www.ncua.gov/Resources/Pages/LCU2012-05.aspx

• FinalIRRRuleandNCUACommentary(theFederalRegis-ter)—www.ncua.gov/Legal/Documents/Regulations/FIR20120126InterestRateRiskProg.pdf

• CaliforniaandNevadaCreditUnionLeagues’May2011Comment Letter—http://members.ccul.org/05research/comments/2011/11_0520CANVCommentsPart741IRR.pdf

IRR Resources

SESLoC fCuCEO: Geri LaChanceAssets: $530 millionMembers: 33,500Headquarters: San Luis Obispo, CA

7credit union digest | august/september 2012 | members first

L.A. financial fCuCFO: David EbersteinAssets: $345 millionMembers: 35,500Headquarters: Pasadena, CA

Greater nevada CuCEO: Wally MurrayAssets: $443 millionMembers: 48,300Headquarters: Carson City, NV

CommonWealth Central CuCEO: Craig WeberAssets: $328 millionMembers: 35,700Headquarters: San Jose, CA

We’ve been following an interagency advisory on interest rate risk management, which basically states that when interest rates go up or down, you’ll want to know what’s happening to your credit union’s net worth. In March of 2011 we started performing simulations over five years to determine the impact to net income when rates change, which translates into what’ll happen to our net worth ratio.

We also started a seven-year simulation this past March as opposed to a five-year simulation. We’re testing 11 different interest rate risk simulations, with seven of them focused on rising rates. When rates rise, you see a negative impact to net worth, but if you look far enough ahead, the earnings turn around and your net worth actually improves. Margins will get squeezed for a time, but over a longer period, margins will rise again. In addition to this, we’re maintaining a static balance sheet so we don’t mask interest rate risk through growth.

We used to only simulate net interest income over 12 months in a rising rate environment, but we’ve changed our IRR policy to focus on how to maintain our credit union’s “well capitalized” distinction if interest rates rise.

late 2014, NCUA is forecasting potential balance sheet risk when rates finally rise. One measurement the regulator uses—the ratio of first mortgages and investments with maturities exceeding five years to net worth—rose from 199 percent in December 2005 to a “peak” of 271 percent in March 2011 at federally insured credit unions nationwide, the regulation’s preface states.

Several credit unions are test-ing 400-500 basis point “shock” sce-narios rather than the “standard 300,” according to an April 2012 white paper published by the Credit Union National Association’s CFO Council. “The NCUA’s

continued scrutiny of interest rate risk is just one indicator of its continued relevance,” it states. “Credit unions need to be able to show they are forecast-ing and planning for a vastly different interest rate environment than what we have now, which may justify testing for bigger shocks than in the past.”

Due to their size, some larger credit unions have only needed to “tweak” the interest rate component of their asset liability management policy, said Chris Collver, senior regulatory and legislative analyst for the California and Nevada Credit Union Leagues. Other credit unions—whether small, medium, or

large—have spent hours of preparation because of staff restraints or the sheer number of balance sheet items tied to interest rate volatility.

What’s helpful is the revised examination questionnaire NCUA made available in May. “A credit union can know ahead of time what the examiner is supposed to be looking for,” Collver said. “The question for this regulation, as with many areas these days, is whether exam-iners will stick to the parameters of the rule and the questionnaire, or if they’ll wander into the over-used and restrictive ‘best practices’ approach.”

We’ve been digging into the specifics of the new rule, but we’ve had an interest rate risk policy and program in place for a number of years that we think meets the general guidelines.

We’re performing quarterly interest rate risk analyses, modeling many interest rate and yield curve scenarios, including changes of 300 and 500 basis points. We look at what happens to net worth when interest rates stay at the shock levels for about four years out, since that’s when a majority of our existing balance sheet would run off. The majority of our long-term assets that have maturities greater than five years are mortgage loans.

It makes sense to look at this in the low-rate environment we are in because of what interest rates are eventually likely to do. The Fed’s extended low-rate forecast could be correct—however, it is not certain. It’s not something we want to bet on.

Although Greater Nevada Credit Union will be subject to the new interest rate risk rule, we anticipate it will largely be a non-event for us. Our credit union recognized a long time ago that it carries significant amounts of fixed-rate longer term assets on its balance sheet. Our board of directors and management team have been addressing each of the five areas outlined within the new rule for a number of years.

We also occasionally bring in outside consultants to conduct IRR- related training for the members of our asset liability committee, which consists of both board members and management staff. In addition, we have an internal process in place for periodically reassessing the assumptions used in our IRR model.

As a result, our overall IRR has been within the low-to-moderate range for quite some time. While the new rule may require us to do a little bit of tweaking to what we already have in place, we do not believe that complying with it will be burdensome.

8 credit union digest | august/september 2012 | members first

shapiro perspective

By Deanne Figueras, Manager of CU Growth

Shapiro Group Celebrates 20 Years

"I look at credit unions as little lighted candles all spread over our great country. These

candles are lighting the way for people to better themselves, not only from an economic standpoint, but from a spiritual standpoint."

Decades after California's financial cooperative pioneer Leo Shapiro said these words, the group based on his phi-losophy is celebrating its 20th anniversary of pooling the resources of the credit union community to help small credit unions operate efficiently and effectively.

1992—beginningsThe California Credit Union League establishes The Shapiro Group to give small credit unions the resources they need to thrive. In 1991, League President and CEO David Chatfield visits Leo Shapiro to discuss the specific needs of smaller credit unions. The group was named in honor of this San Francisco attorney who became a dynamic force in assisting credit unions through political and legal challenges. He eventually became known as “the father of the California credit union movement.”

California credit union pio-neer Leo Shapiro and Dave Chatfield, President and CEO of the California Credit Union League

1993-1995—donations, Awards, and EducationThe Shapiro Group quickly becomes a catalyst for chan-neling donated equipment to Shapiro credit unions, such as computers. In addition, to meet the need for Truth in Savings (TIS) education, the first Shapiro Issues Forum was launched with the help of several individuals and organizations, leading to the creation of the Eternal Flame Award, honoring them for their contributions. The award was renamed the Kim Bannan Eternal Flame Award in 2004 to recognize Bannan for her contributions to the advancement of The Shapiro Group.

1996-1997—Group reaches out to CusA "Small Credit Union Guide" and various grassroots grants are created, along with the Chapter Networking Fund. The fund was started to establish networking groups or other appropriate outreach and programing efforts that would assist Shapiro credit unions within each chapter.

1998—Community investment fund (Cif) CreatedThe CIF was formed to provide an investment opportu-nity for California and Nevada credit unions to enhance the entire credit union movement and give Shapiro cred-it unions and the Richard Myles Johnson Foundation a new source of revenue. Today, CIF proceeds provide for Shapiro credit union grants that help with the costs of asset liability management, marketing, technology, strategic planning, and advocacy efforts.

1999-2002—Grants meet technology needsThanks to the newly established E. Roy Higgins Small Credit Union Technology Fund, which was started with a $10,000 donation by The Golden 1 CU, grants were now available to Shapiro credit unions for technology purposes. The Golden 1 CU donated an additional $25,000 in 2001, 2002, and 2003, provid-ing a total of $85,000. Overall, 124 grants for various operational needs topping $138,000 were provided to Shapiro credit unions from the industry.

2006—Cu partners for AdvocacyThanks to the generous support of larger member credit unions and business partners, the Credit Union Partners for Advocacy program was created to help those with less than $34 million in assets attend the Credit Union National Association's annual Governmental Affairs Conference in Washington D.C., without having to use grant funds.

Linda White, CEO of Unit-ed Health CU, and Barry Jolette, President and CEO of San Mateo CU

Here, we take a look back at The Sha-piro Group's journey, and the pivotal points in history that came to define its core val-ues.

9credit union digest | august/september 2012 | members first

2008—Shapiro Group Cu Summit LaunchedThe first annual summit kicks off with a one-day edu-cational session designed specifically for Shapiro credit unions. It draws 49 credit union professionals from throughout California and Nevada.

CalCom FCU CEO Jon Her-nandez and the Shapiro Advisory Committee lead a breakout session on technology and delivery channels during the first Shapiro Group Credit Union Summit.

2011—first Cathy Arra memorial Scholarship AwardedKetema FCU CEO Lorna Stafford-Bentley is the first Cathy Arra Memorial Schol-arship awardee, which was created in remembrance of the Leagues’ former Manager of CU Growth Cathy Arra for her integral role in the creation of the Shapiro Group Credit Union Summit. The $250 scholarship helps small credit union CEOs defer the summit’s costs, and will be available for the next 10 years.

L-R: Diana Dykstra, President and CEO of the California and Nevada Credit Union Leagues; Lorna Stafford-Bentley, CEO of Ketema FCU and award recipient of the first Cathy Arra Memorial Scholarship, and Eric Bruen, President and CEO of Desert Valleys FCU

2011—Survey Sparks regulator dialogueThe Shapiro Advisory Committee launches a survey of small credit unions, which reveals significant trends in credit union examina-tions by regulators and sparks an expanded survey of all League members. The larger survey is used to relay concerns about regulatory practices on medium and large credit unions to the federal and state regulatory bodies.

1992: $12 million 2005: $33 million 1999: $18 million 2012: $45 million 2001: $23 million

Median Asset Size of Shapiro CUs:

Cathy Arra, former Man-ager of CU Growth for the Leagues

10 credit union digest | august/september 2012 | members first

advocacy

Rep. Brad Sherman, D-CA, has been an outstanding leader for credit unions during his

congressional tenure. He serves as a member of the House Committee on Financial Services, as well as the House Committee on Foreign Affairs.

Sherman is the leading democratic co-sponsor of legislation to allow credit unions access to supplemental capital (HR 3993), and has co-sponsored and authored dozens of bills to improve the quality of operations at credit unions. He is an amazing supporter of credit unions, and he truly understands the industry’s cooperative structure and spirit.

The congressman recently sat down for an interview to discuss the credit union industry’s issues and how the movement can better advocate on behalf of its members. Credit unions are encouraged to repost this interview in membership newsletters.

What is it about credit unions that made you want to champion our issues before Congress?

As soon as I got to Congress in 1997 and began serving on the finan-cial services committee in 1998, I had the privilege of getting to know and working with credit union activists from around the country. Through that process, I became a strong supporter of the member-owned, nonprofit, coop-erative credit union structure because of the benefits it provides for working people to pool their assets and pro-vide one another with great value at minimal cost. All credit union mem-bers I know are proud to talk about their credit union and the services they enjoy—that’s not something you often hear about the big banks.

By Jeremy Empol, Director of Federal Government Affairs

Congressman Highlights CU Difference

As a member of the House Financial Services Committee, how do you view the role of committee members in ensuring credit unions have the opportunity to survive these tumul-tuous times?

We’ve been hearing one message consistently in the financial services committee since the economic down-turn began: credit unions are ready and eager to use their capital to help sustain the recovery. All we’ve been try-ing to do is get the government out of the way. This year I took the lead with fellow committee member Peter King of New York to introduce HR 3993, the Capital Access for Small Business and Jobs Act, which gives credit unions the ability to access supplemental forms of capital. The bill allows financially healthy credit unions to react to market conditions and use alternative sources of capital to support net worth. It doesn’t cost taxpayers a dime, and it helps ensure that credit unions are able to continue lending in tough economic times.

With House and Senate hearings having taken place on member busi-ness lending, and Senate Majority Leader Harry Reid’s commitment to hold a vote, what are the chances of passing HR 1418 as either a stand-alone bill or attachment to a broader package?

Member business lending has been a priority for years, and in this Congress we made great progress in building momentum behind the bill. With time winding down and lim-ited opportunities to pass standalone legislation, I think our best bet is to use the massive bipartisan support behind the bill to attach it to one of the broad

“must-pass” pieces of legislation that Congress will have to take up by the end of this year. I’m working with our allies to make that happen.

Is there anything you’d like to men-tion to credit union CEOs, employees, board members, and volunteers?

Let me tell you why you’re suc-cessful when you’re up against the big goliaths from Wall Street, and give you a little political science lesson. From time to time, members of Congress get a chance to pose for pictures with board members of credit unions, and they do so eagerly because they know these photos will be published in newsletters to their members. Members of Congress know that people will stop them in the supermarket to say “thank you” for supporting credit unions. Now imag-ine, if you will, a chance to have their picture in something mailed out with bank statements. Members of Congress might not know everything, but they know who to get their picture taken with.

Rep. Brad Sherman, D-CA

11credit union digest | august/september 2012 | members first

Staff, Social Media, and Free SpeechBy Thomas H. Wolfe of Moore Brewer Wolfe Jones Tyler & North

legal

In the recent case of Summit Bank v. Rogers,1 the California Court of Appeal dismissed Summit Bank’s defamation claim against Robert Rog-ers, a former employee who posted negative comments on an Internet message board. Rogers’ anonymous posts criticized the CEO, bank’s safety and soundness, and customer service, and encouraged readers to move their accounts.

The bank brought a defamation action against Rogers, who moved to strike the complaint under California’s “anti-SLAPP” statute2 on the grounds it was brought primarily to chill the valid exercise of his constitutional right of free speech regarding a matter of public interest. The trial court denied the motion, but the Court of Appeal reversed and dismissed the bank’s claim.

The court uses a two-step process to consider an anti-SLAPP motion: first, a defendant must meet a thresh-old showing that the challenged cause of action arises from protected activ-ity; and second, the plaintiff must be unable to demonstrate a probability of prevailing on the claim. However, if the protected speech or activity is illegal “as a matter of law,” it is not subject to anti-SLAPP protection.

illegal ‘as a matter of Law’The bank argued that Rogers’ state-

ments were illegal as a matter of law because they violated Cal. Fin. Code §1327, which makes it a misdemeanor to willfully and knowingly make, circu-late, or transmit any untrue derogatory statement about the financial condition of a bank, or that affects its solvency or financial standing.3

To determine whether allegedly protected speech is illegal as a matter of law, the court had to first consider the statute being relied upon for the claim of illegality. Conduct that would otherwise be covered by the anti-SLAPP

statute does not lose its protection simply because it is alleged to have been unlawful.

In considering §1327, the Court of Appeal made the sur-prising move of finding the nearly 100-year-old statute a prohibited content-based restriction on speech in violation of state and federal con-stitutional protections. Under modern civil and criminal defamation law, a claim-ant must demonstrate actual malice, (knowledge that a statement is false, or reckless disregard of whether it was false or not).

The court noted that §1327 con-tains no malice element and found it both overly broad and vague. As drafted, anyone who questions the financial strength and stability of the banking system, or even suggests that a bank is financially unstable, could be subject to criminal liability. Even if Rogers’ speech violated §1327, it cannot be illegal as a matter of law because §1327 cannot provide the foundation for losing anti-SLAPP stat-ute protections.

protected ActivityThe court also found that Rogers’

posts were an act in furtherance of his constitutional right of free speech in connection with “an issue of public interest” under Cal. Code of Civ. Proc. §425.16(e)(3), part of the anti-SLAPP protections. Internet message boards are a public forum, and courts have previously held that posts about cor-porate activity are an issue of public importance. The financial stability of the banking system is a legitimate object of constitutionally protected pub-lic commentary, discussion, criticism, and opinion.

Likelihood of SuccessTo defeat the anti-SLAPP motion,

the bank had to show a probability of success on the merits of its defamation claim. To constitute defamation, a state-ment must contain a provable false-hood. Opinions are protected as long as they don’t include a false assertion of fact. The court observed that Internet blogs and message boards are places where readers expect to see strongly worded opinions rather than objective facts, and they must be viewed from the perspective of the average reader. As such, the bank failed to show a probability of success on the merits.

for Credit unionsWhile social media policies can be

useful, employers must be careful not to overreach. Credit unions are encour-aged to work closely with legal counsel to craft a policy that prohibits unlawful conduct, such as harassment, defama-tion, and privacy violations, but does not attempt to censor protected speech.

1 Summit Bank v. Rogers, No. , A129800, 2012 Cal. App. LEXIS 633 (Cal. Ct. App. May 29, 2012).2 A Strategic Lawsuit Against Public Participation (SLAPP) is a lawsuit brought for the purpose of censoring or intimidat-ing persons attempting to exercise their constitutional right of petition or free speech. California’s “anti-SLAPP” statute, Cal. Code of Civ. Proc. §425.16, allows a SLAPP defendant to bring a special motion to strike unless the plaintiff can demonstrate a probability of success on the merits.3 Cal. Fin. Code §14051 contains a similar prohibition ap-plicable to California credit unions.

12 credit union digest | august/september 2012 | members first

feature

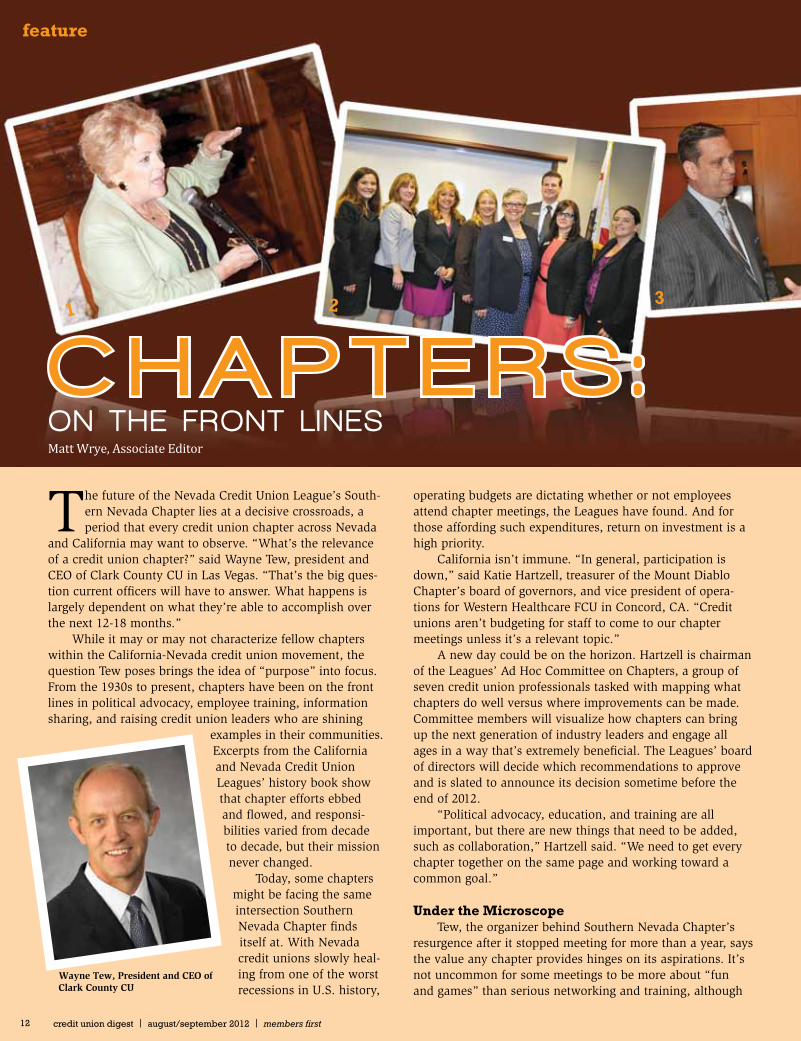

The future of the Nevada Credit Union League’s South-ern Nevada Chapter lies at a decisive crossroads, a period that every credit union chapter across Nevada

and California may want to observe. “What’s the relevance of a credit union chapter?” said Wayne Tew, president and CEO of Clark County CU in Las Vegas. “That’s the big ques-tion current officers will have to answer. What happens is largely dependent on what they’re able to accomplish over the next 12-18 months.”

While it may or may not characterize fellow chapters within the California-Nevada credit union movement, the question Tew poses brings the idea of “purpose” into focus. From the 1930s to present, chapters have been on the front lines in political advocacy, employee training, information sharing, and raising credit union leaders who are shining

examples in their communities. Excerpts from the California and Nevada Credit Union Leagues’ history book show that chapter efforts ebbed and flowed, and responsi-bilities varied from decade to decade, but their mission never changed.

Today, some chapters might be facing the same intersection Southern Nevada Chapter finds itself at. With Nevada credit unions slowly heal-ing from one of the worst recessions in U.S. history,

operating budgets are dictating whether or not employees attend chapter meetings, the Leagues have found. And for those affording such expenditures, return on investment is a high priority.

California isn’t immune. “In general, participation is down,” said Katie Hartzell, treasurer of the Mount Diablo Chapter’s board of governors, and vice president of opera-tions for Western Healthcare FCU in Concord, CA. “Credit unions aren’t budgeting for staff to come to our chapter meetings unless it’s a relevant topic.”

A new day could be on the horizon. Hartzell is chairman of the Leagues’ Ad Hoc Committee on Chapters, a group of seven credit union professionals tasked with mapping what chapters do well versus where improvements can be made. Committee members will visualize how chapters can bring up the next generation of industry leaders and engage all ages in a way that’s extremely beneficial. The Leagues’ board of directors will decide which recommendations to approve and is slated to announce its decision sometime before the end of 2012.

“Political advocacy, education, and training are all important, but there are new things that need to be added, such as collaboration,” Hartzell said. “We need to get every chapter together on the same page and working toward a common goal.”

under the microscopeTew, the organizer behind Southern Nevada Chapter’s

resurgence after it stopped meeting for more than a year, says the value any chapter provides hinges on its aspirations. It’s not uncommon for some meetings to be more about “fun and games” than serious networking and training, although

C H A P T E R S:ON THE FRONT L INESMatt Wrye, Associate Editor

Wayne Tew, President and CEO of Clark County CU

12 credit union digest | august/september 2012 | members first

1 2 3

13credit union digest | august/september 2012 | members first

feature

there’s a time and place for prize giveaways, parties, and socializing when appropriate.

That wasn’t the reason Southern Nevada “went dark.” Earnings and net worth at a handful of chapter-engaged credit unions in the region fell so fast during the last reces-sion that conservatorships and mergers were only a mat-ter of time. “Participation at chapter meetings pretty much died,” Tew said. Local credit unions healing from their steep descents are still dealing with a lackluster real estate mar-ket and high unemployment, putting the pinch on funds for employee activities outside the office.

Against those odds, Tew reached out to local credit union CEOs and the Leagues to see if there was interest in getting the chapter back online. “I think credit unions—particularly in Nevada where so few of us are left—need to have a few points of visibility and commonality for the broader com-munity and legislative purposes,” he said. “One thing we’re trying to do is have a purpose instead of just getting together for food and drinks. It’s about promoting a greater awareness of credit unions.”

As of early summer, the verdict wasn’t in on whether Southern Nevada should keep meeting or dissolve, Tew said. The chapter is coming together once every quarter, and it might schedule more meetings if more people start show-ing up. The conundrum is, meetings are “most relevant” for smaller credit unions, where chances of involvement are slim due to their “overwhelming day-to-day burdens.” On the other hand, larger credit unions “do a lot of things on their own, and don’t necessarily want that extension with other institutions,” Tew said.

The renewed undertaking may prove successful. Tew gives accolades to the chapter’s board of governors and Board Presi-

dent Judy Clark, vice president of operations for Clark County CU, for reinvigorating attendance. He noted the board’s work in securing a visit from Las Vegas Mayor Carolyn Goodman at June’s meeting, which gave local credit union executives the chance to shake hands with a public official.

“They’ve done a good job so far,” Tew said. “Is there rel-evance in continuing to meet more often? That’s what we’re trying to figure out.”

‘prepared and Strategic’It wasn’t necessarily Tony Strickland’s tall stature and

big smile that brought more than 50 credit union employees and business partners to the San Fernando-Antelope Valley Chapter’s April meeting at the Hilton Hotel in Glendale, CA. It was his public status.

Towering above his podium and donning a light gray pin-stripe suit, the California state senator and congressional republican candidate talked about the “discipline” he learned

1: Carolyn Goodman, Mayor of Las Vegas, speaks in June at a Southern Nevada Chapter meeting; 2: California and Nevada Credit Union Leagues President and CEO Diana Dykstra (fourth from right) with Teresa Halleck (left of Dykstra), Chairman of the California Credit Union League and President and CEO of San Diego County CU, and board of governors for the Orange County Chapter; 3: California State Senator Tony Strickland discusses credit union issues with John Dea, President and CEO of Los Angeles FCU, at a San Fernando-Antelope Valley Chapter Meeting; 4: The California and Nevada Credit Union Leagues’ Ad Hoc Chapters Committee (L-R): Marina Miller, Legal Manager for SchoolsFirst FCU; Jeanine Dodman, VP of Branch Networks for Mission FCU; Jason Mertz, Senior Accounting and Operations Representative for MY CU; Alan Ricard (back center), Business Development Coordinator for Alta Vista CU; Katie Hartzell (font center), Committee Chairman and VP of Operations for Western Healthcare FCU; Nancy Johns, Branch Manager for American Airlines FCU; Dawn McGhauey, Director of Human Resources for Financial Horizons CU; and Tracy Vasilia, Manager of Chapters and Electronic Education for the Leagues; 5: Ad Hoc Chapters Committee members brainstorm ideas during their first face-to-face meeting held in May at the Leagues’ headquarters in Ontario, CA.

13credit union digest | august/september 2012 | members first

4 5

featureas a child from his father, a Vietnam War veteran,

before transitioning into his com-mitment to giving credit unions “everything they need” for supporting their communities. With a higher than average number of credit union executives sitting in the room, this wasn’t your average chapter meeting.

“It took six months of planning to get the sena-

tor there,” said Marvel Ford, chapter president and first vice president and risk manage-ment officer for California CU in Glendale. “Putting these types of

meetings together aren’t easy. You have to be prepared and strategic from the very beginning.”

Meetings like this receive “awesome feedback,” Ford said. Organizing them is hard work, but they draw credit union executives and board members in addition to down-the-line staff who regularly attend. She said sometimes the trick to increasing attendance is using the “star power” card. Chapters can only secure a public official or engaging speaker so many times per year, but once a chapter captures its audience’s attention from a single event, it can use that stepping stone to plug upcoming meetings, training sessions, and fundraisers.

“One focal point is, we’re not going to have meetings just for the sake of filling up our calendar,” Ford said. “We’re also asking for feedback to determine if we’re moving in the right direction. You have to pay close attention when you do your strategic planning for the year. I think it helps reinvigo-rate what we do so we don’t get stale.”

She said chapters need to tailor training to the environ-ment their credit unions are operating in. Face-to-face meet-ings are important, not necessary. Webinars can fulfill training needs just as well, if not better, in certain circumstances.

The value factor should also be considered since “some CEOs don’t think spending 40 or 50 dollars every month is worth sending an employee.” Credit union workers “need to return to their CEOs say-ing, ‘This was a great event with a great topic’,” Ford said. During chapter events, she takes the pulse of how people feel. “When you see hands going up to ask questions, and people don’t care if the speaker goes 15 min-utes late, that tells me it was successful.”

If a proposed decision to merge the San Gabriel Valley Chapter into Ford’s San Fernando-Antelope Valley Chapter is approved later this year by the California Credit Union League Board of Directors, the move would create the largest California chap-ter, with 61 member credit unions, eclipsing the Los Angeles Chapter. Even at the chapter’s current size, its board mem-bers couldn’t accomplish their objectives if it wasn’t for their sense of teamwork.

“I definitely look to them to step up. You have to keep them involved and make them accountable,” Ford said. “You can’t do things without them feeling and knowing they’re important. They have to have a voice.”

‘A Change in the times’Chapters have evolved since the Great Depression, and

today doesn’t mark the first time their usefulness has been questioned. Documented stories in the Leagues’ history book point to at least one fact: they’re an ongoing work in process. A League survey in the late 1960s revealed that social func-tions—good food, conversation, and laughter—were “top-rated” programs for chapter-goers.

“That was a far cry from the 30s’ and 40s’, when the men who ran credit union chapters depended on chapters to teach them the most basic functions of credit union opera-tions,” states one account. In fact, a few chapters were already in existence when the League formed in 1933. As time passed, some organizers “weren’t always sure what to do” at meetings. “Clearly, the chapters met (credit unions’) various needs to varying degrees.”

Al George remembers those days quite well. The retiree and board member for San Diego, CA-headquartered North Island CU attended his first San Diego Chapter meeting in 1948, the same year he joined his employer’s credit union, San Diego Gas and Electric CU, and was recruited on the board of directors. It was the beginning of a long journey in the credit union movement. He eventually held positions as board member and chairman of the California Credit Union League, board member and chairman of the Credit Union National Association, and board member for the World Coun-cil of Credit Unions.

“Chapters should be on the front lines in relation to advocacy and the social networking, but I don’t see how they can be on the front lines when it comes to education,” he said. “There are just too many opportunities elsewhere.”

George recalls a heavy exchange of ideas in those early chapter days about the equipment credit unions used in operations, and which brands worked well. “Business machines” fulfilled many of the functions today’s com-puters, software programs, and cloud com-puting are responsible for. Employees also learned about credit union operations and trends in the movement since they were too busy during the workday to dive into those details.

Today’s scene is “neither good nor bad—it’s just a change in the times,” he said. “Executives and managers no lon-ger need person-to-person communica-tions to tell them how to run their shop.” Over the past six decades, the vitality and importance of chapters were questioned several times, with multiple committees

banding together to target areas that could be enhanced. “In some cases, it was questioned whether we should even con-tinue with chapters. Some people thought we had outlived our usefulness, and some think the same to this day.”

14 credit union digest | august/september 2012 | members first

Marvel Ford, FVP and Risk Management Officer for Califor-nia CU, and President of the San Fernando-Antelope Valley Chapter Board of Governors.

Al George, Board Member for North Island CU

feature

‘We’re Here to Make an Impact’ With more than 50 “likes” on Santa Clara Valley Chapter’s Facebook page, Payge Lyn is shooting for at least 50 more.

“We want to keep the momentum going, and raise more awareness,” Lyn said. “Sometimes chapter meetings are the only time we get to network with other credit union employees. Otherwise, we wouldn’t see them.”

At 31, Lyn is information chair for her chapter’s board of governors, and one of Santa Clara Valley’s youngest members. The financial service representative for Meriwest CU, a $1 billion asset credit union in San Jose, CA, said participating in meetings is essential for any credit union employee looking to increase his or her value to the industry, as well as credit union members.

“My perspective has changed big time since I became more involved in the chapter,” said Lyn, who’s been working in the industry for 10 years. “I’m more informed on how credit unions work, and I’m up to date on the latest industry information. It also gives you a greater respect for other credit unions in your region.”

In her position, “getting out the word” on what her chapter provides every month is crucial, not only for interested credit union professionals, but vendors as well. She eventually wants to partner with vendors to raffle

George feels chapters are less important than they once were, but still play a necessary role. Meetings are still ripe with opportunity. “They give you a means of exploring each other’s minds to see if your peers have better ideas than you do,” he said. “To be able to sit and talk eyeball to eyeball with someone and share your experience—something blos-soms from that. The social aspect is as important as ever today to keep the credit union movement viable.”

Looking on the horizon“Get more CEOs involved.” It’s one of several fundamen-

tal ideas that stuck out from a group interview Credit Union Digest completed with the San Fernando-Antelope Valley Chapter Board of Governors on the future of chapters.

Technology is especially important to interacting with meet-ing attendees and offering training courses, as well as harness-ing the power of social media. Organizing events that credit unions will revere and applaud, all for a cost-effective price tag, was another area where priorities should be placed, they said.

One consensus was cooperation and leadership. “We need to integrate a sense of coordinated effort and collective

15credit union digest | august/september 2012 | members first

effectiveness in the area of reaching out to those we serve, and articulate the credit union difference in one voice,” said Board Governor Abiy Fikreslassie, who is also the lending and service center representative for SchoolsFirst FCU in Santa Ana, CA.

Pasadena-based L.A. Financial FCU Collections Manager and Board Governor Jared Falk said if chapters don’t adapt to the needs of credit unions, “even those credit unions with money” will look elsewhere for training opportunities. “It’s hard to generate credit union interest when some chapter boards cannot get their own board members interested,” he said. Serving on a chapter board should be a “prestigious accomplishment” for both the volunteer and credit union he or she works at.

With an eye toward the future, “we are always evolv-ing—and while our message never changes, the way we spread our message will always be adapting depending on the challenges we face,” Falk said. “We need to make sure that we have a consistent and relevant message and agenda that promotes credit union advocacy and education. We need to lift chapters back into a position of prominence.”

prizes on Facebook, and also let Facebook users RSVP for chapter meetings and regional learning centers.

Political advocacy plays a huge role when annual events come around, such as the California Credit Union League’s Government Relations Rally. “I’ll post pictures of us meeting with state senators and assembly members,” Lyn said. “I try to make it fun.”

She’s part of a growing demographic within the California and Nevada credit union industry that leverages social media—Facebook, Twitter, Google Plus, Tumblr, and Pinterest—to communicate to groups of people both inside and outside of credit unions, the Leagues have noticed. The popularity of such platforms has skyrocketed over the past few years, giving Lyn an easy way to update credit union employees on chapter events and efforts.

Her goal is to eventually utilize the full extent of what Facebook offers. There are credit union trends, hot topics, best practices, and operational basics that those working in the movement should know about, and furthering one’s knowledge starts by attending local chapter meetings, Lyn said.

“We can share ideas to help each other at the branch level,” Lyn said. “Chapters are still important because they serve as a future for all of us. If we didn’t have them, we wouldn’t be reaching out to people in the community, and we wouldn’t be aware of each other. We’re here to make an impact.”

Payge Lyn, Financial Service Representative for Meriwest CU, and Information Chair of the Santa Clara Valley Chapter Board of Governors

16 credit union digest | august/september 2012 | members first

economic perspective

The job market is improving, but continued improvement depends largely on two areas: growth in

exports, and higher stock prices. Higher stock prices are critical to keeping Cali-fornia’s technology boom alive.

The accompanying chart depicts the growth pattern in non-farm payrolls in California and Nevada from January 2011 to May 2012. It paints a nice pic-ture, but pay attention to the scale. The actual non-farm job gain for Nevada was 10,000, and for California it was 230,000. On a percentage basis of total jobs in each state, the gains are 0.8 percent and 1.6 percent, respectively. This is cer-tainly a disappointing recovery given the plunge in jobs, but it still represents a slowly improving labor market.

One employment area not depicted on the charts is agriculture. This sector is not significant for Nevada, but it is for California. Economists and the U.S. Bureau of Labor Statistics exclude agriculture jobs due to seasonality. But the agriculture season in California is year-round. Since January 2011, Califor-nia has added roughly 170,000 agricul-ture jobs, almost equal to the non-farm payroll gains.

Agriculture in California, as well as many other states, gets overlooked relative to the total economy. California’s recovery to date has been led by expan-sion in the trade and transportation sector, which has been driven by strong growth through California ports. The biggest single contributor to growth has been demand for California’s agricultural products. Prices surged over the past two years, and California farmers ramped up production. Being originally from a farming community, I can tell you that higher crop revenues spread throughout a community. The money gets spent.

The other area of growth is in “high tech.” Even though it has pro-duced more in the way of spendable income than actual jobs, spending has helped support gains in retail, hospital-

Dwight Johnston, Chief Economist

Why Ag, High-Tech, and Europe Matter

U.S. Bureau of Labor Statistics

ity, and leisure. Gains in high tech are also highly influential on the California state budget. In the most recent budget charade, a portion of the state’s short-fall was potentially “covered” based on Facebook’s assumed $35 initial-public-offering stock price, potentially contrib-uting $1.9 billion in tax revenue.

Beyond agriculture and technology, I recently attended Beacon Economics’ latest forecast forum, and also reviewed UCLA Anderson School of Manage-ment’s forecast—two highly watched events. While Beacon was certainly the more optimistic of the two, both groups are predicting steady growth. Both identified trade and high tech as key components. Those conferences were held before the European Union Summit in late June, but neither of the forecasting teams placed much emphasis on the events in Europe or the potential impact of a less-than-favorable outcome. I hate to differ with two such esteemed forecasting groups, but I will.

What happens in Europe is impor-tant to California and Nevada, as Europe’s economy has slowed signifi-cantly. The European Union’s economy is about the same size as the U.S. econ-omy. Based on the slowdown in Europe

to date, weakness is being noticed in China, Japan, Australia, Brazil, and other countries. While California’s trade business has been very strong, the growth has weakened substantially in the past two months.

Any European Union agreement that does not include some serious stimulus plans will fail. Austerity hasn’t worked for the past two years, and there’s nothing that will change that. To the extent the rest of the world slows, commodity prices would fall as demand shrinks, and the trade sector would no longer be a positive contributor. If the stock market falls, spending resulting from the technology sector would end. California would then face a shortfall, and more public-sector jobs would be on the chopping block.

However, if the European Union does “pull a rabbit out of the hat,” I believe the UCLA and Beacon experts will still both be wrong, and growth will exceed subdued expectations. Exports would perk up, and the boost in business confidence would be felt almost imme-diately. Moreover, I think the optimism would spread to builders and home buyers. We’re all tired of hearing about Europe, but it is a very big deal.

13900

14000

14100

14200

14300

Jan-

11

May

-12

1100

1110

1120

1130

1140

1150

California Nevada

1

Cal Nev

California and nevada non-farm payrolls

California Nevada

17credit union digest | august/september 2012 | members first

market performance

The good news is, total shares at U.S. credit unions (savings, checking, money market, and

certificate of deposit accounts) grew at an annualized pace to 7 percent through first quarter 2012, with regular shares (checking and money market-style accounts) growing at a 16 percent rate. Unfortunately, that’s bad news as well.

Normally this good news wouldn’t have a negative side, but these aren’t normal times. Annualized credit union loan growth across the nation was 2 percent in the same quarter, leaving the bulk of new shares to be turned over to investment portfolios. That’s where the trouble begins.

The recession—which California and Nevada are still in the process of dig-ging out from—brought a sea of change in credit union balance sheets. This is starkly demonstrated in loan-to-share ratios in both states. The ratio in Califor-nia has plunged from 85 to 60 percent, and investment portfolios are growing. The cost of funds typically drops more quickly than asset yields because credit unions, as well as other financial institu-tions, are liability-sensitive.

However, the cost of funds is rapidly approaching rock bottom, and current low-market yields mean that future maturing assets will be replaced at sharply lower yields. Consider the fact that the usual standard maximum investment for most credit unions is a five-year federal agency bond, and that yield is now less than 1 percent.

Compare the average-cost-of-funds chart to investment portfolio yields in the bottom chart. The spread between cost-of-funds and investment portfolio yields was relatively steady at 175-200 basis points until 2008. That spread is now down to roughly 50 basis points. The Federal Reserve is forecasting yields near these levels until late 2014. Should that scenario hold, the cost-of-funds/portfolio yield will be squeezed dry without some action on the part of credit unions.

Dwight Johnston, Chief Economist

Don’t Ignore the Big Squeeze

There is no magic elixir or one-size-fits-all answer. Based on preliminary data, it appears many credit unions since the beginning of the year have opted to let money stay in cash or near-cash investments and hope for a rise in rates. As you may have heard, hope is not a plan. Some credit unions view stay-ing in cash as the safest strategy in this low-rate environment. The fact is, this strategy is as much a forward bet on interest rates as it is a strategy of buying 30-year mortgages. Cash might prevent your portfolio from market value deterio-ration, but it could also destroy earnings if loan demand is dormant.

It seems logical that rates will rise some day, but when? Next month, or next year? Or maybe in the next 10 years? Japan has been mired in a low interest rate environment for almost 15 years.

Some credit unions have proactive and knowledgeable portfolio manag-ers, but expertise varies widely. Credit unions that have little experience need to fast-track on the learning curve, or they’ll get left behind. Some credit unions have either no time or the abil-ity to raise their employees’ level of investment knowledge to invest in more complex securities. And frankly, many boards of directors are simply unwill-ing to take on what they view as added risk. This means the answer for some credit unions is to push share rates even lower.

Growth of investments and com-pression of spreads is not easy for any credit union to manage, but ignoring it won’t make it go away. This should cer-tainly be an agenda item on every credit union’s strategic planning session.

1.00%

2.00%

3.00%

4.00%

5.00%

California Nevada

yield on investments

Source: Callahan and Associates, Inc.

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

California Nevada

Average Cost of funds

Source: Callahan and Associates, Inc.

18 credit union digest | august/september 2012 | members first

By Chris Collver, Senior Regulatory and Legislative Analyst

asked & answered

No Training Needed? Think Again

Asked: What training for a credit union’s staff or

board members is required by law or regulation?

Answered: There aren’t many training requirements spe-cifically stated in state and

federal laws, or regulations. However, even when training isn’t specifically required by statute or regulation, it’s still critical your credit union provide job-appropriate training for staff and board members.

While staff members are respon-sible for carrying out many of the day-to-day requirements contained in regulations, and board members have the broad responsibility of directing and controlling the affairs of a credit union, both groups have a shared responsibility to ensure your credit union complies with all applicable laws and regulations. In order to do so, they need to know the “what” and “why” of those laws and regulations.

Below are areas of training that are specifically stated in laws or regu-lations:

Bank Secrecy Act [Section 5318(h)]—Requires financial institu-tions to have an anti-money launder-ing program that includes an ongoing employee-training program.

NCUA Rules and Regulations §748.2(b) and (c)—Requires all feder-ally insured credit unions to have a Bank Secrecy Act program in writing, approved by the board of directors of the institution, and noted in the minutes. The program must provide training for appropriate personnel. However, no interval is mandated for providing that training.

Regulation CC: Availability of Funds and Collection of Checks [229.19(f)]—Each financial institution must establish procedures to ensure it complies with requirements of a regu-lation, and must provide each employ-ee who performs duties subject to the regulation with a statement of proce-dures applicable to that employee. No interval is mandated for providing that training.

Regulation B: Equal Cred-it Opportunity [Commentary §1002.15(c)(2)]—This section states that “identifying and then training and/or disciplining the employees involved” is an appropriate corrective action for problems discovered as a result of a self-test for compliance with this regulation.

Many violations of the Equal Cred-it Opportunity Act involve discrepan-cies between written policies and the actual practices of employees involved in the lending process. By keeping your staff trained on those require-ments, many of these discrepancies can be avoided.

Safeguarding Member Informa-tion [Appendix A III(C)(2) to NCUA Part 748 Guidelines]—Federally insured credit unions must train their staff to implement the information security system. Appendix A to Part 748 outlines specific requirements for the development of the information security system.

“Financial Literacy” for Board Members of Federal Credit Unions [NCUA Rules and Regulations §701.4(b)(3)]—Board members of federal credit unions must have or gain an understanding of basic finance and accounting principles within six months after election or appointment. A director must have the ability to understand the balance sheet and income statement and ask, as appro-priate, questions of management and auditors. There is currently no similar specific requirement for California or Nevada state-chartered credit unions, but providing such training for your board members would probably fall under the category of “not a bad idea.”

Supervisor Harassment Preven-tion Training [California Government Code §12950.1]—California employ-ers with 50 or more employees must provide sexual harassment prevention training to all supervisors in California. Training must take place within six months of hire or promotion and every two years thereafter.

A reminder: Don’t let the lack of requirements listed here fool you. Even if there is no specific training require-ment contained in a regulation, you are required to be prepared for compli-ance purposes. Therefore, the appro-priate individuals need to be aware of what’s necessary to comply.

Until next time, remember: it’s cool to know the rules!

For a sobering look at the cost of not complying with regulations, see Credit Union Digest’s April/May 2012 “Asked and Answered” column by visiting http://members.ccul.org/07publications/digest_issues/2010/dig0405_2010askedanswered.pdf.

Resource

19credit union digest | august/september 2012 | members first

By Arnold Ramirez, Research and Information Consultant

research & information

Which Rule Applies in Garnishments?

Directly deposited federal benefit payments are entitled to certain exemptions from garnishment

orders under both state and federal law. California Code of Civil Procedure §704.080 affords some of the same protections as the federal rule, albeit in a different manner. This overlap in protections has led to one ques-tion that comes up repeatedly on the California and Nevada Credit Union Leagues’ R&I Hotline: When does each rule apply? The short answer is: The rule affording a credit union member the greatest protection applies.

For background purposes, our nation’s Office of Personnel Manage-ment (OPM), Railroad Retirement Board (RRB), Social Security Admin-istration (SSA), Treasury Department, and Veterans Affairs (VA) Department collectively issued an interim final rule on this topic in February 2011. Additional information is available in TIPs Bulletin #11-12, which can be viewed by visiting http://members.ccul.org/05research/tips/2011/11_12.pdf)

The long answer requires a more extensive review of each rule’s provi-sions. The federal rule, 12 C.F.R. Part 212, does not displace or supersede a state law requirement, provided it is

not inconsistent or in conflict with the federal rule and the credit union has complied with all requirements of the federal rule.

To be in compliance, a credit union must first determine if a mem-ber’s account contains funds protected by either the state or federal rule. Under the federal rule, protected funds are direct deposits attributed to SSA benefit payments, VA benefit pay-ments, RRB benefit payments, or OPM benefit payments. Under California law, protected funds are SSA benefit payments or public benefits, defined as aid payments authorized by California Welfare and Institutions Code §11450, payments for supportive services under §11323.2, and general assistance payments made pursuant to §17000.5.

In the case of SSA benefit pay-ments protected by both rules, the rule providing the greatest amount of pro-tection will prevail. Under the federal rule, the amount of SSA benefit funds exempt from garnishment is the sum of SSA benefit payments posted to the account during the “look back” period (the two-month period preceding the date on which notice of garnishment is received by the credit union) or the balance of the account, whichever is

less. However, under California law there is a statutory amount protected based on the type of benefit and number of benefit recipients on the account. SSA benefits are exempt from garnishment up to $2,425 for a single recipient and $3,650 for two recipients on the same account. Public benefits, which are not covered by the federal rule, are exempt from garnishment up to $1,225 for a single recipient and $1,825 for two recipients on an account.

When determining which rule to apply for SSA benefit payments, a credit union must determine the extent to which each rule protects the member’s deposits and apply the greater protection. If the sum of SSA benefit payments directly deposited to the member’s account during the two-month “look back” period is greater than the statutory limit for protection under the state rule, then the federal exemption should be applied.

But if the amount exempt under state rule is greater than the amount pro-tected under federal rule, regardless of the time it took to accumulate the funds subject to the state rule’s exemption, the state rule should be applied.

19credit union digest | august/september 2012 | members first

20 credit union digest | august/september 2012 | members first

cu business solutions

Overdraft Provider May Put CU at Risk

In April, the Consumer Financial Protection Bureau (CFPB) released Bulletin 2012-03 outlining its super-

visory and enforcement authority over service providers associated with the institutions it supervises.

The bulletin states that the CFPB intends to fully exercise the authority it is granted under Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act, including the ability to examine the supervised service provid-er’s operations on site and its compli-ance with Title X’s prohibition on unfair, deceptive, or abusive acts or practices.

The bulletin also outlines the CFPB’s expectations that financial institutions have an effective process for managing third-party service provider risks.

To avoid potential pitfalls, credit unions should:

• Conduct thorough due diligence to ensure their service provider

understands and can comply with federal consumer financial laws.

• Review the service provider’s poli-cies, procedures, internal controls, and training materials to ensure appropriate oversight and training.

• Set clear expectations and enforce-able consequences in the service provider contract for violations of compliance-related responsibilities.

• Establish internal controls and monitoring to ensure the service provider is complying with federal consumer financial laws.

• Take prompt action to address any violations identified through monitoring, including terminating the relationship, if appropriate.

Clearly, regulatory efforts to protect consumers are intensifying. To avoid the risks, make sure you are maintaining your overdraft strategy with an expert provider that offers:

• A completely transparent program with a 100 percent compliance guarantee.

• Comprehensive employee training.• Easy-to-understand informational

materials to promote responsible program use.

• Reasonable, communicated fees and clearly established overdraft limits.

• Transaction clearing policies.• The ability to easily monitor

excessive usage.While attention to consumer protec-

tion efforts is clearly here to stay, maintain-ing compliance is as simple as contracting with an overdraft program provider that guarantees your program is in line with all regulations and best practices.

This article appears courtesy of our Business Partner, JMFA (www.jmfa.com).

toll free 800.472.1702 | www.ccul.org/03businessCalifornia and Nevada Credit Union Leagues | 2855 E. Guasti Road, Suite 600 | Ontario, CA 91761

Switch to Sprint and Save.

Credit union members who switch to Sprint will get:

• 10percentoff*ofselect

regularly priced Sprint

monthly service plans

• Waivedactivation

fee(upto$36)

• PLUS,a$50servicecredit

for each line you move from

another carrier to Sprint

(validuntil8/31/2012)

Take advantage of the Sprint

Credit Union Member Discount

at LoveMyCreditUnion.org. Then

upon activation, visit www.sprint.com/promo/iL29180PC within

72 hours of port-in activation to

request your service credit.

*Applicationofdiscountrequires2-yearcontract

extension on existing plans. Verification of member-

ship is required at time of activation/upgrade.

Discount does not apply to secondary lines.

For Sprint Credit Union Member Discount program details, visit

www.lovemycreditunion.org/Sprint.

For terms and conditions, visit

www.sprint.com/promo/iL29180PC.

Increasing Your Service, Savings, and Success

21credit union digest | august/september 2012 | members first

Retail Channels Never Die

cu business solutions

“… It’s easy to overstate the importance of self-service channels while downplaying the importance of the in-person experience. But in reality, a consumer’s choice of financial services channels is situational.”

Consumers want options when it comes to accessing

their banking information, adding or removing account funds, and resolving service issues. When accomplishing these tasks, some consumers prefer self-service banking, some prefer a more tradi-tional in-person approach, and many actively use all delivery channels.

Despite the expansion of self-service banking, consumers’ person-to-person interactions with branch staff and live phone reps remain significant. As certainly as we can say that self-service is the way of the future for financial institutions, it seems we can also say that old service channels never die—or at least they don’t die quickly.

These are some of the key find-ings from primary consumer research completed by the FIS Enterprise Strategy team. The implications for financial institutions are significant.

Consumers Want a multichannel Experience

When we asked consumers about their interactions with their primary checking account provider, we learned that the majority (61 percent) of con-sumers use between two and four chan-nels within a 30-day time period. Nearly a quarter of consumers (24 percent) reported using five or more channels. Consumers have proven that there isn’t a retail financial services channel they don’t like.

Generational differences have a huge impact on channel usage. When looking at the consumers reporting use of five or more channels, 41 percent were Gen Y, but only 9 percent were classified as “Mature” (born before 1946).

in-person Service remains Essential

Given the accel-eration in self-service banking and electronic payments adoption over the past decade, it’s easy to overstate the importance of self-service channels while downplaying the importance of the in-person experience. But in reality, a consumer’s choice of financial services channels is situational.

Consumers want the flexibility to use whatever point of contact suits their needs at any given time. The auto insur-ance provider Esurance captures this spirit perfectly in its recently

developed marketing tagline, “People when you want them, technology when you don’t.” Our research validates this concept. Of retail banking consumers, 57 percent are multichannel, having used both in-person and self-service chan-nels of their primary checking account providers within the past 30 days.

Only 20 percent of consumers are completely self-service customers. These consumers don’t use any in-person channels—only online, mobile, ATM and/or automated telephone services. This segment is composed primarily of younger generations and self-directed, mass-affluent consumers.

Conversely, 23 percent of consumers are primarily in-person banking custom-ers. These are consumers who conduct in-person branch or live telephone rep transactions and reported no use of online or mobile banking channels. Many of them, but not all, are older.