chapter 6 merchandise inventory. © 2016 pearson education, inc. learning objectives 1.identify...

TRANSCRIPT

Chapter 6Merchandise

Inventory

© 2016 Pearson Education, Inc.

Learning Objectives

1. Identify accounting principles and controls related to merchandise inventory

2. Account for merchandise inventory costs under a perpetual inventory system

3. Compare the effects on the financial statements when using the different inventory costing methods

6-2

© 2016 Pearson Education, Inc.

Learning Objectives

4. Apply the lower-of-cost-or-market rule to merchandise inventory

5. Measure the effects of merchandise inventory errors on the financial statements

6. Use inventory turnover and days’ sales in inventory to evaluate business performance

6-3

© 2016 Pearson Education, Inc.

Learning Objectives

7. Account for merchandise inventory costs under a periodic inventory system (Appendix 6A)

6-4

© 2016 Pearson Education, Inc.

Learning Objective 1

Identify accounting principles and controls related to merchandise inventory

6-5

© 2016 Pearson Education, Inc.

What Are the Accounting Principles and Controls That Relate to Merchandise

Inventory?• Accounting principles help accountants

classify and report items on the financial statements.

• The accounting principles associated with merchandise inventory are:– Consistency– Disclosure– Materiality– Accounting conservatism

6-6

© 2016 Pearson Education, Inc.

Consistency Principle

• The consistency principle states that a business should use the same accounting methods and procedures from period to period.

• Consistency helps investors and creditors compare financial statements from one period to the next.

6-7

If changes are made in

accounting methods, these

changes must be reported,

generally in the notes to the

financial statements.

© 2016 Pearson Education, Inc.

Disclosure Principle

• The disclosure principle states that a company should report enough information for outsiders to make knowledgeable decisions about the company. Information should be relevant and have faithful representation.

• See the note to the financial statements for Green Mountain Coffee Roasters, Inc., exhibiting this principle on the next slide.

6-8

© 2016 Pearson Education, Inc.

Disclosure Principle

• An example of disclosing inventory information:

6-9

Source: Green Mountain Coffee Roasters, Inc., 2013 Financial Statements, Note 2.

© 2016 Pearson Education, Inc.

Materiality Concept

• The materiality concept states that a company must perform strictly proper accounting only for significant items.

• Information is significant when it would cause someone to change a decision.

6-10

For example, $10,000 is material to a small business

with sales of $100,000.

However, $10,000 isn’t material to a

large company with annual sales of $10,000,000.

© 2016 Pearson Education, Inc.

Conservatism

• The conservatism principle states that a company should report the least favorable figures in the financial statements when two or more possible options are presented.

6-11

• Anticipate no gains but provide for all probable losses

• Conservatively report assets and liabilities

• When in doubt, record an expense instead of an asset

• Choose options that undervalue the business

© 2016 Pearson Education, Inc.

Control Over Merchandise Inventory

• Good inventory controls ensure that inventory purchases and sales are properly authorized and accounted for by the accounting system by: – Ensuring inventory is purchased with proper

authorization.– Tracking and documenting receipt of inventory.– Recording damaged inventory properly. – Performing physical counts of inventory annually. – Recording and removing inventory from

Merchandise Inventory when sold.

6-12

© 2016 Pearson Education, Inc.

Learning Objective 2

Account for merchandise inventory costs under a perpetual inventory system

6-13

© 2016 Pearson Education, Inc.

How Are Merchandise Inventory Costs Determined Under a Perpetual

Inventory System?

• At the end of the period, count the units in ending inventory and assign dollars to the account.

• At the end of the period, determine the units sold during the period and assign dollars to Cost of Goods Sold.

6-14

© 2016 Pearson Education, Inc.

• Note: Each unit originally cost $350• Ending Inventory = Units on hand × Unit cost

= 4 units × $350 per unit = $1,400

• COGS = Units sold × Unit cost= 14 units × $350 per unit = $4,900

6-15

How Are Merchandise Inventory Costs Determined Under a Perpetual

Inventory System?

© 2016 Pearson Education, Inc.

When the costs are different for different groups of inventory, it is more difficult to decide which dollars to assign to the ending inventory.

6-16

How Are Merchandise Inventory Costs Determined Under a Perpetual

Inventory System?

© 2016 Pearson Education, Inc.

• Four basic inventory costing methods are allowable by GAAP:1. Specific identification2. First-in, first-out (FIFO)3. Last-in, last-out (LIFO)4. Weighted-average

6-17

How Are Merchandise Inventory Costs Determined Under a Perpetual

Inventory System?

© 2016 Pearson Education, Inc.

Specific Identification Method

• The specific identification method is used when the company knows exactly which item was sold and exactly what the item cost.

6-18

Used for inventories that

include:AutomobilesUnique artworkJewelsReal estate

© 2016 Pearson Education, Inc.

Specific Identification Method

6-19

© 2016 Pearson Education, Inc.

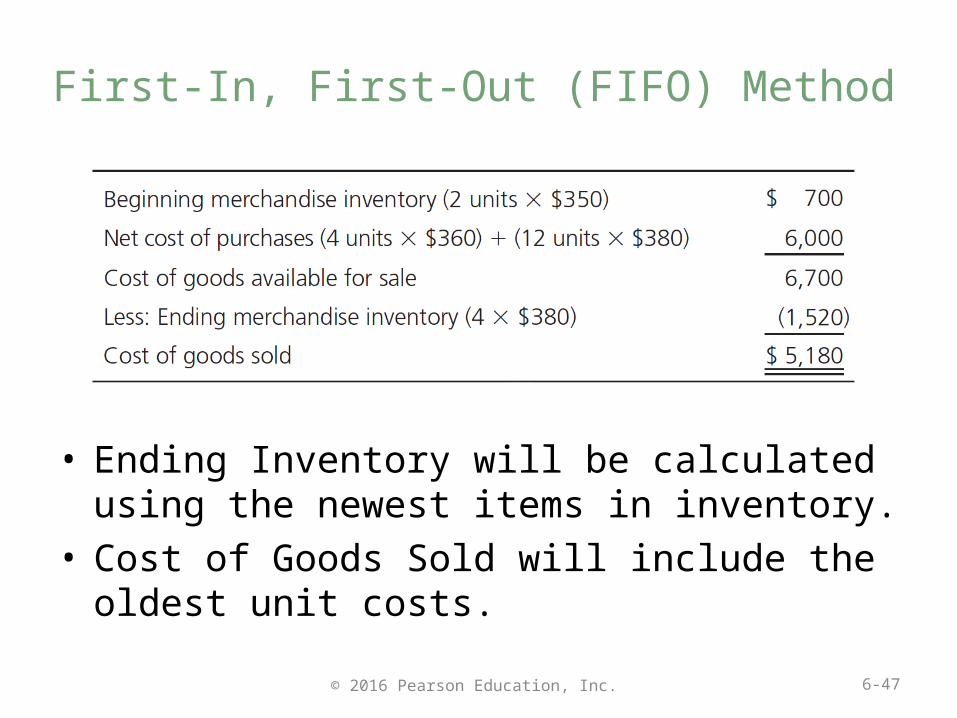

First-In, First-Out (FIFO) Method

• The first-in, first-out method (FIFO) assumes the first units purchased are the first to be sold.

• Cost of Goods Sold is based on the oldest purchases.

• Ending Inventory closely reflects current replacement cost.

6-20

© 2016 Pearson Education, Inc.

First-In, First-Out (FIFO) Method

6-21

© 2016 Pearson Education, Inc.

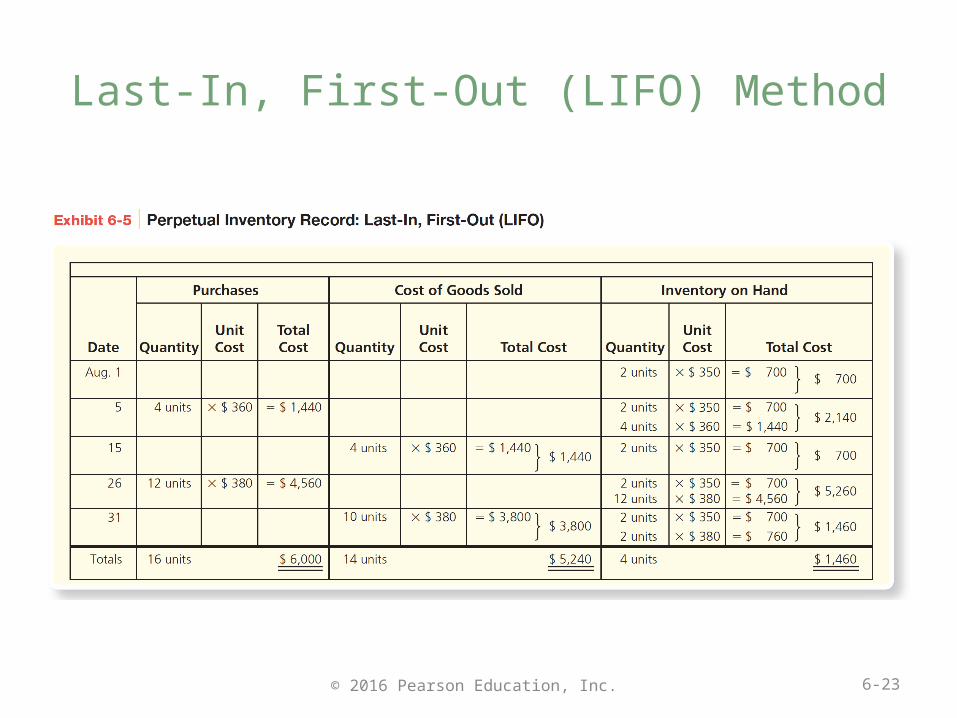

Last-In, First-Out (LIFO) Method

• Last-in, first-out (LIFO) method is the opposite of FIFO.

• As inventory is sold, the cost of the newest item in inventory is assigned to each unit as Cost of Goods Sold.• Cost of Goods Sold closely reflects current

replacement cost.• Ending Inventory contains the oldest costing

units.

6-22

© 2016 Pearson Education, Inc.

Last-In, First-Out (LIFO) Method

6-23

© 2016 Pearson Education, Inc.

Weighted-Average Method

• The weighted-average method computes a new weighted-average cost per unit after each purchase.

• Ending Inventory and Cost of Goods Sold are based on the same weighted-average cost per unit.

6-24

© 2016 Pearson Education, Inc.

Weighted-Average Method

Average cost is computed as:

Cost of goods available for sale ÷ Number of units available= Weighted-average cost per unit

6-25

© 2016 Pearson Education, Inc.

Weighted-Average Method

6-26

© 2016 Pearson Education, Inc.

Learning Objective 3

Compare the effects on the financial statements when using the different inventory costing methods

6-27

© 2016 Pearson Education, Inc.

How Are Financial Statements Affected by Using Different Inventory Costing

Methods?• Income statement

– Cost of Goods Sold is higher under LIFO than under FIFO when costs are rising.

– Net income is lower under LIFO than under FIFO when costs are rising.

• Balance sheet– When costs are increasing, FIFO inventory will

be the highest, and LIFO inventory will be the lowest.

6-28

© 2016 Pearson Education, Inc.

How Are Financial Statements Affected by Using Different Inventory Costing

Methods?

• Note that FIFO results in the highest gross profit, while LIFO shows the highest cost of goods sold.

6-29

© 2016 Pearson Education, Inc.

How Are Financial Statements Affected by Using Different Inventory Costing

Methods?

6-30

© 2016 Pearson Education, Inc. 6-31

How Are Financial Statements Affected by Using Different Inventory Costing

Methods?

© 2016 Pearson Education, Inc.

Learning Objective 4

Apply the lower-of-cost-or-market rule to merchandise inventory

6-32

© 2016 Pearson Education, Inc.

How Is Merchandise Inventory Valued When Using the Lower-of-Cost-or-

Market Rule?

• The lower-of-cost-or-market rule requires that inventory be reported in the financial statements at the lower of the inventory’s original cost or its market value.

6-33

© 2016 Pearson Education, Inc.

Recording the Adjusting Journal Entry to Adjust Merchandise Inventory

Smart Touch Learning paid $3,000 for its TAB0503 inventory. By December 31, it can be replaced for only $2,200, and the decline

value appears permanent.

6-34

© 2016 Pearson Education, Inc.

Learning Objective 5

Measure the effects of merchandise inventory errors on the financial statements

6-35

© 2016 Pearson Education, Inc.

What Are the Effects of Merchandise Inventory Errors on the Financial

Statements?

• An error in inventory can lead to errors in other related accounts.

• Because the ending inventory number is used in other computations, when ending inventory is incorrect, other numbers will also be incorrect, such as:• Cost of goods sold• Gross profit• Net income

6-36

© 2016 Pearson Education, Inc.

What Are the Effects of Merchandise Inventory Errors on the Financial

Statements?

6-37

© 2016 Pearson Education, Inc.

What Are the Effects of Merchandise Inventory Errors on the Financial

Statements?

6-38

© 2016 Pearson Education, Inc. 6-39

What Are the Effects of Merchandise Inventory Errors on the Financial

Statements?

© 2016 Pearson Education, Inc.

What Are the Effects of Merchandise Inventory Errors on the Financial

Statements?

6-40

© 2016 Pearson Education, Inc.

Learning Objective 6

Use inventory turnover and days’ sales in inventory to evaluate business performance

6-41

© 2016 Pearson Education, Inc.

Inventory Turnover

• The inventory turnover ratio measures how rapidly inventory is sold.

• The ratio should be evaluated against industry averages.– A high turnover rate indicates ease of selling.– A low turnover rate indicates difficulty of

selling.

6-42

© 2016 Pearson Education, Inc.

Days’ Sales in Inventory

• The days’ sales in inventory ratio measures the average number of days inventory is held by the company.

• Some types of inventory will move faster than others.

• For inventory with an expiration date, this measure is very important.

6-43

© 2016 Pearson Education, Inc.

Learning Objective 7

Account for merchandise inventory costs under a periodic inventory system (Appendix 6A)

6-44

© 2016 Pearson Education, Inc.

How Are Merchandise Inventory Costs Determined Under a Periodic Inventory

System?• Under a periodic inventory system:

• Inventory is not tracked in the accounting system continuously.

• The beginning inventory balance is carried until the end of the period.

• Purchases are accumulated during the period.• The ending inventory balance replaces the

beginning inventory balance.

6-45

© 2016 Pearson Education, Inc.

How Are Merchandise Inventory Costs Determined Under a Periodic Inventory

System?

6-46

© 2016 Pearson Education, Inc.

First-In, First-Out (FIFO) Method

• Ending Inventory will be calculated using the newest items in inventory.

• Cost of Goods Sold will include the oldest unit costs.

6-47

© 2016 Pearson Education, Inc.

Last-In, First-Out (LIFO) Method

• Ending Inventory will be calculated using the oldest items in inventory.

• Cost of Goods Sold will include the newest unit costs.

6-48

© 2016 Pearson Education, Inc.

Weighted-Average Method• Ending Inventory is calculated using the average

cost per unit.• Cost of Goods Sold will also be costed using

average cost per unit.

6-49

© 2016 Pearson Education, Inc. 6-50