chapter 3 gross income: concepts and inclusions solutions...

TRANSCRIPT

CHAPTER 3

GROSS INCOME: CONCEPTS AND INCLUSIONS

SOLUTIONS TO PROBLEM MATERIALS

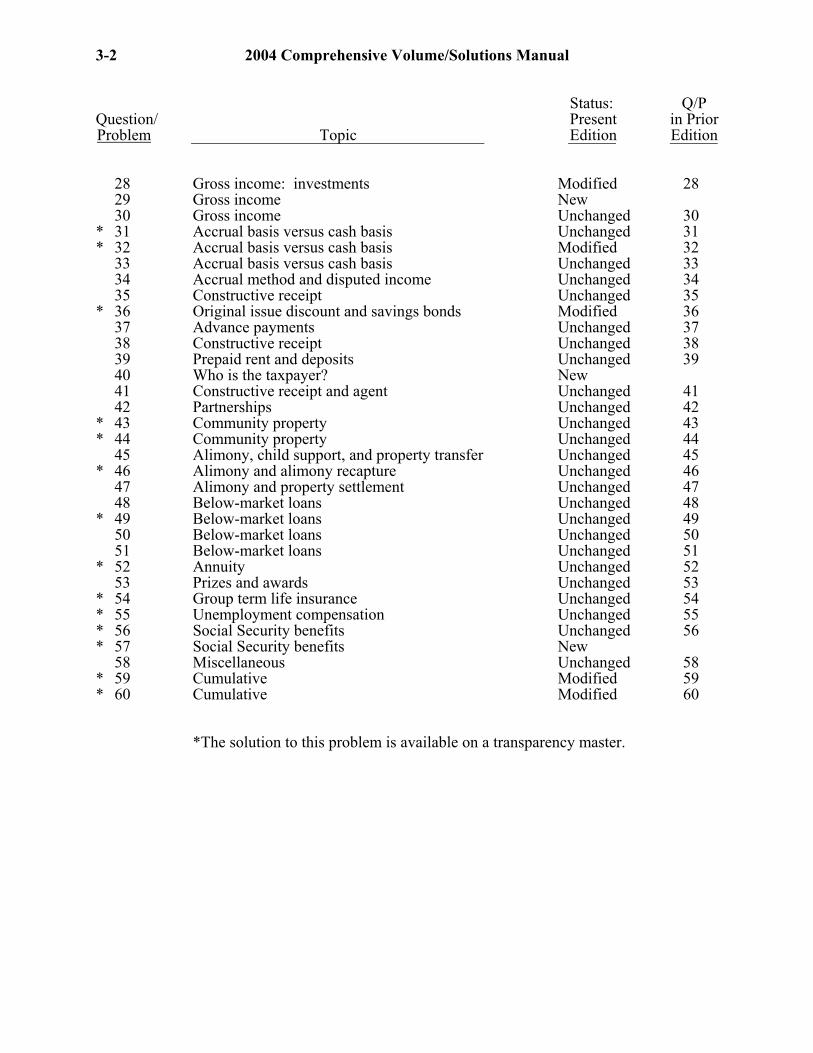

Status: Q/P Question/ Present in Prior Problem Topic Edition Edition

1 Examples of gross income items in the Form 1040 instructions

Unchanged 1

2 Economic versus taxable income Modified 23 Issue ID Unchanged 34 Realization rationale New 5 Recovery of capital Unchanged 56 Constructive receipt and agent New 7 Cash method Unchanged 78 Issue ID New 9 Original issue discount New

10 Original issue discount Unchanged 1011 Accrual basis and prepaid income New 12 Who is the taxpayer? Unchanged 1213 Who is the taxpayer? Unchanged 1314 Who is the taxpayer? Modified 1415 Who is the taxpayer? Unchanged 1516 Community property Unchanged 1617 Transfer of property: divorce Unchanged 1718 Issue ID Unchanged 1819 Alimony and property settlement Unchanged 1920 Below-market loans Unchanged 2021 Below-market loans Unchanged 2122 Issue ID Unchanged 2223 Annuity Unchanged 2324 Group-term life insurance Unchanged 2425 Social Security benefits Unchanged 2526 Economic versus taxable income Unchanged 2627 Issue ID Unchanged 27

3-1

3-2 2004 Comprehensive Volume/Solutions Manual

Status: Q/P Question/ Present in Prior Problem Topic Edition Edition

28 Gross income: investments Modified 2829 Gross income New 30 Gross income Unchanged 30

* 31 Accrual basis versus cash basis Unchanged 31* 32 Accrual basis versus cash basis Modified 32

33 Accrual basis versus cash basis Unchanged 3334 Accrual method and disputed income Unchanged 3435 Constructive receipt Unchanged 35

* 36 Original issue discount and savings bonds Modified 3637 Advance payments Unchanged 3738 Constructive receipt Unchanged 3839 Prepaid rent and deposits Unchanged 3940 Who is the taxpayer? New 41 Constructive receipt and agent Unchanged 4142 Partnerships Unchanged 42

* 43 Community property Unchanged 43* 44 Community property Unchanged 44

45 Alimony, child support, and property transfer Unchanged 45* 46 Alimony and alimony recapture Unchanged 46

47 Alimony and property settlement Unchanged 4748 Below-market loans Unchanged 48

* 49 Below-market loans Unchanged 4950 Below-market loans Unchanged 5051 Below-market loans Unchanged 51

* 52 Annuity Unchanged 5253 Prizes and awards Unchanged 53

* 54 Group term life insurance Unchanged 54* 55 Unemployment compensation Unchanged 55* 56 Social Security benefits Unchanged 56* 57 Social Security benefits New

58 Miscellaneous Unchanged 58* 59 Cumulative Modified 59* 60 Cumulative Modified 60

*The solution to this problem is available on a transparency master.

Gross Income: Concepts and Inclusions 3-3

CHECK FIGURES

26.a. 26.b. 26.c. 26.d. 26.e. 26.f. 27. 28. 29.a. 29.b. 29.c. 30.a. 30.b. 30.c. 31.a. 31.b. 31.c. 32. 33. 34. 35.a. 35.b. 35.c. 36.a. 36.b. 37.a. 37.b. 37.c. 38.a. 38.b. 39.a. 39.b. 40.a. 40.b. 41.a.

Economic gain $1,000; gross income $4,000. Economic income $15,000; gross income $15,000. Economic income $0; gross income $800. Economic income $800; gross income $0. Economic income $10,000; gross income $0. Economic income $1,000; gross income $1,000. Use the cash method. Alternative a. yields the greater after-tax value. Gross income $500 ($200 + $300). Gross income $0. Gross income $0. Gross income $1,500. Gross income $50,000. Gross income $0. Cash basis income $150,000. Accrual basis income $170,000. Cash method. Gross profit $145,000. Accrual method increases gross income by $75,000. Color should report $800 in 2004. Include $110,000 in 2003. Include $8,000 in 2002. Include $8,000 in 2003. $4,416. $934 interest income on 2-year certificate; $0 interest income on 1-year certificate. Gross income of $1,200 may be deferred until 2003. Gross income $590 in 2003. Gross income $450 ($1,200 – $750). Actually received $180,000; constructively received $0. She may be in a lower tax bracket in 2005. Report in the year of receipt $400 under option 1, $800 under option 2, and $0 under option 3. Third option. $12,000 for Gus and $12,000 for corporation. $12,000 flows through S corporation. Corporation recognizes $3,000; Tracy

41.b. 41.c. 42. 43.a. 43.b. 43.c. 44.a. 44.b. 45.a. 45.b. 45.c. 46.a. 46.b. 47. 48. 49. 50.a. 50.b. 50.c. 51.a. 51.b. 52.a. 52.b. 52.c. 53.a. 53.b. 53.c. 54.a. 54.b. 55. 56.a. 56.b. 56.c. 57. 58.a. 58.b. 58.c 58.d. 59. 60.

Same as a. Corporation recognizes $0 in 2003; Tracy recognizes $0 in 2003. $100,000. Diego $59,000; Carmen $59,000. Split evenly. Diego $48,000; Carmen $70,000. Doug $50,800; Liz $54,900. Doug $52,850; Liz $52,850. No tax consequences. Monthly gross income to Nell $1,000; payments are deductible to Kirby. No tax consequences—child support. $85,000. $72,500 alimony recaptured Year 3. Gross income increases $4,500. Accept 6% loan from Hal. Compensation $2,170, interest income $1,273. $0 imputed interest. $0 imputed interest. Imputed interest $225. Compensation income and interest expense to Vito $550; compensation expense and interest income to Vito, Inc. $550. Interest income and dividends paid to the corporation in 2003 $400; interest expense and dividend income to Vito in 2003 $400. Gross income $9,231. Gross income $24,000. Loss $36,923; gross income $9,231. $110,000. $75,000. $0. Alice $72; Kay $1,500. $1,500. $100,440. $29,750. No. $36,900. Reduction if retire of $7,250. The $70,000 is taxable. $7,140 is taxable. $1,200 is taxable. Donna must include one-half of husband’ winnings. Refund due $417. Refund due $1,849.

3-4 2004 Comprehensive Volume/Solutions Manual

recognizes $0.

Gross Income: Concepts and Inclusions 3-5

DISCUSSION QUESTIONS 1. The broad concept of gross income has served the Federal income tax system very well.

An attempt to provide a complete list would probably be futile and would impede the IRS in addressing new transactions. When a never before encountered transaction or event occurs, the IRS could be bound to apply the list which could result in certain sources of income not being taxed. p. 3-3

2. a. The mere appreciation in value of $3,000 ($8,000 – $5,000) is not included in the

taxpayer’s gross income. The economist would include $3,000 in income. b. The economist would include in income the rental value of the owner’s home.

Such imputed income is not gross income for tax purposes. c. The bargain purchase would be considered income under both the accounting and

economic concepts of income. For tax purposes, the bargain purchase element probably would be treated as a constructive dividend to the shareholder.

d. The economist would identify no gain on this transaction. The appreciation of the

property would have been taken into income by the economist over the past three years. The insurance payment would be an exchange for property of like value which has no effect on the taxpayer’s net worth. For tax purposes a gain of $4,000 would be recognized since property with a basis of $2,000 was given up in exchange for cash of $6,000.

e. Both the economic and tax constructs of income would require recognition of the

fair market value of the coins as income when they were found. The taxpayer’s net worth would increase as a result of finding the coins, and for tax purposes, the discovery constitutes a realization event.

pp. 3-3 to 3-5

3. Charley received something of value from the casino. Under the broad concept of

income, the airfare and hotel accommodations would be considered income. However, Charley could argue that the income should be matched with his $15,000 in gambling losses on the trip, and when the income and losses are combined, the net effect is an economic loss. As will be discussed later in the text, the net loss is not deductible, but at least the gambling losses can be used to offset the income from his gambling activities. pp. 3-3 to 3-5

4. The tax laws encourage do-it-yourself activities. If Tom paints his house, the $90 he

saved is not included in gross income. He foregoes only $73 [(1-.27)($100)] in after-tax income from not working and earnings $100. This reasoning assumes that Tom can paint as fast as someone he would hire (i.e., the time consumed is the same). pp. 3-3 and 3-4

5. Northern should report the amount received as a recovery of capital. It is impossible to

determine the cost of the property rights that are being surrendered by Northern. Therefore, if the amount received from the Long Cable Company is less than Northern’s cost of the land, no gain is recognized. pp. 3-6 and 3-7

6. The employer is required to include the $3,000 in gross income in 2003, when the

employer’s agent receives the payment from the customer. pp. 3-7 to 3-10 and 3-16

3-6 2004 Comprehensive Volume/Solutions Manual

7. a. The income should be reported in 2004. In 2003, Jared has not received anything of value.

b. The significance of when the income is recognized by Jared relates to (1) the time

value of money—if the tax is deferred, the present value of the tax decreases; and (2) the marginal tax rates—the taxpayer may be subject to different rates between years because of changes in the tax law, changes in his or her taxable income, changes in the taxpayer’s filing status, and changes in the entity status.

pp. 3-7 to 3-9 8. a. The following issues are suggested from the facts presented:

• Is the cash method an appropriate accounting method for a farmer? See Chapter 15.

• Does Selma have any income when the hay is harvested?

• Is any income recognized when part of the hay is fed to the cattle?

• Is any income recognized when part of the hay is traded for a piece of equipment?

b. Selma’s gross receipts are $750 and her cost of goods sold is $500 ($1,000 X 50%). Therefore, her gross income is $250 ($750 – $500). She does not recognize any income from the value of the hay she fed her cattle because realization will not occur until she has a transaction with another party (when the animals are sold). Note that the $500 cost of the hay she used to feed her cattle may be currently deducted by the cash basis farmer, although it was in fact a capital expenditure (i.e., see special treatment for farmers in Chapter 15).

pp. 3-8 to 3-10 9. The certificate of deposit contains original issue discount, which Alyson must include in

her gross income each year from 2002 through 2005. The annual amount to include in gross income is computed using the compound interest method. Alyson’s amount to include in gross income will be greater in 2003 because the interest earned in 2002 is added to the principal upon which the compound interest is computed in 2003. p. 13-11 and Example 14

10. a. Bethany’s interest income for 2003 is $343 ($4,291 X 8%). The bond has original issue discount of $15,709 ($20,000 – $4,291) which must be amortized over the life of the bond using the effective interest method.

b. Bethany’s basis for the bond on December 31, 2003 is $4,634 ($4,291 + $343). c. The interest income will be greater in 2010 than in 2003 because the interest is

compounding. The interest income recognized each year is added to the original cost of the bond and the 8% interest rate is applied to the cumulative investment.

pp. 3-11 and 3-12

Gross Income: Concepts and Inclusions 3-7

11. Under Revenue Procedure 71-21, if the services will be provided by the end of the tax year following the year of receipt, the unearned portion in the year of receipt can be deferred until the following year. pp. 3-13 to 3-15

12. If Rex sells the car, he must pay the tax on the gain of $3,800 ($9,000 – $5,200). If Rex

gives the automobile to his daughter and she sells it, she will be taxed on the gain of $3,800. Thus, the increase in value that is economically attributable to Rex will become his daughter’s income. If Rex is in a higher marginal tax bracket (probably the case), the family unit will generate tax savings by Rex’s daughter selling the car. Thus, gifts of appreciated property can be a useful tax planning concept. pp. 3-15 and 3-16

13. The tree produces the income, the fruit. In the case of services, the provider of the

services is the tree and therefore must pay the tax on the income he or she produces. The income from property is taxed to the owner of the property. p. 3-14

14. The employee is the agent for his or her employer, the principal. The income of $75 per

hour is earned by the principal through the agent and the income is attributed to the principal. The employee includes in his or her gross income the compensation paid by the employer. p. 3-14

15. The S corporation shareholders and the partners pay the tax on the income earned by the

S corporation and the partnership, regardless of whether the income is actually distributed to the owners. pp. 3-16 and 3-17

16. A joint return cannot be filed by Mike and Debbie, unless Debbie can be located and she

consents to filing a joint return. Mike cannot qualify as an abandoned spouse because he has no dependent children. On separate income tax returns for 2003, Mike and Debbie each must include one-half of the community’s income. This results because they live together for part of the year. Thus, Mike must include in his gross income his share of Debbie’s earnings for the year, including a share of Debbie’s post-separation earnings. pp. 3-17 to 3-19

17. Considering only taxes, Jean should accept the securities. The high basis in the stock

will provide Jean with a tax benefit. She will have a carryover basis of $115,000 in the securities. If she sells the securities for $100,000, she will recognize a $15,000 loss. She will be allowed to offset this loss against other capital gains. If she has no capital gains, she can offset $3,000 of the loss against ordinary income each year, as discussed in Chapter 2. Thus, the loss would offset other income on Jean’s income tax return. pp. 3-20 and 3-21

18. The following issues are suggested from the facts presented:

• Will gains and losses from the sale of property pursuant to the divorce be subject to tax?

• Are the child care payments deductible?

• Would payments with respect to William’s contribution toward her education be taxable to her?

• What is their filing status until the divorce has been completed?

3-8 2004 Comprehensive Volume/Solutions Manual

• Should the payments be arranged so that they are deductible by William and taxable to Abigail? If the payments are taxable to her, what additional amounts should she request in exchange for agreeing to terms that are tax favorable to William?

• Is the daycare that is being provided by the grandparents taxable to either William or

Abigail?

• Who will be able to claim April as a dependent?

pp. 3-19 to 3-22 19. Mary should consider the following tax considerations. The receipt of the $12,000 each

year for ten years would be taxable to her as alimony, provided the payments cease upon her death within the 10-year period. The receipt of the common stock would be a property settlement rather than being alimony. However, to evaluate this option, she needs to know Bob’s basis in the stock because his basis will become her basis. Thus, if she decided to sell the stock, she could have a taxable gain or loss. The installment payments have significant nontax issues such as the risk that Bob will be unable to make the payments. In addition, Mary should compare the present value of the installment payments (on an after-tax basis) with the value ($100,000) of the stock. For example, assuming a 15% marginal tax rate, the after-tax amount received each year is $10,200, and with an after-tax rate of return of 6%, the present value of future payments is only $80,200. pp. 3-20 to 3-22

20. Income is imputed to the lender so as to prevent the lender from shifting income to the

borrower who may be taxed at a lower tax rate. The rules presume that the lender would have earned some income from the funds in the absence of making the loan to the relative. The gift arises because the borrower is deemed to have accrued interest payable to the lender, which the lender forgives. pp. 3-22 to 3-27

21. The other tax effects on the corporation depend upon whether the loan is classified as (a)

an employer-employee loan, or (b) a corporation-shareholder loan. The employer-employee loan creates deductible compensation expense for the corporation equal to the corporation’s interest income. The corporation-shareholder loan is treated as a nondeductible dividend paid to the shareholder. pp. 3-23 to 3-27 and Concept Summary 3-2

22. The following issues are suggested from the facts presented:

• Is the corporation required to impute interest income on the loan to Brad?

• Is Brad required to recognize income from the loan proceeds?

• Is Brad required to recognize income in respect to the favorable interest rate? • Is the loan made to Brad in his capacity as a shareholder or as an employee?

• Is the loan subject to the original issue discount rules?

pp. 3-11 and 3-22 to 3-27

23. All of the payments in the eleventh year must be included in Betty’s gross income. She has recovered her investment of $73,600 as a return of capital over the 10 years (her life expectancy used in calculating the annuity exclusion percentage). pp. 3-27 to 3-30

Gross Income: Concepts and Inclusions 3-9

24. Mary must include in gross income the imputed insurance premium amount on $10,000:

($60,000 – $50,000) $1,000

(.43)(12 months) = $51.60

Larry did not receive any gross income during the year. He has merely received a promise from his employer. pp. 3-32 and 3-33

25. As an annuity, the recipient would receive return of capital treatment and inclusion in gross income for each dollar received. Individuals with low earnings would be taxed the same as high income individuals. The present formula, with the gross income floor below which the benefits are not taxed, benefits lower income individuals. p. 3-33

PROBLEMS 26. a. The taxpayer has a $1,000 economic gain on the sale because the taxpayer’s

economic income would be the selling price less the value of the asset as of the beginning of the year. Gross income for tax purposes is $4,000 ($10,000 – $6,000).

b. The $15,000 is economic income and gross income for tax purposes. c. The use of the automobile does not result in economic income because the taxpayer

owns the corporation and thus owns the automobile. For tax purposes, the taxpayer is deemed to have received an $800 dividend from the corporation.

d. The taxpayer has economic income of $800 from the production in her garden.

However, for tax purposes no income is realized. The realization requirement is not satisfied because the vegetables are consumed by her and her neighbors, rather than sold to others.

e. The increase in value of $10,000 is economic income but is not gross income for

tax purposes because the realization requirement has not been satisfied. f. The taxpayer realized $1,000 economic income and gross income from discharge

of the indebtedness. pp. 3-3 to 3-5 27. Amos should use the cash method of accounting so that the income from services billed

to the insurance company can be deferred until the income is collected. Under the cash method, the amounts billed to the insurance companies will be continuously deferred until the year following his final year of practice. That is, with the cash method of accounting as compared to the accrual method, Amos will enjoy a deferral of two months of billings to insurance companies. Amos’s marginal tax rate may be lower in the first year of practice than in subsequent years. Thus, accelerating income through the use of the accrual method would have some benefit. But the benefit of the lower rates probably would not equal the benefit of deferral. In addition, under the 2001 tax legislation, marginal tax rates are scheduled to decrease each year through the year 2006. pp. 3-7 to 3-9

28. Alternative a. is superior to alternative b. Alternative a. yields the greater after-tax value.

3-10 2004 Comprehensive Volume/Solutions Manual

Alternative a: Value in 5 years, $10,000 X 1.34 $13,400

Less tax .25($13,400 – $10,000) (850) After-tax value $12,550

Alternative b: Principal $10,000

Annual interest (after tax) [(1 – .38)($600)] $372 Reinvested for 5 years, at 3.72%, after-tax annuity factor X 5.39 2,005 After-tax value $12,005

Speech for Tax Class Assume a taxpayer has the following alternative investment opportunities: • Investment in land for $10,000 that will increase in value by 6% each year. • Investment in a taxable bond for $10,000 yielding 6% before tax, and the interest can

be reinvested at 6% before tax. The taxpayer is in the 38% tax bracket (combined Federal and State) for ordinary income and 25% for qualifying capital gains in all years and the investment will be liquidated at the end of five years. The purpose of my presentation is to demonstrate that taxes do affect investment decisions. If neither investment were subject to taxation, the two alternative investments would yield identical earnings (rounding produces a small difference).

Land Value in 5 years ($10,000 X 1.34) $13,400

Bond Principal $10,000 Annual interest $600 Reinvested for 5 years at 6%: annuity factor X 5.64 3,384 Value in 5 years $13,384

Both of the alternative investments are subject to taxation. However, the interest on the taxable bond is taxed annually, whereas the gain on the land is not taxed until the land is sold. In addition, the land is taxed at capital gain rates. Thus, the after-tax results are as follows:

Land Value in 5 years $13,400 Less tax: .25($13,400 – $10,000) (850) After-tax value $12,550

Bond

Principal $10,000 Annual interest (after tax) $372 Reinvested for 5 years at 6%: after-tax annuity factor X 5.39 2,005 Value in 5 years $12,005

Gross Income: Concepts and Inclusions 3-11

Therefore, the investment in the land will produce a greater after-tax value by an amount of $545 ($12,550 – $12,005). The future value of the land will exceed the future value of the bond because the interest on the bond is taxed each year while the appreciation in the land value is not taxed until the end of the five years and the appreciation on the land is taxed at a lower tax rate. Thus, with the bond, the investor has less of an investment that is growing at a compounded rate.

pp. 3-3 to 3-5, 3-35, and 3-36 29. a. Olga has $200 of interest income and a recognized gain of $300 ($10,500 – $200

– $10,000). b. Olga does not recognize income from using the stock as collateral for the debt.

Her assets (cash) and liabilities increased by the same amount, and she continued to own the stock. Thus, there is no realized gain.

c. Mere increases in the value of an asset are not included in gross income. Note the

attorney’s fee should be added to Olga’s cost of the property in calculating her basis for the vacant lot.

pp. 3-3 to 3-5

30. a. The $1,500 is a dividend from the corporation to Amos. The corporation was

entitled to the rebate. The rebate was a reduction in the cost of the corporation’s automobile. The assignment of the $1,500 to Amos was an economic benefit realized solely because he was the controlling shareholder and thus is a dividend to him.

b. The $50,000 payment received under the covenant is included in Amos’s gross

income because the payment is an increase in wealth realized. c. The neighbor’s actions that increased the value of Amos’s property by $1,500 do

not result in the realization of income by him. Amos’s wealth has increased, but the realization requirement is not satisfied, since he did not receive any additional property nor were any improvements made to his property. pp. 3-7 and 3-8

31. a. Gross income using cash method: Cash collections from customers $150,000 Under the cash method, income is recognized when cash or its equivalent is

actually or constructively received, regardless of when it was actually earned. Neither gross income nor taxable income is affected by the uncollectible accounts. Income was not recognized when the income was earned. The deposit is not Al’s money. Rather, Al is the agent holding the money on behalf of the client.

b. Gross income using accrual method:

Cash collections $150,000 Less: Beginning accounts receivable (25,000) Plus: Ending accounts receivable 45,000

$170,000

3-12 2004 Comprehensive Volume/Solutions Manual

c. Al should use the cash method so that he will not have to pay income taxes on uncollected accounts receivable.

pp. 3-7 to 3-9 32. Selma must use the accrual method of accounting for her farm implements business

because inventories are a material income-producing factor to the business.

Calculation of sales: Cash receipts (excluding $50,000 investment and $5,000 customer deposit) $445,000 Accounts receivable: end of the year 15,000

Total sales $460,000 Cost of goods sold:

Cash payments for merchandise $350,000 Accounts payable: end of the year 40,000 Cost of goods available for sale $390,000 Less: ending inventory (75,000) Cost of goods sold (315,000)

Gross profit $145,000

Note that the $5,000 customer deposit on inventory must be excluded from income reported in financial statements presented to the creditors and investors. Otherwise, the deposit cannot be deferred for tax purposes. pp. 3-7 to 3-9

33. Willis, Hoffman, Maloney, and Raabe, CPAs

5191 Natorp Boulevard Mason, OH 45040

October 1, 2003 Ms. Amanda Sims Managing Partner Aspen Associates 100 James Tower Denver, CO 80208 Dear Ms. Sims: I am responding to your suggestion that Aspen Associates should change to the accrual method of accounting for tax purposes as a means of reducing accounting fees. Under the accrual method of accounting, receivables must be recognized as income as the services are performed. This is to be contrasted with the cash method of accounting where no income is recognized until payment is received. Each year, under the accrual method, accelerated tax payments would occur so long as the billing and collection pattern remains the same. Therefore, the partners will pay tax on an additional $75,000 in the first year’s income, and those payments will not be recovered until the company ceases its operations. Assuming the partners are in the 36% (combined State and Federal) marginal tax bracket, the deferred taxes under the cash method are $27,000 (.36 X $75,000). If the partners earn a 1.85% ($500 ÷ $27,000) return, or greater, on the deferred taxes, the additional accounting fees will be recovered. Therefore, I recommend that you continue to use the cash method.

Gross Income: Concepts and Inclusions 3-13

Sincerely, Tara Kelly, CPA Tax Partner pp. 3-8 and 3-9

34. TO: Susan Apple FROM: Bill Swan SUBJECT: Dispute Over Recording of Income by Color Paint Shop, Inc. DATE: October 1, 2004 I am responding to the questions you raised regarding the timing of the reporting of

income by Color Paint Shop, Inc. with respect to the dispute concerning the painting of Samuel Customer’s car. The key issue is whether Color (1) should accrue the $1,000 of income in 2003 and take a $200 loss deduction in 2004 (the IRS view), (2) report the $800 in 2003, or (3) delay recording the $800 income until 2004 (Color’s preferred approach).

An accrual basis taxpayer is required to recognize income when (1) all the events have

occurred to establish the taxpayer’s right to receive the income, and (2) the amount of the income can be determined with reasonable accuracy. In Color’s case, it does not appear that all the events to fix the rights to the income had occurred in 2003. The insurance company had not approved the work by the end of the year. One could reason that Samuel’s approval of the work is the critical event that fixes Color’s right to receive the income, because the insurance company is merely the paying agent of the customer. However, even with this conclusion that the all-events test had been satisfied by the end of 2003, the amount of the income cannot be determined with reasonable accuracy because the insurance company may renegotiate the price. Thus, the transaction should be held open and no income should be reported until 2004. The amount of income Color should report in 2004 is $800. pp. 3-8 and 3-9

35. a. The taxpayer would report the income actually received in 2003. If the salary is

paid according to the agreement, the taxpayer will have received 11 payments of $10,000 each, or $110,000 in 2003. The fact that the employer was willing to negotiate a different payment schedule does not affect the timing of the taxpayer’s income.

b. The cash basis taxpayer must report the $8,000 of income in 2002 when it was

actually received. c. The fact that the employer violated the agreement and paid the taxpayer in 2003

may cause the taxpayer to have a grievance against the employer, but it does not alter the fact that he received the income in 2003. Therefore, the $10,000 is included in his gross income in 2003.

pp. 3-9 and 3-10 36. a. Morris must recognize $4,416 ($10,000 – $5,584) of interest income from the

retirement of the Series EE bonds. His basis was the original cost of $5,584 since Series EE bonds are not subject to the original issue discount rules.

3-14 2004 Comprehensive Volume/Solutions Manual

b. The two-year certificate is subject to the original issue discount rules. The following amount of interest income is recognized each year by Morris.

2001: $9,066 X 5% X 3/12 = $113 2002: $9,179 X 5% X 12/12 = 459 2003: $9,638 X 5% X 9/12 = 362 $934

Thus, Morris’s basis for the CD at redemption is $10,000 ($9,066 + $934). Thus, his basis of $10,000 equals the maturity value of $10,000.

The one-year CD he purchased in 2003 has $700 ($10,700 – $10,000) original issue discount, but amortization of that discount is not required because it matures one-year from the date of purchase.

pp. 3-11 and 3-12

37. a. The $1,200 advance payment can be deferred until 2003 because the property was not delivered until 2003 and the revenue was not recognized for financial accounting purposes until 2003.

b. Gross income of $140 ($20 per month X 7 months) must be reported in 2003.

The prepaid income qualifies for deferral because all of the income will be earned by the end of the tax year following the year or receipt. All of the $450 for the 23-month contract must be included in gross income in 2003 because some of the income will be earned after 2004.

c. The company must include $1,200 in gross receipts and can deduct the cost of the

appliance, $750, in arriving at gross income of $450. The fair market value of the note is not relevant for purposes of determining the accrual method taxpayer’s gross income.

pp. 3-8, 3-9, 3-13, and 3-14 38. a. Freda actually received only $180,000 in 2004. She did not constructively

receive the remaining $60,000 in 2004, since under the terms of the actual contract she did not have the right to receive that amount in 2004.

b. Freda may be bargaining for the deferred payments because she expects to be in a

lower marginal tax bracket in 2005. However, the lower tax rate must be sufficient to compensate for her loss of the use of the income for the period October through December 2004.

pp. 3-7 to 3-11

39. a. • The damage deposit is not taxable at the time it is collected, but the $400

prepaid rent is taxed in the year of receipt. • The $800 prepaid rent is taxed in the year of receipt. • The $800 damage deposit is not taxed in the year of receipt. b. The Bonhaus Apartments should use the third option. By doing so, it maximizes

deferrals without affecting the cash flows.

Gross Income: Concepts and Inclusions 3-15

pp. 3-13 and 3-14

40. a. The corporation is the owner of the property and therefore the $12,000 is rent income to the corporation. Gus received the $12,000 in his capacity as a corporate shareholder and must recognize $12,000 of dividend income, assuming the corporation has earnings and profits of at least that amount.

b. The $12,000 of rent income will flow through the S corporation to Gus as the sole

shareholder of the S corporation. pp. 3-16 and 3-17 41. a. The cash basis corporation must recognize the income of $3,000 in 2003 when its

agent, Tracy, received the check, which is a cash equivalent. Tracy will not recognize any bonus until it is actually or constructively received. The fact that the employer received the fees in 2004 does not affect the time Tracy recognizes the bonus.

b. The corporation must recognize the income in 2003, when the agent, Tracy,

performed the services. Tracy will recognize the 10% bonus in 2004, because neither actual nor constructive receipt of the bonus occurs in 2003.

c. The fact that the customer admits the check will not be honored if presented at the

end of the year means the check is not a “cash equivalent.” Furthermore, the restriction on when the check can be presented for payment is “substantial.” Thus, the income is not realized in 2003.

pp. 3-7 to 3-11 and 3-16 42. Each partner’s gross income from the partnership for the year is $100,000 [($390,000 –

$90,000)/3 = $100,000]. The partner’s gross income is his or her share of the profits under the profit and loss agreement, and generally is not affected by the partner’s withdrawals for the year. p. 3-16

43. a. Diego’s Carmen’s Income Income

The salary of both spouses (allocated one-half to each) $56,000 $56,000 Carmen’s dividends (allocated one-half to each) 3,000 3,000 Total income $59,000 $59,000

Example 29 b. The amount withheld is community property and, therefore, each is entitled to

one-half of the total amount withheld. pp. 3-17 to 3-19 c. Diego’s income = $48,000 salary. Carmen’s income = $64,000 salary + $6,000

dividends, or $70,000. p. 3-18 and Example 27

3-16 2004 Comprehensive Volume/Solutions Manual

44. a. b. California Texas Doug Liz Doug Liz

Salary $48,000 $48,000 $48,000 $48,000 Rent 6,000 3,000 3,000 Dividends 1,900 950 950 Interest 900 900 900 900

$50,800 $54,900 $52,850 $52,850

Under Texas law, the rents and dividends belong to the community even though this income is derived from separate property. Under California law, the income is community or separate depending on the state law classification of the underlying assets. In this case, the interest is community income because the savings account was funded with community property. pp. 3-17 to 3-19 and Example 27

45. a. The use of the house is not alimony because it is not a cash payment. Thus, Nell does not recognize income and Kirby is not entitled to a deduction.

b. The $1,000 per month payments are in cash and satisfy all of the other

requirements to be labeled as alimony. Thus, the payments are deductible to Kirby and are includible in Nell’s gross income. The securities transfer is incident to a divorce and therefore produces no recognized gain to Nell. Kirby’s basis is a carryover basis of $100,000.

c. The $600 per month payments are nondeductible child support, since the payments

cease upon the happening of a contingency related to the child’s age or death. pp. 3-19 to 3-22 46. a. The portion of the payments which are contingent upon their son’s living are

child support. The remaining portion of the payments qualifies as alimony. Therefore, Al has $85,000 ($90,000 – $5,000) alimony from the year 1 payment.

b. Alimony paid for the first three years is $85,000 for year 1, $55,000 for year 2,

and $15,000 for year 3. Alimony recapture is computed as follows:

Year 2 alimony recapture: Year 2 alimony $55,000 –Year 3 alimony (15,000) =Decrease $40,000 –Allowable decrease (15,000) =Year 1 alimony recapture $25,000

Year 1 alimony recapture: Year 1 alimony $85,000 –Average of year 2 and 3 alimony* (22,500) =Decrease $62,500 –Allowable decrease (15,000) =Year 1 alimony recapture $47,500

Total alimony recapture ($25,000 + $47,500) $72,500

*[($55,000 – $25,000) + $15,000]/2 = $22,500

Gross Income: Concepts and Inclusions 3-17

pp. 3-20 to 3-24

47. The receipt of the common stock is not taxable to Sandra because it is a non-cash transfer

of property under the terms of a divorce. The $300 per month actual child support payments are not included in Sandra’s gross income. The $1,000 monthly payment includes $250 of implicit child support. That is, because the payments would be reduced as a result of a contingency related to the child (i.e., attaining age 21), the amount of the contingent reduction is child support. Therefore, Sandra must include only $4,500 ($750 X 6) from alimony in gross income in the current year. pp. 3-20 to 3-22

48. Under the guarantee arrangement, the family would receive before tax interest of $9,000

($150,000 X 6%) on Hal’s certificates of deposit and would pay $10,500 ($150,000 X 7%) interest on Roy’s loan. Furthermore, the interest received will be taxed at 35% (Hal’s marginal tax rate) while the interest paid will be deductible at only 15% (Roy’s marginal tax rate). The transactions will produce a negative cash flow of $3,075 [($9,000) (1 – .35) – ($10,500) (1 – .15) = –$3,075] for the family.

The 6% loan from Hal to Roy would reduce the family’s negative cash flow by $1,275

($3,075 – $1,800) compared to the guarantee. This results because Hal will receive $9,000 interest and Roy will pay the same amount. On an after-tax basis, the $9,000 received by Hal is taxed at 35%, the same as with the certificates of deposit, and the interest is deductible by Roy at a 15% tax rate.

[($9,000) (1 – .35) – ($9,000) (1 – .15) = – $1,800] A zero interest rate loan would have been the best alternative if the total loans between

Roy and Hal had been less than $100,000. The zero interest rate loan would be eligible for the $100,000 exception for gift loans. Therefore, interest would not be imputed, since Roy has no investment income. Roy would not receive any interest income, and Hal would not pay any interest. Since this option is not available, the better option appears to be the 6% loan from Hal to Roy.

[($0) (1 – .35) – ($0) (1 – .15) = $0] pp. 3-22 to 3-27 49. Income

Loan from employer Compensation ($62,000)(.07)(6/12) = $2,170*

Loans to others To controlled corporation ($31,000)(.07)(6/12) = 1,085** To Tab (exempt under $100,000 exception) -0-

Certificates of deposit One year certificate (not subject to OID rules) -0- Two year certificate ($6,000)(.0625)(6/12) 188

*Ridge also has $2,170 of interest expense which may be deductible as investment

interest (to the extent the loan proceeds were used for investment purposes).

**Treated as an additional investment by Ridge and added to his cost of the stock. pp. 3-11, 3-12, and 3-22 to 3-27

3-18 2004 Comprehensive Volume/Solutions Manual

50. a. This loan is a gift loan between individuals that is eligible for the $100,000 exception. Although the sister has $900 of investment income, interest is not imputed under this exception if the borrower’s investment income is not greater than $1,000.

b. This loan is an employer-employee loan for not greater than $10,000. Sam did

not use the funds to buy investments. Thus, no interest is imputed. c. Interest is imputed on this loan. The $100,000 exception is not available on

corporation-shareholder loans. The imputed interest would be calculated as follows:

$15,000 X (5.5% – 4%) X 1/2 = $112 $15,112 X (5.5% – 4%) X 1/2= 113 $225 pp. 3-24 to 3-28 51. a. The employer-employee loan would be eligible for the $10,000 exemption

through June 30, 2004. However, in July 2004, the total outstanding loans exceed $10,000. The $100,000 exemption does not apply to these loans. Therefore, interest is imputed on the $11,000 amount of the loans for the period July through December 2004. Vito, Inc. has interest income and Vito has compensation income of $550 [.10($11,000 X 6/12)]. Vito also has interest expense of $550 and Vito, Inc. has compensation expense of the same amount.

b. A corporation-shareholder loan is not eligible for the $100,000 exemption and

usually does not qualify for the $10,000 exemption (i.e., cannot satisfy the requirement that tax avoidance not be a principal purpose of the loan). Therefore, for 2003 and 2004, the corporation has interest income and dividends paid (not deductible) as follows:

2003 ($8,000 X 10% X 6/12) $400 2004 ($8,400 X 10% X 6/12) $420

($8,400 + $420 + $3,000)(.10)(6/12) 591 $1,011

Vito has dividend income and interest expense of equal amounts.

pp. 3-22 to 3-27 52. a. Cost (her investment) $120,000

Employee’s investment $120,000Number of anticipated payments = 260 = $461.54 exclusion

[Table 3-2] Collections in 2003 (6 payments X $2,000) $12,000 Exclusion for capital recovery ($461.54 X 6 payments) [rounded] (2,769)

Include in gross income $ 9,231

Gross Income: Concepts and Inclusions 3-19

The simplified method is used to calculate the annuity exclusion percentage since this is a qualified retirement plan distribution.

b. Thelma will have recovered her investment as a return of capital prior to the twenty-ninth year. Thus, all annuity payments received in the twenty-ninth year are includible in her gross income.

$2,000 X 12 payments = $24,000

c. Investment in the contract $120,000 Total amount collected 180 X $2,000 = $360,000 Less: capital recovered $360,000 X .23077 (83,077) Unrecovered cost (loss in the final year return) ($ 36,923)

Income from collections in final year: $12,000(1 – .23077) $ 9,231

pp. 3-27 to 3-30

53. a. Joe is required to include $110,000 ($60,000 + $50,000) in gross income associated with the award he received. The award does not satisfy the right type of achievement requirement to qualify for exclusion from gross income. In addition, the provision which requires the recipient to contribute the award to a qualified governmental unit or nonprofit organization is not satisfied.

b. Wanda is required to include the $75,000 of prizes received in her gross income.

She is required to render substantial future services. In addition, the provision which requires the recipient to contribute the award to a qualified governmental unit or nonprofit organization is not satisfied.

c. George can exclude the $900,000 prize received from his gross income. All of

the requirements for exclusion are satisfied. pp. 3-30 and 3-32 54. a. Alice’s gross income from excess coverage is computed as follows: Uniform premiums for $1,000 of protection $ .10

Coverage for a month X 12 months X 12 ($.10 X 12) $ 1.20

$110,000 – $50,000 X 60

$1,000

Includible amount $72.00

Kay is a partner (i.e., not an employee) and is not eligible for the exclusion for group term life insurance. Therefore, she must include the cost of the protection in income, $1,500. pp. 3-32 and 3-33

b. Same as a. for Kay. This amount is the greater of the cost of the protection

($1,500) or the table amount of $1,032 ($200 X .43 X 12 months). pp. 3-32 and 3-33

3-20 2004 Comprehensive Volume/Solutions Manual

55. Salary $ 90,000 Unemployment compensation 8,300* Interest income 90 Dividend income 550 Lottery winnings 1,500 Gross income $100,440 * Unemployment compensation is includible in gross income. The $5 cost of the lottery ticket is deductible as a miscellaneous itemized deduction, not subject to the 2% reduction. Neither the $12,000 loan nor the $2,000 savings account withdrawal are included in gross income. p. 3-33

56. a. Taxable Social Security benefits =

.5[$29,000 + .5($9,000) – $32,000] = .5($1,500) $ 750 Pension benefits, etc. 29,000 AGI $29,750

b. Other income ($29,000 – $8,000) $21,000

Taxable Social Security benefits = .5[$21,000 + $6,000 + .5($9,000) – $32,000] -0- $21,000

AGI in a. above (29,750) Decrease in AGI ($ 8,750)

Note: The taxpayers’ economic income decreased by $2,000 ($8,000 – $6,000), but taxable income decreased by $8,750. However, with a 15% marginal tax rate, their after-tax economic income will decrease by only $687. Decrease in interest income $2,000 Decrease in tax liability (15% X $8,750) (1,313) Decrease in economic income $ 687

c. Lesser of: (1) .85[$59,000 + .5($9,000) – $44,000] = .85($19,500) $16,575

Plus smaller of: Amount calculated by the first formula, which is the lesser of .5($9,000) = $4,500 .5[$59,000 + .5($9,000) – $32,000] = $15,750 or $6,000 4,500

$21,075 or

(2) .85($9,000) $ 7,650 Therefore, Linda and Don would be required to include 85% of the Social

Security benefits ($7,650) in their gross income. Includible Social Security benefits $ 7,650 Other income ($29,000 + $30,000) 59,000

AGI $66,650 AGI in a. above (29,750) Increase in AGI $36,900

Gross Income: Concepts and Inclusions 3-21

Note: The increase in AGI exceeds the increase in earnings because more of the Social Security benefits became taxable.

pp. 3-33 and 3-34

57. a. Not Retired Retired Change

Salary $80,000 Retirement pay $60,000 Interest and dividends 12,000 12,000 Tentative AGI $72,000 $92,000 Social Security ($15,000 X 85%) 12,750

AGI $84,750 $92,000 Less deductions (16,000) (16,000) Taxable income $68,750 $76,000 ($7,250)

b. Their change in after-tax cash flow will be a decrease of $5,075 [$7,250 – ($7,50

X 30%)]. pp. 3-33 and 3-34

58. Donna has substantial tax problems: a. Donna’s share of the partnership income of $70,000 will be taxable to Donna

even though the income was not distributed. p. 3-16 b. A portion of the Social Security benefits will be taxable because Donna has other

income. If Donna and her husband file separate returns, she must include $7,140 ($8,400 X 85%) of the Social Security benefits in her gross income (i.e., the base amount is $0 in this case). Even with a joint return, Donna and her husband would include $7,140 of the Social Security benefits in their gross income (i.e., in this case, the base amount would be $44,000). pp. 3-33 and 3-34

c. Donna must report the $1,200 of interest income even though the creditor

received the money. She owned the property which earned the income. Also, she benefited from the income in that the money was used to satisfy her liability. pp. 3-14 and 3-15

d. Donna will be required to include in gross income one-half of her husband’s

income because they are residents of a community property state. pp. 3-17 to 3-19

CUMULATIVE PROBLEMS 59. Part 1—Tax Computation

Gross income Salary and commissions ($90,000 + $35,000) (Note 1) $125,000 Interest income on certificate of deposit (Note 2) 536 Interest income on Second Bank savings account (Note 3) 1,500 Dividends on CSX stock (Note 4) 2,800 Income from partnership (Note 5) 12,000

3-22 2004 Comprehensive Volume/Solutions Manual

Deductions for adjusted gross income -0- Adjusted gross income $141,836 Itemized deductions State income tax $5,000 Personal property tax 600 Real estate tax 3,100 Home mortgage interest 5,900 Cash contributions 675 (15,275) Personal and dependency exemptions (Note 6) (12,200) Taxable income $114,361 Tax on $114,361 [$6,517 + .27($114,361 – $47,450)] $ 24,583 Less: Tax withheld by employers (18,000) Estimated tax payments (7,000) Net tax payable (or refund due) for 2003 ($ 417) Notes

(1) Assuming that Dan and Freida are cash basis taxpayers, the $2,000 commission

will not be included in gross income until it is received in 2004. (2) The original interest discount rules apply. The OID for 2003 is $536. Maturity value $15,000 2001 OID ($13,605 X 5%) X 3/12 $170 2002 OID ($13,775 X 5%) 689 Adjusted basis at beginning of 2003 ($13,775 + $689) (14,464) 2003 OID $ 536 (3) The $4,500 of interest on the City of Corbin bonds is excluded from gross

income.

(4) The dividends of $2,800 on the CSX stock are included in Dan and Freida’s gross income. Then they are treated as having made a gift of $2,800 to Ben.

(5) Freida’s share of the partnership profits is $12,000 ($100,000 X 12%). Therefore,

she must include this amount in her gross income. (6) Gina qualifies as a dependent. Since she is their child and is a full-time student

under age 24, she does not have to satisfy the gross income test (i.e., it is waived). In any event, this is not a problem since Gina has $0 gross income. Gina does not file a joint return with her husband. Therefore, since all of the requirement are satisfied, Dan and Freida can claim a dependency deduction for Gina. Ben, Freida’s brother, fails to qualify as a dependent because of the gross income test. (Although he is a full-time student, he is not a child of either taxpayer.) Sam, their son, does qualify as a dependent. It appears he has too much gross income ($6,200). However, the gross income test is waived in this case because he is a full-time student during five calendar months. Therefore, Dan and Freida’s personal exemption and dependency deductions are $12,200 ($3,050 X 4).

Gross Income: Concepts and Inclusions 3-23

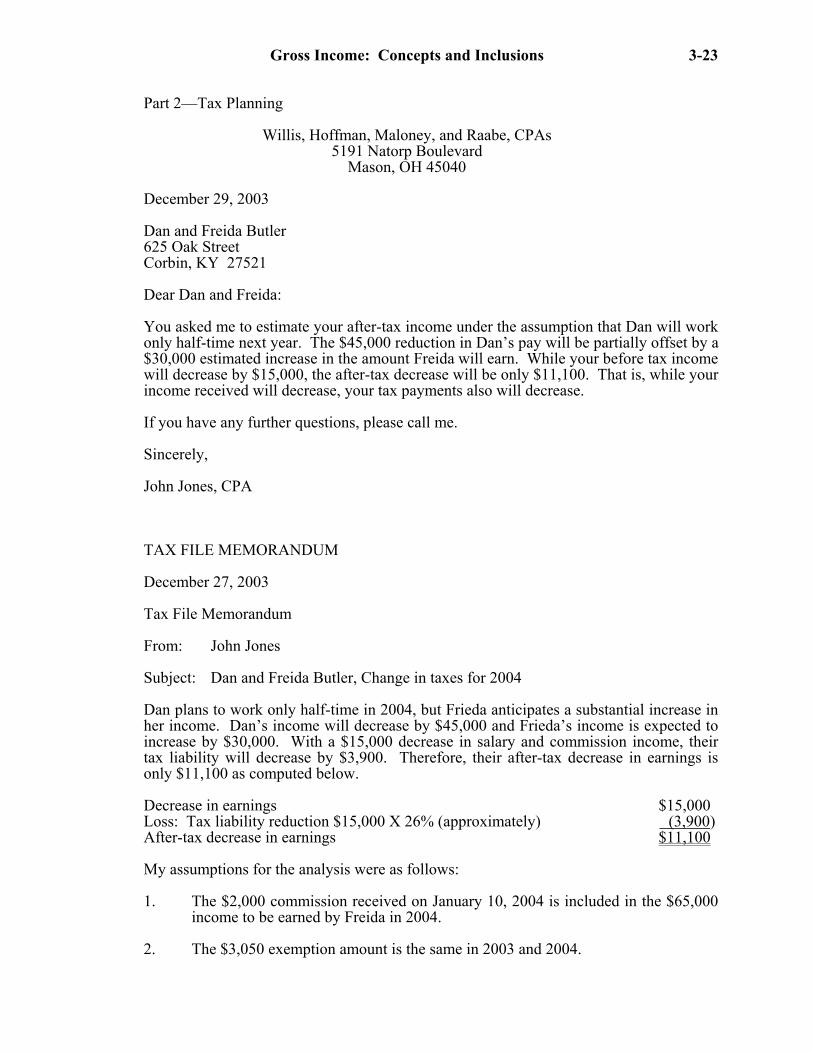

Part 2—Tax Planning

Willis, Hoffman, Maloney, and Raabe, CPAs 5191 Natorp Boulevard

Mason, OH 45040

December 29, 2003 Dan and Freida Butler 625 Oak Street Corbin, KY 27521 Dear Dan and Freida: You asked me to estimate your after-tax income under the assumption that Dan will work only half-time next year. The $45,000 reduction in Dan’s pay will be partially offset by a $30,000 estimated increase in the amount Freida will earn. While your before tax income will decrease by $15,000, the after-tax decrease will be only $11,100. That is, while your income received will decrease, your tax payments also will decrease. If you have any further questions, please call me. Sincerely, John Jones, CPA

TAX FILE MEMORANDUM December 27, 2003 Tax File Memorandum From: John Jones Subject: Dan and Freida Butler, Change in taxes for 2004 Dan plans to work only half-time in 2004, but Frieda anticipates a substantial increase in her income. Dan’s income will decrease by $45,000 and Frieda’s income is expected to increase by $30,000. With a $15,000 decrease in salary and commission income, their tax liability will decrease by $3,900. Therefore, their after-tax decrease in earnings is only $11,100 as computed below. Decrease in earnings $15,000 Loss: Tax liability reduction $15,000 X 26% (approximately) (3,900) After-tax decrease in earnings $11,100 My assumptions for the analysis were as follows: 1. The $2,000 commission received on January 10, 2004 is included in the $65,000

income to be earned by Freida in 2004. 2. The $3,050 exemption amount is the same in 2003 and 2004.

3-24 2004 Comprehensive Volume/Solutions Manual

3. The 27% 2003 tax rate decreases to 26% in 2004. 4. Interest income, dividend income, partnership income, and itemized deductions

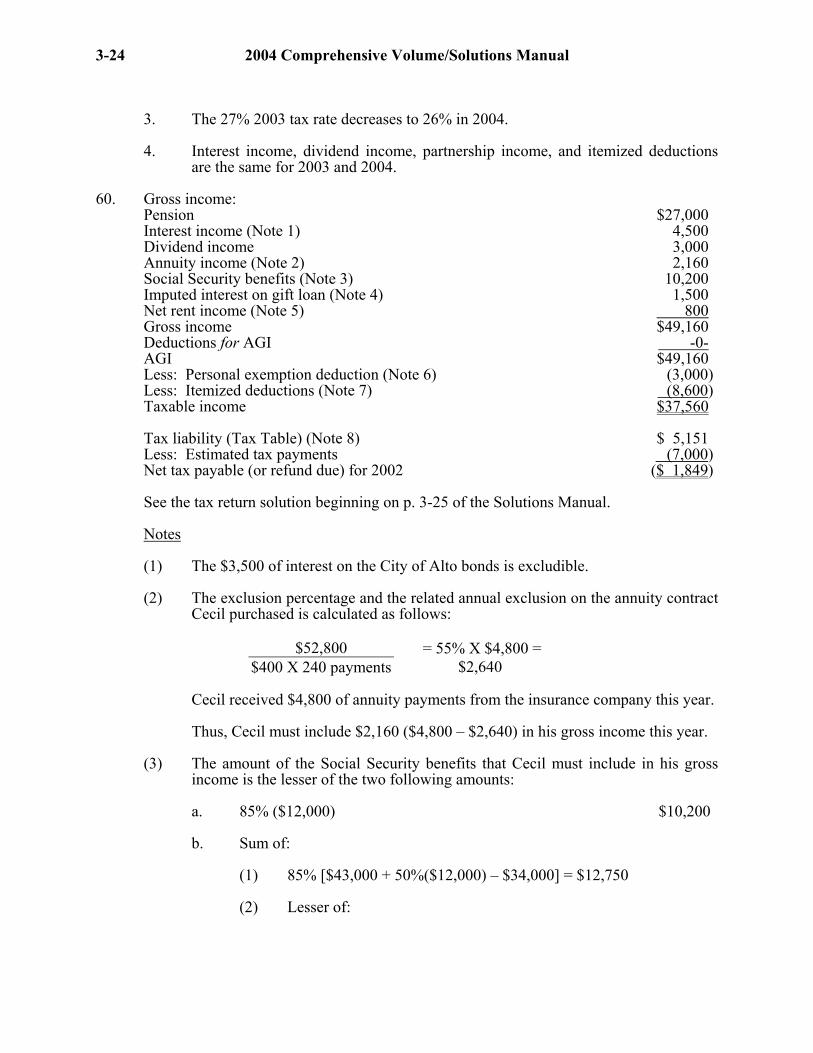

are the same for 2003 and 2004. 60. Gross income:

Pension $27,000 Interest income (Note 1) 4,500 Dividend income 3,000 Annuity income (Note 2) 2,160 Social Security benefits (Note 3) 10,200 Imputed interest on gift loan (Note 4) 1,500 Net rent income (Note 5) 800 Gross income $49,160 Deductions for AGI -0- AGI $49,160 Less: Personal exemption deduction (Note 6) (3,000) Less: Itemized deductions (Note 7) (8,600) Taxable income $37,560 Tax liability (Tax Table) (Note 8) $ 5,151 Less: Estimated tax payments (7,000) Net tax payable (or refund due) for 2002 ($ 1,849)

See the tax return solution beginning on p. 3-25 of the Solutions Manual. Notes

(1) The $3,500 of interest on the City of Alto bonds is excludible. (2) The exclusion percentage and the related annual exclusion on the annuity contract

Cecil purchased is calculated as follows:

$52,800 $400 X 240 payments

= 55% X $4,800 = $2,640

Cecil received $4,800 of annuity payments from the insurance company this year. Thus, Cecil must include $2,160 ($4,800 – $2,640) in his gross income this year. (3) The amount of the Social Security benefits that Cecil must include in his gross

income is the lesser of the two following amounts:

a. 85% ($12,000) $10,200 b. Sum of:

(1) 85% [$43,000 + 50%($12,000) – $34,000] = $12,750

(2) Lesser of:

Gross Income: Concepts and Inclusions 3-25

(a) Amount calculated using 50% formula (lesser of) • 50%($12,000) = $6,000

• 50%[$43,000 + 50% ($12,000) – $25,000] = $12,000

(b) $4,500

Thus, $12,750 + $4,500 = $17,250. Since the amount calculated under a. of $10,200 is less than the amount calculated

under b. of $17,250, the $10,200 is included in Cecil’s gross income.

(4) Since Cecil made a below-market gift loan to Sarah, he needs to determine if any imputed interest should be included in his gross income. The loan qualifies under the $100,000 exception. Since Sarah’s net investment income is only $1,500, Cecil has to include only $1,500 in his gross income rather than $2,800 ($40,000 X 7%).

(5) The net rental income from the townhouse is as follows:

Rent income $6,600 Less: Expenses Utilities $1,500 Maintenance 1,000 Real estate taxes 800 Insurance 500 Depreciation 2,000 (5,800) Net rent income $ 800

(6) Since Sarah is self-supporting, Cecil does not qualify for a dependency deduction

for her. (7) Cecil’s itemized deductions are as follows:

Personal property taxes $2,900 State income taxes 1,300 Charitable contributions 4,400

$8,600 Cecil’s standard deduction would be $8,050 ($6,900 basic standard deduction +

$1,150 additional standard deduction). Thus, Cecil will itemize deductions. (8) Cecil uses the Tax Table for a Head of Household. He maintains a home for his

unmarried daughter Sarah. Since she is unmarried, Sarah does not have to be his dependent.

3-26 2004 Comprehensive Volume/Solutions Manual

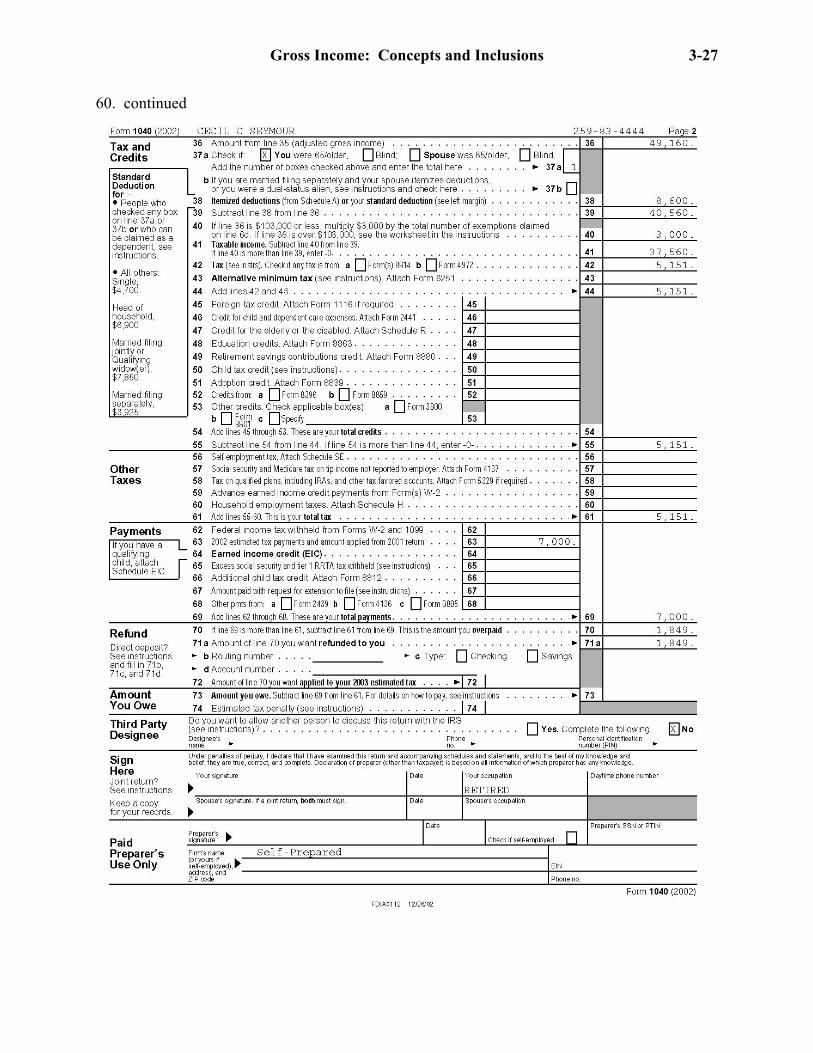

60.

Gross Income: Concepts and Inclusions 3-27

60. continued

3-28 2004 Comprehensive Volume/Solutions Manual

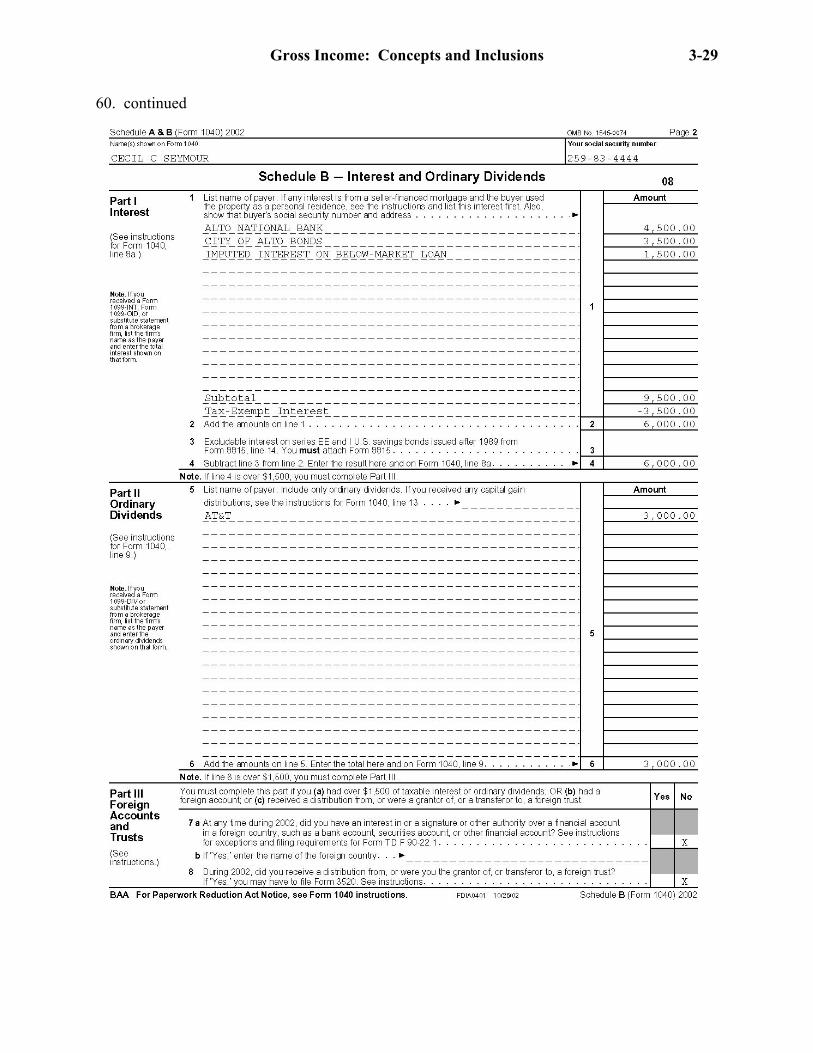

60. continued

Gross Income: Concepts and Inclusions 3-29

60. continued

3-30 2004 Comprehensive Volume/Solutions Manual

60. continued

Gross Income: Concepts and Inclusions 3-31

NOTES