chapter 18 - test bank

DESCRIPTION

Advanced Financial Accounting by Baker 9edTRANSCRIPT

ch18Student: ___________________________________________________________________________

1.

Which of the following funds use the accrual basis of accounting? A. I onlyB. II onlyC. I and III onlyD. I, II, and III

2. A special revenue fund should be used in which of the following situations for a state government?

A. For sales taxes which are to be distributed to towns, cities, villages, etc. of the state.B.

For the proceeds of general obligation bonds which are to be used to construct major long-lived fixed assets.

C. For gasoline taxes which are to be used exclusively to repair state roads and bridges.D.

For investments donated by a prominent citizen which are to be invested permanently, with income being used to support homeless people.

3. For which of the following funds are the principles and accounting most like those of the general fund?

A. Debt service fundB. Internal service fundC. Special revenue fundD. Investment trust fund

4. Which of the following items would not be reported on the financial statements of a special revenue

fund? A. Long-term productive assets.B. Expenditures and revenues.C. Vouchers payable and unreserved fund balance.D. Fund balance reserved for encumbrances and expenditures.

5. A city's museum is supported by a special tax levy and by user charges. The user charges constitute only

10 percent of the resources needed to support the operations of the museum. In which fund should the city account for its museum? A. An enterprise fundB. An agency fundC. An expendable trust fundD. A special revenue fund

6.

Fixed assets and investments are reported in which of the following funds? A. I, II, IIIB. II, IV, VC. I, II, VD. II, III, IV

7.

Which of the following funds report fixed assets on their balance sheets? A. I, IIB. II, IIIC. I, IVD. III, IV

8. Ponca City issued general obligation bonds to finance construction of a new city hall. In the city hall

capital projects fund, the proceeds of the general obligation bonds should be credited to: A. Revenue-General Obligation Bonds.B. General Obligation Bonds Payable.C. Deferred Revenue-General Obligation Bonds.D. Other Financing Sources-Bond Issue Proceeds.

9. The City of Fargo issued general obligation bonds to finance construction of a new fire station. The bonds

were issued at a discount. Which of the following is true?I. The amount expended for the improvement must be decreased.II. The general fund must make up the difference to the face value of the bonds.III. A debt service fund must make up the difference to the face value of the bonds. A. I onlyB. Either I or IIIC. Either II or IIID. Either I or II

10. The costs of a building being constructed by a capital projects fund should be debited, or charged, to

which of the following accounts in the capital projects fund? A. Expenditures.B. Building.C. Construction in Progress.D. Other Financing Uses.

11. When a capital projects fund transfers a premium from the issuance of general obligation bonds to

another fund, the transfer should be accounted for as which type of interfund transaction or transfer? A. As a loan.B. As an interfund transfer.C. As revenue.D. As a reimbursement.

12. A debt service fund for the City of Madison received $50,000 from a capital projects fund. The amount

received represented the premium received from the issuance of general obligation bonds. What account should the debt service fund credit to record this receipt? A. Revenue-General Obligation Bond Premium.B. Matured Bonds Payable.C. Other Financing Sources—Transfer In from Capital Projects Fund.D. Due to Capital Projects Fund.

13. Upon completion of construction and full payment of all construction costs in a capital projects fund, the

entry to record the transfer of any remaining cash should include a debit to:I. Contract Payable-Retained Percentage.II. Transfer Out to Debt Service Fund. A. I onlyB. II onlyC. Either I or IID. Neither I nor II

14. On July 1, 20X8, Cleveland established a capital projects fund to construct a new town hall. Financing for

construction came from the following sources: Construction of the town hall was completed on June 15, 20X9. For the fiscal year ended June 30, 20X9, what amount should Cleveland's capital projects fund report for revenues on its statement of revenues, expenditures, and changes in fund balance? A. $1,000,000B. $1,500,000C. $3,500,000D. $14,500,000

15. On the statement of revenues, expenditures, and changes in fund balance for a capital projects fund,

proceeds of general obligation bonds should be reported: A. in the revenue section of the statement.B. as a direct addition to the beginning balance of unreserved fund balance.C. in the other financing sources (uses) section of the statement.D. as a subtraction from construction expenditures.

16. The capital projects fund of Hood River completed construction of an addition to its city hall at a cost

of $4,000,000. The city council approved payment of the amount due the general contractor, less a 10 percent retainage. How should the capital projects fund account for the 10 percent retainage?I. As a credit of $400,000 to Deferred Revenue-Retained Percentage.II. As a credit for $400,000 to Contracts Payable-Retained Percentage. A. I onlyB. II onlyC. Either I or IID. Neither I nor II

17. The capital projects fund of Hysham completed construction of a new building. The building should be

reported in the:I. government-wide statement of net assets.II. capital projects fund. A. I onlyB. II onlyC. Either I or IID. Neither I nor II

18. During the fiscal year ended June 30, 20X9, the city of Moorhead constructed a new courthouse which

was budgeted to cost $5,000,000. Moorhead used a capital projects fund to account for the construction activities. In July of 20X8, a bid was accepted from Diamond Construction to build the courthouse for $4,800,000. On June 15, 20X9, Diamond completed construction and submitted a bill to the city for $4,900,000. The city accepted the bill and paid Diamond the entire amount owed, except for a 10 percentage retainage. On the statement of revenues, expenditures, and changes in fund balance prepared for the capital projects fund for the year ended June 30, 20X9, expenditures should be reported at A. $4,900,000.B. $4,800,000.C. $4,410,000.D. $4,320,000.

19. The town of Decorah issued general obligation serial bonds at par to finance construction of several new streets in the town. Construction activity was accounted for in a capital projects fund. On the date the general obligation serial bonds were issued, what account was credited in Decorah's capital projects fund? A. Serial Bonds PayableB. Due to Debt Service FundC. RevenuesD. Other Financing Sources-Bond Issue Proceeds

20. The City of Fargo issued general obligation bonds to finance construction of a new fire station. The bonds

were issued at a premium. In the fire station capital projects fund, the premium should be transferred to: A. an agency fund.B. a special revenue fund.C. a debt service fund.D. an expendable trust fund.

21. For which of the following long-term debt obligations would payments not be accounted for in a debt

service fund? A. Notes and warrants secured by specific tax revenues.B. Special assessment bonds sold to acquire enterprise fund assets.C. Notes and warrants.D. Special assessment bonds may be used to finance capital projects.

22. A debt service fund of Clifton received $100,000 from its general fund during the fiscal year ended June

30, 20X9. The cash was used to pay matured interest on Clifton's general obligation bonds, which were issued to finance construction of a new municipal building. On the statement of revenues, expenditures, and changes in fund balance prepared for the debt service fund for the year ended June 30, 20X9, the amount received from the general fund should be reported as: A. revenue.B. a reduction of expenditures.C. another financing source.D. matured interest payments.

23. What account is debited in a debt service fund when it records matured interest payable?

I. Interest ExpenseII. Expenditures A. I onlyB. II onlyC. Either I or IID. Neither I nor II

24. On the statement of revenues, expenditures, and changes in fund balance prepared for a debt service fund,

the cash paid to retire matured serial bonds is reported as:I. expenditures.II. a direct deduction from unreserved fund balance. A. I onlyB. II onlyC. Either I or IID. Neither I nor II

25. Arlington has a debt service fund which it uses to pay the principal and interest on its $2,000,000 of general long-term debt. Interest at 5 percent is due on October 1 and April 1. On October 1, 20X8, and April 1, 20X9, Arlington's debt service fund paid $50,000 of interest due on its bonds. On the balance sheet prepared on June 30, 20X9, for Arlington's debt service fund, interest payable should be reported at: A. $0.B. $16,667.C. $25,000.D. $50,000.

26. What account should be debited in the debt service fund to recognize an installment payment currently

due on general obligation serial bonds?I. Matured Bonds Payable.II. Expenditures-Principal. A. IB. IIC. Either I or IID. Neither I nor II

27. As of May 30, 20X9, the debt service fund of Cody had accumulated $52,000 of assets in a debt service

fund to pay the principal of its currently maturing serial bonds. On June 1, 20X9, $50,000 of serial bonds matured and were paid with the resources accumulated in the debt service fund. In Cody's debt service fund, Matured Bonds Payable was debited for $50,000 and: A. Cash was credited for $50,000.B. Due to General Fund was credited for $50,000.C. Investments was credited for $50,000.D. Reserve for Encumbrances was credited for $50,000.

28. Which of the following statement is true regarding permanent funds?

A. Permanent funds do not have any donor restrictions when they are established.B.

Permanent funds have a donor restriction on the fund principal but the income from the fund may be used to benefit the government's program.

C.

Permanent funds have a donor restriction on the income generated from the fund principal but the principal may be used to benefit the government's program.

D. The cash or accrual basis of accounting may be used to account for a permanent fund.

29. On January 1, 20X1, Washington City received 200,000 from an estate with the stipulation that the money be invested and the income be used to provide maintenance to the city cemetery. The money was invested in 7% governmental securities at 90 to yield an effective interest rate of 10%. The following journal entry would be made to account for the accrued interest of the permanent

fund: A. Option AB. Option BC. Option CD. Option D

30. Required financial statements of funds may include the following, among

others: The financial statements that should be issued by governmental funds and by proprietary funds include

the following: A. Option AB. Option BC. Option CD. Option D

31. At June 30, 20X9, total assets for the various funds of a local municipality were as

follows: Applying GASB 34 criteria, which of the above are major funds for reporting purposes? A. GF, CPF, EFB. CPF, EFC. CPF, ISF, EFD. GF, CPF, ISF, EF

32. GASB 34 specifies two criteria for determining major governmental funds to be reported separately in

the Governmental Fund Balance Sheet and Statement of Revenues, Expenditures, and Changes in Fund Balances. To be considered a major governmental fund, a fund must: A. meet at least one criterion.B. be the general fund or meet at least one criterion.C. be the general fund or meet two criteria.D. either A or C.

33. On October 15, 20X8, an enterprise fund of Blacksburg purchased office supplies at a cost of $10,000.

The inventory of office supplies on hand at the June 30, 20X9, fiscal year end was $4,000. There was no beginning inventory. Blacksburg should make entries that include: A. debiting Supplies $10,000 at October 15, and debiting Expenses $4,000 on June 30.B. debiting Expenditures $10,000 at October 15, and debiting Supplies $4,000 at June 30.C. debiting Supplies $10,000 at October 15, and crediting Supplies $6,000 on June 30.D. debiting Expenditures $10,000 at October 15, and crediting Expenses $4,000 at June 30.

34. The costs of enterprise fund activities are recovered

A. from special tax levies.B. from federal or state governmental grants.C. by user charges.D. by private donations.

35. An enterprise fund of Grist was billed $10,000 for using the services of an internal service fund's data

processing center. What account should Grist's enterprise fund debit to record this billing? A. Due to Internal Service FundB. ExpendituresC. Transfer Out to Internal Service FundD. General Operating Expenses

36. During the fiscal year ended June 30, 20X9, an enterprise fund of St. Cloud acquired computer equipment costing $110,000 on account and issued $400,000 of long-term bonds. Revenues of the enterprise fund will be used to repay bond interest and principal. What effect did these transactions have on St. Cloud's

enterprise fund assets and long-term debt? A. Option AB. Option BC. Option CD. Option D

37. Which of the following characteristics best describes an enterprise fund?

A. Capital maintenance, revenues from general public user charges, and net income.B. Operating budgets, expenditures, and tax revenues from general public.C. Capital maintenance, revenues from user charges to other funds, and net income.D. Capital maintenance, tax revenues from general public, and net income.

38. Which of the following financial statements would not be prepared for an enterprise fund?

A. A statement of cash flows.B. A statement of revenues, expenses, and changes in fund net assets.C. A balance sheet.D. A statement of revenues, expenditures, and changes in fund balance.

39. The following information pertains to Auburn's water and sewer fund, an enterprise fund, for the year

ended June 30, 20X9: Based upon the information presented, what was the increase in the enterprise funds unrestricted net assets for the fiscal year ended June 30, 20X9? A. $200,000B. $240,000C. $300,000D. $320,000

40. On the statement of cash flows prepared for an internal service fund, cash received from customers and

cash paid for operating expenses should be reported as A. investing activities.B. operating activities.C. noncapital financing activities.D. capital and related financing activities.

An internal service fund had the following transactions during the year ended June 30, 20X9, its first year of existence:(1) Received $1,000,000 contribution from the general fund.(2) Acquired fleet of cars for $950,000, paying cash.(3) Billed departments in other funds $500,000 for using cars.(4) Incurred operating costs, exclusive of depreciation, of $240,000.(5) Depreciation expense amounted to $250,000.

41. Refer to the above information. On the internal service fund's balance sheet on June 30, 20X9, total net

assets should be reported at: A. $1,000,000.B. $1,010,000.C. $1,250,000.D. $910,000.

42. Refer to the above information. On the internal service fund's balance sheet at June 30, 20X9, net assets-unrestricted should be reported at: A. $260,000.B. $310,000.C. $550,000.D. $1,250,000.

43. Enterprise and internal service funds should recognize revenues when they are

A. received in cash.B. available and earned.C. measurable and earned.D. measurable and available.

44. Carlisle established a motor vehicle service and maintenance fund to service and maintain all cars and

trucks owned by the town. Revenues of the fund will only come from billings to the funds which use the motor vehicle service and maintenance fund. What type of fund is the motor vehicle service and maintenance fund? A. An enterprise fund.B. A special revenue fund.C. An expendable trust fund.D. An internal service fund.

The City of Warwick received $4,000,000 from one of its most prominent citizens during the year ended June 30, 20X9. The donor stipulated that the $4,000,000 be invested permanently, and that interest and dividends earned on the investments be used to support the homeless people of Warwick. During the year ended June 30, 20X9, dividends received from stock investments amounted to $20,000, while interest received from bond investments amounted to $40,000. At June 30, 20X9, $10,000 of interest was earned, but it will not be received until July of 20X9. The fair value of the securities in which the $4,000,000 was invested had increased $8,000 by June 30, 20X9. 45. Refer to the above information. For the year ended June 30, 20X9, what amount should the trust fund

report as investment earnings on the statement of revenues, expenses, and changes in fund balance? A. $60,000B. $68,000C. $70,000D. $78,000

46. Refer to the above information. On the statement of fiduciary net assets at June 30,

20X9, the nonexpendable trust fund should report investments and interest receivable

of: A. Option AB. Option BC. Option CD. Option D

47. A trust fund of Bruge City received $100,000 from a donor during the year ended June 30, 20X9. During

the year ended June 30, 20X9, $94,000 of the cash received was used to provide food and clothing to the city's poor. How should the trust fund report these resource flows on its statement of changes in fiduciary net assets for the year ended June 30, 20X9? A. As revenues of $100,000 and as expenditures of $94,000.B. As contributions for $100,000 and as deductions for benefits for $94,000.C. As revenues of $100,000 and as an operating transfer out for $94,000.D. As a transfer in from trust fund for $100,000 and as a transfer out for $94,000.

48. A tax collection fund that collects property taxes and then distributes them to local governmental units is an example of a(n): A. trust fund.B. agency fund.C. internal service fund.D. permanent fund.

49. Agency funds report:

A. only assets and liabilities.B. assets, liabilities, fund balance, revenues, and expenditures.C. assets, liabilities, and fund balance.D. only revenues and expenditures.

Riviera Township reported the following data for its governmental activities for the year ended June 30,

20X9: Additional information available is as follows:All of the long-term debt was used to acquire capital assets. Cash of $475,000 is restricted for debt service.

50. Based on the preceding information, on the statement of net assets prepared at June 30, 20X9, what

amount should be reported for total net assets? A. $2,425,000B. $4,200,000C. $2,900,000D. $3,625,000

51. Based on the preceding information, on the statement of net assets prepared at June 30, 20X9, what

amount should be reported for net assets invested in capital assets, net of related debt? A. $4,200,000B. $2,900,000C. $2,825,000D. $3,300,000

52. Based on the preceding information, on the statement of net assets prepared at June 30, 20X9, what

amount should be reported for net assets, unrestricted? A. $425,000B. $900,000C. $525,000D. $825,000

53. A citizen of York purchased a truck in 20X3 for $50,000. On June 10, 20X9, she donated the truck to

York. The fair value of the truck on the date of donation was $30,000. How should York report the truck in its government-wide Statement of Net Assets? A. Machinery and equipment should be increased $50,000.B. Machinery and equipment should be increased $30,000.C. Machinery and equipment should be decreased $20,000.D. No asset should be reported because no expenditures were made to acquire the truck.

54. The general fund of Reston acquired computer equipment costing $70,000 during the fiscal year ended June 30, 20X9. Machinery and Equipment should be reported in Reston's General Fund Balance Sheet and government-wide Statement of Net Assets at June 30, 20X9, as

follows: A. Option AB. Option BC. Option CD. Option D

55. Which of the following fiduciary funds does not require a statement of changes in net assets?

I. Private-purpose trust fund.II. Agency fund. A. I onlyB. II onlyC. Both I and IID. Neither I nor II

56. Government-wide financial statements prepared for a municipality include the

following: A. Option AB. Option BC. Option CD. Option D

57. Revenue and expense on a government-wide statement of activities for a municipality should be

measured on a(n) A. cash basis.B. modified accrual basis.C. accrual basis.D. reconciliation basis.

58. The government-wide financial statements prepared for a municipality should include assets acquired by

the following funds: A. Option AB. Option BC. Option CD. Option D

59. The statement of changes in fiduciary net assets includes all of the following except:

A. employee benefit trust funds.B. investment trust funds.C. private-purpose trust funds.D. agency funds.

60. Which presentation method combines the component unit's results into the primary government's financial results? A. Blended presentationB. Discrete presentationC. Combined presentationD. Consolidated presentation

61. A budgetary comparison schedule presented as required supplementary information for the general fund

should report variances for the difference between:I. Original budget amounts and final budget amounts.II. Final budget amounts and actual amounts. A. I onlyB. II onlyC. Both I and IID. Neither I nor II

62. In accordance with the Single Audit Act of 1984, external auditors issue the standard audit report on the

governmental unit's financial statements and must also issue:I. a special report on the effectiveness with which the governmental unit is achieving its social objectives.II. a special report on the governmental unit's internal control system.III. a special report on the governmental unit's compliance with laws and regulations. A. I onlyB. I and IIC. II and IIID. I, II, and III

63. Which of the following items is optional information for a special-purpose governmental entity when

issuing financial reports? A. Management's Discussion and AnalysisB. Footnotes to the financial repotsC. Supplementary Information to the financial reportsD. All of the above are required.

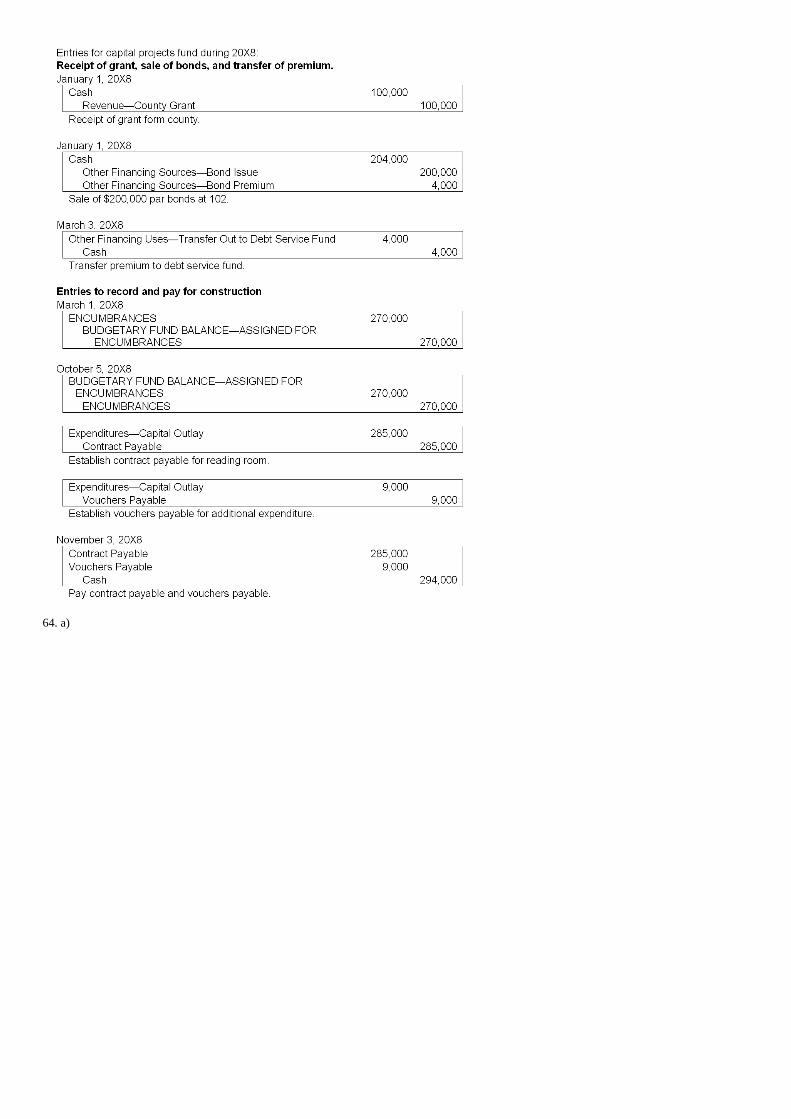

64. The City of Edmond established a capital projects fund for the construction of a reading room for the City

Library. The estimated cost of the construction is $300,000. On January 1, 20X8, an 8 percent, $200,000 bond issue was sold at 102. At that date, the county board provided a $100,000 grant. On March 3, 20X8, the premium from issuance of the bonds was transferred to the debt service fund established to repay the bond principal and interest. On March 1, 20X8, a general contractor's bid was accepted to construct the facility at a cost of $270,000. The construction was completed on October 5, 20X8; its actual cost was $285,000. The city council approved payment of the total actual cost of $285,000. In addition to the $285,000, $9,000 was spent to make the facility ready for use. On November 3, 20X8, the city council gave the final approval for both these payments. After all bills were paid, the remaining fund balance was transferred to the debt service fund.Required:a. Prepare entries for the capital projects fund for 20X8.b. Prepare a statement of revenues, expenditures, and changes in fund balance for 20X8 for the capital projects fund.

65. Prior to closing the accounts at the end of the most recent fiscal year, the Town of Sonora reports the

following amounts (in thousands): Required:Applying the criteria specified in GASB 34, determine which of the above funds should be classified as major funds for reporting purposes.

66. Akron established an internal service fund for its data processing activities on July 1, 20X8. During the

fiscal year ended June 30, 20X9, the following transactions and events occurred:1) On July 1, 20X8, the city council authorized the general fund to contribute $1,000,000 to help establish the internal service fund on July 20, 20X8.2) The internal service fund spent $900,000 of the contribution to acquire a mainframe computer on July 25, 20X8.3) During the year ended June 30, 20X9, the internal service billed other funds of the city $300,000 for use of the computer. By year end, all of the billings were collected except for $30,000.4) The internal service fund incurred general operating expenses of $100,000, exclusive of depreciation, during the year ended June 30, 20X9. All of the expenses were paid by June 30, 20X9, except for $24,000.5) Depreciation expense related to the computer was $180,000.Required:A) Prepare all journal entries that would be recorded by Akron's internal service fund for the year ended June 30, 20X9. Explanations for journal entries are not necessary.B) Prepare a statement of revenues, expenses, and changes in fund net assets for the internal service fund for the year ended June 30, 20X9.C) Calculate the amount of unrestricted net assets at June 30, 20X9.

67. Newport Village was recently incorporated and began financial operations on January 1, 20X8, the beginning of its fiscal year. The following transactions occurred during this first fiscal year, January 1, 20X8, to December 31, 20X8:1. The village council adopted a budget for general operations for the fiscal year ending December 31, 20X8. Revenue was estimated at $650,000. Legal authorizations for budgeted expenditures totaled $620,000.2. Property taxes were levied in the amount of $630,000; 3 percent of this amount was estimated to prove uncollectible. These taxes are available as of the date of levy to finance current expenditures.3. During the year, a village resident donated marketable securities valued at $75,000 to the village under the terms of a trust agreement which stipulates that the principal amount be kept intact. The revenue generated by the securities is restricted to providing support to the village library. Revenue earned and received on these amounted to $3,000 through December 31, 20X8.4. A general fund transfer of $8,000 was made to establish an internal service fund to provide for a permanent investment in inventory.5. The village decided to construct a small recreation facility through a special assessment project authorized to do so at a cost of $100,000. The city is obligated if the property owners default on their special assessments. Special assessment bonds were issued in the amount of $90,000, and the first year's special assessment of $22,500 was levied against the village's property owners. The remaining $10,000 for the project will be contributed from the village's general fund.6. The special assessments for the lighting project are due over a four-year period, and the first year's assessments of $22,500 were collected. The $10,000 transfer from the village's general fund was received by the lighting capital projects fund.7. A contract for $100,000 was let for the installation of the lighting. The capital projects fund was encumbered for the contract. On December, 20X8, the contract was completed and the contractor was paid.8. During the year, the internal service fund purchased various supplies at a cost of $3,000.9. Current property taxes collected during the year was $615,000. Licenses and permit fees collected amounted to $15,000. The allowance for estimated uncollectible taxes is adjusted to $15,000.Required:Prepare journal entries to record each of these transactions in the appropriate fund or funds of Newport Village for the fiscal year ended December 31, 20X8. Use the following funds: general fund, capital projects fund, internal service fund, and private-purpose trust fund. Closing entries are not required. Organize your answer using the following format:

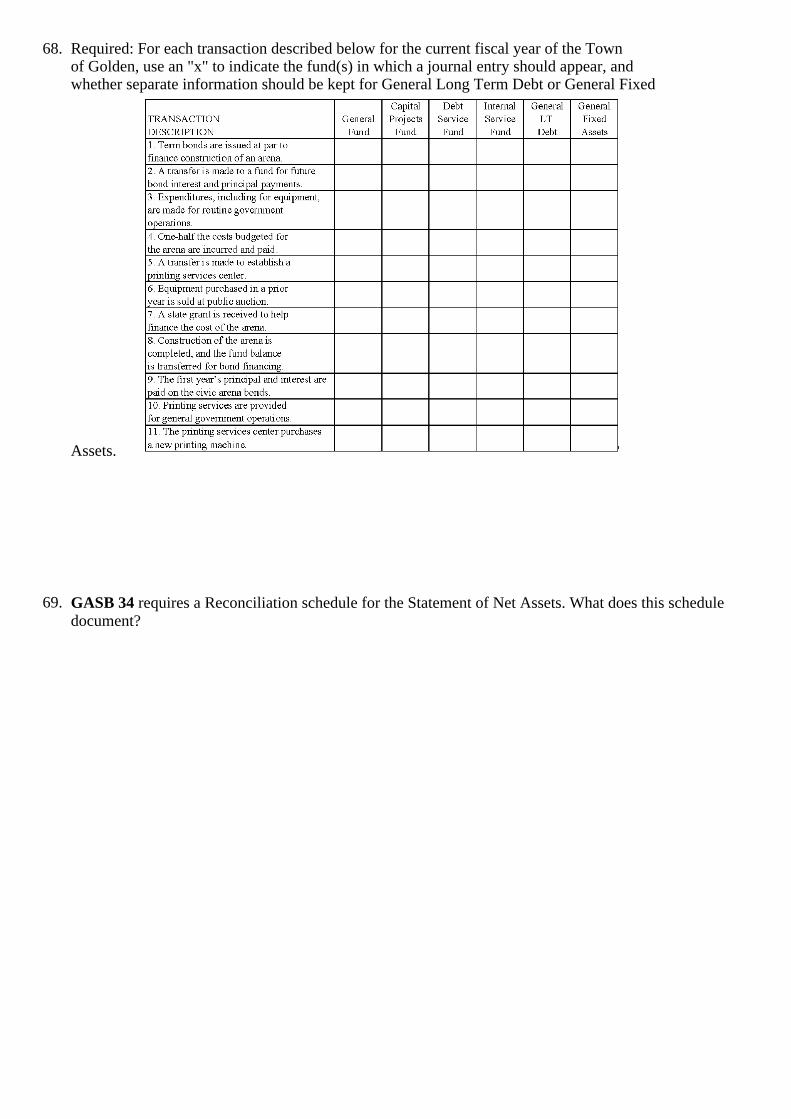

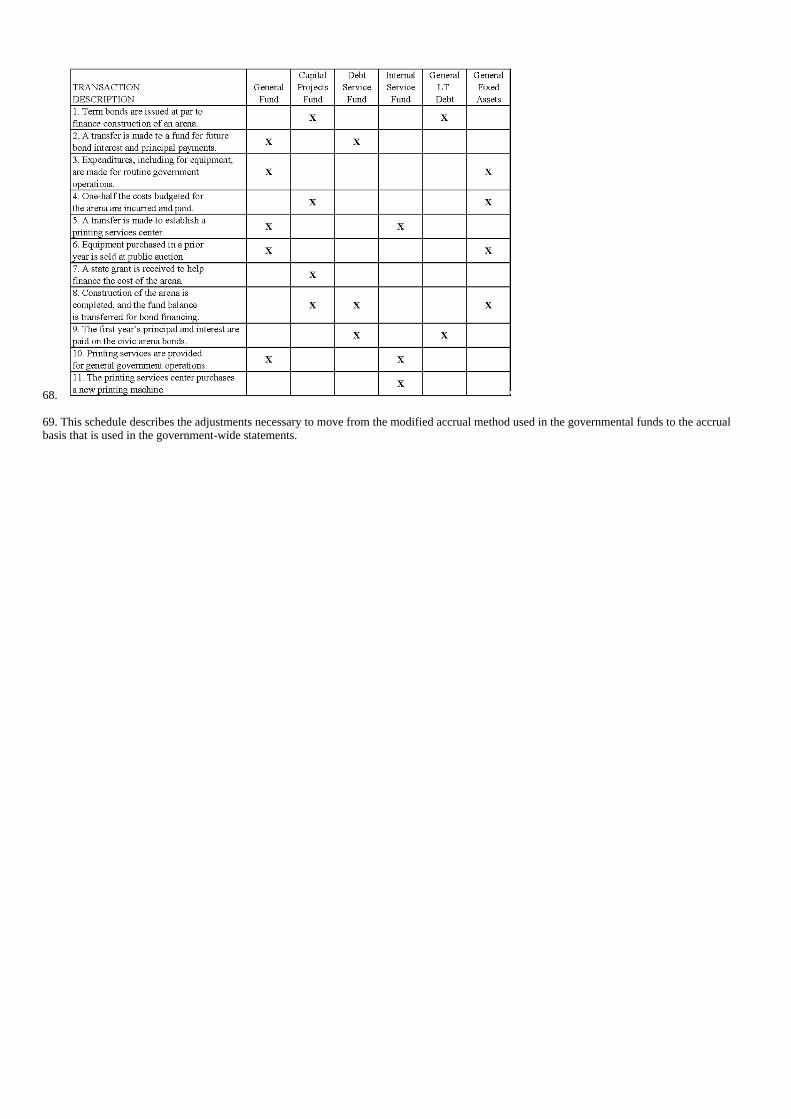

68. Required: For each transaction described below for the current fiscal year of the Town of Golden, use an "x" to indicate the fund(s) in which a journal entry should appear, and whether separate information should be kept for General Long Term Debt or General Fixed

Assets.

69. GASB 34 requires a Reconciliation schedule for the Statement of Net Assets. What does this schedule

document?

ch18 Key 1. D 2. C 3. C 4. A 5. D 6. A 7. B 8. D 9. D 10. A 11. B 12. C 13. B 14. A 15. C 16. B 17. A 18. A 19. D 20. C 21. B 22. C 23. B 24. A 25. A 26. B 27. A 28. B 29. A 30. A 31. A 32. C 33. C 34. C 35. D 36. C

37. A 38. D 39. A 40. B 41. B 42. B 43. C 44. D 45. D 46. B 47. B 48. B 49. A 50. B 51. D 52. A 53. B 54. C 55. B 56. B 57. C 58. B 59. D 60. A 61. B 62. C 63. D

b)

64. a)

*** both tests are met for expenditures** for example, assets of $100 < $150* for example, assets of $100 < $115Application of the 10 percent and 5 percent tests (must meet both of the percentage tests for at least one of the four financial statement items):

b. Total assets, liabilities, revenues, or expenditures/expenses of the individual governmental or enterprise fund are at least 5 percent of the total for all governmental and enterprise funds combined; in this case, the total is:

a. Total assets, liabilities, revenues, or expenditures/expenses of the individual governmental or enterprise fund are at least 10 percent of the governmental or enterprise category; in this case, the totals are:2) The following criteria apply to other governmental (includes Internal Service Fund) or enterprise funds:1) GASB 34 states that the General Fund is always a major fund.65. The major funds for reporting purposes are the General Fund, the Capital Projects Fund, the Internal Service Fund, and the Enterprise Fund—Hydro, determined as follows:

c)

b)

66. a) Journal entries for the year ended June 30, 20X9

67.

68. 69. This schedule describes the adjustments necessary to move from the modified accrual method used in the governmental funds to the accrual basis that is used in the government-wide statements.

ch18 Summary Category # of Questions

AACSB: Analytic 17

AACSB: Reflective Thinking 52

AICPA: FN Decision Making 55

AICPA: FN Measurement 12

AICPA: FN Reporting 2

Baker - Chapter 18 72

Bloom's: Apply 17

Bloom's: Remember 34

Bloom's: Understand 18

Difficulty: 1 Easy 29

Difficulty: 2 Medium 23

Difficulty: 3 Hard 17

Learning Objective: 18-01 Understand and explain the differences in financial reporting requirements of the different fund types. 7

Learning Objective: 18-02 Make calculations and record journal entries for capital projects funds. 15

Learning Objective: 18-03 Make calculations and record journal entries for debt service funds. 10

Learning Objective: 18-04 Make calculations and record journal entries for permanent funds. 2

Learning Objective: 18-05 Understand and explain how governmental funds are reported and rules for separate reporting as major funds.

4

Learning Objective: 18-06 Make calculations and record journal entries for enterprise funds. 6

Learning Objective: 18-07 Understand and explain the financial reporting of proprietary funds. 6

Learning Objective: 18-08 Make calculations and record journal entries for internal service funds. 5

Learning Objective: 18-09 Make calculations and record journal entries for trust funds. 4

Learning Objective: 18-10 Make calculations and record journal entries for agency funds. 3

Learning Objective: 18-11 Understand and explain the preparation of government-wide financial statements. 11

Learning Objective: 18-12 Understand and explain the additional disclosures that accompany government-wide financial statements.

4