chapter 4 payment systems in e-commerce

TRANSCRIPT

Chapter 4

Payment Systems & E-Banking

By:

Marya Sholevar

Department of Banking and Finance

All business activities need the support of payment system, so does the e-commerce. As e-commerce process transactions through the Internet, it requires a more secure, stable and efficient payment system for supporting commerce done electronically. By the success of online banking and online payment in recent years, the market seems to have a solution for e-commerce. Online payment can be conducted in different means, such as intelligent card (IC), e-check, e-Wallet, e-Cash etc. This chapter briefly introduces the online banks and the online payment tools that are common used in e-commerce.

1-Payment Systems

2-1 Cash

2-2 Checking Transfer

2-3 Credit Card

2-4 Stored Value2-5 Accumulating Balance

2-Types of Payment Systems

-Legal tender defined by a national authority to represent value-Most common form of payment in terms of number of transactions-Instantly convertible into other forms of value without intermediation of any kind-Portable, requires no authentication, and provides instant purchasing power-Free” (no transaction fee), anonymous, low cognitive demands-Limitations: easily stolen, limited to smaller transaction, does not provide any float

2-1 Cash

-Funds transferred directly via a signed draft or check from a consumer’s checking account to a merchant or other individual-Most common form of payment in terms of amount spent-Can be used for both small and large transactions -Some float-Not anonymous, require third-party intervention (banks) -Introduce security risks for merchants (forgeries,stopped payments), so authentication typically required

2-2 Checking Transfer

-Represents an account that extends credit to consumers, permitting consumers to purchase items while deferring payment, and allows consumers to make payments to multiple vendors at one time -Credit card associations: Nonprofit associations (Visa, MasterCard) that set standards for issuing banks-Issuing banks: Issue cards and process transactions-Processing centers (clearinghouses): Handle verification of accounts and balances

2-3 Credit Card

Accounts created by depositing funds into an account and from which funds are paid out or withdrawn as needed

*Examples: Debit cards, gift certificates,prepaid cards, smart cards

2-4 Stored Value

-Accounts that accumulate expenditures and to which consumers make period payments

Examples: utility, phone, American Express accounts

2-5 Accumulating Balance

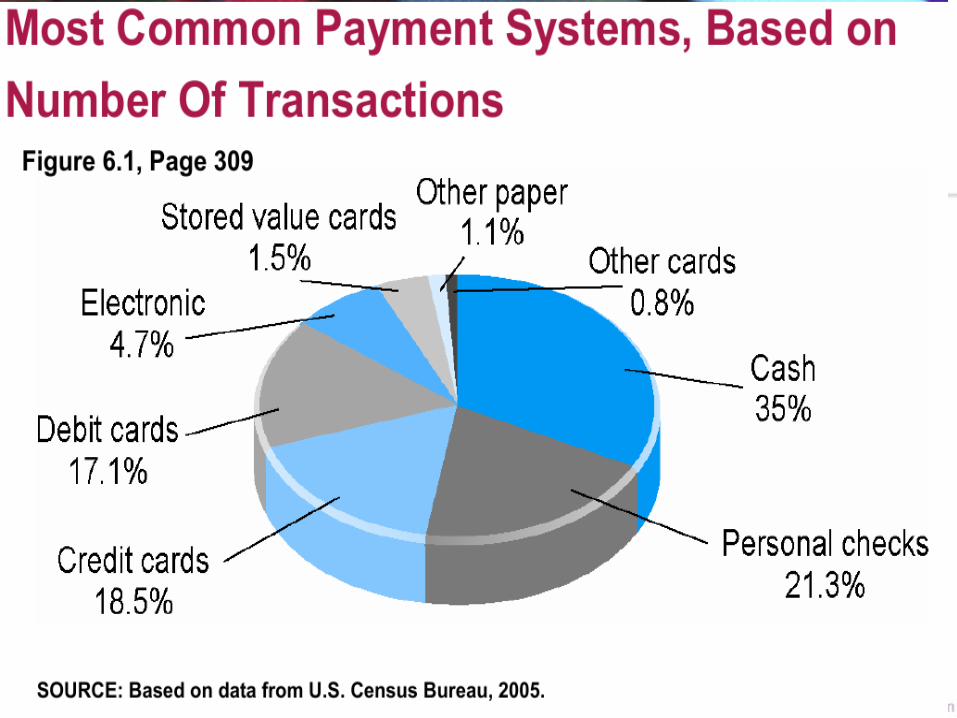

-Credit cards are dominant form of online payment, accounting for around 80% of online payments in 2005-New forms of electronic payment include:

3-1 Digital Wallet3-2 Digital cash3-3 Online stored value systems3-4 Digital accumulating balance payment systems3-5 Digital credit accounts3-6 Digital checking

3-Current Online Payment Systems

-Concept of digital wallet relevant to many of the new digital payment systems-Seeks to emulate the functionality of traditional wallet-Most important functions:

*Authenticate consumer through use of digital certificates or other encryption methods

*Store and transfer value*Secure payment process from consumer to merchant

-Most common types are client-based software applications: Gator eWallet.com, asterCard Wallet

3-1 Digital Wallets

-One of the first forms of alternative payment systems-Not really “cash”: rather, are forms of value storage and value exchange that have limited convertibility into other forms of value, and require intermediaries to convert-Many of early examples have disappeared; concepts survive as part of P2P payment systems

3-2 Digital Cash

-Permit consumers to make instant, online payments to merchants and other individuals based on value stored in an online account -Rely on value stored in a consumer’s bank, checking, or credit card account

3-3 Online Stored Value Systems

-Another kind of stored value system based on credit-card sized plastic cards that have embedded chips that store personal informationTwo types:

*Contact*Contactless

-Examples: Mondex, Octopus

3-3-1 Smart Cards as Stored Value Systems

-Allows users to make micropayments and purchases on the Web, accumulating a debit balance for which they are billed at the end of the month-Examples: Qpass, Valista, Clickshare, Click & Buy, Peppercoin

3-4 Digital Accumulating Balance Payment Systems

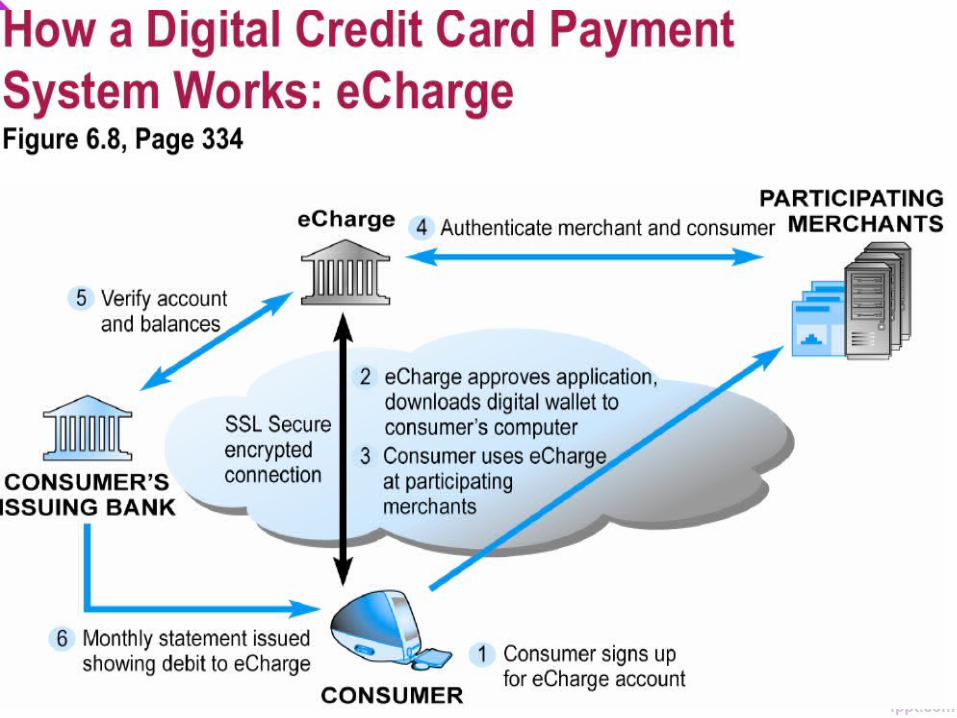

-Extend the functionality of existing credit cards for use as online shopping payment tools-Focus specifically on making use of credit cards safer and more convenient for online merchants and consumers-Example: eCharge

3-5 Digital Credit Card Payment Systems

-Extend the functionality of existing checking accounts for use as online shopping payment tools

-Examples: PayByCheck, Western Union MoneyZap

3-6 Digital Checking Payment Systems

-Mobile payment (m-payments) systems not very well established yet in U.S, but with growth in Wi-Fi and 3G cellular phone systems, this is beginning to change-Juniper Research predicts global m-commerce will total at least $88 billion by 2009, majority of transactions will be micro-m-payments

4- Digital Payment Systems and the Wireless Web

-Online payment systems for monthly bills EBPP expected to grow rapidly, to an estimated 40% of all households by 2007 Main business models in EBPP market include:

*Biller-direct

*Consolidator

5- Electronic Billing Presentment and Payment (EBPP)

-Processed in much the same way that in-store purchases are -Major difference is that online merchants do not see or take impression of card, and no signature is available (CNP transactions) -Participants include consumer, merchant, clearinghouse, merchant bank (acquiring bank) and consumer’s card issuing bank

6- How an Online Credit Card Transaction Works

-Security: neither merchant nor consumer can be fully authenticated -Cost: for merchants, around 3.5% of purchase price plus transaction fee of 20 – 30 cents per transaction -Social equity: many people do not have access to credit cards (young adults, plus almost 100 million other adult Americans who cannot afford cards or are considered poor risk)

6-1 Limitations of Online Credit Card Payment Systems

-E-channels enable financial transactions from anywhere and allow non-stop working time. E-channels like: Internet, WAP based mobile network, Automatic Telephone, ATM network, …-E-Bank is transforming banking business into e-Business through utilizing e-Channels.-Customers’ requests are:

*Non-stop working time*Using services from anywhere

E-channels provide:-Working time 7/24h-Great flexibility

7- Electronic Banking7-1 Introduction

-Electronic Funds Transfer (EFT) is a system of transferring money from one bank account directly to another without any paper money changing hands. EFT is safe, secure, efficient, and less expensive than paper check payments and collections. EFT offers several services that consumers may find practical to be as a means of payment.

7-1 Introduction

Electronic money is money which exists only in banking computer systems and is not held in any physical form.

7-2 Definition of Electronic Money

The following terms all refer to one form or another of electronic banking: -personal computer (PC) banking, -Internet banking, -virtual banking,-online banking, -home banking, -remote electronic banking, -and phone are banking. PC banking and Internet or online banking is the most frequently used designations.

7-3 Electronic Banking Forms

PC banking is a form of online banking that enables customers to execute bank transactions from a PC via a modem. In most PC banking ventures, the bank offers the customer a proprietary financial software program that allows the customer to perform financial transactions from his or her home computer. The customer then dials into the bank with his or her modem, downloads data, and runs the programs that are resident on the customer’s computer.

7-3 Electronic Banking Forms

Internet banking, sometimes called online banking, is an outgrowth of PC banking. Internet banking uses the Internet as the delivery channel by which to conduct banking activity.An Internet banking customer accesses his or her accounts from a browser— software that runs Internet banking programs resident on the bank’s World Wide Web server, not on the user’s PC. Internet banks are also known as virtual, cyber, net, interactive, or web banks.

7-3 Electronic Banking Forms

7-4-1 Choice and Convenience for Customers:7-4-2 Attracting High Value Customers:7-4-3 Enhanced Image7-4-4 Increased Revenues7-4-5 Load Reduction on Other Channels7-4-6 Cost Reduction7-4-7 Organizational Efficiency7-4-8 Easier Expansion:

7-4 Benefits of E-Banking (Importance of E-Banking)

In 70’s, banks started to establish centralized data processing centers.Essentially the roles of these data processing centers are:-collect the handwritten documents from branches -compile the documents-manual data entry by the operators-generate reports for the bank staff and the central bank-execute some banking transactions

7-5 Technology Commencement in Banking

In the mid-1980s, banks accepted product based banking and competed with their products.Banks developed new products for their customers.-Credit card-Credit deposit account (Super Account)-Debit cardsBeside branch, banks brought new channels to give better service to their customers.-ATM-POS

7-6 Product and Service Based Banking

Debit Cards are plastic cards, which look like credit cards, but are electronically connected to a card holder’s depository institution account. Money is automatically withdrawn from the designated account when a purchase is made.Debit cards can be used when there is not enough money in the account, which will result in a non- sufficient fund fee.

7-6-1 Debit Card

Debit cards require the use of PIN (Personal Identification numbers).Personal Identification Number (PIN) is a number that is entered in at an Automated Teller Machine (ATM) or Point of Sale Terminal (POS)

This confirms that the individual is authorized to access that particular account.

7-6-1-1 Personal Identification Numbers(PIN)

Automated Teller Machines (ATM’s) are electronic computer terminals which offer automated, computerized banking.Transactions allowed may include:-Deposits-Cash withdrawals-Transfers between accounts-Account balance information

7-6-2 Automated Teller Machines

Point of Sale Terminal (POS), are located at stores and allows the customer to use a debit card to make a purchase.-A debit card’s magnetic strip is swiped through the POS. -After the required PIN is provided, the transaction is authorized.-If the purchase is under $25.00 a signature may not be required.

7-6-3 Point of Sale Terminal (POS)

SWIFT or Society for Worldwide Interbank Financial Telecommunication):is a co-operative society, founded in 1974 by seven international banks, which operate a global network to facilitate the transfer of financial messages.-transports financial messages in a highly secure way -banks can exchange data for funds transfer between financial institutions-Can do money transfer, currency exchange, loan, deposit etc-Improve the productivity and avoid error

7-6-4 SWIFT

SMS banking uses short text messages sent through the client’s mobile phone.-Kept updated on important information when it concerns your business matters by SMS alert -A client can automatically receive information about his account balance: an SMS is sent to the client immediately after a certain operation is performed, or on request: a client sends the bank a correctly formatted message which processes it and answers the client’s request by SMS.Such as: *Check balance * Account Transfer

7-6-5 SMS Banking

-Customers can use their personal computers at home, office or everywhere to access their accounts for transactions by subscribing to and dialing into the banks’ Intranet proprietary software system by use of password.-More common among corporate customers compared to individual customers.-Reducing cost, increasing speed and improved flexibility of business transactions. Such as Account balance, request transfers between accounts, and pay bills electronically.

7-6-6 Internet Banking

• Online banking and e-banking are modern ways to conduct banking transactions sitting in the comfort of one’s own hoe without going to the bank physically.• E-banking is broader in spectrum than online banking in the sense that it encompasses the use of ATM cards for withdrawal of money and making payments to merchants even without going online.

7-7 Online Banking vs e-Banking

Thank You!