chapter - v analysis and interpretation -...

TRANSCRIPT

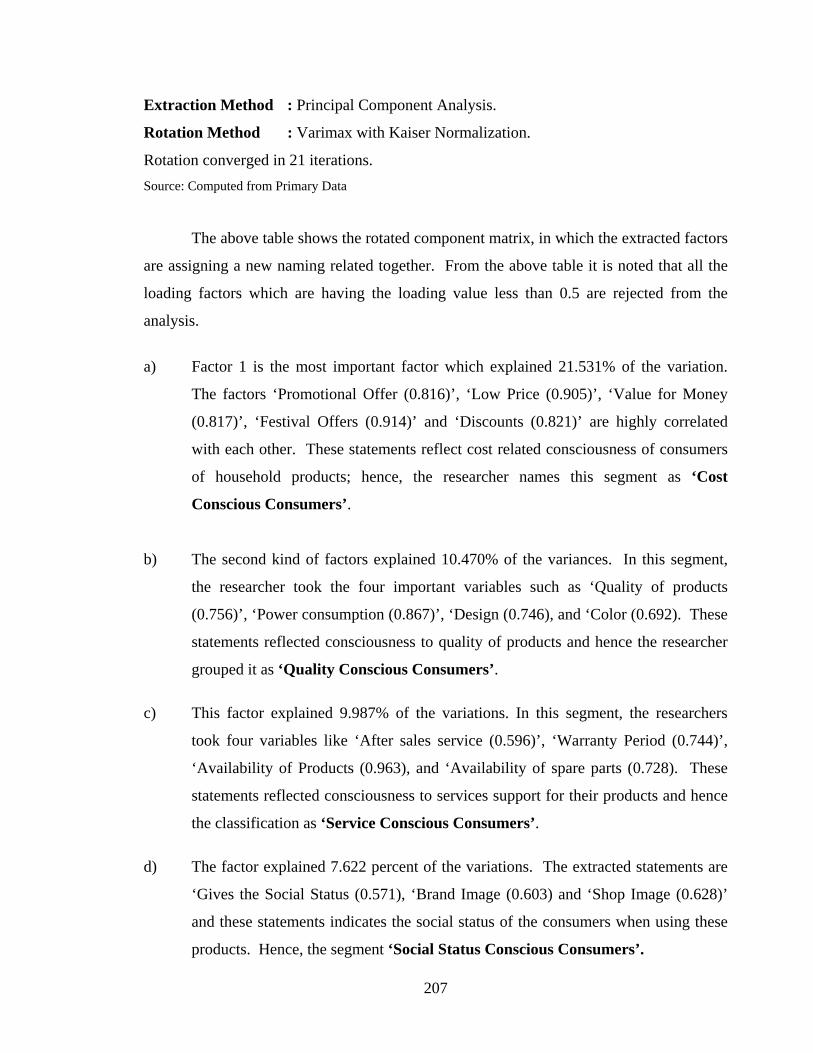

87

CHAPTER - V

ANALYSIS AND INTERPRETATION

5.1 INTRODUCTION

In this chapter an attempt has been made to identify the factors that influenced the

purchase of Household Electronic Consumer Products. For this purpose, a field survey

method was employed to collect the first-hand information from 750 sample respondents.

The respondents have been chosen randomly from different parts of the study area. The

data thus collected were arranged into simple tabular form. The level of satisfaction

perceived by the respondents towards household electronic consumer products was

considered as a dependent variable. The independent variables selected for the study were

living place, age, gender, educational qualification, marital status, occupational status,

monthly income of the family, size of the family, nature of family, level of awareness,

number of products used, type of products used, mode of purchase and finally point of

purchase.

The data were analyzed by using some simple statistical tools like Percentage,

Average, Range, Standard Deviation, Two-way tables and Chi-Square test. In addition to

these tests, Multiple Correlation, Multiple Regression, Multi-Discriminant analysis and

Factor analysis were used appropriately. To further ease analysis and understanding seven

methods of tools/techniques are used and discussed.

I. Chi-Square Test

II. Percentage Analysis

III. Henry Garrett Ranking Technique

IV. Multiple Correlation Analysis

V. Multiple Regression Analysis

VI. Multi-Discriminant Analysis and

VII. Factor Analysis

88

1. CHI-SQUARE TEST

The level of satisfaction of consumers who utilized household electronic products

was measured based on their opinion on satisfaction perceived against their opinion in the

following aspects: Promotional offer, price, emotional value, model, convenience, after

sales service, warranty period, social status, standard of living, quality of product, festival

offers, discounts, power consumption, brand image, shop image, design, color, varieties,

availability, hygiene and packing. The respondents’ opinion were measured based on

scale scoring technique. Likert’s five points scaling was employed and the consumers’

level of satisfaction was classified as low (below 75), medium (76-90) and high (91-100)

based on mean and standard deviation.

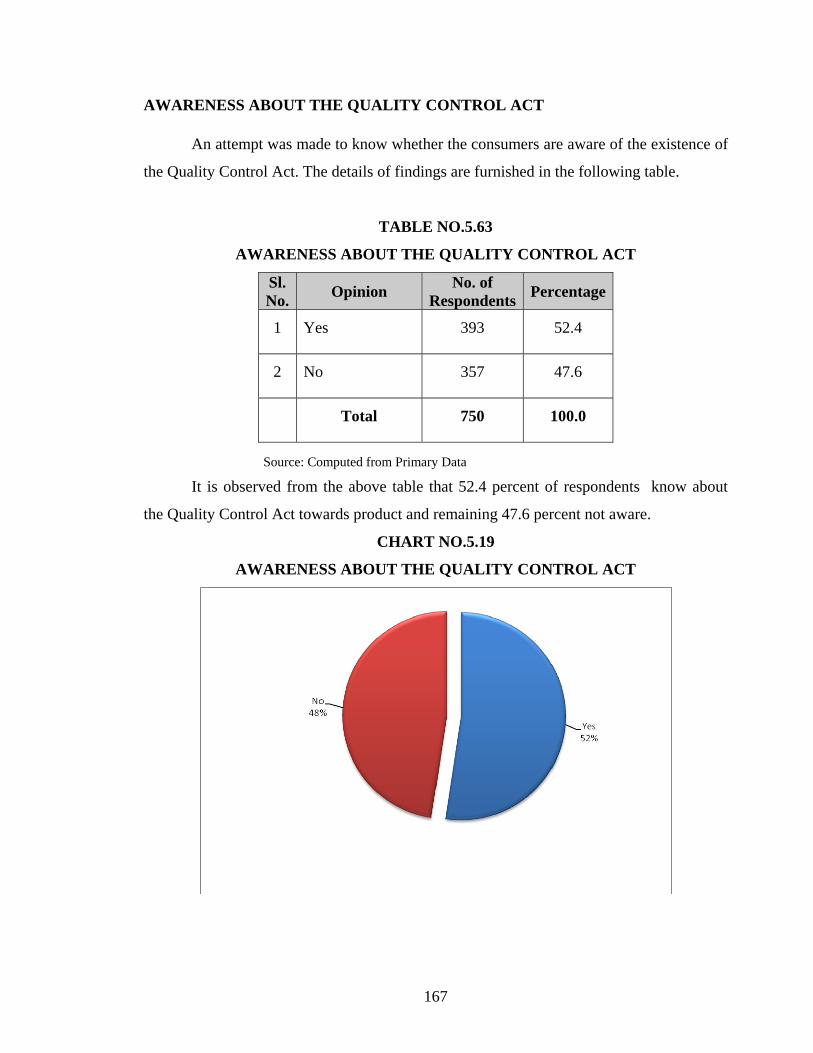

TABLE NO. 5.1

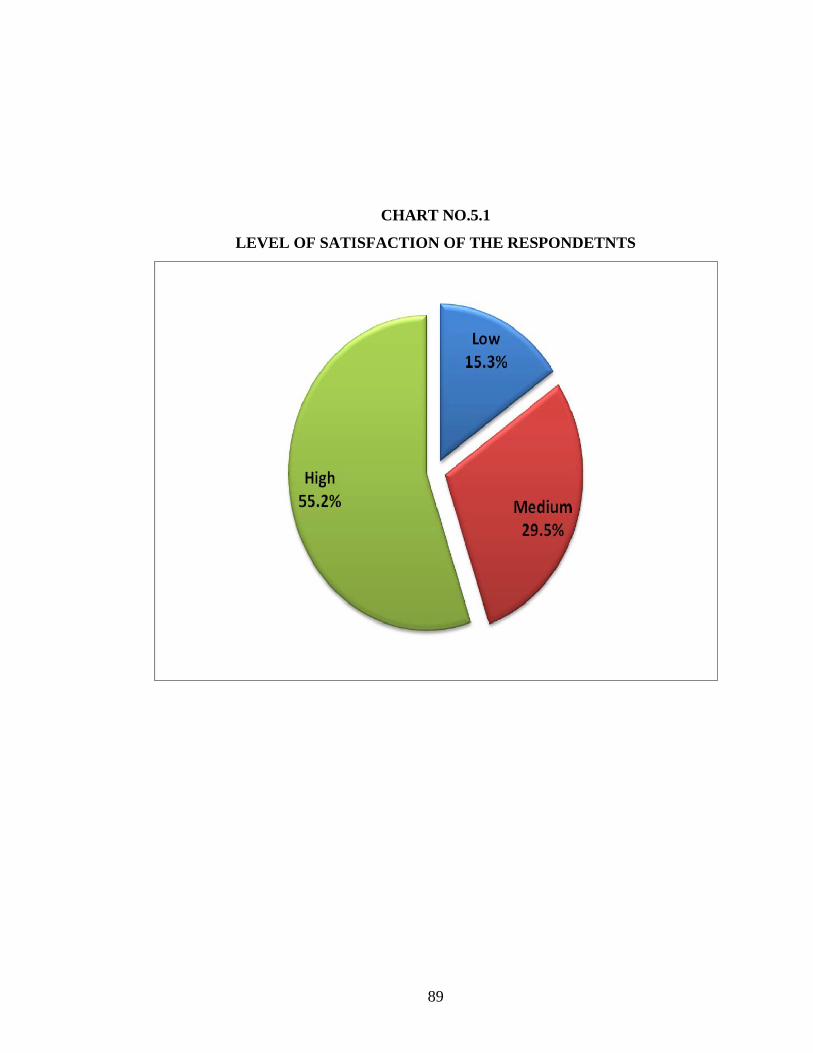

LEVEL OF SATISFACTION OF THE RESPONDENTS

Sl. No. Category No. of

Respondents Percentage

1. Low (below 75) 115 15.3

2. Medium (76-90) 221 29.5

3. High (91-100) 414 55.2

Total 750 100.0

Source: Computed from Primary Data

It is observed from the above table that 15.3 percent of the respondents expressed

their level of satisfaction at the low level. It is followed by 29.5 percent at the medium

level and 55.2 percent of the respondents expressed satisfaction at the high level. The two-

way analysis was prepared based on these three strata for data analysis and through this

method chi-square test was employed to test the relationship between the selected

independent variables and dependent variable.

It is concluded that majority (55.2%) of the respondents are highly satisfied with

regard to the household electronic products.

89

CHART NO.5.1

LEVEL OF SATISFACTION OF THE RESPONDETNTS

90

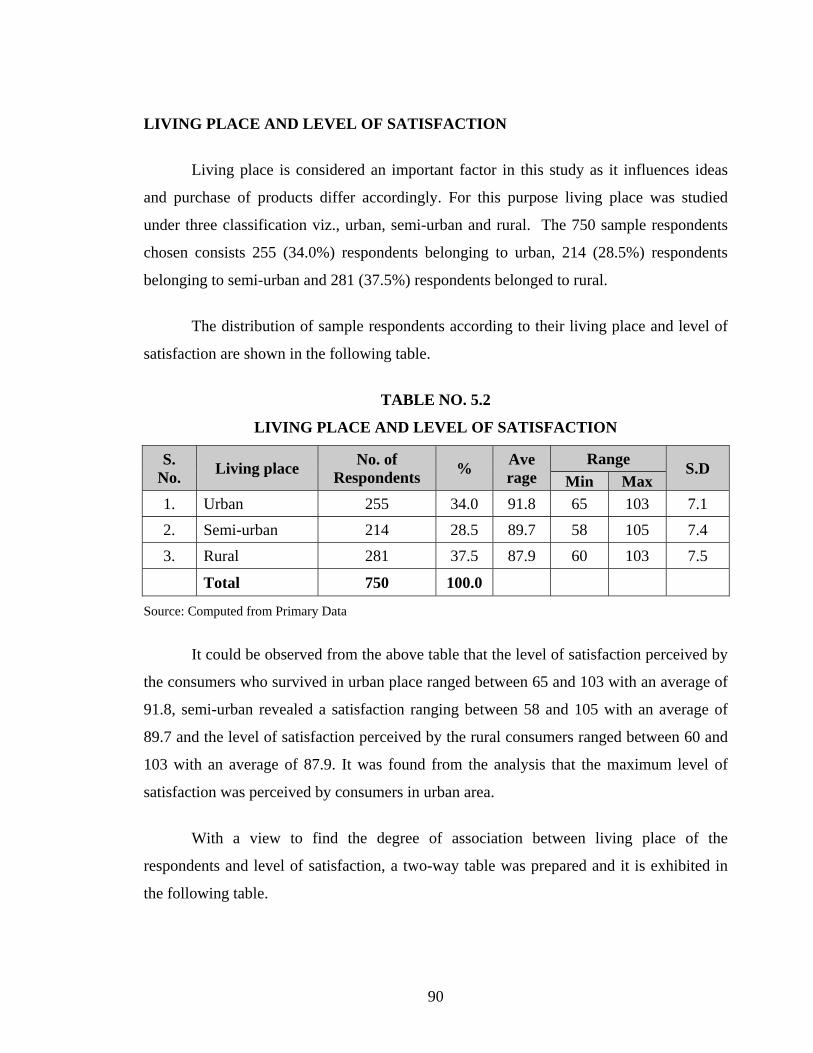

LIVING PLACE AND LEVEL OF SATISFACTION

Living place is considered an important factor in this study as it influences ideas

and purchase of products differ accordingly. For this purpose living place was studied

under three classification viz., urban, semi-urban and rural. The 750 sample respondents

chosen consists 255 (34.0%) respondents belonging to urban, 214 (28.5%) respondents

belonging to semi-urban and 281 (37.5%) respondents belonged to rural.

The distribution of sample respondents according to their living place and level of

satisfaction are shown in the following table.

TABLE NO. 5.2

LIVING PLACE AND LEVEL OF SATISFACTION

S. No. Living place No. of

Respondents % Ave rage

Range S.D Min Max

1. Urban 255 34.0 91.8 65 103 7.1 2. Semi-urban 214 28.5 89.7 58 105 7.4 3. Rural 281 37.5 87.9 60 103 7.5

Total 750 100.0

Source: Computed from Primary Data

It could be observed from the above table that the level of satisfaction perceived by

the consumers who survived in urban place ranged between 65 and 103 with an average of

91.8, semi-urban revealed a satisfaction ranging between 58 and 105 with an average of

89.7 and the level of satisfaction perceived by the rural consumers ranged between 60 and

103 with an average of 87.9. It was found from the analysis that the maximum level of

satisfaction was perceived by consumers in urban area.

With a view to find the degree of association between living place of the

respondents and level of satisfaction, a two-way table was prepared and it is exhibited in

the following table.

91

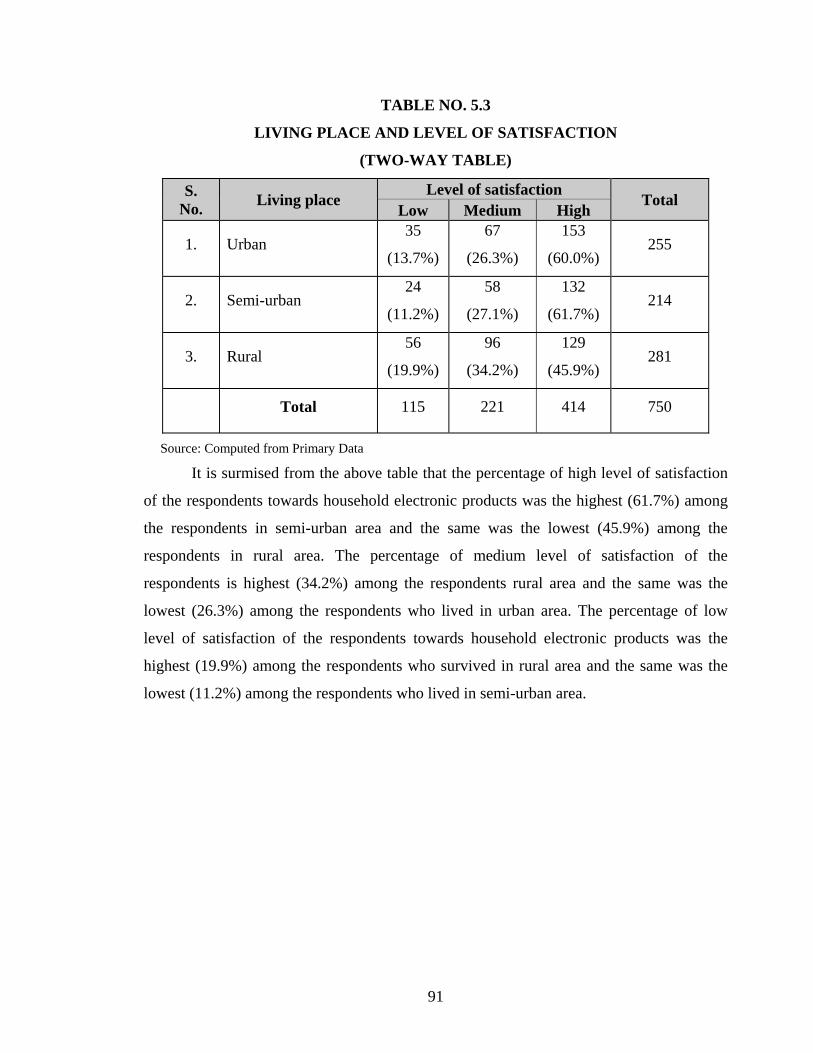

TABLE NO. 5.3

LIVING PLACE AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No. Living place

Level of satisfaction Total Low Medium High

1. Urban 35

(13.7%)

67

(26.3%)

153

(60.0%) 255

2. Semi-urban 24

(11.2%)

58

(27.1%)

132

(61.7%) 214

3. Rural 56

(19.9%)

96

(34.2%)

129

(45.9%) 281

Total 115 221 414 750

Source: Computed from Primary Data

It is surmised from the above table that the percentage of high level of satisfaction

of the respondents towards household electronic products was the highest (61.7%) among

the respondents in semi-urban area and the same was the lowest (45.9%) among the

respondents in rural area. The percentage of medium level of satisfaction of the

respondents is highest (34.2%) among the respondents rural area and the same was the

lowest (26.3%) among the respondents who lived in urban area. The percentage of low

level of satisfaction of the respondents towards household electronic products was the

highest (19.9%) among the respondents who survived in rural area and the same was the

lowest (11.2%) among the respondents who lived in semi-urban area.

92

In order to find the relationship between the living area of the respondents and level

of satisfaction, the following null hypothesis has been framed and tested with the help of

Chi-square test and the result is shown in the following table.

H0 : There is no significant relationship between living place of the respondents

and their level of satisfaction.

H1 : There is a significant relationship between living place of the respondents

and their level of satisfaction.

TABLE NO. 5.4

LIVING PLACE AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Living place 17.148 13.277 4 Significant at 1%

level

Source: Computed

It is evident from the above table that the calculated chi-square value is greater than

the table value and the result is significant at 1% level. Hence, the hypothesis, viz., “living

place of the respondents and level of satisfaction are not associated”, does not hold good.

From the analysis, it is found that there is a close relationship between the living place of

the respondents and level of satisfaction.

93

AGE AND LEVEL OF SATISFACTION

Age is a prominent factor in deciding the level of satisfaction towards the

household electronic products. For this purpose, age of the consumers was classified into

four groups viz., below 25 years, 26-35 years, 36-45 years and above 45 years. The

sample consists of 193 (25.7%) respondents below 25 years age group, 225 (30.0%)

respondents were of 26-35 years age group, 195 (26.0%) respondents were of 36-45 years

age group and 137 (18.3%) respondents belonged to above 45 years group.

The distribution of sample respondents according to the age of the respondents and

their level of satisfaction are shown in the following table.

TABLE NO. 5.5

AGE AND LEVEL OF SATISFACTION

S. No.

Age (in years)

No. of Respondents % Ave

rage

Range S.D Min Max

1. Below 25 193 25.7 89.8 65 104 7.9 2. 26-35 225 30.0 88.9 58 105 7.8 3. 36-45 195 26.0 90.2 65 103 7.3 4. Above 45 137 18.3 88.3 72 102 6.1 Total 750 100.0

Source: Computed from Primary Data

It could be observed from the above table that the level of satisfaction of the

respondents below 25 years towards household electronic products ranged between 65 and

104 with an average of 89.8. The respondents in the age group between 26 and 35 years

revealed their level of satisfaction ranging between 58 and 105 with an average of 88.9, the

level of satisfaction of the respondents between 36 and 45 years age group ranged between

65 and 103 with an average of 90.2 and respondents in the above 45 years group revealed

their level of satisfaction ranging between 72 and 102 with an average of 88.3. It was

found from the analysis that the maximum level of satisfaction of the respondents towards

household electronic products was among the age group between 36 and 45 years.

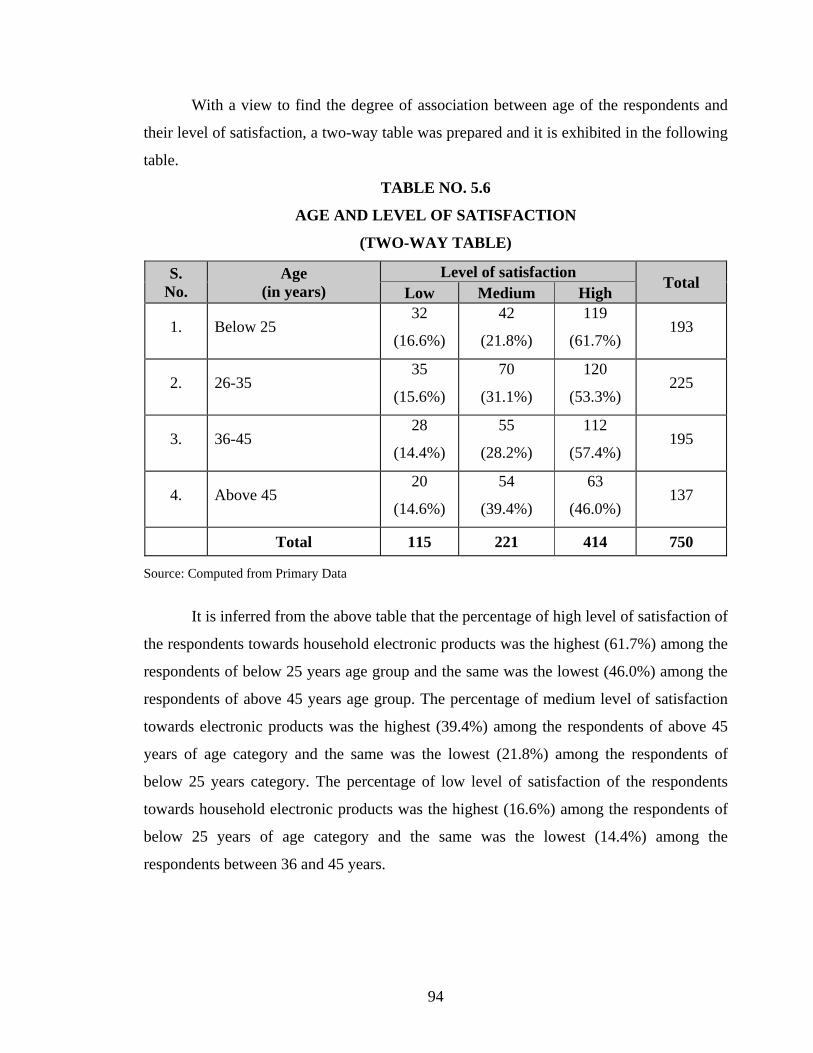

94

With a view to find the degree of association between age of the respondents and

their level of satisfaction, a two-way table was prepared and it is exhibited in the following

table.

TABLE NO. 5.6

AGE AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No.

Age (in years)

Level of satisfaction Total Low Medium High

1. Below 25 32

(16.6%)

42

(21.8%)

119

(61.7%) 193

2. 26-35 35

(15.6%)

70

(31.1%)

120

(53.3%) 225

3. 36-45 28

(14.4%)

55

(28.2%)

112

(57.4%) 195

4. Above 45 20

(14.6%)

54

(39.4%)

63

(46.0%) 137

Total 115 221 414 750

Source: Computed from Primary Data

It is inferred from the above table that the percentage of high level of satisfaction of

the respondents towards household electronic products was the highest (61.7%) among the

respondents of below 25 years age group and the same was the lowest (46.0%) among the

respondents of above 45 years age group. The percentage of medium level of satisfaction

towards electronic products was the highest (39.4%) among the respondents of above 45

years of age category and the same was the lowest (21.8%) among the respondents of

below 25 years category. The percentage of low level of satisfaction of the respondents

towards household electronic products was the highest (16.6%) among the respondents of

below 25 years of age category and the same was the lowest (14.4%) among the

respondents between 36 and 45 years.

95

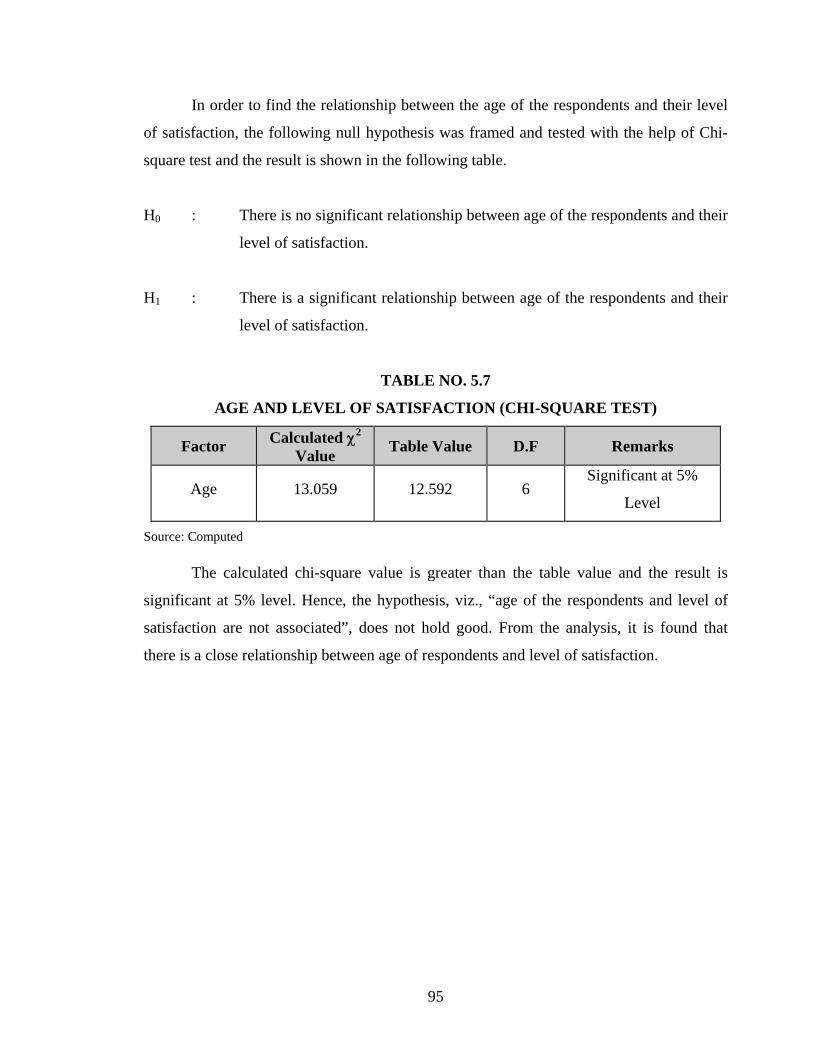

In order to find the relationship between the age of the respondents and their level

of satisfaction, the following null hypothesis was framed and tested with the help of Chi-

square test and the result is shown in the following table.

H0 : There is no significant relationship between age of the respondents and their

level of satisfaction.

H1 : There is a significant relationship between age of the respondents and their

level of satisfaction.

TABLE NO. 5.7

AGE AND LEVEL OF SATISFACTION (CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Age 13.059 12.592 6 Significant at 5%

Level

Source: Computed

The calculated chi-square value is greater than the table value and the result is

significant at 5% level. Hence, the hypothesis, viz., “age of the respondents and level of

satisfaction are not associated”, does not hold good. From the analysis, it is found that

there is a close relationship between age of respondents and level of satisfaction.

96

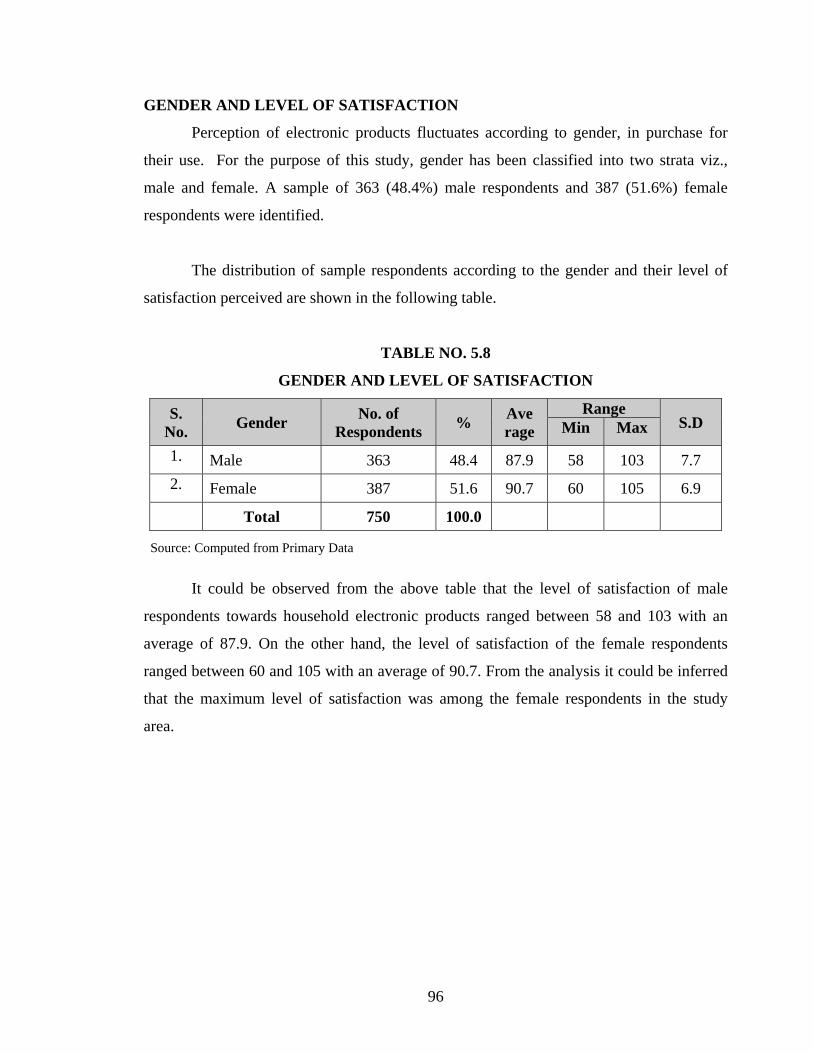

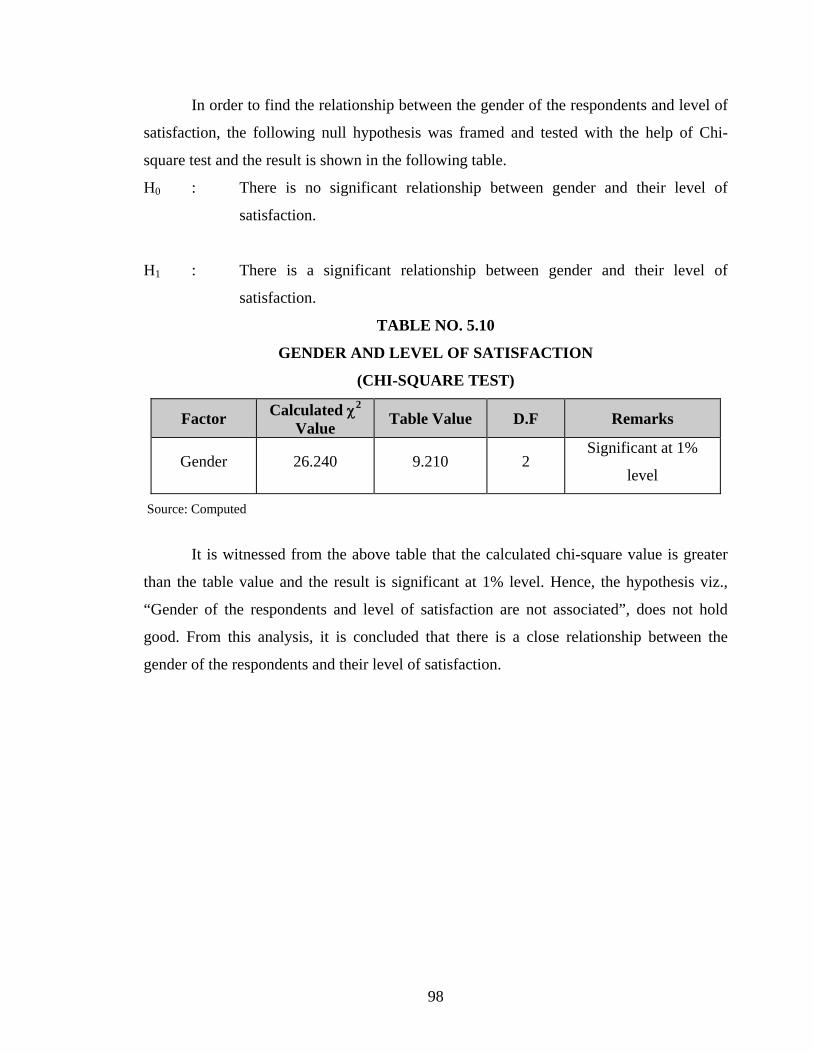

GENDER AND LEVEL OF SATISFACTION

Perception of electronic products fluctuates according to gender, in purchase for

their use. For the purpose of this study, gender has been classified into two strata viz.,

male and female. A sample of 363 (48.4%) male respondents and 387 (51.6%) female

respondents were identified.

The distribution of sample respondents according to the gender and their level of

satisfaction perceived are shown in the following table.

TABLE NO. 5.8

GENDER AND LEVEL OF SATISFACTION

S. No. Gender No. of

Respondents % Ave rage

Range S.D Min Max

1. Male 363 48.4 87.9 58 103 7.7 2. Female 387 51.6 90.7 60 105 6.9 Total 750 100.0

Source: Computed from Primary Data

It could be observed from the above table that the level of satisfaction of male

respondents towards household electronic products ranged between 58 and 103 with an

average of 87.9. On the other hand, the level of satisfaction of the female respondents

ranged between 60 and 105 with an average of 90.7. From the analysis it could be inferred

that the maximum level of satisfaction was among the female respondents in the study

area.

97

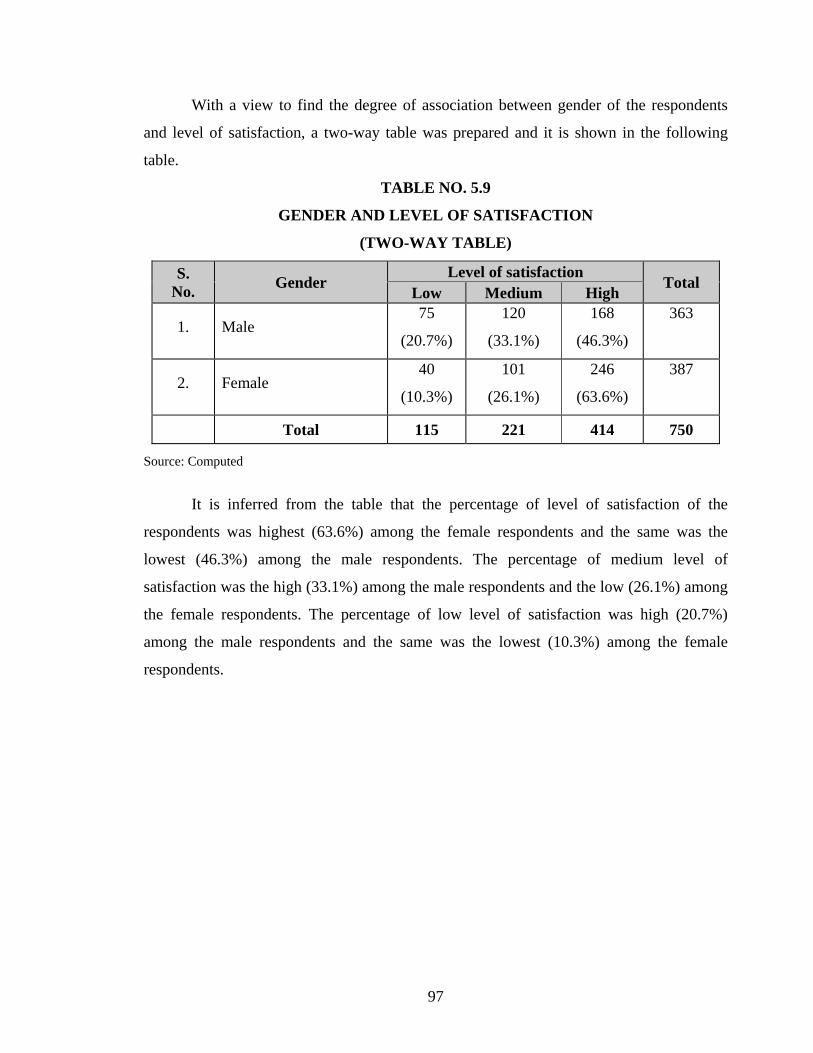

With a view to find the degree of association between gender of the respondents

and level of satisfaction, a two-way table was prepared and it is shown in the following

table.

TABLE NO. 5.9

GENDER AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No. Gender

Level of satisfaction Total Low Medium High

1. Male 75

(20.7%)

120

(33.1%)

168

(46.3%)

363

2. Female 40

(10.3%)

101

(26.1%)

246

(63.6%)

387

Total 115 221 414 750

Source: Computed

It is inferred from the table that the percentage of level of satisfaction of the

respondents was highest (63.6%) among the female respondents and the same was the

lowest (46.3%) among the male respondents. The percentage of medium level of

satisfaction was the high (33.1%) among the male respondents and the low (26.1%) among

the female respondents. The percentage of low level of satisfaction was high (20.7%)

among the male respondents and the same was the lowest (10.3%) among the female

respondents.

98

In order to find the relationship between the gender of the respondents and level of

satisfaction, the following null hypothesis was framed and tested with the help of Chi-

square test and the result is shown in the following table.

H0 : There is no significant relationship between gender and their level of

satisfaction.

H1 : There is a significant relationship between gender and their level of

satisfaction.

TABLE NO. 5.10

GENDER AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Gender 26.240 9.210 2 Significant at 1%

level

Source: Computed

It is witnessed from the above table that the calculated chi-square value is greater

than the table value and the result is significant at 1% level. Hence, the hypothesis viz.,

“Gender of the respondents and level of satisfaction are not associated”, does not hold

good. From this analysis, it is concluded that there is a close relationship between the

gender of the respondents and their level of satisfaction.

99

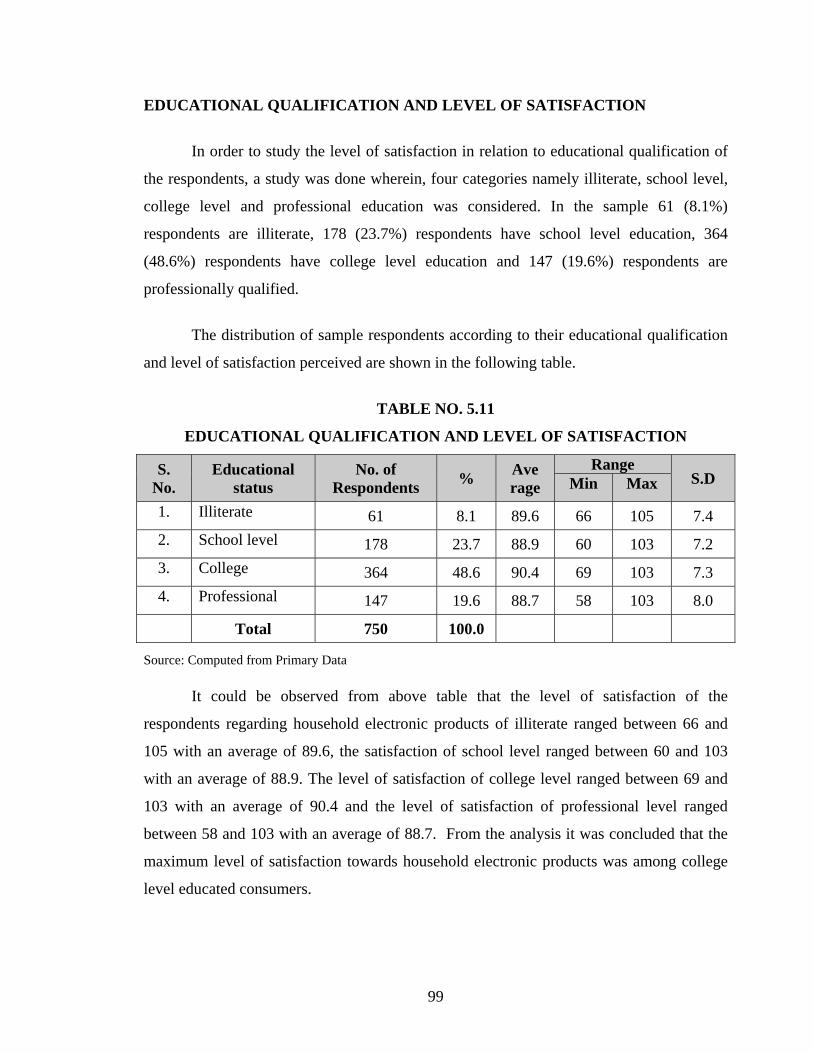

EDUCATIONAL QUALIFICATION AND LEVEL OF SATISFACTION

In order to study the level of satisfaction in relation to educational qualification of

the respondents, a study was done wherein, four categories namely illiterate, school level,

college level and professional education was considered. In the sample 61 (8.1%)

respondents are illiterate, 178 (23.7%) respondents have school level education, 364

(48.6%) respondents have college level education and 147 (19.6%) respondents are

professionally qualified.

The distribution of sample respondents according to their educational qualification

and level of satisfaction perceived are shown in the following table.

TABLE NO. 5.11

EDUCATIONAL QUALIFICATION AND LEVEL OF SATISFACTION

S. No.

Educational status

No. of Respondents % Ave

rage Range

S.D Min Max

1. Illiterate 61 8.1 89.6 66 105 7.4 2. School level 178 23.7 88.9 60 103 7.2 3. College 364 48.6 90.4 69 103 7.3 4. Professional 147 19.6 88.7 58 103 8.0 Total 750 100.0

Source: Computed from Primary Data

It could be observed from above table that the level of satisfaction of the

respondents regarding household electronic products of illiterate ranged between 66 and

105 with an average of 89.6, the satisfaction of school level ranged between 60 and 103

with an average of 88.9. The level of satisfaction of college level ranged between 69 and

103 with an average of 90.4 and the level of satisfaction of professional level ranged

between 58 and 103 with an average of 88.7. From the analysis it was concluded that the

maximum level of satisfaction towards household electronic products was among college

level educated consumers.

100

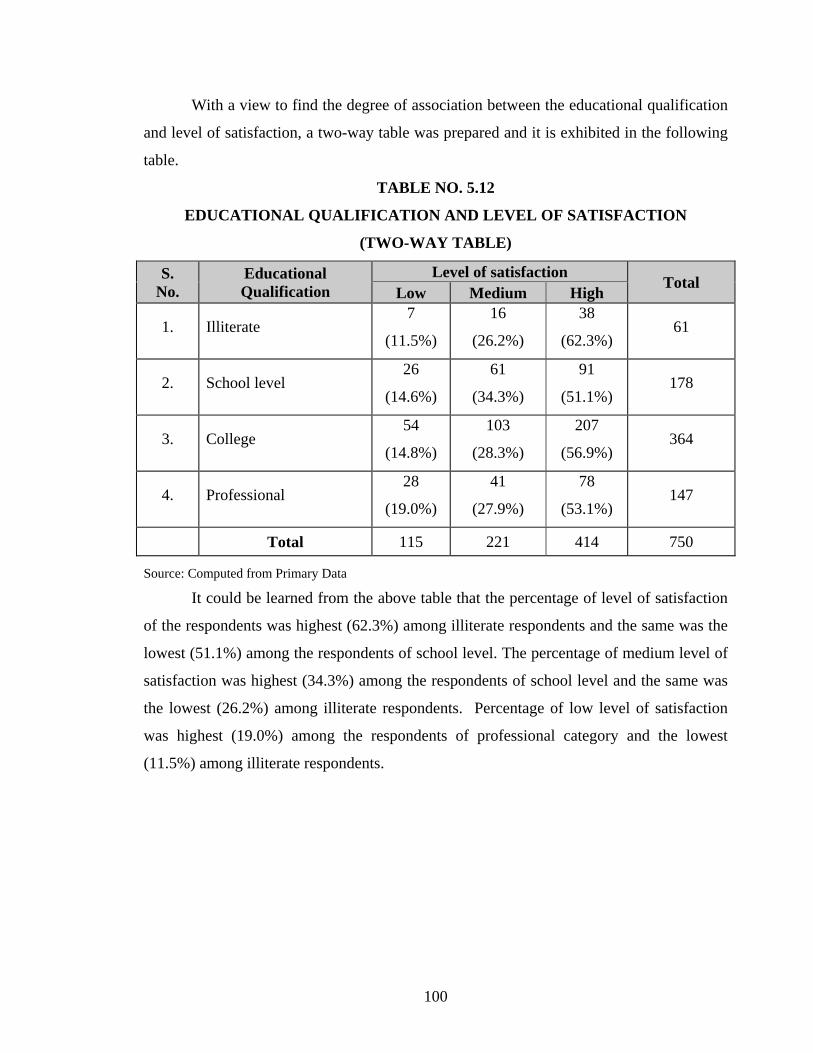

With a view to find the degree of association between the educational qualification

and level of satisfaction, a two-way table was prepared and it is exhibited in the following

table.

TABLE NO. 5.12

EDUCATIONAL QUALIFICATION AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No.

Educational Qualification

Level of satisfaction Total Low Medium High

1. Illiterate 7

(11.5%)

16

(26.2%)

38

(62.3%) 61

2. School level 26

(14.6%)

61

(34.3%)

91

(51.1%) 178

3. College 54

(14.8%)

103

(28.3%)

207

(56.9%) 364

4. Professional 28

(19.0%)

41

(27.9%)

78

(53.1%) 147

Total 115 221 414 750

Source: Computed from Primary Data

It could be learned from the above table that the percentage of level of satisfaction

of the respondents was highest (62.3%) among illiterate respondents and the same was the

lowest (51.1%) among the respondents of school level. The percentage of medium level of

satisfaction was highest (34.3%) among the respondents of school level and the same was

the lowest (26.2%) among illiterate respondents. Percentage of low level of satisfaction

was highest (19.0%) among the respondents of professional category and the lowest

(11.5%) among illiterate respondents.

101

In order to find the relationship between the educational qualification of the

respondents and level of satisfaction, the following null hypothesis was framed and tested

with the help of Chi-square test and the result is shown in the following table.

H0 : There is no significant relationship between educational qualification and

level of satisfaction.

H1 : There is a significant relationship between educational qualification and

level of satisfaction.

TABLE NO. 5.13

EDUCATIONAL QUALIFICATION AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Educational

status 5.336 12.592 6 Not Significant

Source: Computed It is divulged from the table that the calculated chi-square value is less than the

table value and the result is not significant. Hence, the hypothesis “education qualification

of the respondents and their level of satisfaction are not associated”, holds good. From the

analysis it is concluded that there is no relationship between educational qualification of

the respondents and level of satisfaction.

102

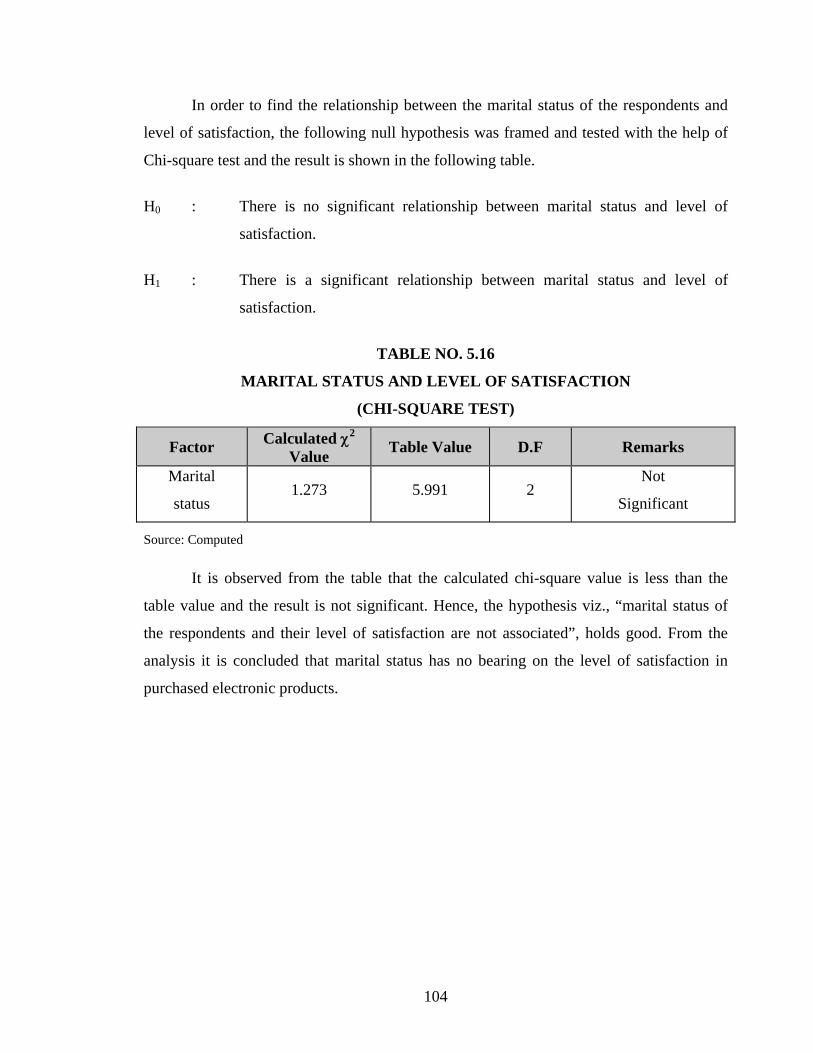

MARITAL STATUS AND LEVEL OF SATISFACTION

Marital status plays an important role in purchase of household electronic products

and study was conducted to learn their level of satisfaction under two categories namely

married and unmarried. The sample chosen consists 383 (51.1%) married respondents and

367 (48.9%) in unmarried category.

The distribution of sample respondents according to the marital status of the

respondents and level of satisfaction are shown in the following table.

TABLE NO. 5.14

MARITAL STATUS AND LEVEL OF SATISFACTION

S.

No. Marital status No. of

Respondents % Ave rage

Range S.D Min Max

1. Married 383 51.1 89.7 65 105 7.5 2. Unmarried 367 48.9 89.0 58 104 7.3 Total 750 100.0

Source: Computed from Primary Data

It could be inferred from the above table that the level of satisfaction of the

respondents towards household electronic products by the married respondents ranged

between 65 and 105 with an average of 89.7 percent and the level of satisfaction of the

respondents towards household electronic products by the unmarried respondents ranged

between 58 and 104 with an average of 89.0. From the analysis it was concluded that the

maximum level of satisfaction was attained by married consumers towards household

electronic products.

103

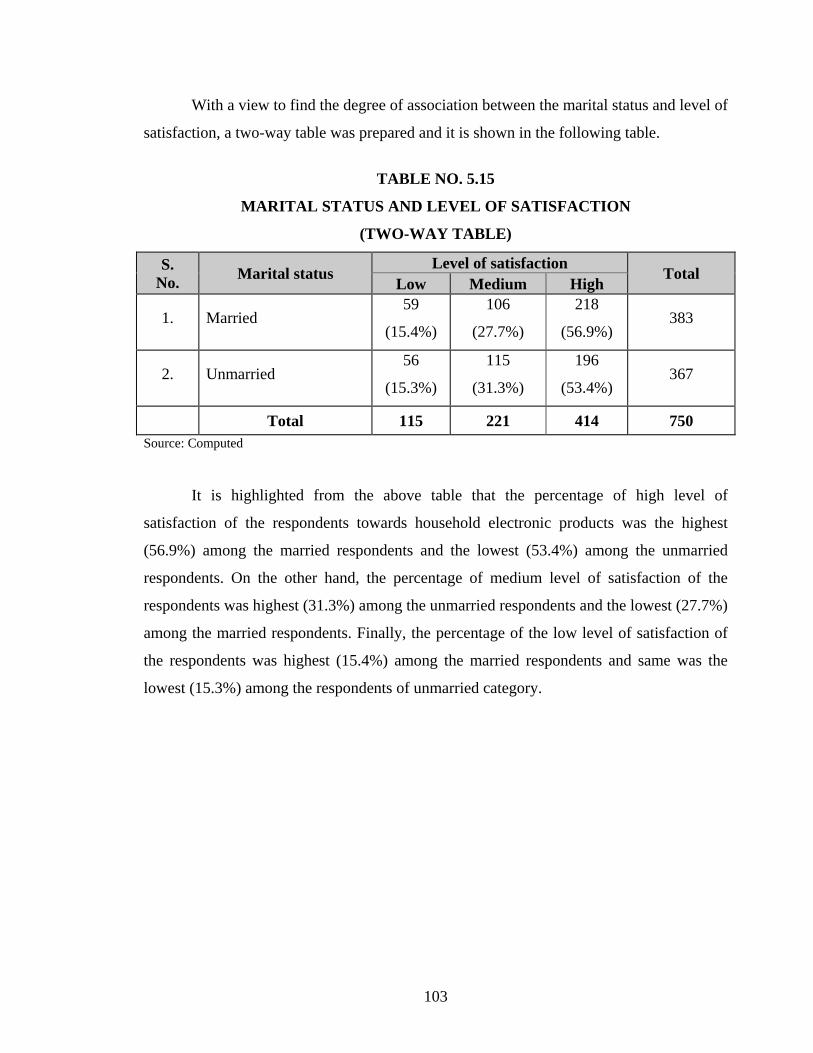

With a view to find the degree of association between the marital status and level of

satisfaction, a two-way table was prepared and it is shown in the following table.

TABLE NO. 5.15

MARITAL STATUS AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No. Marital status Level of satisfaction Total Low Medium High

1. Married 59

(15.4%)

106

(27.7%)

218

(56.9%) 383

2. Unmarried 56

(15.3%)

115

(31.3%)

196

(53.4%) 367

Total 115 221 414 750 Source: Computed

It is highlighted from the above table that the percentage of high level of

satisfaction of the respondents towards household electronic products was the highest

(56.9%) among the married respondents and the lowest (53.4%) among the unmarried

respondents. On the other hand, the percentage of medium level of satisfaction of the

respondents was highest (31.3%) among the unmarried respondents and the lowest (27.7%)

among the married respondents. Finally, the percentage of the low level of satisfaction of

the respondents was highest (15.4%) among the married respondents and same was the

lowest (15.3%) among the respondents of unmarried category.

104

In order to find the relationship between the marital status of the respondents and

level of satisfaction, the following null hypothesis was framed and tested with the help of

Chi-square test and the result is shown in the following table.

H0 : There is no significant relationship between marital status and level of

satisfaction.

H1 : There is a significant relationship between marital status and level of

satisfaction.

TABLE NO. 5.16

MARITAL STATUS AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Marital

status 1.273 5.991 2

Not

Significant

Source: Computed

It is observed from the table that the calculated chi-square value is less than the

table value and the result is not significant. Hence, the hypothesis viz., “marital status of

the respondents and their level of satisfaction are not associated”, holds good. From the

analysis it is concluded that marital status has no bearing on the level of satisfaction in

purchased electronic products.

105

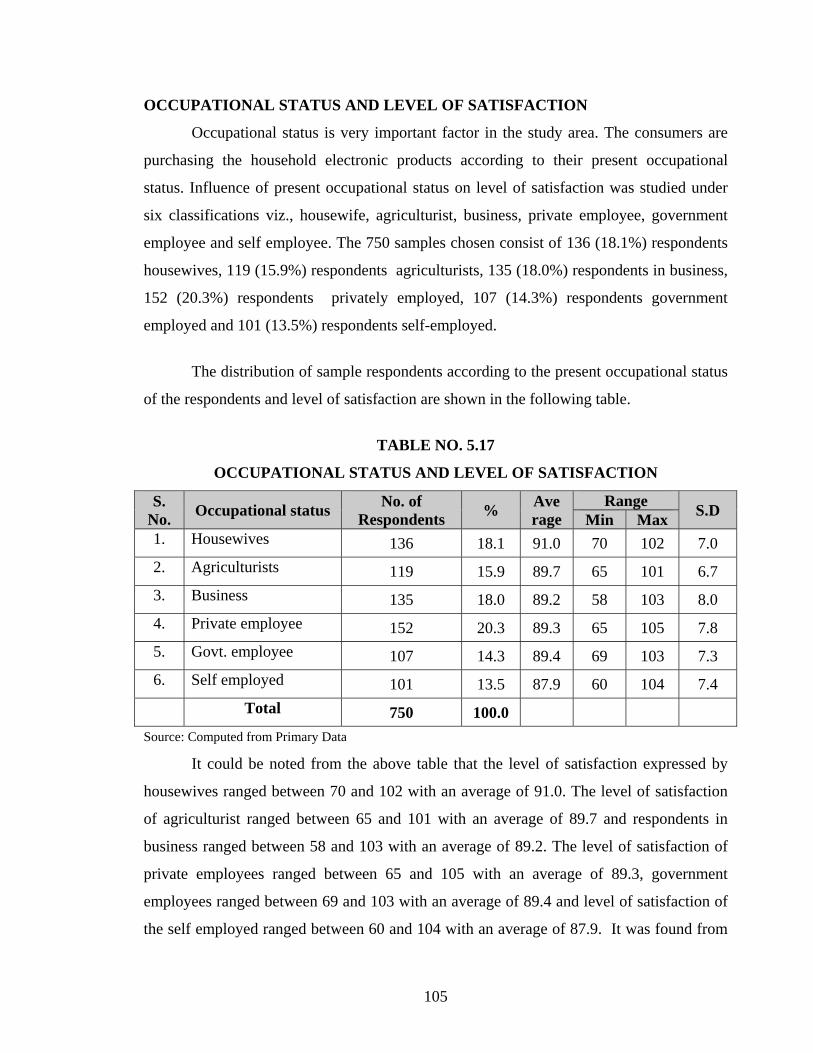

OCCUPATIONAL STATUS AND LEVEL OF SATISFACTION

Occupational status is very important factor in the study area. The consumers are

purchasing the household electronic products according to their present occupational

status. Influence of present occupational status on level of satisfaction was studied under

six classifications viz., housewife, agriculturist, business, private employee, government

employee and self employee. The 750 samples chosen consist of 136 (18.1%) respondents

housewives, 119 (15.9%) respondents agriculturists, 135 (18.0%) respondents in business,

152 (20.3%) respondents privately employed, 107 (14.3%) respondents government

employed and 101 (13.5%) respondents self-employed.

The distribution of sample respondents according to the present occupational status

of the respondents and level of satisfaction are shown in the following table.

TABLE NO. 5.17

OCCUPATIONAL STATUS AND LEVEL OF SATISFACTION

S. No. Occupational status No. of

Respondents % Ave rage

Range S.D Min Max 1. Housewives 136 18.1 91.0 70 102 7.0 2. Agriculturists 119 15.9 89.7 65 101 6.7 3. Business 135 18.0 89.2 58 103 8.0 4. Private employee 152 20.3 89.3 65 105 7.8 5. Govt. employee 107 14.3 89.4 69 103 7.3 6. Self employed 101 13.5 87.9 60 104 7.4 Total 750 100.0

Source: Computed from Primary Data

It could be noted from the above table that the level of satisfaction expressed by

housewives ranged between 70 and 102 with an average of 91.0. The level of satisfaction

of agriculturist ranged between 65 and 101 with an average of 89.7 and respondents in

business ranged between 58 and 103 with an average of 89.2. The level of satisfaction of

private employees ranged between 65 and 105 with an average of 89.3, government

employees ranged between 69 and 103 with an average of 89.4 and level of satisfaction of

the self employed ranged between 60 and 104 with an average of 87.9. It was found from

106

the analysis that the maximum level of satisfaction is perceived by housewives towards

utilizing household electronic products.

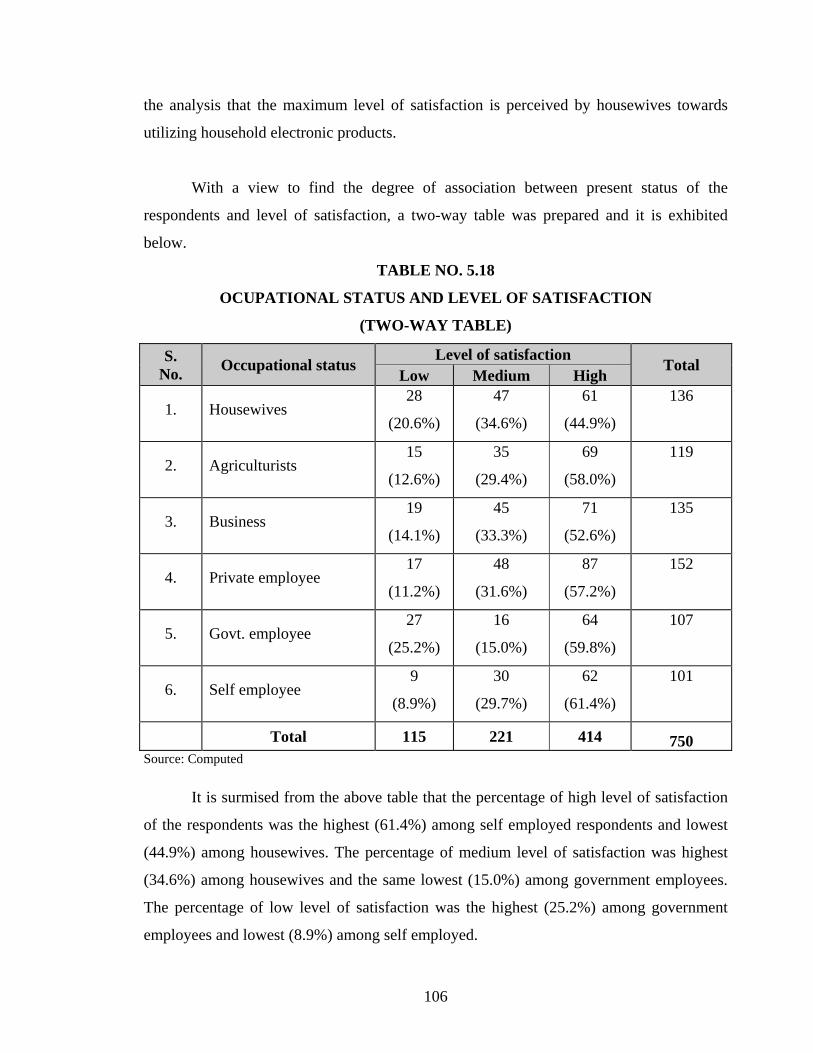

With a view to find the degree of association between present status of the

respondents and level of satisfaction, a two-way table was prepared and it is exhibited

below.

TABLE NO. 5.18

OCUPATIONAL STATUS AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No. Occupational status Level of satisfaction Total

Low Medium High

1. Housewives 28

(20.6%)

47

(34.6%)

61

(44.9%)

136

2. Agriculturists 15

(12.6%)

35

(29.4%)

69

(58.0%)

119

3. Business 19

(14.1%)

45

(33.3%)

71

(52.6%)

135

4. Private employee 17

(11.2%)

48

(31.6%)

87

(57.2%)

152

5. Govt. employee 27

(25.2%)

16

(15.0%)

64

(59.8%)

107

6. Self employee 9

(8.9%)

30

(29.7%)

62

(61.4%)

101

Total 115 221 414 750 Source: Computed

It is surmised from the above table that the percentage of high level of satisfaction

of the respondents was the highest (61.4%) among self employed respondents and lowest

(44.9%) among housewives. The percentage of medium level of satisfaction was highest

(34.6%) among housewives and the same lowest (15.0%) among government employees.

The percentage of low level of satisfaction was the highest (25.2%) among government

employees and lowest (8.9%) among self employed.

107

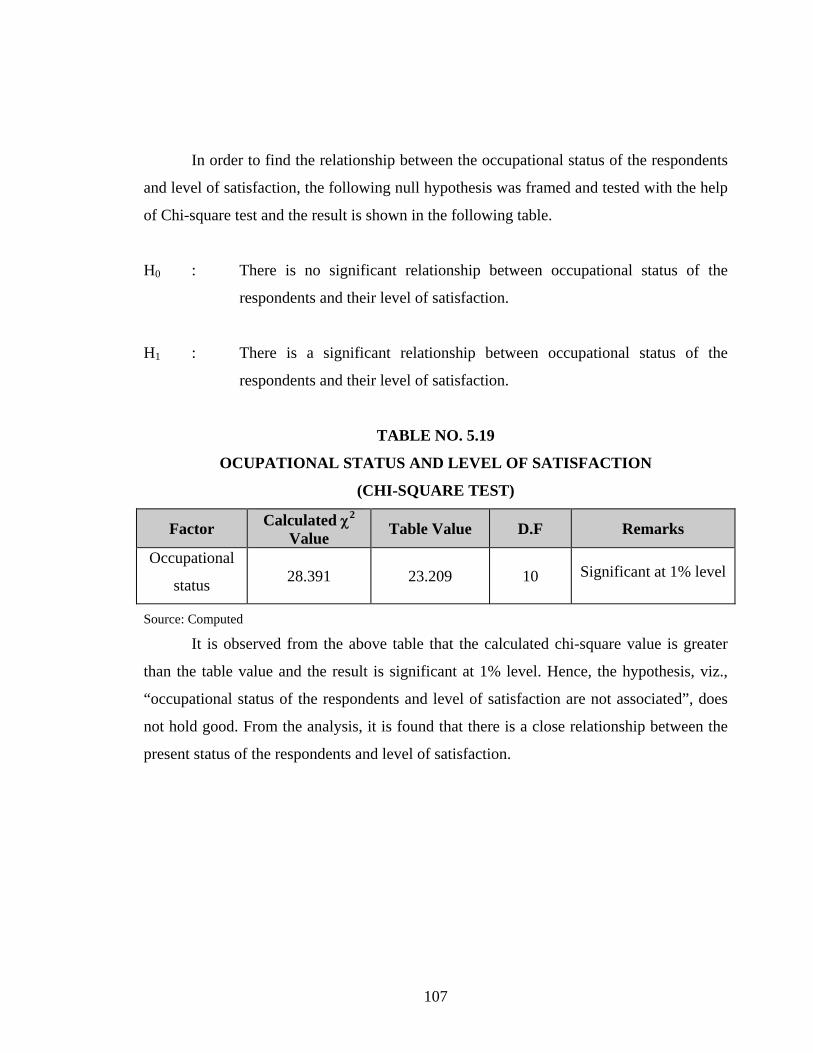

In order to find the relationship between the occupational status of the respondents

and level of satisfaction, the following null hypothesis was framed and tested with the help

of Chi-square test and the result is shown in the following table.

H0 : There is no significant relationship between occupational status of the

respondents and their level of satisfaction.

H1 : There is a significant relationship between occupational status of the

respondents and their level of satisfaction.

TABLE NO. 5.19

OCUPATIONAL STATUS AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Occupational

status 28.391 23.209 10 Significant at 1% level

Source: Computed

It is observed from the above table that the calculated chi-square value is greater

than the table value and the result is significant at 1% level. Hence, the hypothesis, viz.,

“occupational status of the respondents and level of satisfaction are not associated”, does

not hold good. From the analysis, it is found that there is a close relationship between the

present status of the respondents and level of satisfaction.

108

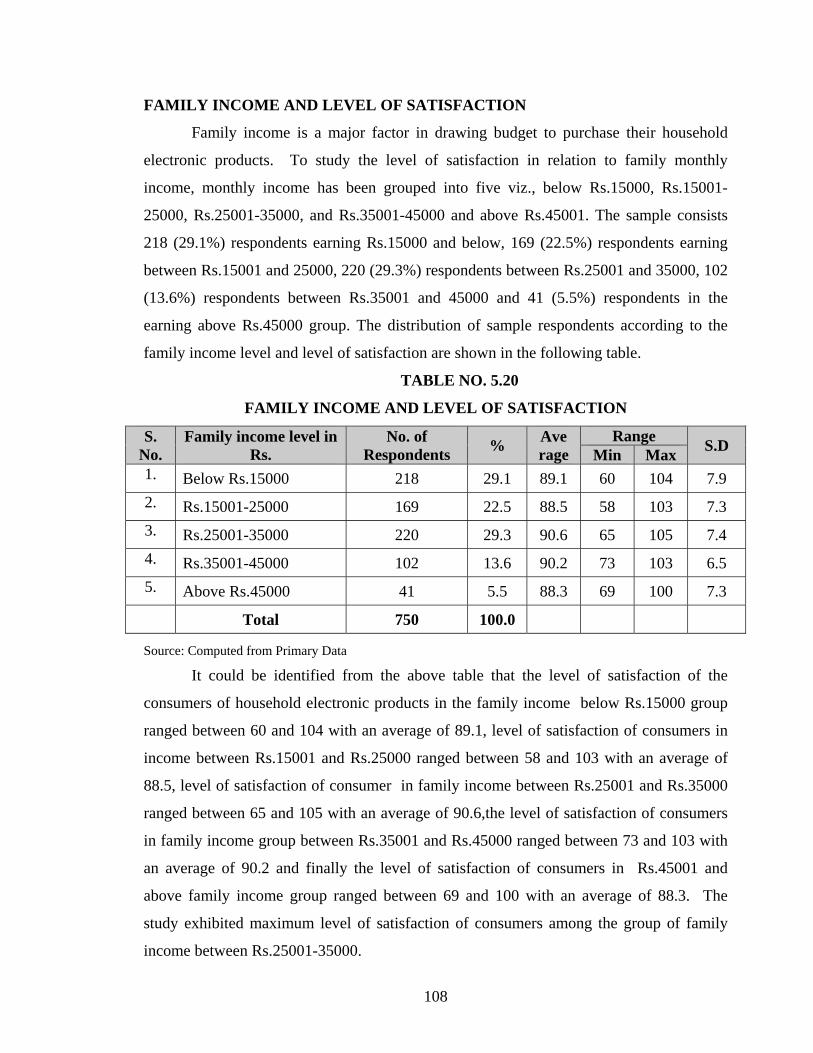

FAMILY INCOME AND LEVEL OF SATISFACTION

Family income is a major factor in drawing budget to purchase their household

electronic products. To study the level of satisfaction in relation to family monthly

income, monthly income has been grouped into five viz., below Rs.15000, Rs.15001-

25000, Rs.25001-35000, and Rs.35001-45000 and above Rs.45001. The sample consists

218 (29.1%) respondents earning Rs.15000 and below, 169 (22.5%) respondents earning

between Rs.15001 and 25000, 220 (29.3%) respondents between Rs.25001 and 35000, 102

(13.6%) respondents between Rs.35001 and 45000 and 41 (5.5%) respondents in the

earning above Rs.45000 group. The distribution of sample respondents according to the

family income level and level of satisfaction are shown in the following table.

TABLE NO. 5.20

FAMILY INCOME AND LEVEL OF SATISFACTION

S. No.

Family income level in Rs.

No. of Respondents % Ave

rage Range S.D Min Max

1. Below Rs.15000 218 29.1 89.1 60 104 7.9 2. Rs.15001-25000 169 22.5 88.5 58 103 7.3 3. Rs.25001-35000 220 29.3 90.6 65 105 7.4 4. Rs.35001-45000 102 13.6 90.2 73 103 6.5 5. Above Rs.45000 41 5.5 88.3 69 100 7.3 Total 750 100.0

Source: Computed from Primary Data

It could be identified from the above table that the level of satisfaction of the

consumers of household electronic products in the family income below Rs.15000 group

ranged between 60 and 104 with an average of 89.1, level of satisfaction of consumers in

income between Rs.15001 and Rs.25000 ranged between 58 and 103 with an average of

88.5, level of satisfaction of consumer in family income between Rs.25001 and Rs.35000

ranged between 65 and 105 with an average of 90.6,the level of satisfaction of consumers

in family income group between Rs.35001 and Rs.45000 ranged between 73 and 103 with

an average of 90.2 and finally the level of satisfaction of consumers in Rs.45001 and

above family income group ranged between 69 and 100 with an average of 88.3. The

study exhibited maximum level of satisfaction of consumers among the group of family

income between Rs.25001-35000.

109

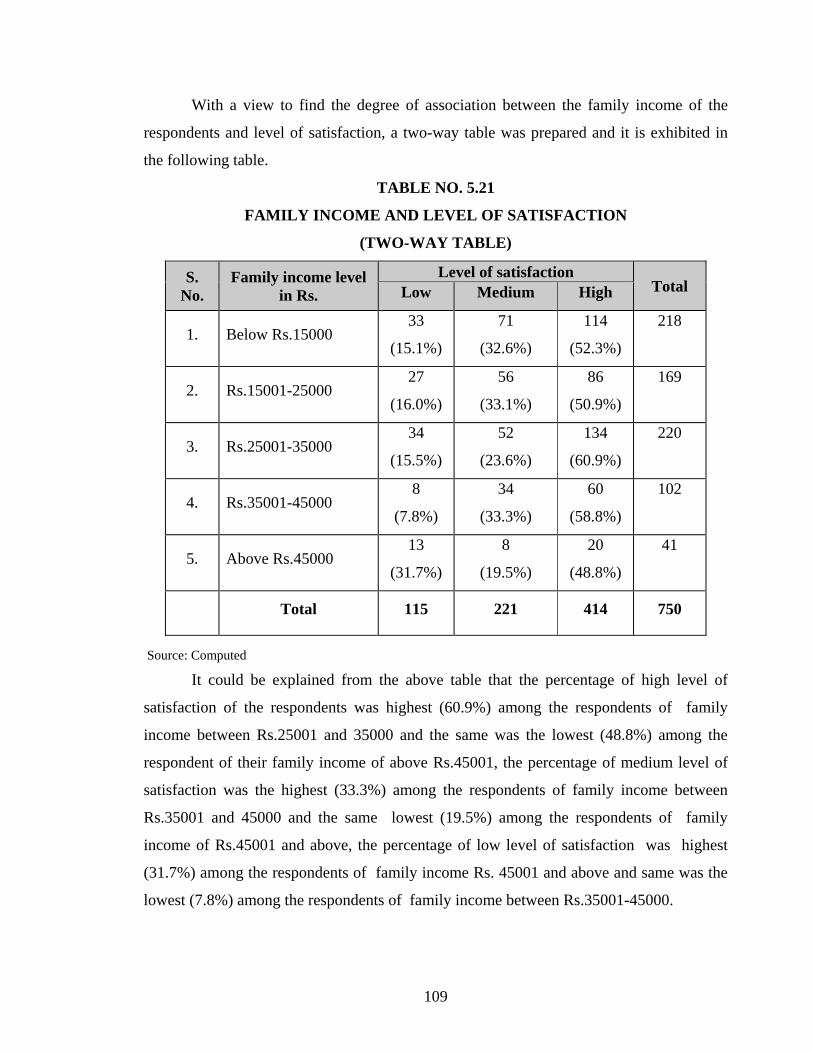

With a view to find the degree of association between the family income of the

respondents and level of satisfaction, a two-way table was prepared and it is exhibited in

the following table.

TABLE NO. 5.21

FAMILY INCOME AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No.

Family income level in Rs.

Level of satisfaction Total Low Medium High

1. Below Rs.15000 33

(15.1%)

71

(32.6%)

114

(52.3%)

218

2. Rs.15001-25000 27

(16.0%)

56

(33.1%)

86

(50.9%)

169

3. Rs.25001-35000 34

(15.5%)

52

(23.6%)

134

(60.9%)

220

4. Rs.35001-45000 8

(7.8%)

34

(33.3%)

60

(58.8%)

102

5. Above Rs.45000 13

(31.7%)

8

(19.5%)

20

(48.8%)

41

Total 115 221 414 750

Source: Computed

It could be explained from the above table that the percentage of high level of

satisfaction of the respondents was highest (60.9%) among the respondents of family

income between Rs.25001 and 35000 and the same was the lowest (48.8%) among the

respondent of their family income of above Rs.45001, the percentage of medium level of

satisfaction was the highest (33.3%) among the respondents of family income between

Rs.35001 and 45000 and the same lowest (19.5%) among the respondents of family

income of Rs.45001 and above, the percentage of low level of satisfaction was highest

(31.7%) among the respondents of family income Rs. 45001 and above and same was the

lowest (7.8%) among the respondents of family income between Rs.35001-45000.

110

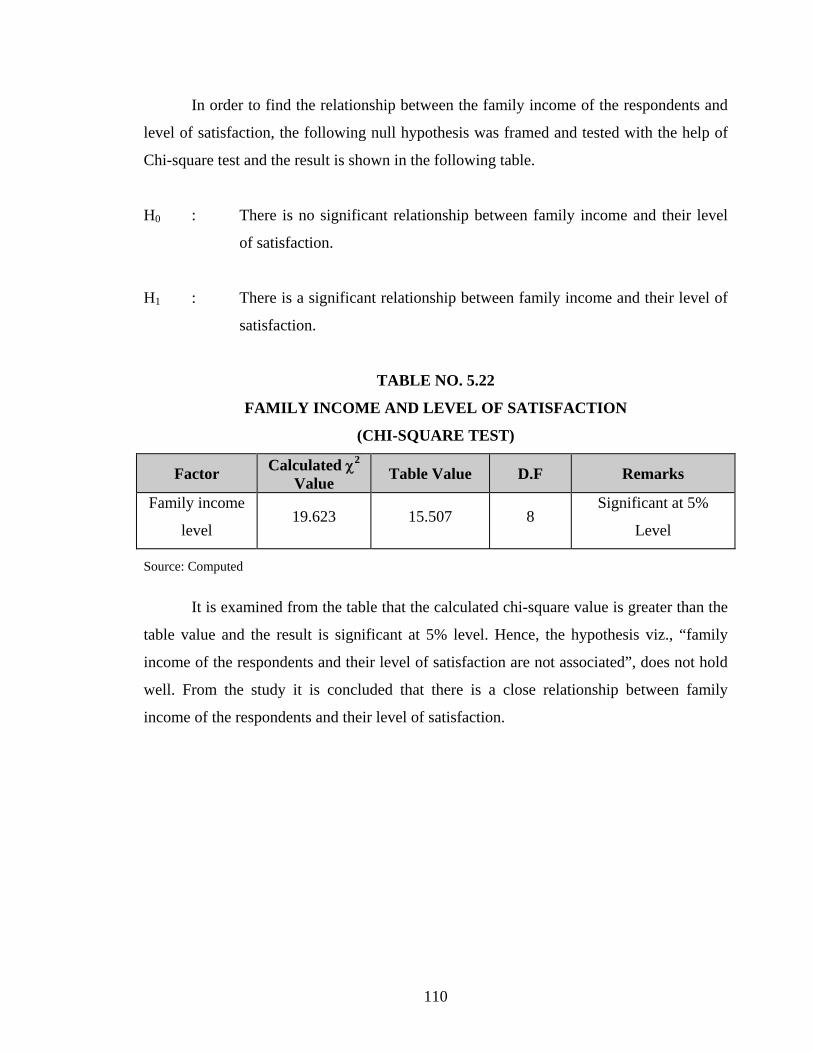

In order to find the relationship between the family income of the respondents and

level of satisfaction, the following null hypothesis was framed and tested with the help of

Chi-square test and the result is shown in the following table.

H0 : There is no significant relationship between family income and their level

of satisfaction.

H1 : There is a significant relationship between family income and their level of

satisfaction.

TABLE NO. 5.22

FAMILY INCOME AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Family income

level 19.623 15.507 8

Significant at 5%

Level

Source: Computed

It is examined from the table that the calculated chi-square value is greater than the

table value and the result is significant at 5% level. Hence, the hypothesis viz., “family

income of the respondents and their level of satisfaction are not associated”, does not hold

well. From the study it is concluded that there is a close relationship between family

income of the respondents and their level of satisfaction.

111

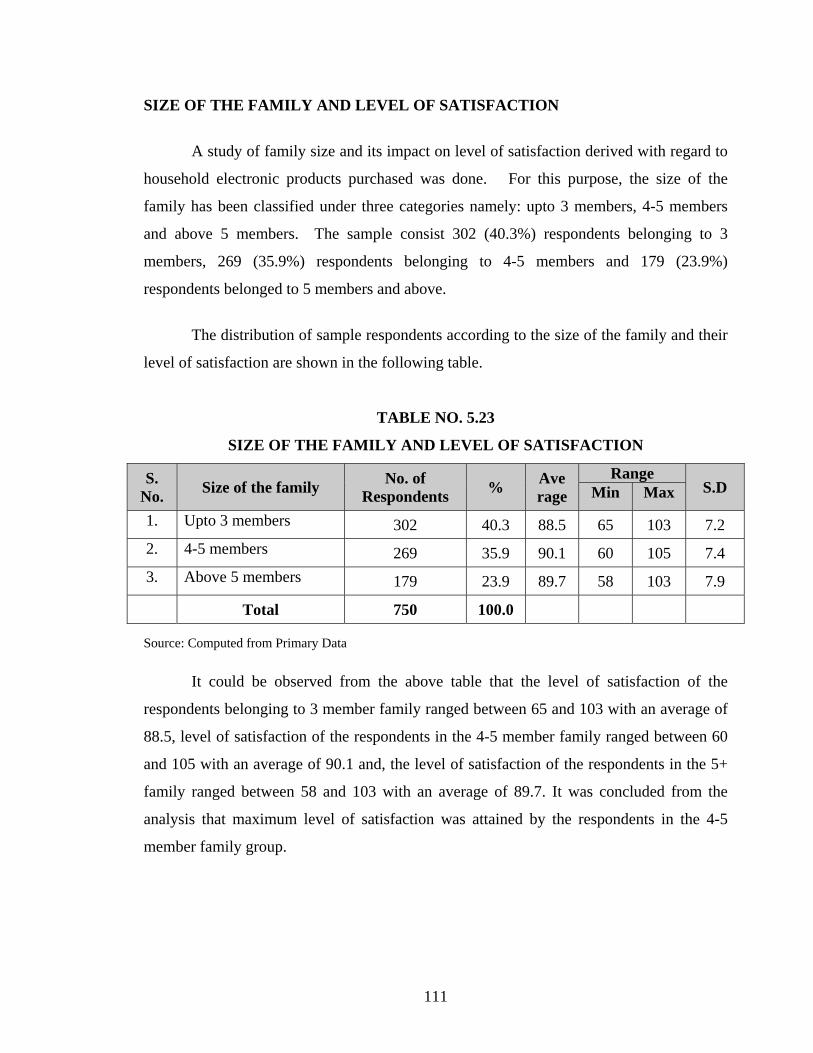

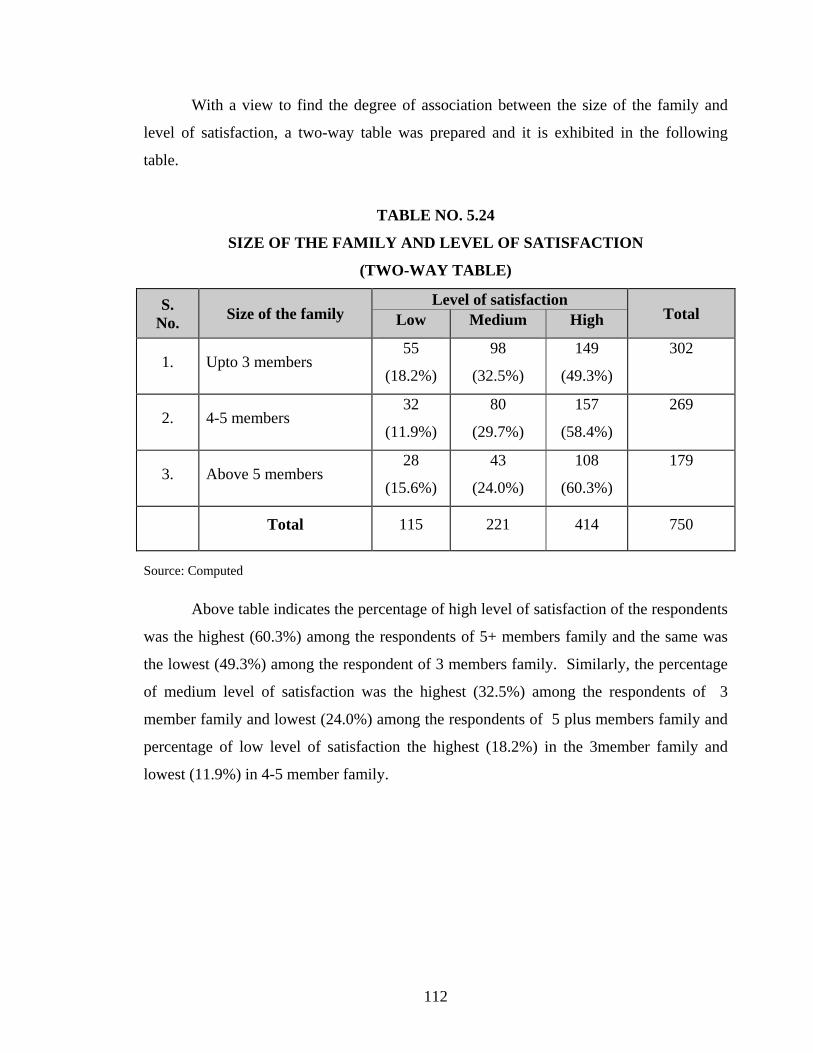

SIZE OF THE FAMILY AND LEVEL OF SATISFACTION

A study of family size and its impact on level of satisfaction derived with regard to

household electronic products purchased was done. For this purpose, the size of the

family has been classified under three categories namely: upto 3 members, 4-5 members

and above 5 members. The sample consist 302 (40.3%) respondents belonging to 3

members, 269 (35.9%) respondents belonging to 4-5 members and 179 (23.9%)

respondents belonged to 5 members and above.

The distribution of sample respondents according to the size of the family and their

level of satisfaction are shown in the following table.

TABLE NO. 5.23

SIZE OF THE FAMILY AND LEVEL OF SATISFACTION

S. No. Size of the family No. of

Respondents % Ave rage

Range S.D Min Max

1. Upto 3 members 302 40.3 88.5 65 103 7.2 2. 4-5 members 269 35.9 90.1 60 105 7.4 3. Above 5 members 179 23.9 89.7 58 103 7.9 Total 750 100.0

Source: Computed from Primary Data

It could be observed from the above table that the level of satisfaction of the

respondents belonging to 3 member family ranged between 65 and 103 with an average of

88.5, level of satisfaction of the respondents in the 4-5 member family ranged between 60

and 105 with an average of 90.1 and, the level of satisfaction of the respondents in the 5+

family ranged between 58 and 103 with an average of 89.7. It was concluded from the

analysis that maximum level of satisfaction was attained by the respondents in the 4-5

member family group.

112

With a view to find the degree of association between the size of the family and

level of satisfaction, a two-way table was prepared and it is exhibited in the following

table.

TABLE NO. 5.24

SIZE OF THE FAMILY AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No. Size of the family

Level of satisfaction Total Low Medium High

1. Upto 3 members 55

(18.2%)

98

(32.5%)

149

(49.3%)

302

2. 4-5 members 32

(11.9%)

80

(29.7%)

157

(58.4%)

269

3. Above 5 members 28

(15.6%)

43

(24.0%)

108

(60.3%)

179

Total 115 221 414 750

Source: Computed

Above table indicates the percentage of high level of satisfaction of the respondents

was the highest (60.3%) among the respondents of 5+ members family and the same was

the lowest (49.3%) among the respondent of 3 members family. Similarly, the percentage

of medium level of satisfaction was the highest (32.5%) among the respondents of 3

member family and lowest (24.0%) among the respondents of 5 plus members family and

percentage of low level of satisfaction the highest (18.2%) in the 3member family and

lowest (11.9%) in 4-5 member family.

113

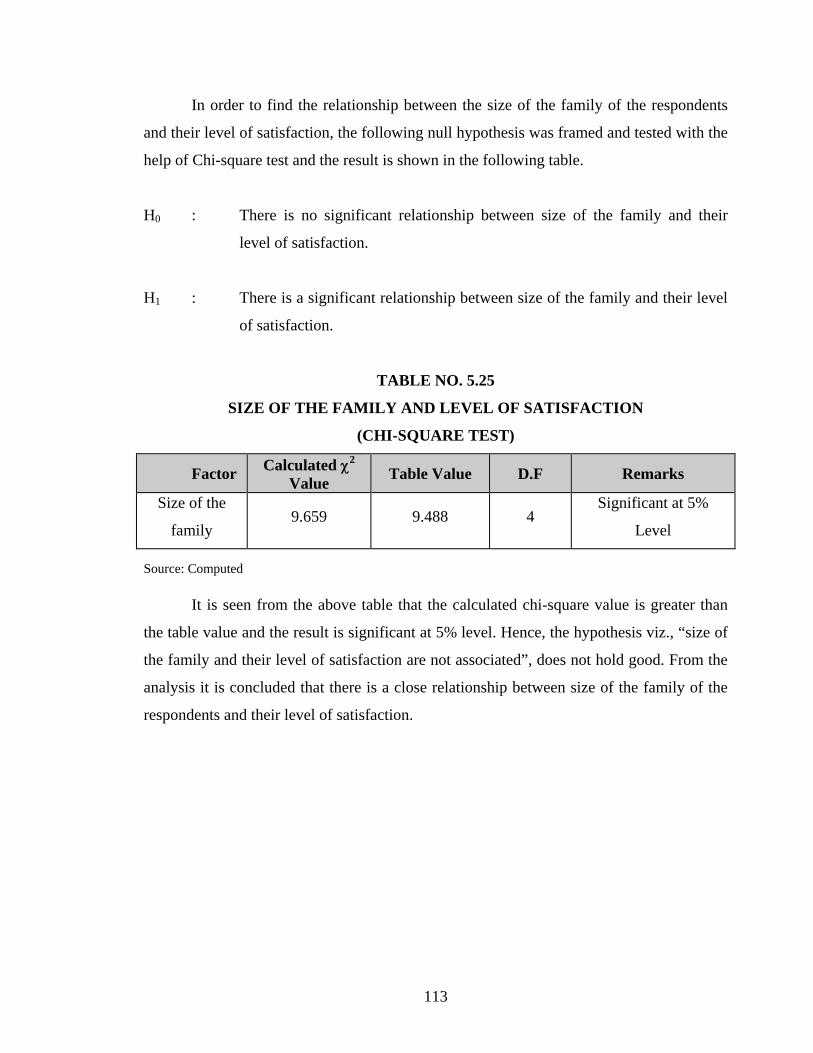

In order to find the relationship between the size of the family of the respondents

and their level of satisfaction, the following null hypothesis was framed and tested with the

help of Chi-square test and the result is shown in the following table.

H0 : There is no significant relationship between size of the family and their

level of satisfaction.

H1 : There is a significant relationship between size of the family and their level

of satisfaction.

TABLE NO. 5.25

SIZE OF THE FAMILY AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Size of the

family 9.659 9.488 4

Significant at 5%

Level

Source: Computed

It is seen from the above table that the calculated chi-square value is greater than

the table value and the result is significant at 5% level. Hence, the hypothesis viz., “size of

the family and their level of satisfaction are not associated”, does not hold good. From the

analysis it is concluded that there is a close relationship between size of the family of the

respondents and their level of satisfaction.

114

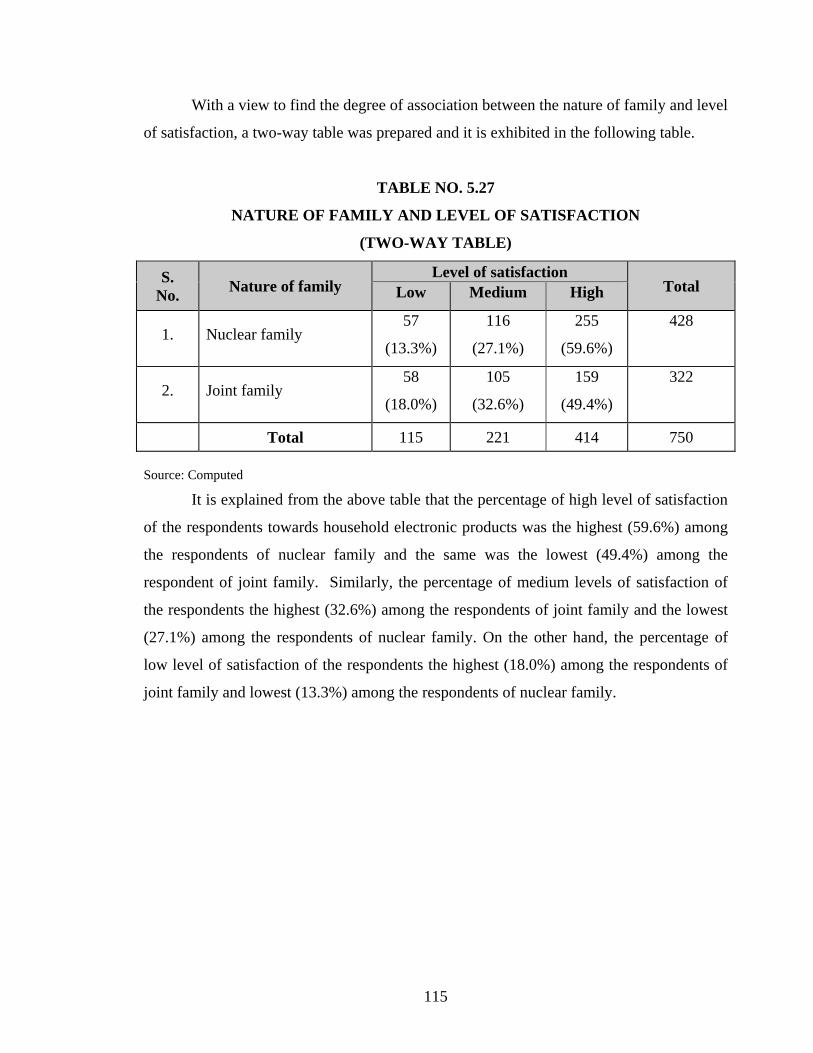

NATURE OF FAMILY AND LEVEL OF SATISFACTION

Household electronic products have become necessary for every family in the

present day lifestyle. The level of perception regarding level of satisfaction is greatly

influenced by the nature of family adopted. The present study is considering the two types

family like nuclear family and joint family. The sample consists of 428 (57.1%)

respondents belonging to nuclear family and 322 (42.9%) joint family.

The distribution of sample respondents in respect to the level of satisfaction is

shown in the table below.

TABLE NO. 5.26

NATURE OF FAMILY AND LEVEL OF SATISFACTION

S. No. Nature of family No. of

Respondents % Ave rage

Range S.D Min Max

1. Nuclear family 428 57.1 89.9 58 105 7.5 2. Joint family 322 42.9 88.6 65 103 7.4 Total 750 100.0

Source: Computed from Primary Data

It could be explained from the above table that the level of satisfaction of the

respondents towards household electronic products of nuclear family ranged between 58

and 105 with an average of 89.9. And the level of satisfaction of the respondents in joint

families ranged between 65 and 103 with an average of 88.6. It was concluded from the

analysis that maximum level of satisfaction is attained by the nuclear family respondents.

115

With a view to find the degree of association between the nature of family and level

of satisfaction, a two-way table was prepared and it is exhibited in the following table.

TABLE NO. 5.27

NATURE OF FAMILY AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No. Nature of family

Level of satisfaction Total Low Medium High

1. Nuclear family 57

(13.3%)

116

(27.1%)

255

(59.6%)

428

2. Joint family 58

(18.0%)

105

(32.6%)

159

(49.4%)

322

Total 115 221 414 750 Source: Computed

It is explained from the above table that the percentage of high level of satisfaction

of the respondents towards household electronic products was the highest (59.6%) among

the respondents of nuclear family and the same was the lowest (49.4%) among the

respondent of joint family. Similarly, the percentage of medium levels of satisfaction of

the respondents the highest (32.6%) among the respondents of joint family and the lowest

(27.1%) among the respondents of nuclear family. On the other hand, the percentage of

low level of satisfaction of the respondents the highest (18.0%) among the respondents of

joint family and lowest (13.3%) among the respondents of nuclear family.

116

In order to find the relationship between the nature of family and their level of

satisfaction, the following null hypothesis was framed and tested with the help of Chi-

square test and the result is shown in the following table.

H0 : There is no significant relationship between nature of family and their level

of satisfaction.

H1 : There is a significant relationship between nature of family and their level

of satisfaction.

TABLE NO. 5.28

NATURE OF FAMILY AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Nature of

family 7.995 5.991 2

Significant at 5%

Level

Source: Computed It is evident from the table that the calculated chi-square value is greater than the

table value and the result is significant at 5% level. Hence, the hypothesis viz., “nature of

family and their level of satisfaction are not associated”, does not hold good. From the

analysis it is concluded that there is a close relationship between nature of family and their

level of satisfaction.

117

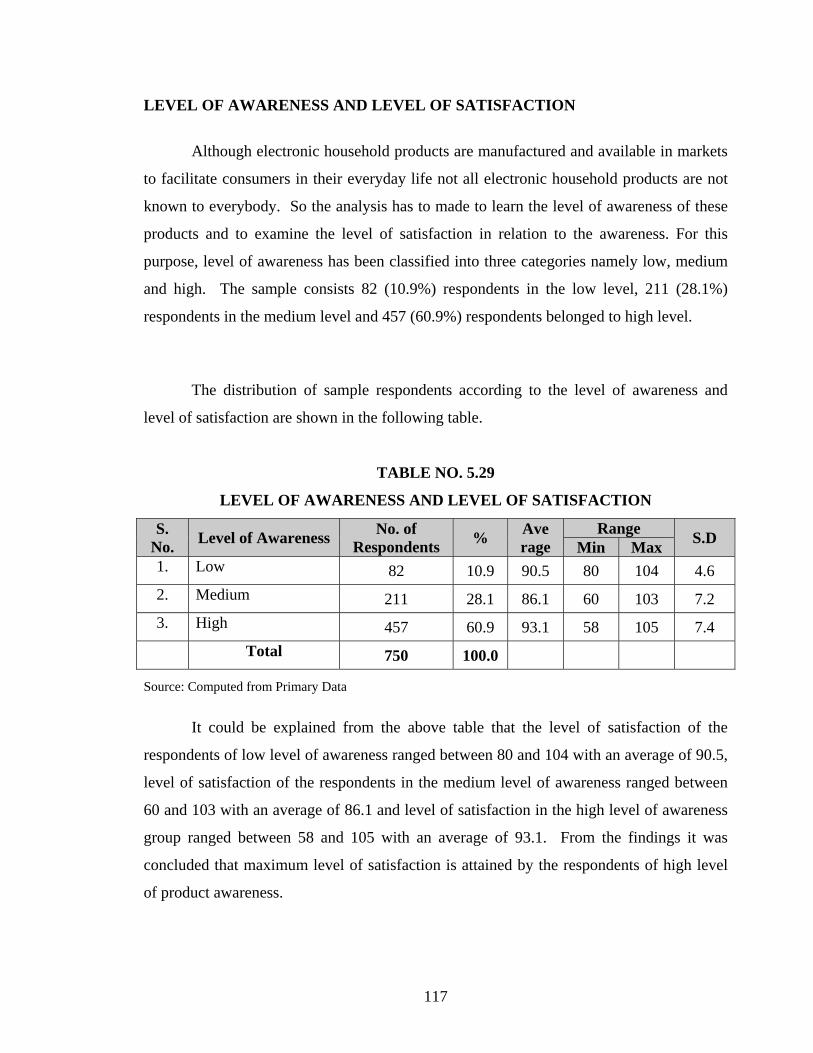

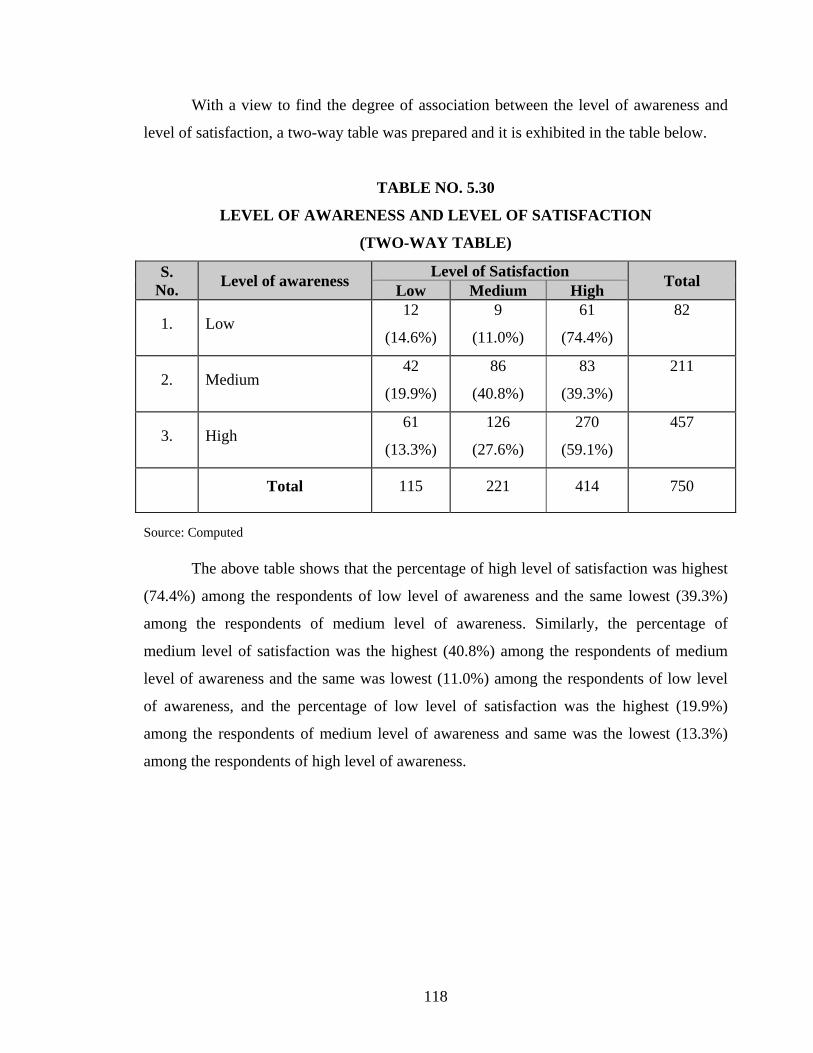

LEVEL OF AWARENESS AND LEVEL OF SATISFACTION

Although electronic household products are manufactured and available in markets

to facilitate consumers in their everyday life not all electronic household products are not

known to everybody. So the analysis has to made to learn the level of awareness of these

products and to examine the level of satisfaction in relation to the awareness. For this

purpose, level of awareness has been classified into three categories namely low, medium

and high. The sample consists 82 (10.9%) respondents in the low level, 211 (28.1%)

respondents in the medium level and 457 (60.9%) respondents belonged to high level.

The distribution of sample respondents according to the level of awareness and

level of satisfaction are shown in the following table.

TABLE NO. 5.29

LEVEL OF AWARENESS AND LEVEL OF SATISFACTION

S. No. Level of Awareness No. of

Respondents % Ave rage

Range S.D Min Max 1. Low 82 10.9 90.5 80 104 4.6 2. Medium 211 28.1 86.1 60 103 7.2 3. High 457 60.9 93.1 58 105 7.4 Total 750 100.0

Source: Computed from Primary Data

It could be explained from the above table that the level of satisfaction of the

respondents of low level of awareness ranged between 80 and 104 with an average of 90.5,

level of satisfaction of the respondents in the medium level of awareness ranged between

60 and 103 with an average of 86.1 and level of satisfaction in the high level of awareness

group ranged between 58 and 105 with an average of 93.1. From the findings it was

concluded that maximum level of satisfaction is attained by the respondents of high level

of product awareness.

118

With a view to find the degree of association between the level of awareness and

level of satisfaction, a two-way table was prepared and it is exhibited in the table below.

TABLE NO. 5.30

LEVEL OF AWARENESS AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No. Level of awareness Level of Satisfaction Total Low Medium High

1. Low 12

(14.6%)

9

(11.0%)

61

(74.4%)

82

2. Medium 42

(19.9%)

86

(40.8%)

83

(39.3%)

211

3. High 61

(13.3%)

126

(27.6%)

270

(59.1%)

457

Total 115 221 414 750

Source: Computed

The above table shows that the percentage of high level of satisfaction was highest

(74.4%) among the respondents of low level of awareness and the same lowest (39.3%)

among the respondents of medium level of awareness. Similarly, the percentage of

medium level of satisfaction was the highest (40.8%) among the respondents of medium

level of awareness and the same was lowest (11.0%) among the respondents of low level

of awareness, and the percentage of low level of satisfaction was the highest (19.9%)

among the respondents of medium level of awareness and same was the lowest (13.3%)

among the respondents of high level of awareness.

119

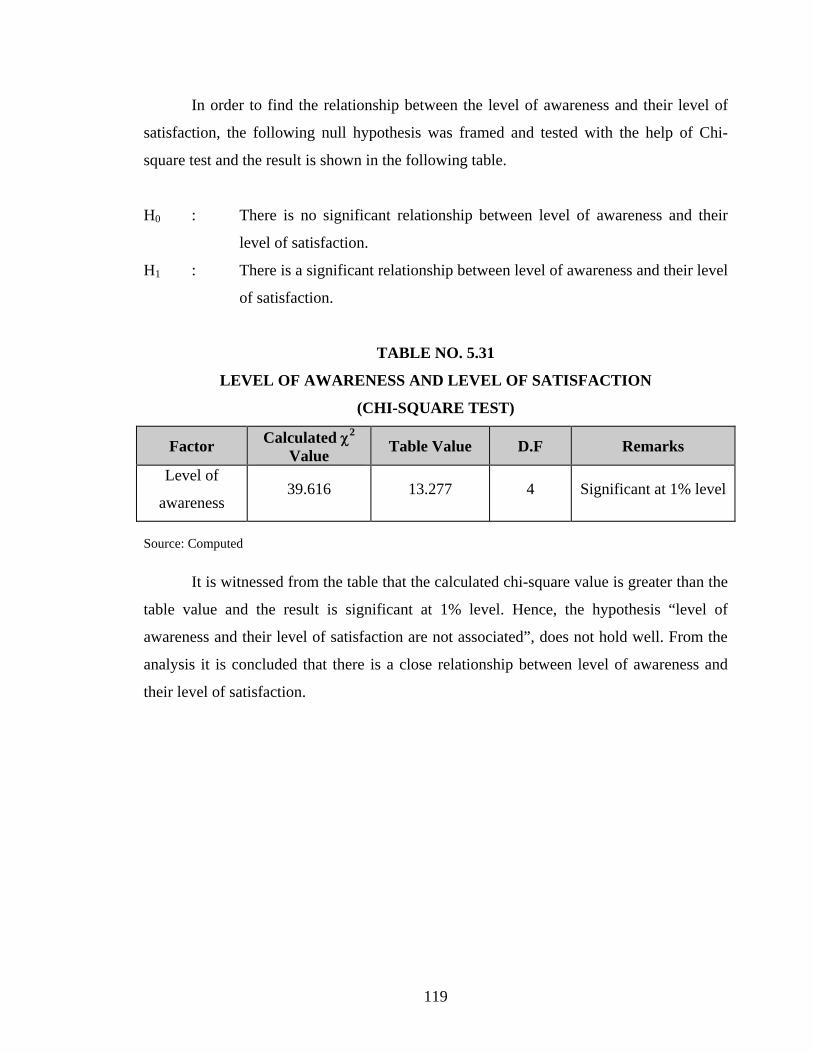

In order to find the relationship between the level of awareness and their level of

satisfaction, the following null hypothesis was framed and tested with the help of Chi-

square test and the result is shown in the following table.

H0 : There is no significant relationship between level of awareness and their

level of satisfaction.

H1 : There is a significant relationship between level of awareness and their level

of satisfaction.

TABLE NO. 5.31

LEVEL OF AWARENESS AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Level of

awareness 39.616 13.277 4 Significant at 1% level

Source: Computed

It is witnessed from the table that the calculated chi-square value is greater than the

table value and the result is significant at 1% level. Hence, the hypothesis “level of

awareness and their level of satisfaction are not associated”, does not hold well. From the

analysis it is concluded that there is a close relationship between level of awareness and

their level of satisfaction.

120

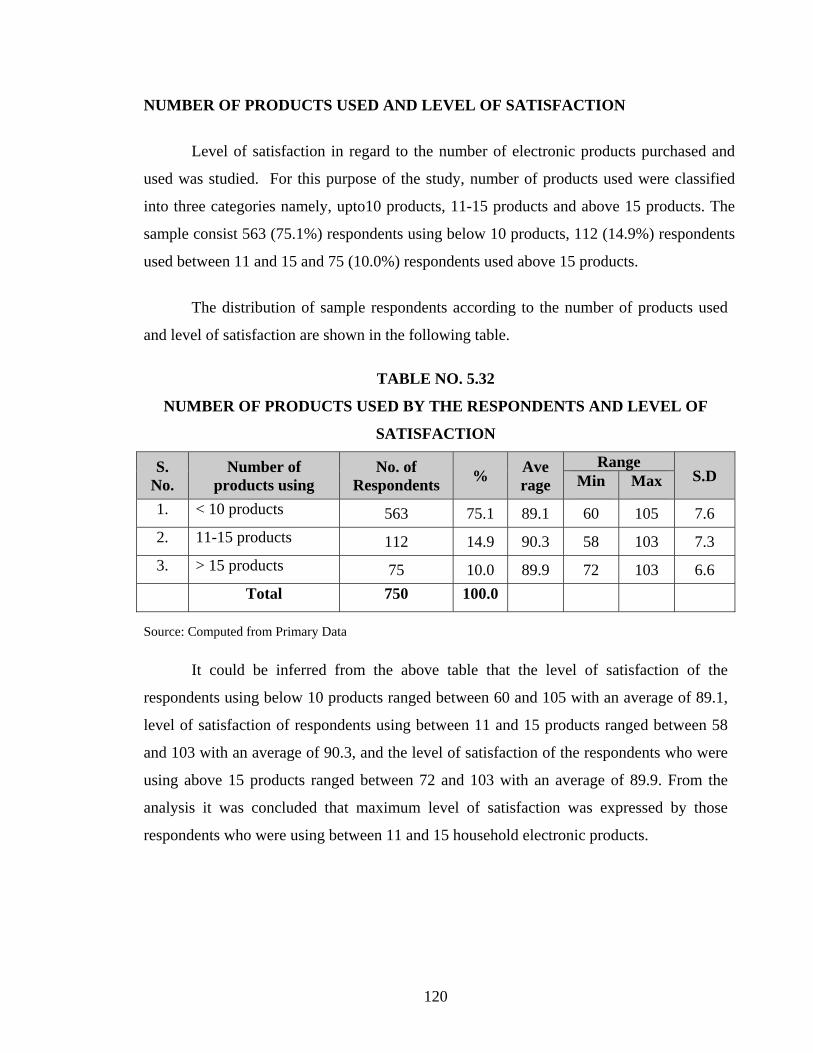

NUMBER OF PRODUCTS USED AND LEVEL OF SATISFACTION

Level of satisfaction in regard to the number of electronic products purchased and

used was studied. For this purpose of the study, number of products used were classified

into three categories namely, upto10 products, 11-15 products and above 15 products. The

sample consist 563 (75.1%) respondents using below 10 products, 112 (14.9%) respondents

used between 11 and 15 and 75 (10.0%) respondents used above 15 products.

The distribution of sample respondents according to the number of products used

and level of satisfaction are shown in the following table.

TABLE NO. 5.32

NUMBER OF PRODUCTS USED BY THE RESPONDENTS AND LEVEL OF

SATISFACTION

S. No.

Number of products using

No. of Respondents % Ave

rage Range

S.D Min Max

1. < 10 products 563 75.1 89.1 60 105 7.6 2. 11-15 products 112 14.9 90.3 58 103 7.3 3. > 15 products 75 10.0 89.9 72 103 6.6 Total 750 100.0

Source: Computed from Primary Data

It could be inferred from the above table that the level of satisfaction of the

respondents using below 10 products ranged between 60 and 105 with an average of 89.1,

level of satisfaction of respondents using between 11 and 15 products ranged between 58

and 103 with an average of 90.3, and the level of satisfaction of the respondents who were

using above 15 products ranged between 72 and 103 with an average of 89.9. From the

analysis it was concluded that maximum level of satisfaction was expressed by those

respondents who were using between 11 and 15 household electronic products.

121

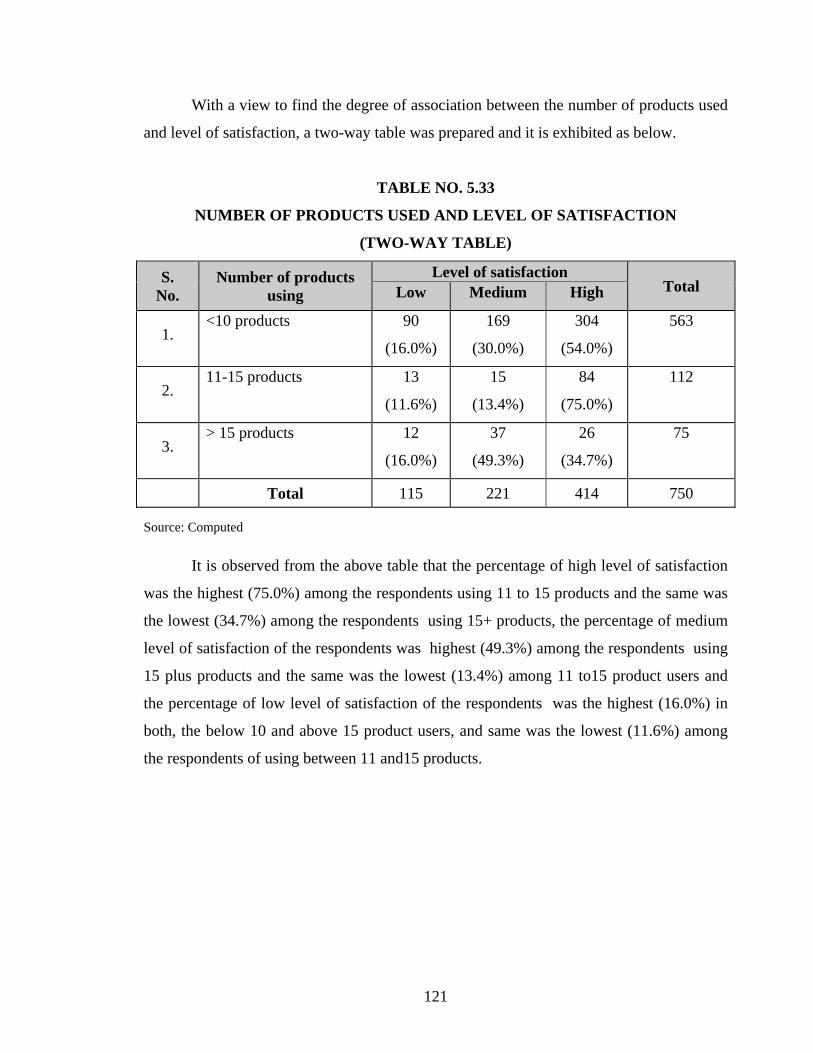

With a view to find the degree of association between the number of products used

and level of satisfaction, a two-way table was prepared and it is exhibited as below.

TABLE NO. 5.33

NUMBER OF PRODUCTS USED AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No.

Number of products using

Level of satisfaction Total Low Medium High

1. <10 products 90

(16.0%)

169

(30.0%)

304

(54.0%)

563

2. 11-15 products 13

(11.6%)

15

(13.4%)

84

(75.0%)

112

3. > 15 products 12

(16.0%)

37

(49.3%)

26

(34.7%)

75

Total 115 221 414 750

Source: Computed

It is observed from the above table that the percentage of high level of satisfaction

was the highest (75.0%) among the respondents using 11 to 15 products and the same was

the lowest (34.7%) among the respondents using 15+ products, the percentage of medium

level of satisfaction of the respondents was highest (49.3%) among the respondents using

15 plus products and the same was the lowest (13.4%) among 11 to15 product users and

the percentage of low level of satisfaction of the respondents was the highest (16.0%) in

both, the below 10 and above 15 product users, and same was the lowest (11.6%) among

the respondents of using between 11 and15 products.

122

In order to find the relationship between the number of products used and their

level of satisfaction, the following null hypothesis was framed and tested with the help of

Chi-square test and the result is shown in the following table.

H0 : There is no significant relationship between number of products used and

their level of satisfaction.

H1 : There is a significant relationship between number of products used and

their level of satisfaction.

TABLE NO. 5.34

NUMBER OF PRODUCTS AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Number of

products used 34.947 13.277 4

Significant at 1%

Level

Source: Computed

It is evident from the table that the calculated chi-square value is greater than the

table value and the result is significant at 1% level. Hence, the hypothesis viz., “number of

products used and their level of satisfaction are not associated”, does not hold good. From

the analysis it is concluded that there is a close relationship between number of products

used and their level of satisfaction.

123

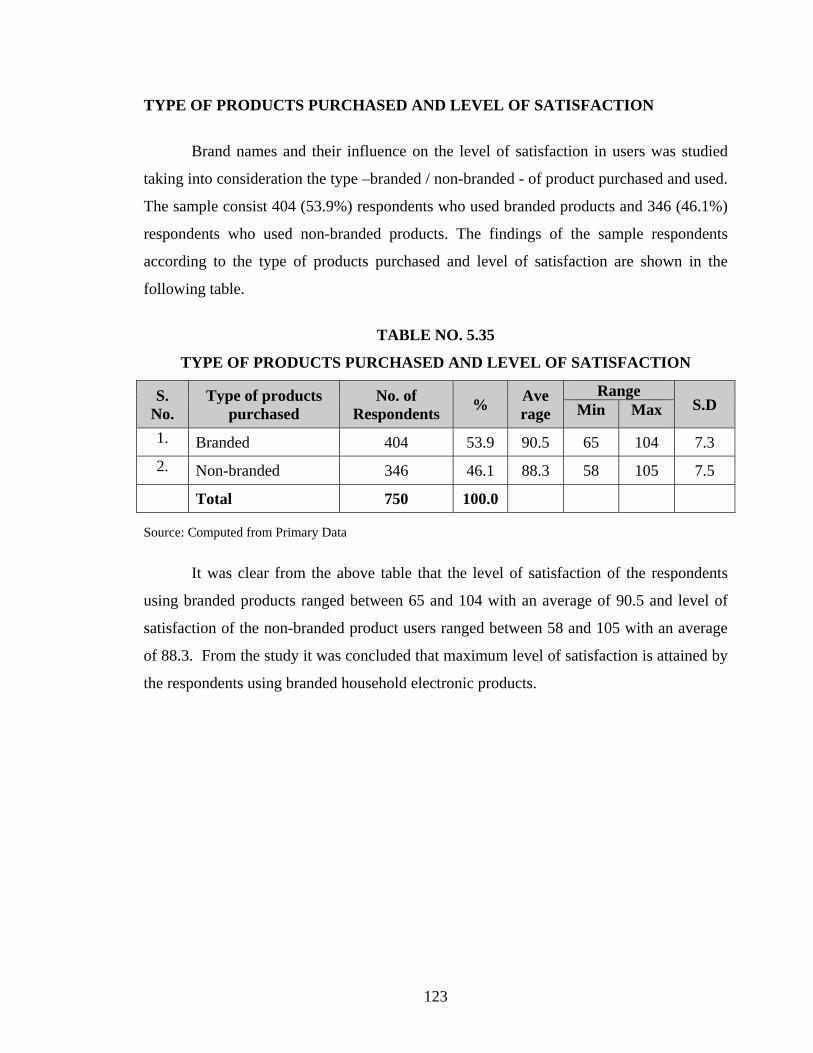

TYPE OF PRODUCTS PURCHASED AND LEVEL OF SATISFACTION

Brand names and their influence on the level of satisfaction in users was studied

taking into consideration the type –branded / non-branded - of product purchased and used.

The sample consist 404 (53.9%) respondents who used branded products and 346 (46.1%)

respondents who used non-branded products. The findings of the sample respondents

according to the type of products purchased and level of satisfaction are shown in the

following table.

TABLE NO. 5.35

TYPE OF PRODUCTS PURCHASED AND LEVEL OF SATISFACTION

S. No.

Type of products purchased

No. of Respondents % Ave

rage Range

S.D Min Max

1. Branded 404 53.9 90.5 65 104 7.3 2. Non-branded 346 46.1 88.3 58 105 7.5 Total 750 100.0

Source: Computed from Primary Data

It was clear from the above table that the level of satisfaction of the respondents

using branded products ranged between 65 and 104 with an average of 90.5 and level of

satisfaction of the non-branded product users ranged between 58 and 105 with an average

of 88.3. From the study it was concluded that maximum level of satisfaction is attained by

the respondents using branded household electronic products.

124

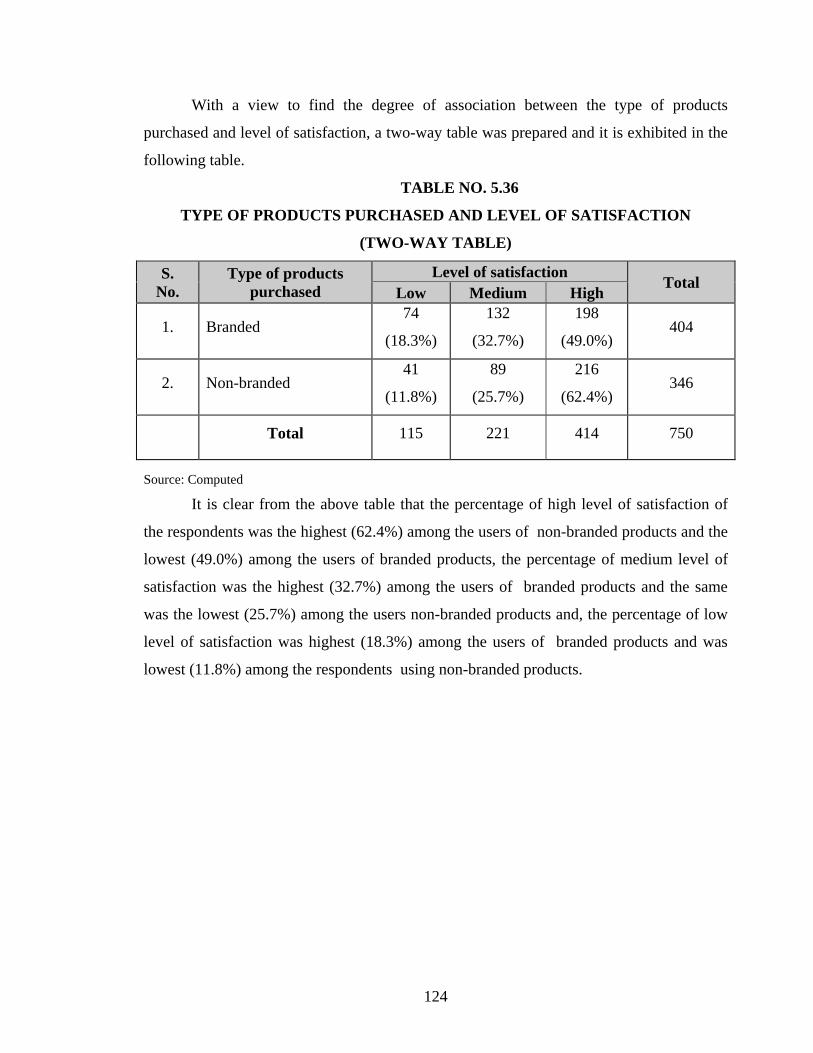

With a view to find the degree of association between the type of products

purchased and level of satisfaction, a two-way table was prepared and it is exhibited in the

following table.

TABLE NO. 5.36

TYPE OF PRODUCTS PURCHASED AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S. No.

Type of products purchased

Level of satisfaction Total Low Medium High

1. Branded 74

(18.3%)

132

(32.7%)

198

(49.0%) 404

2. Non-branded 41

(11.8%)

89

(25.7%)

216

(62.4%) 346

Total 115 221 414 750

Source: Computed It is clear from the above table that the percentage of high level of satisfaction of

the respondents was the highest (62.4%) among the users of non-branded products and the

lowest (49.0%) among the users of branded products, the percentage of medium level of

satisfaction was the highest (32.7%) among the users of branded products and the same

was the lowest (25.7%) among the users non-branded products and, the percentage of low

level of satisfaction was highest (18.3%) among the users of branded products and was

lowest (11.8%) among the respondents using non-branded products.

125

In order to find the relationship between the type of products purchased and their

level of satisfaction, the following null hypothesis was framed and tested with the help of

Chi-square test and the result is shown in the following table.

H0 : There is no significant relationship between type of products purchased and

their level of satisfaction.

H1 : There is a significant relationship between type of products purchased and

their level of satisfaction.

TABLE NO. 5.37

TYPE OF PRODUCTS PURCHASED AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value

Table Value D.F Remarks

Type of products

purchased 14.218 9.210 2

Significant at 1%

Level

Source: Computed

It is exhibited from the table that the calculated chi-square value is greater than the

table value and the result is significant at 1% level. Hence, the hypothesis viz., “type of

products purchased and their level of satisfaction are not associated”, does not hold good.

From the analysis it is concluded that there is a close relationship between type of products

purchased and their level of satisfaction.

126

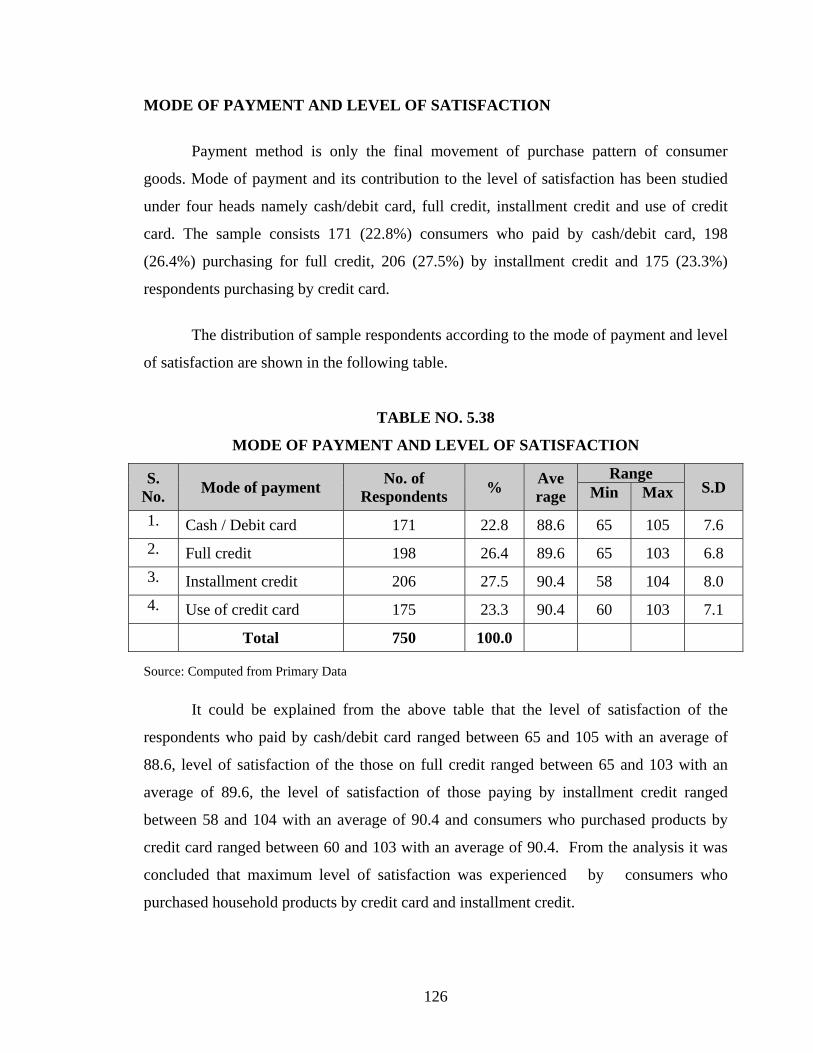

MODE OF PAYMENT AND LEVEL OF SATISFACTION

Payment method is only the final movement of purchase pattern of consumer

goods. Mode of payment and its contribution to the level of satisfaction has been studied

under four heads namely cash/debit card, full credit, installment credit and use of credit

card. The sample consists 171 (22.8%) consumers who paid by cash/debit card, 198

(26.4%) purchasing for full credit, 206 (27.5%) by installment credit and 175 (23.3%)

respondents purchasing by credit card.

The distribution of sample respondents according to the mode of payment and level

of satisfaction are shown in the following table.

TABLE NO. 5.38

MODE OF PAYMENT AND LEVEL OF SATISFACTION

S. No. Mode of payment No. of

Respondents % Ave rage

Range S.D Min Max

1. Cash / Debit card 171 22.8 88.6 65 105 7.6 2. Full credit 198 26.4 89.6 65 103 6.8 3. Installment credit 206 27.5 90.4 58 104 8.0 4. Use of credit card 175 23.3 90.4 60 103 7.1 Total 750 100.0

Source: Computed from Primary Data

It could be explained from the above table that the level of satisfaction of the

respondents who paid by cash/debit card ranged between 65 and 105 with an average of

88.6, level of satisfaction of the those on full credit ranged between 65 and 103 with an

average of 89.6, the level of satisfaction of those paying by installment credit ranged

between 58 and 104 with an average of 90.4 and consumers who purchased products by

credit card ranged between 60 and 103 with an average of 90.4. From the analysis it was

concluded that maximum level of satisfaction was experienced by consumers who

purchased household products by credit card and installment credit.

127

With a view to find the degree of association between mode of payment and level

of satisfaction, a two-way table was prepared and it is exhibited in the following table.

TABLE NO. 5.39

MODE OF PAYMENT AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S.

No. Mode of payment

Level of satisfaction Total

Low Medium High

1. Cash / Debit card 35

(20.5%)

56

(32.7%)

80

(46.8%) 171

2. Full credit 24

(12.1%)

63

(31.8%)

111

(56.1%) 198

3. Installment credit 38

(18.4%)

54

(26.2%)

114

(55.3%) 206

4. Use of credit card 18

(10.3%)

48

(27.4%)

109

(62.3%) 175

Total 115 221 414 750

Source: Computed

It is noted from the above table the percentage of level of satisfaction of the

consumers is the highest (62.3%) among the people using credit card payment and the

same was the lowest (46.8%) among the consumers paying by cash/debit card. Similarly,

the percentage of medium level of satisfaction was the highest (32.7%) among those

paying by cash/debit card and lowest (26.2%) among the consumers availing installment

credit, percentage of low level of satisfaction of consumers was the highest (20.5%) among

those paying by cash/debit card and same was the lowest (10.3%) among the consumers

using credit cards.

128

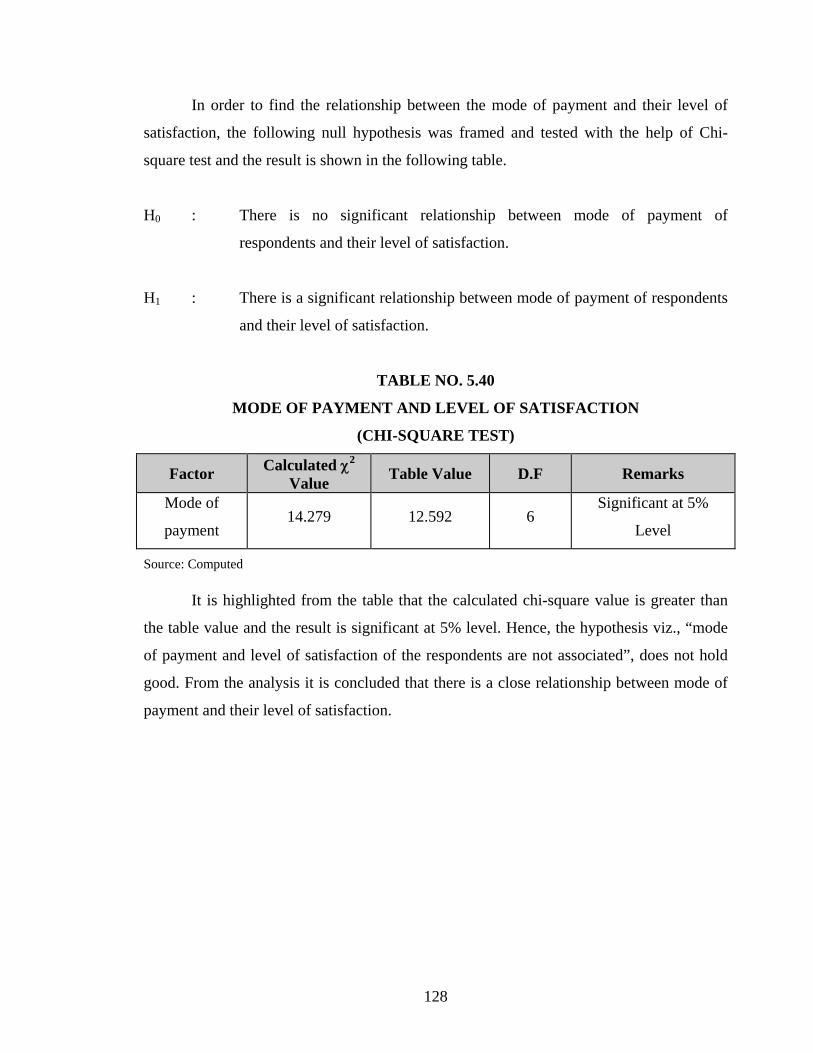

In order to find the relationship between the mode of payment and their level of

satisfaction, the following null hypothesis was framed and tested with the help of Chi-

square test and the result is shown in the following table.

H0 : There is no significant relationship between mode of payment of

respondents and their level of satisfaction.

H1 : There is a significant relationship between mode of payment of respondents

and their level of satisfaction.

TABLE NO. 5.40

MODE OF PAYMENT AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value Table Value D.F Remarks

Mode of

payment 14.279 12.592 6

Significant at 5%

Level

Source: Computed

It is highlighted from the table that the calculated chi-square value is greater than

the table value and the result is significant at 5% level. Hence, the hypothesis viz., “mode

of payment and level of satisfaction of the respondents are not associated”, does not hold

good. From the analysis it is concluded that there is a close relationship between mode of

payment and their level of satisfaction.

129

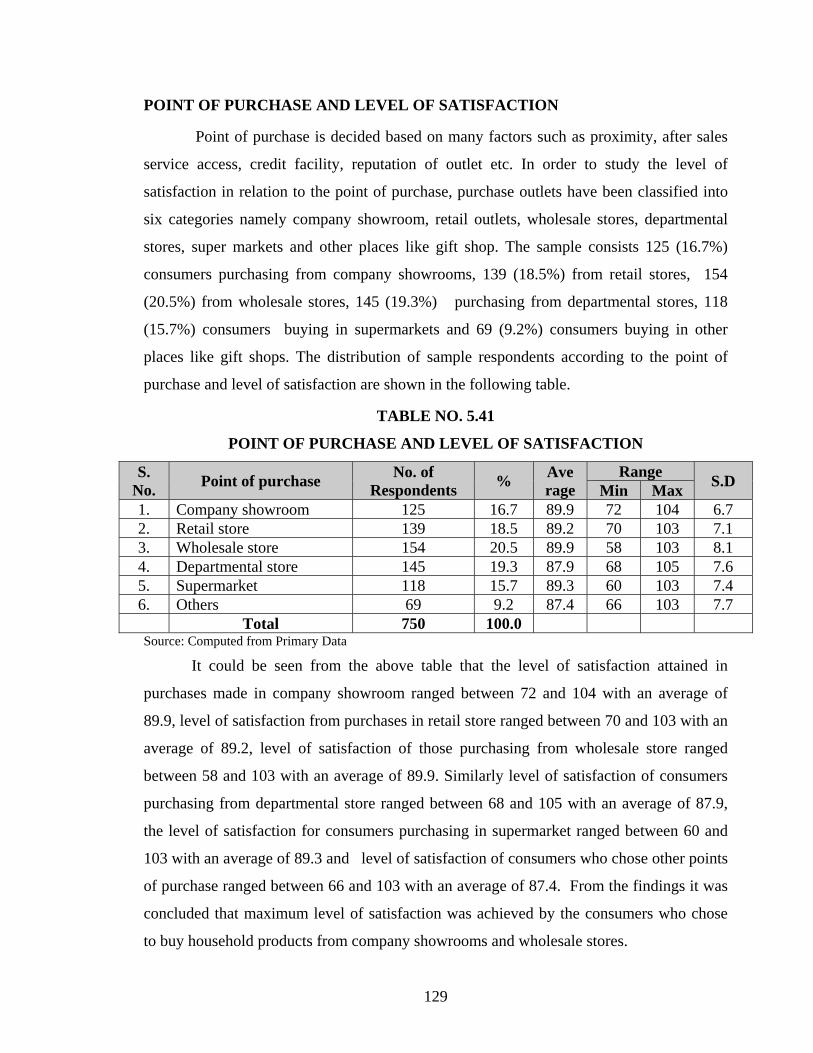

POINT OF PURCHASE AND LEVEL OF SATISFACTION

Point of purchase is decided based on many factors such as proximity, after sales

service access, credit facility, reputation of outlet etc. In order to study the level of

satisfaction in relation to the point of purchase, purchase outlets have been classified into

six categories namely company showroom, retail outlets, wholesale stores, departmental

stores, super markets and other places like gift shop. The sample consists 125 (16.7%)

consumers purchasing from company showrooms, 139 (18.5%) from retail stores, 154

(20.5%) from wholesale stores, 145 (19.3%) purchasing from departmental stores, 118

(15.7%) consumers buying in supermarkets and 69 (9.2%) consumers buying in other

places like gift shops. The distribution of sample respondents according to the point of

purchase and level of satisfaction are shown in the following table.

TABLE NO. 5.41

POINT OF PURCHASE AND LEVEL OF SATISFACTION

S. No. Point of purchase No. of

Respondents % Ave rage

Range S.D Min Max 1. Company showroom 125 16.7 89.9 72 104 6.7 2. Retail store 139 18.5 89.2 70 103 7.1 3. Wholesale store 154 20.5 89.9 58 103 8.1 4. Departmental store 145 19.3 87.9 68 105 7.6 5. Supermarket 118 15.7 89.3 60 103 7.4 6. Others 69 9.2 87.4 66 103 7.7 Total 750 100.0 Source: Computed from Primary Data

It could be seen from the above table that the level of satisfaction attained in

purchases made in company showroom ranged between 72 and 104 with an average of

89.9, level of satisfaction from purchases in retail store ranged between 70 and 103 with an

average of 89.2, level of satisfaction of those purchasing from wholesale store ranged

between 58 and 103 with an average of 89.9. Similarly level of satisfaction of consumers

purchasing from departmental store ranged between 68 and 105 with an average of 87.9,

the level of satisfaction for consumers purchasing in supermarket ranged between 60 and

103 with an average of 89.3 and level of satisfaction of consumers who chose other points

of purchase ranged between 66 and 103 with an average of 87.4. From the findings it was

concluded that maximum level of satisfaction was achieved by the consumers who chose

to buy household products from company showrooms and wholesale stores.

130

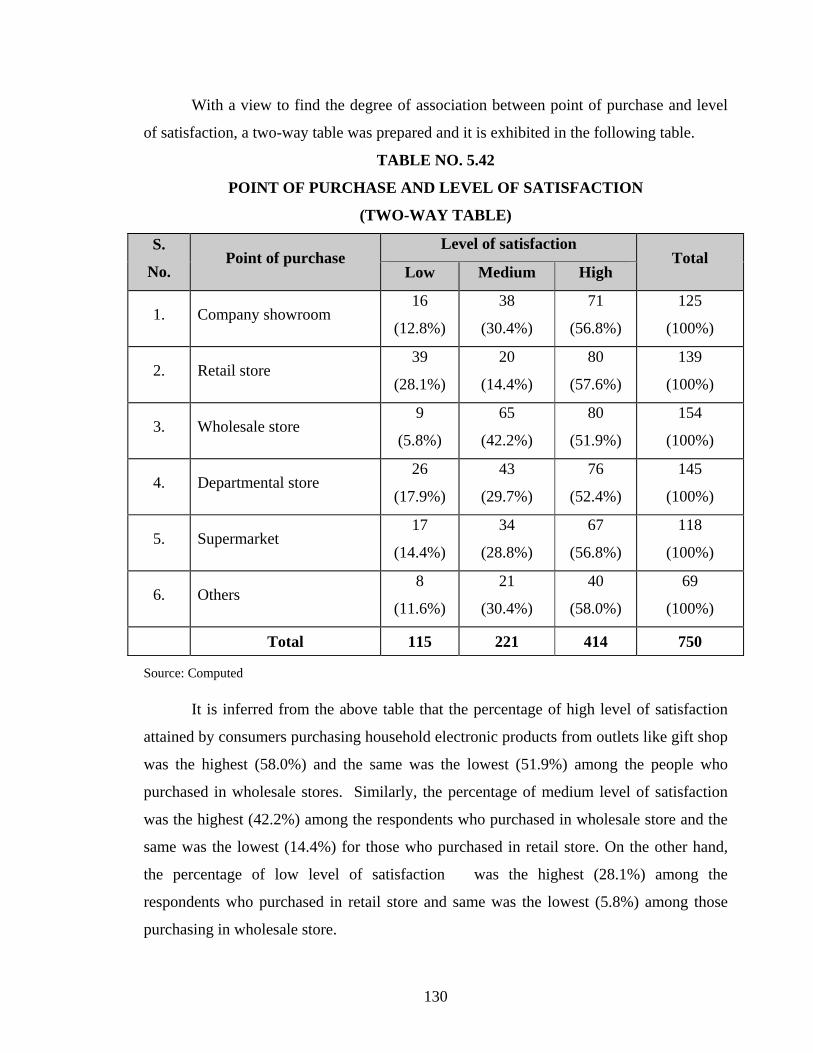

With a view to find the degree of association between point of purchase and level

of satisfaction, a two-way table was prepared and it is exhibited in the following table.

TABLE NO. 5.42

POINT OF PURCHASE AND LEVEL OF SATISFACTION

(TWO-WAY TABLE)

S.

No. Point of purchase

Level of satisfaction Total

Low Medium High

1. Company showroom 16

(12.8%)

38

(30.4%)

71

(56.8%)

125

(100%)

2. Retail store 39

(28.1%)

20

(14.4%)

80

(57.6%)

139

(100%)

3. Wholesale store 9

(5.8%)

65

(42.2%)

80

(51.9%)

154

(100%)

4. Departmental store 26

(17.9%)

43

(29.7%)

76

(52.4%)

145

(100%)

5. Supermarket 17

(14.4%)

34

(28.8%)

67

(56.8%)

118

(100%)

6. Others 8

(11.6%)

21

(30.4%)

40

(58.0%)

69

(100%)

Total 115 221 414 750

Source: Computed

It is inferred from the above table that the percentage of high level of satisfaction

attained by consumers purchasing household electronic products from outlets like gift shop

was the highest (58.0%) and the same was the lowest (51.9%) among the people who

purchased in wholesale stores. Similarly, the percentage of medium level of satisfaction

was the highest (42.2%) among the respondents who purchased in wholesale store and the

same was the lowest (14.4%) for those who purchased in retail store. On the other hand,

the percentage of low level of satisfaction was the highest (28.1%) among the

respondents who purchased in retail store and same was the lowest (5.8%) among those

purchasing in wholesale store.

131

In order to find the relationship between the point of purchase and their level of

satisfaction, the following null hypothesis was framed and tested with the help of Chi-

square test and the result is shown in the following table.

H0 : There is no significant relationship between point of purchase and their

level of satisfaction.

H1 : There is a significant relationship between point of purchase and their level

of satisfaction.

TABLE NO. 5.43

POINT OF PURCHASE AND LEVEL OF SATISFACTION

(CHI-SQUARE TEST)

Factor Calculated χ2 Value

Table Value D.F Remarks

Point of

purchase 45.709 23.209 10

Significant at 1%

Level

Source: Computed

It is observed from the table that the calculated chi-square value is greater than the

table value and the result is significant at 1% level. Hence, the hypothesis viz., “point of

purchase and their level of satisfaction are not associated”, does not hold good. From the

analysis it is concluded that there is a close relationship between point of purchase and

level of satisfaction.

132

II. PERCENTAGE ANALYSIS

AWARENESS ABOUT THE PRODUCTS

Period of awareness by the consumers about products was studied taking twenty-

five items into consideration and findings shown in table below.

TABLE NO.5.44

PERIOD OF AWARENESS ABOUT THE PRODUCTS

No. Products

≤ 5

Years

6-10

Years

> 10

Years Total

1 Radio 25

(3.3%)

346

(46.1%)

379

(50.5%)

750

(100%)

2 TV 175

(23.3%)

230

(30.7%)

345

(46.0%)

750

(100%)

3 Fan 129

(18.6%)

225

(32.4%)

341

(49.1%)

695

(100%)

4 Iron Box 157

(21.7%)

319

(44.2%)

246

(34.1%)

722

(100%)

5 Washing Machine 173

(27.5%)

169

(26.9%)

287

(45.6%)

629

(100%)

6 Refrigerator 187

(28.1%)

286

(42.9%)

193

(29.0%)

666

(100%)

7 Induction Stove 324

(66.7%)

125

(25.7%)

37

(7.6%)

486

(100%)

8 Mixer 154

(25.7%)

249

(41.5%)

197

(32.8%)

600

(100%)

9 Computer 241

(57.9%)

127

(30.5%)

48

(11.5%)

416

(100%)

10 Water Heater 215

(47.9%)

167

(37.2%)

67

(14.9%)

449

(100%)

11 DVD Player 345

(51.2%)

287

(42.6%)

42

(6.2%)

674

(100%)

133

No. Products

≤ 5

Years

6-10

Years

> 10

Years Total

12 Microwave Oven 167

(64.0%)

79

(30.3%)

15

(5.7%)

261

(100%)

13 Air Conditioner 257

(46.8%)

168

(30.6%)

124

(22.6%)

549

(100%)

14 Stabilizer 328

(51.3%)

147

(23.0%)

165

(25.8%)

640

(100%)

15 Rice Cooker 249

(45.9%)

167

(30.8%)

127

(23.4%)

543

(100%)

16 Water Purifier 357

(70.6%)

124

(24.5%)

25

(4.9%)

506

(100%)

17 Electronic Power Controller79

(49.7%)

56

(35.2%)

24

(15.1%)

159

(100%)

18 Home theatre 235

(45.8%)

159

(31.0%)

119

(23.2%)

513

(100%)

19 Vacuum Cleaner 219

(57.2%)

105

(27.4%)

59

(15.4%)

383

(100%)

20 DTH 239

(52.3%)

154

(33.7%)

64

(14.0%)

457

(100%)

21 Digital Camera 138

(35.0%)

154

(39.1%)

102

(25.9%)

394

(100%)

22 Wall Clock 49

(6.5%)

308

(41.1%)

393

(52.4%)

750

(100%)

23 Sewing Machine 158

(34.0%)

168

(36.1%)

139

(29.9%)

465

(100%)

24 Toys 298

(42.1%)

302

(42.7%)

107

(15.1%)

707

(100%)

25 Others _______________ 419

(58.8%)

189

(26.5%)

105

(14.7%)

713

(100%)

Source: Computed from Primary Data

134

It is inferred from the above table that mostly all the respondents were aware about

all the products. Consumers were aware about products like radio, TV, fan, washing

machine and wall clock for more than 10 years with percentage being50.5, 46.0, 49.1, 45.6

and 52.4 percent respectively. The consumers were aware about the products like iron

box, refrigerator, mixer, digital camera, sewing machine and toys for 6-10 years as 44.2,

42.9, 41.5, 39.1, 36.1 and 42.7 percent respectively. The awareness in regard to products

like induction stove, computer, water heater, DVD player, microwave oven, air

conditioner, stabilizer, rice cooker, water purifier, electronic power controller, home

theatre, vacuum cleaner, DTH and other products was below 5 years as 66.7, 57.9, 47.9,

51.2, 64.0, 46.8, 51.3, 45.9, 70.6, 49.7, 45.8, 57.2, 52.3, and 58.8 percent respectively. It is

found from the analysis that majority (70.6%) of the consumers were aware about water

heater for less than 5 years.

135

SOURCE OF INFORMATION OF HOUSEHOLD ELECTRONIC PRODUCTS

In general, everyone in the society has come to know about the household

electronic products through some source or person. For the purpose of identifying source

from where the people got to know about household products, sources are classified into

nine categories viz., Radio, TV, Magazine, Newspapers, Posters and Hoarding, Dealers /

Retailers, Relatives/Family members, Window display and other sources. The details are

furnished in the following table.

TABLE NO.5.45

SOURCE OF INFORMATION OF HOUSEHOLD ELECTRONIC PRODUCTS

(Multiple choices)

Sl. No. Sources* No. of

ResponsesPercentage (Out of 750)

1 Radio 359 47.9

2 TV 658 87.7

3 Magazine 598 79.7

4 Newspapers 469 62.5

5 Posters and Hoarding 398 53.1

6 Dealer / Retailers 356 47.5

7 Relatives / Family members 514 68.5

8 Window display 249 33.2

9 Any other sources 341 45.5

Source: multiple responses were considered

It is surmised from the above table that 47.9 percent of the respondents were aware

about the product by listening to radio, 87.7 percent came to know about the product

through TV, 79.7 and 62.5 percent of the respondents knew about the product by reading

magazines and newspapers. 53.1 percent of the respondents through posters and hoardings,

and 47.5 percent of them came to know about the product through dealer/retailers,68.5

percent through relatives/family friends,33.2 percent by window displays and 45.5 percent

got to know of the products through other sources. It is noted from the analysis that

majority 87.7 percent were informed through the TV.

136

CHART NO.5.2

SOURCE OF INFORMATION OF THE HOUSEHOLD PRODUCTS

137

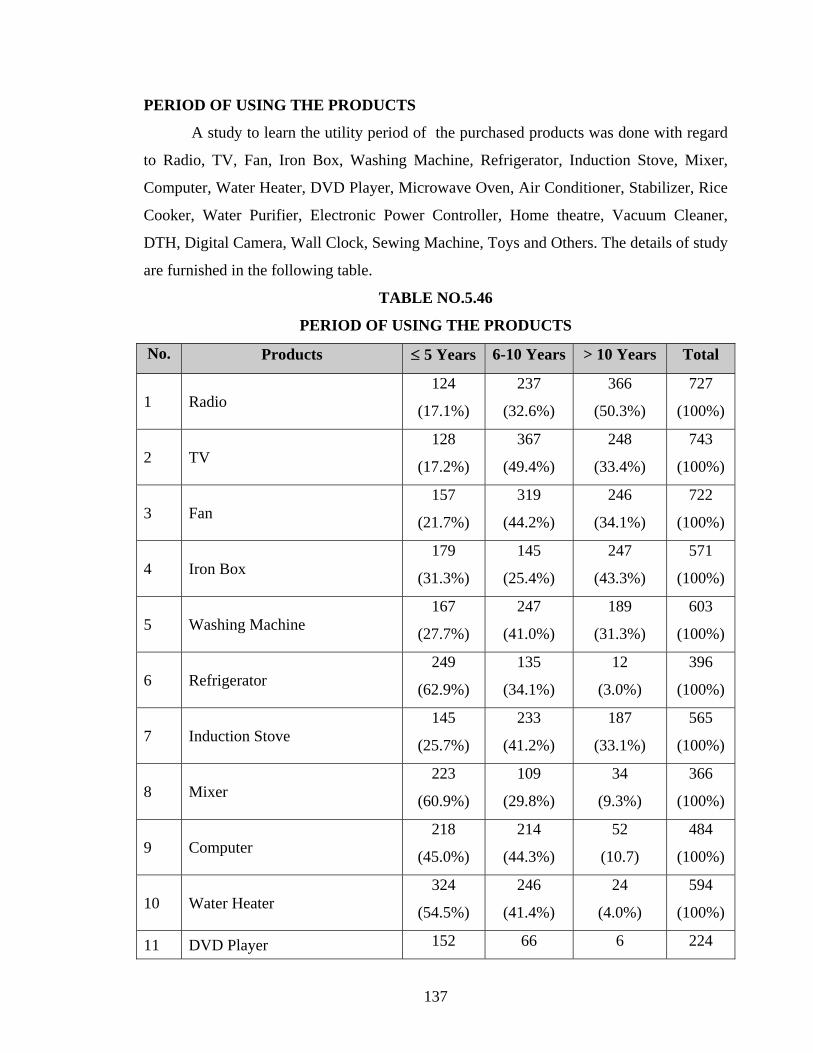

PERIOD OF USING THE PRODUCTS

A study to learn the utility period of the purchased products was done with regard

to Radio, TV, Fan, Iron Box, Washing Machine, Refrigerator, Induction Stove, Mixer,

Computer, Water Heater, DVD Player, Microwave Oven, Air Conditioner, Stabilizer, Rice

Cooker, Water Purifier, Electronic Power Controller, Home theatre, Vacuum Cleaner,

DTH, Digital Camera, Wall Clock, Sewing Machine, Toys and Others. The details of study

are furnished in the following table.

TABLE NO.5.46

PERIOD OF USING THE PRODUCTS

No. Products ≤ 5 Years 6-10 Years > 10 Years Total

1 Radio 124

(17.1%)

237

(32.6%)

366

(50.3%)

727

(100%)

2 TV 128

(17.2%)

367

(49.4%)

248

(33.4%)

743

(100%)

3 Fan 157

(21.7%)

319

(44.2%)

246

(34.1%)

722

(100%)

4 Iron Box 179

(31.3%)

145

(25.4%)

247

(43.3%)

571

(100%)

5 Washing Machine 167

(27.7%)

247

(41.0%)

189

(31.3%)

603

(100%)

6 Refrigerator 249

(62.9%)

135

(34.1%)

12

(3.0%)

396

(100%)

7 Induction Stove 145

(25.7%)

233

(41.2%)

187

(33.1%)

565

(100%)

8 Mixer 223

(60.9%)

109

(29.8%)

34

(9.3%)

366

(100%)

9 Computer 218

(45.0%)

214

(44.3%)

52

(10.7)

484

(100%)

10 Water Heater 324

(54.5%)

246

(41.4%)

24

(4.0%)

594

(100%)

11 DVD Player 152 66 6 224

138

No. Products ≤ 5 Years 6-10 Years > 10 Years Total

(67.9%) (29.5%) (2.7%) (100%)

12 Microwave Oven 245

(48.9%)

154

(30.6%)

105

(20.8%)

504

(100%)

13 Air Conditioner 297

(51.7%)

132

(23.0%)

145

(25.3%)

574

(100%)

14 Stabilizer 215

(44.4%)

154

(31.8%)

115

(23.8%)

484

(100%)

15 Rice Cooker 318

(72.4%)

105

(23.9%)

16

(3.6%)

439

(100%)

16 Water Purifier 57

(55.9%)

25

(24.5%)

20

(19.6%)

102

(100%)

17 Electronic Power Controller 219

(48.1%)

142

(31.2%)

94

(20.7%)

455

(100%)

18 Home theatre 192

(59.6%)

88

(27.3%)

42

(13.0%)

322

(100%)

19 Vacuum Cleaner 222

(55.2%)

142

(35.3%)

38

(9.5%)

402

(100%)

20 DTH 124

(37.8%)

122

(37.2%)

82

(25.0%)

328

(100%)

21 Digital Camera 34

(5.1%)

285

(42.9%)

345

(52.0%)

664

(100%)

22 Wall Clock 148

(37.2%)

142

(35.7%)

108

(27.1)

398

(100%)

23 Sewing Machine 257

(40.3%)

289

(45.3%)

92

(14.4%)

638

(100%)

24 Toys 348

(59.7%)

146

(25.0%)

89

(15.3%)

583

(100%)

25 Others 324

(72.3%)

109

(24.3%)

15

(3.3%)

448

(100%)

Source: Computed

139

It is observed from the above table, consumers using the products like radio, iron

box and digital camera for more than 10 years are 50.3, 43.3 and 52.0 percent respectively.

Percentage of people using TV, fan, washing machine, induction stove and sewing

machine for 6-10 years as 49.4, 44.2, 41.0, 41.2 and 45.3 respectively. Those using

refrigerator, mixer, computer, water heater, DVD player, microwave oven, air conditioner,

stabilizer, rice cooker, water purifier, electronic power controller, home theatre, vacuum

cleaner, DTH, wall clock, toys and other products for below 5 years as 62.9, 60.9, 45.0,

54.5, 67.9, 48.9, 51.7, 44.4, 72.4, 55.9, 48.1, 59.6, 55.2, 37.9, 37.2, 59.7 and 72.3 percent

respectively. It is found from the analysis that majority (72.4%) of the consumers were

using rice cooker for below 5 years.

140

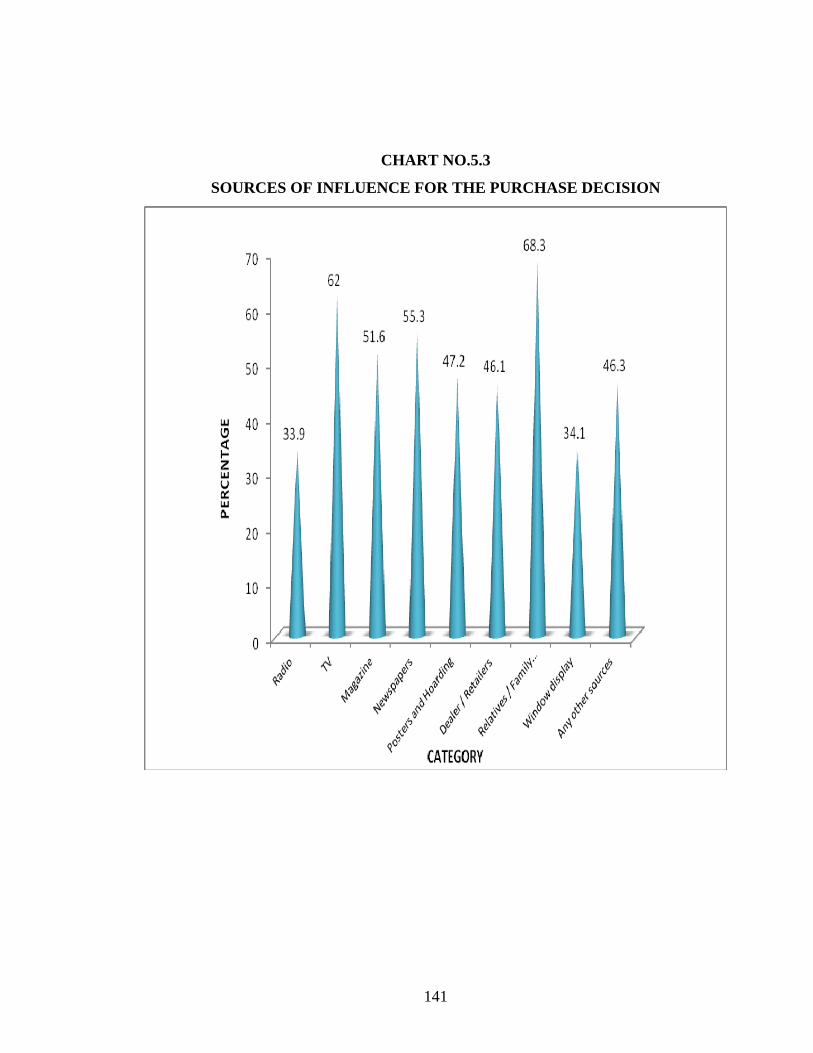

SOURCES OF INFLUENCE FOR THE PURCHASE DECISION

Analysis is made to know about the influencing sources to take purchase decision.

The radio, TV, magazine, newspapers, posters and hoarding, dealers / retailers,

relatives/family members, window display and other sources. The details are furnished in

the following table.

TABLE NO.5.47

SOURCES OF INFLUENCE FOR THE PURCHASE DECISION

Sl. No. Sources* No. of

ResponsesPercentage (Out of 750)

1 Radio 254 33.9 2 TV 465 62.0 3 Magazine 387 51.6 4 Newspapers 415 55.3 5 Posters and Hoarding 354 47.2 6 Dealer / Retailers 346 46.1 7 Relatives / Family members 512 68.3 8 Window display 256 34.1 9 Any other sources 347 46.3

* Multiple responses were considered Source: Computed from Primary Data

It is determined from the above table that the purchase decision was influenced by

Relatives/Family members showing highest percentage of 68.3, followed by TV 62

percent, Newspaper 55.3percent, Magazines 51.6percent, Posters and Hoarding 47.2

percent, other sources 46.3 percent closely followed by Dealers/Retailers 46.1percent,

Window displays 34.1percent and Radio 33.9 percent.

It is noted from the analysis that majority (68.3) of the respondents gained the

maximum impact on the purchase decision through relatives / family members.

141

CHART NO.5.3

SOURCES OF INFLUENCE FOR THE PURCHASE DECISION

142

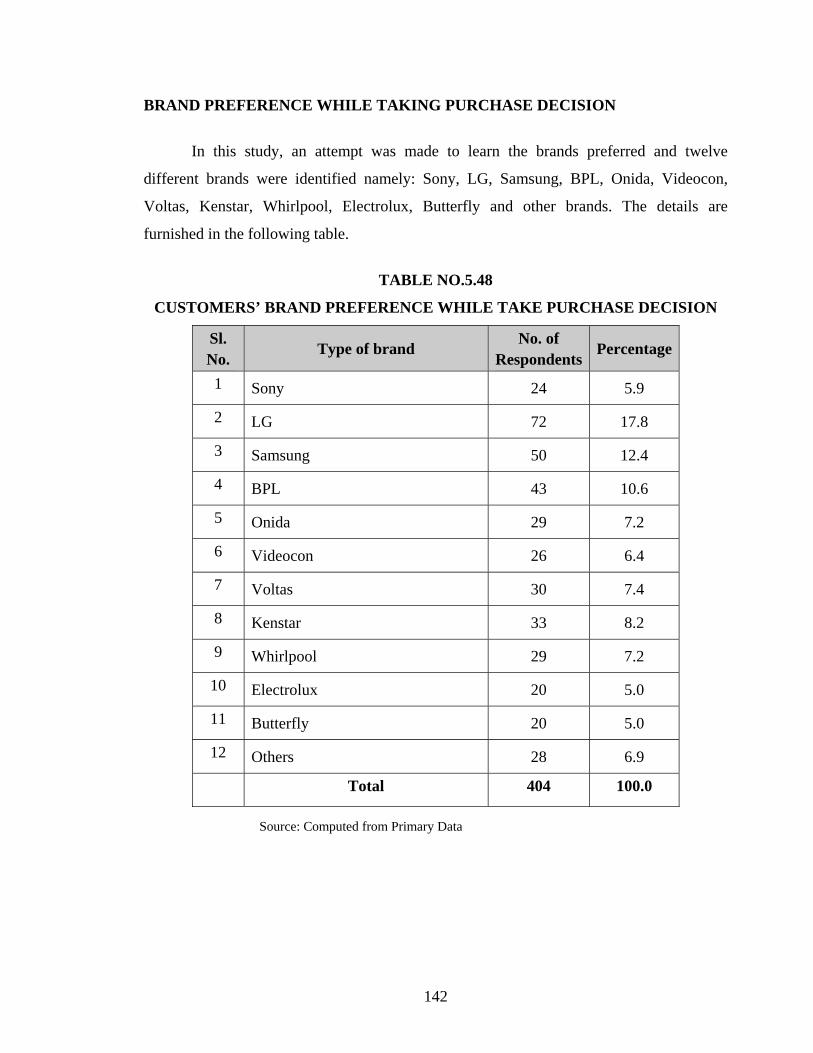

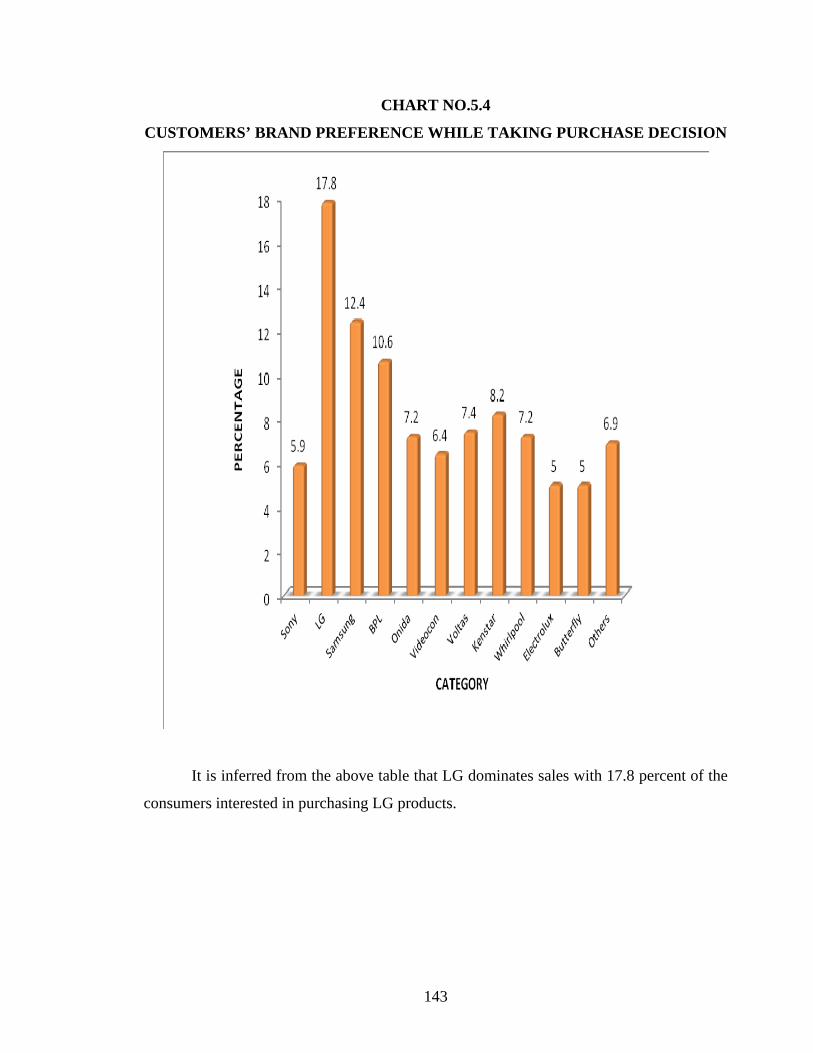

BRAND PREFERENCE WHILE TAKING PURCHASE DECISION

In this study, an attempt was made to learn the brands preferred and twelve

different brands were identified namely: Sony, LG, Samsung, BPL, Onida, Videocon,

Voltas, Kenstar, Whirlpool, Electrolux, Butterfly and other brands. The details are

furnished in the following table.

TABLE NO.5.48

CUSTOMERS’ BRAND PREFERENCE WHILE TAKE PURCHASE DECISION

Sl. No.

Type of brand No. of Respondents

Percentage

1 Sony 24 5.9

2 LG 72 17.8

3 Samsung 50 12.4

4 BPL 43 10.6

5 Onida 29 7.2

6 Videocon 26 6.4

7 Voltas 30 7.4

8 Kenstar 33 8.2

9 Whirlpool 29 7.2

10 Electrolux 20 5.0

11 Butterfly 20 5.0

12 Others 28 6.9

Total 404 100.0

Source: Computed from Primary Data

143

CHART NO.5.4

CUSTOMERS’ BRAND PREFERENCE WHILE TAKING PURCHASE DECISION

It is inferred from the above table that LG dominates sales with 17.8 percent of the

consumers interested in purchasing LG products.

144

SPECIFIC BRAND PREFERENCE OF CUSTOMERS AT EVERY PURCHASE

To identify whether consumers asked and insisted on specific brand at every

purchase, a survey was made and details are furnished in the following table.

TABLE NO.5.49

SPECIFIC BRAND PRERENCE AT EVERY PURCHASE

Sl. No. Opinion No. of Respondents Percentage

1 Yes 259 64.1

2 No 145 35.9

Total 404 100.0

Source: Computed from Primary Data

As shown 64.1 percent of the consumers insisted on specific brand every time they

bought products, whereas 35.9 percent were not so particular about the brand.

CHART NO.5.5

SPECIFIC BRAND PREFERENCE OF CUSTOMERS AT EVERY PURCHASE

145

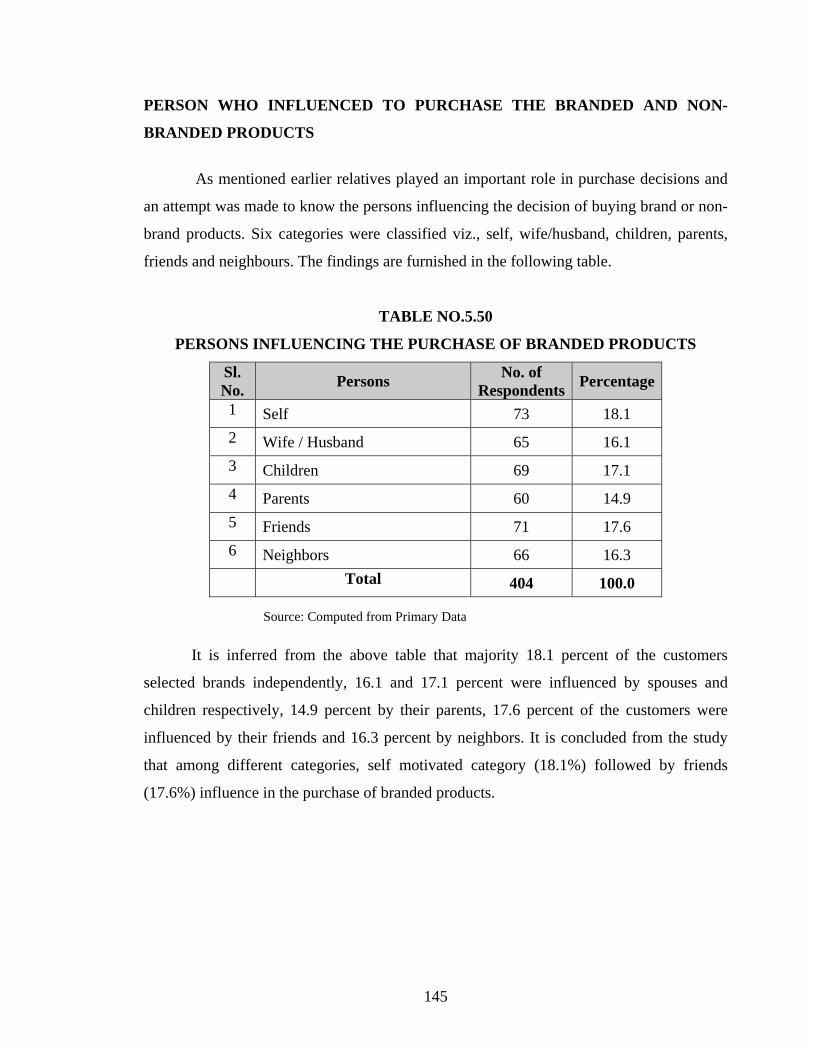

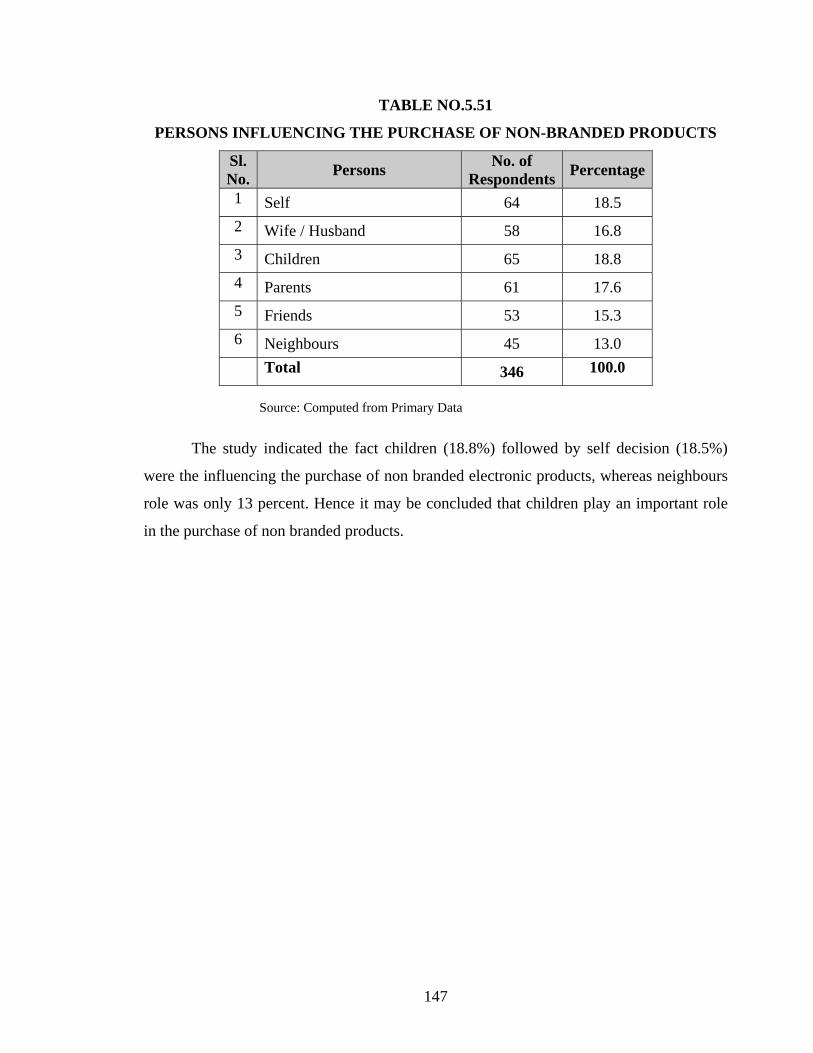

PERSON WHO INFLUENCED TO PURCHASE THE BRANDED AND NON-

BRANDED PRODUCTS

As mentioned earlier relatives played an important role in purchase decisions and

an attempt was made to know the persons influencing the decision of buying brand or non-

brand products. Six categories were classified viz., self, wife/husband, children, parents,

friends and neighbours. The findings are furnished in the following table.

TABLE NO.5.50

PERSONS INFLUENCING THE PURCHASE OF BRANDED PRODUCTS

Sl. No. Persons No. of

Respondents Percentage

1 Self 73 18.1 2 Wife / Husband 65 16.1 3 Children 69 17.1 4 Parents 60 14.9 5 Friends 71 17.6 6 Neighbors 66 16.3 Total 404 100.0

Source: Computed from Primary Data