chapter 8-1 accounting- how it works lecture sheet by md. zamanur rahman asst. professor suggested...

TRANSCRIPT

Chapter 8-1

Accounting- How it works

Chapter 8-2

Chapter 8

Internal Control and

Bank Reconciliation

Accounting Principles, Ninth Edition

Chapter 8-3

1.1. Internal control and Bank ReconciliationInternal control and Bank Reconciliation

2.2. Internal control and Bank ReconciliationInternal control and Bank Reconciliation

3.3. Indicate the features of a bank statement.Indicate the features of a bank statement.

4.4. Prepare a bank reconciliation.Prepare a bank reconciliation.

5.5. Explain the reporting of cash.Explain the reporting of cash.

Study ObjectivesStudy ObjectivesStudy ObjectivesStudy Objectives

Chapter 8-4

FraudFraud

The Sarbanes-The Sarbanes-Oxley ActOxley Act

Internal controlInternal control

Principles of Principles of internal controlinternal control

LimitationsLimitations

Cash equivalentsCash equivalents

Restricted cashRestricted cash

Compensating Compensating balancesbalances

Making depositsMaking deposits

Writing checksWriting checks

Bank statementsBank statements

Reconciling the Reconciling the bank accountbank account

Electronic funds Electronic funds transfer (EFT) transfer (EFT) systemsystem

Cash receipts Cash receipts controlscontrols

Cash Cash disbursements disbursements controlscontrols

Fraud and Fraud and Internal ControlInternal Control

Fraud and Fraud and Internal ControlInternal Control Cash ControlsCash ControlsCash ControlsCash Controls

Control Control Features: Use of Features: Use of

a Banka Bank

Control Control Features: Use of Features: Use of

a Banka BankReporting CashReporting CashReporting CashReporting Cash

Fraud, Internal Control, and CashFraud, Internal Control, and CashFraud, Internal Control, and CashFraud, Internal Control, and Cash

Chapter 8-5

Methods and measures adopted to:

1. Safeguard assets.

2. Enhance accuracy and reliability of accounting records.

3. Increase efficiency of operations, and

4. Ensure compliance with laws and regulations.

Internal ControlInternal ControlInternal ControlInternal Control

SO 1 Define fraud and internal control.SO 1 Define fraud and internal control.

Under the Sarbanes-Oxley Act, all publicly traded U.S. corporations are required to maintain an adequate system of

internal control.

Internal ControlInternal Control

Chapter 8-6

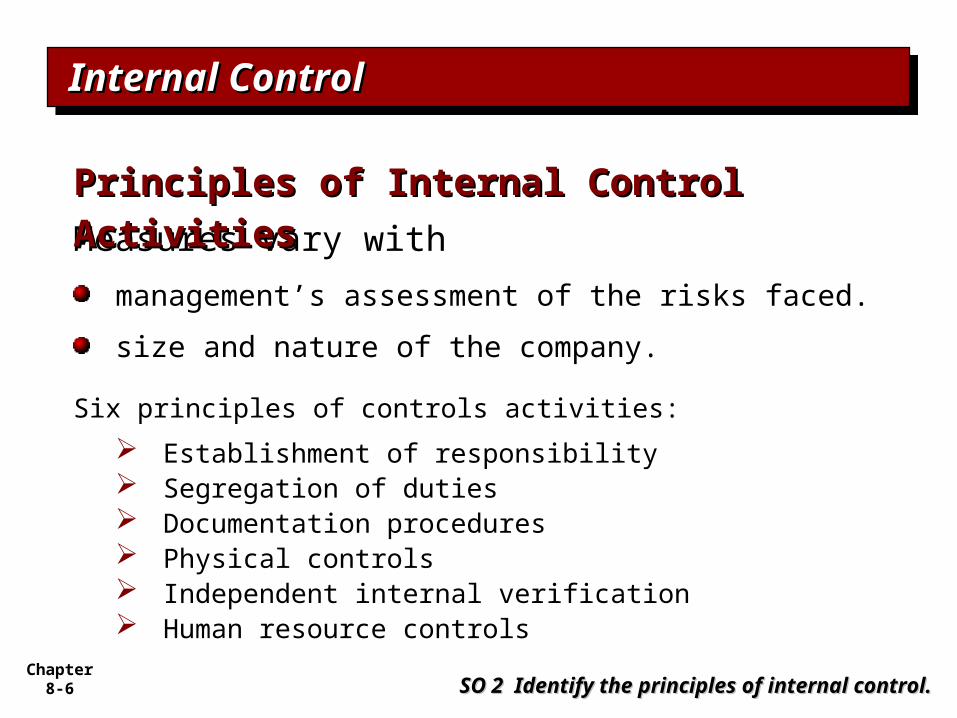

Measures vary with

management’s assessment of the risks faced.

size and nature of the company.

SO 2 Identify the principles of internal control.SO 2 Identify the principles of internal control.

Principles of Internal Control Principles of Internal Control ActivitiesActivities

Internal ControlInternal ControlInternal ControlInternal Control

Six principles of controls activities:

Establishment of responsibility Segregation of duties Documentation procedures Physical controls Independent internal verification Human resource controls

Chapter 8-7 SO 2 Identify the principles of internal control.SO 2 Identify the principles of internal control.

Limitations of Internal ControlLimitations of Internal Control

Costs should not exceed benefit.

Human element.

Size of the business.

Internal ControlInternal ControlInternal ControlInternal Control

Chapter 8-8

Contributes to good internal control over cash.

Minimizes the amount of currency on hand.

Creates a double record of bank transactions.

Bank reconciliation.

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

SO 6 Indicate the control features of a bank account.SO 6 Indicate the control features of a bank account.

Chapter 8-9

BANK STATEMENTSSTUDY OBJECTIVE STUDY OBJECTIVE 11

A A bank statementbank statement shows:shows:11 Checks paid and other debits charged Checks paid and other debits charged

against the accountagainst the account

22 Deposits and other credits made to the Deposits and other credits made to the accountaccount

33 Account balance after each day’s Account balance after each day’s transactionstransactions

A A bank statementbank statement shows:shows:11 Checks paid and other debits charged Checks paid and other debits charged

against the accountagainst the account

22 Deposits and other credits made to the Deposits and other credits made to the accountaccount

33 Account balance after each day’s Account balance after each day’s transactionstransactions

Chapter 8-10

Bank Statements

Debit Memorandum

Bank service charge

NSF (not sufficient funds)

SO 6 Indicate the control features of a bank account.SO 6 Indicate the control features of a bank account.

Illustration 8-10

Credit Memorandum

Collect notes receivable.

Interest earned.

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-11

Reconciling the Bank Account

SO 7 Prepare a bank reconciliation.SO 7 Prepare a bank reconciliation.

Reconcile balance per books and balance per bank to their adjusted (corrected) cash balances.

Reconciling Items:

1. Deposits in transit.

2. Outstanding checks.

3. Errors.

4. Bank memoranda.

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-12

Reconciliation Procedures

SO 7 Prepare a bank reconciliation.SO 7 Prepare a bank reconciliation.

+ Deposit in Transit

- Outstanding Checks

+- Bank Errors

+ Notes collected by bank

- NSF (bounced) checks

- Check printing or other service charges

+- Company Errors

CORRECT BALANCE CORRECT BALANCE

Illustration 8-11

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-13

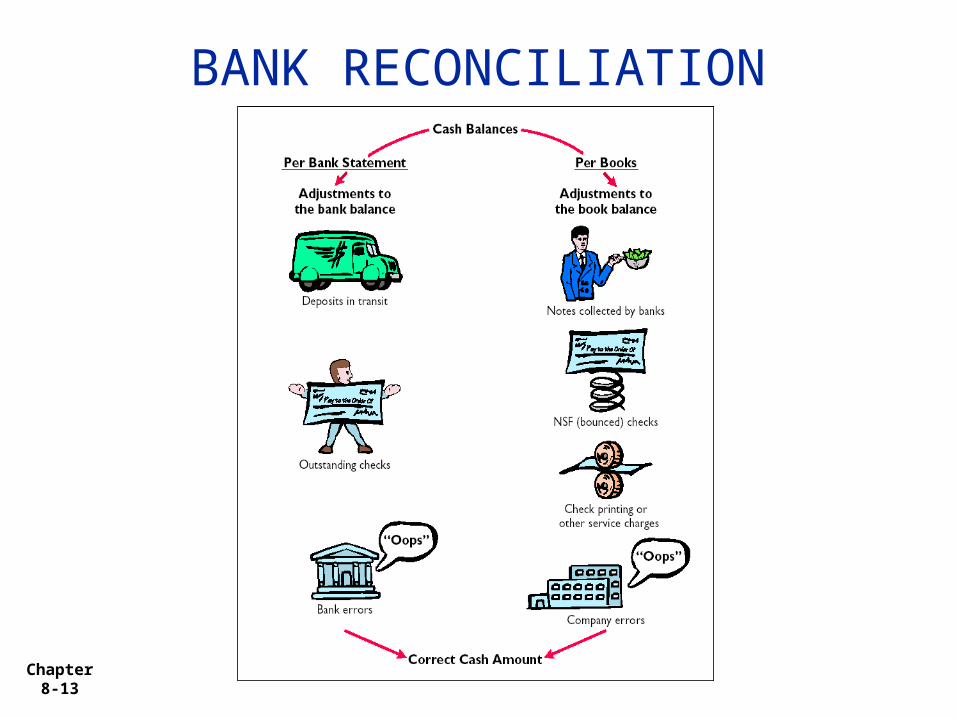

BANK RECONCILIATION

Chapter 8-14

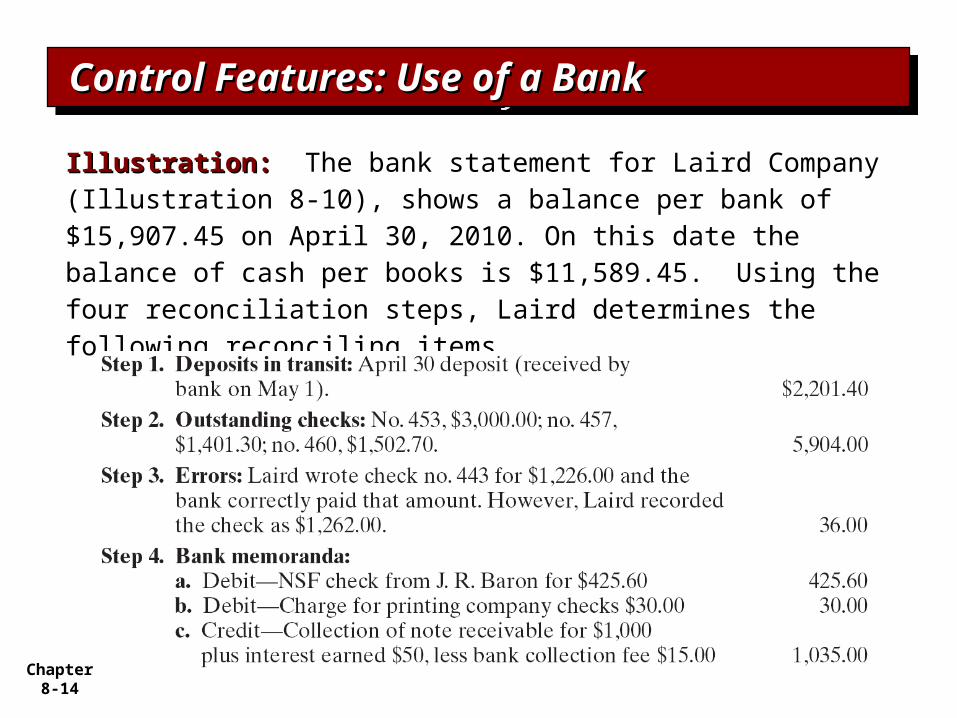

Illustration: Illustration: The bank statement for Laird Company (Illustration 8-10), shows a balance per bank of $15,907.45 on April 30, 2010. On this date the balance of cash per books is $11,589.45. Using the four reconciliation steps, Laird determines the following reconciling items.

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-15

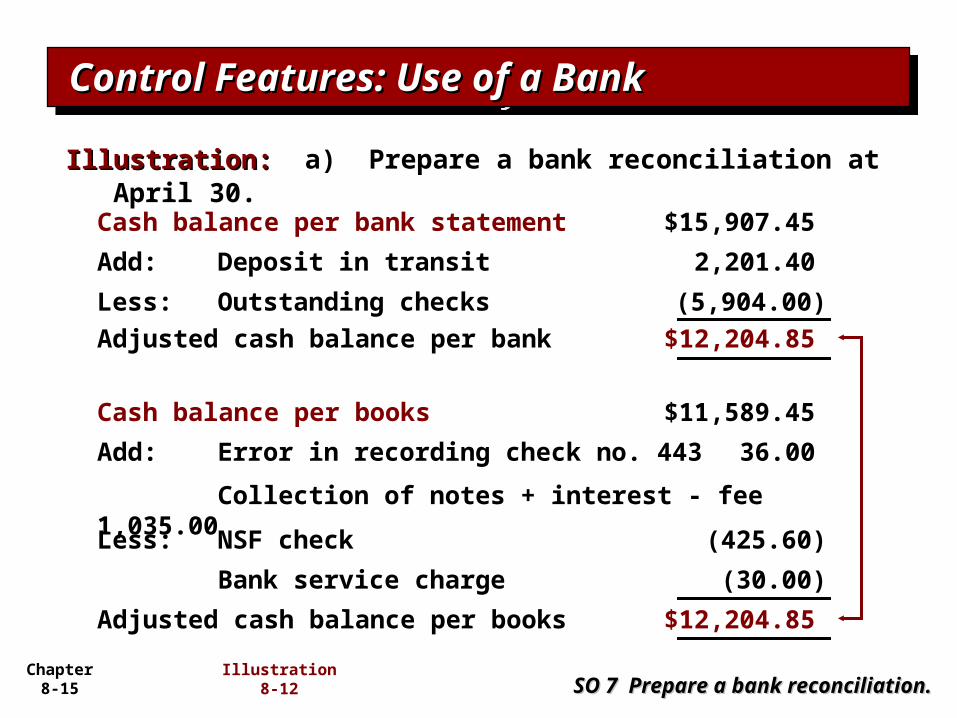

Illustration: Illustration: a) Prepare a bank reconciliation at April 30.

SO 7 Prepare a bank reconciliation.SO 7 Prepare a bank reconciliation.

Cash balance per bank statement $15,907.45

Add: Deposit in transit 2,201.40

Less: Outstanding checks (5,904.00)

Adjusted cash balance per bank $12,204.85

Cash balance per books $11,589.45

Collection of notes + interest - fee 1,035.00

Add: Error in recording check no. 443 36.00

Less: NSF check (425.60)

Bank service charge (30.00)

Adjusted cash balance per books $12,204.85

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Illustration 8-12

Chapter 8-16

The company records each reconciling item used to determine the adjusted cash balance per books.

Collection of Note Receivable: Assuming interest of $50 has not been accrued and collection fee is charged to Miscellaneous Expense, the entry is:

SO 5 Describe the operation of a petty cash fund.SO 5 Describe the operation of a petty cash fund.

Cash 1,035.00Apr. 30

Miscellaneous expense 15.00

Notes receivable1,000.00Interest revenue

50.00

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-17

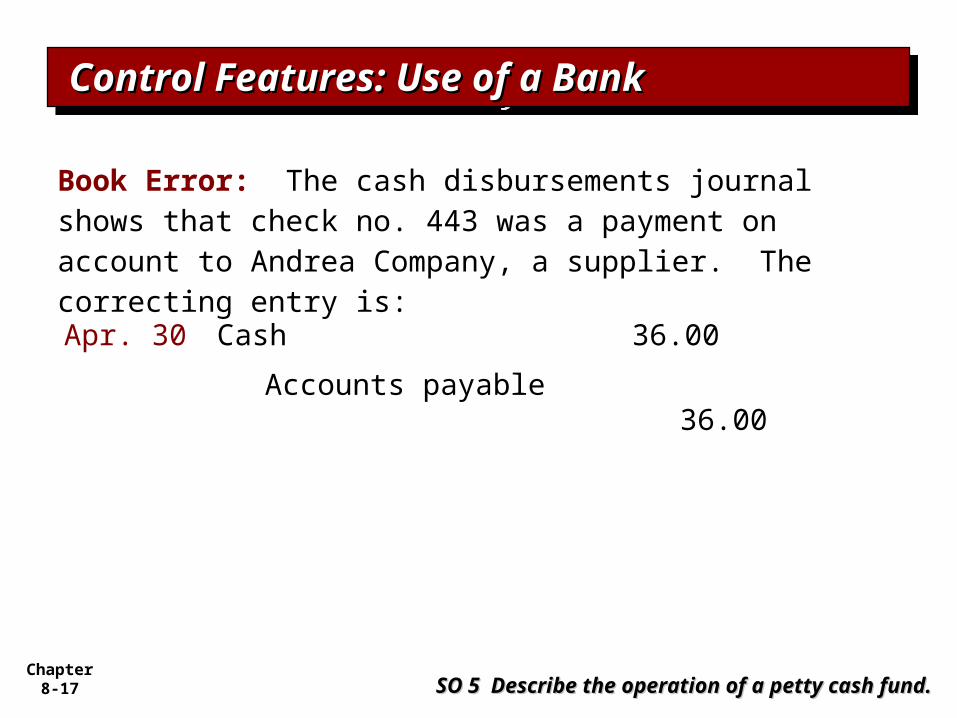

Book Error: The cash disbursements journal shows that check no. 443 was a payment on account to Andrea Company, a supplier. The correcting entry is:

SO 5 Describe the operation of a petty cash fund.SO 5 Describe the operation of a petty cash fund.

Cash 36.00Apr. 30

Accounts payable36.00

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-18

NSF Check: As indicated earlier, an NSF check becomes an account receivable to the depositor. The entry is:

SO 5 Describe the operation of a petty cash fund.SO 5 Describe the operation of a petty cash fund.

Accounts receivable 425.60Apr. 30

Cash425.60

Bank Service Charges: Depositors debit check printing charges (DM) and other bank service charges (SC) to Miscellaneous Expense. The entry is:

Miscellaneous 30.00Apr. 30

Cash30.00

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-19

The reconciling item in a bank reconciliation that will result in an adjusting entry by the depositor is:

a. outstanding checks.

b. deposit in transit.

c. a bank error.

d. bank service charges.

Review QuestionReview Question

SO 7 Prepare a bank reconciliation.SO 7 Prepare a bank reconciliation.

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-20

Electronic Funds Transfers (EFT)

Disbursement systems that uses wire, telephone, or computers to transfer cash balances between locations.

EFT transfers normally result in better internal control since no cash or checks are handled by company employees.

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

SO 7 Prepare a bank reconciliation.SO 7 Prepare a bank reconciliation.

Chapter 8-21

Q8-23. Lori Figgs is confused about the lack of agreement between the cash balance per books and the balance per the bank. Explain the causes for the lack of agreement to Lori, and give an example of each cause.

See notes page for discussion

Discussion QuestionDiscussion Question

SO 7 Prepare a bank reconciliation.SO 7 Prepare a bank reconciliation.

Control Features: Use of a BankControl Features: Use of a BankControl Features: Use of a BankControl Features: Use of a Bank

Chapter 8-22

Reporting CashReporting CashReporting CashReporting Cash

SO 8 Explain the reporting of cash.SO 8 Explain the reporting of cash.

Cash consists of coins, currency (paper money), checks, money orders, and money on hand or on deposit in a bank or similar depository.

Cash equivalents

Restricted cash

Compensating balances

Illustration 8-14

Chapter 8-23

Which of the following statements correctly describes the reporting of cash?

a. Cash cannot be combined with cash equivalents.

b. Restricted cash funds may be combined with Cash.

c. Cash is listed first in the current assets section.

d. Restricted cash funds cannot be reported as a current asset.

Review QuestionReview Question

Reporting CashReporting CashReporting CashReporting Cash

SO 8 Explain the reporting of cash.SO 8 Explain the reporting of cash.