chapter4 - shodhganga.inflibnet.ac.inshodhganga.inflibnet.ac.in/bitstream/10603/31324/9/09_chapter...

TRANSCRIPT

CHAPTER4

Finance companies in a liberalizing economy

The literature on the liberalization of the financial sector has largely

focused on banks and capital markets. This is understandable because they

generally dominate the formal part of the financial sector. However, in a number of

countries it has been observed that private non banking finance companies have

been a dynamic segment of the financial sector responding to specialized credit

needs in the economy. In a number of countries they expanded rapidly especially

during the initial phases of financial liberalization.

Economists like Gurley and Shaw suggested that the impetus to the emergence of

non-bank financial intermediaries (NBFis) in the US might have come mainly from

competitive handicaps (such as reserve requirements) imposed on commercial

banks for purpose of monetary control. They argued that monetary control

discriminated against banks in their competition with non-bank financial

intermediaries and suggested extending central bank's regulatory powers with

respec~ to the liabilities of NBFis as well1• Growth of Non-banking financial

intermediaries was also explained in terms of financial innovations that are

undertaken in response to credit control measures by the central bank (Minsky

1957). The emergence and role of non-banking financial companies (with a

corporate structure) has been studied across countries i.

The role of finance affiliates of industrial companies, (particularly of auto

companies in the US) in providing consumer finance and in underwriting the

sales of their parent companies attracted the attention of researchers as way

back as the 1950s (Banner:1958). Subsequently, the focus was on the difference

between contracting and lending behavior of non-bank finance companies

compared to conventional banks (Carey, Post and Sharp:1988). On examining the

private corporate loan market, they found that finance companies are more likely

to finance information-problematic firms and serve observably high-risk

i The term Non banking finance intermediaries (NBFis) signifies non banking companies engaged in some form of financial intermediation, while NBFC would include non bank finance companies that do not necessarily carry out the intermediary function and has a broader connotation. In this study we mostly use the term NBFC or private finance companies interchangeably

115

borrowers as compared to commercial banks. Similarly, Remolona et al. (1992)

found that the growth of finance companies in the consumer loan market took

place in the relatively risky segments of credit market where command over

specialized information was critical to lending2 An interesting comparison of the

risk characteristics of banks vis-a-vis finance companies is to be found in

Simonson (1994) who ·observed that finance companies who lend against asset

values placed emphasis on skills in marketing of foreclosed assets. As a result

they are able to reduce their exposure firm specific risks and information

asymmetries.

In general, the emergence of Non Bank finance companies has been attributed to

the fact that they are able to complement the role of banks by providing services

for which banks are not well suited. By doing so, they fill the gaps in the financial

sector. In particular, NBFCs are able to overcome legal and tax impediments and

information disadvantages suffered by banks.

The role of non banking finance companies started to attract renewed interest with

the developing countries starting to liberalise their financial sectors from the mid

1980s. It was soon observed that while private NBFCs had certain advantages,

they were also hit by periodic crisis be it in Latin America (Zaga and Nankani:

2005: pp 213), in Africa (Aryeetey:1997 and Lewis and Stein:1997) 3 and also in

the East Asia especially during the financial crisis of 1997 (e.g. Carmichael and

Pomerleano:2002). These developments also raised issues pertaining to

regulation of finance companies especially in the wake of financial liberalisation.

The experience of India during the 1990s has been somewhat similar, albeit with

its specificities.

After two rounds of nationalization of commercial banks (i.e., in 1969 and 1980),

public sector banks had come to dominate the financial sector in lndiaii. Despite

the systematic decline in the share of the private sector in banking (during the

1970s and 1980s), 'private initiative' had managed to survive, or rather thrive, in

the form of finance companies4• These companies were also quick to respond to

the opportunities thrown open by economic reforms initiated in 1991 (unlike

commercial banks). There was rapid expansion in their number and scope of

;; Discussed in chapter 2 116

activities. But this phase came to an end, rather abruptly in 1997, with the dramatic

collapse of a relatively large private fi.nance company and was followed by a series

of closures of such companies. Following an overhaul of the regulatory framework

for NBFCs, the period after 1997 was marked by a change in the composition in

this segment.

Private finance companies in India prior to 1997 had some distinct characteristics.

First was the legal status. A large number of these entities were registered as

companies under the Indian Companies Act. They could therefore, be categorized

to be in the formal sector on this count5. However, there were also several

thousands of firms organized as partnerships, sole-proprietorship and other

entities not registered under any statute (and are not dealt in this study).

Technically, the latter were not a part of the corporate sector. But in common

parlance. they were also called 'finance companies'.

Second, was their diversity in terms of size, scope and range of activates. This

was evident from the definition adopted by the Reserve Bank of India (RBI) prior

to 1997 which categorized companies engaged in hire purchase, housing finance,

investment, loan, equipment leasing or a mutual benefit financial company, (but

not an insurance or stock holding company or a stock exchange) as a Non banking

finance company (NBFC)6.

The third feature was that despite being termed, as 'companies', the operational

practices of a substantial number of finance companies, especially the smaller

ones, were akin to intermediaries in the informal sector. It needs to be emphasized

that the formal and the informal sectors instead of being two discrete financial

enclaves have been a continuum in the modus of their operations. For most

practical purposes, the gray area between the two could be regarded as the semi

formal segment (Ghate: 1992). And many of these finance companies operated in

this twilight zone. Finally, the regulatory control by the RBI over private finance

companies was, (at least in practice), minimal, till the mid nineties.

The rapid proliferation of finance companies particularly during the nineties and

their collapse seems to follow the experience of some of the other countries cited

earlier. However, the fact remains that these companies in the private sector had

117

over the years, come to play, a distinct role in the mobilization and allocation of

financial resources for economic activities that were inadequately catered to by the

banking sector. In view of these features, an analysis of the developments relating

to finance companies is relevant for understanding the allocative outcome of the

liberalization of the credit sector. In particular, we address the following questions:-

• What were the reasons for the emergence and growth of private finance companies in India?

• What explains their further proliferation and collapse during the early phase of financial liberalization in India?

• What was the regulatory response? • What are the implications of these developments for the allocation of

resources?

For addressing the above questions, in Section 2 we analyse the growth of finance

companies in India during the 80s and their rapid expansion during the 90s.

Section 3 analyses the reasons for their growth especially during the initial phase

of liberalization and their collapse (in 1997). The issue is relevant since this period

coincides with liberalization of the economy in general, and the credit sector in

particular. The period from 1997-98 onwards was marked by remarkable change

in the regulatory structure for finance companies apart from the major shake out

that occurred in terms of their numbers. While this chapter is mainly focused on

the developments from 1991 to 1997, section 4 provides a brief account of the

developments after 1997-98. Observations follow in the last section.

Data: A major constraint in studying NBFCs is the lack of an aggregate time series

with a comprehensive and consistent coverage. In general, this sector continues to

be characterized by lack of consistent data set. Therefore there is no option but to

piece together information available from different sources for the purpose of

analyzing this sector from 1991.

We rely mainly on published data from RBI on NBFCs. This data is published in

their annual study conducted on a sample basis on the finances of private finance

and investment companies. The data on finance companies available prior to 1998

is not comparable to the data subsequent to 1998 on account of the dramatic

change in the regulatory structure and the number of companies. We also use

data from the Ministry of Corporate affairs and private databases apart from

drawing on some anecdotal evidence from the press.

118

Section 2 Growth and proliferation of Finance Companies

(1980s and 1990s)

An interesting change in the

corporate sector in India during the

80s and 90s was the rapid increase

in the number of finance

companies. Table 4.1 shows that

there was an increase in number of

finance companies through the 80s

and first half of the 90s7. However,

during the first half of the nineties

the increase was even more

pronounced. Over 22,475 new

financial companies came into

existence from 1991 to 1995 Uust

five years) as compared to 24,009

companies existing in 1990. While

Table 4.1: Number of finance Companies in India

Year Public Ltd. Private Ltd Total

1980 899 5999 6898 1981 1064 5999 7063 1982 1283 7691 8974 1983 1687 9413 11100 1984 2266 11253 13519 1985 2576 12782 15358 1986 2935 14421 17356 1987 3337 16281 19618 1988 3192 16119 19311 1989 3373 17733 21106 1990 3783 20226 24009 1991 6255 27265 33520 1992 6680 29152 35832 1993 8523 35312 43835 1994 10635 38334 48969 1995 14102 41893 55995 1996 11655 40274 51929

Source: RBI Bulletin, several issues, based on data from Dept of Company Affairs

the data in Table 4.1 includes government companies, the increase in the number

of finance companies was mainly in the private sector8.

60000

50000

40000

30000

20000

10000

0

Number of Finance Companies

l ·i I '

~ H ~ . . · .. ~

II • I I 1111111' I''

Figure 4 .1

I ~

1 .~

:· 1'1

119

Mobilization of saving: The increase in the number of finance companies was

accompanied by a rise in their share in financial intermediation. Given the

predominant position of scheduled banks in the mobilization of savings, deposits

mobilized by finance companies as a percentage of deposits held by banks was

modest till the late eighties (Table 4.2). Deposits of NBFCs 9 which were only 3.9

percent of the total bank deposits in 1981 gradually increased to about 8 percent by

1990. From the early 1990s this ratio increased to over 22 percent by 1995.

•;< Table 4.2: Deposits of NBFCs and scheduled banks (Figures in Rs. Crores)

Year Deposits Deposits Percentage Fin-Cos Banks Share

1 2 3 4 1981 1476 37988 3.88

1985 4356 72571 6.00 1986 4960 85704 5.79 1987 5942 102938 5.77 1988 7500 118678 6.32 1989 10485 140150 7.48 1990 14543 175441 8.29 1991 17236 204774 8.42 1992 20439 230758 8.86 1993 44956 274562 16.37 1994 56437 324721 17.38 1995 85495 376011 22.74 1996 101673 420449 24.18

Source RBI Bulletin: Growth of Def)Osits with Non-Bankinq Cos. Several issues •v

The increase in the mobilization of deposits was accompanied by a shift in the

distribution of deposits

towards NBFCs in the

private sector as compared

to NBFCs in the public

sector. The rapid increase in

the number of finance

Table4.3: Distribution ofdeposits by type of ownership of NBFCs

Year Percentage share Pub-Sec Pvt-sec

1992 42.3 1993 41.6 1994 38.1 1995 35.3

Source: CMIE (Banking and Finance 1998)

' -,,

57.7 58.4 61.9 64.7

companies in the private sector and in the deposits mobilized by them point to the

direction of entrepreneurial initiative after the first round of liberalization of the

economy.

Finance Companies and the Stock market: Finance companies had largely

relied on deposits as a major source of external finance. The Government

restricted the raising of capital from the stock market to manufacturing

120

companies by virtue of its powers under the Capital Issues and Control Act (CCI

Ac.l) 11• However, with the repeal of the CCI Act in 1992, financial companies

started to raise funds on the securities market. By 1995, they were the single

largest category in terms of resources raised through public issues accounting

for, as much as, 9.7 percent of total capital raised through listed instruments. Of

the Rs 5499 crore raised by finance companies in 1995, Rs 4961 crore was

raised by Private finance companies (Table 4.3).

f-Table 4.4 Capital raised by non-bankin' finance companies

Year 1992 1993 1994 1995 1996 1997 1998 1a Amount Issued by NBFCs (Rs. Cr) 2060 1590 2533 5499 5503 5411 5757 2b Share in total issues by all Cos (%) 14.7 5.6 5.4 9.7 17.1 16.8 14.2 r--

Amount raised by Pvt sector (Rs.Cr) 3c 107 988 669 4961 3056 1477 1556 NBFCs

4d Share of Pvt fin. Cos in total (%) 0.8 3.5 1.4 8.8 9.5 4.6 3.8 issues Number of capital issues by NBFCs

Year 1992 1993 1994 1995 1996 1997 1998 1 Number of Issues by NBFCs (No) 41 89 108 343 556 300 63

~ 2 Share in total issues of listed Cos (%) 7.9 8.3 8.3 16.3 29.2 27.9 14.3 3 No of issues by NBFCs in the (No)

32 78 94 335 548 292 47 Private sector

4 Share in total issues by all Cos (%) 6.2 7.3 7.2 15.9 28.8 27.2 10.7

r CMIE: Capttal Markets 1998

Correspondingly, the number of capital issues by finance companies especially

by private companies also increased (Table 4.4), the implication of which is

diSCUSSed later.

Capital structure: Even with the public equity issues, the capital structure of

finance companies (on the aggregate) underwent a change during 1993-94 to

1997-98. While the share of borrowing increased, the share of internal

resources in the form of reserves and surpluses and trade dues declined and the

share capital went up, albeit marginally,

Table 4.5 : Capital structure of finance companies in the private sector ITEM 1993-94 1994-95 1995-96 1996-97 1997-98 1998-99

Share capital 11.3 11.3 11.5 13.2 12.1 12.3 Borrowings 49.9 53.6 53.2 55.2 56.3 55.8

Debentures 2.4 4.0 7.3 6.8 9.3 11.9 From banks 11.2 13.1 12.5 12.2 11.0 9.4 Public deposits 16.4 16.1 15.9 19.5 20.6 15.1

Of total borrowings, debt 26.0 29.2 33.4 33.9 37.2 33.0

Trade dues 20.9 16.2 15.1 14.0 14.9 15.2 Reserves, surplus & 18.0 18.9 20.2 17.4 16.6 16.7 provisions

Total 100 100 100 100 100 100 Source: RBI Bulletin: Performance of Finance and investment companies Several issues.

121

The Collapse and shakeout: From 1996, things had begun to change. In late

1996, anomalies and fraud came to light in the accounts of a relatively large

finance company 'CRB securities'. Instead of further entry into the NBFC sector

what followed through 1997 and 1998 was 'shakeout' and 'exit' with ramifications

for the financial and the real sectors, particularly for those segments depended on

private finance companies for loans and for savers who held deposits of such

companies.

Net addition to number of Finance Companies 11000

9000

7000

5000

3000

1000

-1000 I;;

-3000 --5000

Figure 4.2

122

Section 3 Emergence, proliferation and Collapse of private finance companies

As mentioned at the outset, the emergence of Non-banking financial

companies has been mostly attributed to their ability to provide services that banks

are not well suited and their advantage in overcoming informational disadvantages

suffered by banks 12. The Working group on finance companies set up by the RBI

attributed the growth of finance companies (during the 80s) to the following three

factors 13.

• Low regulation in comparison to Banks. • Credit controls left out a section of borrowers and the NBFCs catered to them • High degree of customer orientation and simpler sanction procedures.

While examining the emergence and growth of finance companies in India (prior to

1991 ), it is worth noting that non-banking finance companies in India have not

been a homogenous segment. They have comprised of companies engaged in

diverse activities like loan financing, investment holding, share trading, hire

purchase, lease financing, housing finance, chit funds etc. Their heterogeneity

suggests that factors leading to the emergence of different types of finance

companies may have been varied 14•

Restrictions of bank credit in India (prior to the 1990s) were mainly targeted at

trading activities, especially, trade in commodities. Loan companies filled the gap

by supplying short-term credit to wholesale and retail trade. Nationalized banks

found it difficult to lend to small firms and traders. Higher proportionate transaction

costs on small loans, absence of marketable (or verifiable) collateral led to certain

borrowers to be rationed out by banks (Ghate: 1992). Loan finance companies

displayed greater flexibility in terms and conditions on their loans with simpler

procedures and lower transaction costs. Nearness to the borrower and

specialization in lending for a narrow range of activities gave them comparative

advantage in getting around the problem of informational asymmetry. Finance

companies, oust like their rural counterparts) thus catered to segments, (albeit in

the urban areas) who may have been denied credit by the formal sector. Shortage

of credit arising from quantitative controls and directed bank credit, and inability of

banks to service a class of borrowers (discussed in chapter 2) were thus factors

that led to emergence of loan finance companies.

123

The growth of the Hire purchase and leasing companies has been closely linked to

the transport business leasing of equipment and vehicle activity became significant

from mid eighties. Hire purchase covered a wider range that included financing of

consumer durables. From the mid eighties, manufacturing companies also set up

leasing and hire purchase companies (as subsidiaries) in order to support their

own product lines. Finance for purchase of commercial vehicles and consumer

durables, was lacking from banks (Dasgupta et al15.) Thus, the rise of Leasing and

hire purchase companies was closely linked to needs of investment financing by

manufacturing companies and demand for credit for purchase of automobiles and

consumer durables in the urban areas16. The rise of leasing companies was also

aided by tax laws that were liberal to the lessor for claiming tax breaks on

depreciation allowance even if they were not into manufacturing.

The reasons for the emergence of investment companies seem to have been

different from that of loan, leasing and hire-purchase companies. The emergence

of some of the investment companies in India was closely linked to the logic of

corporate control, reducing tax liabilities, apart from their carrying on investment

and finance activities as is understood in the conventional sense.

The expansion of capacity, especially, by companies belonging to large industrial

houses was subject to strict control through the 70s and the 80s. These

companies were required to obtain licenses and clearance under section 22 of the

Monopolies and Restrictive Trade practices Act, 196917. Investment companies

served as special purpose vehicles (SPVs) for cross-holding of shares. This

helped in avoiding detection of interconnection between group companies 18.

While the link between corporate business and finance companies was known,

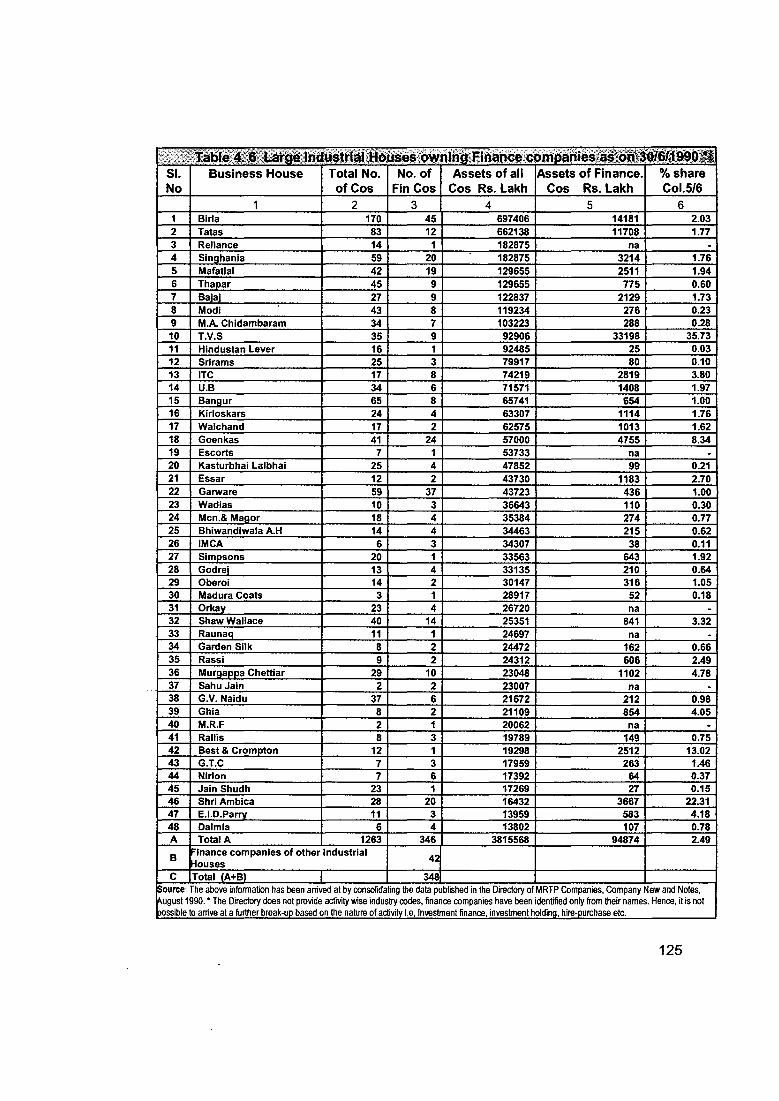

empirical evidence has been difficult to obtain in published sources 19• In an

exercise by us, we found that of 1267 companies belonging to large industrial

houses (i.e. assets more than Rs 1 00 crore) in 1990, 348 were finance companies.

Table 4.6 provides evidence of the close link between large industrial h9uses in

the private corporate sector and investment and share-trading companies.

124

:1;~:~!tl:~bl&:~»t§~~t;.a:fo~'tnaustr1iUBPli$es1;owrifnQ'~J;.in~o~~;~rnt»ariiesra$te>RAffJjtif~9QB 51. Business House Total No. No. of Assets of all Assets of Finance. %share No of Cos Fin Cos Cos Rs.Lakh Cos Rs.Lakh Col.5/6

1 2 3 4 5 6 1 Birla 170 45 697406 14181 2.03 2 Tatas 83 12 662138 11708 1.77 3 Reliance 14 1 182875 na . 4 Singhania 59 20 182875 3214 1.76 5 Mafatlal 42 19 129655 2511 1.94 6 Thapar 45 9 129655 775 0.60 7 Bajaj 27 9 122837 2129 1.73 8 Modi 43 8 119234 276 0.23 9 M.A. Chidambaram 34 7 103223 288 0.28 10 T.V.S 35 9 92906 33198 35.73 11 Hindustan Lever 16 1 92485 25 0.03 12 Sri rams 25 3 79917 80 0.10 13 lTC 17 8 74219 2819 3.80 14 U.B 34 6 71571 1408 1.97 15 Bangur 65 8 65741 654 1.00 16 Kirloskars 24 4 63307 1114 1.76 17 Walchand 17 2 62575 1013 1.62 18 Goenkas 41 24 57000 4755 8.34 19 Escorts 7 1 53733 na . 20 Kasturbhai Lalbhai 25 4 47852 99 0.21 21 Essar 12 2 43730 1183 2.70 22 Garware 59 37 43723 436 1.00 23 Wadias 10 3 36643 110 0.30 24 Men.& Magor 18 4 35384 274 0.77 25 Bhiwandiwala A.H 14 4 34463 215 0.62 26 IMCA 6 3 34307 38 0.11 27 Simpsons 20 1 33563 643 1.92 28 God rei 13 4 33135 210 0.64 29 Oberoi 14 2 30147 316 1.05 30 Madura Coats 3 1 28917 52 0.18 31 Orkav 23 4 26720 na . 32 Shaw Wallace 40 14 25351 841 3.32 33 Raunaq 11 1 24697 na . 34 Garden Silk 8 2 24472 162 0.66 35 Rassi 9 2 24312 606 2.49 36 Murgappa Chettiar 29 10 23048 1102 4.78 37 Sahu Jain 2 2 23007 na . 38 G.V. Naidu 37 6 21672 212 0.98 39 Ghia 8 2 21109 854 4.05 40 M.R.F 2 1 20062 na . 41 Rallis 8 3 19789 149 0.75 42 Best & Crompton 12 1 19298 2512 13.02 43 G.T.C 7 3 17959 263 1.46 44 Nirlon 7 6 17392 64 0.37 45 Jain Shudh 23 1 17269 27 0.15 46 Shri Ambica 28 20 16432 3667 22.31 47 E.I.D.Parry 11 3 13959 583 4.18 48 Dalmia 6 4 13802 107 0.78 A Total A 1263 346 3815568 94874 2.49

B inance companies of other Industrial 42 Houses c Total (A+B) I 34$

Source: The above information has been arrived at by consolidating the data published in the Directory of MRTP Companies, Company New and Notes, August 1990. • The Directory does not provide activity wise industry codes, finance companies have been identified only from their names. Hence, it is not possible to arrive at a further break-up based on the nature of activity I.e, Investment finance, investment holding, hire-purchase etc.

125

Investment companies had total assets of Rs. 948 crores which was approximately

2.5 percent of the total assets of these large industrial houses20. Holding

companies that held shares of group companies for purposes of control were not

financial intermediaries in the strict sense. But in practice, there was considerable

overlap between share-trading companies (that is, companies that actively traded

in shares) and holding companies that held shares of group companies.

On the whole, one could infer that the impetus to growth of NBFCs in India came

from diverse sources. The main reason was unsatisfied demand for credit of the

private sector due to general and selective controls on bank credit and the

comparative advantage of finance companies in lending to particular class of

borrowers such as traders and small firms. Developments outside the financial

sector, namely the growth of the consumer durables and the automobile industry

also added to the demand for credit. At the same time, the logic of corporate

control and channeling inter-corporate investment played a part in the emergence

of some of the investment holding companies.

The explanations given in the literature on financial development seem to broadly

explain the emergence and growth of NBFC till the late 80s, with some specificities

pertaining to India. However, the issue that does not square up is the rapid growth

and proliferation of these companies after 1991. The proliferation and collapse of

finance companies during the 90s cannot as such be attributed to further financial

repression since this period coincides with liberalization of the economy in general

and the financial sector in particular. Therefore these developments need to be

examined in further detail.

Proliferation and collapse of finance companies during the 1990s:

Liberalization of the real sector (especially the industrial sector) was launched in

1991 with the abolition of the licensing system for the industrial sector and controls

on issue and pricing of capital by private corporate sector. Freeing of the industrial

sector from clutches of the license-raj, and prospects of private sector entry into

financial services such as banking, mutual funds, merchant banking generated

126

euphoria among Indian companies. Large industrial houses that had diversified

into unrelated areas to evade licensing controls started to reconsider diversification

strategies. Industrial houses refurbished existing investment companies, or set up

new ones, to enter a prospective high growth area, namely, financial services. At

the same time, smaller stand-alone finance, investment and share-trading

companies mushroomed in various small and medium towns (Business World:

1996). As already stated, the rise in the number of finance companies during the

first half of nineties was accompanied by aggressive mobilization of deposits

The deregulation of capital issues in 1992 made it easier for finance companies to

raise capital on stock markets. As the number of finance companies listed on the

stock market continued to increase, all seemed to go well in the financial markets

from 1992-93 to 1995-96. During 1994-95 and 1995-96, the industrial sector grew

at a healthy rate of 9.4 percent and 11.8 percent respectively. Total resources

raised on the capital market increased from Rs 29,044 crores in 1992-93 to Rs

49,220 crores in 1994-95. But behind this fa9<3de, all was not well. First, the

borrowing profile of NBFCs had undergone a change for the worse. By 1994, the

share of high interest deposits (above 14 percent) had increased for three

consecutive years (1991 to 1993) in comparison to the position in 1990 (table 4.7).

Even though the maturity pattern did not undergo such a dramatic change (as the

cost of borrowing), yet the share of short-term loans below one year and below two

years maturity had increased by 1996 (table 4.8 ). Such a change strained their

liquidity position.

127

:;···:."; .. ::.:··· Ta~l~~ j~B;z.~J!e~nta]Jfidi$6ibiltion·ofrQi~Jt$K\Yitll:NBFCs.ll!,f,;~iith'i:::?:rR:'0':\;:. Term 1990 1991 1992 1993 1994 1995 1996

< 1 yr 1.95 0.90 1.40 1.29 16.63 19.94 20.72 1yr- 2 yr 8.15 1.27 1.60 0.71 10.62 17.80 16.85 2- 5 yrs 75.31 83.34 84.20 66.98 23.06 21.22 25.07 > 5 yrs 14.58 14.49 12.80 31.03 49.70 41.04 37.36

100 100 100 100 100 100 100 Source: RBI Bulletin, several issues. Finance companies include Miscellaneous Non-Banking Companies. Data mainly pertains to regulated deposits.

Second, finance companies had expanded their activities by providing credit for

consumer goods, transport equipment, real estate etc during the boom phase

(1993-94 to 1995-96). But their overhead costs on hiring of personnel, setting up

branch offices grew faster. There is anecdotal evidence to suggest that salaries in

finance companies for fresh entrants had reached astronomical levels (Financial

Express: 1998). Total expenditure grew faster than 'income earned from 1994-95

onwards (table 4.9) and not surprisingly, had adversely impacted the growth of

operating profits. ~~~~~~~~~~~~~~~~~~~~~==~~~~

~:~:~.r~~f ~·~·JGr~~l)~l(!~il~g?,ffl~~i~!i~n~itutfi'ian<t"'~e~~ti,~9:#J:§~t!~lP1:'~~~~l~>J~.1· ITEM 1993-94 1994-95 1995-96 1996-97 1997-98 1998-99

Main income 37.2 38.9 54.9 17.3 8.9 3.4

Total expenditure 34.3 55.7 51.6 25.7 14.0 9.5

Operating profits 39.0 18.1 6.3 -25.2 -30.3 -86.9 Source: RBI

Third, interest rates on bank lending and availability of bank credit to finance

COil}Qanies had hardened considerably by 1995. NBFCs relied to a substantial

degree on bank loans21. That apart, the RBI policy on lending by banks to NBFCs

underwent frequent changes during this period. This contributed to uncertainty on

availability of funds. In 1994, the banks were permitted to extend bridge loans or

interim finance to all companies including finance companies against public issues

and market borrowing up to 75 percent of the amount called up as against 50

percent earlier. But very soon (in Sept 1994) this decision was reversed with RBI

advising banks not to extend bridge loans/ interim finance to all categories of

NBFCs. 22

128

The RBI then clamped down on the overall credit to loan and finance companies

and residuary non-banking companies to twice the Net-owned funds (NOF) as

against 3 times of NOF. In 1995-96, RBI imposed further restriction on borrowing

by NBFCs from banks keeping in view of the unduly large increase in credit to

NBFCs. The RBI then went on to prescribe the maintenance of liquid assets at a

minimum 15 percent (in place of 10 percent) for hire purchase and leasing

companies. In July 1996, quite interestingly, the RBI removed the interest rate

ceiling on public deposits of NBFCs, which were said to have complied with the

registration requirements, and within the ceiling on deposits prescribed for them.

This decision was reversed in January 1998. It must also be remembered that the

registration requirement at that point of time ( 1997), did not have a statutory

backing

Finally, the industrial sector witnessed a downturn in 1996-97. With the downturn

directly impinging on demand for automobiles23 and trucks, leasing companies

started to face a mismatch between their assets and liabilities Though the extent

of the exposure of NBFCs to the real estate market is not known, a downturn in

property prices was an added blow. .

Lack of entry - exit barriers: The lack of credible entry barriers into the financial

services industry coupled with the ease with which finance companies could also

exit (that is, simply-disappear) after raising funds (deposits or capital issues)

meant that the situation was ripe for fly-by-night operators. Excessive entry into

the NBFC segment made it difficult for lay investors to distinguish between

reputed companies and fly by night operators. Giving details, the Centre for

Monitoring of the Indian Economy (CMIE), in its January 1997 report on the

capital markets, noted that the most important difference that marks the period

following the abolition of control of the government over capital issues in 1991 is

the entry of finance companies on the stock market. They add that a large

number of these companies were small in size.

129

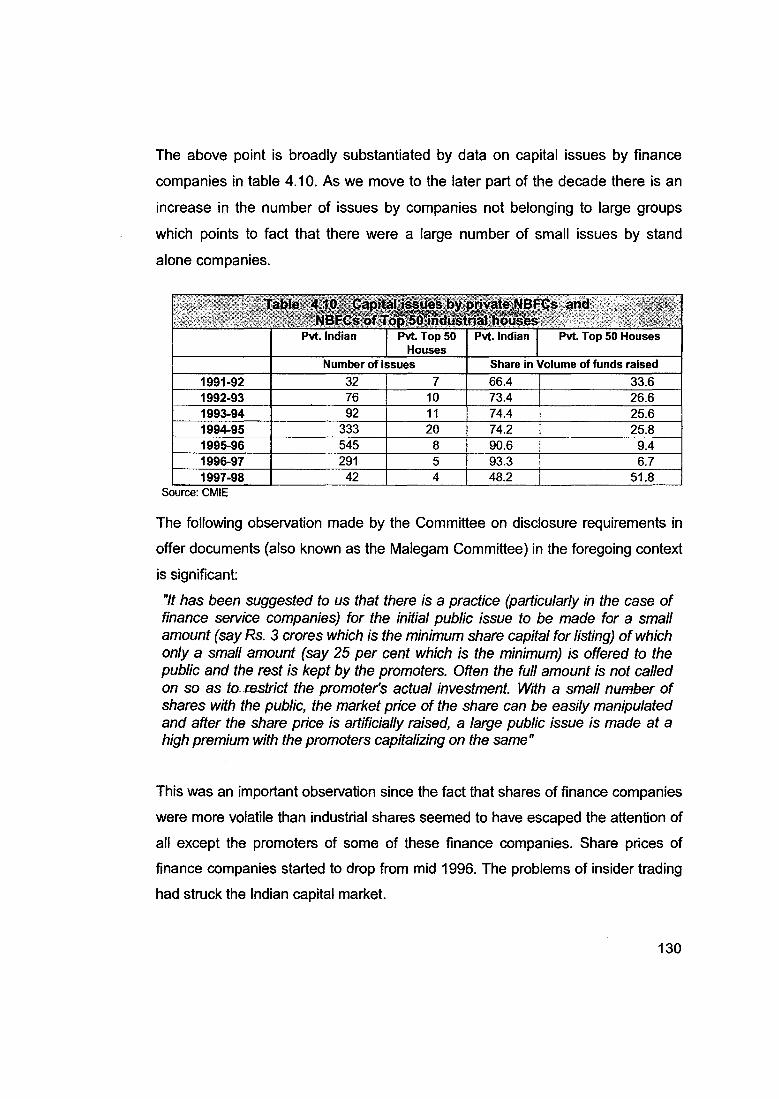

The above point is broadly substantiated by data on capital issues by finance

companies in table 4.1 0. As we move to the later part of the decade there is an

increase in the number of issues by companies not belonging to large groups

which points to fact that there were a large number of small issues by stand

alone companies.

The following observation made by the Committee on disclosure requirements in

offer documents (also known as the Malegam Committee) in the foregoing context

is significant:

"It has been suggested to us that there is a practice (particularly in the case of finance service companies) for the initial public issue to be made for a small amount (say Rs. 3 crores which is the minimum share capital for listing) of which only a small amount (say 25 per cent which is the minimum) is offered to the public and the rest is kept by the promoters. Often the full amount is not called on so as to_restrict the promoter's actual investment. With a small numl3er of shares with the public, the market price of the share can be easily manipulated and after the share price is artificially raised, a large public issue is made at a high premium with the promoters capitalizing on the same"

This was an important observation since the fact that shares of finance companies

were more volatile than industrial shares seemed to have escaped the attention of

all except the promoters of some of these finance companies. Share prices of

finance companies started to drop from mid 1996. The problems of insider trading

had struck the Indian capital market.

130

The trigger: In late 1996, anomalies and fraud in accounts of CRB securities

came to light. What followed through 1997 is interesting. By March 1997, about

141 listed finance companies had got themselves rated by one of the credit rating

agencies, (most of them, for the first time). With the fall of CRB securities, month

after-month, credit rating agencies downgraded a large number of the companies.

Firms that got downgraded had just about obtained a rating for the first time.

Table 4.11 Collapse of NBFCs during 1997 Month New/ Down Other bad news

Up Grading :grading

Jan-97 9 4 Income tax raids on 50 large companies for claiming false depreciation

Feb-97 3 1 Mar-97 1 1 Apr-97 2 3 May-97 7 1 CRB frauds made public, CRB Markets ltd Down graded Jun-97 3 6 Beginning of run on deposits. lTC Classic Ltd faces loses

Jul-97 33 11 RBI decides to closely monitor 121arQe NBFs, AUQ-97 9 Rate war amonQ NBFCs in Auto finance, Lending rates decline Sep-97 Three Bangalore companies booked for violation of deposits norms Oct-97 6 14 Hire purchase companies suffer losses as banks enter the business Nov-97 4 6 20 finance companies issued notices on lease back transactions Dec-97 4 RBI bans DSJ finance from raising fresh finance

81 47 Source: Compiled from the CMIE Monthly Rev1ew Jan to Dec 1997.

The downgrading of some companies made it difficult even for healthier

companies to renew deposits or obtain external funds. The 'Contagion' was

accentuated by a continuing downturn in generat economic activity, particularly in

industrial production and a decline in property prices. Regular media coverage of

events, (as they unfolded), with captions like 'DCM Finance faces run on deposits'

(Financial Express, Nov 1997), news of involvement of finance companies in tax

evasion, and other such news dampened expectations of investors even with

respect to well managed NBFCs. Impending changes in the regulatory

environment had already created doubts about the viability of a number of

companies.

131

The situation took a turn for the worse with reports of banks putting brakes on

lending to virtually all finance companies (including those companies that had not

raised public deposits, though, this was later denied by the RBI). As the finance

companies ran into rough weather, the primary market for capital issues was

contaminated by comprehensive mistrust on the part of general investors. From

mid 1997 for the next one year, hardly any capital was raised, not only by the

finance companies, but also by manufacturing companies.

The severity of the crisis is seen from the various reports from April 1997 to

March 2000, which show that CRISIL had downgraded 149 NBFCs due to

deterioration in their business and financial risk profiles. NBFCs downgrading

peaked during the 12 month period from October 1997 to September 1998

during which more than 94 NBFCs were down graded.

All this while, new sources of competition had emerged. While finance subsidiaries

of banks had started to expand their activities rapidly, the excessive entry that had

already occurred in this sector had started to take its toll on the margins. Through

the three years (95 through 1998) profitability deteriorated and followed a sharp

decline in the growth in income as well (figure 4.3)24.

Growth in Income of Finance companies

60 and Operating profits to income ratio

so

- 40 c 1!1 .. 30 Cll a. 20

10

0 1.0 ,.... 00 m 0 ...... N "" q- 1.1') 1.0 ,.... 00 m 00 00 00 00 m m q> m m m m m m m .;, .}, ,.!. ob a, 6 ...... ..:. r:, ..t- .;, .}, ,.!. ob 00 00 00 00 00 m m m m m m m m m m m m m m m m m m m m m m m ...... ...... ...... ...... .... ...... .... .... .... .... ...... ...... .... ......

-Income --- operating profits/income

Figure 4.3 (Based on RBI data)

132

Problems with regulation and supervision: Till 1997 the NBFCs were regulated

through directions issued by the RBI in terms of the powers vested in it under

Chapter Ill B of the RBI Act 1934. The directions issued by the RBI covered

matters like the issue of advertisements by NBFCs for soliciting deposits, carrying

out of inspections, terms and conditions on public deposits raised by NBFCs etc.

The RBI had issued 3 sets of directions applicable to different classes of finance

companies. These directions stipulated limits on the duration of deposits that could

be accepted by finance companies, the ceilings on the rate of interest that could

be paid on such deposits, and the ratio of liquid assets that had to be maintained

by such companies. Under the directions existing in 1991 the finance companies

were also required to file their statement of accounts with the RBI on a regular

basis. The views of various official committees which went into the working of

finance companies in India, when seen together, point to three major problems in

the institutional set up for regulating these companies. The shortcoming in the

regulatory and supervisory system made it difficult for the regulatory authorities to

react to the (post 1991) changes with greater speed and dispatch.

The first problem was that the number of

companies (by 1991) was so large that

the existing infrastructure with the

Department of non-banking companies of

RBI was inadequate for the purpose.

Figures in Table 4.12 are but one

indicator of the growing inadequacy of the

existing regulatory and supervisory

system especially from the mid eighties. It

shows that the percentage of companies

submitting their statistical returns to the

RBI declined dramatically during the 90s.

Though the RBI directions prevailing till

1991 had norms for net-owned funds to

133

deposits for each category of NBFCs, compliance could hardly be ensured. Apart

from shortage of staff and infrastructure, lack of data on NBFCs made it difficult to

draw out priorities for carrying out of inspections and checks. In effect, the data in

the table 4.12 when seen in conjunction with the data on the proliferation of new

companies suggests that very little was known on a large number of new

companies that were set up during the early nineties.

Second, whatever little attention was given towards supervision and regulation

was concentrated, on the liabilities side of these companies, that is, on their

deposit taking activity. The asset side of the NBFCs was more of less ignored.

Even the statistical data published by the RBI reflects this bias. A time series is

available on the deposits mobilized by NBFCs (though its coverage is not

complete). But very little is known on the assets side (except on the aggregate)

and the deployment of funds by these companies. This is a little disappointing in

the context of this study, for in the absence of asset side data, it is difficult to

assess the allocative impact of collapse of NBFCs.

Finally, there was the continuing problem of jurisdiction of the regulatory

machinery. As long back as 1975, the James Raj committee on non-banking

finance companies had noted that the demarcation of functions between the

Department of Company Affairs in the Government of India and the RBI on the

subject of regulation of finance_companies was not clear. They had further noted

that co-ordination between the two on the subject was poor. With the introduction

of the economic reforms in 1991, followed by the reforms of the financial sector,

Ministry of Finance in the Union Government came to occupy a key position in

determining the pace and sequencing of the reform measures. The RBI continued

to be responsible for the regulation of deposits-taking activity of the NBFCs. By

1992, the Securities Exchange Board (with powers to regulate the securities

markets) had come into existence. The Department of Company Affairs, in the

Union Government continued to have the responsibility of registration of

companies and carrying out statutory inspections of companies in terms of the

134

provisions of the companies Act. But the multifarious activities of the NBFCs had

always cut across jurisdictional lines. With rapid diversification and proliferation of

finance companies in the early nineties, finance companies started to

simultaneously take up fund and fee based activities (closely linked to the stock

markets). It seems likely that the problem of coordination between different

agencies (on specific matters as above) may have become more acute. The most

serious indictment on the collective lapse of various regulatory authorities came in

the report of the Joint Parliamentary Committee (JPC) that enquired into a major

scandal arising from irregularities in securities and banking transactions, which hit

the stock markets in 1992. Their observations go as follows:

"The committee concludes that some of the non-banking financial companies played a dubious role in the scam. It is astonishing that no authority either in the Government of India or in the Reserve Bank of India appears to have taken stock of the possible role of non-banking financial companies in securities and banking transactions nor of the limitations in the Reserve Bank of India Act to deal with such contingencies. Over the period of several years an entirely new sector of financial activity was allowed to grow and flourish without giving any thought to the deleterious consequences of the activities of this new sector."

The JPC also went on to recommend that the Government should consider

bringing about changes in the relevant regulatory system through changes in the

legal provisions. The process of consultation between different government

departments, for drafting of legislation and getting bills passed for revamping the

regulatory system was inevitably time consuming especially since some of the new

measures were intertwined with the complex agenda of carrying out reforms of the

financial and the real sectors on a wider scale. It is to this last aspect that we tum

to in the next section.

135

Section 4 Finance companies under the new Regulatory and supervisory regime

With NBFCs rapidly proliferating, from 1992 onwards, it was high time to give

shape to a comprehensive regulatory and supervisory framework. The

recommendations in the report submitted by the Working group on non-banking

financial companies, (known as the Shah committee), were accepted in 1992-93.

In 1993-94, the RBI set up another expert group (the Khanna committee) for

working the supervisory framework for NBFCs.25 This report, submitted in mid

1996, dealt with operational aspects of regulation and supervision of the NBFCs,

such as, specifying norms, reporting requirements for different class of NBFCs

etc.).

Meanwhile, as an interim measure, in June 1994, the RBI issued a detailed set of

prudential guidelines for NBFCs as per which these companies were required to

achieve a capital adequacy norm of 6 percent by March 31 1995 and 8 percent by

March 31 1996 and obtain a minimum credit rating from one of the approved credit

rating agencies. (Till then none of the NBFCs had a credit rating). But these

measures could not be given a statutory backing at that time as it required an

amendment to the RBI Act 1934. A Board of financial supervision was also set up

by the RBI to specifically look after the functioning of the NBFCs.

The new regulatory regime: The dramatic events following large scale

misappropriation of funds and the collapse of an NBFC (discussed in the previous

section) hastened the putting in place of a more comprehensive regulatory and

supervisory regime for NBFCs based more or less on the recommendations of the

Shah and the Khanna committee. The efforts to reform the regulatory and

supervisory framework culminated in the Union Government amending the RBI

Act (Chapter 111-B and V) in January 1997 and vesting more powers with the RBI.

The amended Act made it mandatory for all NBFCs (barring some exceptions) to

register with the RBI. In January 1998, the RBI issued a comprehensive set of

regulatory, prudential and supervisory measures with regard to NBFCs.

136

1) ENTRY NORMS: The entry by finance companies was restricted by making registration mandatory in 1998. A minimum limit of Rs 251akhs of net-owned funds (NOF) stipulated for accepting public deposits (this limit was later revised toRs 1 crore in 1999).

2) Credit rating made a prerequisite for accepting public deposits, and only companies with minimum rating of 'A' eligible to raise public deposits. Un incorporated entities cannot accept public deposits

3) ACCOUNTING & DISCLOSURE REQUIREMENTS: Revised reporting formats prescribed for NBFCs. The frequency of reporting greater in respect of companies accepting public deposits. The onus of correct reporting on accounts and the obligation to bring non-compliance to the notice of RBI placed on the auditors.

4) PRUDENTIAL NORMS: Emphasis towards strengthening the prudential norms. The amended act empowers RBI to give directions to the NBFCs regarding prudential norms; Capital adequacy requirement for NBFCs with NOF of Rs. 251akhs and above and accepting public deposits has been raised to 10 percent in place of 8 percent stipulated earlier. Credit I Investment concentration norms with regard to exposure to single borrower and a single group of companies were been stipulated at 15 percent and 25 percent of NOF. Composite limits for credit and investment have also been prescribed in recognition of the fact that NBFCs participate in the credit and securities market simultaneously. New income recognition standards and stipulations for providing for non-performing assets have also been laid down.

5) Liquid Assets and Reserve fund: NBFCs are required to maintain liquid assets of a minimum of 5 percent of their deposits in unencumbered security (Government bonds or guaranteed bonds) and create a Reserve Fund through transfer at least 20 percent of net profits to the reserve fund.

6) CLASSIFICATION OF NBFCS: Given the large number of companies required to be regulated and supervised, a three way classification of NBFCs has been adopted. The degree and closeness with which companies would be regulated and supervised would rest on the extent of the deposit taking activity and the size of the company. The companies have been classified as a) those accepting public deposits, b) those·not accepting deposits but engaged in loan, investment, hire purchase and leasing activities and c) those not accepting deposits and holding shares of 90 percent or more of shares of group companies and do not trade in securities. Companies would qualify to be classified as hire purchase and leasing companies only if a minimum of 60 percent of income and assets are related to these activities26

.

7) SUPERVISORY FRAMEWORK: The supervision of NBFCs to comprise of off-site and on-site inspections. While off-site surveillance system would be based on the statutory returns and would cover almost all categories of companies, the frequency of on-site inspection would be higher for large companies. Inspections to focus on the quality of assets; fund flow and capital adequacy management. NBFCS are to be given supervisory ratings based on compliance of prudential norms.

8) ROLE OF AUDITORS: The amended act gives powers to the RBI to direct the NBFCs and their Auditors on matters relating to Balance Sheet and cause Special Audit as also to impose Penalty on erring Auditors; The RBI is empowered to use outside expertise, such as auditors, professional bodies like the Institute for Chartered Accountants for inspections The auditor has now been thrust with the responsibility of making the report on aggregate amount of deposits and giving a declaration on the correctness of the statements.

9) Depositor protection: The act prohibits NBFCs from accepting deposits for violation of the provisions of the RBI Act and direct NBFCs not to alienate their assets The amended act authorized the Company Law Board to direct a defaulting NBFC to repay deposits

10) Imposition of penalties: The act empowers RBI to impose Penalty directly on the erring NBFCs

11 )Winding up of NBFCs: The RBI is empowered to file winding up petition against the erring NBFCs;

137

The new regime that evolved since 1997-98 covers various aspects relating to the

functioning of NBFCs that include classification, registration, prudential

requirements, supervision and regulation, the role of auditors and protection of

depositors. Some of the main features of the revised regulatory framework are

summarized in Table 4.13. In the new regulatory and supervisory regime, there is

a conspicuous shift towards restricting entry and registration mandatory especially

for deposit taking companies. As compared to the earlier approach where the

emphasis was mainly on regulating the liabilities side, there is also focus on

adhering to prudential standards and maintaining asset quality. Deposit taking

companies are subject to much higher degree of regulation. While non deposit

taking NBFCs are not required to maintain minimum capital adequacy ratios and

are not subject to exposure norms, they are subject to prudential norms relating

to asset classification and provisioning.

The regulatory and supervisory framework for NBFCs has been evolving since

1998 with modifications and changes every year the details of which have been

documented in RBI publications. In the context of this study the relevant issue is

the impact that these changes have had on the composition of the NBFC sector

and in turn the allocation of financial resources

Impact of the changes in the regulatory and sup-ervisory framework: In

response to the changes in the regulatory framework, all of the NBFCs existing

on January 9, 1997 were required to submit up to July 8, 1997 an application for

statutory registration. The Bank received 37,478 applications from existing

companies of which 907 4 companies were found to have NOF of Rs. 25 lakhs

and above and 2371 companies were accepting public deposits. The RBI

observed that many companies did not apply to RBI for a certificate of

registration but continued to do their business in violation of the provisions

contained in the RBI Act.

138

There has been a consolidation in the NBFC sector since 1997-98 marked by

company acquisitions, portfolio buyouts and the entry of foreign players into the

secto(17. The number of deposit taking NBFCs and the share of deposits in their

overall liabilities came down. As of March

1999, there were 996 deposit taking NBFCs

reporting to the RBI with about Rs 8338

crores of deposits. By 2008, there were about

127 40 registered NBFC. Of these only 364

that were authorised to. accept public

deposits (i.e. categorised as category 'A' }

had deposits of Rs 2042 crores. The

remaining companies that did not accept

deposits were classified as categories 'B' and

'C.' Category B and C NBFCs have been

doing business out of their own funds or institutional borrowings and as such

they need not be subject to the stringent Reserve Bank of India regulations.

There are a large number of NBFCs engaged only in investment activity. Many of

these have been floated by big companies as their investment arms. In general,

along with the consolidation of the sector there has been a decline in the number

of deposit taking NBFCs as also in the quantum of deposits held by them.

~;~}li$l)l~:4l01:5'®mfi<>$J~()if:~r;tll~~iPJJ&at~~$i•;ln•~~fi~1~fit:,~S~fl:fi~;· Liabilities 2004-05 2005-06 2006-07 2007-08 1. Paid up Capital 6.1 4.8 4.7 4.4 2. Reserves & Surplus 12.6 14.9 12.1 11.7 3. Public Deposit 10.9 6.5 4.3 2.7 4. Borrowings 64.0 65.9 66.8 67.8 5. Other Liabilities 6.3 7.9 12.1 13.4 Assets 1. Investments 11.0 11.4 15.3 15.0 2. Loan & Advances 35.4 28.2 22.8 25.2 3. Hire Purchase Assets 40.0 52.9 54.0 45.0 4. Equipment Leasing Assets 5.6 4.0 2.8 1.4 5. Bill Business 1.3 0.1 0.0 0.0 6. Other Assets 6.7 3.3 5.1 13.3 Total liabilities/ assets Rs Cr. 36,003 37,828 48,554 74,562 Source: RBI, Report on trend and progress in banking in India, Several issues

139

While deposit taking activity might have declined, an important development has

been the increase in the NBFCs (Non deposit taking) in terms of their number

and asset size. Accordingly; the regulatory framework has been widened to

include issues of systemic significance. Non Deposit taking NBFCs with asset

size of Rs.1 00 crore and above have been defined as systemically important and

an elaborate prudential framework was put in place which stipulates Capital

Adequacy, Liquidity and Disclosure Norms.

Consequent to the application of the new regulatory regime in terms of the

requirements for registration, capital adequacy, prudential norms and pending

legal issues several companies have had to stop business. Over 7 45 NBFCs

have been issued winding up orders, The application for registration of 16768

companies stands rejected and the registration of 287 companies has been

cancelled. In other words the composition and the dimensions of the NBFC

sector continues to be in a state of flux with its composition changing partly on

account of the changes in the regulatory regime as well as due to the emerging

competition from banks and their affiliates 28•

In the case of the banking sector there has been a system of collection and

collation of data on the composition of bank loans by borrower categories and

the type of customers being serviced. In the case of the NBFCs, a corresponding

profile of the asset side (by user categories) is not available. Even now the

consolidated data on NBFC is largely for the deposit taking companies. However

with the decline in the deposit taking activity by finance companies and a

corresponding increase in the asset financing activity, the focus of data collection

and reporting should also perhaps reflect this change.

In view of the above, it is difficult to ascertain the type of clients, borrower

categories, their occupational profile, whether they are corporate or non

corporate entities. However, there are a few pointers that are indicative of the

nature of changes that may have occurred with regard to the target population

that the NBFC are servicing. First and foremost there has been a clear decline in

the number of companies. Second, there has been a change in composition

140

whereby the market is dominated by a handful of players that include captive

finance companies, bank affiliates, a few large stand alone finance companies

and MNC players.

The consolidation process has imparted stability to the sector and tractability for

the regulators. This is broadly a positive development especially from the point of

financial stability. However, the winding up or the withdrawal of a large number of

small finance companies has also meant that the degree of geographical

penetration has come down. The fact that smaller finance companies cater to a

class of borrowers like small enterprises and other small businesses has meant

that access to finance, especially asset based financing for these types of

activities of the economy has shrunk. Unless there is a compensatory

improvement in the availability of bank credit these developments imply a decline

in access to finance and therefore negative fallout from the perspective of

allocation of financial resources in the economy.

Some scholars who have been studying this sector over time are of the view that

finance companies were playing an important role in financing many of the fast

growing sectors in the economy, particularly small industrial enterprises,

construction, services and trade activities. Proprietorship and partnership firms

also depend heavily on NBFCs for finance. Vaidyanathan (2005) has argued that

non-banking finance companies, both corporate as well as non-corporate, are

the best route to finance future 'income-based' activities especially in the non

corporate sector due to the fact that they have the ability to rate

partnership/proprietorship groups and monitor them and recover the money lent

to them. He also observes that the trend in commercial banks today is to merge

existing branches rather than to create new ones. In such a situation, it may not

be possible for commercial banks to enlarge the network to cover a larger portion

of the "non-corporate sector (Vaidyanathan 2003). It is also seen that the large

finance companies, especially MNC affiliates tend to focus on large corporate

clients. Therefore a large un serviced gap in terms of availability of finance has

emerged in the economy, especially since lending from commercial banks to

small enterprises, partnership and proprietary firms and such categories has also

slowed down as shown in chapter 3 .

141

Section 5 Some implications of the collapse of finance companies

The rapid growth of finance companies in India coinciding with the

liberalization of the economy in general and the financial sector in particular, and

the efforts made, subsequently, to put in place a new regulatory regime raises

issues that are of wider significance. In concluding this paper we touch upon some

of these issues.

One noticeable impact of the financial sector reforms has been of drawing the

private finance companies more closely into the regulatory net. The impact of new

regulatory requirements and entry norms was dramatic. In general there was a

drastic shrinkage in the number of companies with concomitant implications for the

availability of finance.

First, financial sector reforms in most developing countries focussed largely on the

formal banking sector and the securities market. Emphasis has been on the

possible increase in savings and improvement in the allocative efficiency of the

financial sector (especially banks) following financial liberalization. The response of

non-bank financial intermediaries following such reforms received comparatively

less attention. This is surprising especially because with their innovativeness non

bank finance companies across the world have demonstrated their ability to

penetrate and deliver finance and finance related services that banks and stock

markets have found difficult. Several developing countries seem to have

experienced rapid growth of private finance companies in the first phase of

liberalization. The Indian case also falls in line with the international experience

as far as rapid growth of NBFC is concerned. At the same time they have been a

fragile segment of the market.

Second, that investment companies were not financial intermediaries in the strict

sense. They hold shares of group companies for purposes of control. But the

dividing line between companies that hold shares only for purposes of control and

those that trade in securities is not a constant one. Inter-penetration between non-

142

bank financial companies and other manufacturing I services companies holds a

potential for collusive behavior, carrying out restrictive practices resulting in fraud

and diversion of funds. This is a matter of concern from the point of 'efficient

allocation of investible resources'. There may be a case for having a monitoring

mechanism for maintaining share holding patterns and trading activity of

investment-holding companies.

Third, a specific problem arises from the categorization of NBFCs adopted by the

RBI. Even though there are companies that are specialized, there are several

companies whose activities overlap. Classifying companies in terms of their

principal activity, say leasing, loan finance etc. on the basis of assets devoted, or

the share of income arising from that activity, and devising prudential norms and

regulations accordingly, is likely to prove inadequate. It needs to be recognized

that watertight compartmentalization in financial services is no longer feasible.

Regulatory authorities will have to adapt to inter-penetration between different

financial services. Not surprisingly, the RBI has had to change the classificatory

scheme more than once and has now recognized this aspect

The very fact that the dimensions of the NBFC sector continues to be in a state

of flux with its composition changing in response to new regulations as well as

the new felt needs in the economy suggests that financial innovations and

technological progress will always tend to undermine the effectiveness of

regulations, old or new. Therefore, strengthening the regulatory framework by itself

may not be a panacea to all problems.

Fourth, a general principle that is seen in the regulatory response to the

mushrooming of finance companies in the mid 1990s is that during a phase

characterized by a shift, from a regime based on controls to one said to be based

on 'market discipline,' there is a 'regulatory vacuum' when the old rules and

regulations stand discredited, if not totally discarded, but new rules, have either not

been fully internalized, or worse still, not written at all. In other words, there is a

'regulatory lag' that is characterized by trial and error and learning. If the gap is too

143

long there are bound to be entities who take advantage of regulatory arbitrage that

is possible in such a situation.

Fifth, in the foregoing context it would not be wrong to infer that large scale entry of

finance companies during a transition phase from a regime of controls to one

based on market signals is characterized by herd behavior. This coupled with the

total absence of barriers to entry (and exit) into financial services provides ample

scope for innovative forms of arbitrage and frauds. Growth and entry into financial

services during such a period cannot therefore be explained merely in terms of the

controls over the banking system, financial repression or credit rationing behavior

of banks and other intermediaries.

Increased freedom of entry into the financial sector and the freedom to bid for

funds through interest rate and new instruments can lead to excessive risk-taking.

An important point to note is that the risk taking behaviour of private finance

companies in India was in sharp contrast to the somewhat risk averse behaviour

of the banking sector dominated by public sector banks. Interestingly both types

of behaviour, over time, had the effect of reducing the flow of credit.

The literature on financial liberalization in developing countries (which followed the

lead given by Mckinnon and Shaw) focused mainly on the positive effects of

freeing interest rates, relaxing of restrictions on credit allocation and permitting

greater competition in the financial sector. The experience gained across different

countries show that the outcome of a process of liberalization of the financial

sector is also contingent on institutional factors, in particular, the initial conditions

relating to the regulatory and supervisory systems. It is also seen that deregulation

of the financial sector can facilitate a too rapid growth of some financial institutions

and allow unsuitable persons and institutions to enter into financial business,

particularly when the regulatory framework is evolving. Therefore it is important to

pay attention to the initial conditions, particularly the limits of the existing regulatory

system, the level competence of the regulators and the prevailing accounting

standards and incentive mechanisms of the agents in the financial sector. This

144

precaution is essential while deciding on the pace and sequencing of financial

sector reforms. Financial regulation is not an exogenous process that can be

imposed on a country's financial institutions and markets. The slow and painful

journey towards putting in place, a regulatory system for NBFCs in India shows

that institutional reform is perhaps the most difficult and time consuming of the

tasks unlike what text book models postulate.

Implications for resource allocation: The Reserve Bank has repeatedly

stressed that NBFCs play an important role in delivering credit to the

unorganised sector and to small borrowers at the local level in response to local

requirements. If that is true then the collapse of such a large number of NBFC

segment would have certainly chocked off credit to a large section of borrowers

at the lower end of the production and trade spectrum. It is however difficult to

arrive at a clear estimate of the impact of the collapse of the NBFCs on the

availability and distribution of finance.

The sheer magnitude of shrinkage in this sector can be gauged partially by the

fact that of the 36,269 applications received only 12,7 40 companies stand

registered by the end of 2007-08. This segment is now dominated mainly by

larger NBFCs that managed to survive. But the demise of smaller of NBFCs

especially in small and medium towns has led to shrinkage in finance for trade

and smaller businesses including manufacturing the effects of which on the

economy remains to be-assessed perhaps through primary surveys as published

data does not effectively capture the impact. The banking sector has also had to

cope with increased demand for capital provisioning. Therefore, the void left

behind by the NBFCs in all likelihood has remained unfilled for a prolonged

period except in certain areas like housing finance and personal loans to the

premium segments of the markets where bank finance has continued to grow.

While the Finance companies discussed in this chapter were mainly

concentrated in urban areas, the lessons arising from their proliferation, collapse

in the 1990s and the subsequent transformation in this sector continue to be

145

relevant from a regulatory point. This experience is also relevant even with

reference to the rural sector that has seen the emergence of large number of ·

micro finance institutions which we discuss in chapter 6. At the end of this

chapter it suffices to observe that the question of distributional effects of financial

liberalization thus remains relevant, even if, the story of NBFCs in India has only

been a sideshow.

***********

146

End notes

Non-bank intermediaries have also been studied with reference to their impact on money supply. While banks and finance companies are financial intermediaries, banks have been considered to be unique in their ability to create demand deposits (thereby adding to the money supply). However it has been argued that with the increasing range of financial assets, the distinction between what constitutes money and what does not within a range of financial assets is not obvious (See Gurley and Shaw (1960), Tobin (1963). 2 That movement in consumer credit induced macroeconomic impact in the sense its cyclical movements impacted on consumer demand was studied in Klein: (1971 ).

3 In a study on financial liberalization in the four African countries namely Ghana, Tanzania, Malawi and Nigeria by Aryeetey (1997) shows that semi-formal sector comprising of non-bank finance companies showed considerable financial innovation. Non-bank finance companies and informal financial agents showed a dramatic increase in their numbers as well size of operations. They note that these developments made little impact on the market fragmentation and resource mobilization. Recounting the experience of financial liberalization in Nigeria after 1986, Lewis and Stein ((1997) note that with a relaxation of barriers to entry in financial services, the market conditions encouraged the emergence of new financial institutions (apart from banks who continued to be dominant). They go on to state that:-

' ... the wholesale entry of new firms drastically changed the structure and competitive environment of the sector. A diversifying array of market actors made the system more opaque and unstable. Many of the new entrants focused on rent seeking, speculation and fraud, rather than conventional intermediation. The flow of personnel and capital to non-banking financial institutions (NBFis) created a vortex of activity which altered the character of financial markets and eventually undermined the foundation of the sector'.

4 One could categorize the areas that were dominated by private initiative in finance as being in the 'informal' and 'semi-formal' segments of the financial sector. The informal segment consisted of organizations with a non-corporate structure doing lending, hire-purchase and chit fund business. These included indigenous bankers, pawnbrokers, sole-proprietor or partnership firms, and moneylenders ubiquitous in rural India. The semi formal segment included unregistered private financiers and the formal segment included private finance companies.

5 The Report of the Committee on Informal Financial Sector Statistics, categorizes NBFCs to be in the formal financial sector.

6 Miscellaneous non-banking companies comprising mainly of chit funds and prize chits were also under the broad category of financial companies (RBI 1987).

7 The number of financial companies (given in Table 4.1) has been compiled by the Department of Company affairs on the basis of registered companies, classified in terms of their main object clause at the time of registration. However, they may include companies that may have been dormant and not carrying out any business. Therefore the numbers indicated should be considered as an outer figure of the number of NBFCs actually at work.

8 This inference is based on the following: In comparison to the number of finance companies at work shown in Table 4.1, the number of companies filling their statistical returns to the RBI is much smaller. The RBI publishes data on deposits mobilized by reporting companies on an annual basis. This data includes government owned NBFCs. While the extent of non-reporting for private NBFCs would be high, it can be expected that most of the government owned NBFCs would be

147

filling this data with the RBI. The number of government companies reporting such deposits remained constant during the 90s.

9 Deposits of Financial companies include both regulated and exempted deposits. Regulated deposits mainly include deposits raised from the public. Exempted deposits include, secured debentures, borrowing from bank

10 The Working group on finance companies (also known as the Shah committee) set up by the Reserve Bank of India (in 1992) attributed growth in deposits of finance companies during the eighties to higher interest rates offered by such companies on their deposits. It noted that there was a shift in the portfolio composition of financial savings of the household sector in favor of company deposits (which include deposits of NBFCs). The shift in the portfolio of financial saving of the household sector in favor of company deposits continued into the 90s, right unto 1996-97, after which it has shown a swing back in favor of bank deposits. Though the rates of interest on public deposits of NBFCs (in the corporate sector) were controlled by the RBI, and kept above the corresponding rates on bank deposits, financial companies often used non-price means to attract savers through gifts, discounts and other promotional measures

11 Official documents accordingly do not provide any data on the capital raised by finance companies for the period before 1990

12 Chandavarkar ( 1992) drew a useful distinction between the 'spontaneous' and the 'reactive' constituents of the informal financial sector. According to him, the core of informal finance is the 'spontaneous' segment comprising of saving associations, indigenous bankers, pawnbrokers etc. (what this paper does not deal with). The other constituent of informal finance is 'reactive', since it develops primarily as a reaction to the deficiencies in, and controls over, formal finance. This analogy also seems relevant even in regard to the emergence of private financial companies. 13 Report of the Working Group on Financial Companies, Chapter Ill Para 3.3):

14 A disaggregated empirical analysis of the factors leading to the growth of each of these categories of companies, though desirable is beyond the scope of this paper. 15 Dasgupta, Nayar and associates in their study on urban informal markets in India show that growth of hire-purchase companies can be attributed to the reluctance of banks to enter into this activity and inflexible bank procedures.

16 In developed industrial economies, changes in consumer credit, especially credit for automobiles (and housing mortgages) has been identified as being a precursor to cyclical changes industrial output (P.A Klein: 1971). Given the rising importance of credit for the purchase of consumer durables and vehicles in India this phenomenon is becoming important in India too.

17 The establishment and expansion of industrial capacity by large companies in India was subject to restrictions under sections 21, 22 and 23) of the Monopolies and Restrictive Trade Practices Act, 1969. These restrictive provisions became applicable in the case of every company whose assets (together with its interconnected undertakings) crossed the threshold limits prescribed under that Act. Sections 21, 22 and 23 of the MRTP Act were later abolished in 1991.

18 The link between large industrial groups and investment and holding companies (then known as investment trusts) has been commented upon in some earlier studies on the Indian corporate sector. Joshi (1957) while discussing the emergence of Investment Trusts notes, that investment trusts were not widely held and most of them were controlled by managing agents. Subsequently Gupta (1969) in his study on the structure of industrial finance in India confirms the link between some investment companies and industrial groups. A more recent account has been given in

148

Sudip Dutta (1997) who notes that investment companies have been a popular means of keeping stakes under control in the Indian corporate sector.

19 The Monopolies Research Unit in the Department of Company Affairs of the Government of India was engaged in investigating into such interconnection. However in most cases, such interconnection was contentious and difficult to prove. The M RU was later wound up after 1991.

20 These figures were arrived at on the basis of investment, holding and finance companies identified from the list of MRTP companies published by the Department of Company Affairs