chapter 9: taxes on goods and services. use of goods and service tax (g&s) overall, us reliance...

TRANSCRIPT

Chapter 9:Taxes on Goods and Services

Use of goods and service tax (g&s)

Overall, US reliance on goods and services is less than in most industrialized countries

Heavier reliance on individual income, social security payroll, and corporate income taxes

Benefits of taxation on economic activity (goods and services)

1. Can provide revenue when applied to a broad base and minimize economic distortions when used in combination with other types of taxes

2. Can provide a mean to extract revenue from those with high incomes but who have evaded income tax

3. Can be used to account for the social costs (externalities) of some goods

4. May have a beneficial effect of stimulating production, since taxes consumption and therefore stimulates savings. Let’s individual make decision on what goods and services to purchase

Types of taxes on goods and services 1. General: a sales tax that applies to all

transactions, with limited exceptions (ex: food).

2. Excise: a selective sales tax that applies to specific items (ex: lodging tax in Chicago)

3. Specific Per unit - applies only to a limited number of units

purchased or sold (ex: fuel tax) Value-added (Ad valorem) – applied to the value of the

good (ex: hotel tax)

4. Can be either multi-stage (applied every transaction) or single-stage (one point in the production or consumption process)

Use of G & S tax

May be collected for use of any activity or only specific functions of government

Ex: Most motor fuel taxes are used for highway maintenance and construction

Examples of Federal Excise Taxes Transportation

(Charge for use of transportation facilities) Truck, semi Tires Aviation fuels Motor fuel Inland waterway fuels Air transport tax Use of international air travel Heavy vehicle use

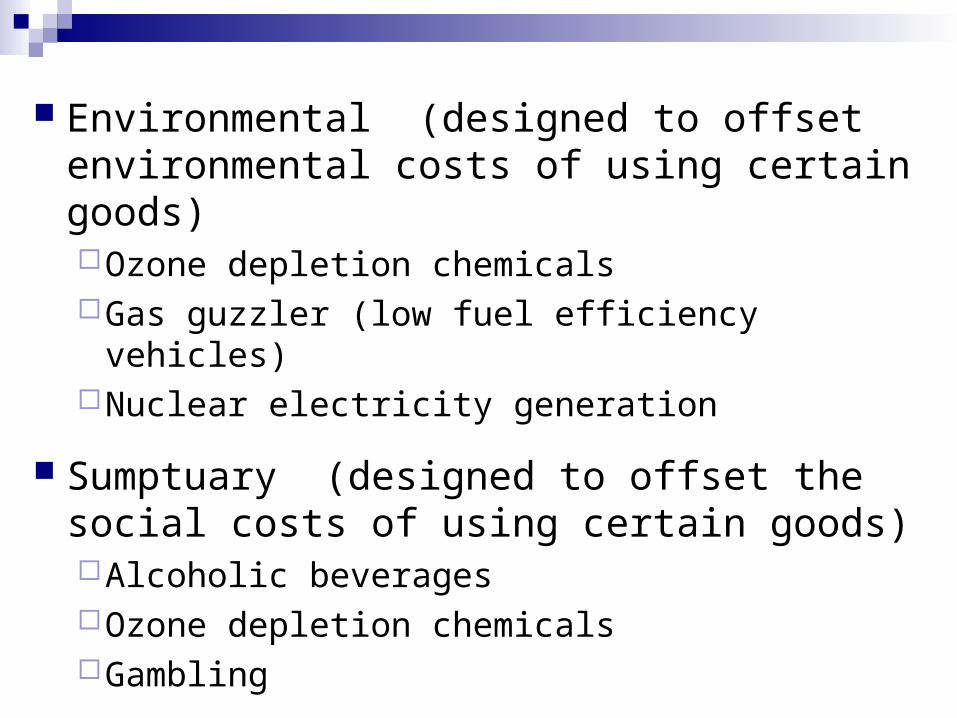

Environmental (designed to offset environmental costs of using certain goods)Ozone depletion chemicalsGas guzzler (low fuel efficiency vehicles)Nuclear electricity generation

Sumptuary (designed to offset the social costs of using certain goods)Alcoholic beveragesOzone depletion chemicalsGambling

Others (attempts to capture extraordinary ability to pay (luxury tax) or revenue from non-residents (lodging)

Luxury passenger vehicles Lodging taxes Coal Certain vaccines Telephone and teletype services Private foundation investment income Firearms and ammunition

Most revenue comes from fuel, alcohol and tobacco taxes

Use of G&S taxes As a source of Federal govt. revenues is

small Accounts for half of state and municipal

revenues come Benefit for local govt. is that G&S taxes

produce revenues even in conditions of general economic depression

Economic transactions and taxation

Creation and production of any economic good or service passes through several stages of exchange between various producers and consumers

At any level of exchange a consumption tax may apply

Some types of taxes apply to multiple levels (such as VAT)

Others only apply to a single level (either manufacturing, wholesale or retail)

Economic impact of consumption taxes

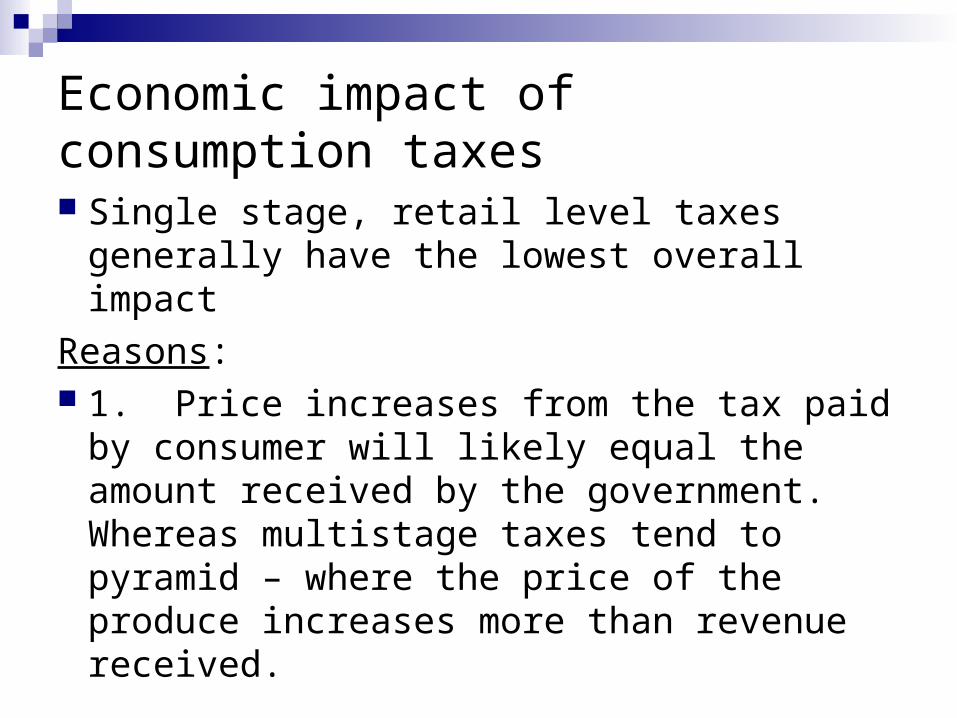

Single stage, retail level taxes generally have the lowest overall impact

Reasons: 1. Price increases from the tax paid by

consumer will likely equal the amount received by the government. Whereas multistage taxes tend to pyramid – where the price of the produce increases more than revenue received.

Example 10% excise tax on a tractor

Manufacturer sells it for $1,500 plus 10%, $1,650.

Sells to a retailer for a 50% markup (includes both the original price plus the additional tax) for $2,475.

The tax then has a balloon effect on the price of the good at each economic stage

2. Multistage taxes have an impact on each stage of a transaction. Integrated firms (that combine manufacturing, wholesale or retail) gain an advantage in the market. Distorts what would otherwise be purely economic decisions.

3. Retail application of tax only cannot be escaped by moving up the production stage. With multistage taxes, there is an incentive to avoid tax burden by combining or shifting processes.

Selective Excise Taxation

Selective excises apply differential tax treatment to specific products or services

This causes whose purchasing or selling them to bear an additional burden

Major benefit is to target specific consumers (high income) or target socially undesirable activities

Types of Excise taxes

1. Luxury-based 2. Sumptuary 3. Benefit-based 4. Regulatory & Environmental 5. Other excises

Luxury-based

Aimed at goods whose purchase reflects extraordinary purchasing power and taxpaying ability

Applied to goods such as jewelry, furs, entertainment services, expensive automobiles, aircraft, yachts

Rarely provide much in additional revenues, although have political appeal

Objections to luxury taxes

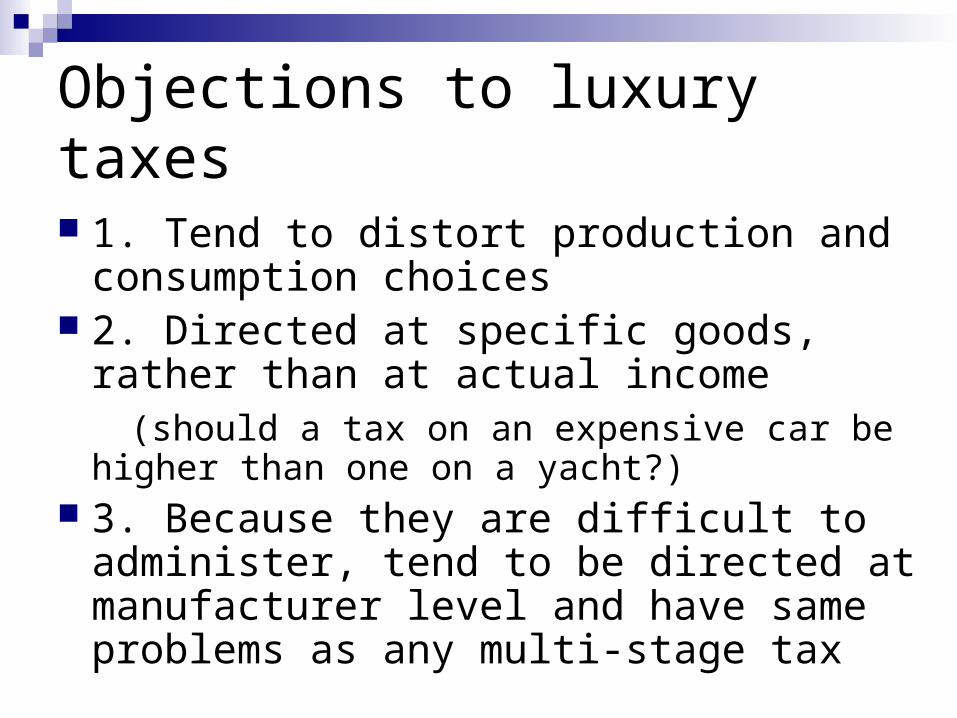

1. Tend to distort production and consumption choices

2. Directed at specific goods, rather than at actual income

(should a tax on an expensive car be higher than one on a yacht?)

3. Because they are difficult to administer, tend to be directed at manufacturer level and have same problems as any multi-stage tax

Sumptuary

Aim to discourage excess consumption of some items considered unhealthy, unsafe or immoral

Some of the oldest taxes in the US Examples: alcohol, tobacco, gambling Demand for items is often insensitive to price, so

there is a secondary incentive of providing a revenue base, so rarely are rate set so high as to completely discourage the activity

Politically attractive since they raise revenues without much public protest

Objections to sumptuary excises

1. Since consumption continues anyway, tax may divert consumption from more important consumption

2. Places a higher tax burden on lower income families

3. When administered per unit, does not distinguish brand and quality. When combined low quality brand and low income consumers, places a greater burden on low income households

Benefit-based Excises

Operates as a quasi-price for a public good

Primary example – motor fuel tax and use of highways and roads

Acts as a way to approximate a charge on road use

Is less expensive than toll collection

Drawbacks of benefit-based

Only works when there is a high degree of complementarity (use of one good always accompanies the use of a second)

During times of inflation the costs of road/highway maintenance will increase and this may not be accompanied by an increase in revenue

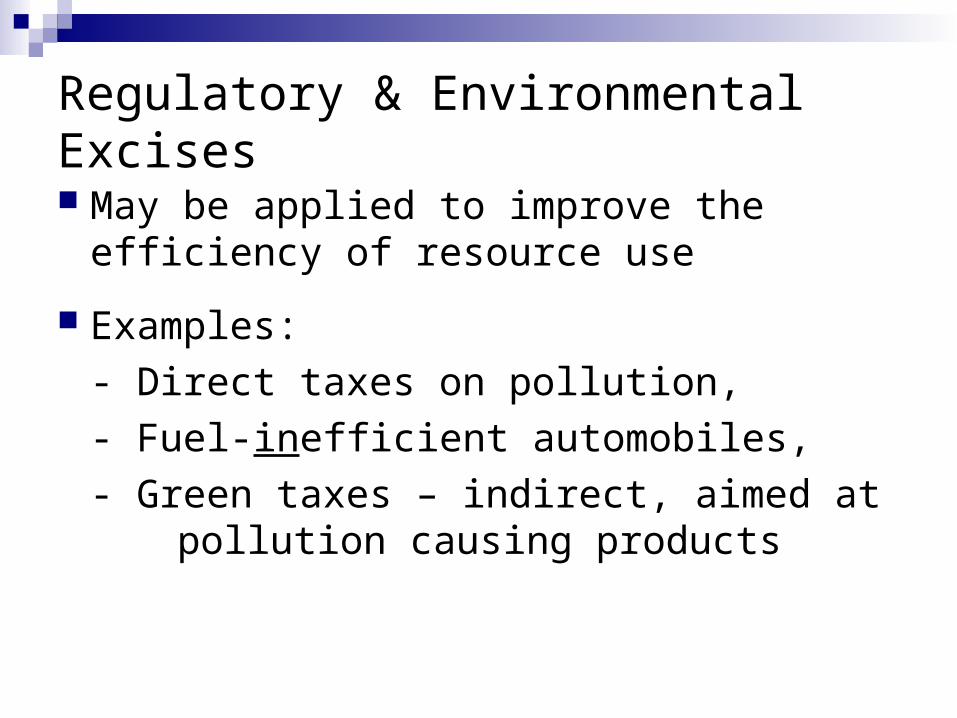

Regulatory & Environmental Excises

May be applied to improve the efficiency of resource use

Examples:

- Direct taxes on pollution,

- Fuel-inefficient automobiles,

- Green taxes – indirect, aimed at pollution causing products

Critiques of Environmental Excise Taxes Difficult to determine the appropriate

amount to charge

Green taxes are heavily used in Europe. While tend to be a more efficient means of environmental protection, US relies more heavily on old model of government regulation

Sales and value-added taxes

Consumption is the major alternative to income as a general basis for distributing the costs of government services

Proposal to shift burden from income to consumption is based on two main points:

1. Increases economic growth – may encourage savings

2. Improves fundamental equity – consumption is a good measure of tax bearing responsibility, and allows individuals to decide on resource allocation

Administration of general sales tax

Direct – uses the logic that any income not saved was spent, so only taxes the amount of spending. Because of the difficulty of verifying savings, no government currently uses.

Indirect – Can use either retail sales tax or a value-added tax (VAT)

Both retail and VAT apply a uniformed, non-pyramiding tax on household consumption

US retail tax reaches that end by taxing only the last stage of the production-consumption process

VAT Applies to each transaction in the full production-distribution process, but is refunded to businesses. Only the consumer bears the additional cost.

VAT Collected in most of the world’s developed economies, except US

Retail Sales tax American retail sales taxes have a number

of common features. All are value added (assessed according

the sale value of the item), tax is suspended when item is re-sold, all include separate quote of tax in each transaction

All states but five: Alaska, Delaware, Montana, New Hampshire, Oregon

Yield over 1/3 of state tax revenues

Two additional evaluation criteria are used for sales taxes

1. Uniformity – tax structure should produce a uniform rate to all consumption expenditures and should apply to the amount actually paid by consumers. So the burden is again on consumption, and the market distortion is less.

Ex: a general sales tax will always be preferable to a tax that targets specific types of consumption.

2. Neutrality – to avoid distortions in the distribution chain, should apply evenly to all distribution channels.

Ex: reducing the tax on wholesale purchases or by bulk.

Problems with producer’s purchases and sales taxes Consumers are not the only ones making

purchases in an economy. Producers also purchase goods and

services Taxing goods purchased by producers is a

tempting source of revenues since the tax rate is hidden from constituents (voters)

However, a tax on producer’s purchases has the same effect of any tax low on the production chain

Increases costs at any level are passed on to the next level at a multiplicative rate, increasing the overall costs of all items

May affect means of production (since purchasing capital intensive items may be more expensive) as well as creating an incentive for producers to produce their own goods rather than purchasing them on the market

Rule of thumb is to exclude producer’s purchases from sales tax whenever possible

Methods for avoiding producer taxation

1. Component-part – if an item is going to be re-sold as part of a physical ingredient in a final product it is not taxable.

Ex: Flour in bread, Engines in automobiles

2. Direct Use– exempts both ingredients and machinery used in the production of the final product. Produces a smaller tax base, but is more closely linked to final consumption.

Ex: Flour and purchasing the oven.