chapter 5 the federal reserve the federal reserve system tools of monetary policy the federal...

Post on 20-Dec-2015

221 views

TRANSCRIPT

Chapter 5 The Federal ReserveChapter 5 The Federal ReserveChapter 5 The Federal ReserveChapter 5 The Federal Reserve

• The Federal Reserve System

• Tools of Monetary Policy• The Federal Reserve System

• Tools of Monetary Policy

I. The Federal Reserve SystemI. The Federal Reserve SystemI. The Federal Reserve SystemI. The Federal Reserve System

• “the Fed”

• originally a lender of last resort to prevent bank panics

• today, also conducts monetary policy

• “the Fed”

• originally a lender of last resort to prevent bank panics

• today, also conducts monetary policy

Fed StructureFed StructureFed StructureFed Structure

• Board of Governors• 7 members, 14 yr. nonrenewable

terms• 1 member is Chair

-- Alan Greenspan (1987)

• Board of Governors• 7 members, 14 yr. nonrenewable

terms• 1 member is Chair

-- Alan Greenspan (1987)

• Regional Banks• 12 districts• FRBNY is most important• perform bank services

• Regional Banks• 12 districts• FRBNY is most important• perform bank services

• FOMC• 12 members

-- Board

-- FRBNY President

-- 4 other district presidents (rotate)• meet every 6 weeks to vote on

monetary policy (FF rate target)• FRBNY implements FOMC votes

• FOMC• 12 members

-- Board

-- FRBNY President

-- 4 other district presidents (rotate)• meet every 6 weeks to vote on

monetary policy (FF rate target)• FRBNY implements FOMC votes

Fed independenceFed independenceFed independenceFed independence

• How?• Fed is self-financing• Fed governors serve long-terms

• Why?• economic vs. political goals• long-term vs. short-term goals

• How?• Fed is self-financing• Fed governors serve long-terms

• Why?• economic vs. political goals• long-term vs. short-term goals

• Fed is NOT completely independent• Fed powers can be limited by

Congress

• Fed is NOT completely independent• Fed powers can be limited by

Congress

II. Tools of Monetary PolicyII. Tools of Monetary PolicyII. Tools of Monetary PolicyII. Tools of Monetary Policy

• reserve requirement• % deposits banks must hold as

cash or Fed deposits• changing this will affect MS but• this is expensive to change, and is

too powerful

• reserve requirement• % deposits banks must hold as

cash or Fed deposits• changing this will affect MS but• this is expensive to change, and is

too powerful

• discount loans• loans from the Fed to banks• Fed can change interest rate or

availability of loans but• most banks do not use them• not very effective in controlling MS

• discount loans• loans from the Fed to banks• Fed can change interest rate or

availability of loans but• most banks do not use them• not very effective in controlling MS

• open market operations• main monetary policy tool• Fed buys/sells Treasuries through

private dealers• in 1998 made $35 billion in profit• FOMC votes on federal funds rate

target• FRBNY sells/buys to meet the

target

• open market operations• main monetary policy tool• Fed buys/sells Treasuries through

private dealers• in 1998 made $35 billion in profit• FOMC votes on federal funds rate

target• FRBNY sells/buys to meet the

target

if Fed BUYS Treasuriesif Fed BUYS Treasuriesif Fed BUYS Treasuriesif Fed BUYS Treasuries

• banks reserves increase,

FF rate decreases• immediately

• other short-term rates fall, MS increases• weeks - months

• economic expansion • 1 year

• banks reserves increase,

FF rate decreases• immediately

• other short-term rates fall, MS increases• weeks - months

• economic expansion • 1 year

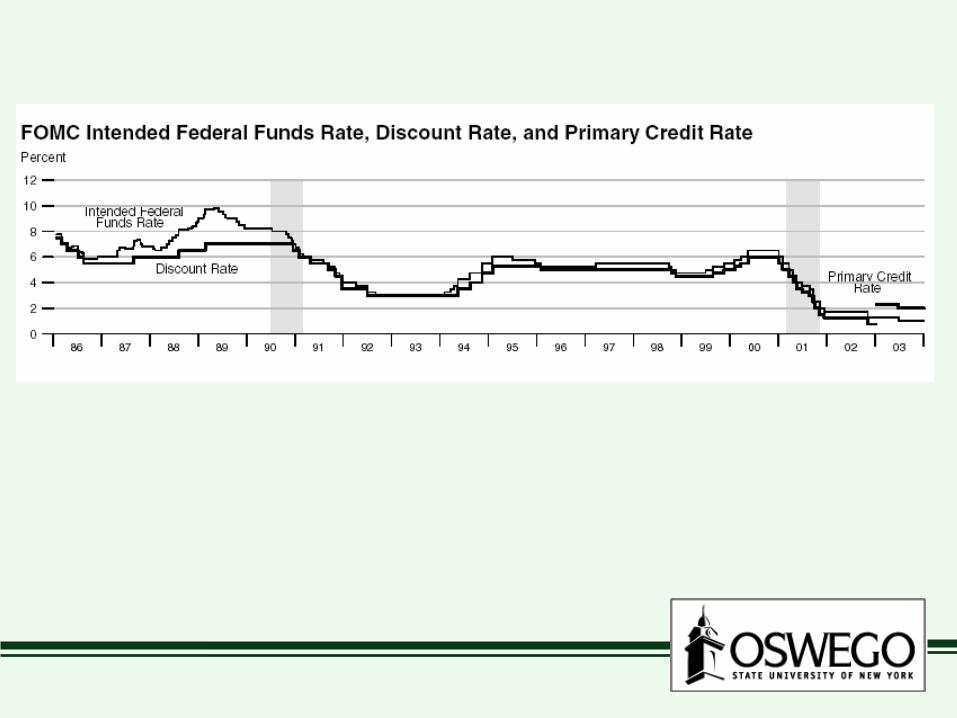

FF rate target, 2000-2003

As FF rate falls, other ST rates also fall

Open market reposOpen market reposOpen market reposOpen market repos

• temporary changes in bank reserves

• Repo• Fed buys Treasuries with seller

repurchasing them later• temporary increase in reserves

• temporary changes in bank reserves

• Repo• Fed buys Treasuries with seller

repurchasing them later• temporary increase in reserves

• reverse repo• Fed sell Treasuries and agrees to

repurchase• temporary decrease in reserves

• reverse repo• Fed sell Treasuries and agrees to

repurchase• temporary decrease in reserves

Chapter 6. Monetary PolicyChapter 6. Monetary PolicyChapter 6. Monetary PolicyChapter 6. Monetary Policy

• Goals

• Recent history• Goals

• Recent history

I. GoalsI. GoalsI. GoalsI. Goals

• price stability/low inflation• goal: below 3%• 2003: 1.87% (CPI)

• low unemployment• goal: natural rate (4%?)• 12/03: 5.7%

• price stability/low inflation• goal: below 3%• 2003: 1.87% (CPI)

• low unemployment• goal: natural rate (4%?)• 12/03: 5.7%

• economic growth• % increase in real GDP• goal: 3%• 4th Q 2003: 4% annual rate

• financial market stability• calm investors• intervene if markets “too high” or

“too low”

• economic growth• % increase in real GDP• goal: 3%• 4th Q 2003: 4% annual rate

• financial market stability• calm investors• intervene if markets “too high” or

“too low”

Sometimes goals conflictSometimes goals conflictSometimes goals conflictSometimes goals conflict

• low inflation vs. economic growth

• or

• low inflation vs. financial market stability

• but in 1990s, enjoyed strong growth, low inflation

• low inflation vs. economic growth

• or

• low inflation vs. financial market stability

• but in 1990s, enjoyed strong growth, low inflation

II. Monetary policy in 1990sII. Monetary policy in 1990sII. Monetary policy in 1990sII. Monetary policy in 1990s• Fed targets FF rate

• FOMC votes on FF rate target• current target: 1%

(since 6/2003)

• Fed targets FF rate• FOMC votes on FF rate target• current target: 1%

(since 6/2003)

1990-91 recession1990-91 recession1990-91 recession1990-91 recession

• Fed slow to recognize recession and cut FF rate• ‘90-’92 falls from 8% to 3%

• mild recession, but mild/slow recovery

• Fed slow to recognize recession and cut FF rate• ‘90-’92 falls from 8% to 3%

• mild recession, but mild/slow recovery

1994-951994-951994-951994-95

• FOMC announces FF rate target after meeting

• FF rate target raise 8 times (3-6%)• prevent inflation• surprise to financial markets• “soft landing”

• currency intervention to increase Yen/$

• FOMC announces FF rate target after meeting

• FF rate target raise 8 times (3-6%)• prevent inflation• surprise to financial markets• “soft landing”

• currency intervention to increase Yen/$

1998199819981998

• Russian debt default

• Asian currency crisis

• Fed cuts FF rate

• bailout of LTCM to prevent financial panic

• Russian debt default

• Asian currency crisis

• Fed cuts FF rate

• bailout of LTCM to prevent financial panic

1999199919991999

• increases in FF rate for another “soft landing”

• reversed in 2000 after economy slows

• 3/91 - 3/01• longest U.S. expansion

• increases in FF rate for another “soft landing”

• reversed in 2000 after economy slows

• 3/91 - 3/01• longest U.S. expansion

TodayTodayTodayToday

• FF rate target cut from 6.5% to 1% 2000-03

• Recession 2001 (March-Nov.)• slow recovery, esp. job market

• FOMC has indicated that they will keep FF rate low for now• not worried about inflation

• FF rate target cut from 6.5% to 1% 2000-03

• Recession 2001 (March-Nov.)• slow recovery, esp. job market

• FOMC has indicated that they will keep FF rate low for now• not worried about inflation