chapter 6 cash management, savings, credit, and debt planning · pdf file... cash management...

TRANSCRIPT

CHAPTER 6 Cash Management, Savings, Credit, and Debt Planning

1) What is NET WORTH?

a) Why plan?

Owner equity Amount left to live on after all assets are converted to cash and all debts are paid The true “retirement” number

2) How do you calculate net worth?

TA – Debt = NW

3) REASONS FOR UNDERTAKING NET WORTH PLANNING

a) Establish a financial discipline

b) Organize a financial life around a future target

c) Measure financial progress on a regular basis

d) Feel financially secure about future

4) Calculation of Net Worth

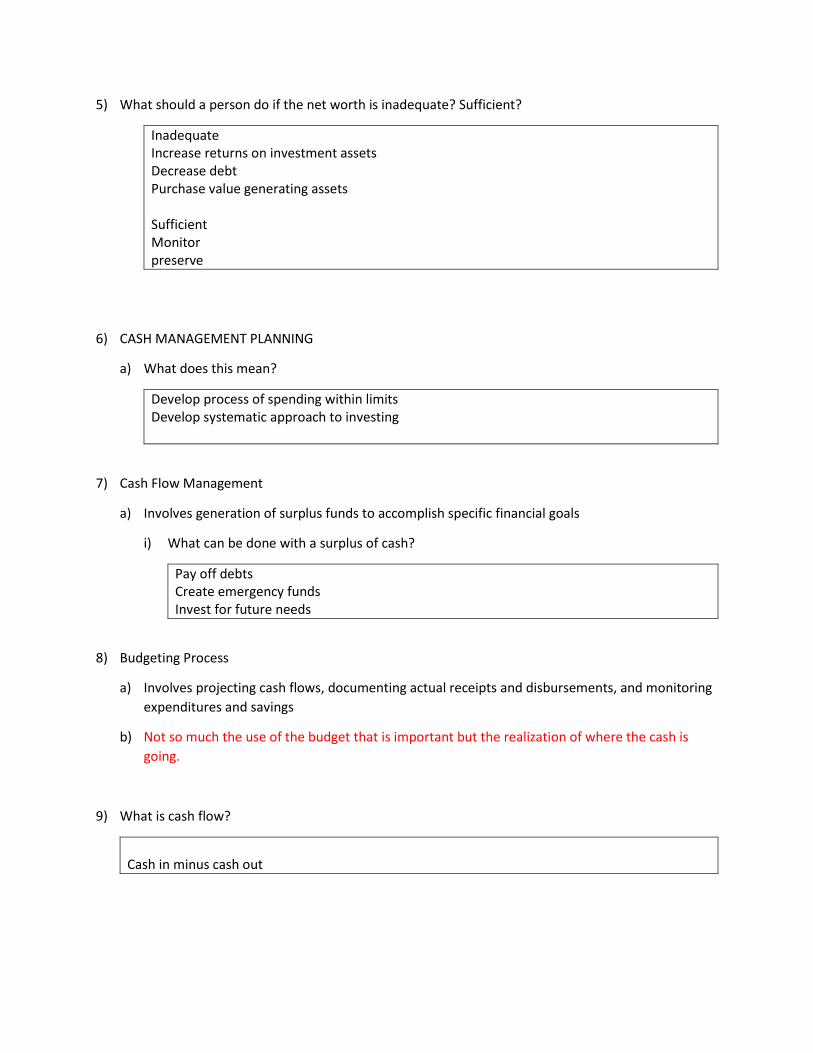

5) What should a person do if the net worth is inadequate? Sufficient?

Inadequate Increase returns on investment assets Decrease debt Purchase value generating assets Sufficient Monitor preserve

6) CASH MANAGEMENT PLANNING

a) What does this mean?

Develop process of spending within limits Develop systematic approach to investing

7) Cash Flow Management

a) Involves generation of surplus funds to accomplish specific financial goals

i) What can be done with a surplus of cash?

Pay off debts Create emergency funds Invest for future needs

8) Budgeting Process

a) Involves projecting cash flows, documenting actual receipts and disbursements, and monitoring

expenditures and savings

b) Not so much the use of the budget that is important but the realization of where the cash is

going.

9) What is cash flow?

Cash in minus cash out

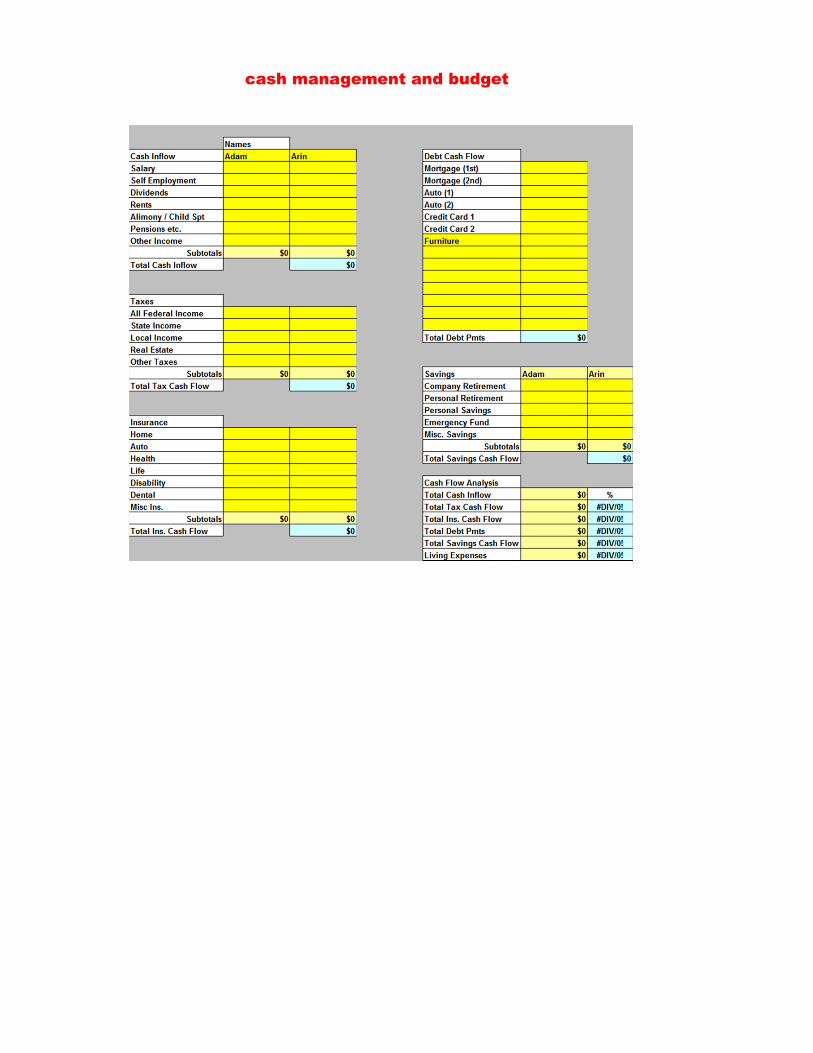

cash management and budget

10) What is meant by SYSTEMATIC SAVINGS PLANNING?

Monthly set (fixed) investment amounts Individual Retirement accounts are set this way.

11) GOAL SETTING

12) Pay yourself first! What does this mean?

a) How do you achieve it?

13) How do we take control of our cash flow?

a) EXPENSE REDUCTION

b) INCOME ACCELERATION

14) Goal Setting

a) Avg person should try to save between 10 – 20% of income (retirement and personal savings)

15) What can you do if you cannot meet your goals?

Change goals Get another job Reduce expenses

16) EMERGENCY FUNDING STRATEGIES

a) The text lists these as potential sources. They are by far the worst choices. (liquidity, returns,

risk, taxes, interest and penalties)

i) Home Equity Line of Credit

ii) Accumulated Cash Value in Life Insurance Policy

iii) Company Savings Plan

iv) Money Earmarked as IRA Investment

17) CRITERIA FOR SAVINGS MEDIA SELECTION

What about money market mutual funds?

18) DEBT OR CREDIT?

a) Debt and credit are two sides of the same coin

19) SOURCES OF CONSUMER CREDIT

a) COMMERCIAL BANKS

b) CONSUMER FINANCE COMPANIES

c) CREDIT UNIONS

d) SAVINGS AND LOAN ASSOCIATIONS

e) LIFE INSURANCE COMPANIES

f) AUTO DEALERS

20) CREDIT HISTORY

a) What are these FACTORS that affect CREDIT HISTORY

Character Capacity capital

b) Credit Rating

FICO Creditkarma.com

21) BURDEN OF DEBT

a) Every family should limit the debt it can conveniently handle

b) Use business policy on debt as a guide

i) In business limit is reached when debt reaches level of equity

ii) Consumers should limit debt so personal debt/equity ratio remains below 1

iii) Not very practical ,especially for younger people, since they have student loans

c) Alternatively, consumers can set installment debt limit below 10-15% of monthly income

(1) More realistic: This is usually the debt that gets us into the most trouble (Byerly)

22) BANKRUPTCY

a) Is no longer taboo. But it should always be avoided

What does not escape bankruptcy?

School debt Taxes Healthcare???

23) Debt management tools

a) This website offers a “free to try” debt management tool

i) http://www.debtanalyzer.com

ii) I am not promoting this tool other than to say it is typical of the tools that are available

(some very cheap)

b) The technique is called debt stacking or debt snowball

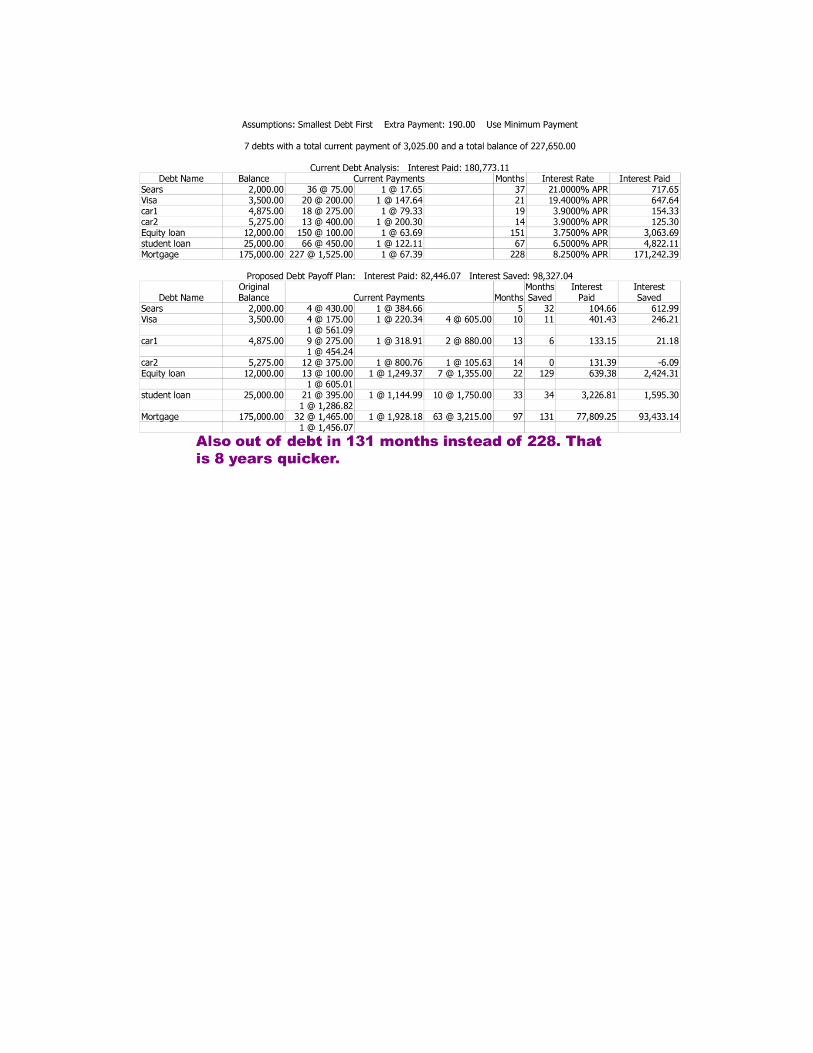

c) Strategy for getting out of debt

1) Most people would say the best way to get out of debt is to payoff high interest debt first.

2) When most people payoff a debt, the payment becomes part of the discretionary cash that

can be used for any expense item.

3) Psychologically, it might be best to start with the debt with the lowest balance. Clients will

see reduction in the number of debts and be encouraged to continue. (Byerly)

4) Debt stacking maintains a constant total payment to debt.

a) As a debt is paid off the payment is then added to the payment of the next debt in

order.

b) Discipline is needed to continue this process.

.

The column of data shows a quick cash flow analysis to determine how much money can be moved toward the snowball.

Enter the debts along with balance, interest rates, and minimum payments.

The debts should be sorted from lowest balance to highest balance.

Additional funds are then attributed to the lowest balance debt.

As you can see, in January the first debt is paid off. The remainder for that debt in January is added to the next debt in line. This continues until that debt is paid off in February.