chapter - iv progress of dairy industry in india and...

TRANSCRIPT

87

CHAPTER - IV

PROGRESS OF DAIRY INDUSTRY IN

INDIA AND TAMILNADU

4.0 Introduction

The objective of the present piece of research is to examine

the problems and prospects in production and marketing of milk

in the district of Kanyakumari. Hence, before examining these

issues it becomes pertinent to understand the situation of the

dairy industry and factors influencing the overall performance of

milk sector at the macro level. The present chapter is directed

towards this end.

4.1 Features of Dairying in India

Dairying in India is exemplary of smallholder dairying as

practiced in much of Asia and Africa—with some wrinkles. Like

smallholder dairying in general, the Indian milk production

sector is characterized by a very large number of very small

herds. Milk from small herds is collected immediately after each

milking at centralized cooling facilities to maintain a cold chain.

Also typical of smallholder dairying, a majority of the milk

produced (more than 80 percent) is distributed as drinking milk

or home-based manufactured products through an informal

marketing system. [Ahluwalia, Montek S. (2005)]1

88

The unique aspects of smallholder dairying in India

include: [Banerjee (1994)]2

� Production of milk from buffalo exceeds cow milk

production. Buffalo yield less milk than crossbred cows,

but are well-adapted to the extreme heat and humidity of

India. Moreover, many Indians prefer buffalo milk over cow

milk because of its higher butterfat content.

� Cows are considered sacred in the Hindu religion that

predominates in India, and cow slaughter is rare. Some

buffalo are slaughtered, but the high incidence of

vegetarianism limits domestic markets for buffalo meat.

Consequently, cull dairy animals; represent a disposal cost

rather than a source of income to Indian dairy farmers.

� Feed for Indian dairy animals consists mainly of crop

residues and by products. Forage and feed grain

production is limited due to pricing incentives to grow

cereals and pulses to feed India's vast population.

� India has an extensive government-supported dairy

cooperative structure. Cooperatives not only market their

members' milk, but also supply feeds and many dairy

services. Private dairy companies tend to duplicate the

operating procedures of the cooperatives.

89

4.2 The Indian Milk Production Sector

4.2.1 General Characteristics

India surpassed the United States in 1998 to become the

largest single milk producing country in the world. In 2005,

Indian milk production represented 14.6 percent of world milk

production, exceeding the combined production of the top five

dairy countries in the EU.

Milk production has grown steadily and rapidly over the

last 25 years, from 50 million MT in 1979-80 to 92 million MT in

2004-05. Growth in milk production has exceeded the growth in

India's population, elevating per capita milk availability over the

same period from 75 grams/day to more than 225 grams/day.

The dairy production sector of India is atomistically (perhaps

micro-atomistically) structured. Milk production is primarily a

supplementary occupation for small landholders or landless

laborers. There are no official counts of dairy farms and

estimates vary widely among sources. Best estimates indicate

that approximately 70 million rural households (primarily small

and marginal farmers and landless laborers) are engaged in milk

production. The average herd size is about two milking animals,

and average daily milk production per herd is about four liters.

Cattle are fed primarily on byproducts from crop

production. Green forage occupies about 4 percent of India's

90

arable cropland. Concentrate feeds do not usually contain feed

grains, but could include starch from rice and wheat milling and

molasses from sugar production. Green forages include berseem

clover, oats, ryegrass and sorghum. Villages in some areas often

have unimproved common pasture lands.

Manure is a valuable resource for fuel and fertilizer. Much

of the manure from dairies is formed into dung pies and dried

for use or sale as a heating and cooking fuel. Manure that is not

used for fuel is applied directly to cropland, reducing chemical

fertilizer needs.

Dairying is practiced throughout India, but concentrated in

the northwestern states where the climate is more temperate.

The top five states account for more than one-half of current

production. Major surplus producing states (percent of milk

production more than twice the percentage of population) are

Punjab and Haryana. West Bengal and Bihar are major milk

deficit states.

More than one-half of India's milk production comes from

buffalo. The predominant buffalo breed is the Murrah, a river

type buffalo that has been selected for milk production. Buffalo

milk is preferred to cow milk by consumers in many parts of

India because of its relatively high butterfat content. The percent

91

of total milk coming from buffalo has remained practically

constant at about 55 percent since the early 1960s.

India's dairy cow population is a combination of

indigenous cattle and cross-breed (mostly Holsteins) with

indigenous stock. Purebred dairy cows do not tolerate the heat

and animal diseases prevalent in India. Cross breeding increases

milk production while preserving native heat tolerance and

disease resistance. Milk production capacity is highest in cross

breeds followed by buffalo and native cattle. The cow population

has been growing at a considerably smaller rate than buffalo.

But more rapid increases in yields from increasing adoption of

cross-breeding have resulted in the relative shares of cow and

buffalo milk remaining constant. [Chand R. (2005)]3

4.2.2 Milk Production Costs

On average, milk production costs in India are very low by

international standards. In its 2005 annual dairy report, the

International Farm Comparison Network (IFCN) reported 2004

costs and returns for eleven Indian dairies in four states. Cash

costs less non-milk returns, ranged from US$2.50 to US$15 per

100 kg (US$1.13 to US$6.80 per hundredweight). Total costs

ranged from US$15 to US$23 per 100 kg (US$6.80 to US$10.43

per hundredweight). All but one of the eleven representative

92

farms had herds of from two to six dairy animals (cows and/or

buffalo).

These are impressively low costs of production, compared to

U.S. total costs (less non-milk returns) in the neighborhood of

US$11.80 to US$13.60 per hundredweight. They result from

very low labor costs (paid labor and opportunity costs for family

and operator labor), feed costs, depreciation, and opportunity

cost for land. For example, labor costs for some of the smaller

representative farms were reported at US$0.20 per hour. Land

cost for some farms is zero. Indian dairy farmers' cash expenses

and overhead costs are low enough to more than offset the

negative effect on unit costs of production of very low milk yields

per animal.

But Indian costs of milk production must be interpreted

carefully. While they may accurately represent average costs

under existing conditions, they do not likely reflect marginal

costs, especially if ambitious expanded production goals are

achieved and economic conditions in rural areas improve. [FAO

(2002)]4

4.2.3 Milk Prices

Each cooperative and most private dairy firm set and

moves their milk price independently, based on the profitability

of final product sales, local competition, and other factors. There

93

is no systematic milk price reporting, probably because of wide

variability in prices among and within plants and the difficulty of

obtaining reliable price data from thousands of reporting units.

The Food and Agricultural Organization of the United

Nations (FAO) does report a country average time series of milk

prices by species. Prices for both cow and buffalo milks have

been gradually increasing with significant gains since 2002. The

gap between buffalo and cow milk prices has been steady in

percentage terms at about a 30 percent premium for buffalo

milk. India cow milk prices between 1991 and 2005 averaged 70

percent of U.S. milk prices; buffalo milk prices averaged 92

percent. Indian milk prices as reported by FAO were very stable

compared to U.S. prices.

4.3 Processing Sector

4.3.1 General Description

A primary characteristic of milk processing and dis-

tribution in India is the dominance of the informal sector. About

one-third of the milk produced is retained on the farm for food

and feed. Of the two-thirds leaving the farm, approximately 75

percent goes to the unorganized or informal sector and the

remaining 25 percent is handled by the formal sector.

The large informal sector exists partly because consumers

have been unwilling to pay the additional costs of pasteurization

94

and packaging, which can raise retail prices by more than 100

percent. Moreover, consumers often regard raw milk and

traditional products obtained from reliable vendors as of better

quality than formally processed dairy products.

In the informal sector, raw milk may be sold directly to the

consumer by the farmer or the farmer may sell it to a "milkman"

who re-sells to consumers or to a creamery. The creamery also

sells to consumers but may sell to sweet shops and restaurants.

The informal sector encompasses the marketing of raw milk and

traditional products such as locally manufactured ghee, fresh

cheese and sweets. This sector is quite well organized, with a

complex net of market agents. It may also not be entirely

informal, since some market agents pay municipal fees and

possess vendor licenses.

The formal sector is relatively new in historical terms, and

consists of western-style dairy processing based on

pasteurization, although adapted to the Indian market in terms

of products. The formal sector consisted of 678 dairy plants in

2002, registered under the Milk and Milk Products Order

(MMPO) and has grown rapidly during the last decade.

4.3.2 Milk Procurement and Processing

About 110,000 dairy cooperative village societies, involving

about 12 million farmer members, had been organized by 2003-

95

04 to supply milk to processing firms and directly to consumers.

Until the early 1990s, milk processing was mainly reserved for

the cooperative sector through licensing. As part of domestic

economic reforms and commitments to the WTO, the Indian

dairy sector was liberalized in a phased manner starting in

1991. The government removed all restrictions on setting up new

milk-processing capacity in March 2002.

Following partial decontrol of the dairy sector in the early

1990s, many private sector processors entered the market and

established milk-processing facilities, mostly in milk surplus

areas. Some of the private sector plants also adopted the

cooperative model of making informal contracts with local

farmers and providing various inputs and services to the

farmers. Nestle made large investments in its milk shed to

improve productivity levels and the quality of raw milk. However,

a large proportion of private dairy plants depend on

contractors/subcontractors to meet their raw material

requirement.

Based on 1999-2000 sales, the largest Indian dairy

companies/cooperatives were: Gujarat Cooperative Milk

Marketing Federation (GCMMF), Mother Dairy, Nestle India,

Hindustan Lever Ltd., Britannia, Andhra Pradesh Dairy

Development Cooperative Federation (APDDCF), Hatsun Agro,

96

and Vadial. The GCMMF dominates the processing sector, and

has about three times the sales of its nearest competitor.

4.4. Milk and Product Distribution

4.4.1 Past and Present Systems

Sale and distribution of fluid milk may occur directly from

the farm or the milk collection stations or through local

distributors. The remaining milk is cooled, transported to

processing plants, and converted into market (fluid) milk and

milk products that are distributed by a variety of means. Loose

or bulk pasteurized milk is dispensed to the consumer in the

Mother Dairy kiosks. Each dairy cooperative has its own

channels for distributing milk and other products. Private dairy

companies distribute products through local shops because

refrigerated distribution channels are sparse. Initiatives are

beginning to enlarge their markets into other states. Larger

cooperatives are beginning to expand through their own and

franchised market outlets.

The principal outlet for the popular traditional sweets

made from condensed milk is sweetshops or halwais. These are

located in markets of virtually every city and are generally

subject to government oversight. A limited number of dairy

outlets are in newly-built shopping centers in the upper-middle

and upper class sections of cities like New Delhi, Mumbai,

97

Bangalore, etc. Fashioned after western-style merchandizing,

they handle Indian dairy products and imported items such as

cheeses from a number of European and Oceanic countries.

4.4.2 Future Trends

Emergence of a more affluent segment of the Indian

population, albeit small as percent of total population but large

in numbers, seems to be prompting a shift to more value-added

dairy products. Packaged market milk is gaining in popularity

compared to "loose" milk. Markets for UHT milk and flavored

milks are growing but are still niche markets. It must be

remembered, however, that a niche market of 0.1 percent of the

Indian population is more than 1.1 million persons.

Traditional Indian dairy products such as paneer and

dairy-based sweets, with longer shelf-life, are being marketed as

branded products by cooperative and private companies. Butter,

ghee and ice cream are competitive markets dominated by a few

firms that have the manufacturing and merchandizing

capabilities to compete in these markets.

In spite of a dispersed market, a competitive climate, and

the present uncertainty about the nature and rate of change of

dairy product marketing and consumption in India, a number of

foreign investments have been made in recent years. Of

particular interest are two firms located in Wisconsin. Schreiber

98

Foods, Green Bay, has recently acquired 51 percent of Dynamic

Dairy Industries Ltd., which produces a broad range of products

including process cheese. A plan to market buffalo milk

Mozzarella cheese in the USA is part of collaboration between

Winona Foods, Green Bay, and Himalaya International.

While dairy products undoubtedly are now widely regarded

as premium foods in India, it may become more difficult for dairy

products to keep this status when more people enter the middle

and upper income groups. It seems likely that middle and upper

income consumers would not be satisfied with the sort (two to

four day shelf-life) of milk sold by processors in the formal sector

in parts of India. The formal dairy processing sector will benefit

if it can capitalize on the demands of upper and middle income

people for convenience, hygiene and quality.

The affordability of dairy products varies widely across

India. Middle and upper income consumers— possibly as many

as 450 million people in the future— will have the purchasing

power to purchase desired quantities of dairy products. However,

the remainder of the population, including many people living in

rural areas, will be subject to important income constraints.

As in many parts of the world, India's dairy industry will

witness increases in demand for dairy products from the food

service industry, the ingredients market, and away-from-home

99

food consumption businesses. Improved milk quality would

likely increase the importance of these sources of milk and dairy

product demand in India.

4.5 Trade Issues

4.5.1 India's Dairy Trade

Dairy trade is a small part of India's small agricultural

trade portfolio. In 2004, FAO reported Indian dairy exports of

US$78 million and imports valued at US$11 million. Exports

were record high in 2004, buttressed by large exports of casein

(reported as SMP by FAO). Together with SMP, whole milk

powder and butter/ghee comprised 94 percent of 2004 dairy

export value.

India's dairy imports consist mainly of butter/ghee, some

hard cheeses, and dry whey products. Butter/ ghee imports

were one-fifth of exports.

Both imports and exports are highly variable from year-to-

year. India's dairy trade balance has ranged from US$-30

million to US$65 million between 1989 and 2004. India's very

small volume of imports of dairy products is due partly to

restricted market access through import tariffs and partly to

sanitary requirements for some products. In 2001, India

removed all quantitative restrictions on agricultural imports.

100

4.5.2 U.S. - India Dairy Trade

U.S.-India dairy trade is small and decidedly one sided. In

2005, the U.S. exported less than US$3 million in dairy products

to India and imported US$60 million. Nearly all of the U.S. dairy

imports from India in 2005 were in the form of casein and

casein-ates. Casein imports totaled US$53 million, and India

was the third largest supplier of casein, behind Ireland and New

Zealand. The value of casein imports from India nearly doubled

between 2004 and 2005.

Most U.S. dairy products are restricted from India by

sanitary/heath certification rules adopted in 2004. Among other

things, these rules prohibit imports of dairy products derived

from animals administered supplemental recombinant Bovine

Somatatropin (rBST or BGH) or subjected to estrogenic

treatment. Since these products are widely-used in the U.S.,

most exporters cannot meet these standards.

4.5.3 India Dairy Trade Prospects

Dairy imports are a contentious issue in India. While

government policy generally supports more open trade, dairy

interests are strongly opposed to allowing great access to

imports. Some of this opposition seems to reflect a

misunderstanding of India's current dairy trade balance, or,

101

perhaps, a general negative perception regarding the possible

benefits of expanded trade.

Opposition also comes from those concerned about the

impact of more open trade on the fate of rural residents and

rural communities. The Government of India and many

agricultural trade groups have expressed a strong interest in

maintaining self-sufficiency in dairy and other agricultural

products. However, India may experience pressures to import

more dairy products in the future if demand for dairy products

unfolds strongly in response to increases in population and

incomes. [Foreign Agriculture Service (2005)]5

Alternatively, if strong internal demand for dairy products

fails to materialize, India, as the largest milk producer in the

world, may feel pressures to export dairy products. For example,

if India's real GDP growth should moderate to 4.5 percent and

assuming an income elasticity of demand of 0.6 percent and

population increases of 1.4 percent year, then domestic dairy

product purchases in India might increase at only about 4.1

percent per year. Under such a scenario, projected domestic

supplies of dairy products could put strong downward pressure

on prices and increase the incentives of dairy firms to export.

102

4.6 Government Policies Affecting Dairy

4.6.1 General Agricultural Policies

Since independence in 1947, a primary goal of Indian

agricultural policy has been food self- sufficiency. This goal has

been pursued through direct and indirect support for the

farming sector to reduce cash costs of production and through

setting minimum prices for food crops that stabilize and

enhance revenue.

Direct support includes input subsidies for production

inputs and services. The largest subsidies are for fertilizer and

irrigation. Fertilizer subsidies go to both farmers and fertilizer

manufacturers. Fertilizer is made available to farmers at fixed

prices under market. For imported fertilizer, the difference

between the import cost and the fixed price is subsidized. For

fertilizers produced domestically, manufacturers are paid a sub-

sidy representing their economic costs of manufacturing and

distributing fertilizers. The total fertilizer subsidy in 2005-06 is

estimated at $3.7 billion.

Irrigation is subsidized in two ways; through charging less

than market rates for electrical power used for pumping

groundwater and through public investment in surface water

distribution systems and covering distribution costs. Power and

103

water subsidies were estimated to total about $6.4 billion in

2003-04.

Minimum procurement prices apply to a large number of

crops. For rice and wheat, the primary food crops, the minimum

prices serve as intervention prices. That is, the government

purchases these commodities for storage and distribution under

the Indian Public Distribution System, which supplies foodstuffs

at subsidized prices to the poor. Since the government accepts

all rice and wheat offered at the announced support prices,

purchases vary according to crop size and private sector

demand.

Good crops and reduced consumption in the late 1990s led

to large government purchases and a buildup of government rice

and wheat stocks. The Indian government was forced to

subsidize exports in order to reduce stocks to a manageable

level. Later, stocks were depleted and in 2006, the government

needed to import wheat in order to meet its distribution needs.

Indirect forms of government support for farmers include

agricultural research and outreach, underwriting crop

insurance, and financial and institutional support for

cooperatives, including farm credit cooperatives.

Direct support in the form of subsidies and minimum

prices is limited to the crop sector of Indian agriculture.

104

Livestock and dairy are not directly supported, but receive some

indirect support through induced production of crops that yield

byproducts and residues for feeding to livestock. But at the same

time, subsidies and price guarantees for specific crops restrict

the area devoted to other, unsupported crops, notably fodder.

More generally, current agricultural supports have been

criticized for "locking in" crop production patterns that are

becoming increasingly separated from domestic consumption

patterns. Expanding consumer incomes in areas with strong

economic growth has increased demand for horticultural crops,

poultry and dairy products, and edible oils. Current support

policies provide little incentives for shifting production to higher-

demand products. Subsidies have also been criticized for

causing mining of groundwater and for restricting private

investment in agriculture.

The 2004 Indian national elections resulted in a new

coalition government (United Progressive Alliance, or UPA) led by

the Indian National Congress Party. The UPA-selected Indian

Prime Minister, Dr. Manmohan Singh, has publicly supported

making agriculture more market-oriented. But agricultural

reform is not an easy task in India because of the involvement of

states— states must agree to and implement policies recom-

mended and funded by the central government. Given the

105

diversity of agriculture among states, acrimony is more likely

than harmony.

4.6.2 Dairy Policies

Economic conditions existing in India in the decade

following independence created an environment that gave rise to

unique policies and institutions that shaped development of the

country's dairy industry. In the 1950s and 1960s, India was one

of the largest dairy importing countries in the world. For

example, India's commercial imports of milk powder peaked at

over 50 thousand metric tons in 1963-64. This contrasts sharply

with the zero milk powder imports recorded by India in 2005.

The large dairy imports in the 1960s stunted development

of India's dairy industry, causing milk production in the country

to plateau at about 20 to 22 million metric tons per year in that

decade. This happened partly because frequently it was cheaper

for India's domestic firms to import milk powder and butter or

butter oil and make reconstituted milk, rather than buy milk

from India's farmers.

This situation concerned India's policy makers who

reasoned that an expanding domestic dairy industry would be a

good vehicle for promoting employment and rural development.

Moreover, government officials and persons in the dairy industry

recognized that India's population growth, urbanization, income

106

growth, the high income elasticity of demand for dairy products,

and changes in consumption habits, all might support profitable

expansion of the country's dairy industry. Hence, the

government of India embarked on an import substitution policy

that would produce near self-sufficiency in dairy products.

Initially, this policy was basically a dairy cooperative

development initiative.

The foundation for this initiative was the cooperative

movement in the state of Gujarat. In 1952, the Kaira District

Cooperative Milk Producers' Union (currently the Gujarat

Cooperative Milk Marketing Federation) gained the right to

supply the Bombay market with fluid milk. This assured market

allowed the cooperative to grow rapidly but also provided a

challenge in maintaining a cold chain and balancing milk

production with fluid milk demand. The cooperative adopted a

unique tiered system of milk collection and processing. Village

cooperative societies collected and cooled milk from tens of

thousands of small dairy farmers throughout the state. District

unions consolidated society shipments and operated

manufacturing plants to handle fluid surpluses. Marketing and

coordination were at the state level. The cooperative adopted the

AMUL brand and developed nationwide brand recognition.

107

The tiered system ultimately became known as the Anand

Model (for the location of the cooperative federation

headquarters), and was promoted and financially supported by

the Indian government through the National Dairy Development

Board (NDDB), created in 1965.

4.6.3 Government Support for Operation Flood

The purpose of Operation Flood was to create a white flood

of milk throughout India by widely replicating and financially

supporting the Anand Model. The first phase of Operation Flood

was launched in 1970 under an agreement with the World Food

Program. This agreement provided aid and financing in the form

of 126,000 tons of skim milk powder and 42,000 tons of butter

oil-surplus dairy products obtained from the then European

Economic Community (EEC). In brief, the Operation Flood

program carried out the following functions:

� Organized village dairy cooperatives.

� Created the physical and institutional infrastructure

for milk procurement, processing, marketing and

production enhancement services.

� Established dairies at India's major metropolitan

centers—i.e., Bombay, Calcutta, Delhi and Madras.

� The second phase of the program was implemented

between 1981 and 1985. It incorporated state dairy

108

development projects that had been undertaken with

assistance of the Indian Dairy Corporation into an

overall program. This effort was financed with $150

million from the World Bank and commodity assis-

tance from the EEC.

� The third phase focused on making the cooperative

efforts self-sustaining. Employing World Bank, EEC

and the NDDB's internal resources, this phase

expanded the production, processing, marketing and

professional management capabilities of the dairy

industry.

� In addition to financial support, the Government of

India sharply limited commercial dairy imports from

the early years of Operation Flood until the early

1990s. This action was justified in part as protection

for an "infant industry." The permitted dairy imports

were "canalized" (channeled) through the NDDB as

importing agency.

4.6.4 The Lifting of Restrictions on India's Domestic Dairy

Industry

India's dairy sector was regulated and protected through

restrictions on imports and exports of dairy products and

domestic regulations until the early 1990s. The industry became

109

progressively more liberalized after 1991 as a result of changes

that culminated in the repeal of certain licensing requirements

and changes in the Milk and Milk Products Order (MMPO) to

reform India's dairy economy. Among the restrictive measures

contained in the MMPO that were eventually eliminated was one

that specified the milksheds from which dairy processors could

procure milk.

Prior to the 1990s, milk procurement, processing and

supply to urban consumers was primarily in the hands of

cooperatives. The entry of most big proprietary firms into the

processing sector was restricted through licenses. As part of

broader economic reforms introduced in 1991, licensing of dairy

industry firms ended and the industry was opened to private

competition.

Within a year after the 1991 reforms, more than 100 new

private sector dairy plants were set up in the India's dairy

industry. Unfortunately, some of the new private plants sold

adulterated and contaminated milk products. Consequently, the

government brought back a licensing system under the MMPO of

1992, requiring state regulation of dairy plants producing

10,000 to 75,000 liter of milk per day or manufacturing of milk

products containing 500 to 3,750 tons of milk solids per year.

Plants producing over 75,000 liters of milk per day or handling

110

more than 3,750 tons of milk solids per year had to be registered

with the central government.

The 1992 MMPO defined "milksheds" in reference to the

region from which the marketable surplus of milk was to find its

way to a processing plant. The edict in the 1992 MMPO relating

to milksheds was implemented by state or central government

Registering Authorities.

In 2001 the MMPO was amended to require compulsory

registration only for larger dairy plants that processed over

20,000 liters pay day. The MMPO was last amended in 2002 to

raise the registration requirement to 200,000 liters per day and

to eliminate state authority to assign milksheds. Most private

companies applauded the end of milk shed definition by the Reg-

istering Authority. Some of them were able to substantially

expand their procurement area. [Indian Dairy (2005)]6

4.7 State Wise Production Performance in Milk As noted earlier, in the present section it is attempted to

examine the performance of states in terms of milk production

and the inequality in them.

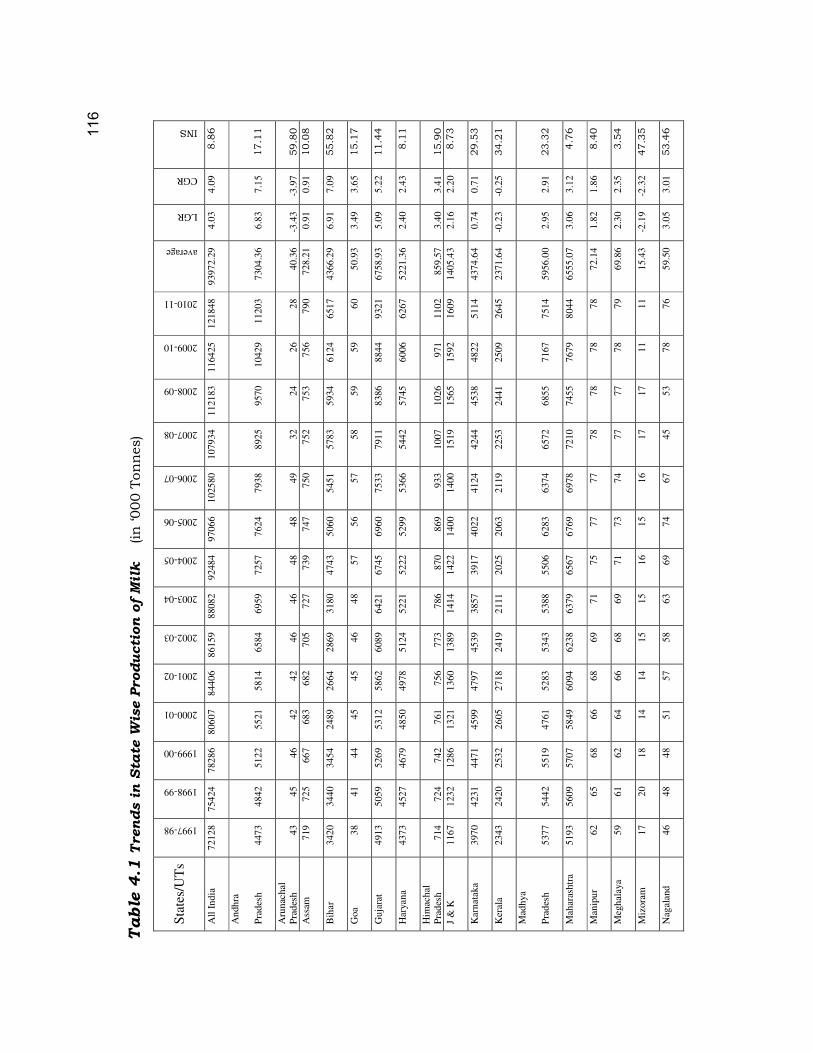

4.7.1 Trends in State Wise Production of Milk The performance of the state at the macro level, with

dispersion or deviation in it, is being determined by the

performance by its district. Based on this view, before embarking

111

upon the analysis of the production of milk at the micro level, in

the present section it is attempted to examine the state wise

production of milk and the inequality in production.

As it could be seen in table 5.1, the total production of milk

in India in the year 1997-98 stood at 721.28 million tonnes. A

state wise analysis of milk production in the same year indicates

that the highest level of milk production has been registered by

Uttar Pradesh with 129.34 lakh tonnes of milk production. This

state alone constituted 17.93 per cent of the country’s total milk

production. This is being followed by the other states in the

declining order of milk production as: Punjab (71.65 lakh

tonnes), Rajasthan (64.87 lakh tonnes), Madhya Pradesh (53.77

lakh tonnes), Maharashtra (51.93 lakh tonnes), Gujarat (49.13

lakh tonnes), Andhra Pradesh (44.73 lakh tonnes), Haryana

(43.73 lakh tonnes), Tamil Nadu (40.61 lakh tonnes), Karnataka

(39.7 lakh tonnes), Bihar (34.2 lakh tonnes), West Bengal (34.15

lakh tonnes), Kerala (23.43 lakh tonnes), J & K (11.67 lakh

tonnes), Assam (7.19 lakh tonnes), Himachal Pradesh (7.14 lakh

tonnes), Orissa (6.72 lakh tonnes), Delhi (2.67 lakh tonnes),

Manipur (0.62 lakh tonnes), Meghalaya (0.59 lakh tonnes),

Tripura (0.57 lakh tonnes), Nagaland (0.46 lakh tonnes),

Arunachal Pradesh (0.43 lakh tonnes), Chandigarh (0.43 lakh

tonnes), Goa (0.38 lakh tonnes), Pondicherry (0.36 lakh tonnes),

112

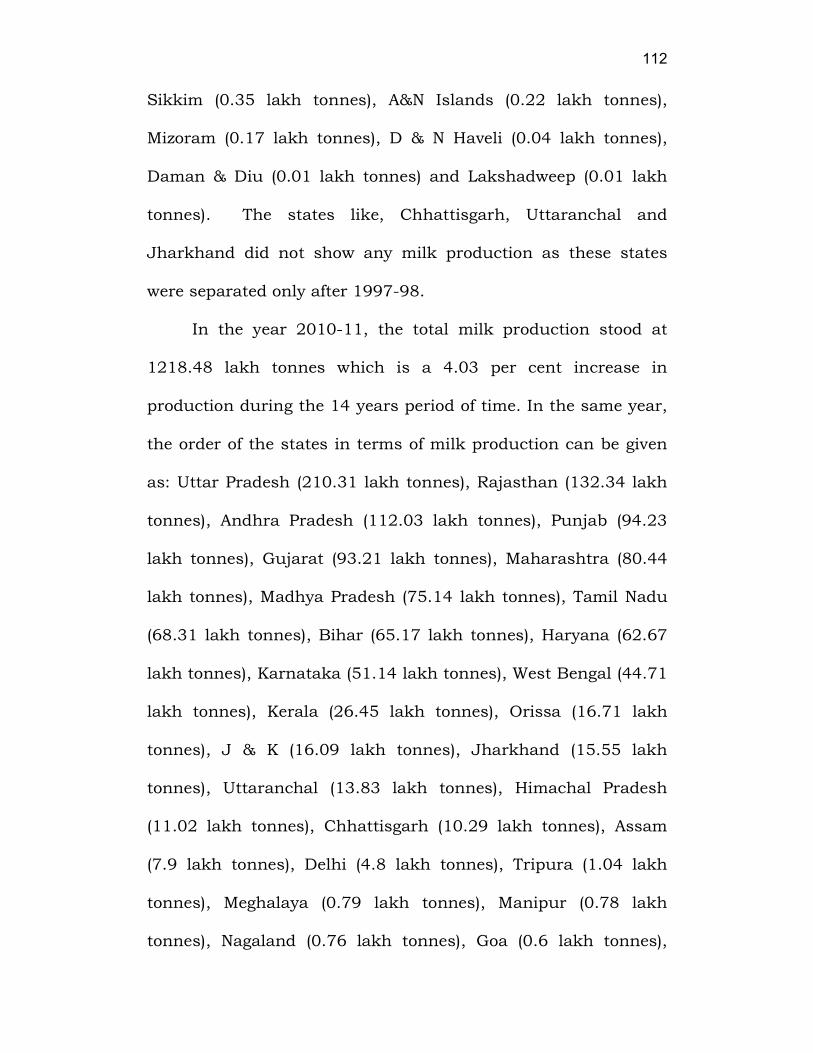

Sikkim (0.35 lakh tonnes), A&N Islands (0.22 lakh tonnes),

Mizoram (0.17 lakh tonnes), D & N Haveli (0.04 lakh tonnes),

Daman & Diu (0.01 lakh tonnes) and Lakshadweep (0.01 lakh

tonnes). The states like, Chhattisgarh, Uttaranchal and

Jharkhand did not show any milk production as these states

were separated only after 1997-98.

In the year 2010-11, the total milk production stood at

1218.48 lakh tonnes which is a 4.03 per cent increase in

production during the 14 years period of time. In the same year,

the order of the states in terms of milk production can be given

as: Uttar Pradesh (210.31 lakh tonnes), Rajasthan (132.34 lakh

tonnes), Andhra Pradesh (112.03 lakh tonnes), Punjab (94.23

lakh tonnes), Gujarat (93.21 lakh tonnes), Maharashtra (80.44

lakh tonnes), Madhya Pradesh (75.14 lakh tonnes), Tamil Nadu

(68.31 lakh tonnes), Bihar (65.17 lakh tonnes), Haryana (62.67

lakh tonnes), Karnataka (51.14 lakh tonnes), West Bengal (44.71

lakh tonnes), Kerala (26.45 lakh tonnes), Orissa (16.71 lakh

tonnes), J & K (16.09 lakh tonnes), Jharkhand (15.55 lakh

tonnes), Uttaranchal (13.83 lakh tonnes), Himachal Pradesh

(11.02 lakh tonnes), Chhattisgarh (10.29 lakh tonnes), Assam

(7.9 lakh tonnes), Delhi (4.8 lakh tonnes), Tripura (1.04 lakh

tonnes), Meghalaya (0.79 lakh tonnes), Manipur (0.78 lakh

tonnes), Nagaland (0.76 lakh tonnes), Goa (0.6 lakh tonnes),

113

Pondicherry (0.47 lakh tonnes), Chandigarh (0.45 lakh tonnes),

Sikkim (0.43 lakh tonnes), Arunachal Pradesh (0.28 lakh

tonnes), A&N Islands (0.25 lakh tonnes), Mizoram (0.11 lakh

tonnes), D&N Haveli (0.11 lakh tonnes), Lakshadweep (0.02 lakh

tonnes) and Daman & Diu (0.01 lakh tonnes).

A comparison of the state wise production in the year

1997-98 and 2010-11 would indicate that between these two

years there is a wide change in the order of the states in terms of

production. While some of the states could increase their milk

production and reach a higher rank, the production in some

states like, Arunachal Pradesh, Kerala, Mizoram have

experienced a decline in the production which made them to get

relegate to the back in terms of their ranks.

The order of the states in terms of average level of milk

production for the entire study period can be given as: Uttar

Pradesh (165.739 lakh tonnes), Rajasthan (91.3929 lakh

tonnes), Punjab (84.75 lakh tonnes), Andhra Pradesh (73.0436

lakh tonnes), Gujarat (67.5893 lakh tonnes), Maharashtra

(65.5507 lakh tonnes), Madhya Pradesh (59.56 lakh tonnes),

Tamil Nadu (53.9543 lakh tonnes), Haryana (52.2136 lakh

tonnes), Karnataka (43.7464 lakh tonnes), Bihar (43.6629 lakh

tonnes), West Bengal (38.065 lakh tonnes), Kerala (23.7164 lakh

tonnes), Jammu and Kashmir (14.0543 lakh tonnes), Orissa

114

(11.8564 lakh tonnes), Jharkhand (9.82 lakh tonnes),

Uttaranchal (9.4164 lakh tonnes), Himachal Pradesh (8.5957

lakh tonnes), Assam (7.2821 lakh tonnes), Chhattisgarh (6.7614

lakh tonnes), Delhi (3.4064 lakh tonnes), Tripura (0.8521 lakh

tonnes), Manipur (0.7214 lakh tonnes), Meghalaya (0.6986 lakh

tonnes), Nagaland (0.595 lakh tonnes), Goa (0.5093 lakh

tonnes), Chandigarh (0.4436 lakh tonnes), Sikkim (0.4171 lakh

tonnes), Pondicherry (0.41 lakh tonnes), Arunachal Pradesh

(0.4036 lakh tonnes), Andaman and Nicobar Islands (0.235 lakh

tonnes), Mizoram (0.1543 lakh tonnes), D&N Haveli (0.0764 lakh

tonnes), Lakshadweep (0.0171 lakh tonnes) and Daman & Diu

(0.01 lakh tonnes).

The growth rates worked out for the study period would

provide a clear view on the order of the states in terms of their

performance in the milk production. Accordingly, in terms of

linear growth rate worked out, the order of the states can be

given as: Jharkhand (12.77 per cent), Uttaranchal (10.9 per

cent), Chhattisgarh (10.75 per cent), Orissa (7.24 per cent),

Bihar (6.91 per cent), Andhra Pradesh (6.83 per cent), Rajasthan

(5.59 per cent), Gujarat (5.09 per cent), Delhi (4.67 per cent),

Tamil Nadu (4.18 per cent), Uttar Pradesh (3.78 per cent), Goa

(3.49 per cent), Himachal Pradesh (3.4 per cent), D&N Haveli

(3.36 per cent), Maharashtra (3.06 per cent), Nagaland (3.05 per

115

cent), Tripura (3 per cent), Madhya Pradesh (2.95 per cent),

Lakshadweep (2.82 per cent), Pondicherry (2.44 per cent),

Haryana (2.4 per cent), Meghalaya (2.3 per cent), Punjab (2.22

per cent), J & K (2.16 per cent), West Bengal (2.15 per cent),

Sikkim (2.01 per cent), Manipur (1.82 per cent), Assam (0.91 per

cent), A&N Islands (0.78 per cent), Chandigarh (0.77 per cent)

and Karnataka (0.74 per cent). Daman & Diu do not experience

any growth in output, while the districts like Kerala (-0.23 per

cent), Mizoram (-2.19 per cent) and Arunachal Pradesh (-3.43

per cent) have shown a declining growth during the study period.

11

6

Table

4.1

Tren

ds i

n S

tate

Wis

e P

roducti

on o

f M

ilk

(in

‘000 T

on

nes)

Sta

tes/

UT

s

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

average

LGR

CGR

INS

All

In

dia

7

21

28

754

24

782

86

806

07

844

06

86

15

9

8808

2

9248

4

9706

6

1025

80

1079

34

1121

83

1164

25

1218

48

9397

2.2

9

4.0

3

4.0

9

8.8

6

An

dh

ra

Pra

des

h

447

3

484

2

512

2

55

21

58

14

6584

6959

7257

7624

7938

8925

9570

1042

9

1120

3

7304

.36

6.8

3

7.1

5

17.1

1

Aru

nac

hal

Pra

des

h

43

45

46

42

42

46

46

48

48

49

32

24

26

28

40.3

6

-3.4

3

-3.9

7

59.8

0

Ass

am

719

7

25

66

7

683

682

705

727

739

747

750

752

753

756

790

728

.21

0.9

1

0.9

1

10.0

8

Bih

ar

342

0

344

0

345

4

24

89

26

64

2869

3180

4743

5060

5451

5783

5934

6124

6517

4366

.29

6.9

1

7.0

9

55.8

2

Goa

38

41

44

45

45

46

48

57

56

57

58

59

59

60

50.9

3

3.4

9

3.6

5

15.1

7

Gu

jara

t 4

91

3

505

9

526

9

53

12

58

62

6089

6421

6745

6960

7533

7911

8386

8844

9321

6758

.93

5.0

9

5.2

2

11.4

4

Har

yan

a 4

37

3

452

7

467

9

48

50

49

78

5124

5221

5222

5299

5366

5442

5745

6006

6267

5221

.36

2.4

0

2.4

3

8.1

1

Him

ach

al

Pra

des

h

714

7

24

74

2

761

756

773

786

870

869

933

1007

1026

971

1102

859

.57

3.4

0

3.4

1

15.9

0

J &

K

116

7

123

2

128

6

13

21

13

60

1389

1414

1422

1400

1400

1519

1565

1592

1609

1405

.43

2.1

6

2.2

0

8.7

3

Kar

nat

aka

397

0

423

1

447

1

45

99

47

97

4539

3857

3917

4022

4124

4244

4538

4822

5114

4374

.64

0.7

4

0.7

1

29.5

3

Ker

ala

234

3

242

0

253

2

26

05

27

18

2419

2111

2025

2063

2119

2253

2441

2509

2645

2371

.64

-0.2

3

-0.2

5

34.2

1

Mad

hya

Pra

des

h

537

7

544

2

551

9

47

61

52

83

5343

5388

5506

6283

6374

6572

6855

7167

7514

5956

.00

2.9

5

2.9

1

23.3

2

Mah

aras

htr

a 5

19

3

560

9

570

7

58

49

60

94

6238

6379

6567

6769

6978

7210

7455

7679

8044

6555

.07

3.0

6

3.1

2

4.7

6

Man

ipu

r 6

2

65

68

66

68

69

71

75

77

77

78

78

78

78

72.1

4

1.8

2

1.8

6

8.4

0

Meg

hal

aya

59

61

62

64

66

68

69

71

73

74

77

77

78

79

69.8

6

2.3

0

2.3

5

3.5

4

Miz

ora

m

17

20

18

14

14

15

15

16

15

16

17

17

11

11

15.4

3

-2.1

9

-2.3

2

47.3

5

Nag

alan

d

46

48

48

51

57

58

63

69

74

67

45

53

78

76

59.5

0

3.0

5

3.0

1

53.4

6

11

7

Ori

ssa

672

7

33

85

0

876

929

941

997

1283

1342

1431

1625

1598

1651

1671

1185

.64

7.2

4

7.8

2

22.5

4

Pu

nja

b

716

5

739

4

770

6

77

77

79

32

8173

8391

8554

8909

9168

9282

9387

9389

9423

8475

.00

2.2

2

2.2

7

5.4

4

Raja

sth

an

648

7

692

3

728

0

74

55

77

58

7789

8054

8310

8713

1030

9

1137

7

1193

1

1233

0

1323

4

9139

.29

5.5

9

5.6

0

26.4

5

Sik

kim

3

5

35

35

35

37

45

48

46

48

49

42

42

44

43

41.7

1

2.0

1

2.1

5

34.7

8

Tam

il N

adu

406

1

427

3

458

6

49

10

49

88

4622

4752

4784

5474

6277

6540

6651

6787

6831

5395

.43

4.1

8

4.2

3

23.1

6

Tri

pu

ra

57

76

77

77

90

79

84

86

87

89

91

96

100

104

85.2

1

3.0

0

3.1

8

21.2

2

Utt

ar P

rades

h

129

34

136

18

141

52

138

57

146

48

15

28

8

1594

3

1651

2

1735

6

1809

4

1886

1

1953

7

2020

3

2103

1

1657

3.8

6

3.7

8

3.8

5

7.6

0

Wes

t B

engal

3

41

5

344

1

346

5

34

71

35

15

3600

3686

3790

3891

3983

4087

4176

4300

4471

3806

.50

2.1

5

2.1

5

7.2

4

A&

N I

slan

ds

22

22

23

22

23

26

25

24

20

23

24

26

24

25

23.5

0

0.7

8

0.7

7

23.2

8

Chand

igar

h

43

43

42

43

43

43

44

43

46

46

47

47

46

45

44.3

6

0.7

7

0.7

7

8.0

7

D&

N H

avel

i 4

8

8

8

8

8

8

4

5

5

10

10

10

11

7.6

4

3.3

6

3.2

9

96.3

0

Dam

an &

Diu

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1.0

0

0.0

0

0.0

0

0.0

0

Del

hi

267

2

90

29

0

291

294

296

299

303

310

288

445

450

466

480

340

.64

4.6

7

4.4

5

45.9

0

Laksh

adw

eep

1

2

1

2

2

2

1

1

2

2

2

2

2

2

1.7

1

2.8

2

3.4

1

89.0

4

Pon

dic

herr

y

36

36

37

37

37

37

40

41

43

45

46

46

46

47

41.0

0

2.4

4

2.4

7

10.2

0

Chh

atti

sgar

h

0

0

0

777

795

804

812

831

839

849

866

908

956

1029

676

.14

10.7

5

65.1

3

114.6

5

Utt

aran

chal

0

0

0

10

25

10

66

1079

1188

1195

1206

1213

1221

1230

1377

1383

941

.64

10.9

0

69.3

8

112.3

7

Jhar

khan

d

0

0

0

910

940

952

954

1330

1335

1401

1442

1466

1463

1555

982

.00

12.7

7

72.4

3

88.2

5

Sou

rce:

Na

tion

al D

air

y D

evelo

pm

en

t B

oard

, 2012.

Note

:

LG

R –

Lin

ear

Gro

wth

Rate

CG

R =

Com

pou

nd G

row

th R

ate

INS

= I

nstu

bilit

y In

dex

118

In terms of compound growth rate, the order of the states

can be given as: Jharkhand (72.43 per cent), Uttaranchal (69.38

per cent), Chhattisgarh (65.13 per cent), Orissa (7.82 per cent),

Andhra Pradesh (7.15 per cent), Bihar (7.09 per cent), Rajasthan

(5.6 per cent), Gujarat (5.22 per cent), Delhi (4.45 per cent),

Tamil Nadu (4.23 per cent), Uttar Pradesh (3.85 per cent), Goa

(3.65 per cent), Himachal Pradesh (3.41 per cent), Lakshadweep

(3.41 per cent), D&N Haveli (3.29 per cent), Tripura (3.18 per

cent), Maharashtra (3.12 per cent), Nagaland (3.01 per cent),

Madhya Pradesh (2.91 per cent), Pondicherry (2.47 per cent),

Haryana (2.43 per cent), Meghalaya (2.35 per cent), Punjab (2.27

per cent), J & K (2.2 per cent), Sikkim (2.15 per cent), West

Bengal (2.15 per cent), Manipur (1.86 per cent), Assam (0.91 per

cent), A&N Islands (0.77 per cent), Chandigarh (0.77 per cent)

and Karnataka (0.71 per cent).

While the state of Daman & Diu (0 per cent) has

experienced no growth in milk production, the states like, Kerala

(-0.25 per cent), Mizoram (-2.32 per cent) and Arunachal

Pradesh (-3.97 per cent) have recorded a negative growth rate.

The instability index, a sophisticated technique to measure

stability or the volatility in the growth in production of milk by

states indicates that Meghalaya (3.54 per cent) has recorded the

119

least volatility. The order of the other states in terms of

increasing instability index can be given as: Maharashtra (4.76

per cent), Punjab (5.44 per cent), West Bengal (7.24 per cent),

Uttar Pradesh (7.6 per cent), Chandigarh (8.07 per cent),

Haryana (8.11 per cent), Manipur (8.4 per cent), J & K (8.73 per

cent), Assam (10.08 per cent), Pondicherry (10.2 per cent),

Gujarat (11.44 per cent), Goa (15.17 per cent), Himachal

Pradesh (15.9 per cent), Andhra Pradesh (17.11 per cent),

Tripura (21.22 per cent), Orissa (22.54 per cent), Tamil Nadu

(23.16 per cent), A&N Islands (23.28 per cent), Madhya Pradesh

(23.32 per cent), Rajasthan (26.45 per cent), Karnataka (29.53

per cent), Kerala (34.21 per cent), Sikkim (34.78 per cent), Delhi

(45.9 per cent), Mizoram (47.35 per cent), Nagaland (53.46 per

cent), Bihar (55.82 per cent), Arunachal Pradesh (59.8 percent),

Jharkhand (88.25 per cent), Lakshadweep (89.04 percent), D&N

Haveli (96.3 per cent), Uttaranchal (112.37 per cent) and

Chhattisgarh (114.65 per cent).

Thus from the analysis it can be concluded that all the

states, except a few have shown positive growth in the

production of milk. [Economic Survey (20050-06)]7

120

4.7.2 Ranking of States by Production Performance in Milk

The above analysis on the trends in the growth of milk

production of Indian states and the inequality in the growth as

measured by the instability indicated a mixed trend. This

means, in terms of quantity of production as measured in terms

of the average production for the study period, in terms of

growth rates and in terms of instability, different states showed

different performance and hence it is difficult to identify the

overall production performance of the states. To overcome this

problem and to understand the order of the states in terms of

their production performance, the Composite Rank Index has

been worked out. The composite Rank Index is the ranking of the

rank sum total of the indicators used to measure production

performance. The indicators used to measure the performance

are the average production of the states during the study period,

the linear and compound growth rates and the instability index.

Among these measures, the average, linear growth rate and

instability index are considered to arrive at the rank sum total.

121

Table 4.2 Composite rank index of production performance

of milk by states

States/UTs

RANKING

Average LGR Instability Rank Sum

Total

Composite

Rank

A&N Islands 31 29 20 80 32

Andhra Pradesh 4 6 16 26 3.5

Arunachal Pradesh 30 35 30 95 35

Assam 19 28 11 58 21

Bihar 11 5 29 45 11

Chandigarh 27 30 7 64 25.5

Chhattisgarh 20 3 35 58 22

D&N Haveli 33 14 33 80 31.5

Daman & Diu 35 32 1 68 27

Delhi 21 9 26 56 19.5

Goa 26 12 14 52 17

Gujarat 5 8 13 26 3.5

Haryana 9 21 8 38 9

Himachal Pradesh 18 13 15 46 12.5

J & K 14 24 10 48 16

Jharkhand 16 1 31 48 16

Karnataka 10 31 23 64 25.5

Kerala 13 33 24 70 29

Lakshadweep 34 19 32 85 33

Madhya Pradesh 7 18 21 46 12.5

Maharashtra 6 15 3 24 2

Manipur 23 27 9 59 23

Meghalaya 24 22 2 48 16

Mizoram 32 34 27 93 34

Nagaland 25 16 28 69 28

Orissa 15 4 18 37 7.5

Pondicherry 29 20 12 61 24

Punjab 3 23 4 30 5

Rajasthan 2 7 22 31 6

Sikkim 28 26 25 79 30

Tamil Nadu 8 10 19 37 7.5

Tripura 22 17 17 56 19.5

Uttar Pradesh 1 11 6 18 1

Uttaranchal 17 2 34 53 18

West Bengal 12 25 5 42 10

Source: Computed from Table5.1.

The average level of production and the linear growth rate

are ranking in the declining (descending) order of the sates while

the instability index is measured in terms of increasing

122

(ascending) value. This is so because, while the increasing

average and growth rate are indicators of favourable nature of

production, the increasing value of instability is an indication of

higher volatility which is not preferable.

The ordering or the states by each indicator and the

composite Rank Index arrived at indicates that Uttar Pradesh

has taken up the first rank in terms of milk production

performance. The order of the other states in terms of

performance can be given as: Maharashtra, Andhra Pradesh,

Gujarat, Punjab, Rajasthan, Orissa, Tamil Nadu, Haryana, West

Bengal, Bihar, Himachal Pradesh, Madhya Pradesh, Jammu and

Kashmir, Jharkhand, Meghalaya, Goa, Uttaranchal, Delhi,

Tripura, Assam, Chhattisgarh, Manipur, Pondicherry,

Chandigarh, Karnataka, Daman & Diu, Nagaland, Kerala,

Sikkim, D&N Haveli, Andhaman &Nicobar Islands,

Lakshadweep, Mizoram and Arunachal Pradesh. [Government of

India (2003)]8

Thus from the analysis it can be concluded that the overall

production performance is favourable for Uttar Pradesh.

Tamilnadu is endowed with a sizeable livestock population.

The department of Economics and Statistics conduct periodical

livestock survey in the state.

123

The following table gives an idea of the changes in the

livestock population as recorded in the 1997, 2001, and 2004.

Table 4.3 Livestock census of Tamilnadu (in lakhs)

Year Cattle Buffaloes Total

1997

2001

2004

90.47

91.82

91.41

27.41

27.08

16.58

117.88

118.90

107.99

Source: Tamilnadu – An Economic Appraisal – Various Issues.

It is possible to know from the contents of the above table

that the number of cattle remains the same, the number of

buffaloes in Tamilnadu is progressively declining from 27.4 lakhs

in 1997 to 16.58 in 2004, resulting in a total decline.

The buffaloes used to serve a dual propose to provide milk

as well as ploughing the field. With increasing mechanization of

agriculture the importance of buffaloe is slowly declining.

Further, fodder requirements in the case of buffaloes are

comparatively larger and with increasing cost of fodder, the

number of buffaloes maintained is on the decrease.

The state is very much interested in the production of milk.

The objective is to increase productivity of cattle. It is found that

with the introduction of exotic and cross breed of cow, it is

124

possible to raise, productivity by replacing the indegeous breed

with exotic and cross breed. The following table gives

information regarding the average yield rate of milk (Kgs.). per

animal/per day.

Table 4.4 Average yield rate of milk/animal in Tamilnadu

Breed 2000-01 2001-02 2002-03

Exotic and Cross breed

Indigenous

6.002

2.698

6.244

2.696

6.150

2.554

Source: Tamilnadu – An Economic Appraisal – Various Issues.

Turning to the situation in Kanyakumari district, the

following table gives the trends in the number of milk animals

enumerated in the three livestock censuses.

Table 4.5 Livestock census of Kanyakumari district (‘000)

Year Cattle Buffaloes Total

1997

2001

2004

82.656

(0.91)

101.3

(1.10)

101.712

(2.00)

14.416

(0.52)

11.9

(0.43)

6.077

(0.36)

97.072

(0.82)

113.2

(0.95)

107.789

(0.99)

Source: Tamilnadu – An Economic Appraisal – Various Issues.

125

As in the state, in the district also the proportion of

buffaloe is decreasing. It is possible to know from the contents

of the table that the district which has 2.68 percent of the state

population had 0.91 percent, 1.18 percent and 2.0 percent in

1997, 2001 and 2004 of the state’s cattle population.

Table 4.6 Estimated milk production in Tamilnadu

(in 000 tonnes)

Year

Cows

Indigenous Exotic

and cross breed

Total Buffaloes Total

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

1285.35

1266.88

1271.28

1278.58

1264.71

812.89

811.05

799.900

791.752

789.214

1811.51

1904.68

1885.77

2044.45

2102.29

3889.95

3984.17

4026.98

4121.65

4227.43

3096.86

3171.56

3157.05

3323.03

3367.00

4702.84

4795.22

4826.82

4913.40

5016.65

1811.77

1816.53

1465.22

1429.70

1416.75

770.77

765.25

759.32

760.32

761.46

4908.63

4988.09

4622.27

4752.73

4783.75

5473.61

5560.47

5568.15

5673.32

5778.11

Source: Statistical Handbook of Tamilnadu, Various Issues.

The contents of the above table show the trend in milk

production over a ten year period (2000-01 to 2009-10). It is

observed that over the period, while the contribution of buffaloes

has decreased from 811.79 tonnes to 761.461 tonnes that of

cows increased from 3096.86 tonnes to 5016.65 tonnes. It is

126

also found that while the contribution of indigenous cows

decreased from 1285.35 tonnes to 789.17 tonnes, that of exotic

and cross breed cows registered to phenomenal increase from

1311.51 tonnes to 4227.43 tonnes by 2.33 times. This reflects

the trend in substituting indigenous cows with exotic and cross

breeds of cows and the higher productivity of the latter.

(Statistical Hand Book, Tamilnadu, 2011)9

Table 4.7 Estimated milk production in Kanyakumari

district (in 000 tonnes)

Year

Cow’s Milk

Total

Buffaloes Total

Indigenous Exotic and cross breed

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

13.313

13.494

12.447

8.178

2.147

0.735

1.557

1.500

1.175

1.327

90.927

85.681

59.520

66.526

87.324

99.274

100.678

112.132

132.741

139.04

104.242

98.521

1.967

74.704

89.47

100.009

102.23

113.63

133.916

140.375

14.714

14.270

5.385

4.842

3.453

2.053

3.013

4.011

4.924

2.683

119.006

112.791

77.352

79.546

92.92

102.062

103.24

117.64

138.840

143.058

Source: Statistical Handbook of Tamilnadu, Various Issues.

The table above shows the trends in milk production in

Kanyakumari district over the ten year period. It shows

instability declining between 2002-03 and 2004-05 and then

picking up crowning the 2000-01 level in the last two years. In

127

the district also, while the contribution of indigenous cows is

declining (from 13.318 1000 tonnes in the start first 1327 tonnes

in 2009-10. The share of buffaloes has declined from 14764

tonnes to 2683 tonnes in the period. The last column shows

production in the district as a percentage of production in the

state which also shows a declining trend, from 2.42% in 2000-01

to 1.67% in 2003-04. Bettering since then and atleast

recovering to the initial level in 2008-09. Here also the decline in

the contribution of indigenous cows from the start, has been

compensated by the contribution of oxotic and cross breeds in

later years (since 2004-05).

Constraints to Expanding Milk Production

The major limiting factors to increasing India's milk

production are:

• Crop residual/byproduct ration. Opportunities to expand

milk yields by improving the quality of crop residuals and

byproducts are limited. Moreover, the demand for food grains

to feed India's large and growing population restricts the

availability of grain for dairy animals and largely precludes

displacing grain crops with green forage crops.

• Building dairy management skills. A major challenge to

expanding Indian milk production is improving cow

128

management expertise for the vast number of dairy farmers

in India. Many of these farmers are women who suffer a

lower literacy rate than the male population, making training

difficult.

• Adherence to the smallholder model. There is a mind set—

perhaps a good and reasonable mind set—that the

smallholder model must be maintained to alleviate rural

poverty. While larger, more productive dairy operations are

tolerated by government officials, they are viewed with some

skepticism because of their perceived effect on rural

employment and income distribution. But larger farms may

be necessary if demand grows rapidly and India wishes to

remain self-sufficient in milk production.

129

REFERENCES

1. Ahluwaltia, Montek S. “Reducing Poverty and Hunger in India: The Role of Agriculture. Essays: Lessons Learned from the Dragon (China) and the Elephant (India)”, Annual Report. International Food Policy Research Institute, 2005, pp. 235-238.

2. Bannerjee, A. “Dairying Systems in India”, World Annual

Review, Vol. 79. United Nations Food and Agricultural Organization. 1994, p.115.

3. Chand, R., Dairying in India: Experiences and Development Prospects, Paper presented at Australian Bureau of Agricultural Economics Seminar. August 2005, pp. 67-70.

4. Food and Agricultural Organization of the United Nations. FAO Statistical Databases, 2002, pp.5-7.

5. Foreign Agricultural Service, U.S. Department of Agriculture, Dairy: World Markets and Trade, Circular Series FD 2-05. December 2005, pp. 67-69.

6. India Dairy and Products Annual, 2005, p.95.

7. Economic Survey, 2005-06, p.35.

8. Government of India. Ministry of Agriculture, Department of Animal Husbandry, Dairying & Fisheries, Animal Husbandry Statistics.

9. Statistical Hand Book of Tamilnadu, 2011.