chapter no.02 manual i - mumbai department list... · period 31.03.1977 in respect of railways and...

TRANSCRIPT

Manual I_ page no 1

Chapter No.02

Manual I

Under clause – Clause (4) (1) (b) (i) of Chapter II of the Right to Information Act, 2005

The particulars of organization, functions & duties of the Department :

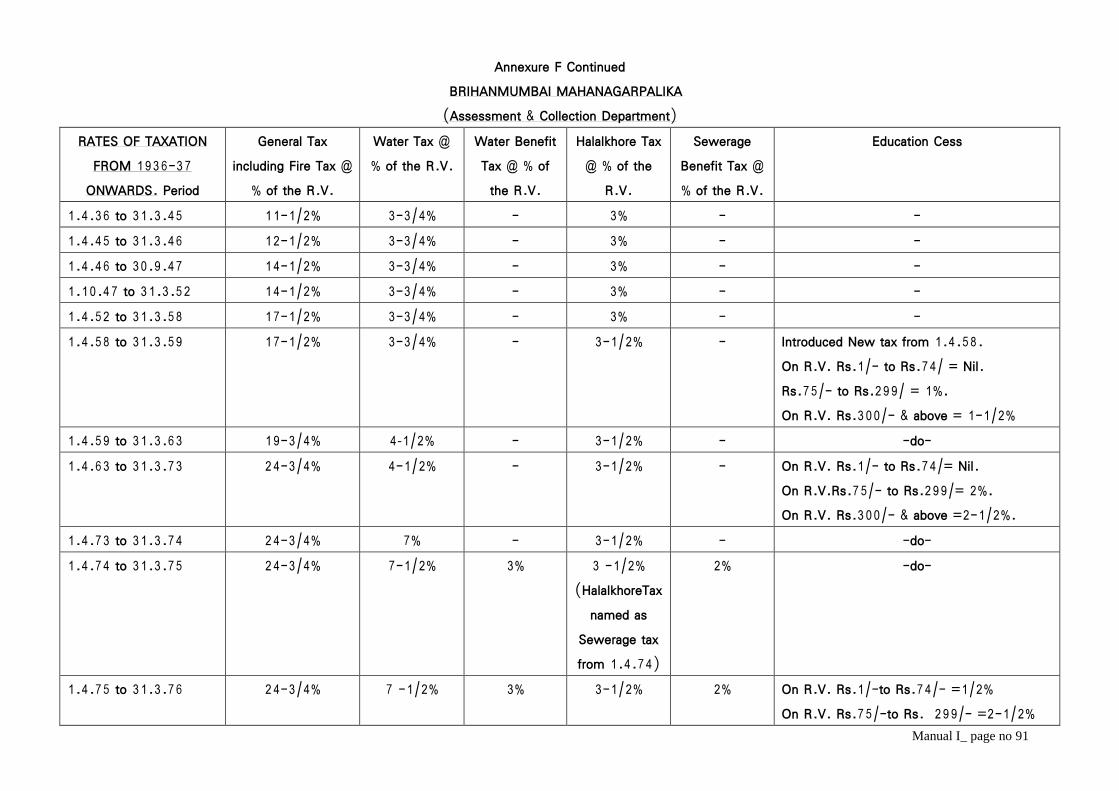

All the activities of the Department are performed under the provisions in the Chapter VIII of the Mumbai Municipal Corporation Act, 1888. Property Taxes and Octroi are the main sources of the revenue of the Corporation. About 60% of Municipal Revenue is yielded by the said sources. Collection of said taxes is made by the Department. It would not be worthless to say that the Department is the Major Pillar of Municipal Finance as the Corporation has to carry out all its project works through it. The Head of the Department is designated as Assessor & Collector and there are three main branches of the Department as stated below :-

(1) Assessment & Collection, (2) Octroi, (3) Election Branch.

All these branches are working under overall control of Assessor & Collector. Assessment & Collection, Octroi and Election branch are placed under the control of Assessor & Collector.

(1) Assessment & Collection Branch. Assessment & Collection branch is divided into three main Zones, namely City, Western Suburbs and Eastern Suburbs and each zone is headed by each Dy. Assessor & Collector. In addition to this, Computerization work related to the Department is under the control of the Dy. Assessor and & Collector (Computer). At Zonal Offices, there are various sections, viz. Establishment, Expenditure, Cash/Accounts, Legal, Transfer, Theatre Tax, Survey Section, Typing Section and work of these Sections is carried out by the Officers, Employees in various cadres such as Legal Officers, Administrative Officers, Head Clerks, Surveyors, Stenos,

Manual I_ page no 2

Typists, Clerks, Peons, etc. At Administrative Ward level, Assistant Assessor & Collector is the overall In-charge of the Ward. There are two sections in each administrative Ward, viz. Indoor & Outdoor. Ward Superintendent is the In-charge of and responsible for Outdoor Section and Dy. Superintendents, Ward Inspectors, and Clerks related to the outdoor work etc. are working under his Control. The administrative area of the Ward is divided into various sub-sections (Known as Ward Sections). Ward Inspector is responsible for the Ward Section allotted to him. All the Ward Sections are divided in 2-3 groups for supervision and control of the work of Ward Inspectors by the Superintendent and Deputy Superintendents. In Indoor Section, staff consisting of Head Clerks, Clerks and Typists are working under the control, supervision and guidance of the Assistant Assessor & Collector of the Ward. Assistant Assessor & Collector of the Ward is responsible for all the activities, functions, performance related to the work of the indoor section in particular and outdoor work in general. Other than the 24 administrative Wards, following Individual Sections are in operation

(1) Vigilance Branch (2) Computer Cell (3) Government, Port Trust, Railway Section (4) Wheel Tax (5) Appeal Section (Court Cases) (6) Theatre Tax (7) Maharashtra Tax on Buildings (8) Repair Cess (9) Statistics (10) Expenditure section (11) New Tax Cell

(1) The Vigilance Branch of the Department is headed by the Dy. Assessor & Collector (Vigilance) comprises of three Superintendents, four Senior Surveyors & three Ward Inspectors, they perform their duties for surprise, random checking of

Manual I_ page no 3

the property and reports regarding changes warranting revision, if found. The concerned Ward Superintendents acts for such revision in Ratable Value by reporting the property on Tabulated Ward Report. (2) Computer Section - As per MMC Act, 1888 sec 200(1) property tax bills, sec 144 GPR bills and as per MHADA Act repair cess bills are generated by computer section. The Computer Cell also monitors the work of issuing bills, bill books (indoor, Outdoor), UCP, Issue Advice, Annexure of Property Tax, Repair Cess, G.P.R. & get them printed through Municipal Printing Press, Further after going through, the output furnished by vendor appointed viz. M/s ABM Knowlegeware Ltd., printing & Dispatching job is monitored by computer section. Furthermore, the demand & amended demand so generated, is furnished to C.A for uploading in SAP. Moreover, the collection of MTOB tax from 24 wards is consolidated and report is sent to CA Department to remit the Government taxes to the Government treasury. Before 01.04.2007 this work was decentralized and was done at ward level. From 01.04.2007 all activities of collection for Assessment & Collection Department are done through SAP system. For this purpose, computer section has collected all required data in respect of all revenue heads from all 24 wards and provided the master data and OSM data to M/s ABM Knowledgeware, the authorized agency of Municipal Corporation of Greater Mumbai. The below mentioned works are carried out by this department

1. Module Development Changes, additions in the programming work. 2. All logs for corrections in the program 3. Co-ordination with the vendor of software development. 4. Implementation of GIS. 5. Implementation of 360 degree for survey of property 6. SAP-MM Module work,user id transfer,new id creation, password reset etc.

(3) Government, Port Trust & Railways Branch of the Department comprising of Superintendents, Deputy Superintendents, Ward Inspectors, Head Clerk & clerks, Peons is functioning under the control of Assistant Assessor & Collector for assessment of the Central & State Government & Railways properties and collection of a sum called as Service Charges in lieu of Property Taxes from the concerned

Manual I_ page no 4

authorities, as provided vide provisions of Section 144(1) (2) (2a) (3) in respect of properties entitled for exemption U/s 143(b) of MCGM Act 1888.

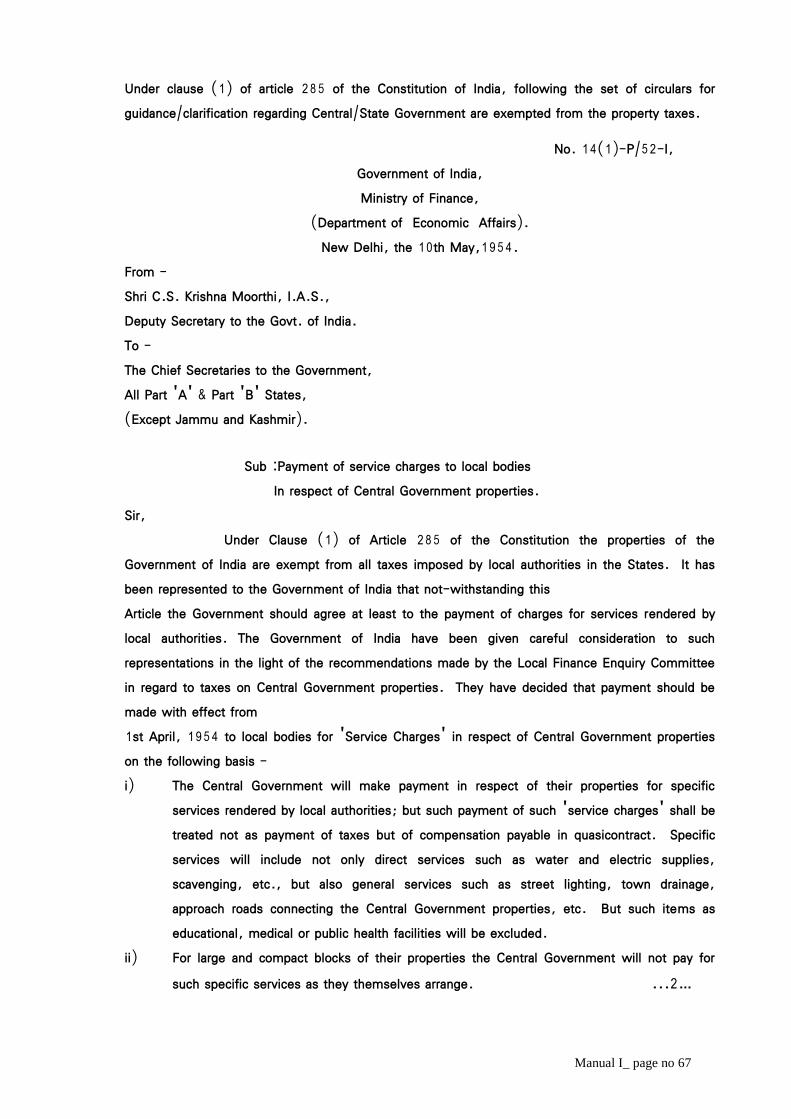

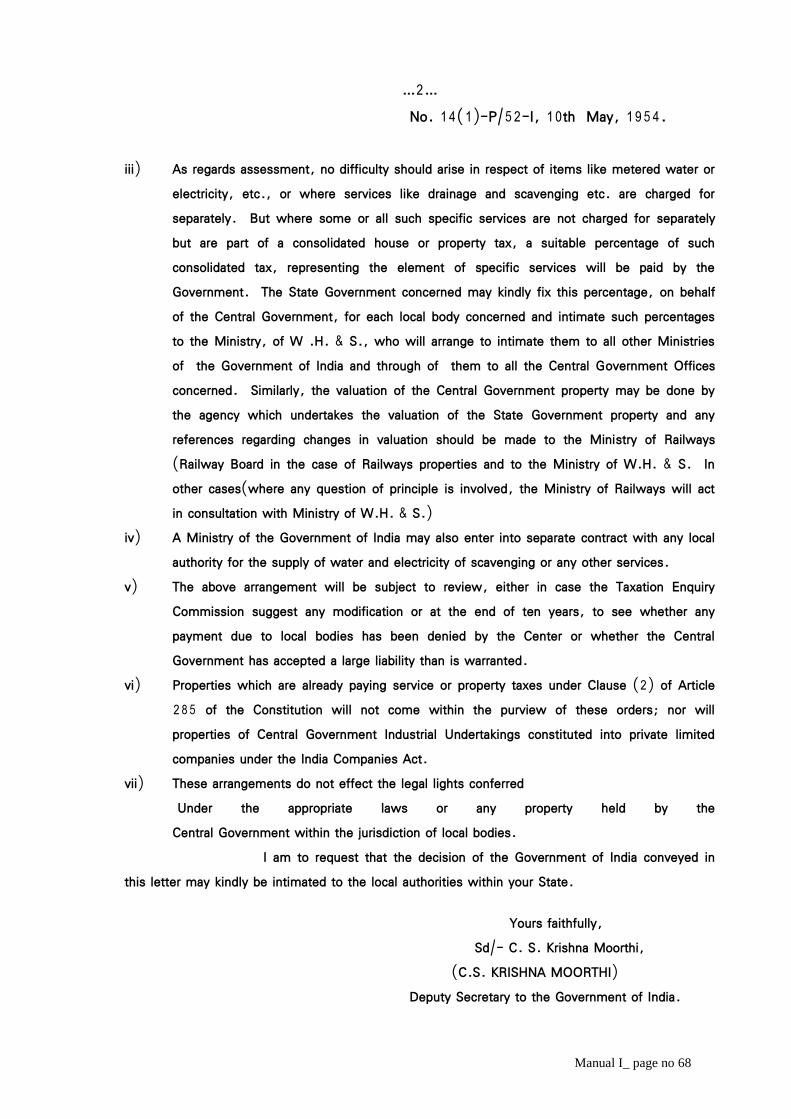

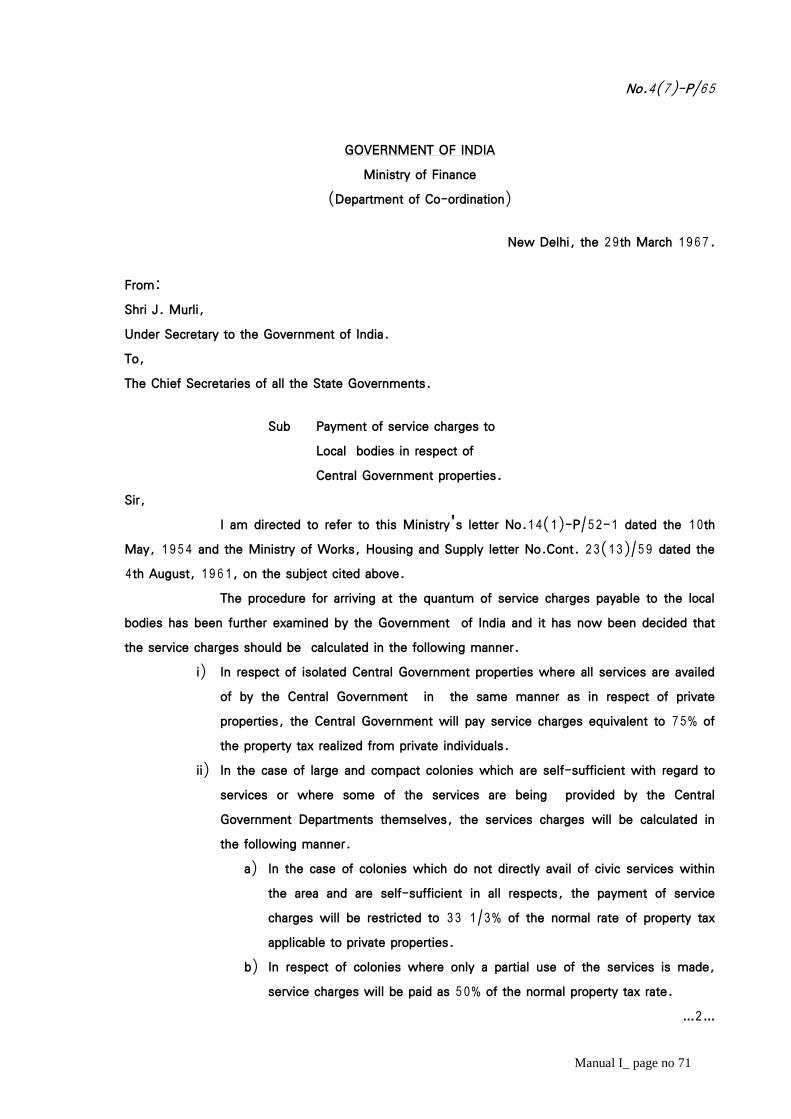

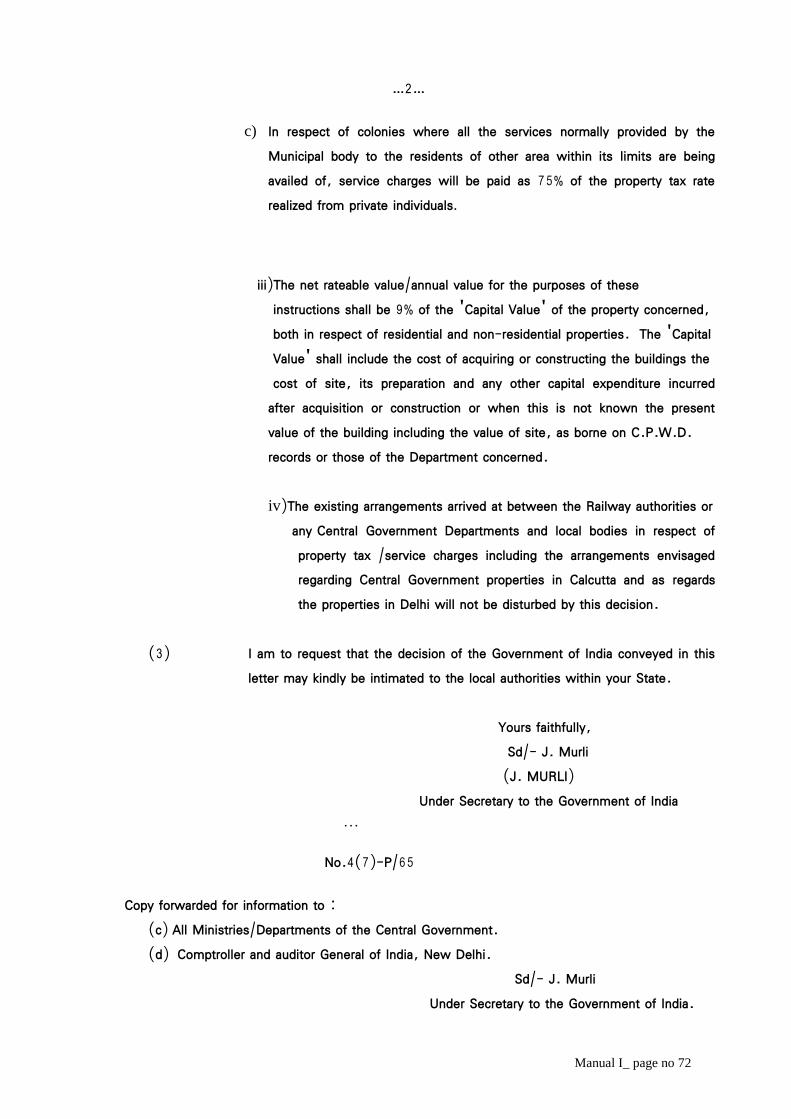

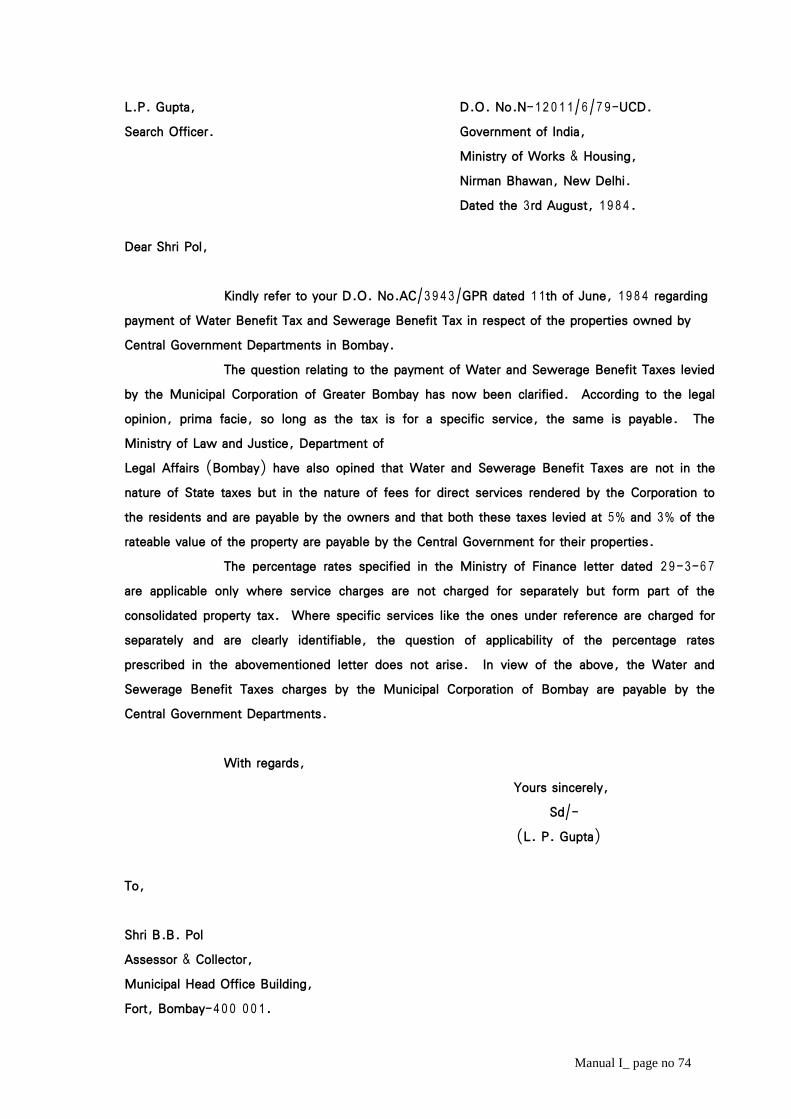

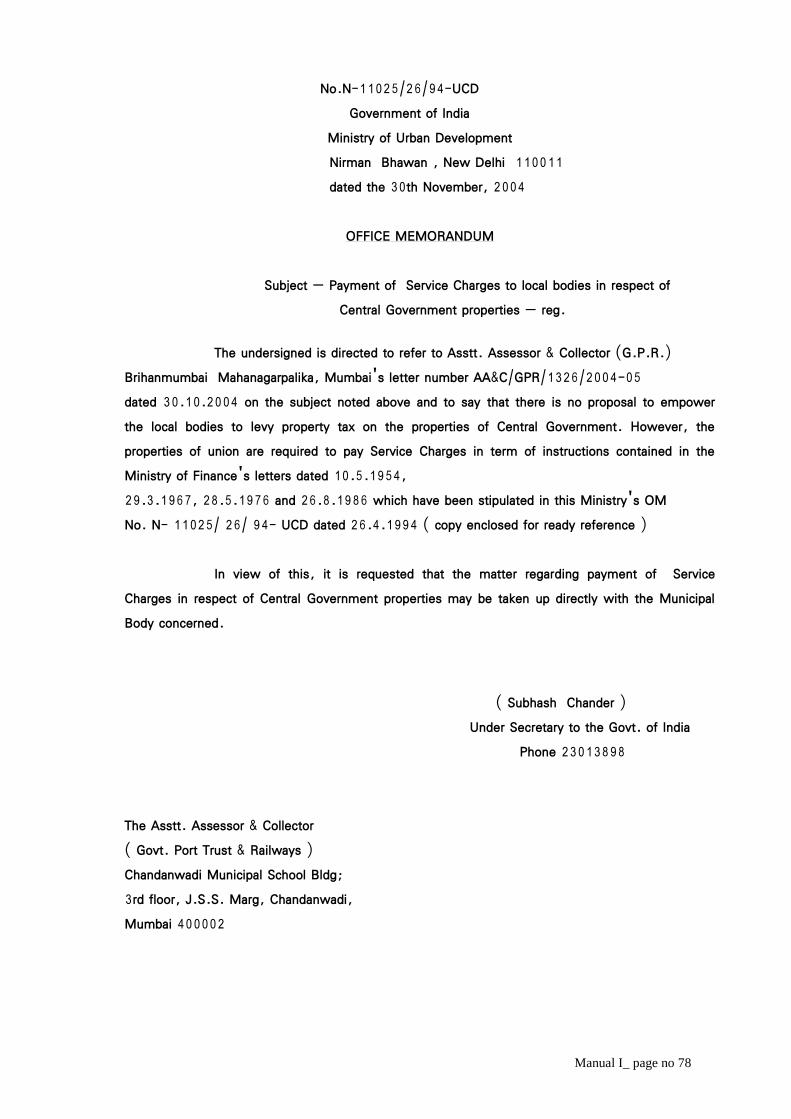

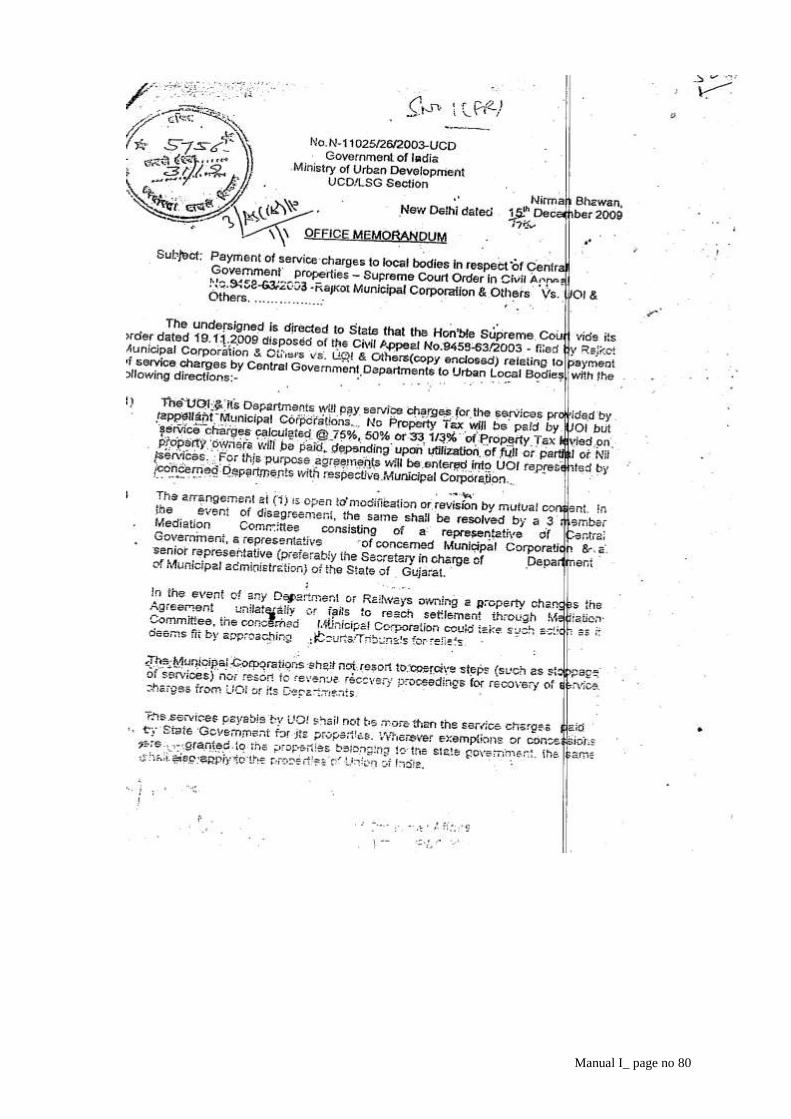

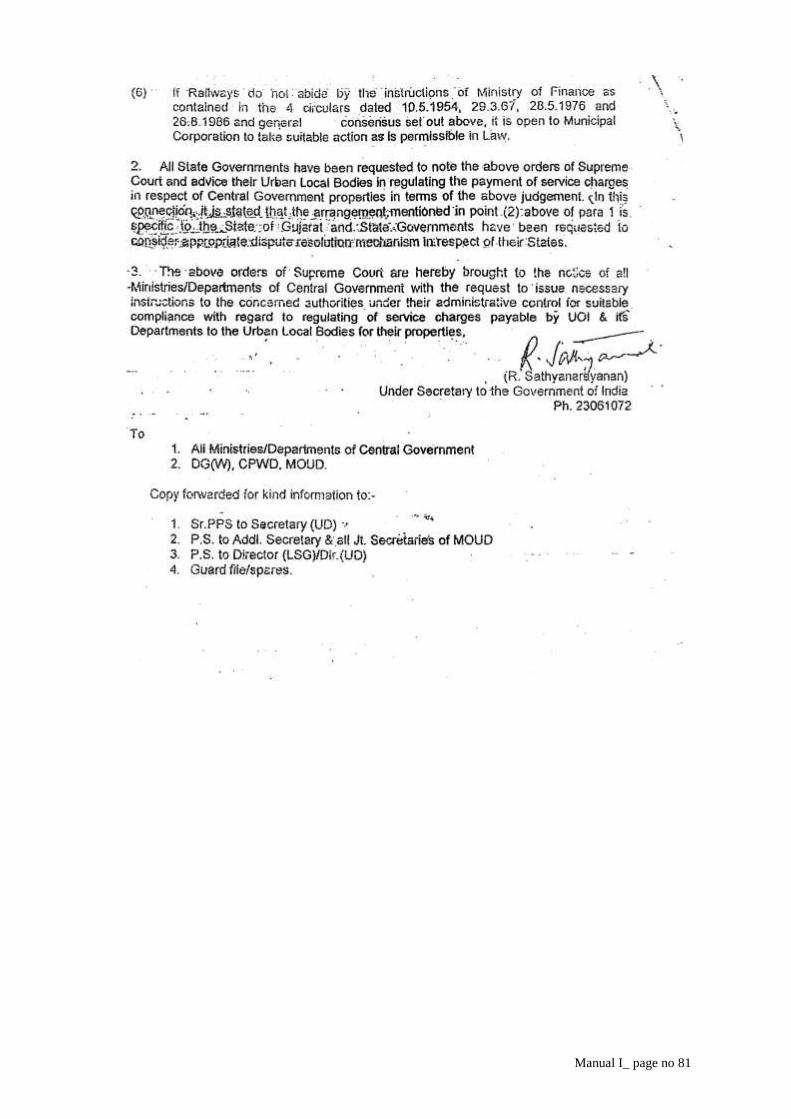

Similarly, under clause (1) of article 285 of the Constitution of India, the properties vested in the Central / State Government are exempted from the Property Taxes. However, the Central Government has decided to pay the Service Charges in lieu of the Property Taxes for the services provided by the Corporation. The Central Government has issued, from time to time the various circulars for guidance/clarification in this behalf. The set of such circulars is attached at Pg. 67 to 81.

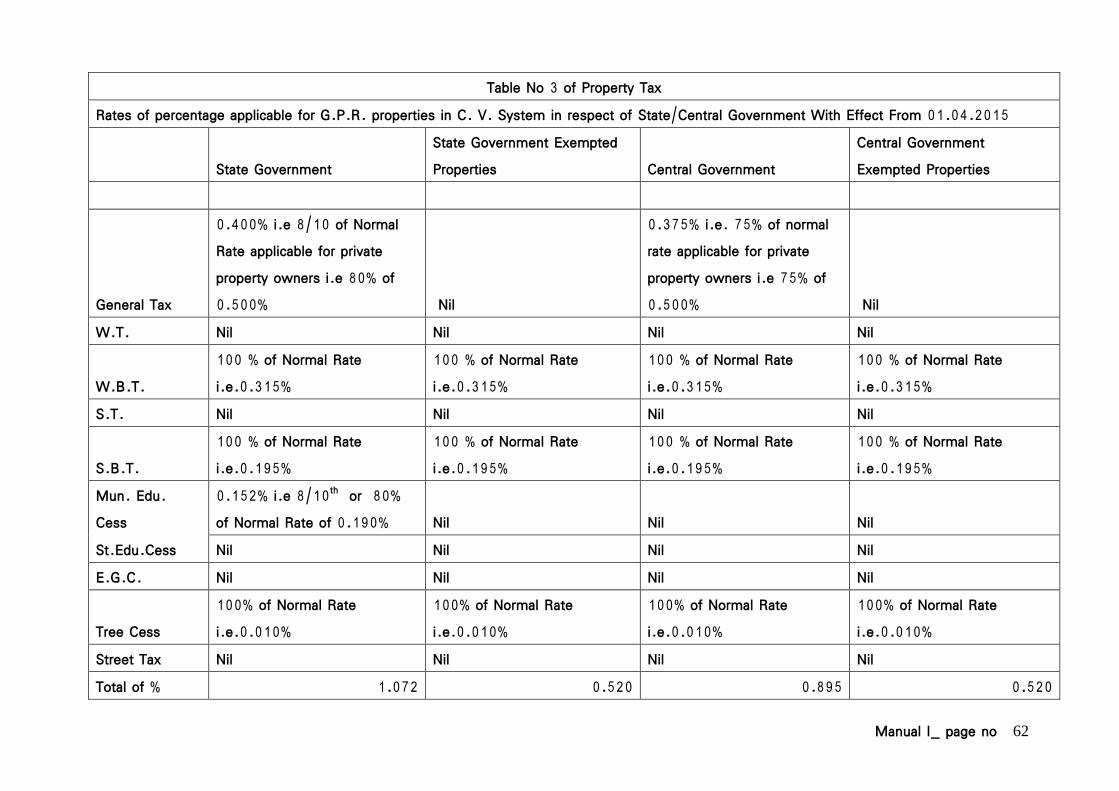

The rates of service charges in lieu of property taxes in respect of G.P.R. properties are shown at Manual I Annexure C-1 (Pg. No. 60 to 65)

As per the provisions of Section 144 (2) of MCGM Act 1888, a person is appointed by State Government with the concurrence of Corporation for fixing Ratable Value of the properties vested in the Central / State Government. The person so appointed for fixing the Ratable Value of Government properties takes a review of the properties newly erected or demolished during the each block period of 5 years, called a quinauennial period.

The Ratable Value of such properties is decided considering the rate at 9% of the total capital cost comprising of cost of the land, cost of construction and cost of electrical installations. The information with respect of cost of land, cost of construction, & cost of electrical installations along with other necessary details is obtained from Govt. Authorities, in the proforma attached at page 82 of Manual I .

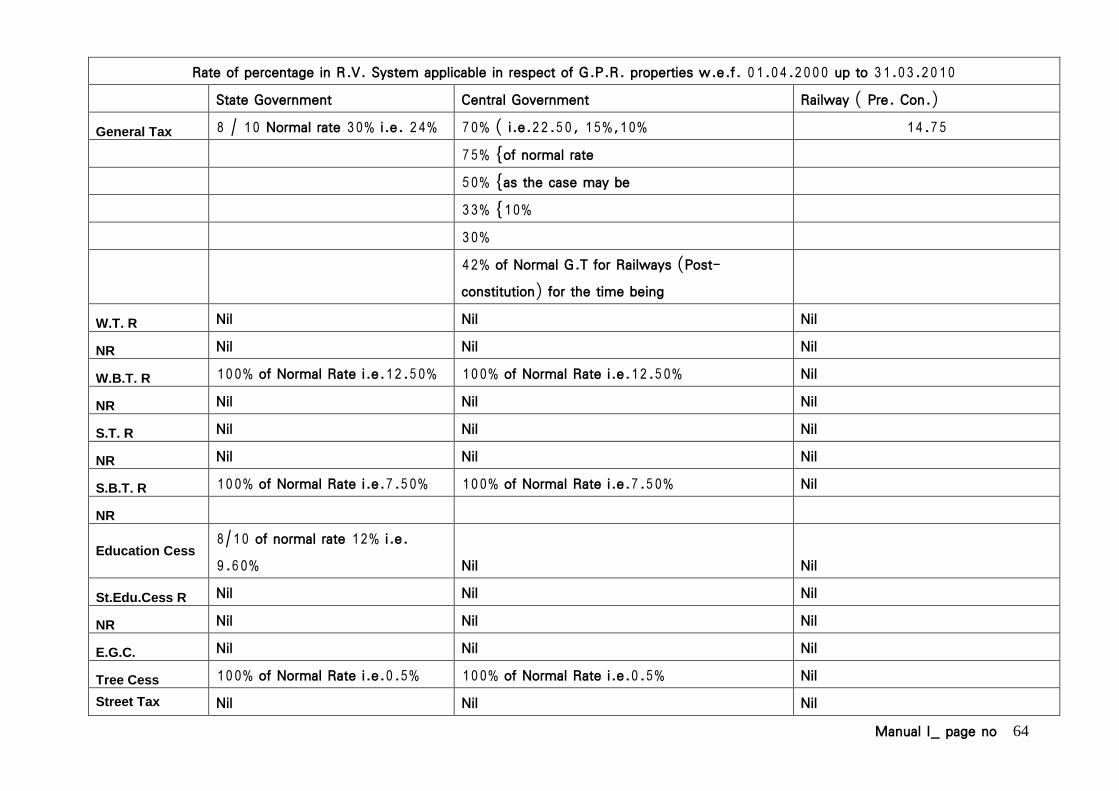

The Ratable Value of the properties vested in the Railways and Mumbai Port Trust is decided bilaterally by adopting, by and large, similar principles as in the case of properties vested in Central / State Government. The said work is completed up to period 31.03.1977 in respect of Railways and provisionally up to 31.03.1994 in respect of Mb.P.T. except 2 categories of Mb.P.T properties in respect of which the assessment is complete up to 31.03.1964.

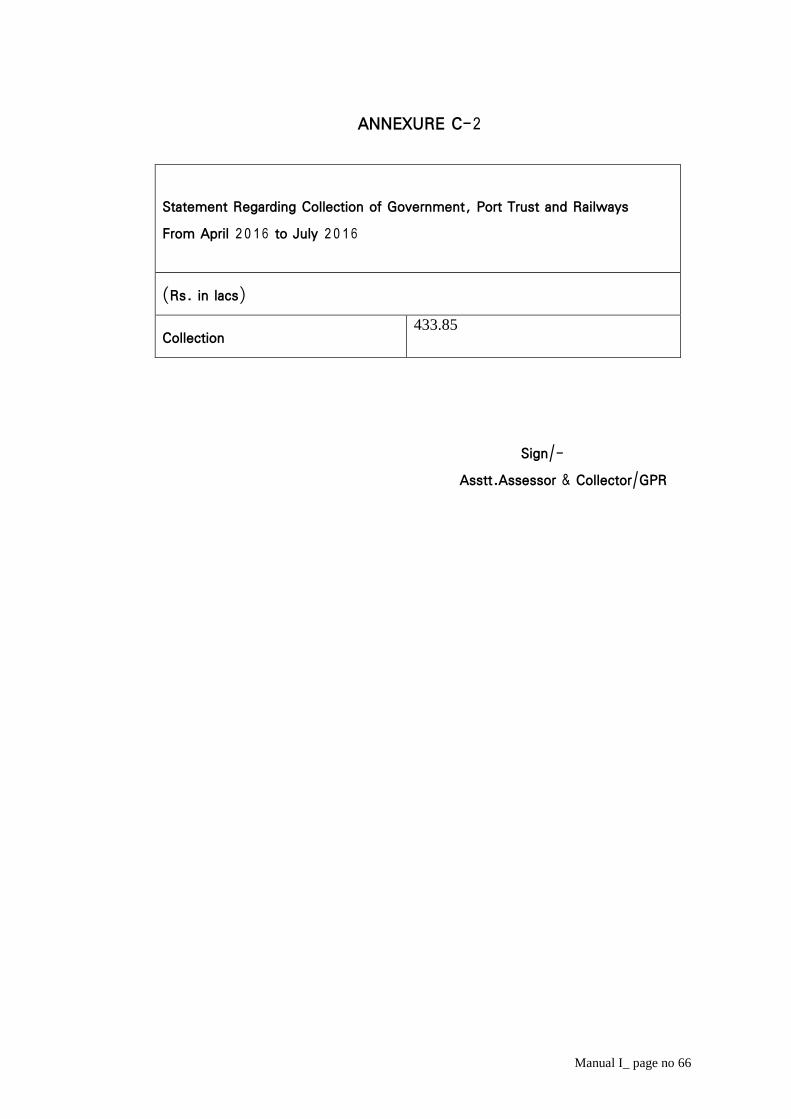

The work of fixation of Ratable Value of Government properties (State and Central Government) is completed upto31.03.1979 and is in progress for the further period from 01.04.1979 to 31.03.1994. The details of collection period on

Manual I_ page no 5

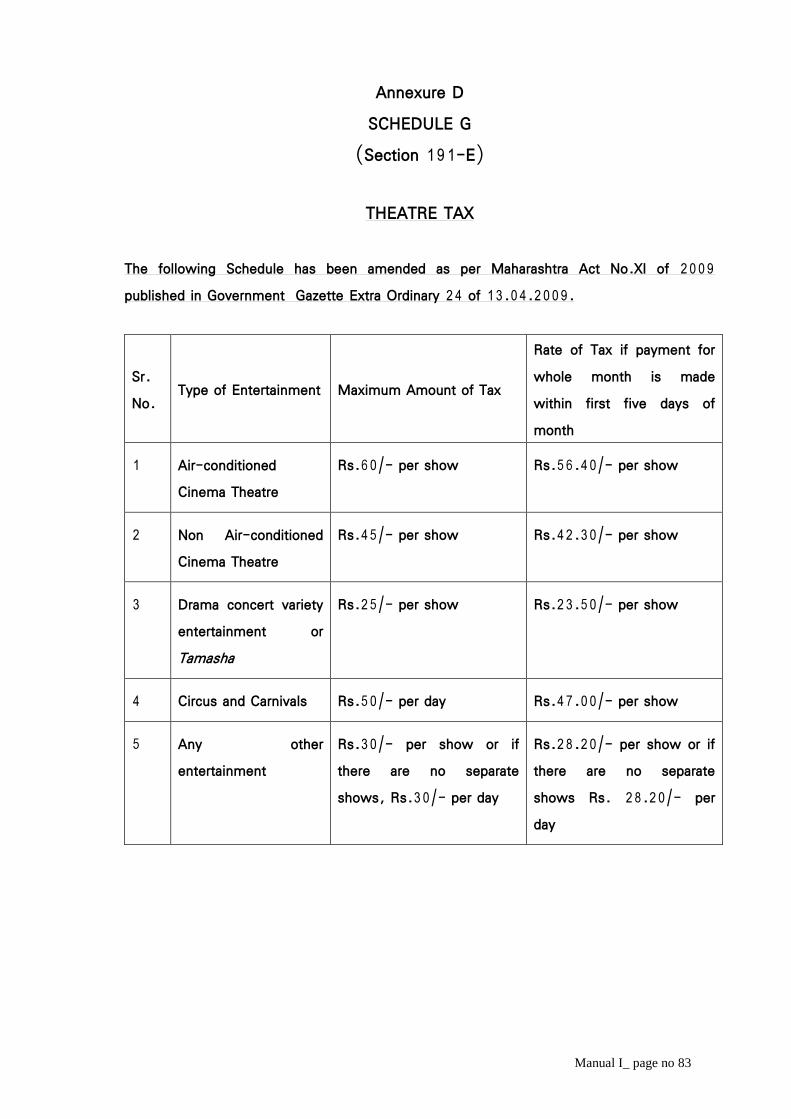

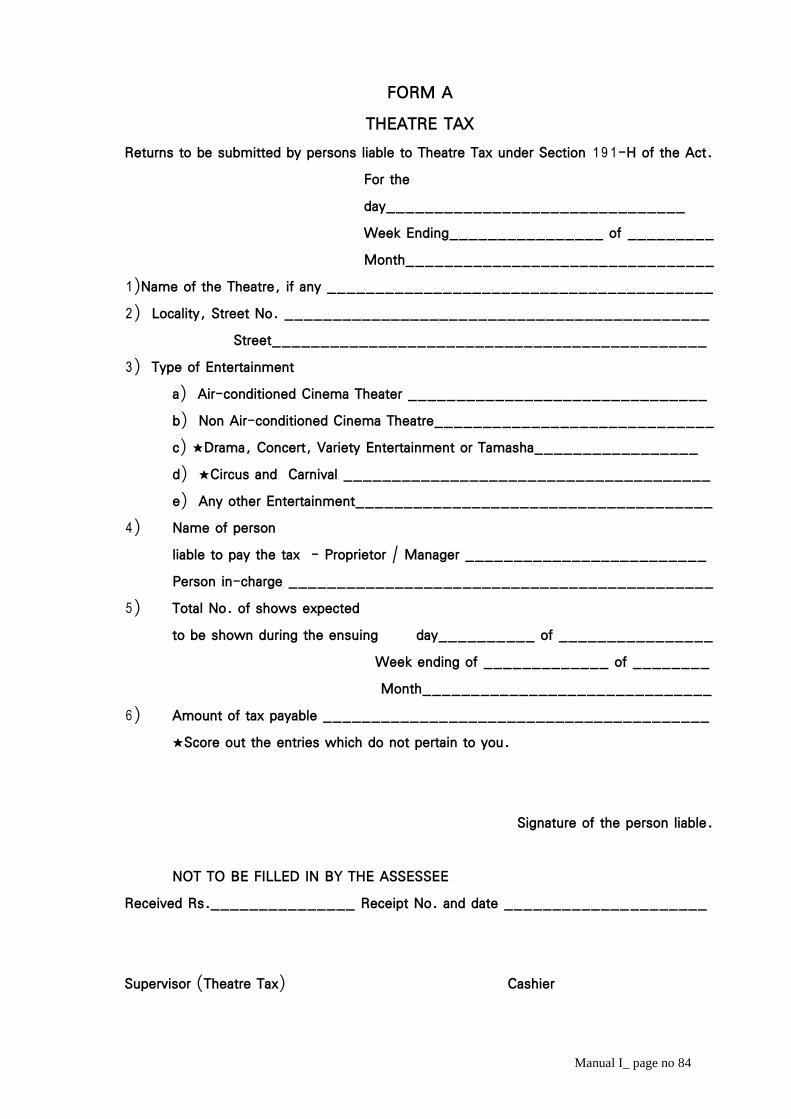

Dt.01.04.2015 to 31.07.2015 is shown in the Manual I Annexure C-2 (Pg. No. 66) (4) The Wheel Tax was levied up to the period ended 31.03.1999. As per directions given by Government of Maharashtra, Wheel Tax is abolished with effect from 01.04.1999. (5) The Appeal Section working at Head office of Assessment & Collection Department under the Head of Assistant Assessor & Collector mainly submits the affidavit for all Court Cases under section 217 of MMC Act in Small Causes Court. This section co-ordinate the work between Legal Department & Assessment Department for all Court Cases mainly in Small Causes Court & others. The staff attends the Small Causes Court daily & assist the Assistant Law Officer as necessary. If First Appeal is to be preferred for cases disposal off in Small Causes Court, Appeal Committee Meeting is arranged periodically & minutes of the Appeal Committee Meeting is prepared & circulated to all concerns time to time. (6) Theatre Tax: Under Section 191 E (1) to (3) of the Act, a Theatre Tax at the rates not exceeding those specified in Schedule G (Annexure D) is levied in respect of Theatre, Cinema, Circus, Carnivals and other places of entertainment for every performance or show held or conducted thereat or therein and to which persons are admitted on payment. The Cinema Theatre also included the places where movies are screened with the help of scientifically developed technology / machinery / equipment. This Tax is payable in advance before the commencement of each show or if there are no separate shows before any person is admitted to the entertainment on any day, by every Proprietor, Manager or person in-charge of the entertainment. For this purpose, under the provision of section 191(F) & 191(H), every Proprietor, Manager or person In-charge of entertainment has to submit a return signed by him in the Form A appended hereto for the purpose of levy of Theatre Tax. Further under section 471 of M.M.C. Act, 1888, minimum fine of Rs.500/- to Rs. 2500/- can be imposed on the person primarily liable of payment of theatre tax in case of non-submission of Returns.

Manual I_ page no 6

If any person fails to pay Theatre Tax, a notice of demand is to be served on the defaulter after three days of the show or performance. No fee is, however, to be charged for such notice. If the tax is not paid or sufficient cause is not shown for nonpayment of same to the satisfaction of the Commissioner within 15 days from the date of service of notice of demand, it can be recovered by distress and sale of moveable property or attachment and sale of the immoveable property of the defaulter as if the amount were a property tax due by him. Refund of Theatre Tax is also admissible if a show or performance in respect of which the tax has been paid does not take place and an application there for is made within seven days from the date of such a show or performance.

Exemption from payment of Theatre Tax can be granted to the show or performance by the Municipal Commissioner provided it is exempted from payment of duty leviable under the Bombay Entertainment Duty Act, 1923 and that such exemption is applied for with an Exemption Certificate under the Bombay Entertainment Duty Act, 1923 prior to the show or performance or series of shows or performances.

The Municipal Commissioner may, however, in his discretion permit the production of the said certificate at a later date in any special case or class of cases.

Generally exemption from payment of Theatre Tax is granted, if the entertainments are in aid of the following and they are exempted from payment of entertainment duty.

(1) Building fund of an Institute or School. (2) Educational fund of an Institute. (3) Poor Boys’ fund. (4) Scholarship fund of a school or a college. (5) Entertainment aimed at promotion of artistic and cultural activities. (6) Exemption from Theatre Tax to be granted to all entertainments held on

payment of admission fee of One Rupee or less except cinema shows. (7) The object of charity or other object in aid of which funds are to be

utilized should be one that falls within the limits of Greater Bombay and

Manual I_ page no 7

should not pertain to places outside Greater Bombay. The rates of Theatre Tax are determined by the Corporation from year to year

before 20th day of March of each year, subject to limitations laid down in Schedule G-I appended to the Bombay Municipal Corporation Act. The rates determined by the Corporation are required to be published in the major local newspapers. Prevailing rates of the said tax are as per the maximum rates as shown in the Schedule G-1 as Annexure D (Pg. No. 83).

(7) Maharashtra Tax on Buildings : 1) M.T.O.B. Act: Maharashtra Tax on Buildings (With Larger Residential

Premises) Maharashtra Act No.29 of 1979. 2) Larger residential premises mean the premises having floorage exceeding

125 sq. meters and the Ratable Value of which is more than Rupees one thousand and five hundred.

3) Residential premises: This means any building or part thereof used on intended for independent use for residential purpose.

4) Floorage: Means the total floor area of the premises excluding thickness of walls (i.e. carpet area).

5) Garages or quarters intended for the use of servants and used as such by them are excluded from the levy.

6) Objective of the Act is that– There should be a check on extravagant use of available living space.

More residential accommodation of which there is an acute scarcity may become available in thickly populated cities and buildings which will come up after imposition of such tax might not contain, any, or might contain less no. of larger residential flats or premises.

Though the appropriate amendments into Maharashtra Tax on Large Building act 1977 have been done by the state government, notification in respect of the rate at which the said tax is to be levied is not yet published by them. As a result the bills for the said tax have not been issued since 2010-11. However the recovery in respect of the arrears is being carried by the department.

Manual I_ page no 8

Levy & Collection of Tax The Maharashtra Tax on Buildings (with Larger Residential Premises) (Re-enacted) Act, 1979, under section 3(A) provided for the levy of taxes on residential premises in Corporation areas, the floorage which exceeds 125 square meters in Greater Mumbai. This tax is belongs to Maharashtra Government and collected by Municipal Corporation of Greater Mumbai. The tax shall be levied and collected on the basis of property tax.

Primary Responsibility for Tax : As per Section 3 the tax is leviable on any residential premises, if actual occupier is the owner of the property then said tax is leviable under section 4 (1) of the Act. As per Section 4 (2), the primary liability of taxes as follows::

(a) If the premises are let from the lessor. (b) If the premises are sub-let from the superior lessor.

Under Section 5(1) if any person from whom the tax is leviable under the provision of Section 4, pays the tax in respect of any residential premises in a building he shall, if he is not himself in occupation thereof, during the period for which he has paid the tax, be entitled to receive the amount of tax from the person in actual occupation of such premises for the period aforesaid.

As per the provision of Section 7, the Assessing Authority is appointed by the Commissioner for the purpose of assessment of the tax.

Powers, duties & functions of Assessing Authority: As per Section 8(1) the Assessing Authority prepares a list of buildings

containing taxable premises including their proportionate Ratable Value. The Assessing Authority may inspect any buildings or premises or make such enquiries as it thinks fit under this provision. As per the provision of Section 16, the Assessing Authority, Appellate Authority or any of these officers authorized by any of these authorities, after due notice between sunrise and sunset can enter any taxable premises for the purpose of collecting particulars relating thereto or for taking measurement of the premises can call upon the owner of the premises.

Manual I_ page no 9

Under Section 8 (3), the State Government may call upon the owner of every such taxable premises to furnish to the Assessing Authority a return containing all the particulars of the property within two months from the appointed day or such longer period as it may specify in that behalf, to enable the Assessing Authority to prepare and publish a list of taxable premises.

Under the provision of Section 20, if any person fails, without reasonable cause to furnish to the Assessing Authority any return under Section 8, the Assessing Authority may after giving a show cause notice impose a penalty which may extend to one hundred rupees.

Under Section 21, if any person makes a false statement or furnishes false information in the return he shall on conviction be punished with simple imprisonment for a term which may extend to six months or with fine which may extend to one thousand rupees or with both.

Section 9 (2) provides for the preparation of the assessment list for the first time within one year from the appointed day or such longer period as the State Government may specify in that behalf and every such subsequent list is prepared before the 30th day of June of the year to which it relates.

Under Section 9 (3) if after preparation of the assessment list under sub-Section (2) any modification on account of deletion, alteration or addition of an entry in the list is rendered necessary, the Assessing Authority prepares a list of such modification.

Section 10 (1) provides for the publication of a notice in local newspapers on 1st of July of two relevant years specifying therein the stipulated period for inspection of the assessment list. Accordingly the necessary public notice to that effect is given in some of the local newspaper, Government Gazette and also displayed on the Ward Office Notice Board. The list as modified is kept open for inspection by the public during the period from 1st July to 23rd July in the respective Ward Office.

The stipulated period fixed by the Assessing Authority in this regard is from the first of July to 23rd July within which any person claiming to be either the owner of occupier of the premises, included in the list, and any agent of such

Manual I_ page no 10

person, is at liberty to inspect the list and to take extract there from without any charge.

Objection against the tax: As per provision of Section 10 (3), the objections to the list of modification

are to be given in the office of the Assistant Assessor & Collector of the respective Ward. Under the provision of Section 10 (3), objection to the Assessment list or list of modification made by the owner are registered in a book kept by the Assessing Authority for this purpose. The Assessing Authority investigates and disposes of the objections, after allowing the reasonable opportunity to the complainant. After hearing of the objections the result thereof is entered in the book kept under Section 10 (3) and the assessment list and list of modifications are amended accordingly. The authentication of assessment list and the list of modification is made by the Assessing Authority under Section 10 (5). Appeal against the tax: Appointment of Appellate Authority is made by the Commissioner under Section 11(1). Any assesse objecting to the amount of tax assessed by the Assessing Authority or denying his liability to pay the tax so assessed appeals to the Appellate Authority against the assessment in the prescribed manner by filing in ‘B’ form in duplicate within fifteen days after the presentation of the bill. No such appeal shall, however, lie unless the tax has been paid. Under Section 11(5) at the hearing of the appeal the Assessing Authority also has the right to be heard. Under Section 11(8) The orders passed by the Appellate Authority are final and cannot be called in question in any court. Collection of tax: Under the provision of Section 12 (2), the M.T.O.B. Tax is collected in the same manner in which the property tax is collected.

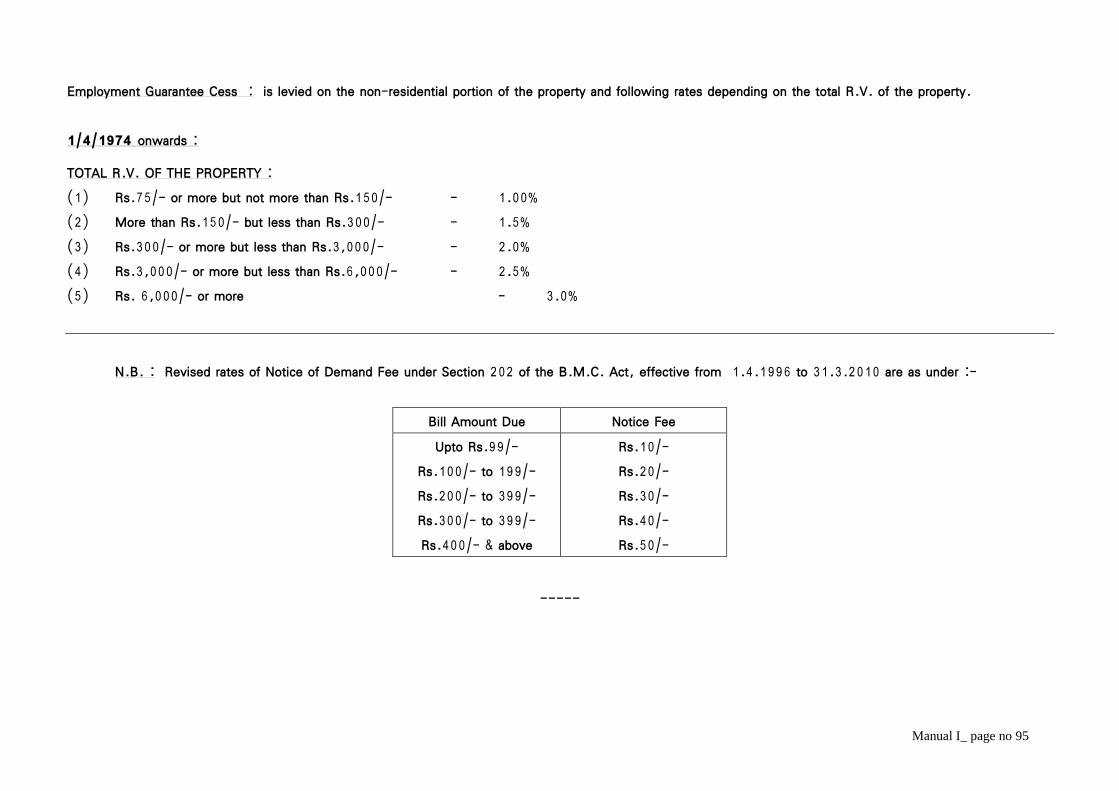

Manual I_ page no 11

1) Notice of Demand fees is payable if the bill is not paid within fortnight from the date of service of the bill. 2) Penalty to the extents of 10% of the amount of bill is recoverable after the

period of three months as per section 19 (1). The 5% rebate / commission as a cost of collection of the tax to be received

from State Government to the Corporation. Refund of tax paid: Section 17, provides for the refund of M.T.O. B. Tax if paid in excess or recovered wrongly. As per Section 18, the refund is admissible if the claim is made within one year from the date of payment of tax and in case of appeal has been preferred within one year from the date of receipt of the appeal order. Exemption from tax:

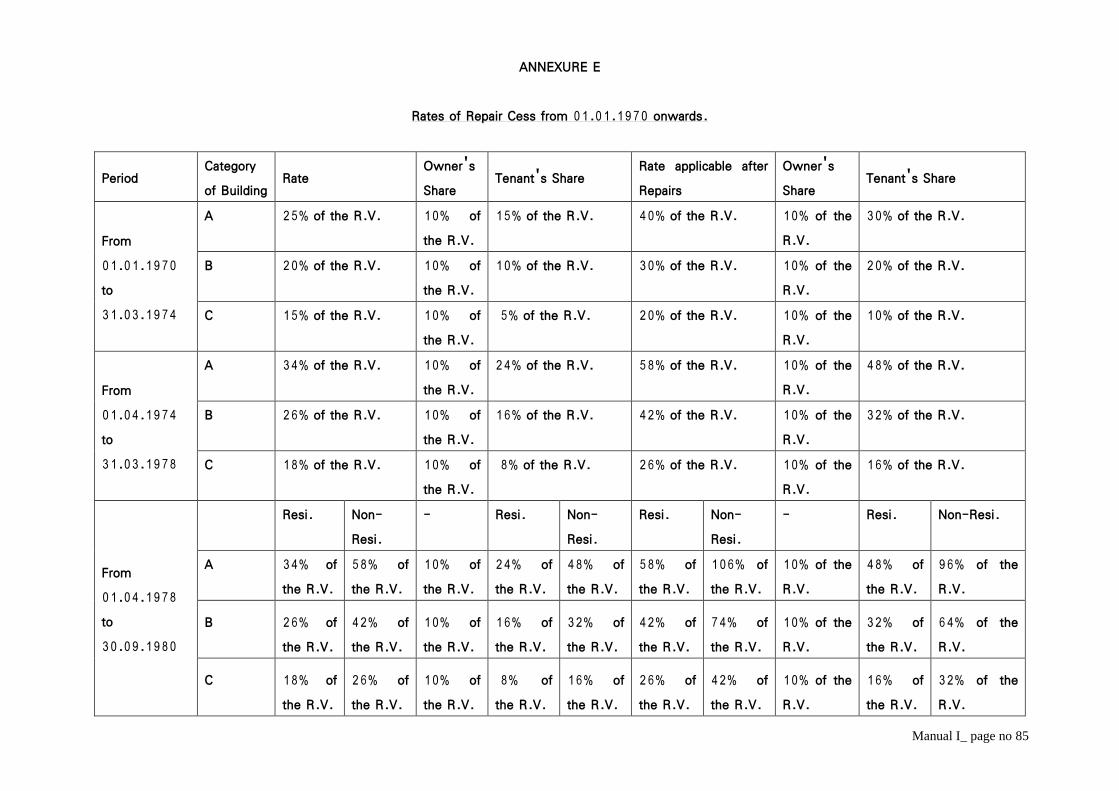

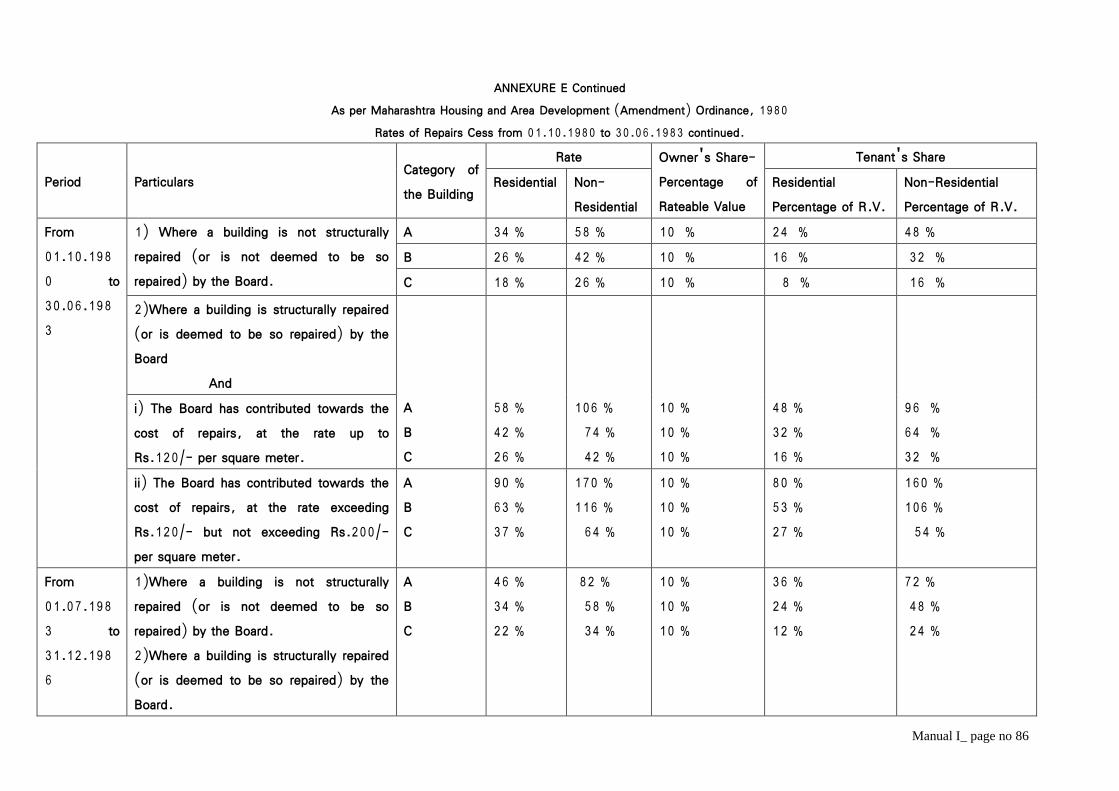

Under the provision of Section 24, the following buildings are exempted from payment of the Tax. a) Buildings vesting in or belonging to the Central or State Government. b) Buildings vesting in any other Government or belonging to any purpose and not use or not intended to be used for purpose of profit. c) Buildings vesting in the Board of Trustees of the Port of Mumbai and not used or not intended to be used for the purpose of profit. d) Buildings or parts thereof vesting in or in occupation of consulates of foreign States or of any members of the staff of such officials and such buildings or parts are not used or not intended to be used for the purpose of profit. (8) Repairs Cess: The Maharashtra Housing And Area Development Act, 1976 (MHADA Act). The Repairs Cess is leviable on buildings situated only in the City Zone of Mumbai. For the purpose of levy of Repairs Cess, all the buildings have been classified into three categories considering the age of building such as :-

Manual I_ page no 12

Note: No Repair Cess is levied on the buildings totally erected on or after 01.01.1 970.

Under Sec.82 (2) of Maharashtra Housing & Area Development Act, 1976, the Repairs Cess is collected by Municipal Corporation of Greater Mumbai in the same manner in which the property tax is collected.

Exemption of certain buildings and lands from payment of Repair Cess:- Under Section 83(1) of Maharashtra Housing & Area Development Act,

1976 the following lands and buildings shall be exempt from payment of the cess, i) Properties of the Central Government; ii) Properties of the State Government; iii) Properties of the MCGM; iv) Properties of MHADA; v) Properties of the Trustees of the Port of Mumbai, and not used or intended

to the used for the purpose of profit; vi) Properties vesting in, or leased to, a public trust registered under the

Bombay Public Trusts Act, 1950, and exclusively occupied for public worship or for educational purposes;

vii) Properties of co-operative housing societies: viii) Properties of any Diplomatic or Consular Mission of foreign State; ix) Properties exclusively in the occupation of the owner which are not repaired

by the Mumbai Buildings Repairs & Reconstruction Board (MBRRB) ; x) Properties exclusively used for non-residential purposes which are not

repaired by the Mumbai Buildings Repairs & Reconstruction Board (MBRRB);

Category A : The Buildings erected before 01.09.1940.

Category B : The buildings erected between the period from 01.09.1940 to to 31.12.1950 (Both inclusive).

Category C : The buildings erected between the period from 01.01.1951 to to 31.12.1969 (Both inclusive).

Manual I_ page no 13

xi) Residential properties exclusively occupied on leave and licence basis which are not repaired by the Mumbai Buildings Repairs & Reconstruction Board (MBRRB);

xii) All open plots of lands. The rates of the Repair Cess leviable in respect of buildings of ‘A’, ‘B’ &

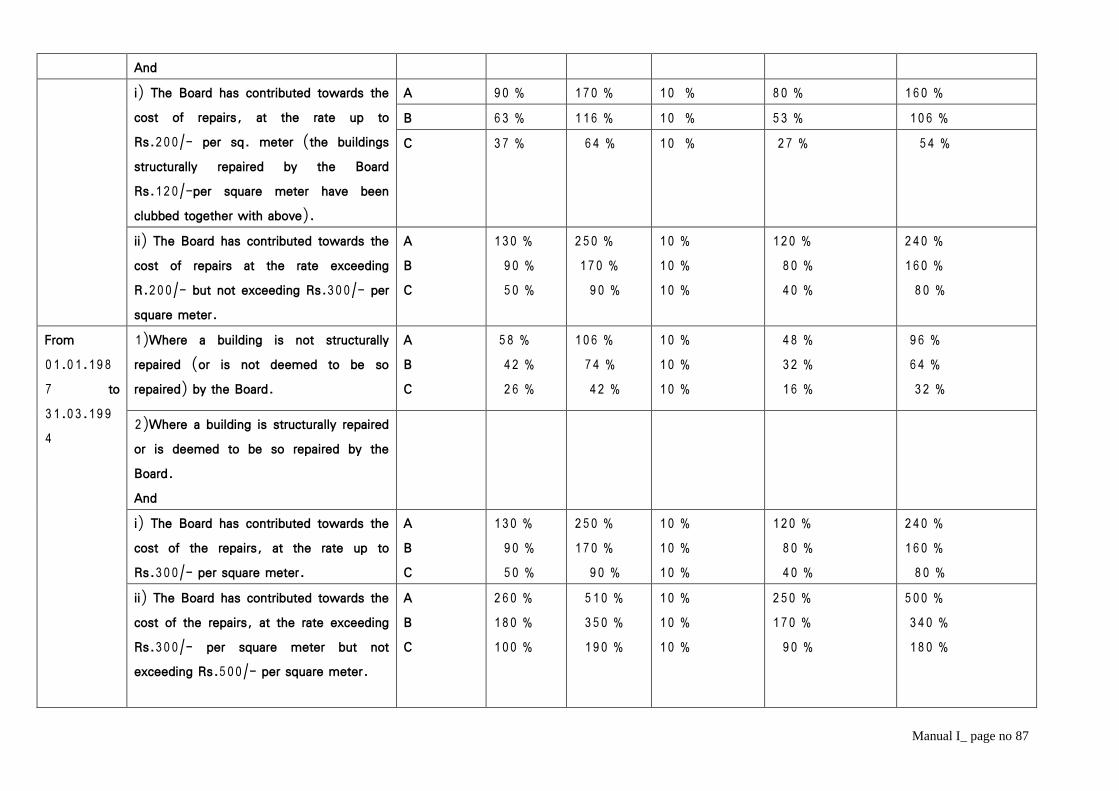

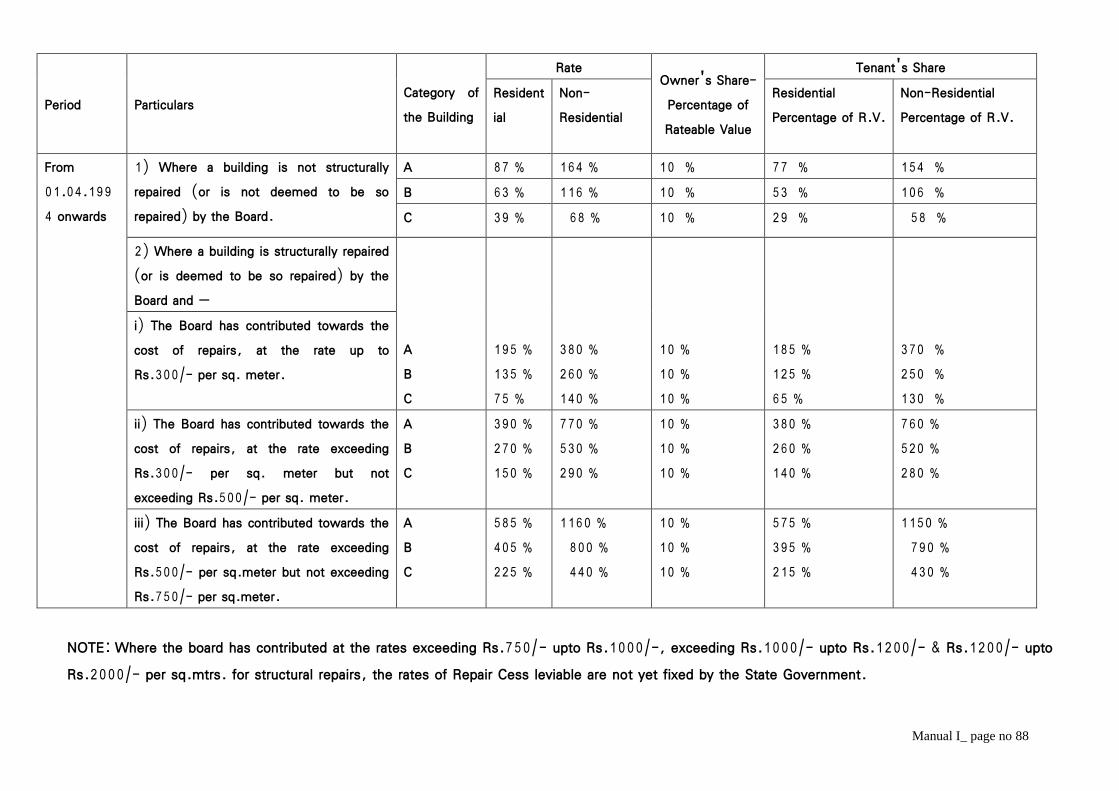

‘C’ categories respectively are 87%, 63%, 39% of the Ratable Value of the building where a building is not structurally repaired by the Mumbai Buildings Repairs & Reconstruction Board (MBRRB), 195%, 135% and 75% of the Ratable Value, where the MBRRB has contributed upto Rs.300/-per Sq. Meter for structural repairs, 390%, 270% and 150% of the Ratable Value, where MBRRB has contributed from Rs.300/- to 500/- per Sq. Meter for structural repairs and 585%, 405% & 225% of the Ratable Value, where MBRRB has contributed above Rs.500/- to Rs.750/- per Sq. Meter for structural repairs of residential properties. Where MBRRB has contributed above Rs.750/- to Rs.1000/- & above Rs.1000/- to Rs.1200/- & above Rs.1200/- up to Rs.2000/- per sq. mtr. for structural repairs, the rates of Repair Cess leviable are not yet conveyed to this Corporation by the State Government.

Where any part of the building is or are used for non-residential purposes the rates of cess leviable at present in respect therof are 164%, 116% & 68% of the ratable value of non residential part of the building, where a building is not structurally repaired by the board and at 380%, 260% & 140% where the board has contribute up to Rs.300/- per sq. Meter for structural repair and at 770%, 530% & 290% where the Board has contributed between Rs.300/- to Rs.500/- for structural repairs and at 1160%, 800% & 440% where the Board has contributed between Rs.500/- to Rs.750/- for structural repairs.

The Rate pamphlet furnishing the Rates of Repairs Cess from 1.1.1970 onwards is shown in Annexure E (Pg. No. 85 to 88).

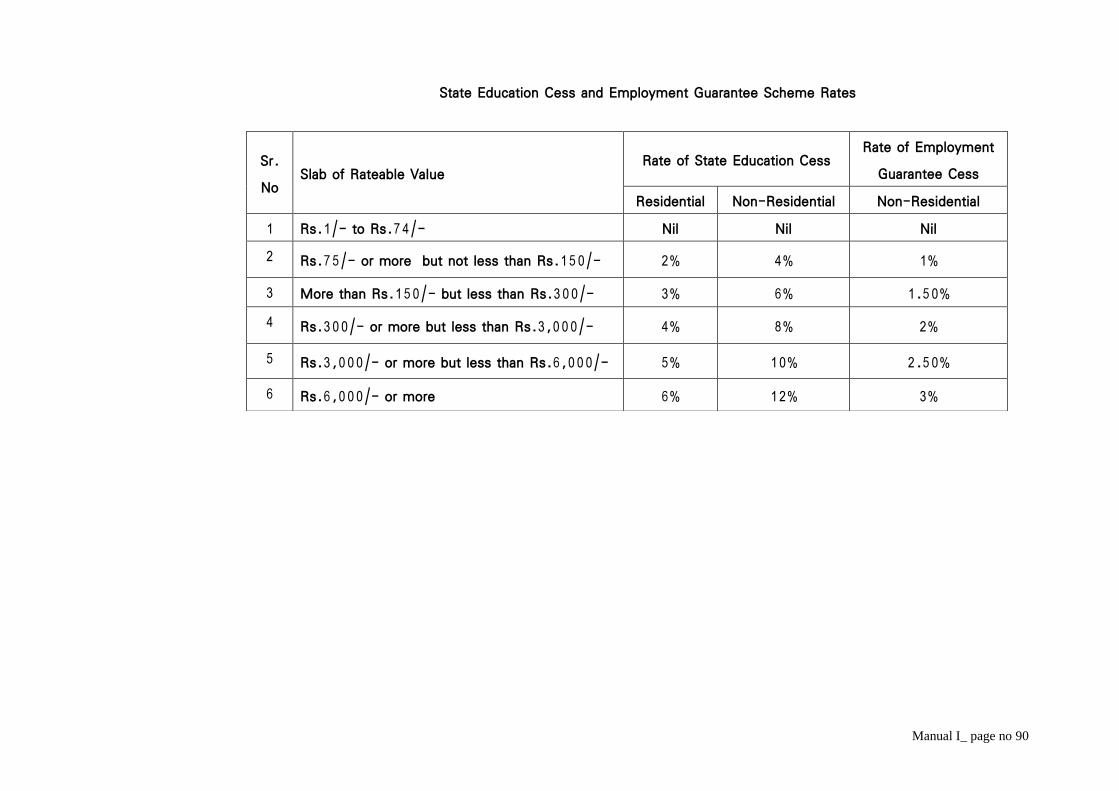

(9) Statistics:- Reply to all Questions raised in Vidhan Sabha&Vidhan Pareshad regarding Assessment & Collection (Star Question, Non Star Question, Ashwasan, Harkaticha Mudda, Kapat Suchana, Lakshavedhi Suchana & reply to questions raised by Corporator under Section 66A, 66 B, 66C. Put up Proposals & to take a Sanction of Competent Authority of all Municipal Committee & to submit DL to Municipal secretary. To put up Proposal of Policy matter & after sanction of Competent

Manual I_ page no 14

Authority, issue the circulars as required. As per Report received from computerized system, prepare Administrative Report & submit to Municipal Commissioner’s sanction. To prepare Revenue &Expenditure Revised Budget & Budget Estimate of Financial Year, for Assessment & Collection Department & Budget Speech.

(10)Expenditure section:- Preparation of proposals regarding maintenance & Servicing, Keeping track of maintenance & servicing of Computers, Printers ,Franking Machine. Preparation of P.O. Migo etc. in Sap system. Preparation of Budget. Preparation of proposals for advances, Closing advances &paper work regarding advances. Making payment EMD, Security Deposit, Bank Guarantee, legal contract etc. DL to Municipal secretary, Preparation of monthly collection report of St.Education Cess & Employment Guarantee Cess related to State Government & reported to C.A.(Finance).

To preserve & update Dead Stock Register (9) Capital Value System : -

In order to overcome the shortcomings of the old system, Capital Value based property tax system has been introduced. The new system is simple, transparent and self-assessable. The implementation has been carried out in the month of December 2012 with the retrospective effect of 01.04.2010 by amending the law as per due process. The amendments to the BMC Acts came into force from 01.04.2010. During the intervening period a Joint Select Committee was appointed by the Legislative Assembly to look in to the proposed change. This committee after long deliberations approved the amendments after effecting some changes. Corporation has also passed a resolution bearing No.1091 of 27.01.2010 approving the change over from the Ratable Value System to the Capitalized Value System with effect from 01.04.2010. An Expert Committee was appointed to prepare the rules and the classification of the lands & building with respect to age of the building, type of construction, user category and other factor if any and also to assign the weightages

Manual I_ page no 15

thereto. Objections & suggestions were invited after publishing the Draft Rules and after going through the same, the Expert Committee submitted their report with some changes. The Standing Committee of Corporation sanctioned the said draft rules with some changes vide resolution No.169 of 09.05.2012. A Consultant was also appointed to recommend the rates of taxation required to be adopted on the Capital Value. The Committee was specifically told to ensure that revenue neutrality is not compromised while fixing such rates. After approval to Tax Rates by the Standing Committee vide their resolution No.148 dated 09.05.2012, Final Capital Value based Property Tax bills were issued to tax payers in the month of December 2012. The levy of Capital Value based Property Tax is within the maximum limit prescribed in the Act as specified below- 1. No increase in existing tax for residential houses having carpet area up to 500

sq.ft. 2. Capping up to two times of the existing tax for residential houses having carpet

area of more than 500 sq.ft. 3. Capping up to three times of the existing tax for commercial properties. 4. The Capital Value will be revised only after every Five years, and the increase in

taxes cannot be more than 40% of the tax payable in the earlier year of such revision. However, the Tax Rates at that time will be decided by the Standing Committee / Corporation and the extent of increase in taxes could be kept to the minimum.

5. The flats/premises let outs on Leave & License will be treated as self occupied and the ceiling provided in the Act has to be applied on the presumptive tax of such flat as per self-occupied premises.

6. The telescopic concession in property tax for the re-developed buildings under various schemes has been continued under the new tax system also.

7. Capital Value of Buildings and Lands situated within the limits of Brihanmumbai Mahanagarpalika has been revised with effect from 1.4.2015 as per the provision of section 154(1C) of Mumbai Mahanagarpalika Act,1888 .

Manual I_ page no 16

As per the provision of section 140A of MMC Act,1888, the property tax levied w.e.f.1.4.2015 shall not ,in any case, exceed 40 per centum of the amount of the property tax payable in the year immediately preceding the year of revision as per section 154 (1C)of MMC Act,1888. But as per the provision of proviso inserted after 4th proviso of section 140A vide Maharashtra state ordinance no.13 of 2015, Amount of property tax leviable in respect of residential building or residential tenements, having area of 46.45 Sq. mt. (500 Sq ft.) or less , shall not exceed the amount of property tax levied and payable on 31st March,2015.

Standing Committee has passed the resolution bearing no. 1442 dated 19.3.2015 approving the rules for fixation of capital value w.e.f 1.4.2015.

Corporation has passed resolution bearing no. 1297 dated 20.3.2015 approving the proposal of Tax Rate for 2015-16 having 14.52% increase in 2014-15 revenue.

Rules for fixing Capital Value and tax rates for the period 2010-11 to 2014-15 and from 2015-16 are at Manual I page no. 17 to 37 and page no. 38 to 56 respectively. The said Rules and tax rates are available in 24 ward offices as well as on MCGM website namely http://portal.mcgm.gov.in.

Manual I_ page no 17

RULES FOR FIXING CAPITAL VALUE OF LANDS AND BUILDINGS

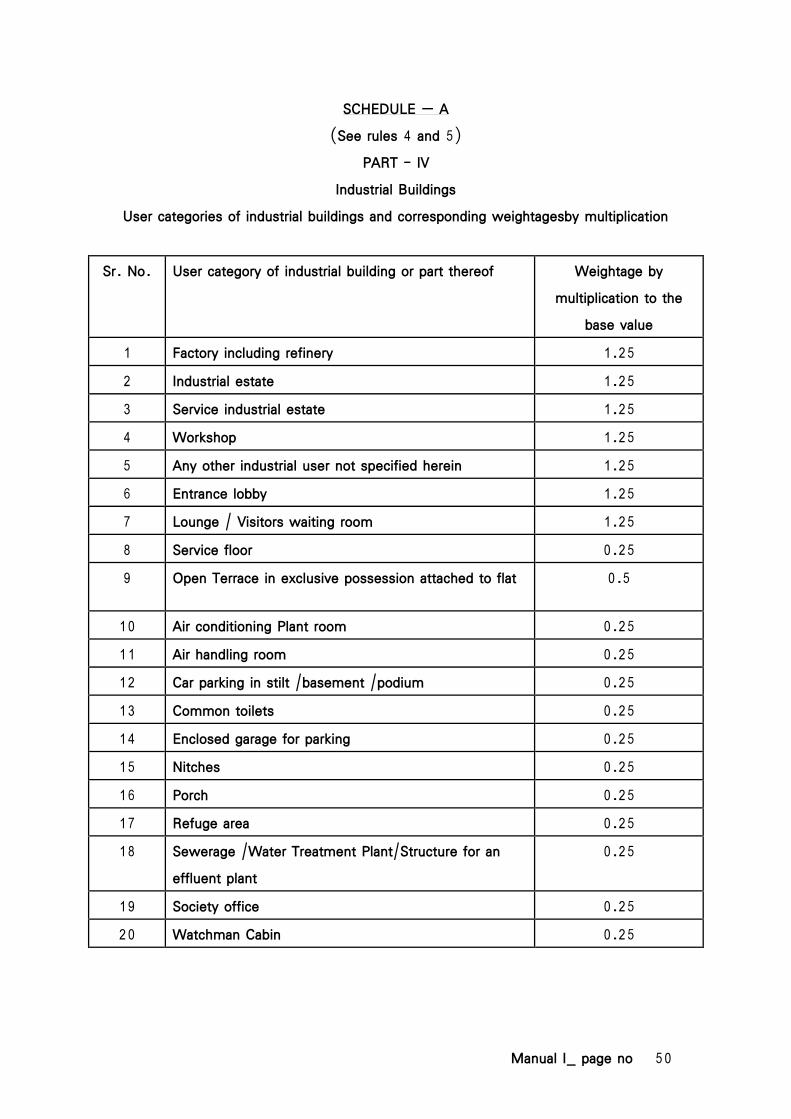

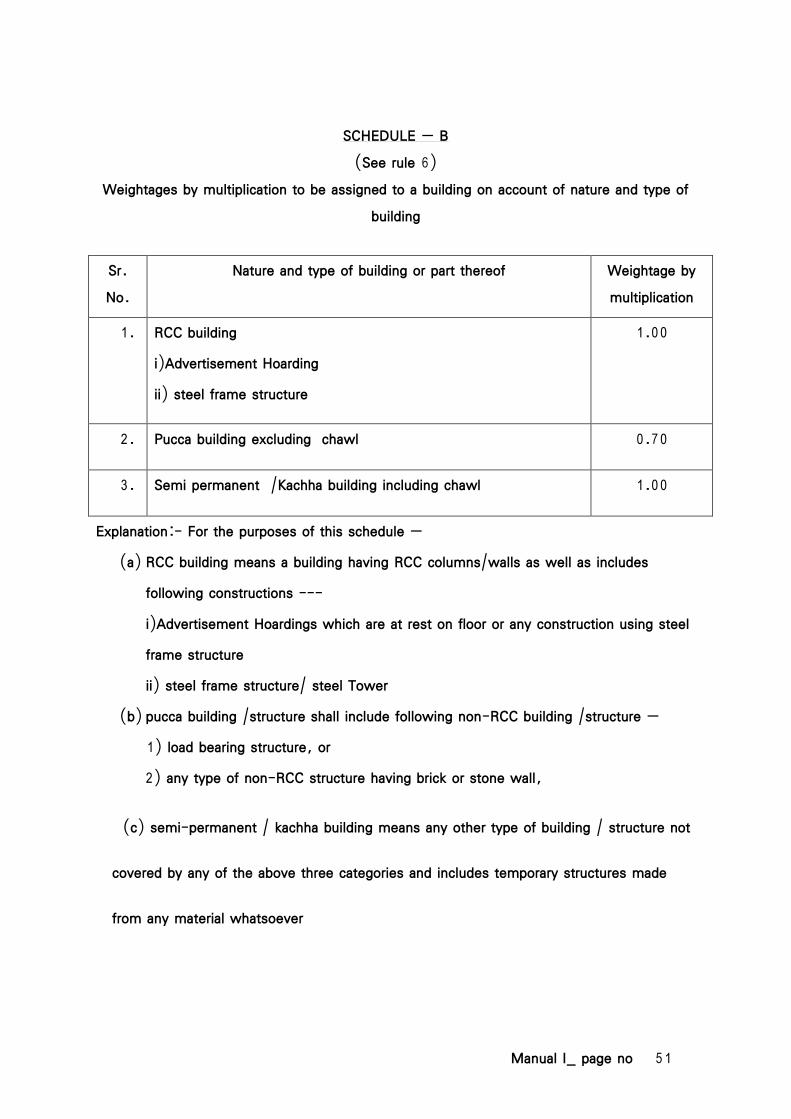

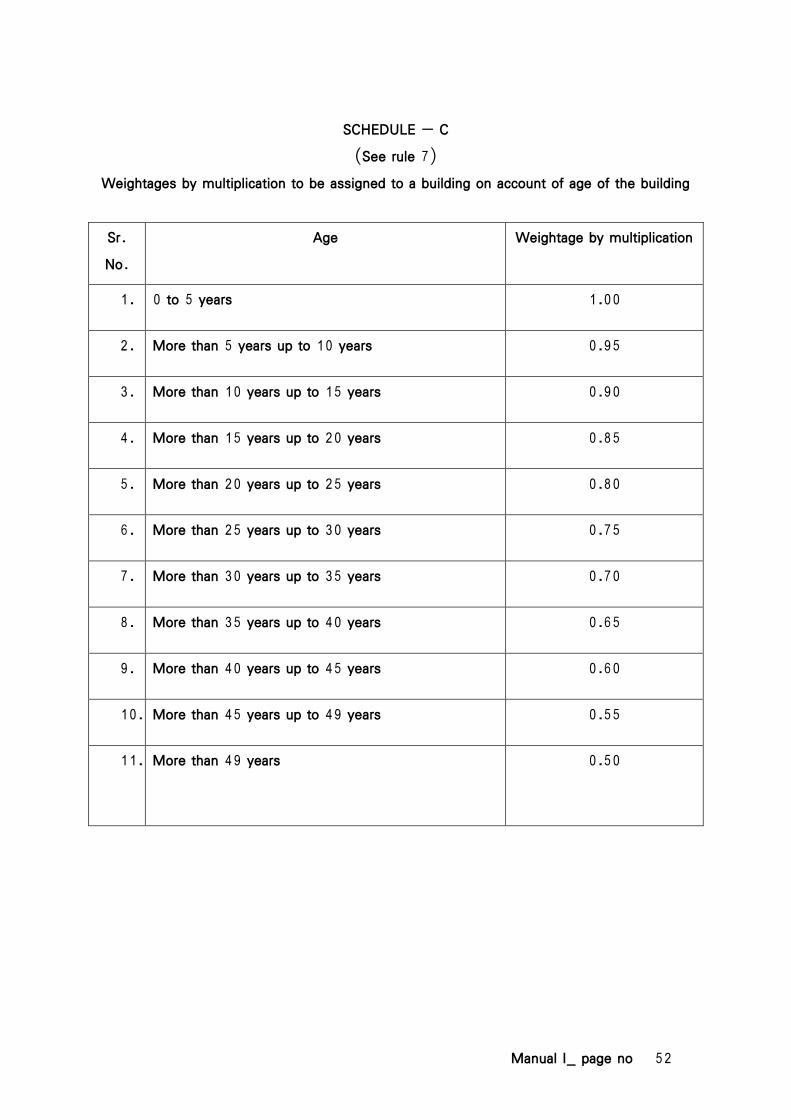

No.AC/NTC/1310/2011-12 dated 20.03.2012. In exercise of the powers conferred by clause (e) of sub-section (1A) and sub-section (1B) of section 154 of the Mumbai Municipal Corporation Act (Act No. Bom. III of 1888), and of all other powers enabling him in this behalf, the Commissioner, after having obtained the approval of the Standing Committee, as required under the said sub-section (1B), hereby makes the following rules to provide for the factors and categories of users of buildings or lands and the weightage by multiplication to be assigned to various such factors and categories for the purpose of fixing the capital value of buildings and lands in Brihan Mumbai, namely :- 1. Short title and commencement : – (1) These rules may be called the Factors and Categories of Users of Buildings or Lands (Assignment of Weightages by Multiplication) Fixation of Capital Value Rules, 2010. (2) They shall come into force forthwith. 2. Definitions - In these rules, unless the context otherwise requires:- (a) 'Act' means the Mumbai Municipal Corporation Act (Bom. III of 1888); (b) 'flat' means a separate part or portion of a building used or intended to be used for residence, or office, or show-room, or shop, or godown, or for carrying on any industry, or business, or profession, or vocation; (c) 'hoarding' includes boards used to display advertisements, erected on poles, on the ground or on a building; (d) 'land appurtenant to a building' means open spaces on all sides of a building required to be kept open in accordance with the relevant provisions of the Development Control Regulations for Greater Bombay, 1991 or any such Regulations, for the time being in force; (e) 'luxurious RCC building' includes a RCC building having a swimming pool, whether in use or not, and also any one or more of the following amenities or facilities, namely: – (i) gymnasium, (ii) club house, (iii) jogging track, (iv) health club, (v) private terrace as a part of each flat in a building; (f) 'multiplex' means a cinema house having more than one screen within a building;

Manual I_ page no 18

(g) 'open land' includes land not built upon or land being built upon, but does not include land appurtenant to a building; (h) 'Ready Reckoner' means the Stamp Duty Ready Reckoner, for the time being in force, referred to in sub-section (1A) of section 154 of the Act; (i) 'relative rate of base value' means the rate of open land, or rate of land plus residential building, office, shop, commercial or industrial building, as the case may be, as indicated in the Ready Reckoner; (j) 'schedule' means a schedule to these rules; (k) 'section' means a section of the Act; (l) 'star hotel' means hotel classified as a star hotel with a specific number of stars assigned thereto by the Ministry of Tourism, Government of India; (m) 'storage tank' includes a tank, whether underground or on any floor of a building, used for the storage of commodities, except the one used for storage of water; (n) 'tower' includes television tower, cable tower, telecom tower or any other such tower, transmission tower, cellular antenna, broadcasting antenna or the like, erected on the surface, or on top, or on any other open space, of a building; (o) words and expressions used in these rules and not defined,- (i) but defined in the Act, shall have the meanings respectively assigned to them in the Act, or (ii) where defined in the Maharashtra Regional and Town Planning Act,1966 or in the Development Control Regulations for Greater Mumbai, 1991, or any such Regulations, for the time being in force, shall have the meanings respectively assigned to them in the said Town Planning Act or in the Development Control Regulations, as the context may require. 3. Capital value of open land :- Save as otherwise provided in these rules, where, within the precincts of a building there is vacant land other than the land appurtenant to the building, such land shall be treated as open land and the capital value thereof shall be fixed accordingly, as provided for in rule 21. 4. User categories of open land and weightages by multiplication to be assigned thereto: - User categories of open land shall be as specified in column (2) of Part I of schedule ‘A’ and the weightages by multiplication to the base value, to be respectively assigned thereto for the purpose of fixing capital value, shall be as shown in column (3) of the said Part I of schedule ‘A’. 5. User categories of buildings or part thereof and weightages by multiplication to be assigned thereto:- User categories of buildings or part thereof shall be as specified in

Manual I_ page no 19

column (2) of each of Parts II, III and IV of schedule ‘A’ and the weightages by multiplication to the relative base value, to be respectively assigned thereto for the purpose of fixing capital value, shall be as shown in column (3) of each of the said Parts II, III and IV of schedule ‘A’. 6. The nature and type of building and the weightage by multiplication to be assigned thereto: - The nature and type of a building shall be as specified in column (2) of schedule ‘B’ and the weightages by multiplication to be assigned thereto for the purpose of fixing capital value, shall be as shown in column (3) of the said schedule ‘B’. 7. The weightage by multiplication to be assigned to a building on account of the age thereof: - The weightage by multiplication to be assigned to a building on account of age factor, for the purpose of fixing capital value, shall be according to the age of the building as shown in column (2) of schedule ‘C’ and the weightage by multiplication to be assigned thereto shall be as shown in column (3) of the said schedule ‘C’. 8. The weightage by multiplication on account of floor factor to be assigned to RCC building with lift: - Weightage by multiplication on account of floor factor to be assigned to a RCC building with lift, for the purpose of fixing capital value, shall be according to the number of floors as shown in column (2) of schedule ‘D’ and the weightage by multiplication to be assigned thereto shall be as shown in column (3) of the said schedule ‘D’. 9. Area of hoarding or tower for the purpose of fixing capital value: -Area of hoarding or tower for the purpose of fixing capital value thereof shall mean,- (a) in the case of a hoarding, the area of the square of the extremities of the poles on which the hoarding is erected plus the area of the hoarding; and (b) in the case of a tower, the area covered by the extremities of the foundation of the tower. 10. Built-up area of a flat or a building:- (1) The total built-up area of a flat shall be reckoned by including the area of the following items, namely:- (i) terrace in exclusive possession, (ii) mezzanine floor, (iii) loft (excluding loft in residential flat) or attic, (iv) dry balcony and (v) niches; and (2) The total built-up area of a building shall be reckoned by including the areas of the following items, namely:- (i) total area of the flats in the building computed in accordance with sub rule (1), (ii) basement, (iii) stilt, (iv)porch, (v) podium, (vi) service floor, (vii) refuge area, (viii) entrance lobby, (ix) lounge, (x) air- conditioning plant room, (xi) air handling room, (xii) the structure for an effluent treatment plant and (xiii) watchman cabin

Manual I_ page no 20

(3) The built-up area of any of the following items shall not be reckoned while computing the built-up area of a building or part thereof, namely:- (i) lift room above topmost storey, (ii) lift well, (iii) stair-case and passage thereto

including staircase room, (iv) chimney and elevated tank, (v) meter room, (vi) pump room, (vii) underground and overhead water tank, (viii) septic tank, (ix)flower-bed and (x) loft in residential flat.

(4) Where only the carpet area of a flat or building is available on the record of the Corporation and the total built-up area thereof, computed in the manner as aforesaid in sub-rule (1), or, as the case may be, sub-rule (2), is not available on such record, then the total built-up area of the flat or, as the case may be, of a building shall be arrived at in the following manner, namely :- Built-up area = 1.2 x carpet area as available on the record of the Corporation + the built-up area of the items specified in sub-rule(1),or, as the case may be, sub-rule (2), unless already reckoned in such carpet area. 11. Fixation of capital value of a flat or building or part thereof.- (1) While fixing the

capital value of a flat, the capital value of any one or more of the relevant items specified in sub-rule (1) of rule 10, as fixed in accordance with the provisions of rules 14,15, or sub-rule(1) of rule 16, as the case may be, shall be added to the capital value of the flat.

(2) While fixing the capital value of a building or part thereof, the capital value of any of the one or more of the relevant items specified in sub-rule (2) of rule 10 as fixed in accordance with the provisions of sub-rule (2) or, as the case may be, (3) of rule 16, shall be added to the capital value of the building or part thereof.

12. Fixation of capital value of a building where there are tenants:-The capital value of a building or part thereof which is occupied by a tenant shall be fixed at 75% of the capital value of such building or part thereof; fixed in accordance with the provisions of sub-rule (1), or, as the case may be, sub-rule(2) of rule 11. Explanation.- For the removal of doubts, it is hereby declared that the provisions of this rule shall not apply to a building or part thereof if, - (1) it is occupied by a licensee to whom it is given on leave and licence; (2) it is occupied by an office bearer or officer or an employee of the landlord.

Manual I_ page no 21

13.Fixation of capital value of religious buildings :- The capital value of a religious building which is a temple, math, gurudwara, mosque, takth, church, durgah, synagogue, or agiary or the like, and is used or intended to be used for the purpose of religious worship or offering prayers or performance of any religious rites or rituals by a person of, or belonging to, the relevant religion, creed, or sect, shall be fixed at the rate of base value applicable to a residential building as indicated in the Ready Reckoner; and by applying the relevant weightages by multiplication provided for in these rules. 14. Fixation of capital value of open terrace: - If an open terrace in exclusive possession is attached to a flat, the capital value of such terrace of a non-residential flat shall be fixed at 40% of the relative rate of base value of such flat, and of residential flat at 10% of the relative rate of base value of such flat; and by applying the relevant weightages by multiplication provided for in these rules. 15. Fixation of capital value of mezzanine floor, loft and attic floor,- (a) the capital value of mezzanine floor shall be fixed at 70% of the relative rate of base value of the flat beneath the mezzanine floor; and by applying the relevant weightages by multiplication provided for in these rules; (b) the capital value of loft or attic floor shall be fixed at 50% of the relative rate of base value of the flat beneath the loft, or as the case may be, the attic; and by applying the relevant weightages by multiplication provided for in these rules; Provided that, where the rate of base value applicable to the mezzanine floor, loft or attic floor having regard to its user is higher or, as the case may be, lower than the rate of base value applicable to the flat beneath such mezzanine floor, loft or attic floor, the capital value of such mezzanine floor, loft or attic floor shall be fixed at 70% or 50%, as the case may be, of such higher or lower rate of base value; and by applying the relevant weightages by multiplication provided for in these rules. 16. Fixation of capital value of certain other items which are part of a flat or a building or part thereto,- (1) The capital value of dry balcony and niches shall be fixed at 25% of the relative rate of base value of the flat, if any one of these items are part of the flat; and by applying the relevant weightages by multiplication provided for in these rules. (2) The capital value of any one or more of the following items, namely:- (i)porch, (ii) air-conditioning plant room, (iii) air-handling room, (iv) structure for an effluent plant, (v) watchman cabin and (vi) refuge area, shall be fixed at 25% of the relative rate of base value of the building or part thereof, if any one or more of these items are part of the building or part thereof; and by applying the relevant weightages by multiplication provided for in these rules.

Manual I_ page no 22

(3) The capital value of any one or more of the following items, namely:- (i) service floor, (ii) entrance lobby and (iii) lounge, shall be fixed at the relative rate of base value of the building or part thereof, if any of these items are part of the building or part thereof; and by applying the relevant weightages by multiplication provided for in these rules. 17. Fixation of capital value in respect of demolished building:- (1) Where a building is fully demolished, or has fully collapsed, the land beneath it shall be deemed to be open land and the capital value thereof shall be fixed accordingly, as provided for in rule 21. Explanation. –For the purpose of this rule, it is hereby declared that where a building is, or is being, demolished, or has collapsed, resulting in the land on which it stood or stands being rendered open land, or only walls or the like are standing but there is no structure as such which can be occupied, and on such demolition, or collapse, debris or any remains of the demolished or collapsed building are not yet removed, the land beneath such building shall be deemed to be open land. (2) Where only part of a building is demolished or has partly collapsed and the remaining part is yet occupied by occupiers, land beneath the portion of the building which is demolished or has collapsed shall be deemed to be open land and the portion of the structure which is occupied shall be treated as a building, for the purpose of fixing the capital value thereof. (3) Notwithstanding anything contained in sub rules (1) and (2), where a cessed building is, or is being, demolished, or has collapsed, the land beneath the building or portion of the building which is demolished or collapsed shall be deemed to be open land and the capital value thereof shall be fixed as open land and assigning thereto a weightage by multiplication of 0.30 of the base value of open land. 18. The capital value of storage tank .-The capital value of storage tank shall be fixed in the following manner, namely : – (1) storage tank above the ground level :- (a) land - at the rate of open land in the Ready Reckoner and weightage by multiplication to be assigned thereto shall be 1.25, (b) storage tank - capacity of storage tank in litres multiplied by the rate of Rs.40 per litre, with weightage by multiplication to be assigned thereto on account of age factor as in schedule ‘C’, (c) total capital value of a storage tank = total of items (a) and (b). (2) storage tank below the ground level :-

Manual I_ page no 23

(a) land - at the rate of open land in the Ready Reckoner and weightage by multiplication to be assigned thereto shall be 1.25, (b) storage tank - capacity of storage tank in litres multiplied by the rate of Rs.50 per litre, with weightage by multiplication to be assigned thereto on account of age factor as in schedule ‘C’, (c) Total capital value of a storage tank = total of items (a) and (b). 19. Capital value of amenities of luxurious RCC building not to be separately fixed again.- Where the capital value of a luxurious RCC building is fixed under these rules, then no capital value of the amenities specified in the definition of the expression ‘luxurious RCC building’ shall be separately fixed for the purpose of levy of property tax. 20. Valuation of open land capable of utilising more than 1 floor space index (F.S.I.) or transfer of development right (T.D.R.) –As the Ready Reckoner provides for the rate of base value of open land with 1 floor space index, open land which is capable of utilizing more than 1 floor space index or any transfer of development right shall be valued at an increased rate in proportion to the higher floor space index or transfer of development right proposed to be utilized and approved under the building plan submitted to the Corporation for approval. 21. Capital value of open land or building or part thereof.-Capital value of open land or building shall be fixed under the provisions of the Act and these rules in the following manner, namely:- (1) Capital value (CV) of open land – Rate of base value (BV) of a open land according to Ready Reckoner X weightage by multiplication as per user category (UC) (Part I of schedule ‘A’) X permissible or approved floor space index (FSI) X area of land (AL) . CV = BV x UC x FSI x AL (2) Capital value (CV) of a building – Relative rate of base value (BV) of a building according to Ready Reckoner X weightage by multiplication as per user category(UC) (Parts II, III, or as the case may be, IV of schedule ‘A’) X weightage by multiplication as per the nature and

Manual I_ page no 24

type of building (NTB) (schedule ‘B’) X weightage by multiplication on account of age of building (AF) (schedule ‘C’) X weightage by multiplication on account of floor factor (FF) for RCC building with lift (schedule ‘D’) X built-up area (BA) . CV = BV x UC x NTB x AF x FF x BA Examples: - Some examples based and worked out on the formulae as aforesaid are shown in the Appendix.

22. Non-application of Guidelines of Stamp Duty Valuation. - Notwithstanding anything contained in the 'Important Guidelines of Stamp Duty Valuation' as specified in the Ready Reckoner, the provisions made in these rules shall have primacy over those guidelines and none of those guidelines shall apply for fixing capital value under the Act and these rules.

Manual I_ page no 25

SCHEDULE – D

(See rule 8) Weightages by multiplication to be assigned to a building on account of floor factor for a RCC building with lift

Sr. No.

Floor Weightage by multiplication

(1) (2) (3) 1 Basement used for car-parking 0.70 2 Basement used for other than car parking 1.00 3 Lower ground floor 1.00 4 Upper ground floor 1.00 5 Ground floor 1.00 6 From 1st to 4th floor 1.00 7 From 5th to 10th floor 1.05 8 From 11th to 20th floor 1.10 9 From 21st to 30th floor 1.15 10 From 31st to 50th floor 1.20 11 From 51st to 75th floor 1.25 12 From 76th to 100th floor 1.30 13 Above 100th floor 1.35

Manual I_ page no 26

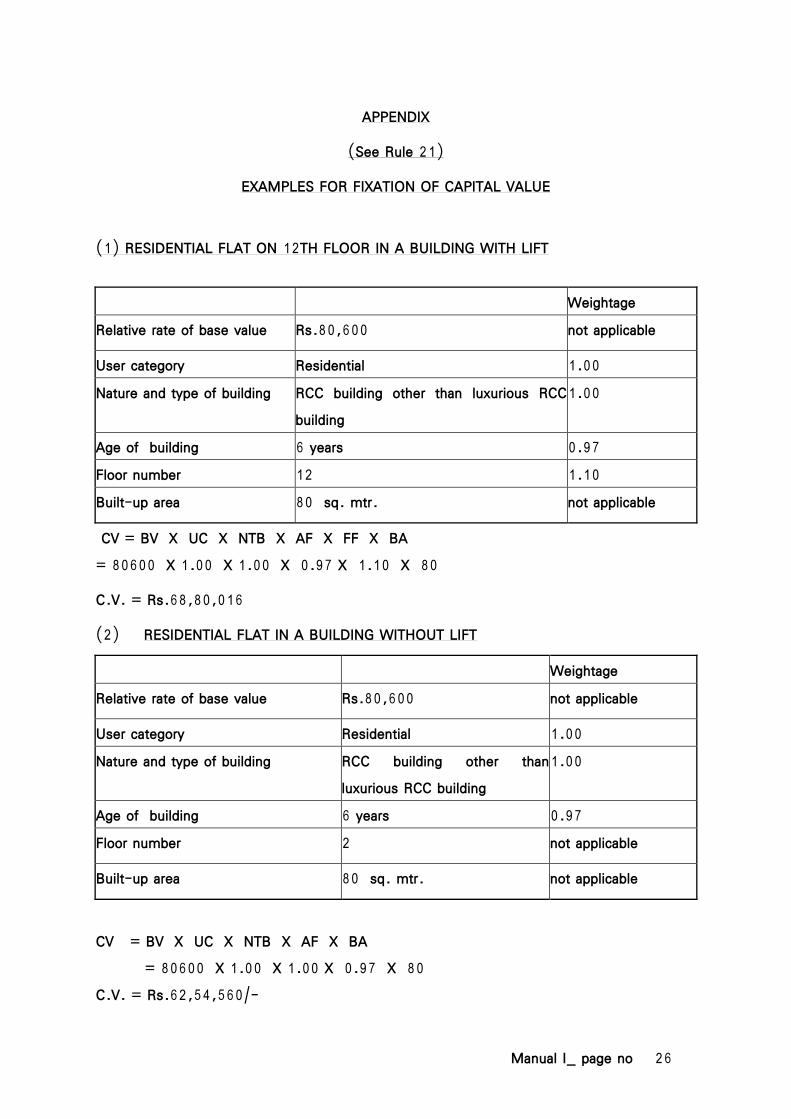

APPENDIX

(See Rule 21)

EXAMPLES FOR FIXATION OF CAPITAL VALUE

(1) RESIDENTIAL FLAT ON 12TH FLOOR IN A BUILDING WITH LIFT

Weightage Relative rate of base value Rs.80,600 not applicable

User category Residential 1.00 Nature and type of building RCC building other than luxurious RCC

building 1.00

Age of building 6 years 0.97 Floor number 12 1.10 Built-up area 80 sq. mtr. not applicable

CV = BV X UC X NTB X AF X FF X BA = 80600 X 1.00 X 1.00 X 0.97 X 1.10 X 80

C.V. = Rs.68,80,016

(2) RESIDENTIAL FLAT IN A BUILDING WITHOUT LIFT

Weightage Relative rate of base value Rs.80,600 not applicable

User category Residential 1.00 Nature and type of building RCC building other than

luxurious RCC building 1.00

Age of building 6 years 0.97 Floor number 2 not applicable

Built-up area 80 sq. mtr. not applicable

CV = BV X UC X NTB X AF X BA = 80600 X 1.00 X 1.00 X 0.97 X 80 C.V. = Rs.62,54,560/-

Manual I_ page no 27

(3) OFFICE IN A BUILDING WITHOUT LIFT HAVING A MEZZANINE FLOOR

Weightage Relative rate of base value Rs.108000 not applicable

User category Office 1.00 Nature and type of building RCC building other than

luxurious RCC building 1.00

Age of building 6 years 0.97 Floor number Ground floor not applicable

Built-up area 80 sq. mtr. not applicable

Built-up area of mezzanine floor 20 sq.mtr. 0.70

(1) CV of Flat = BV X UC X NTB X AF X BA = 108000 X 1.00 X 1.00 X 0.97 X 80 C.V. = Rs.83,80,800

(2) C.V. Mezzanine floor = BV x UC x NTB x AF x BA

=(108000 x0.70) x1.00 x 1.00 x 0.97 x 20

= 14,66,640

(3) Total Capital Value = (1) + (2)

= 82, 94, 400 + 14,66,640

= Rs. 98,47, 440

(4) RESIDENTIAL FLAT IN A BUILDING WITHOUT LIFT HAVING OPEN TERRACE IN EXCLUSIVE POSSESSION ATTACHED TO THE FLAT

Weightage Relative rate of base value Rs.80,600 not applicable

User category Residential 1.00 Nature and type of building RCC building other than luxurious RCC

building 1.00

Age of building 6 years 0.97 Floor number 2 not applicable

Manual I_ page no 28

Built-up area 80 sq. mtr. not applicable

Built-up area of open terrace 10 sq.mtr. 0.10

(1) CV of Flat = BV X UC X NTB X AF X BA = 80600 X 1.00 X 1.00 X 0.97 X 80 C.V. = Rs.62,54,560/-

(2) C.V. Open terrace = BV x UC x NTB x AF x BA

= (80600 x 0.10) x1.00 x 1.00 x 0.97 x 10

= 78,182/-

(3) Total Capital Value = (1) + (2)

= 62,54,560 + 78,182

= Rs. 63,32,742/-

(5) RESIDENTIAL FLAT ON 12TH FLOOR IN A BUILDING WITH LIFT

Weightage Relative rate of base value Rs.80,600 not applicable User category Residential 1.00 Nature and type of building RCC building other than luxurious

RCC building 1.00

Age of building 36 years 0.79 Floor number 12 1.10 Built-up area 80 sq. mtr. not applicable CV = BV X UC X NTB X AF X FF X BA = 80600 X 1.00 X 1.00 X 0.79 X 1.10 X 80

C.V. = Rs.56,03,312

(6) RESIDENTIAL FLAT IN A BUILDING WITHOUT LIFT

Weightage Relative rate of base value Rs.80,600 not applicable

User category Residential 1.00

Manual I_ page no 29

Nature and type of building RCC building other than luxurious RCC building

1.00

Age of building 36 years 0.79 Floor number 2 not applicable

Built-up area 80 sq. mtr. not applicable

CV = BV X UC X NTB X AF X BA = 80600 X 1.00 X 1.00 X 0.79 X 80 C.V. = Rs.50,93,920

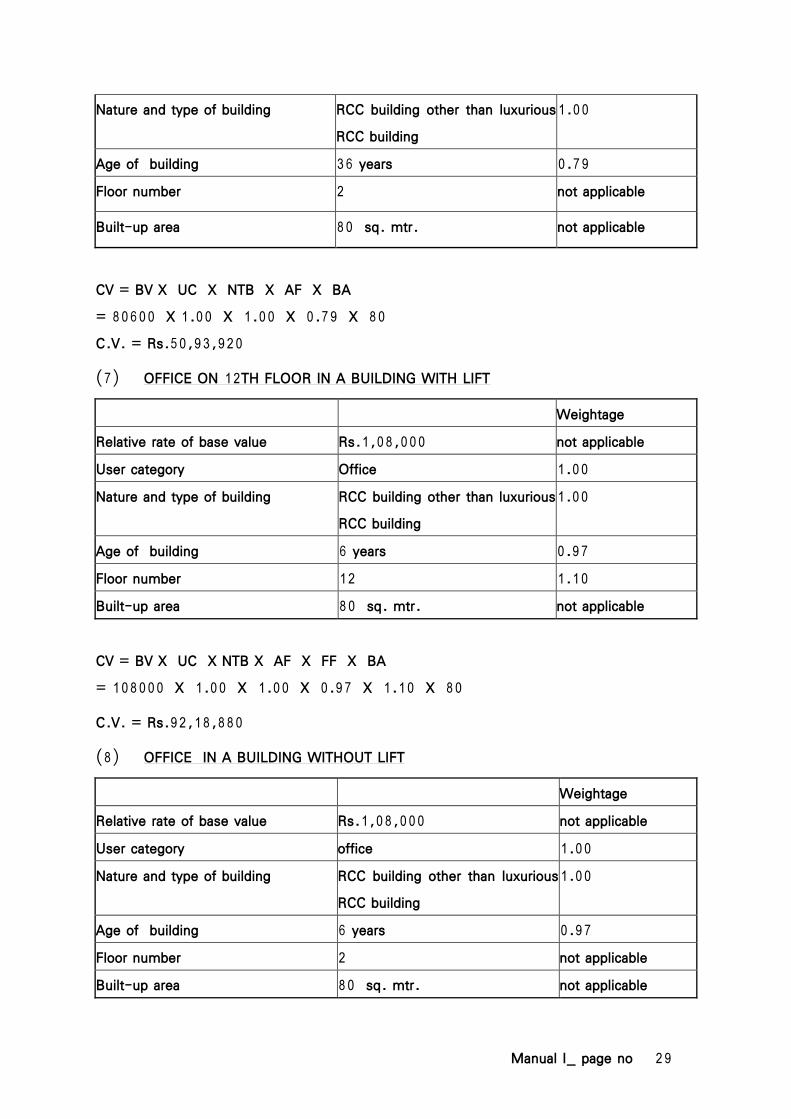

(7) OFFICE ON 12TH FLOOR IN A BUILDING WITH LIFT

Weightage Relative rate of base value Rs.1,08,000 not applicable User category Office 1.00 Nature and type of building RCC building other than luxurious

RCC building 1.00

Age of building 6 years 0.97 Floor number 12 1.10 Built-up area 80 sq. mtr. not applicable CV = BV X UC X NTB X AF X FF X BA = 108000 X 1.00 X 1.00 X 0.97 X 1.10 X 80

C.V. = Rs.92,18,880

(8) OFFICE IN A BUILDING WITHOUT LIFT

Weightage Relative rate of base value Rs.1,08,000 not applicable User category office 1.00 Nature and type of building RCC building other than luxurious

RCC building 1.00

Age of building 6 years 0.97 Floor number 2 not applicable Built-up area 80 sq. mtr. not applicable

Manual I_ page no 30

CV = BV X UC X NTB X AF X BA = 108000 X 1.00 X 1.00 X 0.97 X 80 C.V. = Rs.83,80,800 (9) OFFICE IN A BUILDING ON 12TH FLOOR WITH LIFT

Weightage Relative rate of base value Rs.1,08,000 not applicable

User category Office 1.00 Nature and type of building RCC building other than luxurious

RCC building 1.00

Age of building 36 years 0.79 Floor number 12 1.10 Built-up area 80 sq. mtr. not applicable

CV = BV X UC X NTB X AF X FF X BA = 108000 X 1.00 X 1.00 X 0.79 X 1.10 X 80

C.V. = Rs.75,08,160

(10) OFFICE IN A BUILDING WITHOUT LIFT

Weightage Relative rate of base value Rs.1,08,000 not applicable

User category office 1.00 Nature and type of building RCC building other than luxurious

RCC building 1.00

Age of building 36 years 0.79 Floor number 2 not applicable Built-up area 80 sq. mtr. not applicable

C.V. = BV X UC X NTB X AF X BA = 108000 X 1.00 X 1.00 X 0.79 X 80 C.V. = Rs.68,25,600/-

Manual I_ page no 31

(11) OPEN LAND IN ISLAND CITY

Weightage Rate of base value Rs.36,400 not applicable

User Category Residential 1.00 Nature and Type of Building not applicable not applicable Age of Building not applicable not applicable F.S.I. Factor 1.33 1.33 Land Area 80 sq. mtr. not applicable

CV = BV X UC X FSI X LA = 36400 X 1.00 X 1.33 X 80

C.V. = Rs.38,72,960

(12) OPEN LAND WHERE RESIDENTIAL BUILDING PLAN WITH HIGHER F.S.I. HAS BEEN APPROVED

Weightage Rate of base value Rs.36,400 not applicable

User Category Open Land (Resi) 1.00 Nature and Type of Building not applicable not applicable Age of Building not applicable not applicable F.S.I. Factor 2.50 2.50 Land Area 80 sq. mtr. not applicable

CV = BV X UC X FSI X LA = 36400 X 1.00 X 2.50 X 80 C.V. = Rs.72,80,000

Manual I_ page no 32

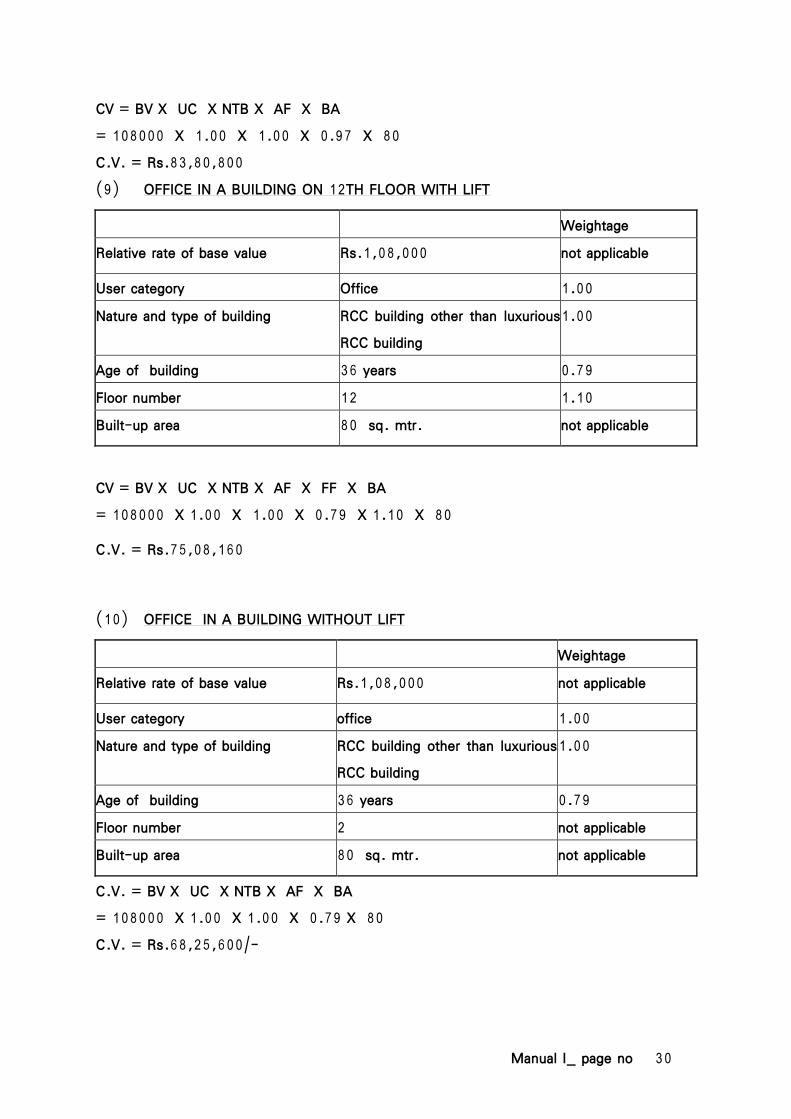

(13) OPEN LAND IN SUBURBAN AREA

Weightage Rate of base value Rs.33,200/- not applicable

User Category Residential 1.00 Nature and Type of Building not applicable not applicable Age of Building not applicable not applicable F.S.I. Factor 1.00 1.00 Land Area 80 sq. mtr. not applicable

CV = BV X UC X FSI X LA = 33200 X 1.00 X 1.00 X 80

C.V. = Rs.26,56,000

Manual I_ page no 33

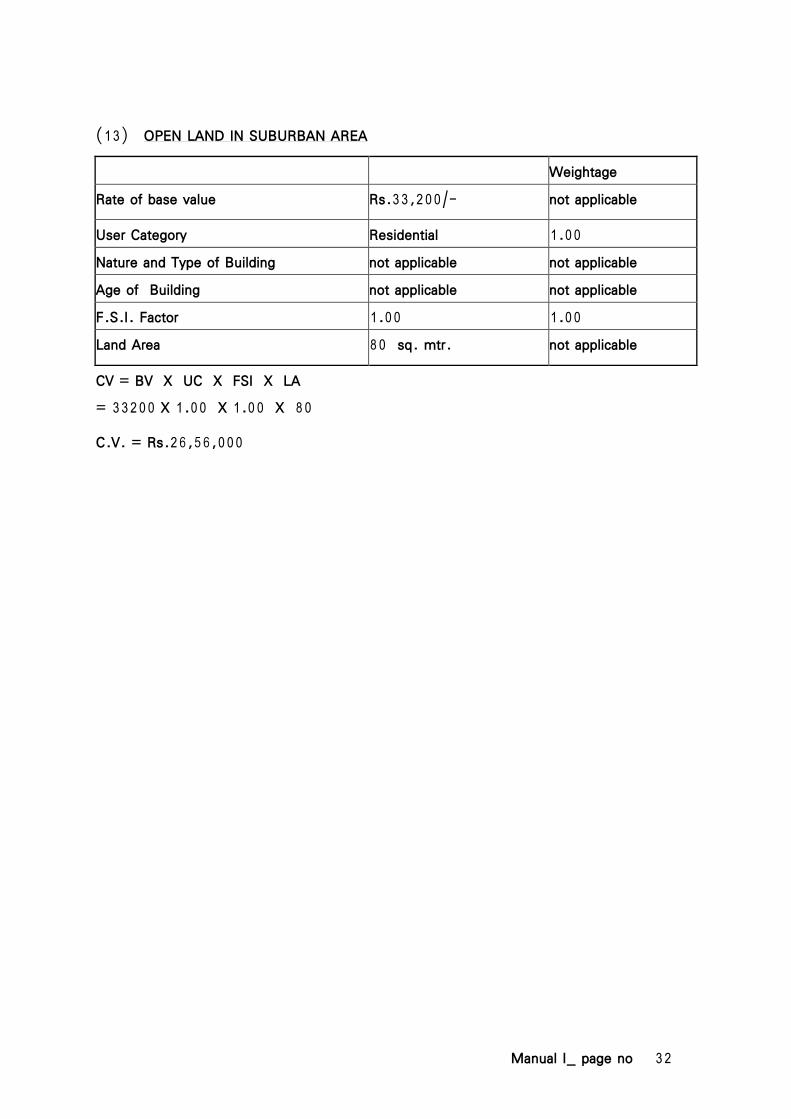

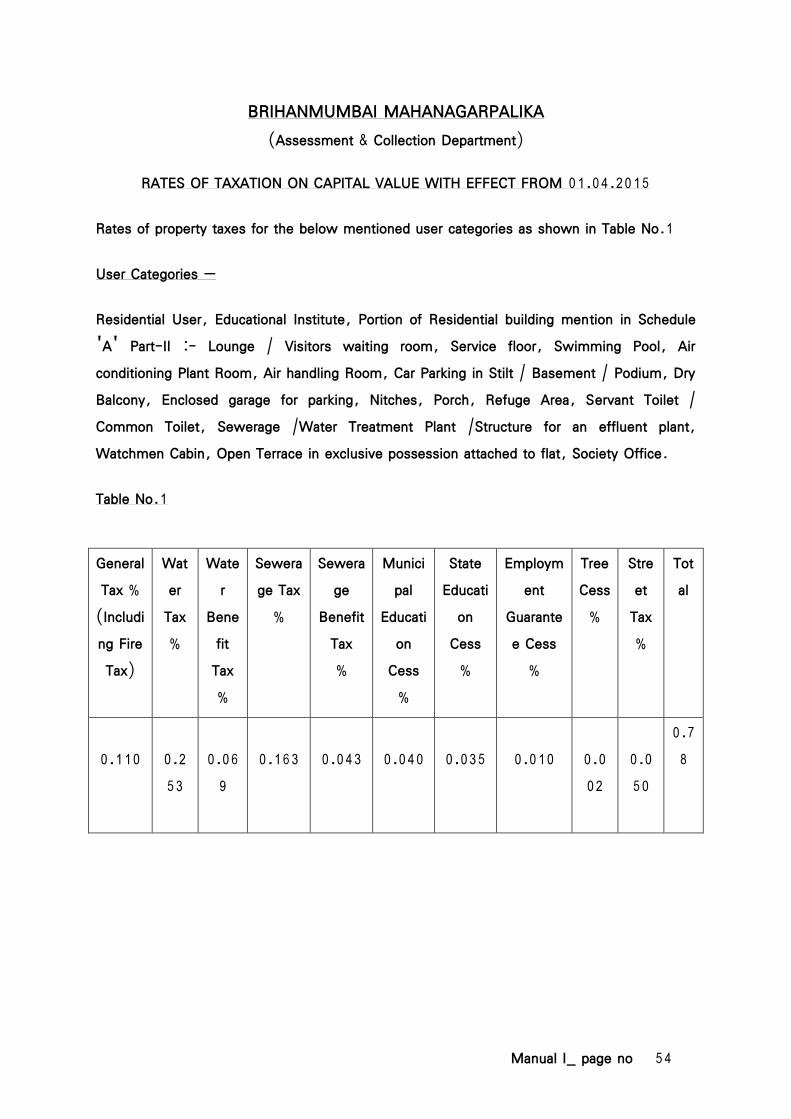

BRIHANMUMBAI MAHANAGARPALIKA (Assessment & Collection Department)

RATES OF TAXATION ON CAPITAL VALUE WITH EFFECT FROM 01.04.2010

Rates of property taxes for the below mentioned user categories as shown in Table No.1 User Categories – Residential Buildings- Bunglow, Car park in stilt or basement, or podium, Club House and any other amenity in Co-Operative Housing Society used by its members, Duplex flat/ Apartment, Enclosed Garage, Pent House, Room, or flat , or apartment, or tenement and the like, Row House, Society Office, Swimming Pool, Educational Institutions, Salt Pan, Quarry, Passenger Terminal at Airport, Hangers and Workshop at Airport. Table No.1 General Tax

Fire Tax

Street Tax

Municipal Education Cess

Water Tax

Water Benefit Tax

Sewerage Tax

Sewerage Benefit Tax

Tree Cess

State Education Cess

Employment Guarantee Cess

0.110%

0.0137%

0.051%

0.041%

0.253%

0.069%

0.163%

0.043%

0.002%

0.033%

0.010%

Manual I_ page no 34

BRIHANMUMBAI MAHANAGARPALIKA (Assessment & Collection Department)

RATES OF TAXATION ON CAPITAL VALUE WITH EFFECT FROM 01.04.2010

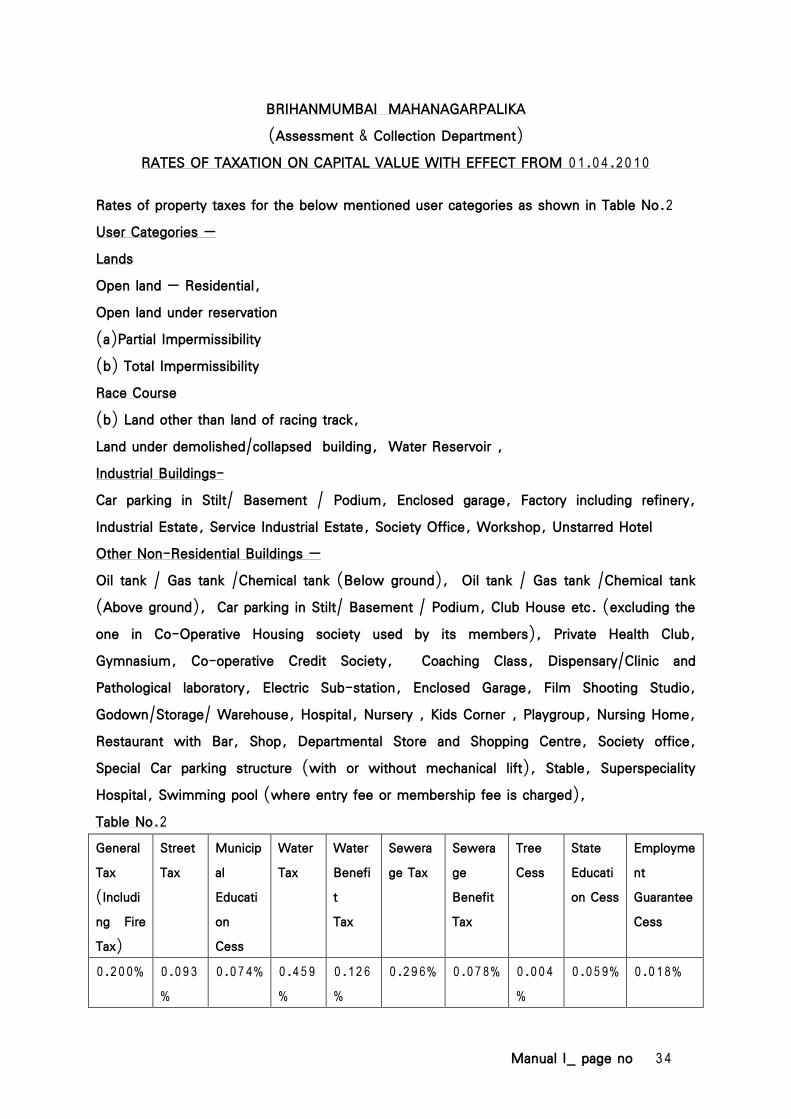

Rates of property taxes for the below mentioned user categories as shown in Table No.2 User Categories – Lands Open land – Residential, Open land under reservation (a)Partial Impermissibility (b) Total Impermissibility Race Course (b) Land other than land of racing track, Land under demolished/collapsed building, Water Reservoir , Industrial Buildings- Car parking in Stilt/ Basement / Podium, Enclosed garage, Factory including refinery, Industrial Estate, Service Industrial Estate, Society Office, Workshop, Unstarred Hotel Other Non-Residential Buildings – Oil tank / Gas tank /Chemical tank (Below ground), Oil tank / Gas tank /Chemical tank (Above ground), Car parking in Stilt/ Basement / Podium, Club House etc. (excluding the one in Co-Operative Housing society used by its members), Private Health Club, Gymnasium, Co-operative Credit Society, Coaching Class, Dispensary/Clinic and Pathological laboratory, Electric Sub-station, Enclosed Garage, Film Shooting Studio, Godown/Storage/ Warehouse, Hospital, Nursery , Kids Corner , Playgroup, Nursing Home, Restaurant with Bar, Shop, Departmental Store and Shopping Centre, Society office, Special Car parking structure (with or without mechanical lift), Stable, Superspeciality Hospital, Swimming pool (where entry fee or membership fee is charged), Table No.2 General Tax (Including Fire Tax)

Street Tax

Municipal Education Cess

Water Tax

Water Benefit Tax

Sewerage Tax

Sewerage Benefit Tax

Tree Cess

State Education Cess

Employment Guarantee Cess

0.200% 0.093%

0.074% 0.459%

0.126%

0.296% 0.078% 0.004%

0.059% 0.018%

Manual I_ page no 35

BRIHANMUMBAI MAHANAGARPALIKA (Assessment & Collection Department)

RATES OF TAXATION ON CAPITAL VALUE WITH EFFECT FROM 01.04.2010

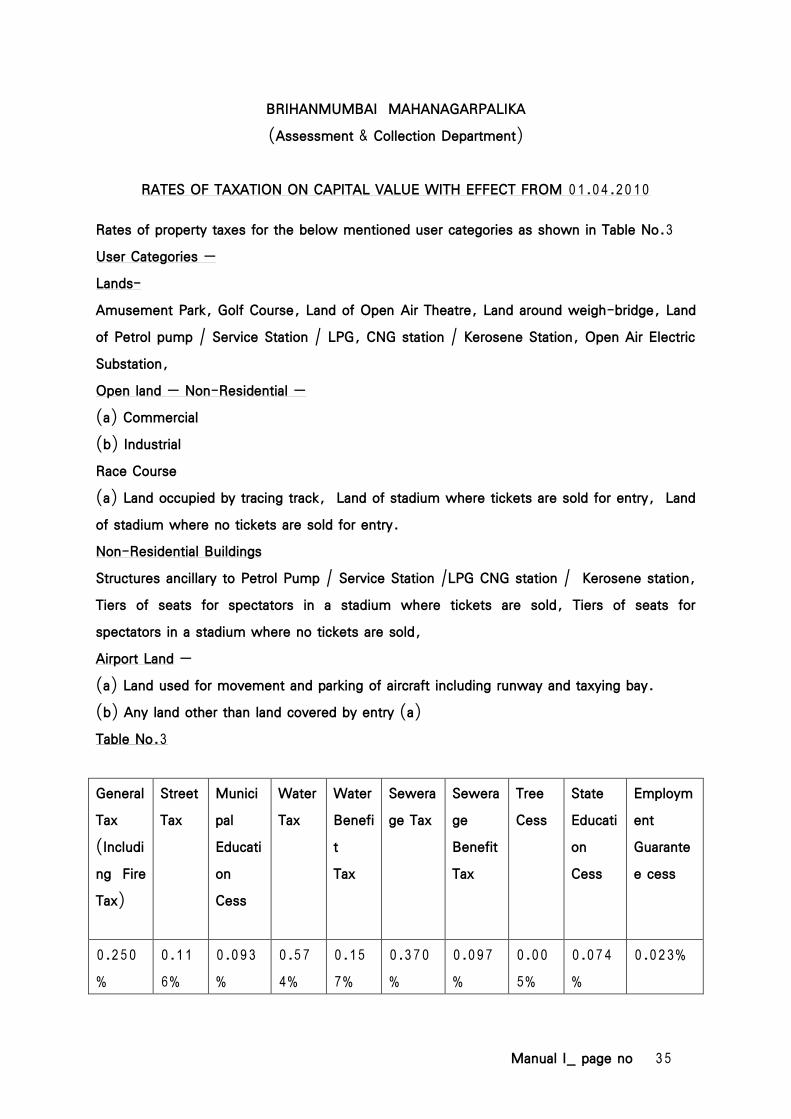

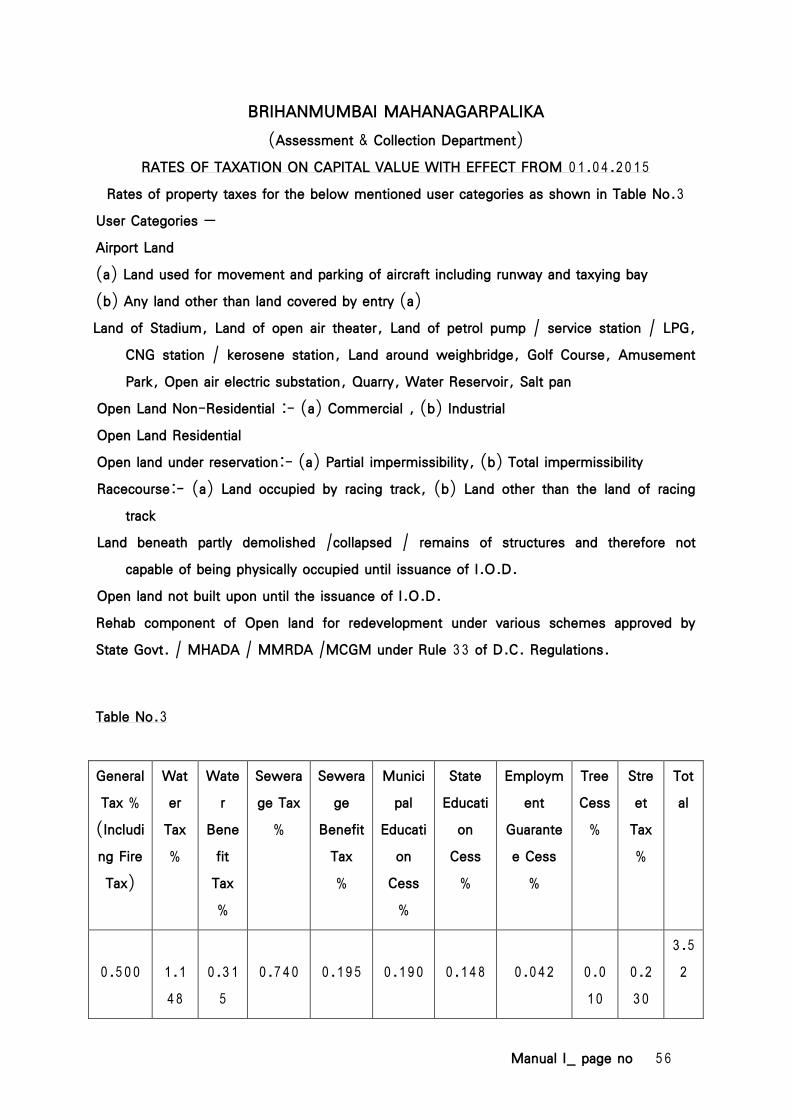

Rates of property taxes for the below mentioned user categories as shown in Table No.3 User Categories – Lands- Amusement Park, Golf Course, Land of Open Air Theatre, Land around weigh-bridge, Land of Petrol pump / Service Station / LPG, CNG station / Kerosene Station, Open Air Electric Substation, Open land – Non-Residential – (a) Commercial (b) Industrial Race Course (a) Land occupied by tracing track, Land of stadium where tickets are sold for entry, Land of stadium where no tickets are sold for entry. Non-Residential Buildings Structures ancillary to Petrol Pump / Service Station /LPG CNG station / Kerosene station, Tiers of seats for spectators in a stadium where tickets are sold, Tiers of seats for spectators in a stadium where no tickets are sold, Airport Land – (a) Land used for movement and parking of aircraft including runway and taxying bay. (b) Any land other than land covered by entry (a) Table No.3 General Tax (Including Fire Tax)

Street Tax

Municipal Education Cess

Water Tax

Water Benefit Tax

Sewerage Tax

Sewerage Benefit Tax

Tree Cess

State Education Cess

Employment Guarantee cess

0.250%

0.116%

0.093%

0.574%

0.157%

0.370%

0.097%

0.005%

0.074%

0.023%

Manual I_ page no 36

BRIHANMUMBAI MAHANAGARPALIKA (Assessment & Collection Department)

RATES OF TAXATION ON CAPITAL VALUE WITH EFFECT FROM 01.04.2010

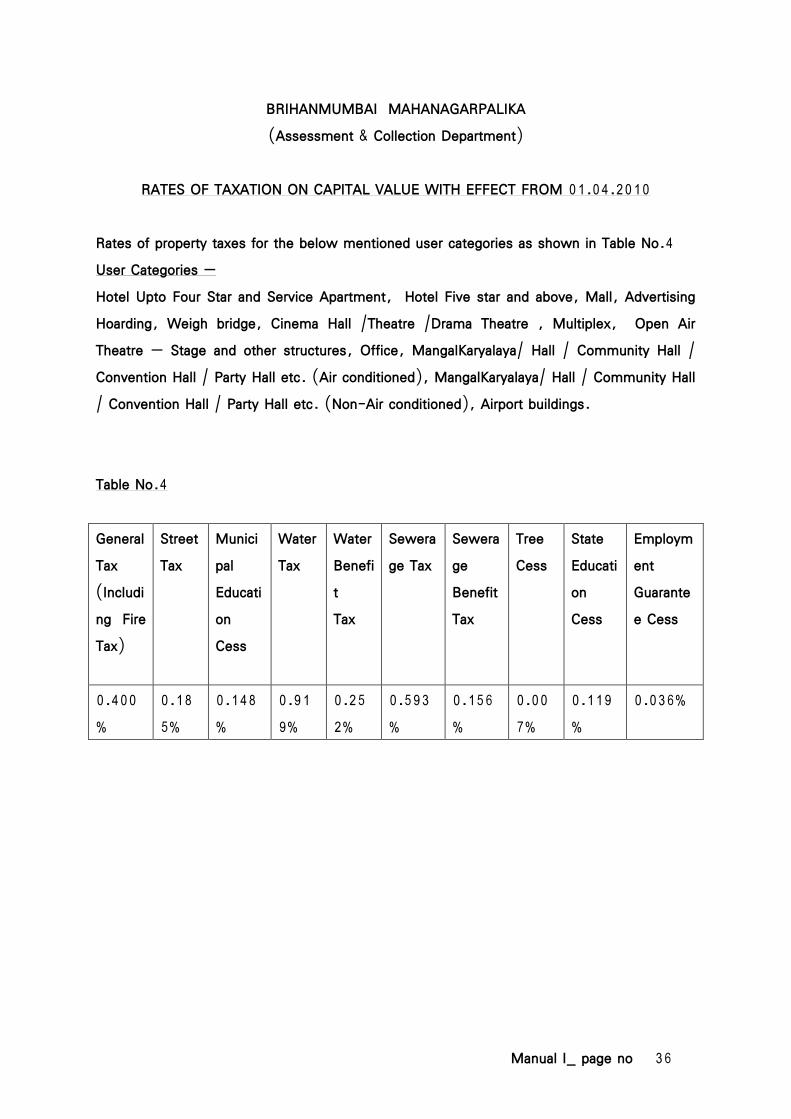

Rates of property taxes for the below mentioned user categories as shown in Table No.4 User Categories – Hotel Upto Four Star and Service Apartment, Hotel Five star and above, Mall, Advertising Hoarding, Weigh bridge, Cinema Hall /Theatre /Drama Theatre , Multiplex, Open Air Theatre – Stage and other structures, Office, MangalKaryalaya/ Hall / Community Hall / Convention Hall / Party Hall etc. (Air conditioned), MangalKaryalaya/ Hall / Community Hall / Convention Hall / Party Hall etc. (Non-Air conditioned), Airport buildings. Table No.4 General Tax (Including Fire Tax)

Street Tax

Municipal Education Cess

Water Tax

Water Benefit Tax

Sewerage Tax

Sewerage Benefit Tax

Tree Cess

State Education Cess

Employment Guarantee Cess

0.400%

0.185%

0.148%

0.919%

0.252%

0.593%

0.156%

0.007%

0.119%

0.036%

Manual I_ page no 37

BRIHANMUMBAI MAHANAGARPALIKA (Assessment & Collection Department)

RATES OF TAXATION ON CAPITAL VALUE WITH EFFECT FROM 01.04.2010

Rates of property taxes for the below mentioned user categories as shown in Table No.5 User Categories – Bank, Automatic Teller Machine Center and Money Changing Center, Tower, Asset Management company and trustee company of Mutual Fund, Non-Banking Financial Institution, Commodity Exchange, Life and non-life insurance corporation or company, Security Exchange Board of India , Stock Exchange. Table No.5 General Tax (Including Fire Tax)

Street Tax

Municipal Education Cess

Water Tax

Water Benefit Tax

Sewerage Tax

Sewerage Benefit Tax

Tree Cess

State Education Cess

Employment Guarantee Cess

0.800%

0.370%

0.296%

1.837%

0.504%

1.185%

0.311%

0.015%

0.237%

0.073%

Manual I_ page no 38

CORPORATION OF GREATER MUMBAI

RULES FOR FIXING CAPITAL VALUE OF LANDS AND BUILDINGS W. E. F. 1-4-2015

No.AC/NTC/1147/2014-15 . In exercise of the powers conferred by clause (e) of sub-section (1A), sub-section (1B) and sub-section (1C) of section 154 of the Mumbai Municipal Corporation Act (Act No. Bom. III of 1888), and of all other powers enabling him in this behalf, the Commissioner, after having obtained the approval of the Standing Committee, as required under the said sub-section (1B), hereby makes the following rules to provide for the factors and categories of users of lands and buildings and the weightage by multiplication to be assigned to various such factors and categories for the purpose of fixing the capital value of lands and buildings in Brihan Mumbai , namely :-

1. Short title and commencement : – (1) These rules may be called the Factors and Categories of Users of Buildings or Lands (Assignment of Weightages by Multiplication) Fixation of Capital Value Rules, 2015.

(2) They shall come into force from 1st April 2015.

2.Definitions - In these rules, unless the context otherwise requires :-

(a) 'Act' means the Mumbai Municipal Corporation Act (Bom. III of 1888);

(b) 'flat' means a separate part or portion of a building used or intended to be used for residence, or office, or show-room, or shop, or godown, or for carrying on any industry, or business, or profession, or vocation;

(c) 'hoarding' includes boards used to display advertisements, erected on poles, on the ground or on a building;

(d) 'land appurtenant to a building' means open spaces on all sides of a building required to be kept open in accordance with the relevant provisions of the Development Control Regulations for Greater Bombay, 1991 or any such Regulations, for the time being in force;

(e) 'deleted'

(f) 'multiplex' means a cinema house having more than one screen within a building;

Manual I_ page no 39

(g) 'open land' includes land not built upon or land being built upon, but does not include land appurtenant to a building;

(h) 'Ready Reckoner' means the Stamp Duty Ready Reckoner, for the time being in force, referred to in sub-section (1A) of section 154 of the Act;

(i) 'relative rate of base value' means the rate of open land, or rate of land plus residential building, office, shop, commercial or industrial building, as the case may be, as indicated in the Ready Reckoner;

(j) 'schedule' means a schedule to these rules;

(k) 'section' means a section of the Act;

(l)'star hotel' means hotel classified as a star hotel with a specific number of stars assigned thereto by the Ministry of Tourism, Government of India

(m) 'storage tank' includes a tank, whether underground or on any floor of a building, used for the storage of commodities, except the one used for storage of water;

(n) 'tower' includes television tower, cable tower, telecom tower or any other such tower, transmission tower, cellular antenna, broadcasting antenna or the like, erected on the surface, or on top, or on any other open space, of a building;

(o) words and expressions used in these rules and not defined,-

(i) but defined in the Act, shall have the meanings respectively assigned to them in the Act, or

(ii) where defined in the Maharashtra Regional and Town Planning Act,1966 or in the Development Control Regulations for Greater Mumbai, 1991, or any such Regulations, for the time being in force, shall have the meanings respectively assigned to them in the said Town Planning Act or in the Development Control Regulations, as the context may require.

3. Capital value of open land :- Save as otherwise provided in these rules, where, within the precincts of a building there is vacant land other than the land appurtenant to the

Manual I_ page no 40

building, such land shall be treated as open land and the capital value thereof shall be fixed accordingly, as provided for in rule 21.

4. User categories of open land and weightages by multiplication to be assigned thereto: - User categories of open land shall be as specified in column (2) of Part I of schedule ‘A’ and the weightages by multiplication to the base value, to be respectively assigned thereto for the purpose of fixing capital value, shall be as shown in column (3) of the said Part I of schedule ‘A’.

5. User categories of buildings or part thereof and weightages by multiplication to be assigned thereto:- User categories of buildings or part thereof shall be as specified in column (2) of each of Parts II, III and IV of schedule ‘A’ and the weightages by multiplication to the relative base value, to be respectively assigned thereto for the purpose of fixing capital value, shall be as shown in column (3) of each of the said Parts II, III and IV of schedule ‘A’.

6. The nature and type of building and the weightage by multiplication to be assigned thereto: - The nature and type of a building shall be as specified in column (2) of schedule ‘B’ and the weightages by multiplication to be assigned thereto for the purpose of fixing capital value, shall be as shown in column (3) of the said schedule ‘B’.

7. The weightage by multiplication to be assigned to a building on account of the age thereof: - The weightage by multiplication to be assigned to a building on account of age factor, for the purpose of fixing capital value, shall be according to the age of the building as shown in column (2) of schedule ‘C’ and the weightage by multiplication to be assigned thereto shall be as shown in column (3) of the said schedule ‘C’.

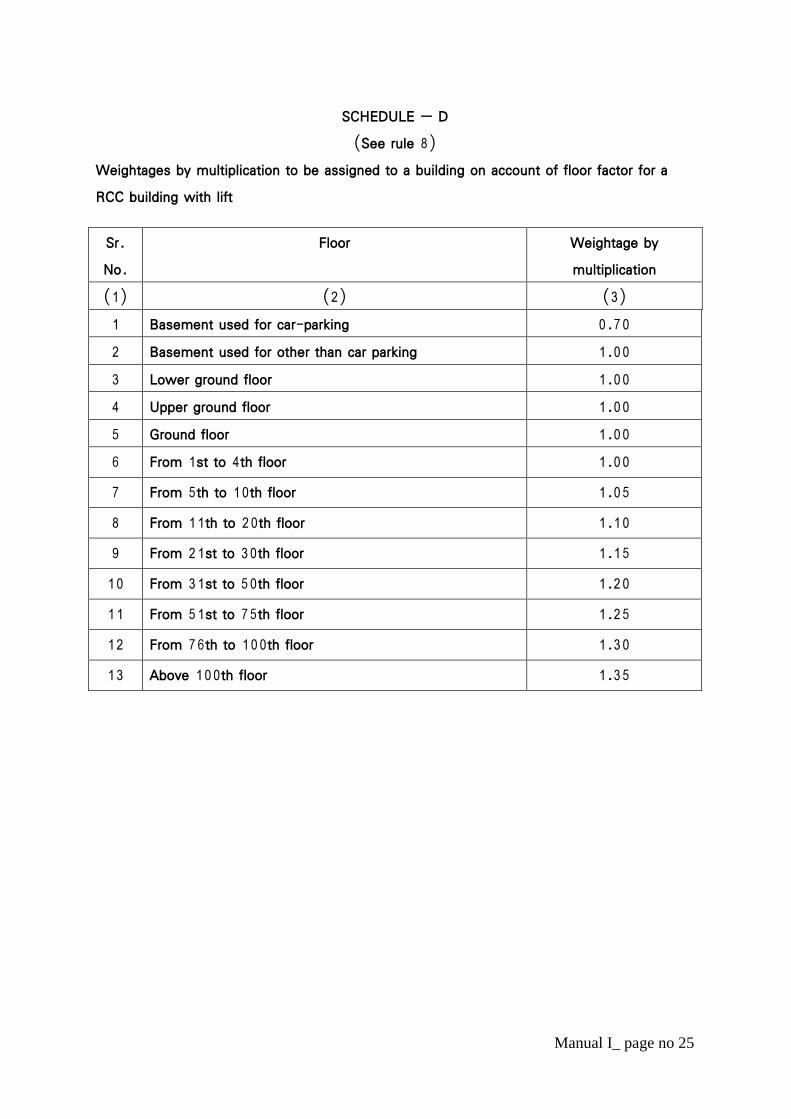

8. The weightage by multiplication on account of floor factor to be assigned to RCC building with lift: - Weightage by multiplication on account of floor factor to be assigned to a RCC building with lift, for the purpose of fixing capital value, shall be according to the number of floors as shown in column (2) of schedule ‘D’ and the weightage by multiplication to be assigned thereto shall be as shown in column (3) of the said schedule ‘D’.

9. Area of hoarding or tower for the purpose of fixing capital value: -Area of hoarding or tower for the purpose of fixing capital value thereof shall mean,-

Manual I_ page no 41

(a) in the case of a hoarding, the area of the square of the extremities of the poles on which the hoarding is erected plus the area of the hoarding; and

(b) in the case of a tower, the area covered by the extremities of the foundation of the tower.

10. Carpet Area area of a flat or a building:-

(1) The total carpet area of a flat shall be reckoned by including the area of the following items, namely:- (i) terrace in exclusive possession, (ii) mezzanine floor, (iii) loft (excluding loft in residential flat) or attic, (iv) dry balcony and (v) niches; and

(2) The total carpet area area of a building shall be reckoned by including the areas of the following items, namely:- (i) total area of the flats in the building computed in accordance with sub rule (1), (ii) basement, (iii) stilt, (iv)porch, (v) podium, (vi) service floor, (vii) refuge area, (viii) entrance lobby, (ix) lounge, (x) air- conditioning plant room, (xi) air handling room, (xii) the structure for an effluent treatment plant room and (xiii) watchman cabin (xix)sewerage treatment plant room (xv) water treatment plant room

(3) The carpet area of any of the following items shall not be reckoned while computing the carpet area of a building or part thereof, namely:-

(i) lift room above topmost storey, (ii) lift well, (iii) stair-case and passage thereto including staircase room, (iv) chimney and elevated tank, (v) meter room, (vi) pump room, (vii) underground and overhead water tank, (viii) septic tank, (ix)flower-bed and (x) loft in residential flat, (xi) entrance lobby of residential building

(4) ‘deleted’

11. Fixation of capital value of a flat or building or part thereof.-

(1) While fixing the capital value of a flat, the capital value of any one or more of the relevant items specified in sub-rule (1) of rule 10, as fixed in accordance with the provisions of rules 14,15, or sub-rule(1) of rule 16, as the case may be, shall be added to the capital value of the flat.

Manual I_ page no 42

(2) While fixing the capital value of a building or part thereof, the capital value of any of the one or more of the relevant items specified in sub-rule (2) of rule 10 as fixed in accordance with the provisions of sub-rule (2) or, as the case may be, (3) of rule 16, shall be added to the capital value of the building or part thereof.

7. 'deleted'

13.Fixation of capital value of religious buildings :- The capital value of a religious building which is a temple, math, gurudwara, mosque, takth, church, durgah, synagogue, or agiary or the like, and is used or intended to be used for the purpose of religious worship or offering prayers or performance of any religious rites or rituals by a person of, or belonging to, the relevant religion, creed, or sect, shall be fixed at the rate of base value applicable to a residential building as indicated in the Ready Reckoner; and by applying the relevant weightages by multiplication provided for in these rules.

14. Fixation of capital value of open terrace: - If an open terrace in exclusive possession is attached to a flat, the capital value of such terrace of a non-residential flat shall be fixed at 50% of the relative rate of base value of such flat, and of residential flat at 20% of the relative rate of base value of such flat; and by applying the relevant weightages by multiplication provided for in these rules.

15. Fixation of capital value of mezzanine floor, loft and attic floor,-

(a) the capital value of mezzanine floor shall be fixed at 70% of the relative rate of base value of the flat beneath the mezzanine floor; and by applying the relevant weightages by multiplication provided for in these rules;

(b) the capital value of loft or attic floor shall be fixed at 50% of the relative rate of base value of the flat beneath the loft, or as the case may be, the attic; and by applying the relevant weightages by multiplication provided for in these rules;

Provided that, where the rate of base value applicable to the mezzanine floor, loft or attic floor having regard to its user is higher or, as the case may be, lower than the rate of base value applicable to the flat beneath such mezzanine floor, loft or attic floor, the capital value of such mezzanine floor, loft or attic floor shall be fixed at 70% or 50%, as the case may

Manual I_ page no 43

be, of such higher or lower rate of base value; and by applying the relevant weightages by multiplication provided for in these rules.

16. 'deleted'.

17. Fixation of capital value in respect of demolished building:-

(1) Where a building is fully demolished, or has fully collapsed, the land beneath it shall be deemed to be open land and the capital value thereof shall be fixed accordingly, as provided for in rule 21.

Explanation – " deleted"

(2) Where only part of a building is demolished or has partly collapsed and the remaining part is yet occupied by occupiers, land beneath the portion of the building which is demolished or has collapsed shall be deemed to be open land and the portion of the structure which is occupied shall be treated as a building, for the purpose of fixing the capital value thereof.

(3) "deleted"

18. 'deleted'.

19. 'deleted'.

19 A Assessment of Amenities in Luxurious RCC bldg

Where Property tax in respect of amenities of luxurious RCC building was not levied since 1st April 2010 as per Rule 19, while determining the property tax leviable from 1st April 2015, subject to capping as provided for in section 140A such tax shall be considered which would have been continued to levy from 1st April 2010

20. Valuation of open land capable of utilising more than 1 floor space index (F.S.I.) or transfer of development right (T.D.R.) –As the Ready Reckoner provides for the rate of base value of open land with 1 floor space index, open land which is capable of utilizing more than 1 floor space index or any transfer of development right shall be valued at an

Manual I_ page no 44

increased rate in proportion to the higher floor space index or transfer of development right proposed to be utilized and approved under the building plan submitted to the Corporation for approval.

21. Capital value of open land or building or part thereof.-Capital value of open land or building shall be fixed under the provisions of the Act and these rules in the following manner, namely:-

(1) Capital value (CV) of open land –

Rate of base value (BV) of a open land according to Ready Reckoner X weightage by multiplication as per user category (UC) (Part I of schedule ‘A’) X permissible or approved floor space index (FSI) X area of land (AL) .

CV = BV x UC x FSI x AL

(2) Capital value (CV) of a building –

Relative rate of base value (BV) of a building according to Ready Reckoner X weightage by multiplication as per user category(UC) (Parts II, III, or as the case may be, IV of schedule ‘A’) X weightage by multiplication as per the nature and type of building (NTB) (schedule ‘B’) X weightage by multiplication on account of age of building (AF) (schedule ‘C’) X weightage by multiplication on account of floor factor (FF) for RCC building with lift (schedule ‘D’) X carpet area (CA) .

CV = BV x UC x NTB x AF x FF x CA

22. Non-application of Guidelines of Stamp Duty Valuation. - Notwithstanding anything contained in the ’Important Guidelines of Stamp Duty Valuation’ as specified in the Ready Reckoner, the provisions made in these rules shall have primacy over those guidelines and none of those guidelines shall apply for fixing capital value under the Act and these rules.

Manual I_ page no 45

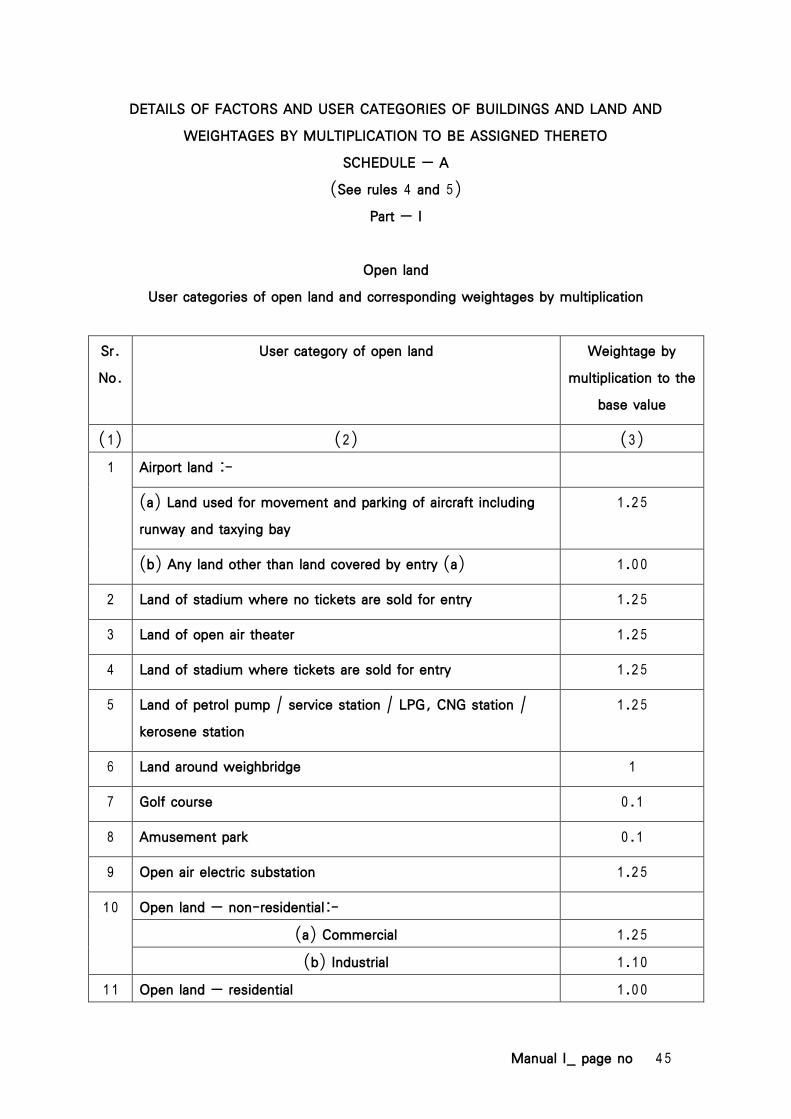

DETAILS OF FACTORS AND USER CATEGORIES OF BUILDINGS AND LAND AND WEIGHTAGES BY MULTIPLICATION TO BE ASSIGNED THERETO

SCHEDULE – A (See rules 4 and 5)

Part – I

Open land User categories of open land and corresponding weightages by multiplication

Sr. No.

User category of open land

Weightage by multiplication to the

base value

(1) (2) (3) 1 Airport land :-

(a) Land used for movement and parking of aircraft including runway and taxying bay

1.25

(b) Any land other than land covered by entry (a) 1.00

2 Land of stadium where no tickets are sold for entry 1.25

3 Land of open air theater 1.25

4 Land of stadium where tickets are sold for entry 1.25

5 Land of petrol pump / service station / LPG, CNG station / kerosene station

1.25

6 Land around weighbridge 1

7 Golf course 0.1

8 Amusement park 0.1

9 Open air electric substation 1.25

10 Open land – non-residential:- (a) Commercial 1.25 (b) Industrial 1.10

11 Open land – residential 1.00

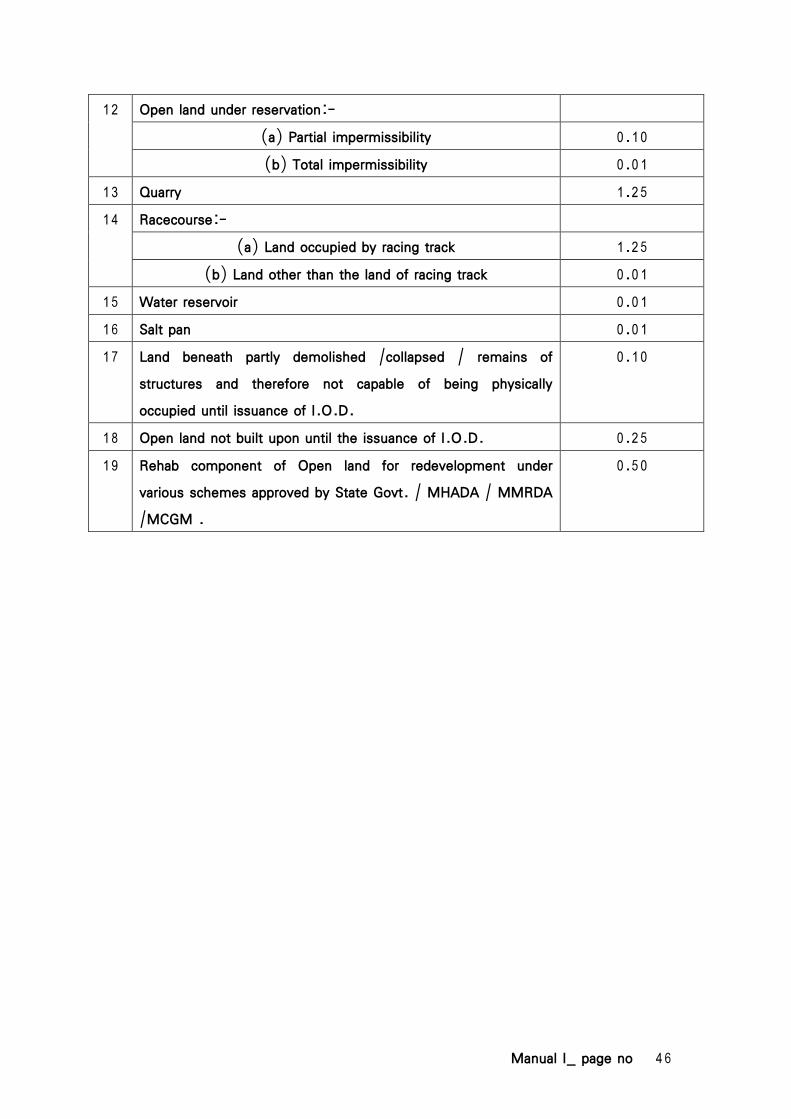

Manual I_ page no 46

12 Open land under reservation:- (a) Partial impermissibility 0.10 (b) Total impermissibility 0.01

13 Quarry 1.25 14 Racecourse:-

(a) Land occupied by racing track 1.25 (b) Land other than the land of racing track 0.01

15 Water reservoir 0.01 16 Salt pan 0.01 17 Land beneath partly demolished /collapsed / remains of

structures and therefore not capable of being physically occupied until issuance of I.O.D.

0.10

18 Open land not built upon until the issuance of I.O.D. 0.25 19 Rehab component of Open land for redevelopment under

various schemes approved by State Govt. / MHADA / MMRDA /MCGM .

0.50

Manual I_ page no 47

SCHEDULE – A (See rules 4 and 5)

PART – II Residential Buildings

User categories of residential buildings and corresponding weightages by multiplication Sr. No. User category of residential building or part

thereof Weightage by multiplication to