chapter 20 - california state university, bakersfieldlbacon/chap16.doc · web viewchapter 16...

TRANSCRIPT

CHAPTER 16ACCOUNTING FOR STATES AND LOCAL GOVERNMENTS

(PART ONE)

ANSWERS TO QUESTIONS

1. User needs are often complex and contradictory. Specific procedures in the governmental reporting process are an outgrowth of those needs. GASB Concepts Statement No.1, “Objectives of Financial Reporting,” has identified three primary user groups: citizenry, legislative and oversight bodies, and investors and creditors. The needs of these users are broad and no one set of financial statements and principles can satisfy all expectations. The satisfaction of diverse user needs is a constant focus of governmental accounting. This has lead to the dual-perspective model of GASB No. 34 requiring two distinctive types of financial statements.

2. Accountability and control have been a constant goal of governmental accounting. Governmental accounting provides the citizenry of a democracy a method for evaluating the governmental actions of raising and allocating resources. Elected and appointed officials have authority over the public’s money. They should be held accountable for generating and using cash and meeting current claims. Therefore these officials should be evaluated upon their honesty, wisdom, and stewardship.

3. GASB Statement No.34 has refined the reporting of governmental activities by providing information about the government as a whole. Focusing on accountability does not meet all user needs. Reporting under GASB No. 34 still focuses on current financial resources, but provides an additional focus on all assets and all liabilities that must be paid, thus meeting broader user needs.

4. Two financial statements make up the government-wide financial statements: The Statement of Net Assets and The Statement of Activities. There are a number of fund-based financial statements. The two fundamental financial statements covered in Chapter 16 include: a Balance Sheet and a Statement of Revenues, Expenditures, and Changes in Fund Balances.

5. In fund-based accounting, governmental funds use the current resources measurement focus and the modified accrual basis for the timing of revenue and expense recognition. The current financial resources focus includes only current assets and current liabilities to be paid out of these current assets. The modified accrual basis recognizes revenues when they become available and measurable and expenditures when they cause a reduction in current financial resources.

Proprietary and Fiduciary funds generally use the economic resources measurement focus and the accrual basis for the timing of revenue and expense recognition. The economic resources measurement focus includes all government activities and capital assets and long-term liabilities in the Statement of Activities. The current financial resources focus includes only items expected to be converted to cash in the current period, or to pay current liabilities soon after the current period.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-1

6. Government-wide financial statements use the economic resources measurement focus and accrual accounting for the timing of revenue and expense recognition similar to for-profit organizations. This economic resources measurement focus includes all government activities and capital assets and long-term liabilities in the Statement of Activities.

7. Current financial resources are primarily cash, investments and receivables. These items are expected to be used to meet the current period government needs. This also can include supply inventories and prepaid expenses.

8. Liabilities are recognized under the current financial resources when a claim against current financial resources is created. Governmental funds account for only those liabilities paid from fund assets.

9. Governmental Funds: Account for activities with a service orientationa. General Fundb. Special Revenue Fundc. Capital Projects Fundd. Debt Service Funde. Permanent Fund

Proprietary Funds: Account for functions that are financed (at least in part) by user charges.a. Enterprise Fundb. Internal Service Fund

Fiduciary Funds: Account for moneys held by the government in a trustee capacity.a. Investment Trust Fundb. Private-Purpose Trust Fundc. Pension Trust Fundd. Agency Fund

10. The following fund types fall within the governmental funds classification:a. The General Fund is used to account for ongoing activities such as public safety and

sanitation. More specifically, the General Fund records any functions that do not fall under one of the other fund types.

b. Special Revenue Funds account for financial resources that have been restricted as to expenditure for a specified operating purpose.

c. Capital Projects Funds account for moneys (and their eventual expenditure) to be used in acquiring or constructing government facilities or other fixed assets.

d. Debt Service Funds account for the accumulation of resources that will be used eventually to pay the principal and interest of long-term debts incurred by the service activities.

e. The Permanent Fund accounts for assets contributed to the government by an external donor with the stipulation that the principal cannot be spent but any income can be used within the government, often for a designated purpose.

11. The following fund types fall within the proprietary funds classification:

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-2 Solutions Manual

a. An Enterprise Fund accounts for any governmental activity that is financed in whole or in part by outside user charges, such as a subway system.

b. An Internal Service Fund is used to record any activity that provides service to other departments or agencies within the government on a cost-reimbursement basis. A motor pool or a centralized computer operation can be accounted for as Internal Service Funds because they only exist to serve the other functions of government.

12. Fiduciary Funds: Account for moneys held by the government in a trustee capacity.a. Investment Trust Fund. Accounts for the outside portion of investment pools where the

reporting government has accepted funds from other governments resulting in a larger investment and hopefully a higher return.

b. Private-Purpose Trust Fund. Accounts for money held in a trustee capacity, for example, money confiscated from illegal operations.

c. Pension Trust Fund. Accounts for the employee retirement system.d. Agency Fund. Accounts for resources held by the government as an agent for

individuals, private organizations, or other government units.

13. In government-wide financial statements, financial figures are shown as either governmental activities or business-type activities. All governmental funds and most internal service funds appear in the governmental acitivites. All of the enterprise funds and any remaining internal service funds are lumped into the business-type activites. Fiduciary funds are not shown in the government-wide financial statements.

14. In fund-based financial statements, for the governmental funds, a separate column is shown for (a) the General Fund, (b) any other fund that qualifies as major, and (c) all other funds as a whole in a single column.

15. The physical recording of a budget is viewed as a method of expressing public policy and financial intent, providing a financial plan for the period. The budget establishes spending limitations, which enhances financial planning and control. The adoption of the budget for each activity anticipates the inflow of financing resources and approved expenditure levels. Subsequently, comparisons can be draw between actual and budgeted figures at any time during the fiscal period thus evaluating performance.

16. Comparisons between the original budget, the final budget, and actual figures must be reported for each government in the required supplemental information presented after the notes to the financial information. Alternatively, the information can be presented as a separate statement within the government’s fund-based financial statements.

17. An encumbrance is the recording of a purchase commitment (a contract or order). The encumbrance entry is recorded at the time the commitment is made prior to incurring a liability. This supports the spending control emphasis of the fund-based financial statements. Reviewing the Expenditures account and the Encumbrances balance provides the total amount of financial resources spent and committed. Thus the chances of an over-commitment of resources is decreased. The encumbrance is removed when there is a legal liability. No liability has been incurred so encumbrances are not included in government-wide financial statements.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-3

18. Encumbrances (purchase commitments) that remain outstanding at the end of a fiscal period are reported within the Equity section as a reserved fund balance. No liability is reported; instead, the need to hold resources to satisfy the eventual cost of the commitment is disclosed.

19. Expenditures include outflows or reductions of net financial resources from the acquisition of goods or services and should be recognized in the fiscal period in which the fund liability is incurred and is measurable. Accrual and modified accrual based accounting recognize expenditures when a claim against the current financial resources is incurred. Fund-based accounting records expenditures instead of expenses and capital assets. Therefore, expenditures are incurred for not only goods and services but also buildings and machines.

20. Expenditures include outflows or reductions of net financial resources from the acquisition of goods or services and should be recognized in the fiscal period in which the fund liability is incurred and is measurable. Accrual and modified accrual based accounting recognize expenditures when a claim against the current financial resources is incurred.

21. The fund-based financial statements focus on expenditures rather than expenses. Most expenditures and transfers should be recorded when the liability is incurred. Therefore, the entire amount of capital assets is treated as expenditure. Government-wide financial statements would treat capital assets similar to for-profit organizations. Buildings, machines, and other capital assets are capitalized and expensed.

22. Traditionally the purchase method has been used. The purchase of supplies and other prepaid expenses are recorded as expenditures. Another method is the consumption method, which is similar to for-profit organization. Supplies and prepayments are recorded as assets when acquired. As they are consumed they are recorded as Expenditures matching them with the appropriate fiscal period.

23. The four classifications of revenues that a state or local government can recognize are: a. Derived tax revenues. A tax assessment is imposed because an underlying exchange

takes place. For example revenues are recognized on a sales tax where a sale occurs and a tax is imposed.

b. Imposed nonexchange revenues. An assessment is imposed but no underlying transaction taxes place. Examples include property taxes and fines or penalties that are levied. Revenues are recognized in the period when resources are required to be used or the first period that use is permitted.

c. Government-mandated nonexchange transactions. Monies are provided from one government to another to help pay for required programs. Examples include grants from the federal government to a city only used for a mandated purpose. Revenues are recognized when all eligibility requirements have been met.

d. Voluntary nonexchange transactions. Monies conveyed willingly to a state or local government by an individual, another government, or an organization usually for a specific purpose but without mandated requirements. Revenues are recognized when all eligibility requirements have been met. An example would be money donated to the city for parks.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-4 Solutions Manual

24. No revenues are recognized in either method because the proceeds of bonds must be paid back. In fund-based financial statements Cash would be debited and Other Financing Resources would be credited because it is not considered revenue. If the bonds were issued for a capital project the entry would be recorded in the Capital Project Fund. Payment of interest and debt is recorded when they become due becoming a claim on current financial resources. An Expenditure account is recognized for the debt and related interest usually in the Debt Service Fund.

In government-wide financial statements cash and debt are both increased and payment of debt would be similar to for-profit financial statements.

25. A special assessment is an improvement to property made by the government, which is paid for in part or in whole by the owners of the property being benefited. Adding curbing and sidewalks to a local street would be an example of a special assessment if the residents of that street were required to pay apportion of the cost. Typically the government places a lien on the property to insure payment while issuing the debt.

The accounting for special assessment projects depends on the liability of the government. If the government is in no way liable for the work done and the debt incurred, an Agency Fund is used to account for the monetary inflows and outflows. The government is simply serving as a conduit to get the project completed and any debt paid.

If the government is responsible (even secondarily responsible) for the cost of the project, a more elaborate method of accounting is necessary. In the government-wide financial statements the debt and the infrastructure asset are recorded as in financial accounting. The taxes are assessed and collected and used to pay the debt.

The infrastructure asset and long-term debt are not recorded in the fund-based financial statements. The expenditures for the work are recorded in a Capital Projects Fund while cash collection is recorded in the Debt-Service Fund.

26. In fund based financial statements interfund transactions are recorded in both funds simultaneously at the time of authorization. For example, monetary transfers from the General Fund to another fund such as Debt Service Fund would be recorded in both funds.

There is no entry in the government-wide financial statements because they occur solely with governmental activities or business activities.

27. Intra-activity transactions occur within governmental-type funds, and within enterprise funds, that do not affect the overall governmental or business activity balance. This includes transactions between governmental funds internal service funds. Therefore they are not reported on government-wide financial statements.

Inter-activity transactions occur between governmental funds and enterprise funds, that affect the overall governmental and business activity balance. Therefore they are reported on government-wide financial statements.

28. An internal exchange transaction is a transfer within the government that is recorded as if the transaction had actually occurred with an outside party. Such transactions between

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-5

the government entity and its own internal service or enterprise fund are reported as revenues and expenditures or expenses. An example would be a payment from a city to the motor pool. This would be included in the fund-based financial statements as if were a transaction with an outside party. On government-wide financial statements transactions with a government entity and its own internal service funds would be considered an intra-activity transactions because both fund typed are classified as government activities and therefore there would be no impact on overall figures. Payment to business-type activities enterprise funds are considered intra-activity transactions and would appear on government-wide statements.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-6 Solutions Manual

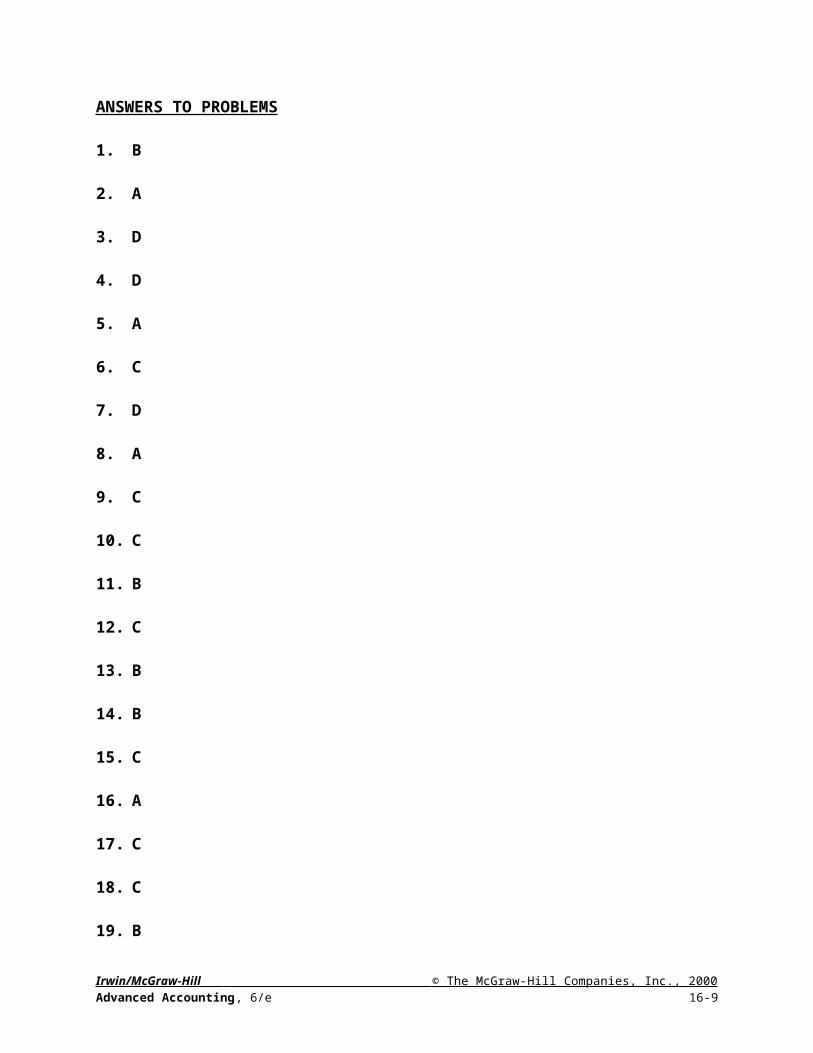

ANSWERS TO PROBLEMS

1. B

2. A

3. D

4. D

5. A

6. C

7. D

8. A

9. C

10. C

11. B

12. C

13. B

14. B

15. C

16. A

17. C

18. C

19. B

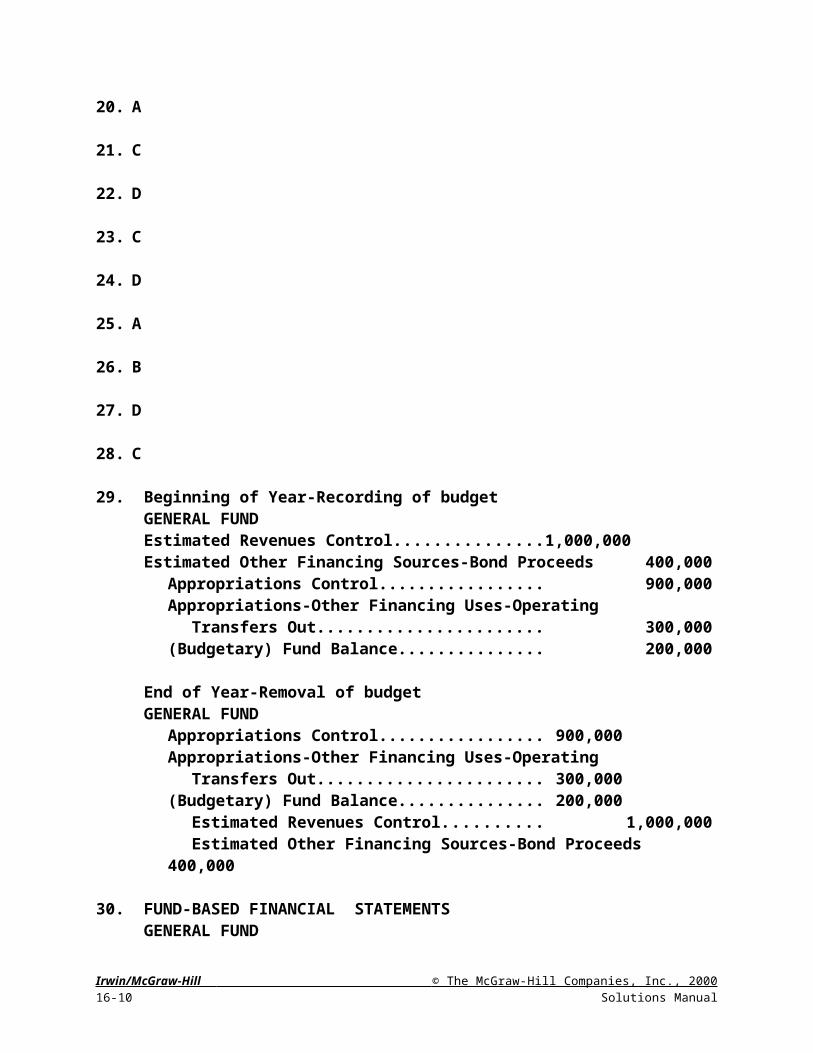

20. A

21. C

22. D

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-7

23. C

24. D

25. A

26. B

27. D

28. C

29. Beginning of Year-Recording of budgetGENERAL FUNDEstimated Revenues Control........................................ 1,000,000Estimated Other Financing Sources-Bond Proceeds 400,000

Appropriations Control............................................ 900,000Appropriations-Other Financing Uses-Operating

Transfers Out....................................................... 300,000(Budgetary) Fund Balance....................................... 200,000

End of Year-Removal of budgetGENERAL FUND

Appropriations Control............................................ 900,000Appropriations-Other Financing Uses-Operating

Transfers Out....................................................... 300,000(Budgetary) Fund Balance....................................... 200,000

Estimated Revenues Control.............................. 1,000,000Estimated Other Financing Sources-Bond Proceeds 400,000

30. FUND-BASED FINANCIAL STATEMENTSGENERAL FUNDEncumbrances Control 88,000

Fund Balance-Reserved for Encumbrances 88,000

Fund Balance-Reserved for Encumbrances 88,000Encumbrances Control 88,000

Expenditures Control 89,400Vouchers Payable 89,400

Vouchers Payable 89,400Cash 89,400

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-8 Solutions Manual

GOVERNMENT-WIDE FINANCIAL STATEMENTSGovernment ActivitiesComputer 89,400

Vouchers (or Accounts) Payable 89,400

Vouchers (or Accounts) Payable 89,400Cash 89,400

31. GOVERNMENT-WIDE FINANCIAL STATEMENTSGOVERNMENT ACTIVITIESIssuances of BondsCash 830,000

Bonds Payable 830,000Completion of ConstructionBuildings 920,000

Cash 920,000

FUND-BASED FINANCIAL STATEMENTSGENERAL FUNDTo Record TransferOther Financing Uses-Transfers Out 90,000

Cash 90,000

CAPITAL PROJECTS FUNDCash 90,000

Other Financing Sources 90,000Sale of Bonds Cash 830,000

Other Financing Sources-Bonds Proceeds 830,000Completion of ConstructionExpenditures 920,000

Contracts Payable 920,000

32. FUND-BASED FINANCIAL STATEMENTSa. General Fund

Estimated Revenues ControlEstimated Other Financing Sources Control(Budgetary) Fund Balance

Appropriations Control

b. Capital Projects FundCash

Other Financing Sources-Bond Proceeds

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-9

c. General FundEncumbrances

Fund Balance Reserved for Encumbrances

d. General FundFund Balance Reserved for Encumbrances

EncumbrancesExpenditures Control

Vouchers Payable

e. General Fund Vouchers Payable

Cash

f. General FundOther Financing Uses-Transfers Out-Capital Projects

Due to Capital Projects Fund (Special Assessment)

Capital Projects FundDue from General Fund

Other Financing Sources-Transfers In -General Fund

g. General FundOther Financing Uses-Transfers Out-Motor Pool

Cash

Internal Service FundCash

Other Financing Sources-Transfers In-General Fund

h. General FundProperty Taxes Receivable

Revenues - Property TaxesAllowance for Uncollectible Taxes

i. Special Revenue FundThe following entries are made on the assumption that the appropriate payment of the supplement is an eligibility requirement for the grant.

Cash Deferred Revenue

j. Expenditures—SalariesCash

Deferred Revenue

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-10 Solutions Manual

Revenues—Grant

GOVERNMENT-WIDE FINANCIAL STATEMENTS

a. No entry

b. Governmental Activities Cash

Bonds Payable

c. No entry

d. Governmental Activities Equipment

Vouchers Payable

e. Governmental Activities Vouchers Payable

Cash

f. No entry

g. No entry (assuming the internal service fund is treated as a government activity so that this is an intra-activity transaction)

h. Governmental Activities Property Taxes Receivable

Revenues - Property TaxesAllowance for Uncollectible Taxes

i. Governmental Activities Cash

Deferred Revenues

j. Governmental Activities Expense-Public Safety

Cash

Deferred Revenue Revenue

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-11

33. FUND-BASED FINANCIAL STATEMENTS

a. General FundEncumbrances Control 94,000

Fund Balance-Reserved for Encumbrances 94,000

b. General FundExpenditures (or Supplies) 1,200

Due to Internal Service Fund 1,200

c. Capital Projects FundCash 700,000

Other Financing Sources-Bonds Proceeds 700,000

d. General FundOther Financing Uses-Transfers Out-

Swimming Pool 20,000Cash 20,000

e. General FundFund Balance-Reserved for Encumbrances 94,000

Encumbrances Control 94,000Expenditures 96,000

Vouchers Payable 96,000

f. General FundOther Financing Uses-Transfer Out 32,000

Cash 32,000

Capital Projects FundCash 32,000

Other Financing Uses-Transfer Out 32,000

g. Special Revenue FundCash 30,000

Deferred Revenues 30,000

h. Special Revenue FundDeferred Revenues 5,000

Revenues 5,000

Expenditures 5,000Cash 5,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-12 Solutions Manual

GOVERNMENT-WIDE FINANCIAL STATEMENTS

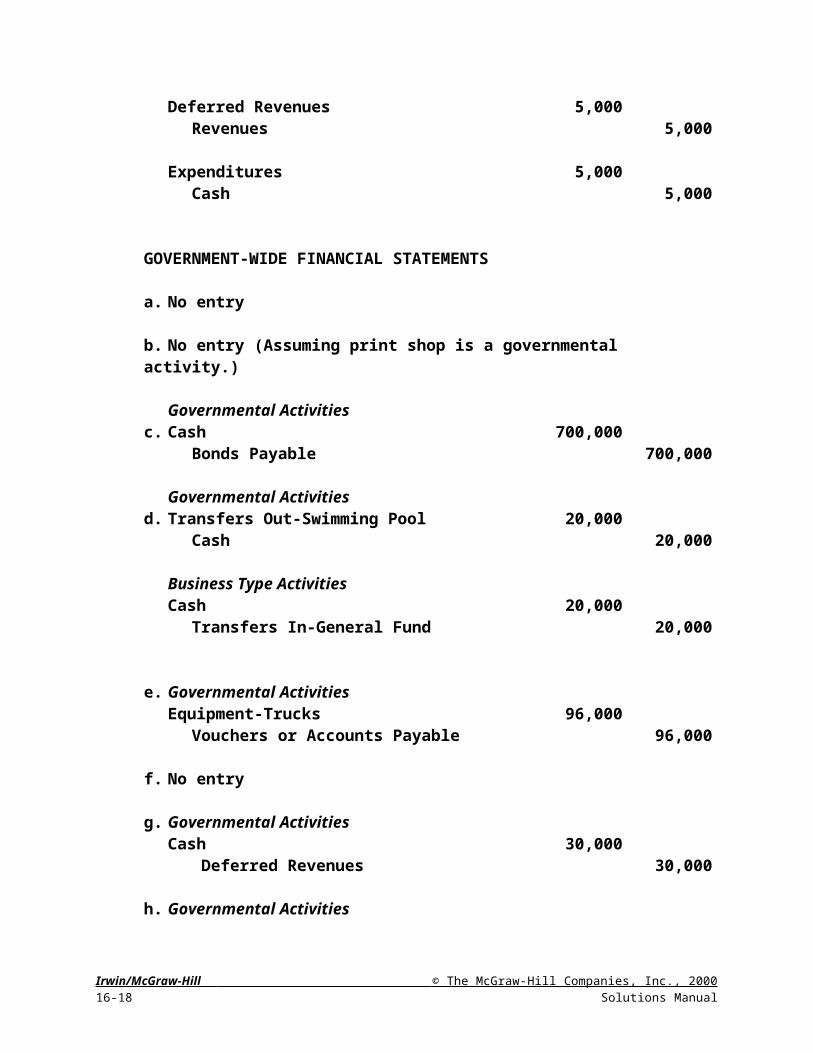

a. No entry

b. No entry (Assuming print shop is a governmental activity.)

Governmental Activitiesc. Cash 700,000

Bonds Payable 700,000

Governmental Activitiesd. Transfers Out-Swimming Pool 20,000

Cash 20,000

Business Type ActivitiesCash 20,000

Transfers In-General Fund 20,000

e. Governmental Activities

Equipment-Trucks 96,000Vouchers or Accounts Payable 96,000

f. No entry

g. Governmental Activities Cash 30,000

Deferred Revenues 30,000

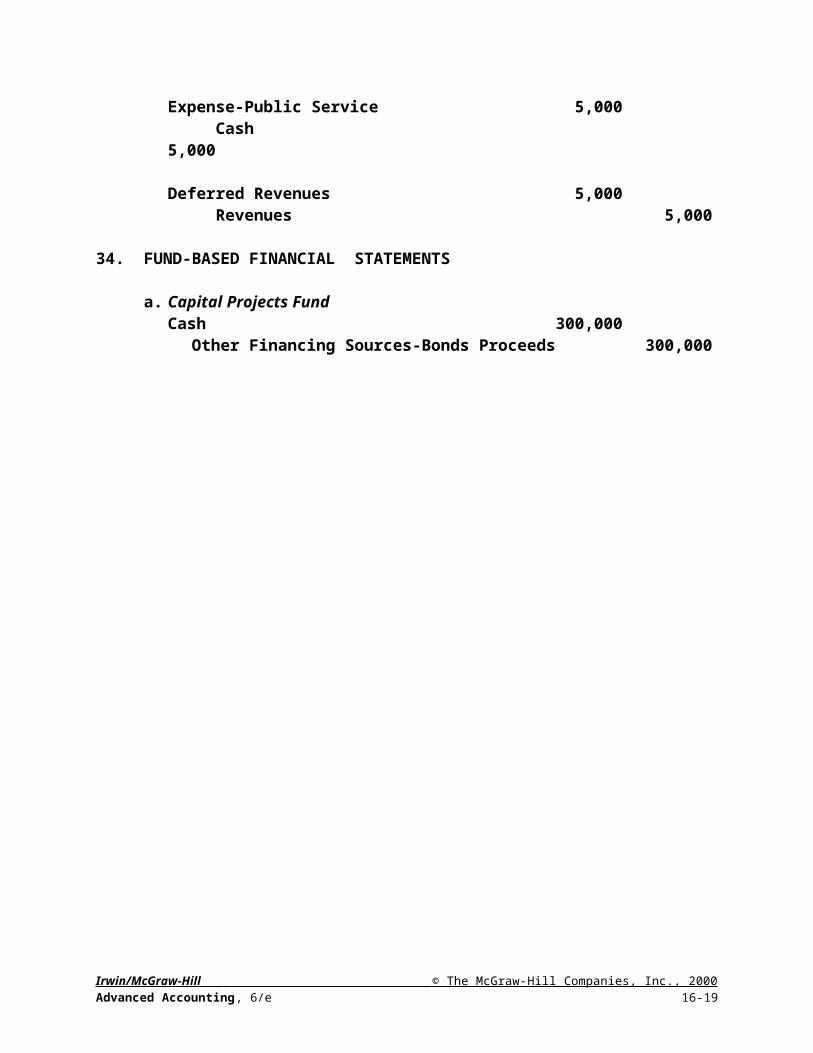

h. Governmental Activities Expense-Public Service 5,000

Cash5,000

Deferred Revenues 5,000Revenues 5,000

34. FUND-BASED FINANCIAL STATEMENTS

a. Capital Projects FundCash 300,000

Other Financing Sources-Bonds Proceeds 300,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-13

b. Capital Projects FundEncumbrances 400,000

Fund Balance-Reserved For Encumbrances 400,000

c. General FundOther Financing Uses-Transfers Out 20,000

Cash 20,000

Debt Service FundCash 20,000

Other Financing Sources-Transfer In 20,000

d. General FundFund Balance-Reserved for Encumbrances 11,800

Encumbrances 11,800

Expenditures Control-Machinery and Equipment 12,000Vouchers Payable 12,000

e. General FundInventory of Supplies 2,000

Cash 2,000

f. Special Revenue FundCash 5,000

Deferred Revenues 5,000

g. General FundTaxes Receivable 600,000

Revenues Control 576,000Allowance for Uncollectible Current Taxes 24,000

GOVERNMENT-WIDE FINANCIAL STATEMENTS

a. Governmental ActivitiesCash 300,000

Bonds Payable 300,000

b. No entry

c. No entry

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-14 Solutions Manual

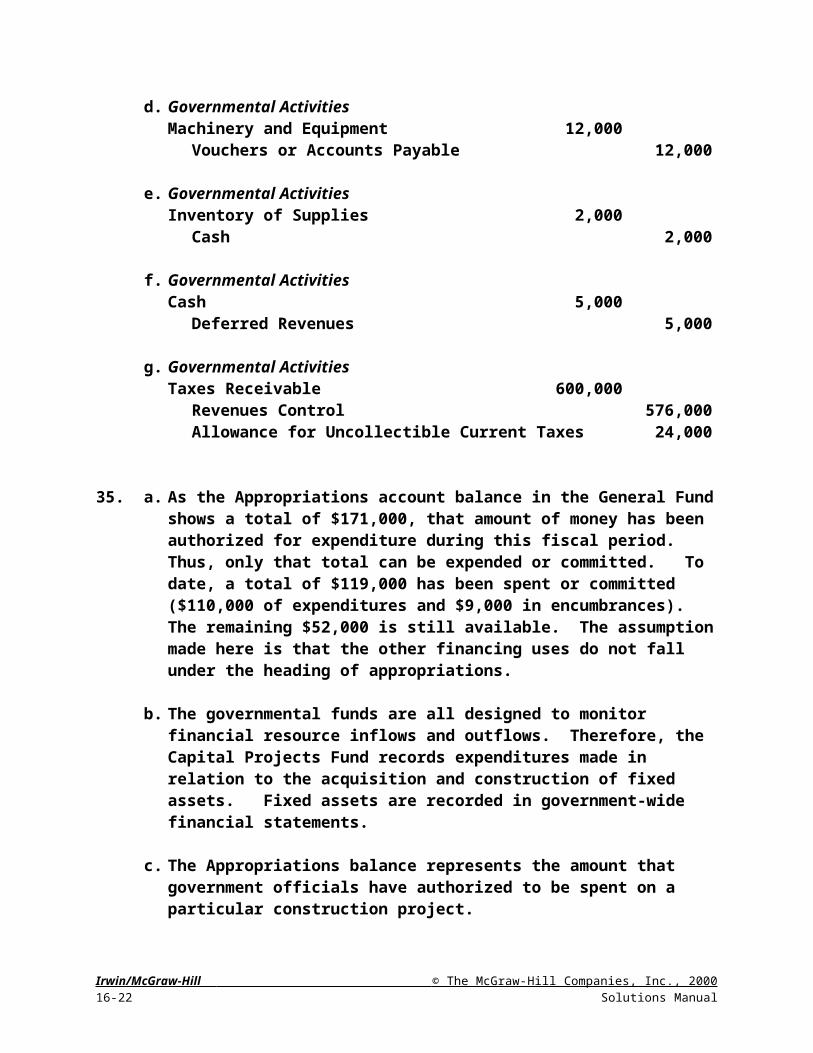

d. Governmental ActivitiesMachinery and Equipment 12,000

Vouchers or Accounts Payable 12,000

e. Governmental ActivitiesInventory of Supplies 2,000

Cash 2,000

f. Governmental ActivitiesCash 5,000

Deferred Revenues 5,000

g. Governmental ActivitiesTaxes Receivable 600,000

Revenues Control 576,000Allowance for Uncollectible Current Taxes 24,000

35. a. As the Appropriations account balance in the General Fund shows a total of $171,000, that amount of money has been authorized for expenditure during this fiscal period. Thus, only that total can be expended or committed. To date, a total of $119,000 has been spent or committed ($110,000 of expenditures and $9,000 in encumbrances). The remaining $52,000 is still available. The assumption made here is that the other financing uses do not fall under the heading of appropriations.

b. The governmental funds are all designed to monitor financial resource inflows and outflows. Therefore, the Capital Projects Fund records expenditures made in relation to the acquisition and construction of fixed assets. Fixed assets are recorded in government-wide financial statements.

c. The Appropriations balance represents the amount that government officials have authorized to be spent on a particular construction project.

d. To alert readers to the commitment, a year-end reclassification entry is also made to reduce the “Fund Balance Unreserved, Undesignated” in order to report a “Fund Balance-Reserved for Encumbrances.”

e. The most likely explanation for the zero balance in the Fund Balance-Unreserved, Undesignated is that this capital project was begun during the current year, and thus, no closing entries have, as of yet, been made.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-15

f. Two possible reasons can be put forth for the $150,000 Other Financing Sources balance. First, a bond may have sold. Since the debt itself would be recorded in the government-wide financial statements, the governmental fund must record the receipt by means of an Other Financing Sources designation. Second, the $150,000 may have come from an interfund transfer. An operating transfer is not considered revenue by the recipient and is, therefore, recorded as an Other Financing Source.

g. The Debt Service Fund is utilized to accumulate money to pay off the principal and interest of any long-term liability incurred by the governmental funds. The debt itself is maintained in the government-wide financial statements. Payment of the debt and interest is made from the Debt Service Fund and recorded as an expenditure.

h. Special assessment projects are undertaken by a government to benefit particular properties with the owners bearing part (or all) of the cost. Curbing, as an example or the installation of lights usually are special assessment projects. If the government has no responsibility for the costs, recording of all financial resources inflows and outflows is made in an Agency Fund. However, if the government does have some responsibility (if, for example, the government is secondarily liable for any debts incurred), the construction is recorded in a Capital Projects Fund. Thus, the receivable balance shown here would indicate that this project is being recorded in this manner. Collection will be made from the citizens being benefited and used in paying for the construction.

i. The purchase method is apparently being used to record materials and supplies. In this approach, such acquisitions are recorded as expenditures when liabilities are initially incurred. Subsequently, at the end of the year, any materials or supplies that remain are entered into the records as assets with an offsetting amount shown as a “Fund Balance Reserved for Inventory of Supplies.” This designation indicates that the government is reporting an asset that is not free for future expenditure.

j. Budgetary entries are optional for Debt Service Funds but are rarely used. Expenditure levels (for principal and interest) are set contractually by the debt indenture. Thus, additional fiscal control is not obtained by the inclusion of budgetary amounts.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-16 Solutions Manual

36. a. Estimated Revenue $232,000Appropriation 225,000

Budgetary Fund Balance $ 7,000

Since estimated revenues exceed the appropriations, a surplus is anticipated which is mirrored through a credit balance in the Budgetary Fund Balance account.

b. Initially, all of the school supplies are recorded in an asset account such as “Inventory of Supplies.” As the supplies are used, the cost is reclassified into an Expenditures account.

c. At the end of 2000, the Encumbrances balance will be closed out to the Fund Balance account. This reduces the unreserved amount to be shown. When the balance sheet is produced, the Reserved Fund Balance amount will be reported to indicate that financial resources must be held to pay off this commitment when it becomes an actual liability.

d. FUND-BASED FINANCIAL STATEMENTSGeneral FundFund Balance-Reserved for Encumbrances 111,000

Encumbrances 111,000

Expenditures Control 120,000Vouchers Payable 120,000

GOVERNMENT-WIDE FINANCIAL STATEMENTSGovernmental Activities Vehicles 120,000

Vouchers or Accounts Receivable 120,000

e. General FundOther Financing Uses-Transfers Out 33,000

Cash 33,000

Debt Service FundCash 33,000

Other Financing Sources-Transfer In 33,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-17

f. REVENUES:Government grant appropriately expended $ 24,000Property taxes to be received currently 190,000Business licenses and parking meters 14,000

Total revenues $228,000

g. EXPENDITURES:Salary for police officers $ 21,000Rent on equipment 3,000City hall 1,044,000

Salary for ambulance drivers 24,000Ambulance 120,000School bus 40,000

Total expenditures $1,252,000

Note: Assuming the consumption method is in use, the supplies that have been used to date (40% from b.) should also be recorded as expenditures.

h. FUND-BASED FINANCIAL STATEMENTSCapital Projects FundCash 300,000

Other Financing Sources 300,000

GOVERNMENT-WIDE FINANCIAL STATEMENTSGovernmental Activities Cash 300.000

Bonds Payable 300,000

37. FUND-BASED FINANCIAL STATEMENTSa. General Fund

Estimated Revenues Control 834,000Appropriations Control 540,000Estimated Other Financing Uses-

Operating Transfers 242,000Budgetary Fund Balance 52,000

b. Capital Projects FundEncumbrances Control 8,000,000

Fund Balance-Reserved for Encumbrances 8,000,000

c. Capital Projects FundCash 8,000,000

Other Financing Sources Control 8,000,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-18 Solutions Manual

d. Capital Projects FundFund Balance-Reserved for Encumbrances 8,000,000

Encumbrances Control 8,000,000

Expenditures Control 8,000,000Contracts Payable 8,000,000

Contracts Payable 8,000,000Cash 8,000,000

e. General FundOther Financing Uses Control 1,000,000

Cash 1,000,000

Debt Service FundCash 1,000,000Other Financing Resources 1,000,000

f. Debt Service FundExpenditures Control-Bonds 900,000Expenditures Control-Interest 100,000

Cash 1,000,000

g. General FundProperty Taxes Receivable 800,000

Revenues Control 768,000Allowance for Uncollectible Taxes 32,000

h. Special Revenue FundCash 120,000

Revenues Control 120,000

i. Permanent FundInvestments 300,000

Fund Balance-Reserved for Park Beautification 300,000

GOVERNMENT-WIDE FINANCIAL STATEMENTS

a. No entry

b. No entry

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-19

c. Governmental Activities Cash 8,000,000

Bonds Payable 8,000,000

d. Governmental Activities Buildings 8,000,000

Cash 8,000,000

e. No entry

f. Governmental Activities Bond Payable 900,000Interest Expense 100,000

Cash 1,000,000

g. Governmental ActivitesProprety Taxes Receivable 800,000

Revenues Control 768,000Allowance for Uncollectible Taxes 32,000

h. This entry is made in the Governmental Activities unless the toll road is reported as an Enterprise Fund.

Cash 120,000Revenues—Reserved for Highway Maintenance 120,000

i. Government ActivitiesInvestments 300,000

Revenues—Donations 300,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-20 Solutions Manual

38.CITY OF JENNINGS

GENERAL FUNDStatement of Revenues, Expenditures, and Changes in Fund Balance

(Condensed)Year Ending December 31, 2001

Revenues $ 740,000Expenditures (420,000 )

Excess (deficiency) of revenues over expenditures $ 320,000 Other financing sources (uses):

Bond Proceeds $300,000Transfers in 50,000Transfers out (470,000 )

Total Other Financing Uses and Sources (120,000 ) Excess of Revenues and Other Sources over

Expenditures and Other Uses 200,000Increase in Reserve for Encumbrances (90,000)Change in Fund Balance $110,000

Fund Balance, Beginning 170,000Fund Balance, Ending $280,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-21

CITY OF JENNINGSGENERAL FUND

Balance Sheet (condensed)December 31, 2001

AssetsCash $ 30,000Investments 410,000Taxes receivable 220,000Due from Capital Projects Fund 60,000

Total assets $720,000

LiabilitiesVouchers payable $180,000Contracts Payable 90,000Due to Debt Service Projects Fund 40,000Deferred revenues 40,000

Total Liabilities $350,000

EquityFund balances:Reserved for encumbrances $90,000Unreserved, undesignated fund balance 280,000

Total Fund Balance 370,000

Total liabilities and fund equity $720,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 16-22 Solutions Manual

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e 16-23