chapter 4 profitability analysis -...

TRANSCRIPT

Chapter 4

Profitability Analysis

Introduction

Profitability is the result of financial as well as operational

efficiency of a business organisation. Assessment of the financial

position of the CSMs will be incomplete, if the overall profitability of the

business organisation is not evaluated thoroughly. Therefore, an

attempt is made to evaluate the profitability of the five sample CSMs

with the help of gross profit ratio, net profit ratio and return on

investment ratio in this chapter.

Concept of profit and profitability

Profit is generally known as the excess total revenue over total

costs. Profit is the main motivating force for the business activities.

Profits are the report card of the past and the inventive gold star for the

future. If an enterprise fails to make profit, capital invested is eroded

and if this situation prolongs, the enterprise ultimately ceases to exist1.

Profit is the whetstone of the operational performance and the

touch stone of financial stability. Profit which is the surplus of business

income over business expenditure, provides for

i] adequate returns to investors,

ii] replacement of fixed assets,

iii] improved standard for the workers and

iv] expansion of the business.,

■Ml'WWiWBWaBK

especially in an inflationary environment2. Profit is, therefore,

considered as soul of the business management.

According to Lord Keynes, profit is an engine that drives

business enterprise3. It is comprehensive indicator of the ability of the

management to coordinate the functions of planning, decision making

and administration. Therefore, it is considered as the primary measure

of the success of business management4.

It is true that the modern concept of financial management is

concerned with maximisation of wealth as against profit maximisation

that has found a significant place in economics. It must, however, be

pointed out that it is profit that provides wealth5. Therefore the

business executives emphasise return on investments rather than

maximisation of wealth6.

Profits determine the liquidity and solvency of the firm. They

serve as yardstick for judging the competence and efficiency of the

management. Profits are essential for the purpose of financing future

activities7.

Profit maximisation is the art of making as much profit as

possible for a business organisation. This is a slogan which raises

several questions. Over what time horizon, are profits to be maximised?

There is likely to be a conflict between short-run and long-run growth.

If the aim is maximising the present discounted value of all future

profits, what is the correct discount rate to be used? Profit maximisation

83

is a sensible objective, only if the owners are risk-neutral. There is

normally a trade off to be made between risk and mean expected

profits. Also the directors or owners may have their own objectives,

these range from desire for a large empire or jobs for their relatives or

the concern about environment. All these have to be traded off against

profit. Other things being equal, however, businesses prefer higher

profits8.

Keirstead (1959) expressed the view that profits originate from

monopoly, successful innovation and a correct estimation of uncertain

factors either particular to the industry or general to the whole

economy9.

The major objective of any business activity is to maximise it’s

wealth through profit. Profit planning is a disciplined method, whereby

the environs impinging on an organisation are analysed, the available

resources and internal competencies are identified and plans are made

to achieve them. It is a routine work and covers a definite span.

Initially, it is concerned with the gap analysis and evaluation of reasons

for the variations in the financial plan and the actuals10.

Profits are essential for a business organisation. But it is not

correct, if the organisation aims at maximising profit, without

concerning the social consequences. It is a misfortune that the word

“profit” is used in wrong sense that the business enterprise should

maximise profits at the cost of employees, customers and society.

84

Nevertheless, any business organisation should earn adequate profits to

sustain it’s operation so as to receive funds from investors for it’s

growth and to serve the society.

Howard and Upton observed, “the word profitability may be

defined as the ability of a given investment to earn a return on it’s

use .

Weston and Bringham observed that profitability is the net19

surplus of a large number of policies and decisions . Thus, profitability

is the ability of business organisation to earn profits as an absolute

figure alone will not help to assess the adequacy of income or changes

in efficiency as shown by the financial performance of a business

organisation. The remaining final profit in absolute quantities may rather

be confusing and it will be difficult to interpret due to variations in the

size of investments and/or the volume of sales. Therefore, it becomes

necessary to relate profit figures either to the volume of sales or to the

quantum of investment and thereby we have to derive quantitative

relationship in the form of either ratios or percentages. Thus, profit is

an absolute connotation, whereas profitability is a relative concept.

Inspite of the several social objectives to be fulfilled by the

CSMs, it is necessary to earn minimum rate of return on the capital

employed atleast for their existence. Also the profit earned by the

CSMs gives margin of safety to the sundry creditors and it is a source

of fringe benefits or welfare measure to the employees. If profit is

85

earned by CSMs, the price of the yarn can be reduced by giving rebates

to the customers, Thus, the importance of profit and profitability for

the CSMs is significant.

Determinants of profitability

There are several factors influencing profitability. Factors such

as size of firm, scale of operation, efficiency of technology, market

concentration, product diversification and vertical integration are among

those causes which result in inter-industry and inter-firm differences in

profitability . Also market conduct of the firm comprising adver

tisement, marketing strategy, pricing, etc., have considerable

implication for profitability.

However, it is very difficult to identify these factors and the task

of gauging their influence on profit, even with the help of the most

powerful computers is further more formidable one.

However, the businessmen and the investors will look upon the

following few elements.

i] Past profit - a steady upward trend is ideal, but caution against

creative accounting is necessary.

ii] Past sales and present market trends - many help by advising how

to move the stuff out of the warehouse and so they allot much more

importance to marketing ability.

iii] Existing demand for the product.

iv] Probable changes in competition.

86

v] Economic outlook.

vi] Company’s ability to control costs.

There are three ways for maximising profit (viz.)

i] increasing price,

ii] reducing price and increasing volume of sales and

iii] reduction of cost14.

Whereas the price and volume of sales are influenced by many

external factors, reduction of cost is fairly under the control of

management.

Measure of profit

There are many measures to assess profitability of a business.

' They comprise the following.

1. Net profit margin

2. Total assets turnover

3. Return on assets

4. Dupont return on assets

5. Operating income margin

6. Operating assets turnover

7. Sales to fixed assets

8. Return on operating assets

9. Return on investment (ROI)

10. Return on total equity

11. Return on common equity

12. Gross profit margin.

The above represent the standard measures that most analysis

and texts usually refer to in the course of an analysis of profitability15.

• These measures are meant to serve different purposes. For

example, net profit margin refers to the net surplus realised by the

business and the next three ratios will throw light on the efficiency in

utilisation of assets. Similarly, return to common equity helps to

evaluate the performance of the business in earning rewards for the

shareholders.

However, the well-known concepts of determining profitability

are gross profit ratio, operating profit ratio, net profit ratio and return

on investments.

Gross profit is realised after prime cost and factory on cost are

met from the sales revenue. The gross profit ratio will facilitate the

evaluation of efficiency of management in controlling over the cost of

sales (prime cost and factory on cost) and prices. Net profit after tax is

the surplus of gross profit after the office on cost and selling and

distribution on cost are met out that can be claimed by the owners of

the business. Therefore, the net profit ratio to sales helps in assessing

the feasibility of the scale of operations and management of overheads.

The third important measure of profitability is the Return on Investment

(ROI) by which the net profit after tax is related to total capital

employed by the business. This helps to find out whether the precious

capital has been profitably employed in the business. Thus, ratio of

88

gross profit to sales, ratio of net profit to sales and the ratio of net

profit to investments or capital employed have been chosen in this study

for evaluating the management of prime cost and factory on cost,

viability of scale of operation and effective utilisation of investments.

Gross profit ratio

Gross profit ratio relates to gross profit to sales. Gross profit is

the surplus of sales revenue over and above the cost of production

(prime cost and factory overheads). Since prime cost is the major part

of cost of production, gross profit ratio becomes crucial indicating the

efficiency of management of cost of production as well as choice of

pricing strategy and achievement in sales.

Net profit ratio

Net profit ratio relates to net profit after tax to sales. Since net

profit is the surplus of gross profit over fixed costs (office on cost and

selling distribution on cost), the net profit ratio shows the extent of

managerial efficiency in controlling over the fixed costs.

Return on Investment (ROI)

Net profit after tax is related to total capital employed by the

business in the form of return on investments. Therefore ROI helps to

evaluate utilisation of resources in the business. Thus, ROI will be a

measure of the productivity of capital, guiding decision on investments.

In ROI, investment comprises share capital, long term loan, accumulated

profit and reserves including depreciation reserve. The interval

89

between investments and net profit involves time value of money and

therefore, investments have been compounded to the years of net profit

The compounding factor is the weighted average of the interest rate in

each CSM. Closing balance of investment of the preceding year has

been compounded and added to the investments during the current year

for computation of investments for ROI.

Multiple Regression Analysis

Multiple Regression Analysis has been employed for identifying

the reasons of profit/loss. Since presence of irrelevant independent

variable may vitiate the results of enter-regression method, the study

has used step-wise regression method, discarding irrelevant

independent variables and accepting relevant independent variables,

influencing profitability models.

In the multiple regression analysis of the factors influencing net

profit, following independent variables were considered.

X3 = Saleable waste

X4 = Gross Value Added by Manufacture (GVAM)

X5 = Value of production

Xi = Prime cost

x2 = Salaries

x3 = Interest charges

X4 = Contingencies

X5 = Net Value Added by Manufacture (NVAM)

X6 = Value of Production

Gross Profit Analysis

Ratio of gross profit to sales has been one of the popular

methods of evaluating the performances of the management in respect

of control over direct costs which, of course, account for major chunk of

total cost of production. Effective management of direct costs and

prices invariably yields large amount of gross profit to sales.

Particulars of ratio of gross profit to sales in the sample CSMs

during the period of review can be found in Tables 4.1 to 4.5. None of

the five sample CSMs could earn gross profit continuously without

failure during the period under review. Also variation in gross

profit/gross loss could not be explained easily in terms of changes in

91

sales. In almost all the CSMs, gross loss often coincided with significant

rise in sales.

Ramanathapuram District Co-operative Spinning Mills Ltd., Achankulam (RSM)

Particulars of gross profit ratios of RSM can be found in Table

4.1. This CSM made gross profit in the first three years and in 1996-97

with gross profit ratios declining continuously from 11.86 percent to

1.35 percent. During the first three years, value of sales continuously

rose from 387.80 lakh rupees in 1989-90 to 456.25 lakh rupees in

1991-92, but gross profit fell from 45.99 lakh rupees in 1989-90 to

8.07 lakh rupees in 1991-92. Even the highest sales at 1020.88 lakh

rupees in 1995-96 could not prevent gross loss of 48.31 lakh rupees.

Yet in the very next year, sales of 899.24 lakh rupees could yield gross

profit of 12.14 lakh rupees.

Therefore, RSM lacks control over direct costs and prices which

need strong management. In RSM gross profits were earned in the

years which had high value of NVAM as in 1989-1992. Again

substantial gross loss was incurred in the years marked by very low

amount of NVAM as in 1992-93, 1994-95 and in the last three years

(vide Table 3.2).

Regression analysis of gross profit yielded three models

involving value of production, GVAM and material cost. While value of

production accounted for 47.00 percent of variation in gross profit,

GVAM influenced 34.00 percent and material cost accounted for 14.30

92

Table 4.1 Ramanathapuram District Co-operative

Spinning Mills Ltd., Achankulam (RSM) Gross Profit Ratio

(Rs. in lakhs)SI. Gross Value of Gross ProfitNo. Year profit sales in Rs. ratio in %

in Rs. [% x 100](1) (2) (3) (4) (5)

1 1989-1990 45.99 387.80 11.86

2 1990-1991 38.85 418.96 9.27

3 1991-1992 8.07 456.25 1.77

4 1992-1993 (-)59.80 551.10 -

5 1993-1994 (-)28.88 567.10 -

6 1994-1995 070.53 683.20 -

7 1995-1996 048.31 1,020.88 -

8 1996-1997 12.14 899.24 1.35

9 1997-1998 078.86 833.76 -

10 1998-1999 065.99 694.22 -

11 1999-2000 036.88 689.70 -

Mean 2.20

' Regression models of RSM

Equations R2 df FYj = 72.613 - 0.127x5

(0.045) 0.470 1,9 7.996*

Yu = 32.183 - 0.20rX5 + 0.575”x4 (0.036) (0.152) 0.810 2,8 17.021”

Y in = 33.107 - 0.506-xs + 0.798"x4 + 0.395"xi (0.067) (0.094) (0.085)

0.953 3,7 47.535”

* - Significant at 5 percent level of probability ** ~ Significant at 1 percent level of probability Figures in brackets are respective standard errorsSource : Computed from the Annual Audited Statement of Final Accounts of RSM

93

percent of variation in gross profit. An increase of one lakh rupees in

production would reduce gross loss by fifty thousand rupees.

Expansion of GVAM by one lakh rupees would raise gross profit

by eighty thousand rupees, whereas reduction of one lakh rupees in

material cost would add forty thousand rupees to gross profit. It is,

therefore, necessary to improve value addition especially through

reduction of material cost for improvement of gross profit of the CSM.

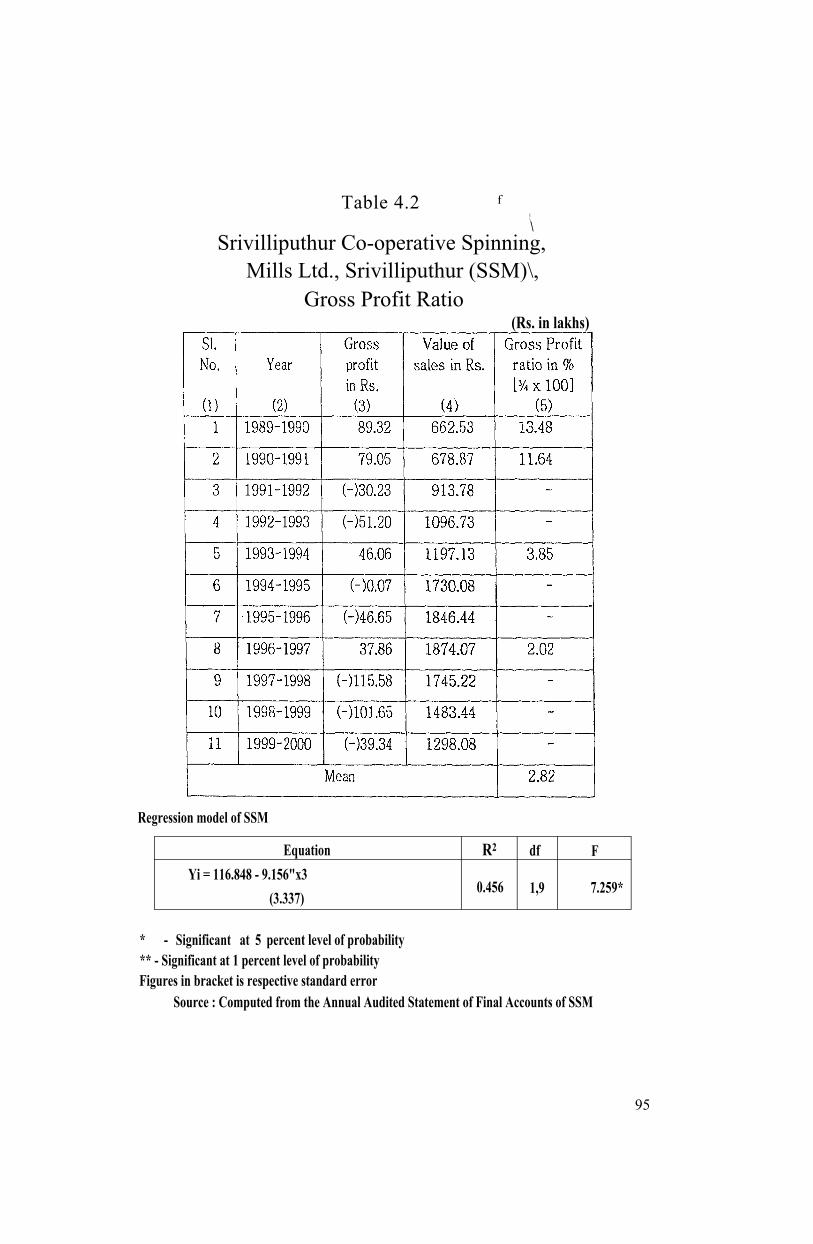

Srivilliputhur Co-operative Spinning Mills Ltd., Srivilliputhur (SSM)

Data on gross profit ratios of SSM are furnished in Table 4.2.

This CSM incurred gross loss in seven out of eleven years. In the

remaining four years, it earned gross profit with gross profit ratio falling

from 13.48 percent in 1989-90 to 2.02 percent in 1996-97. Thus,

gross profit ratios show continuous declining trend. Huge gross loss of

Rs.l 15.58 lakh during the year 1997-98, despite substantial sales of

Rs. 1,745.22 lakh, indicated that the problem was mainly in control over

direct costs and prices. In SSM also, gross profit and minimisation of

gross loss are found to be associated with significant increase in NVAM

as in 1989-90, 1990-91, 1993-94 and 1994-95. Similarly sharp

increase in gross loss was incurred during 1997-99, marked by

significant fall in the amount of NVAM (vide Table 3.2).

The regression analysis reveals that the saleable waste was the

most crucial factor influencing 45.60 percent of the variation in gross

profit. Reduction of saleable waste by one lakh rupees would raise

94

i\\

Srivilliputhur Co-operative Spinning, Mills Ltd., Srivilliputhur (SSM)\,

Table 4.2 f

Gross Profit Ratio(Rs. in lakhs)

Regression model of SSM

Equation R2 df FYi = 116.848 - 9.156"x3

(3.337)0.456 1,9 7.259*

* - Significant at 5 percent level of probability** - Significant at 1 percent level of probability Figures in bracket is respective standard error

Source : Computed from the Annual Audited Statement of Final Accounts of SSM

95

gross profit by nine lakh rupees. Therefore the unit should concentrate

on purchase of material inputs of appropriate quality, thus minimising

saleable waste. Other crucial factors like material cost, labour cost,

GVAM and value of production make insignificant contribution towards

gross profit. However, the above remedial measures are bound to raise

value addition and thereby profitability.

Thiruchirapalli District Co-operative Spinning Mills Ltd., Karur (TSM)

Data on gross profit ratios of TSM are furnished in Table 4.3.

This CSM during the period under review, incurred gross loss in nine

out of eleven years. A substantial increase in sales in 1991~92 could

not prevent the gross loss and again both the gross loss and the value

of sales were also at their highest in 1998-99. However, NVAM seems

to have some influence on gross profit/gross loss. The first two years

witnessed gross profit, while the value of NVAM was high. Similarly,

substantial increase in NVAM during 1997-98 resulted in significant fall

in gross loss which rose in 1998-99 with decrease in the value of

NVAM (vide Table 3.2).

The regression analysis of the causes of the gross profit/gross

loss shows that the gross profit was largely influenced by gross value

added by manufacture (GVAM) followed by variation in saleable waste

and labour cost. As per the predicted models 49 percent of the changes

in gross profit was determined by GVAM, 38 percent by saleable waste

and 8.5 percent by labour cost.

96

Table 4.3

Thiruchirapalli District Co-operative

Spinning Mills Ltd., Karur (TSM)Gross Profit Ratio

(Rs. in lakhs)

SI.No.

(1)

Year

(2)

Gross profit in Rs.

(3)

Value of sales in Rs.

(4)

Gross Profit

ratio in % [V* x 100]

(5)1 1989-1990 125.31 849.11 14.76

2 1990-1991 118.01 792.81 14.89

3 1991-1992 R50.13 1142.35 -

4 1992-1993 H86.47 946.76 -

5 1993-1994 (-)32.20 1028.35 -

6 1994-1995 (->154.90 843.89 -

7 1995-1996 (-)156.57 613.28 -

8 1996-1997 (-)63.81 685.14 -

9 1997-1998 (-)21.93 1366.02 -

10 1998-1999 (~)180.43 2254.30 -

11 1999-2000 (-)64.19 957.85 -

Mean 2.70

Regression model of TSM

Equation R2 df FYt = - 83.299 + 0.826%- 0.712* x2 - 4.892'xa

(0.088) (0.177) (1.287)0.959 3,7 54.685”

** ~ Significant at 1 percent level of probability Figures in brackets are respective standard errorsSource : Computed from the Annual Audited Statement of Final Accounts of TSM

97

If TSM could improve GVAM by one lakh rupees, gross profit

would go up by Rs.82,600. Similarly, if labour could be reduced by one

lakh rupees, the increase in gross profit would be Rs.71,200. When the

saleable waste is reduced by one lakh rupees, gross profit would move

up by 4.89 lakh rupees.

Mere increase in sales would not improve gross profit. The

analysis reveals that value addition through control over direct costs

and prices alone would raise gross profit and reduction of saleable

waste would be a vital component in this strategy.

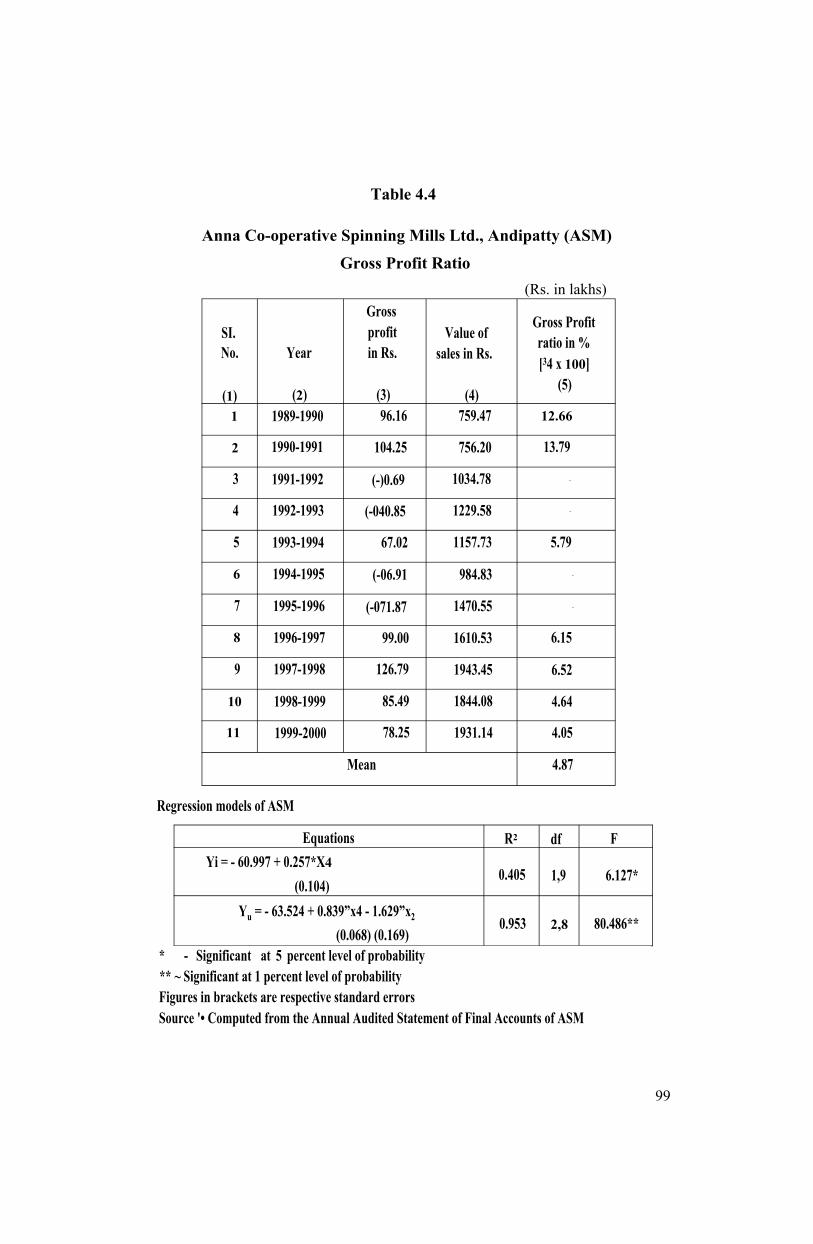

Anna Co-operative Spinning Mills Ltd., Andipatty (ASM)

Data on gross profit ratios of ASM are furnished in Table 4.4.

This CSM has posted better performance than other sample CSMs

making gross profit in seven out of eleven years. However, this CSM

also has suffered from almost continuous fall in gross profit ratios.

Again, fluctuations in sales and gross profit have been erratic in this

CSM also, with sharp increase in sales yielding gross loss as in 1991-

92 and fall in sales resulting in gross profit as in 1993-94. However,

value of NVAM was quite high in the years which posted gross profit in

ASM (vide Table 3.2).

Regression analysis of gross profit has yielded two models

involving GVAM and labour cost. The value of “R2” are found to be

0.405 and 0.953 respectively in the two models. In view of the wide

difference in the values of “R2”, the second model carrying higher value

98

Table 4.4

Anna Co-operative Spinning Mills Ltd., Andipatty (ASM) Gross Profit Ratio

(Rs. in lakhs)

SI.No.

(1)

Year

(2)

Gross profit in Rs.

(3)

Value of sales in Rs.

(4)

Gross Profit ratio in % [34 x 100]

(5)

1 1989-1990 96.16 759.47 12.66

2 1990-1991 104.25 756.20 13.79

3 1991-1992 (-)0.69 1034.78 -

4 1992-1993 (-040.85 1229.58 -

5 1993-1994 67.02 1157.73 5.79

6 1994-1995 (-06.91 984.83 -

7 1995-1996 (-071.87 1470.55 -

8 1996-1997 99.00 1610.53 6.15

9 1997-1998 126.79 1943.45 6.52

10 1998-1999 85.49 1844.08 4.64

11 1999-2000 78.25 1931.14 4.05

Mean 4.87

Regression models of ASM

Equations R2 df FYi = - 60.997 + 0.257*X4

(0.104)0.405 1,9 6.127*

Yu = - 63.524 + 0.839”x4 - 1.629”x2 (0.068) (0.169)

0.953 2,8 80.486**

* - Significant at 5 percent level of probability** ~ Significant at 1 percent level of probability Figures in brackets are respective standard errorsSource '• Computed from the Annual Audited Statement of Final Accounts of ASM

99

of “Rz” can be considered. Accordingly, both GVAM and labour cost

together account for about 95 percent of the variations in gross profit.

If GVAM raises by one lakh rupees, gross profit will raise by Rs.83,900,

while increase of one lakh rupees in labour cost will reduce gross profit

by Rs.1.63 lakh. Thus, GVAM and labour cost are found to be the most

important factors in the gross profit of ASM.

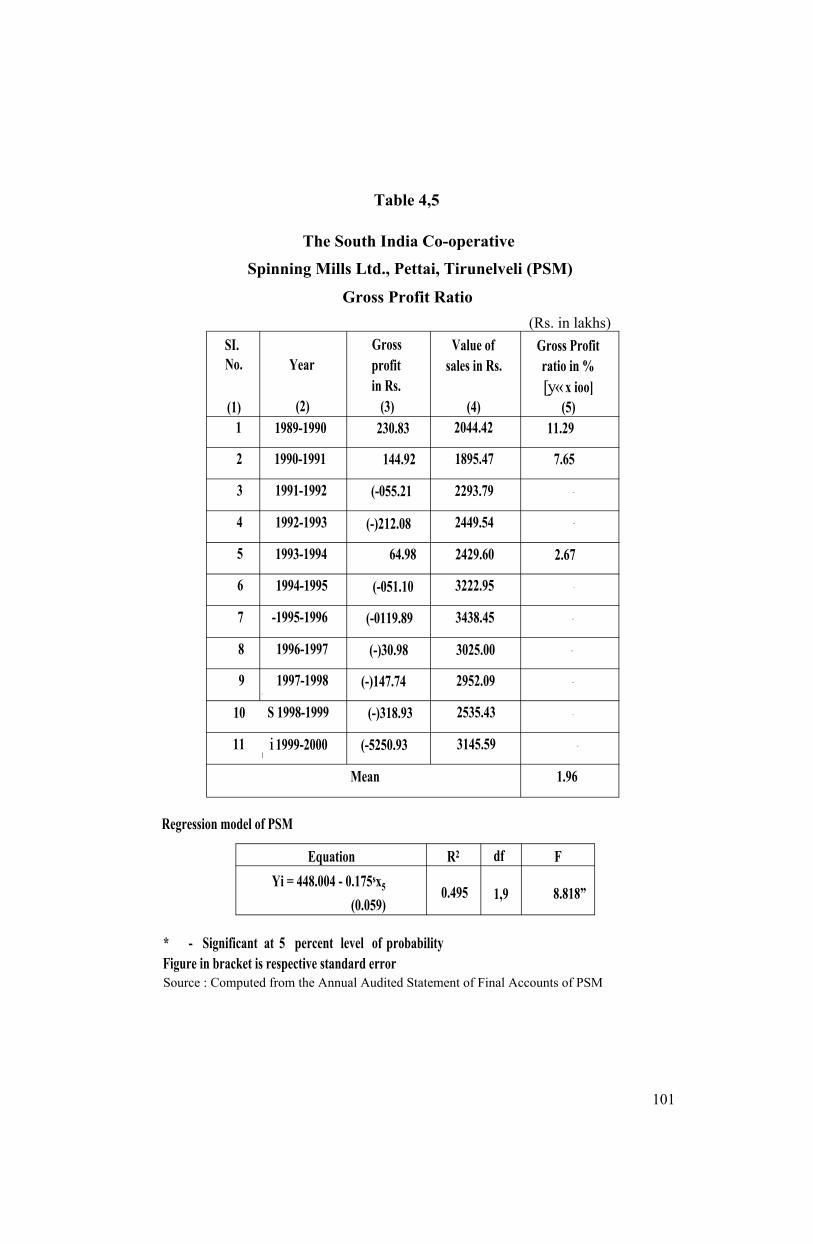

The South India Co-operative Spinning Mills Ltd., Pettai, Tirunelveli (PSM)

As it will be found in Table 4.5, PSM earned gross profit in three

years and the gross profit ratio declined from 11.29 percent in 1989-90

to 2.67 percent in 1993-94. Gross loss grew considerably from 1997-

98 onwards, when there was a continuous fall in production (in the price

level of 1989-90) vide Table 3.1. Also perusal of Table 3.2 shows that

gross profit in PSM in the first two years coincided with high value of

NVAM. Also substantial gross loss was incurred during 1997-2000,

when the amount of NVAM took a nose dive.

Regression analysis has thrown one model. Accordingly, value of

production is the most important factor influencing about -50 percent

variation in gross profit. An increase of one lakh rupees in value of

production would reduce gross loss by 0.175 lakh rupees.

Summary of Gross Profit Analysis

Regression analysis has highlighted factors influencing gross

profit of the CSMs under study. It will be found that GVAM is the most

important influence on gross profit as found in 3 out of the 5 CSMs. In

100

Table 4,5

The South India Co-operative Spinning Mills Ltd., Pettai, Tirunelveli (PSM)

Gross Profit Ratio(Rs. in lakhs)

SI. Gross Value of Gross ProfitNo. Year profit sales in Rs. ratio in %

in Rs. [y« x ioo](1) (2) (3) (4) (5)

1 1989-1990 230.83 2044.42 11.29

2 1990-1991 144.92 1895.47 7.65

3 1991-1992 (-055.21 2293.79 -

4 1992-1993 (-)212.08 2449.54 -

5 1993-1994 64.98 2429.60 2.67

6 1994-1995 (-051.10 3222.95 -

7 -1995-1996 (-0119.89 3438.45 -

8 1996-1997 (-)30.98 3025.00 -

9 1997-1998'

(-)147.74 2952.09 -

10 S 1998-1999 (-)318.93 2535.43 -

11 i 1999-2000[

(-5250.93 3145.59 -

Mean 1.96

Regression model of PSM

Equation R2 df FYi = 448.004 - 0.175sx5

(0.059)0.495 1,9 8.818”

* - Significant at 5 percent level of probabilityFigure in bracket is respective standard errorSource : Computed from the Annual Audited Statement of Final Accounts of PSM

101

addition, saleable waste, labour cost and value of production have been

identified as crucial factors in two CSMs each. Material cost influenced

gross profit in one CSM. It may, however, be pointed out that value of

production, GVAM, material cost and saleable waste are closely related

and, therefore, they can be dealt with together. The CSMs under study

will have to raise their level of production and improve GVAM through

reduction of material cost and saleable waste. The existing practice of

centralised procurement of cotton for all the CSMs in the state needs

reconsideration and revision. The executives of each CSM can be

authorised to procure cotton from the local or nearby market. This will

help to reduce material cost and saleable waste. Again labour cost will

have to be regulated through application of norms of productivity. By

these measures the CSMs will be able to control their cost of

production, raise sales and improve gross profit.

Net Profit Analysis

Whereas the ratio of gross profit to sales reliably indicates the

effectiveness of management of direct costs and prices, the ratio of net

profit to sales enables us to gauge the management of fixed costs of the

business. Effective managements control fixed costs/indirect costs and

keep them below the level of gross profit, thus generating net profit. It

is true that the sample CSMs incurred gross loss in many years, thereby

wiping out the chances of net profit. However, remedial action should

cover both earning of gross profit through effective management of

direct costs and prices as well as controlling over fixed costs.

102

addition, saleable waste, labour cost and value of production have been

identified as crucial factors in two CSMs each. Material cost influenced

gross profit in one CSM. It may, however, be pointed out that value of

production, GVAM, material cost and saleable waste are closely related

and, therefore, they can be dealt with together. The CSMs under study

will have to raise their level of production and improve GVAM through

reduction of material cost and saleable waste. The existing practice of

centralised procurement of cotton for all the CSMs in the state needs

reconsideration and revision. The executives of each CSM can be

authorised to procure cotton from the local or nearby market. This will

help to reduce material cost and saleable waste. Again labour cost will

have to be regulated through application of norms of productivity. By

these measures the CSMs will be able to control their cost of

production, raise sales and improve gross profit.

Net Profit Analysis

Whereas the ratio of gross profit to sales reliably indicates the

effectiveness of management of direct costs and prices, the ratio of net

profit to sales enables us to gauge the management of fixed costs of the

business. Effective managements control fixed costs/indirect costs and

keep them below the level of gross profit, thus generating net profit. It

is true that the sample CSMs incurred gross loss in many years, thereby

wiping out the chances of net profit. However, remedial action should

cover both earning of gross profit through effective management of

direct costs and prices as well as controlling over fixed costs.

102

Particulars relating to ratio of net profit to sales in the sample

CSMs can be found in Tables 4.6 to 4.10. Given the performance of

gross profit, none of the CSMs could show satisfactory performance in

respect of net profit. Among the sample CSMs, ASM recorded net profit

in five out of eleven years and RSM incurred net loss during the entire

period under review. The performance of other three CSMs (SSM, TSM

and PSM) can be placed between ASM and RSM. It is true that TSM and

PSM incurred gross loss in nine and eight years respectively as against

SSM incurring gross loss for seven years. The TSM and SSM could

show better showing in net profit than RSM, because of the latter’s

relatively greater failure to control indirect costs/fixed costs.

Ramanathapuram District Co-operative Spinning Mills, Ltd., Achankulam (RSM)

Particulars of net profit ratios of RSM are to be found in Table

4.6. This is the only CSM in the sample that incurred net loss during

the entire period under review. Even though it recorded gross profit

ratios which were higher than PSM during 1989-91, they incurred net

loss in these two years, while PSM earned net profit in that period.

Obviously RSM had greater difficulties in managing fixed costs than

other CSMs in the sample. In this CSM also interest charges was one

among the largest items of fixed costs, raising significantly from 1995-

96 onwards. This was the only CSM in which expenditure on salaries

was the largest item in the fixed cost. Therefore both of them, besides

gross loss, were responsible for mounting net loss through out the

period under review.

103

Table 4.6Ramanathapuram District Co-operative

Spinning Mills Ltd., Achankulam (RSM) Net Profit Ratio

(Rs. in lakhs)

Regression models of RSM

Equations R2 Df FYi = - 9.136 - 3.049”x2

(0.833)0.598 1,9 13.391”

Yu = - 79.238-5.778Mxz+ 0.866* x5 (0.564) (0.137)

0.933 2,8 55.380”

Ym= - 39.802 - 6.154'x2 + 0.986% ~ 3.237% (0.390) (0.098) (0.963)

0.974 3,7 88.167”

* ~ Significant at 5 percent level of probability** ~ Significant at 1 percent level of probability Figures in brackets are respective standard errorsSource : Computed from the Annual Audited Statement of Final Accounts of RSM

104

Regression analysis of the net profitability considerably confirms

the above view. Expenditure on salaries influences 59.80 percent of the

variations, while it is 93.30 percent, when NVAM is combined with

salary. The third model involving salary, NVAM and contingencies

accounted for 97.40 percent of the variations in net profit. An increase

of one lakh rupees in salaries would reduce net profit by 6.15 lakh

rupees. Addition of one lakh rupees to NVAM would add 0.99 lakh

rupees in net profit. An increase of one lakh rupees in contingencies

would reduce net profit by 3.24 lakh rupees.

Analysis of gross profit ratio has already highlighted corrective

measures like expansion of GVAM through control over material cost

for augmenting, gross profit.

This exercise must be followed by similar control over

expenditure, salaries, depreciation and contingencies in order to

strengthen the profitability.

Srivilliputhur Co-operative Spinning Mills Ltd., Srivilliputhur (SSM)

Particulars of net profit ratios of this CSM are furnished in Table

4.7. Though SSM could make gross profit in four out of eleven years, it

could report net profit in one year only. It was already noted that the

gross profit ratio exhibited declining trend. Declining gross profit and

rising fixed cost wiped off net profit in the remaining three years

reporting gross profit. Amount of interest charges was continuously

brought down from Rs.52.89 lakh in 1989-90 toRs.37.32 lakh in

105

Table 4.7 Srivilliputhur Co-operative

Spinning Mills Ltd., Srivilliputhur (SSM) Net Profit Ratio

(Rs. in lakhs)

Regression model of SSM

Equation R2 df FY [ = 147.704 - 5.386*xa

(1.798)0.499 1,9 8.974"

* - Significant at 5 percent level of probabilityFigures in bracket is respective standard errorSource : Computed from the Annual Audited Statement of Final Accounts of SSM

106

1994-95, but afterwards both interest charges and expenditure on

salary increased continuously, thereby raising net loss. Especially

during the last three years, net loss had become very large, ranging

between Rs.262.34 lakh and Rs.377.50 lakh. During this period there

was a sharp fall in NVAM.

Regression analysis of net profit yielded only one model

involving interest charges, which would influence about 50 percent

changes in net profit. An increase of one lakh rupees in interest charges

would reduce profit by Rs.5.39 lakh. Besides improving gross profit,

the CSM should address itself to full utilisation of capital through sound

management of working capital which is dealt with under operating

cycle in Chapter 5.

Thiruchirapalli District Co-operative Spinning Mills Ltd., Karur (TSM)

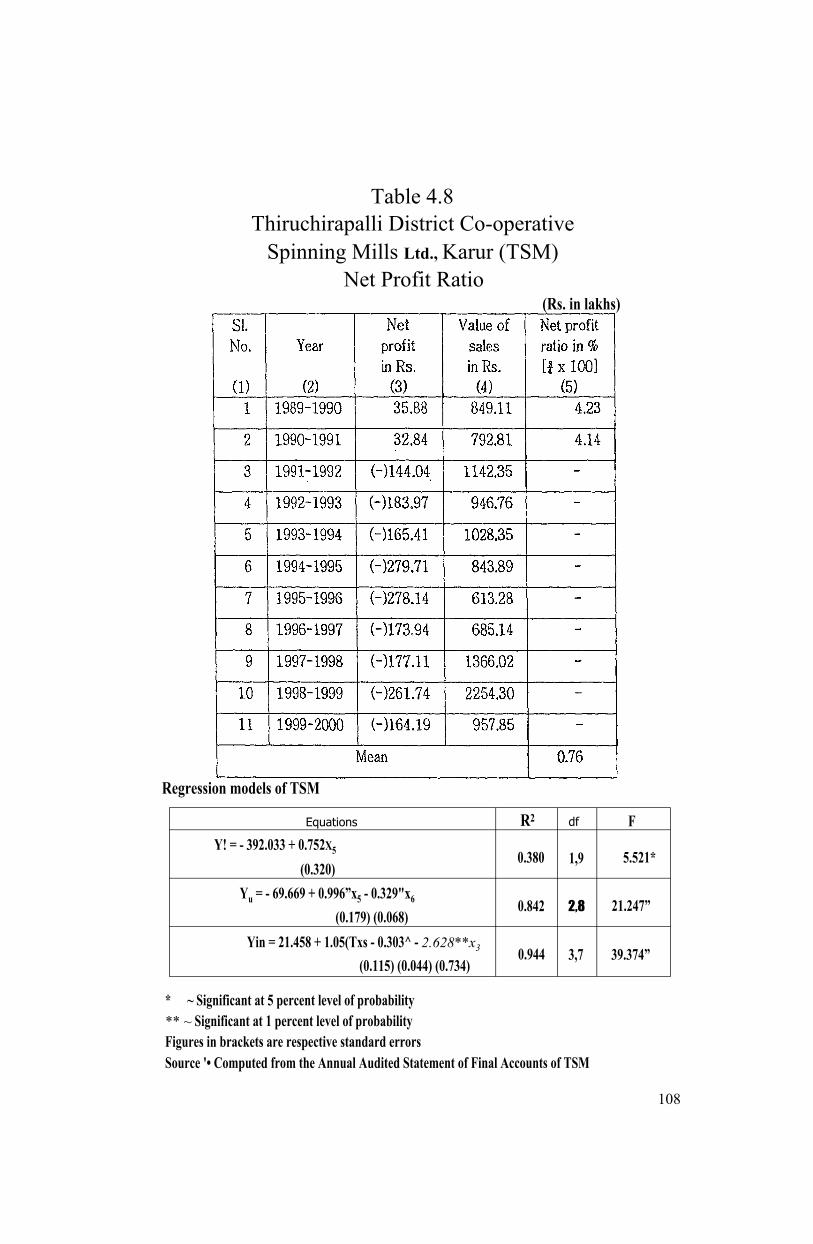

Net profit ratios of TSM are furnished in Table 4.8. This CSM

achieved net profit of about 4.00 percent during the first two years,

when it earned gross profit and incurred net loss in the remaining nine

years under study, because of gross loss. Among fixed costs, interest

charges claimed largest amount especially in 1993—94 and during 1995-

98. It may be noted that there was a slump on sales in 1995-97.

Comparison of the performance in net profit/net loss and NVAM

suggests that net profit and NVAM were directly related and there was

inverse relationship between net loss and NVAM. During 1989-91, TSM

earned net profit and the period was marked by high amounts of

107

Table 4.8 Thiruchirapalli District Co-operative

Spinning Mills Ltd., Karur (TSM) Net Profit Ratio

(Rs. in lakhs)

Regression models of TSM

Equations R2 df FY! = - 392.033 + 0.752x5

(0.320)0.380 1,9 5.521*

Yu = - 69.669 + 0.996”x5 - 0.329"x6 (0.179) (0.068)

0.842 2,8 21.247”

Yin = 21.458 + 1.05(Txs - 0.303^ - 2.628**x3 (0.115) (0.044) (0.734)

0.944 3,7 39.374”

* ~ Significant at 5 percent level of probability** ~ Significant at 1 percent level of probability Figures in brackets are respective standard errorsSource '• Computed from the Annual Audited Statement of Final Accounts of TSM

108

NVAM. Similarly, TSM incurred heavy net loss in 1994-95, 1995-96

and 1998-99, when NVAM was at its lowest in TSM.

Regression analysis has yielded three models involving NVAM,

value of production and interest charges, which together accounted for

94.40 percent of the variations in net profit. Gross profit analysis

already indicated the influence of GVAM along with saleable waste and

labour cost on gross profit. Naturally NVAM continues to be crucial

factor in net profit. An increase of one lakh rupees in NVAM would rise

net profit by 1.05 lakh rupees, thus making NVAM as the most crucial

factor in net profit. Because of the negative relationship between value

of production and net profit, the second model can be ignored. As per

the third models interest charges account for 10.20 percent of changes

in net profit. An increase of one lakh rupees in interest charges would

reduce net profit by 2.63 lakh rupees. Thus NVAM and interest charges

are important for net profit.

Anna Co-operative Spinning Mills Ltd., Andipatty (ASM)

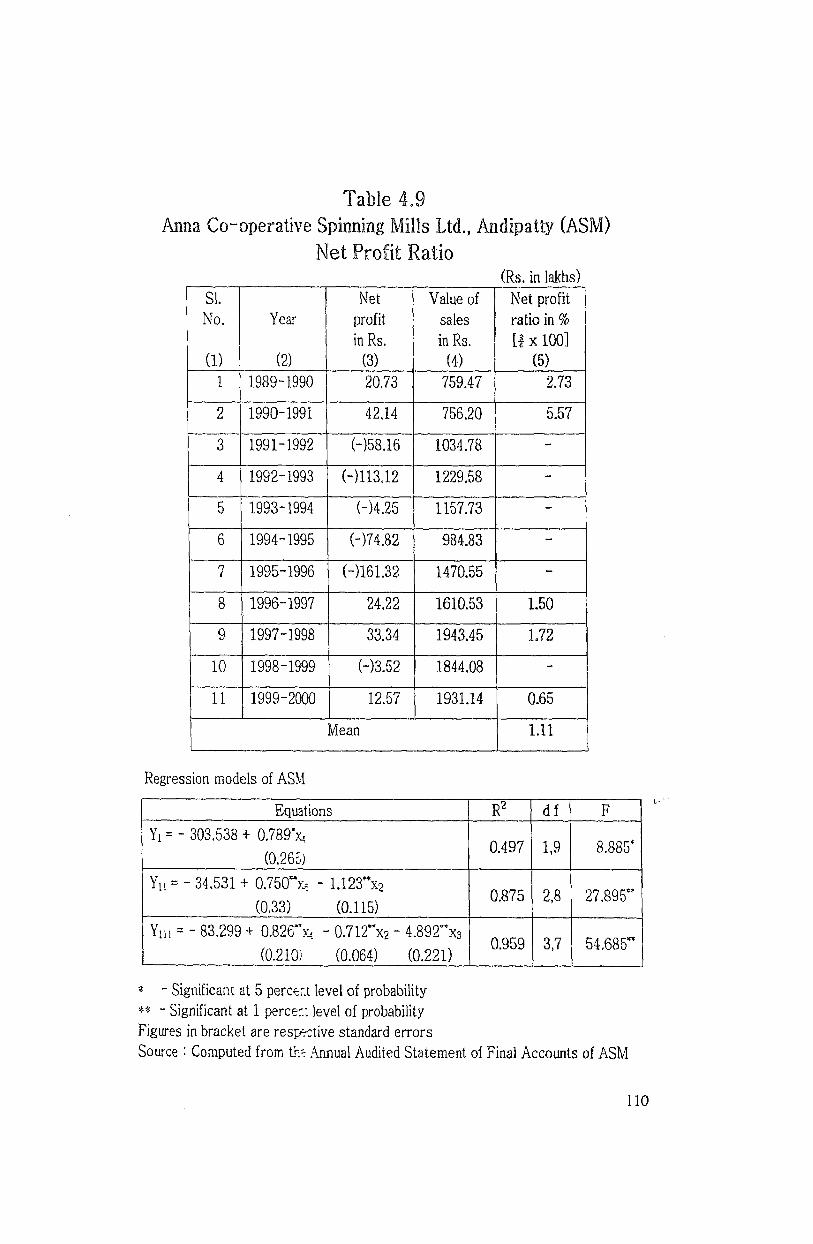

Net profit ratios of ASM are furnished in Table 4.9. As in gross

profit in net profit also ASM has registered better performance than

others, earning net profit in five out of eleven years. The net profit

ratios ranged between 5.57 percent in 1990-91 and 0.65 percent in

1999-2000. Gross profit of Rs.85.49 lakhs in 1998-99 could not prevent

net loss of Rs.3.52 lakhs, while gross profit of Rs.78.25 lakh in 1999-

2000 could yield net profit of Rs.12.56 lakh indicating uncontrolled

variations in fixed cost.

109

Though interest charges were the largest item of fixed costs, the

amount of interest remained reasonably stable, fluctuating between

Rs.48.39 lakh in 1989-90 and Rs.32.17 lakh in 1999-2000. Expenditure

on salaries registered considerably increase in 1995-96 and during

1997-2000. Therefore, the CSM has to control these two items of

expenditure in order to regulate fixed costs and improve net profit.

Also NVAM is another factor influencing net profit. Drastic reduction of

NVAM during 1991-92 and 1994-96 witnessed increase in net loss and

improvement of NVAM in the last four years, helped to raise net profit

in three years and minimise net loss in one year (1998-99).

Regression analysis has yielded three models involving

contingencies salary and interest charges. Contingency expenditure had

negative influence over net profit involving inverse relationship between

the two factors. However, the first model shows positive influence of

contingency expenditure on net profit and therefore the model can be

ignored. As per the second model, both contingency expenditure and

salary together influence 87.5 percent of variation in net profit. When

interest charges (in the third model) is included the three factors are

responsible for about 95.90 percent of changes in net profit. When

salary expenditure increases by one lakh rupees, net profit falls by

Rs.1.12 lakh. When interest charges raise by one lakh rupees, net profit

falls by Rs.4.89 lakh. Thus salary and interest charges are factors to be

reckoned with in ASM.

I l l

The South India Co-operative Spinning Mills Ltd., Pettai, Tirunelveli (PSM)

Data on net profit ratios of this CSM can be found in Table 4.10.

Though PSM earned gross profit in three years, it could yield net profit

in the first two years only, when the net profit ratio fell from 6.26

percent to 1.49 percent. In this CSM also the largest item of fixed cost

"was interest charges which rose sharply from 1990-91 onwards and

interest charges exceeded Rs.100 lakh in 1995-96 and the CSM paid

Rs.237.22 lakh as interest in 1999-2000. Thus, interest charges was a

decisive factor in raising the amount of net loss in PSM. Administrative

expenses were stable during the period under review. The CSM

suffered reduction of net profit in 1990~91, despite there was

substantial increase in the amount of NVAM. However decrease in

NVAM was among the factors responsible for growing net loss,

especially during the last three years.

Regression analysis of net profitability has yielded three models

involving interest charges, NVAM and value of production. Interest

charges would account for 68.00 percent of variation in net profit. An

increase of one lakh rupees in interest charges would reduce the net

profit by Rs.0.26 lakh. Interest charges and NVAM would be responsible

for 82.80 percent of variation in net profit. An increase of one lakh

rupees in NVAM would yield increase in net profit by Rs.0.58 lakhs.

Interest charges, NVAM and value of production would explain

93.30 percent of variation in net profit. Since the third model shows

112

These CSMs can improve NVAM largely through increase in

GVAM and control over depreciation. The CSMs have to regulate the

salaries and contingencies on the basis of capacity to pay. Improvement

of gross profit would be the major factor contributing to net profit aided

by control over fixed costs like interest charges, depreciation, salaries

and contingencies. .

Return on Investment (ROI) Analysis

Return on investment (ROI) is a measure of evaluating the

wisdom of investment decision as well as competence of management of

long term finance. As already noted, gross loss incurred by the sample

CSMs in most of the period under review and consequent net loss have

considerably eroded the efficacy of the concept of return on

investments. Still exercise in ROI will show the position of long term

funds and the exact condition of the management of fixed capital.

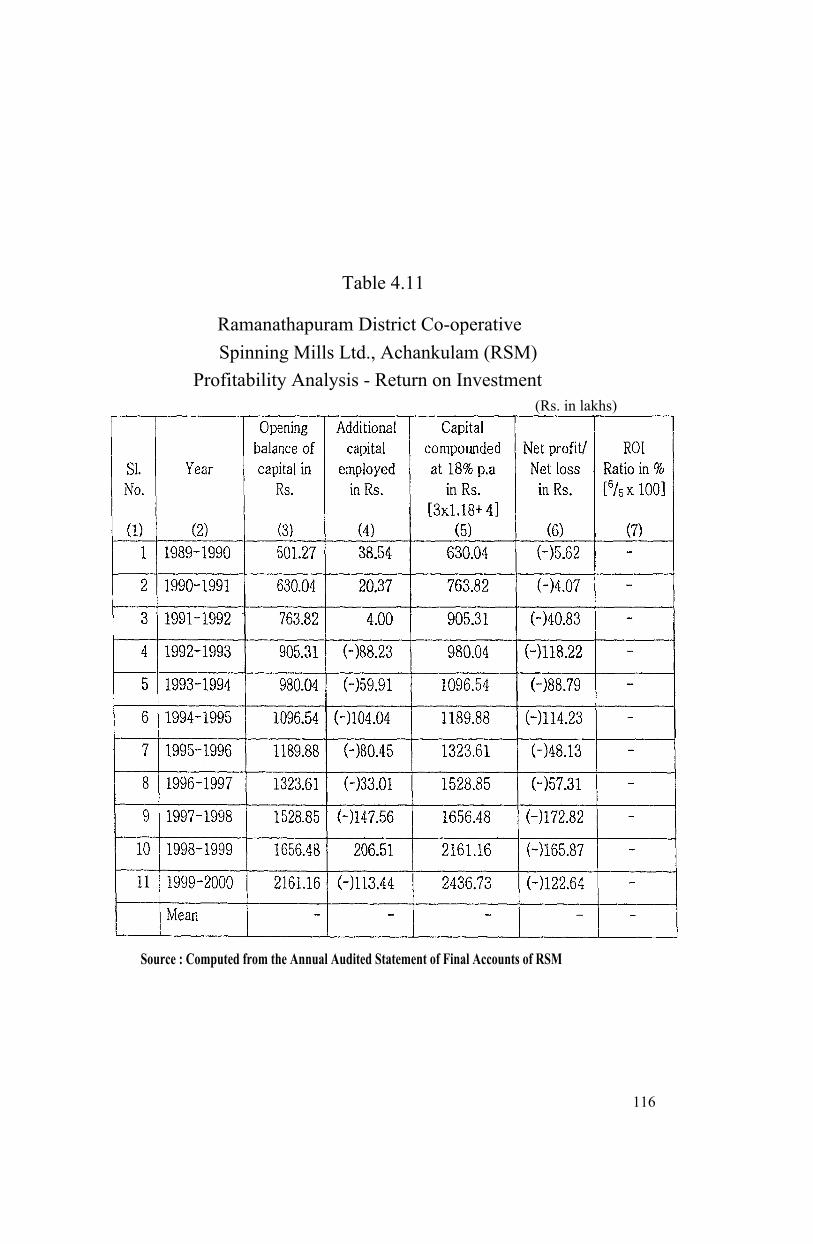

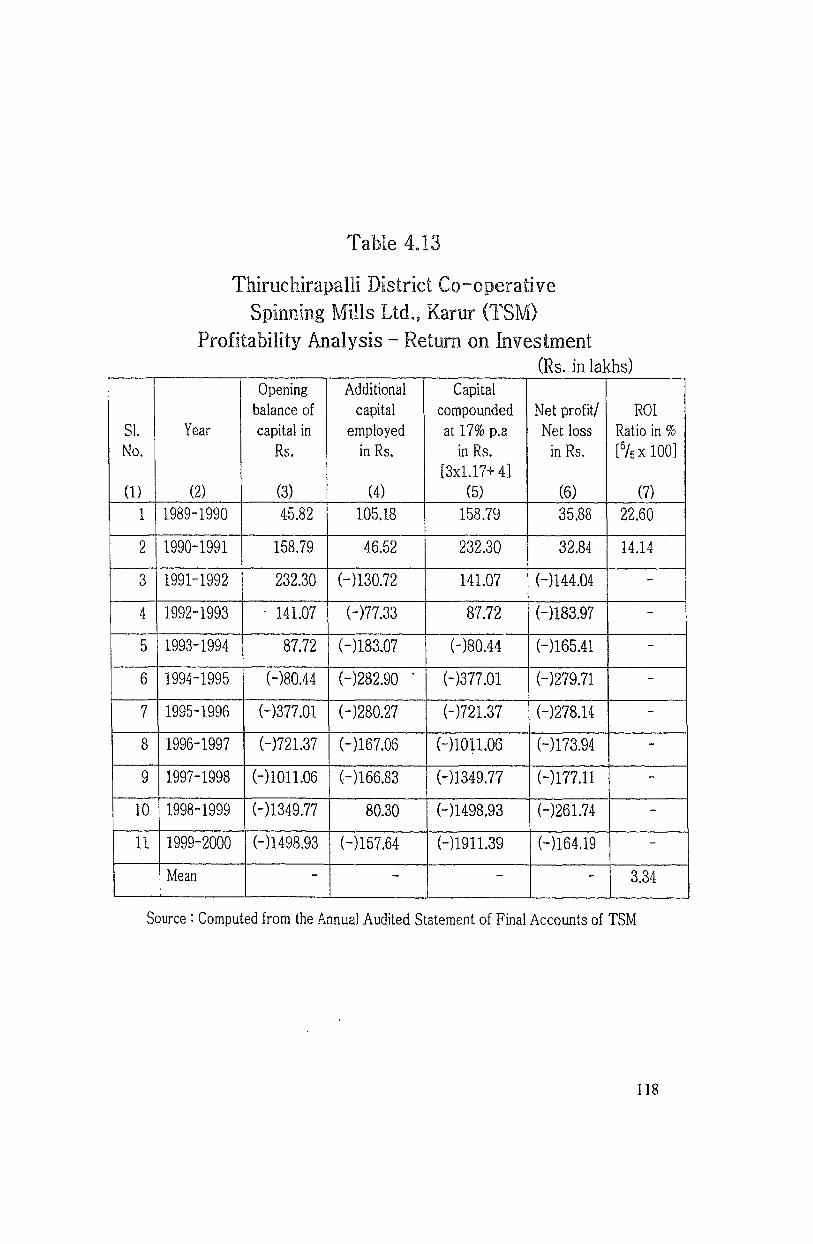

Data on return on investments for the sample CSMs can be found

in Table 4.11 to 4.15. For most of the years of study, ROI could not be

calculated because of net loss suffered by the sample CSMs. While ASM

could report ROI for five years, RSM incurred net loss during the entire

period. For the remaining three CSMs (SSM, TSM, and PSM), ROI could

be calculated for one or two years. In profitable years ROI could

exceed 14.00 percent in three years only - during 1989-91 in TSM and

in 1989-90 in PSM. In the other CSMs, ROI has been less than 10

percent.

115

negative influence of value of production over net profit, the model is

ignored. Thus, interest charges and NVAM are the main factors

influencing net profit. Thus PSM should concentrate on reduction of

interest charges and improvement of NVAM and value of production.

Summary of Net Profit Analysis

The most important determinant of net profit in a business is the

gross profit available for meeting fixed costs. Among the sample CSMs,

ASM earned gross profit in seven out of eleven years under review.

The remaining four CSMs earned gross profit in fewer years, incurring

gross loss in seven to nine years in the period of the study. The gross

loss was the most important reason for the lackluster performance inI

respect of net profit. Some CSMs in the sample incurred net loss,

despite gross profit.

Regression analysis of the factors influencing net profit has

helped us to identify reasons responsible for variations in net profit and

net loss. Interest charge is found to be the most pervasive factor

influencing profitability in 4 CSMs, followed by NVAM in 3 CSMs,

salaries and value of production in 2 CSMs each and contingencies in

one CSM. Sound management of interest charges involves full utilisation

of fixed capital and optimum turnover of working capital. Improvement

of production, GVAM and sales, which have been recommended for

improvement of gross profit, would result in maximisation of utilisation

of fixed assets.

114

These CSMs can improve NVAM largely through increase in

GVAM and control over depreciation. The CSMs have to regulate the

salaries and contingencies on the basis of capacity to pay. Improvement

of gross profit would be the major factor contributing to net profit aided

by control over fixed costs like interest charges, depreciation, salaries

and contingencies.

Return on Investment (ROI) Analysis

Return on investment (ROI) is a measure of evaluating the

wisdom of investment decision as well as competence of management of

long term finance. As already noted, gross loss incurred by the sample

CSMs in most of the period under review and consequent net loss have

considerably eroded the efficacy of the concept of return on

investments. Still exercise in ROI will show the position of long term

funds and the exact condition of the management of fixed capital.

Data on return on investments for the sample CSMs can be found

in Table 4.11 to 4.15. For most of the years of study, ROI could not be

calculated because of net loss suffered by the sample CSMs. While ASM

could report ROI for five years, RSM incurred net loss during the entire

period. For the remaining three CSMs (SSM, TSM, and PSM), ROI could

be calculated for one or two years. In profitable years ROI could

exceed 14.00 percent in three years only - during 1989-91 in TSM and

in 1989~90 in PSM. In the other CSMs, ROI has been less than 10

percent.

115

Table 4.11

Ramanathapuram District Co-operativeSpinning Mills Ltd., Achankulam (RSM)

Profitability Analysis - Return on Investment(Rs. in lakhs)

Source : Computed from the Annual Audited Statement of Final Accounts of RSM

116

Continuous net losses caused serious erosion in the capital base

in the sample CSMs. Among the five CSMs, three CSMs, namely, SSM,

TSM and PSM posted disastrous performance, which wiped out the

capital and saddled the CSMs with heavy net loss which amounted to

Rs.627.75 lakh in SSM, Rs. 1,911.39 lakh in TSM and Rs, 1,359.69 lakh in

PSM as on 31.03.2000. Without compounding, the accumulated loss in

the above three CSMs were Rs.546.58 lakh in SSM, Rs.l,168.00 lakh in

TSM and Rs.l,805.84 lakh in PSM as on 31.03.2000. Thus, the three

CSMs had completely lost capital and had huge net loss aggregating

Rs.3,520.42 lakh. In the remaining two CSMs (RSM and ASM), capital

base has been preserved despite net losses incurred during the period

under review. However, the actual amount of capital in these two CSMs

was far smaller than the compounded capital shown in column 5 for the

years 1999-2000 in Table 4.11 and 4.14. The actual amount of capital

in RSM as on 31.3.2000 was Rs. 144.05 lakh as against Rs.2,436.73 lakh

shown as compounded capital for the year 1999-2000. In ASM the

actual amount of capital left with ASM stood at Rs.770.14 lakh, whereas

the compounded capital was Rs.4,048.40 lakh for the year 1999-2000.

ASM was the only CSM where the amount of capital had grown during

eleven years from Rs.714.68 lakh in 1989-90 to Rs.770.14- lakh in

1999-2000. In RSM the amount of capital decreased from Rs.501.27

lakh to Rs. 144.05 lakh during the period under review. In other three

CSMs (SSM, TSM and PSM), capital has been displaced by the

accumulated loss as already noted. It may, therefore, be concluded that

out of five CSMs, RSM and ASM alone have chances of resurrection,

121

while the other three CSMs required extraordinary measures of

injecting new capital for discharging the accumulated net loss and

sustaining their operations.

Summary

Lackluster performance of the sample CSMs in profitability has

confirmed the hypotheses that the business operations of the CSMs

would not be profitable. The losses have been due to inadequacies in

value addition, production and sales as well as high costs of materials,

labour costs, saleable waste and contingencies. Thus, besides fall in

demand for yarn (due to fall in the production of handloom), internal

factors like selection and purchase of raw materials, wages and lack of

monitoring of production influenced the performance of these five

sample CSMs. The above causes of losses are inter-related and they

should be tackled by a package of remedial measures. Localisation of

procurement of cotton will help to reduce the material cost, saleable

waste and enhance production, value addition and sales. The resulting

acceleration in operation would help to bring down the incidence of

interest and contingencies charges. Further the CSMs should modernise

their facilities for reducing cost and improving quality, since

modernisation is the most vital factor for profitability. The CSMs should

ensure that their SPP is atleast equal to SITRA’s standard to ensure

productivity and profitability.

122

1 ] Gupta R.K., Profitability, Financial Structure and Liquidity, Printwell Publishers, Jaipur, 1989, p. 28.

2l Harley W.C.F., Cash Planning, Forecasting and Control, Business Books Limited, London, 1979, p. 3.

3] Jain C.P., Profit Planning and Control, National Publishing House, Jaipur, 1989, p. 3.

4l Barthwal, Industrial Economics, Willey Eastern Ltd., New Delhi, 1992, Pp. 211-226.

5] Hampton J.J., Financial Decision Making Concepts, Problems and Cases, Prentice Hall of India, New Delhi, 1983, p. 10.

3] Patel M., Corporate Financial Objectives, some Emperical findings Agarval (Ed), Readings in Financial Management, Indian Institute of Finance, New Delhi, 1995, p. 7.

7 ] Peacock M.A. and Taylor A.H., Handbook of Financial Planning, Gower Publishing Co. Ltd., Westwoods, UK, 1981, p. 145.

3] John Black, Dictionary of Economics, Oxford University Press, Oxford, 1997, p. 273.

3] Keirstead B.S., Capital Interest and Profits, MacMillan Ltd., 1959, p. 6.

3] Barry Render, Ralph M. and Stair Sr., Quantitative Analysis for Management, Prentice Hall Publishing Inc., New Jersey, 1997, p. 3.

L ] Howard B.B. and Upton M., Introduction to Business Finance, McGraw Hill, New York, 1961, p. 160.

I ] Weston J.F. and Bringham E.F., Essentials of Managerial Finance, Hold Renechart & Winston, New York, 1971, p. 48.

i 3 Barthwal, Industrial Economics, Willey Eastern Limited, New Delhi, 1992, p. 211.

I] Natarajan S., “Profit maximisation”, The Management Accountant, Volume IX, November 1974, p. 241.

j] Stigler G.J., The Theory of Price, Prentice Hall, New Jersey, 1952, p. 82.

References

123