chapter 6: real estate market analysis 1 © 2014 oncourse learning. all rights reserved

TRANSCRIPT

Chapter 6:

Real Estate Market Analysis

1© 2014 OnCourse Learning. All Rights Reserved.

2

R.E. “Market Analysis”

is a collection of practical analytical tools and procedures designed to help answer decision questions, such as:

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

3

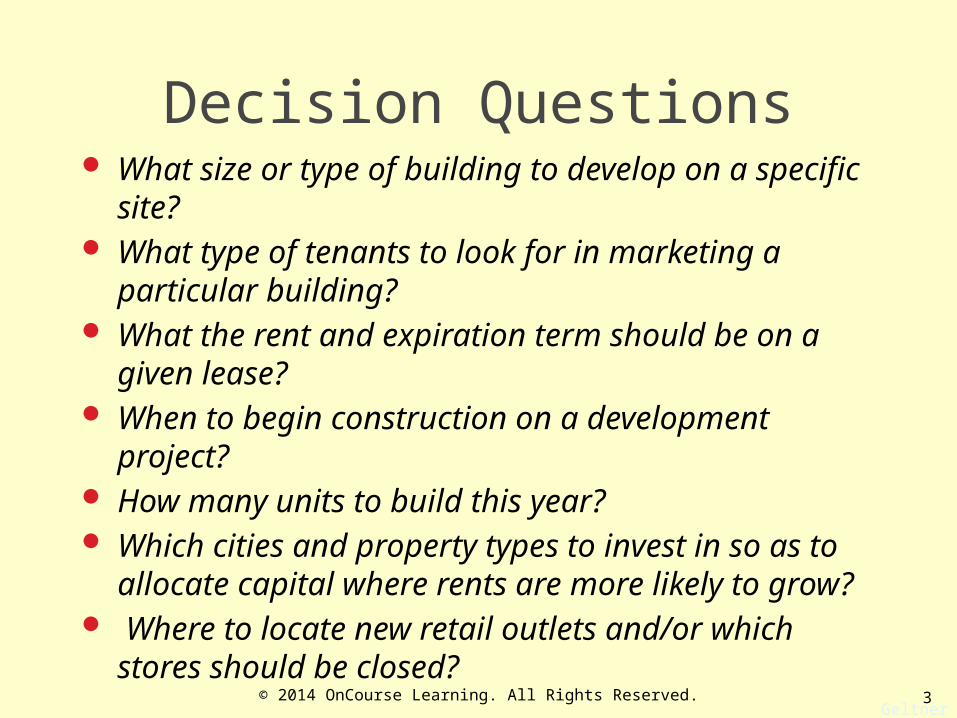

Decision Questions What size or type of building to develop on a specific site? What type of tenants to look for in marketing a particular

building? What the rent and expiration term should be on a given

lease? When to begin construction on a development project? How many units to build this year? Which cities and property types to invest in so as to

allocate capital where rents are more likely to grow? Where to locate new retail outlets and/or which stores

should be closed?

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

4

Market Analysis usually requires quantitative or qualitative understanding

(& prediction) of:

Demand Side

Supply Side

of the Space Usage Market relevant to some R.E. decision.

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

5

Two Major Types (levels) of Market Analysis:

Specific micro-level analysis Applies to single property, site, or user E.g., feasibility analysis or site analysis for a

development project “shoe leather…” (also mktg consultants like Claritas)

Broader, more general characterization of a space market Applies to an entire R.E. space market segment or

submarket E.g., forecast of supply & demand (&/or rents and

vacancy rates) in Chicago office market, or Class A office Mkt in downtown Chicago

“research shops” (or subscriptions)

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

6

General market-level analyses focus onFive major market indicators:

1. Vacancy rate

2. Market Rent

3. Quantity of new construction starts

4. Quantity of new construction completions

5. Absorption of new space

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

7

Vacancy Rate: Percentage of the stock of space that is currently not

occupied Vac.Rate = (Empty SF)/(Total SF) = 1 – Occup.Rate

Watch out for sub-lease space: Space leased but unoccupied is vacant.

Vacancy Rate is an indicator of equilibrium (balance between supply & demand in the space market)

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

8

Some vacancy is normal and natural in a market, due to:

Search time & moving costs (hence LT leases): Don’t take “first deal” Search for “good deal” (takes time to find) More uncertainty LL sets higher reservation rent (but

tenant sets lower rent target, so deals tougher). Higher moving costs or search costs LL sets lower

reservation rent (& tenant accepts higher rent target, so deals easier, longer term leases).

“Overbuilding”: Impossible to perfectly predict demand growth “Lumpy supply”

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

9

The “natural vacancy rate”:

Rate around which vacancy tends to cycle Rate that indicates supply/demand balance Above which rents fall, below which rents rise Tends to be higher in more volatile & faster-growth

markets Tends to be lower in more supply-restricted markets

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

10

Boston Office Sub-Markets Vacancy Rate: 1989-2009

0%

5%

10%

15%

20%

25%

30%19

89

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Suburban CBD Cambridge

What does it look like the natural vacancy rate is in the Boston office market?Is it higher in the CBD or the suburbs?

© 2014 OnCourse Learning. All Rights Reserved.

11

Rent:

Rent on new leases in the market Another equilibrium variable (along with vacancy

rate) Most important space market variable Tricky to accurately quantify (private info,“apples

vs oranges” problems) Watch out for “asking rent” vs. “effective rent”

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

12

Example:

$10 rent but 1-yr abatement in 5-yr lease:

What would you say is the “effective rent”?

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

13

Example:

$10 rent but 1-yr abatement in 5-yr lease:

What would you say is the “effective rent”?

10*(4/5) = $8.

Or, more carefully, if tenant can borrow @ 8%:

=PMT(0.08,5,NPV(0.08,10,10,10,10)) = $8.30.

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

14

Consider “real rent”

rent adjusted for general inflation (as better indicator of market trend)

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

15

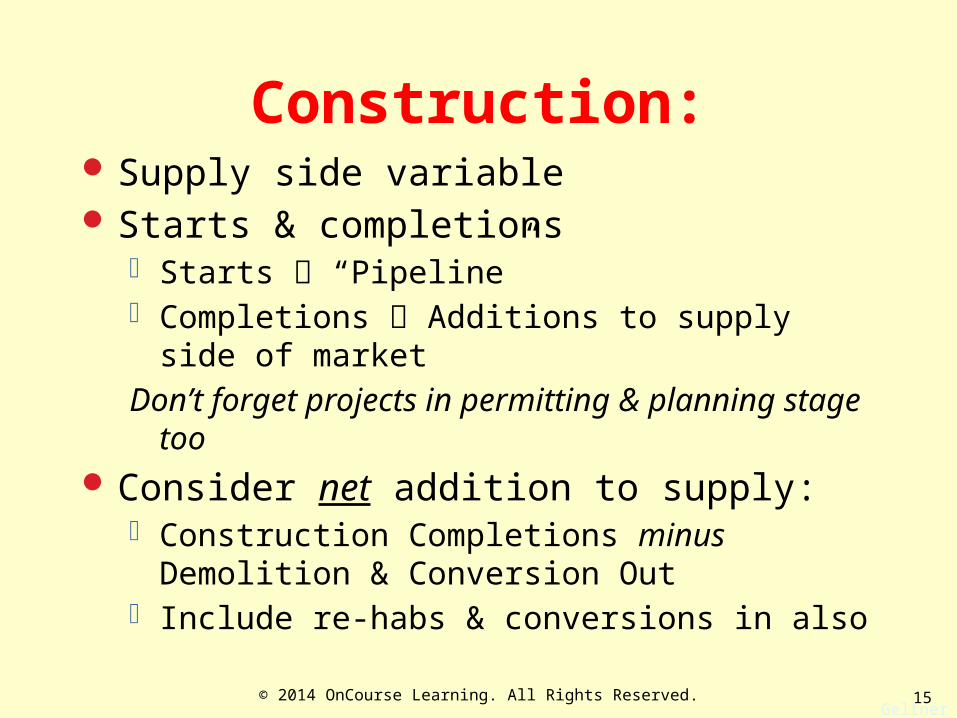

Construction: Supply side variable Starts & completions

Starts “Pipeline” Completions Additions to supply side of market

Don’t forget projects in permitting & planning stage too Consider net addition to supply:

Construction Completions minus Demolition & Conversion Out

Include re-habs & conversions in also

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

16

Absorption: Change in occupied space Demand side variable “Gross absorption” = Total new lease signings

Includes moves within the market “Net absorption” = Net increase in occupied

space Net absorption more relevant for indicating

market demand: (Vacant SF)t = (Vacant SF)t-1

+ (Constr)t – (Net Absorption)t

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

17

These market indicator variables:

Vacancy, Rent, Construction, Absorption

Can be used to help characterize & understand the current market, and forecast how it may change relevant to R.E. decisions.

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

18

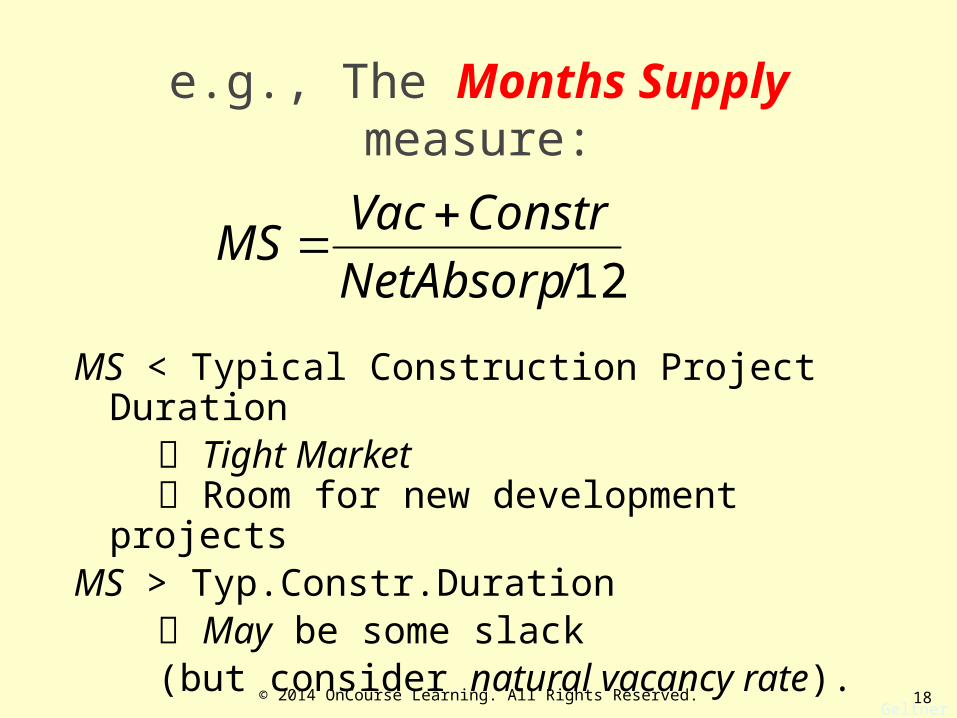

e.g., The Months Supply measure:

MS < Typical Construction Project Duration Tight Market Room for new development projects

MS > Typ.Constr.Duration May be some slack (but consider natural vacancy rate).

12/NetAbsorp

ConstrVacMS

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

19

Perhaps enhance with aMonths Excess Supply measure?...

Compare this to typical construction time and what is in pipeline…

12/

%%

FNetAbsorpS

ConstrSFStockSFNatVacVacMES

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

© 2014 OnCourse Learning. All Rights Reserved. 20

WASHINGTON DC

NEW YORK

LOS ANGELES

SAN FRANCISCO

DALLAS / FORT WORTH

ATLANTA

BOSTON

CHICAGO

HOUSTON

9.28

6.29

6.19

5.57

4.68

4.53

3.32

3.01

2.51

10.05

7.56

4.95

5.89

4.82

6.53

4.16

2.86

2.02

1998-2000 ANNUAL AVG 2001-2004F ANNUAL AVG

Absorption in Largest U.S. Multi-Tenant Office Markets

Source: Torto Wheaton Research. Millions of square feet. Forecast 2001-2004

21

Co

nst

ruct

ion

, Ab

sorp

tio

n, &

Vac

ancy

(sa

me

sc

ale

ac

ros

s 3

me

tro

s)

0%2%4%6%8%10%12%14%16%18%20%22%24%26%28%

0

10

20

30

40

50

60

70

80

90

1986Q3

1987Q3

1988Q3

1989Q3

1990Q3

1991Q3

1992Q3

1993Q3

1994Q3

1995Q3

1996Q3

1997Q3

1998Q3

1999Q3

2000Q3

2001Q3

2002Q3

2003Q3

2004Q3

2005Q3

2006Q3

2007Q3

2008Q3

2009Q3

2010Q3

Gro

ss A

skin

g Re

nt ($

/SF-

YR)

New York

Real Rent (constant 2011 dollars) Vacancy (Right Axis)

0%2%4%6%8%10%12%14%16%18%20%22%24%26%28%

0

10

20

30

40

50

60

70

80

90

1986Q3

1987Q3

1988Q3

1989Q3

1990Q3

1991Q3

1992Q3

1993Q3

1994Q3

1995Q3

1996Q3

1997Q3

1998Q3

1999Q3

2000Q3

2001Q3

2002Q3

2003Q3

2004Q3

2005Q3

2006Q3

2007Q3

2008Q3

2009Q3

2010Q3

Gro

ss A

skin

g Re

nt ($

/SF-

YR)

San Francisco

Real Rent (constant 2011 dollars) Vacancy (Right Axis)

0%2%4%6%8%10%12%14%16%18%20%22%24%26%28%

0

10

20

30

40

50

60

70

80

90

1986Q3

1987Q3

1988Q3

1989Q3

1990Q3

1991Q3

1992Q3

1993Q3

1994Q3

1995Q3

1996Q3

1997Q3

1998Q3

1999Q3

2000Q3

2001Q3

2002Q3

2003Q3

2004Q3

2005Q3

2006Q3

2007Q3

2008Q3

2009Q3

2010Q3

Gro

ss A

skin

g Re

nt ($

/SF-

YR)

Atlanta

Real Rent (constant 2011 dollars) Vacancy (Right Axis)

Vac

ancy

& R

ent

(sa

me

sc

ale

ac

ros

s 3

me

tro

s)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1982Q1

1983Q1

1984Q1

1985Q1

1986Q1

1987Q1

1988Q1

1989Q1

1990Q1

1991Q1

1992Q1

1993Q1

1994Q1

1995Q1

1996Q1

1997Q1

1998Q1

1999Q1

2000Q1

2001Q1

2002Q1

2003Q1

2004Q1

2005Q1

2006Q1

2007Q1

2008Q1

2009Q1

2010Q1

2011Q1

Vaca

ncy

as P

erce

nt o

f Exi

sting

Sto

ck

Cons

truc

tion

& A

bsor

ption

As P

erce

nt o

f Exi

sting

Sto

ck a

t A

nnua

lized

Rat

e

New York

Construction Completions (Left Axis) Avg 0.7%/yr Absorption (Left Axis) Avg 0.3%/yr Vacancy (Right Axis) Avg 11.3%

(Note: 2001Q3 is -17% & -19% (ann ra te) for construction & absorption due to 9/11 terrorist a ttack.)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1982Q1

1983Q1

1984Q1

1985Q1

1986Q1

1987Q1

1988Q1

1989Q1

1990Q1

1991Q1

1992Q1

1993Q1

1994Q1

1995Q1

1996Q1

1997Q1

1998Q1

1999Q1

2000Q1

2001Q1

2002Q1

2003Q1

2004Q1

2005Q1

2006Q1

2007Q1

2008Q1

2009Q1

2010Q1

2011Q1

Vaca

ncy

as P

erce

nt o

f Exi

sting

Sto

ck

Cons

truc

tion

& A

bsor

ption

As P

erce

nt o

f Exi

sting

Sto

ck a

t A

nnua

lized

Rat

e

San Francisco

Construction Completions (Left Axis) Avg 2.5%/yr Absorption (Left Axis) Avg 1.6%/yr Vacancy (Right Axis) Avg 13.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1982Q1

1983Q1

1984Q1

1985Q1

1986Q1

1987Q1

1988Q1

1989Q1

1990Q1

1991Q1

1992Q1

1993Q1

1994Q1

1995Q1

1996Q1

1997Q1

1998Q1

1999Q1

2000Q1

2001Q1

2002Q1

2003Q1

2004Q1

2005Q1

2006Q1

2007Q1

2008Q1

2009Q1

2010Q1

2011Q1

Vaca

ncy

as P

erce

nt o

f Exi

sting

Sto

ck

Cons

truc

tion

& A

bsor

ption

As P

erce

nt o

f Exi

sting

Sto

ck a

t A

nnua

lized

Rat

e

Atlanta

Construction Completions (Left Axis) Avg 4.3%/yr Absorption (Left Axis) Avg 3.1%/yr Vacancy (Right Axis) Avg 17.5%

22

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1986Q3

1987Q3

1988Q3

1989Q3

1990Q3

1991Q3

1992Q3

1993Q3

1994Q3

1995Q3

1996Q3

1997Q3

1998Q3

1999Q3

2000Q3

2001Q3

2002Q3

2003Q3

2004Q3

2005Q3

2006Q3

2007Q3

2008Q3

2009Q3

2010Q3

Gro

ss A

skin

g Re

nt ($

/mo/

unit

, Con

stan

t 201

0 $

)

Apartment Market Asking Rents Net of Inflation: 1986-2011, Seven Metros

Atl

Bos

Chi

Dal

NY

SF

DC

Source: CoStar Group

Recall from Chapter 1: Space markets are “segmented” – different rents can prevail @ same time in different

locations, or for different types of uses.

© 2014 OnCourse Learning. All Rights Reserved.

23

Recall from Chapter 1: Space markets are “segmented” – different rents can prevail @ same time in different

locations, or for different types of uses.

0

10

20

30

40

50

60

70

80

90

1986Q3

1987Q3

1988Q3

1989Q3

1990Q3

1991Q3

1992Q3

1993Q3

1994Q3

1995Q3

1996Q3

1997Q3

1998Q3

1999Q3

2000Q3

2001Q3

2002Q3

2003Q3

2004Q3

2005Q3

2006Q3

2007Q3

2008Q3

2009Q3

2010Q3

Gro

ss A

skin

g Re

nt ($

/mo/

unit

, Con

stan

t 201

0 $

)

Office Market Asking Rents Net of Inflation: 1986-2011, Seven Metros

Atl

Bos

Chi

Dal

NY

SF

DC

Source: CoStar Group

© 2014 OnCourse Learning. All Rights Reserved.

Defining the scope of the market analysis…

Geographic/Property type market segments (or sub-markets)

Time-frame of the study (historical, forecast to when?)

24© 2014 OnCourse Learning. All Rights Reserved.

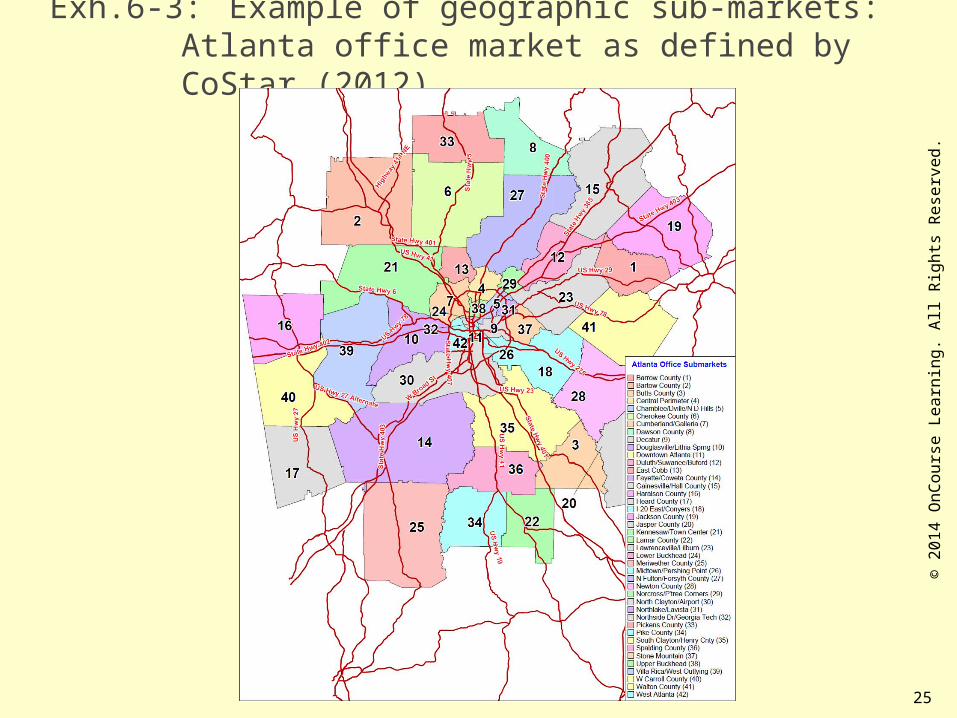

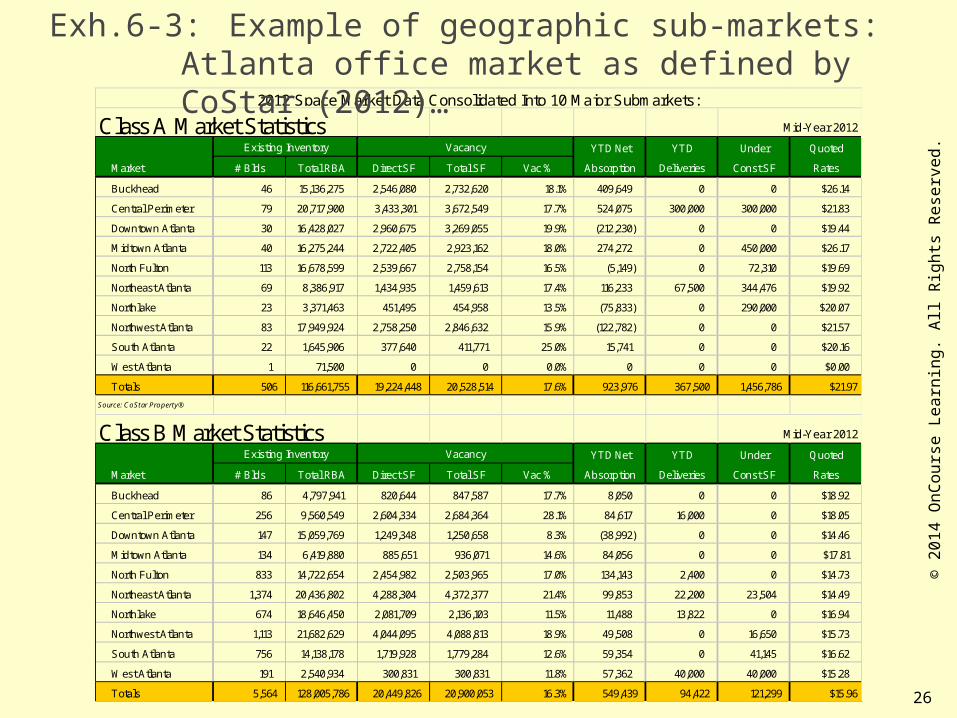

Exh.6-3: Example of geographic sub-markets: Atlanta office market as defined by CoStar (2012)…

25

© 2

014

OnC

ours

e Le

arni

ng. A

ll Ri

ghts

Res

erve

d.

Class A Market Statistics Mid-Year 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Buckhead 46 15,136,275 2,546,080 2,732,620 18.1% 409,649 0 0 $26.14

Central Perimeter 79 20,717,900 3,433,301 3,672,549 17.7% 524,075 300,000 300,000 $21.83

Downtown Atlanta 30 16,428,027 2,960,675 3,269,055 19.9% (212,230) 0 0 $19.44

Midtown Atlanta 40 16,275,244 2,722,405 2,923,162 18.0% 274,272 0 450,000 $26.17

North Fulton 113 16,678,599 2,539,667 2,758,154 16.5% (5,149) 0 72,310 $19.69

Northeast Atlanta 69 8,386,917 1,434,935 1,459,613 17.4% 116,233 67,500 344,476 $19.92

Northlake 23 3,371,463 451,495 454,958 13.5% (75,833) 0 290,000 $20.07

Northwest Atlanta 83 17,949,924 2,758,250 2,846,632 15.9% (122,782) 0 0 $21.57

South Atlanta 22 1,645,906 377,640 411,771 25.0% 15,741 0 0 $20.16

West Atlanta 1 71,500 0 0 0.0% 0 0 0 $0.00

Totals 506 116,661,755 19,224,448 20,528,514 17.6% 923,976 367,500 1,456,786 $21.97

Source: CoStar Property®

Class B Market Statistics Mid-Year 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Buckhead 86 4,797,941 820,644 847,587 17.7% 8,050 0 0 $18.92

Central Perimeter 256 9,560,549 2,604,334 2,684,364 28.1% 84,617 16,000 0 $18.05

Downtown Atlanta 147 15,059,769 1,249,348 1,250,658 8.3% (38,992) 0 0 $14.46

Midtown Atlanta 134 6,419,880 885,651 936,071 14.6% 84,056 0 0 $17.81

North Fulton 833 14,722,654 2,454,982 2,503,965 17.0% 134,143 2,400 0 $14.73

Northeast Atlanta 1,374 20,436,802 4,288,304 4,372,377 21.4% 99,853 22,200 23,504 $14.49

Northlake 674 18,646,450 2,081,709 2,136,103 11.5% 11,488 13,822 0 $16.94

Northwest Atlanta 1,113 21,682,629 4,044,095 4,088,813 18.9% 49,508 0 16,650 $15.73

South Atlanta 756 14,138,178 1,719,928 1,779,284 12.6% 59,354 0 41,145 $16.62

West Atlanta 191 2,540,934 300,831 300,831 11.8% 57,362 40,000 40,000 $15.28

Totals 5,564 128,005,786 20,449,826 20,900,053 16.3% 549,439 94,422 121,299 $15.96

Existing Inventory Vacancy

Existing Inventory Vacancy

2012 Space Market Data Consolidated Into 10 Major Submarkets:

Exh.6-3: Example of geographic sub-markets: Atlanta office market as defined by CoStar (2012)…

26

© 2

014

OnC

ours

e Le

arni

ng. A

ll Ri

ghts

Res

erve

d.

Exh.6-3: Example of geographic sub-markets: Atlanta office market as defined by CoStar (2012)…

Class C Market Statistics Mid-Year 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Buckhead 259 1,849,733 140,517 140,517 7.6% (814) 0 0 $18.01

Central Perimeter 371 3,242,745 489,551 489,551 15.1% 33,846 0 0 $13.90

Downtown Atlanta 221 4,762,046 885,019 885,019 18.6% 40,760 0 0 $15.42

Midtown Atlanta 232 1,722,184 141,457 152,881 8.9% (4,861) 0 0 $15.72

North Fulton 852 4,315,854 466,578 468,743 10.9% 98,111 0 0 $12.88

Northeast Atlanta 1,634 8,417,983 1,100,365 1,103,960 13.1% (3,853) 0 0 $13.08

Northlake 1,603 9,065,346 698,939 701,635 7.7% 79,970 0 0 $13.44

Northwest Atlanta 1,748 9,303,317 983,138 987,399 10.6% 83,859 0 0 $13.69

South Atlanta 1,650 8,575,900 1,007,506 1,007,506 11.7% 39,149 0 0 $13.71

West Atlanta 475 3,201,587 928,581 928,581 29.0% 27,561 0 0 $11.89

Totals 9,045 54,456,695 6,841,651 6,865,792 12.6% 393,728 0 0 $13.68

Source: CoStar Property®

Total Office Market Statistics Mid-Year 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Buckhead 391 21,783,949 3,507,241 3,720,724 17.1% 416,885 0 0 $24.32

Central Perimeter 706 33,521,194 6,527,186 6,846,464 20.4% 642,538 316,000 300,000 $19.95

Downtown Atlanta 398 36,249,842 5,095,042 5,404,732 14.9% (210,462) 0 0 $17.99

Midtown Atlanta 406 24,417,308 3,749,513 4,012,114 16.4% 353,467 0 450,000 $24.10

North Fulton 1,798 35,717,107 5,461,227 5,730,862 16.0% 227,105 2,400 72,310 $17.15

Northeast Atlanta 3,077 37,241,702 6,823,604 6,935,950 18.6% 212,233 89,700 367,980 $15.75

Northlake 2,300 31,083,259 3,232,143 3,292,696 10.6% 15,625 13,822 290,000 $16.49

Northwest Atlanta 2,944 48,935,870 7,785,483 7,922,844 16.2% 10,585 0 16,650 $17.75

South Atlanta 2,428 24,359,984 3,105,074 3,198,561 13.1% 114,244 0 41,145 $16.27

West Atlanta 667 5,814,021 1,229,412 1,229,412 21.1% 84,923 40,000 40,000 $13.52

Totals 15,115 299,124,236 46,515,925 48,294,359 16.1% 1,867,143 461,922 1,578,085 $18.47

Existing Inventory Vacancy

Existing Inventory Vacancy

27

© 2

014

OnC

ours

e Le

arni

ng. A

ll Ri

ghts

Res

erve

d.

Market analysis methodology:

Simple trend extrapolation vs Structural analysis

28© 2014 OnCourse Learning. All Rights Reserved.

Trend extrapolation:

Take advantage of inertia in space market (past partly predicts the future)

Consider trends and cyclesPotential to use statistical techniques (time-

series analysis: autoregression, ARIMA, VAR, vector error-correction)

Potential to bring in capital market factors as predictors

29© 2014 OnCourse Learning. All Rights Reserved.

Structural Analysis:

Model the structure of the market (underlying determinants of supply & demand, e.g. population growth and employment growth)

Forecast the underlying determinants (e.g., economic base analysis like we talked about in Ch.3), then use model to predict space market.

30© 2014 OnCourse Learning. All Rights Reserved.

Formal analysis requires:

Demand model (including elasticities) Supply model (including elasticities & lags) Equilibrium model (including landlord behavior)

Useful for gaining fundamental understanding of the market, and making long-term forecasts

Used more primarily in consultants reports and academic studies

31© 2014 OnCourse Learning. All Rights Reserved.

Exh.6-4: Widely used decision-making tool:Basic short-term (1-3 yr) structural market analysis:

Inventory existing supply Identify sources of space usage demand

Quantify relationship between demand sources and quantity of

space usage

Forecast demand sources

SUPPLY SIDE DEMAND SIDE

Inventory construction pipeline

Forecast of new demandForecast of new supply

Forecast space shortfall or surplus

Decision implicatons?

32© 2014 OnCourse Learning. All Rights Reserved.

Property Type Demand Drivers

Residential single family(Owner occupied)

· Population· Household formation (child rearing ages)· Interest rates· Employment growth (business & professional occupations)

Residential multifamily(Apartment renters)

· Population· Household formation (non-child-rearing ages)· Local housing affordability· Employment growth (blue collar occupations)

Retail · Aggregate disposable income· Aggregate household wealth· Traffic volume (specific sites)

Office Employment in office occupations:· Finance, Insurance, Real Estate (FIRE)· Business & professional services· Legal services

Industrial · Manufacturing employment· Transportation employment· Airfreight volume· Rail & truck volume

Hotel & convention · Air passenger volume· Tourism receipts or number visitors

Exh.6-5: Major drivers of the demand side of the space market:

33© 2014 OnCourse Learning. All Rights Reserved.

© 2

014

OnC

ours

e Le

arni

ng. A

ll Ri

ghts

Res

erve

d.

34

A simple formal structural model of a space market:

Supply side . . .

)()1()( tCtStS Stock (aggreg.supply) response:

(2)

otherwise

KLtRifKLtRtC

,0

,)(),)(()( Construction (developer behavior):

(1)

R(t) = Rent at time t ($/SF).L = Construction lag (yrs).K = Replacement cost rent level.ε = Price elasticity of supply (responsivenesss)

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

35

A simple formal structural model of a space market:Demand side . . .

)()()( tNtRtD

Tenant demand:

N = Underlying “need” (e.g., employment)

η = Price elasticity of demand

τ = Technology parameter (e.g. SF/employee)

(3)

)1()( tDtOS

Occupied space:(lag to implement demand reflects search & move time)

(4)

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

36

A simple formal structural model of a space market:

Supply & demand sides (equilibrium) . . .

))/))(((1)(1()( VVtvtRtR

Rent adjustment (landlord & potential tenant behavior):

(6)

v(t) = Vacancy rate at time t.

V = “Natural” vacancy rate for the mkt.

Vacancy rate “physics” (definition):

)(/))()(()( tStOStStv (5)

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

37

Put these six equations together . . .

Numerical example typical parameters:· Supply sensitivity = 0.3· Demand sensitivity = 0.3· Technology = 200 SF/employee· Demand intercept = 10 million SF· Rent sensitivity = 0.3· Construction lag L = 3 years

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

38

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0

10

20

30

40

50

60

70

80

90

100

1 4 7 10 13 16 19 22 25 28 31 34 37 40

Co

nst

r. M

SF

Va

c, R

en

t, E

mp

l.

Year

Employment(000s) Vacancy(%)Rent($/SF/YR) Construction Completions(MSF/YR)

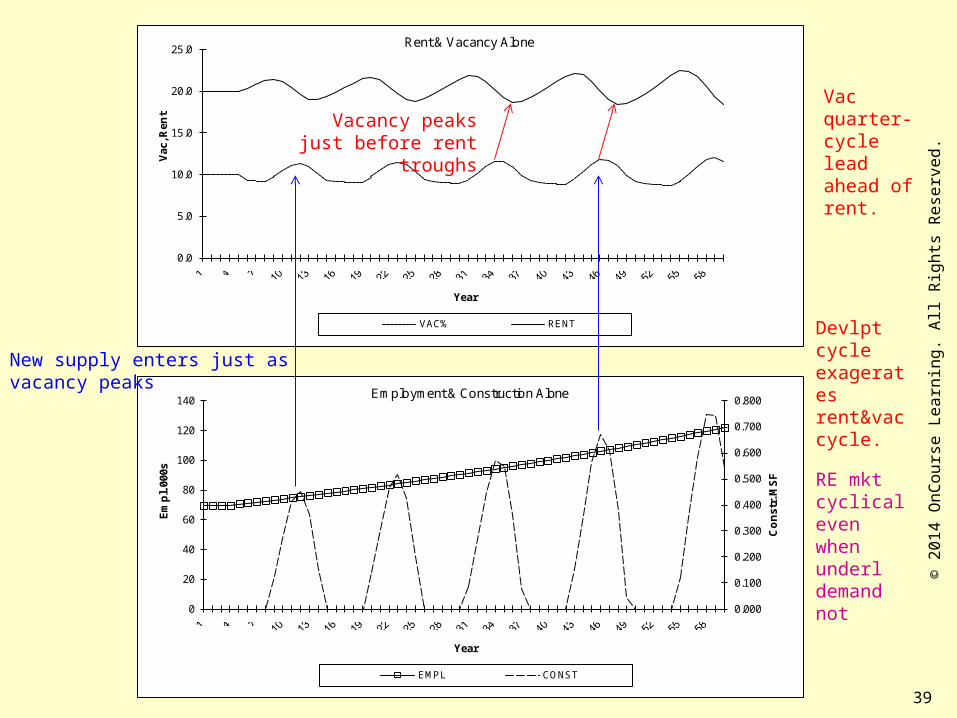

Exh.6-6 Simulated Space Mkt Dynamics

11-year cycle, even though no business cycle!

© 2

014

OnC

ours

e Le

arni

ng. A

ll Ri

ghts

Res

erve

d.

39

0.0

5.0

10.0

15.0

20.0

25.0

Vac

, Ren

t

Year

Rent & Vacancy Alone

VAC% RENT

Vacancy peaks just before rent troughs

RE mkt cyclical even when underl demand not

Devlpt cycle exagerates rent&vac cycle.

0.000

0.100

0.200

0.300

0.400

0.500

0.600

0.700

0.800

0

20

40

60

80

100

120

140

Co

nst

r. M

SF

Em

pl.

000s

Year

Employment & Construction Alone

EMPL CONST

New supply enters just as vacancy peaks

Vac quarter-cycle lead ahead of rent.

© 2

014

OnC

ours

e Le

arni

ng. A

ll Ri

ghts

Res

erve

d.

40

Market Dynamics

The real estate cycle may be different from and partially independent of the underlying business cycle in the local economy.

The cycle will be much more exaggerated in the construction and development industry than in other aspects of the real estate market, such as rents and vacancy.

The vacancy cycle tends to slightly lead the rent cycle (vacancy peaks before rent bottoms).

New construction completions tend to peak when vacancy peaks.

Geltner MIT/CRE

Specifics depend on the parameter values.(& CAVEAT: This is a simple model, ignores forward-looking behavior.)

© 2014 OnCourse Learning. All Rights Reserved.

41

Market Dynamics

In the preceding model, were any of the market participants forward-looking?

What features of the above results do you think are due to myopia or purely adaptive behavior on the part of the market participants?

In the real world, what factors or elements in the real estate system will tend to be forward-looking?

In the real world, will it be possible to perfectly forecast the future? Will some market participants likely be somewhat myopic or adaptive in their behavior?

Geltner MIT/CRE© 2014 OnCourse Learning. All Rights Reserved.

42

SPACE MARKET

SUPPLY (Landlords)

DEMAND (Tenants)

RENTS &

OCCUPANCY

LOCAL &

NATIONAL ECONOMY

FORECAST FUTURE

ASSET MARKET

SUPPLY

(Owners

Selling)

D EMAND

(Investors

Buying)

CASH

FLOW

MKT

REQ’D

CAP

RATE

PROPERTY

MARKET

VALUE

DEVELOPMENT INDUSTRY

IS DEVELPT

PROFITABLE ?

CONSTR

COST INCLU LAND

IF YES

ADDS NEW

CAPITAL MKTS

= Causal flows.

= Information gathering & use.

Geltner MIT/CRE

Rising supply Falling cash

flow Falling asset prices

Less dvlpt…

Forward-looking decisions & negative feedback equilibrates the system…

Consider constr pipeline, underl demand evolution…

Exhibit 2-2

© 2014 OnCourse Learning. All Rights Reserved.

43

SPACE MARKET

SUPPLY (Landlords)

DEMAND (Tenants)

RENTS &

OCCUPANCY

LOCAL &

NATIONAL ECONOMY

FORECAST FUTURE

ASSET MARKET

SUPPLY

(Owners

Selling)

D EMAND

(Investors

Buying)

CASH

FLOW

MKT

REQ’D

CAP

RATE

PROPERTY

MARKET

VALUE

DEVELOPMENT INDUSTRY

IS DEVELPT

PROFITABLE ?

CONSTR

COST INCLU LAND

IF YES

ADDS NEW

CAPITAL MKTS

= Causal flows.

= Information gathering & use.

Geltner MIT/CRE

Rising prices Increased demand Rising prices…

But positive feedback can cause spirals that result in cycles…

Rising prices Increased demand

More dvlpt…

Exhibit 2-2

© 2014 OnCourse Learning. All Rights Reserved.

44Geltner MIT/CRE

Both the space market & the asset market can tend to be cyclical, but the cycle is not necessarily the same…

40

50

60

70

80

90

100

110

120

1986Q4

1987Q4

1988Q4

1989Q4

1990Q4

1991Q4

1992Q4

1993Q4

1994Q4

1995Q4

1996Q4

1997Q4

1998Q4

1999Q4

2000Q4

2001Q4

2002Q4

2003Q4

2004Q4

2005Q4

2006Q4

2007Q4

2008Q4

2009Q4

2010Q4

Inde

xed

to 1

986Q

4 =

100

Exhibit 2-5. Example Space Market Rents & Asset Market Prices (adjusted for inflation): 1986-2011*

Rent Price

Source: CoStar Group, NCREIF, MIT

*The lines depicted here are illustrative examples typical of the US commercial real estate markets, but not exact correlates of the same markets. The rent line is based on asking rents for office space in seven major metro areas (source: CoStar); the asset price line isthe NCREIF-based TBI (source: MIT) transaction price index for institutional investment property. Both the rent line and the asset price line are net of CPI inflation.

© 2014 OnCourse Learning. All Rights Reserved.

45Geltner MIT/CRE

40

50

60

70

80

90

100

110

120

1986Q4

1987Q4

1988Q4

1989Q4

1990Q4

1991Q4

1992Q4

1993Q4

1994Q4

1995Q4

1996Q4

1997Q4

1998Q4

1999Q4

2000Q4

2001Q4

2002Q4

2003Q4

2004Q4

2005Q4

2006Q4

2007Q4

2008Q4

2009Q4

2010Q4

Inde

xed

to 1

986Q

4 =

100

Exhibit 2-5. Example Space Market Rents & Asset Market Prices (adjusted for inflation): 1986-2011*

Rent Price

Source: CoStar Group, NCREIF, MIT

*The lines depicted here are illustrative examples typical of the US commercial real estate markets, but not exact correlates of the same markets. The rent line is based on asking rents for office space in seven major metro areas (source: CoStar); the asset price line isthe NCREIF-based TBI (source: MIT) transaction price index for institutional investment property. Both the rent line and the asset price line are net of CPI inflation.

Both the space market & the asset market can tend to be cyclical, but the cycle is not necessarily the same…

Space mkt cycle

Asset mkt cycle

Both mkts cycle together

© 2014 OnCourse Learning. All Rights Reserved.