chapter 17: accounting for corporate income · pdf filechapter 17: accounting for corporate...

TRANSCRIPT

1

Chapter 17: Accounting for corporate income taxes

MotivationTemporary and permanent differences

Deferred taxesA. Future taxable amounts and deferred taxes

B. Future deductible amounts and deferred taxes

Accounting for net operating losses

2

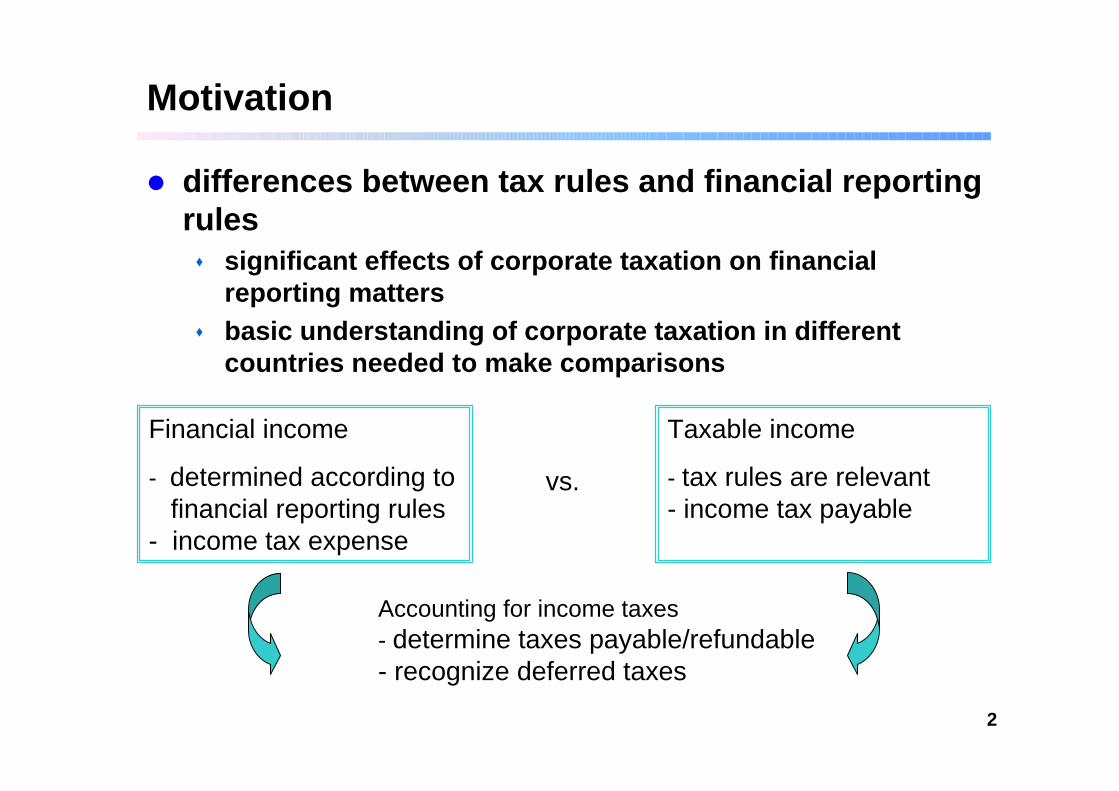

Motivation

� differences between tax rules and financial reporting rules� significant effects of corporate taxation on financia l

reporting matters� basic understanding of corporate taxation in differen t

countries needed to make comparisons

Financial income

- determined according tofinancial reporting rules

- income tax expense

Taxable income

- tax rules are relevant- income tax payable

vs.

Accounting for income taxes- determine taxes payable/refundable- recognize deferred taxes

3

Example

Big Orange Inc. - Tax reporting numbers

2000 2001 2002 2003 Total

Revenues € 250.000 € 250.000 € 320.000 € 280.000

Expenses 220.000 220.000 170.000 170.000

Taxable income € 30.000 € 30.000 € 150.000 € 110.000 € 320.000

Income tax payable (35%) € 10.500 € 10.500 € 52.500 € 38.500 € 112.000

Big Orange Inc. - Financial reporting numbers

2000 2001 2002 2003 Total

Revenues € 300.000 € 300.000 € 250.000 € 250.000 Expenses 220.000 220.000 170.000 170.000

Pretax financial income € 80.000 € 80.000 € 80.000 € 80.000 € 320.000

Income tax expense (35%) € 28.000 € 28.000 € 28.000 € 28.000 € 112.000

4

Differences between income tax expenses and income taxes payable usually offset each other over time:

� Offsetting property holds only if differences betwe enfinancial income and taxable income are temporary .

Comparison of income tax expenses and income taxes payable; Big Orange Inc.

2000 2001 2002 2003 Total

Income tax expense 28.000 28.000 28.000 28.000 112.000

Income taxes payable 10.500 10.500 52.500 38.500 112.000

Difference 17.500 17.500 -24.500 -10.500 0

5

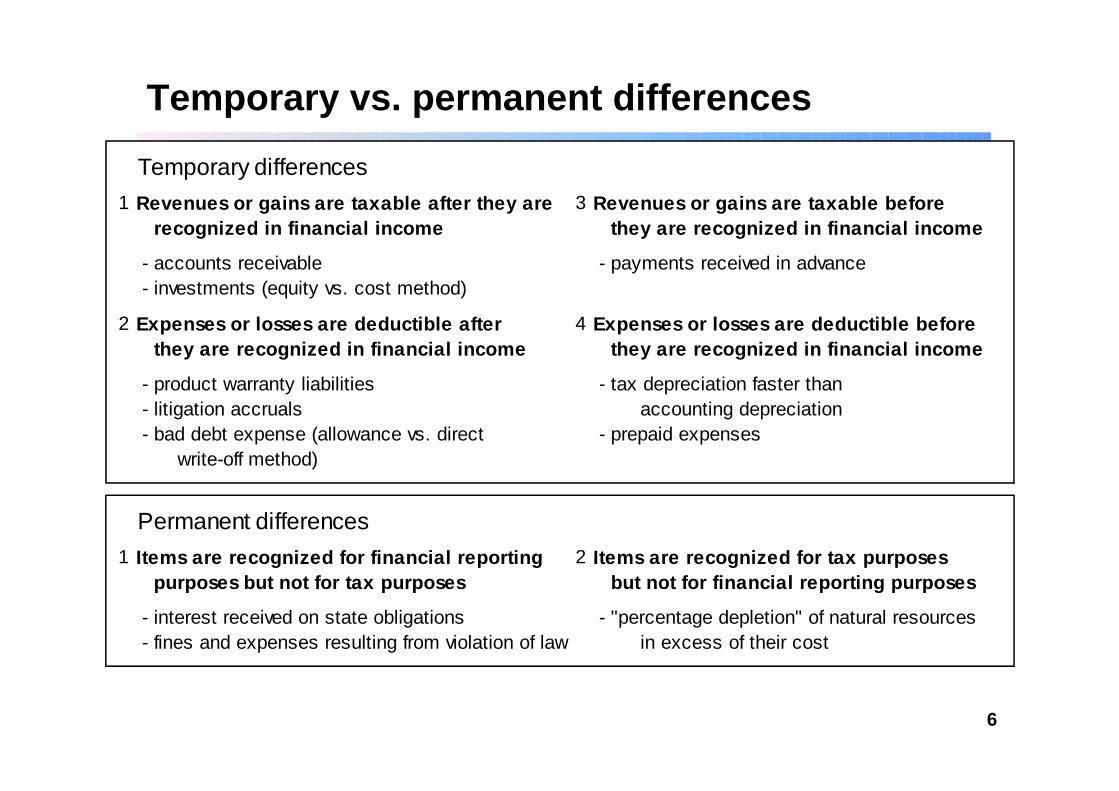

Temporary vs. permanent differences

� „difference“ between tax basis of an asset or liabili tyand its reported (carrying or book) amount in the financial statements� gives rise to differences between financial income an d

taxable income� differences can be temporary or permanent

� Temporary difference � difference is reversed over time� results in taxable amounts or deductible amounts� Taxable (deductible) amounts increase (decrease) futu re

taxable income

� Permanent difference� difference does not reverse over time; no deferred tax es

6

Temporary vs. permanent differences

Temporary differences

1 Revenues or gains are taxable after they are 3 Revenues or gains are taxable before recognized in financial income they are recogn ized in financial income

- accounts receivable - payments received in advance - investments (equity vs. cost method)

2 Expenses or losses are deductible after 4 Expenses or losses are deductible before they are recognized in financial income they a re recognized in financial income

- product warranty liabilities - tax depreciation faster than - litigation accruals accounting depreciation - bad debt expense (allowance vs. direct - prepaid expenses write-off method)

Permanent differences

1 Items are recognized for financial reporting 2 Items are recognized for tax purposes purposes but not for tax purposes but not for financial reporting purposes

- interest received on state obligations - "percentage depletion" of natural resources - fines and expenses resulting from violation of law in excess of their cost

7

Deferred Taxes

� result from temporary differences between book basis and tax basis of an asset or liability

� accounting for deferred tax is the recognition of thetax implied by the valuation of the assets and liabilities included in the balance sheet� it‘s not amounts of tax bills that the tax authorities have

allowed the taxpayer to postpone or have asked for in advance

8

Asset Liability Asset Liability

tax value tax value tax value tax value> < < >

carrying carrying carrying carryingamount amount amount amount

Example: Accounts Certain Plant and Certainreceivable, net accruals and equipment, long-termof allowance provisions net liabilities

Deductible Taxabletemporary differences temporary differences

Deferred tax asset Deferred tax liabilitiy

9

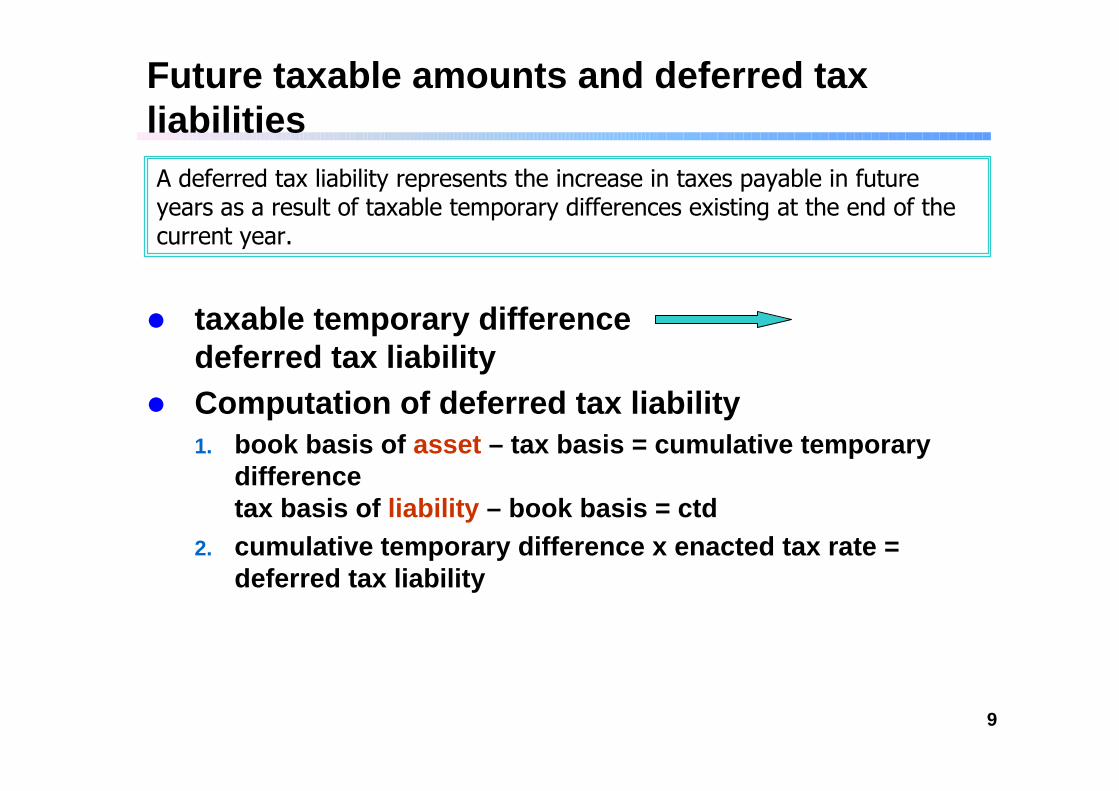

Future taxable amounts and deferred tax liabilities

� taxable temporary differencedeferred tax liability

� Computation of deferred tax liability1. book basis of asset – tax basis = cumulative temporary

differencetax basis of liability – book basis = ctd

2. cumulative temporary difference x enacted tax rate = deferred tax liability

A deferred tax liability represents the increase in taxes payable in future years as a result of taxable temporary differences existing at the end of the current year.

10

Computation of income tax expenses

� two components of income tax expense� Current tax expense (income tax payable for the period )� Deferred tax expense (increase in the deferred tax liab ility account)

� example: Sutton, p. 558, problem 17.2

Total income tax expense Income tax payable Change in (benefit) (refundable) deferred income taxes

= +

Note, if permanent differences exist, we make a mistake if we want to deter-mine income tax expenses simply by applying the enacted tax rate to pretax financial income.

Example for permanent difference: (Tax rate 40%)

Financial income taxable income

Revenues 100 100

Gen. Expenses 50 50

Fines 10 --

40 50

Income tax 20

11

B. Future deductible amounts and deferredtax assets

� deductible temporary differencedeferred tax asset

� Computation of deferred tax asset1. book basis of liability – tax basis = cumulative temporary

difference ORtax basis of asset – book basis = cumulative temporary difference

2. cumulative temporary difference × enacted tax rate = deferred tax asset

A deferred tax asset represents the increase in taxes refundable (or saved) in future years as a result of deductible temporary differences existing at theend of the current year.

12

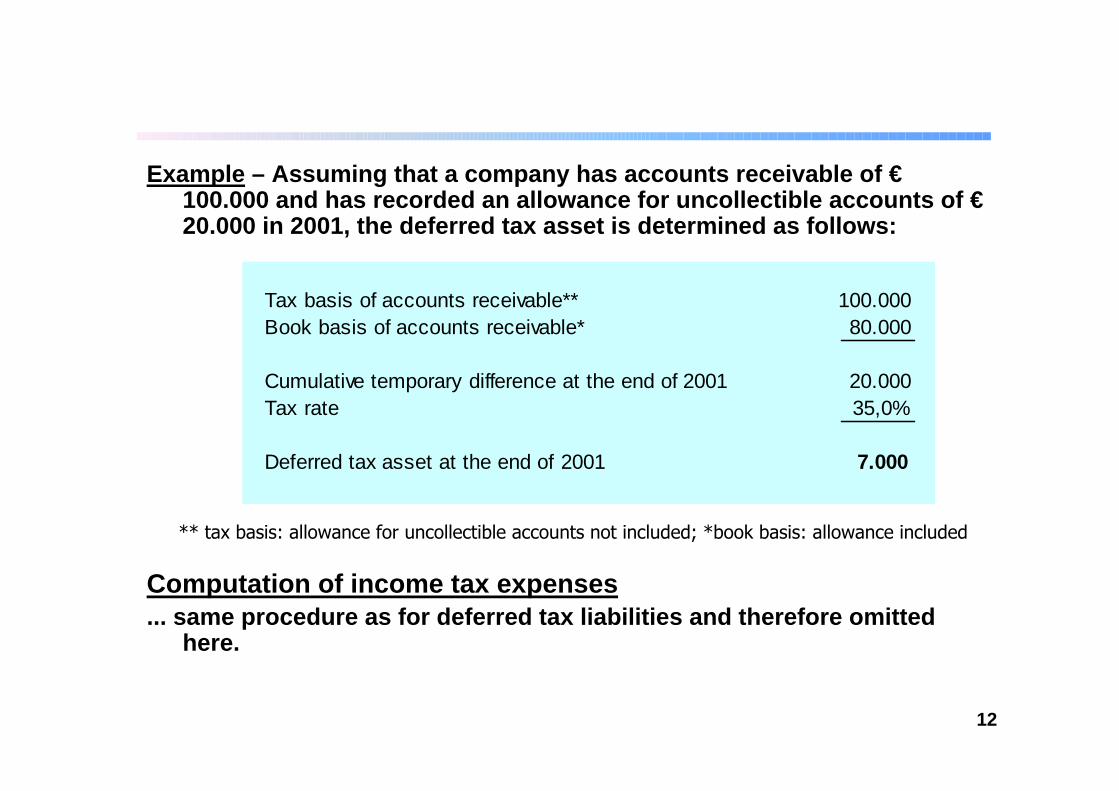

Example – Assuming that a company has accounts receivable of € 100.000 and has recorded an allowance for uncollecti ble accounts of € 20.000 in 2001, the deferred tax asset is determined as follows:

Computation of income tax expenses... same procedure as for deferred tax liabilities and therefore omitted

here.

Tax basis of accounts receivable** 100.000Book basis of accounts receivable* 80.000

Cumulative temporary difference at the end of 2001 20.000Tax rate 35,0%

Deferred tax asset at the end of 2001 7.000

** tax basis: allowance for uncollectible accounts not included; *book basis: allowance included

13

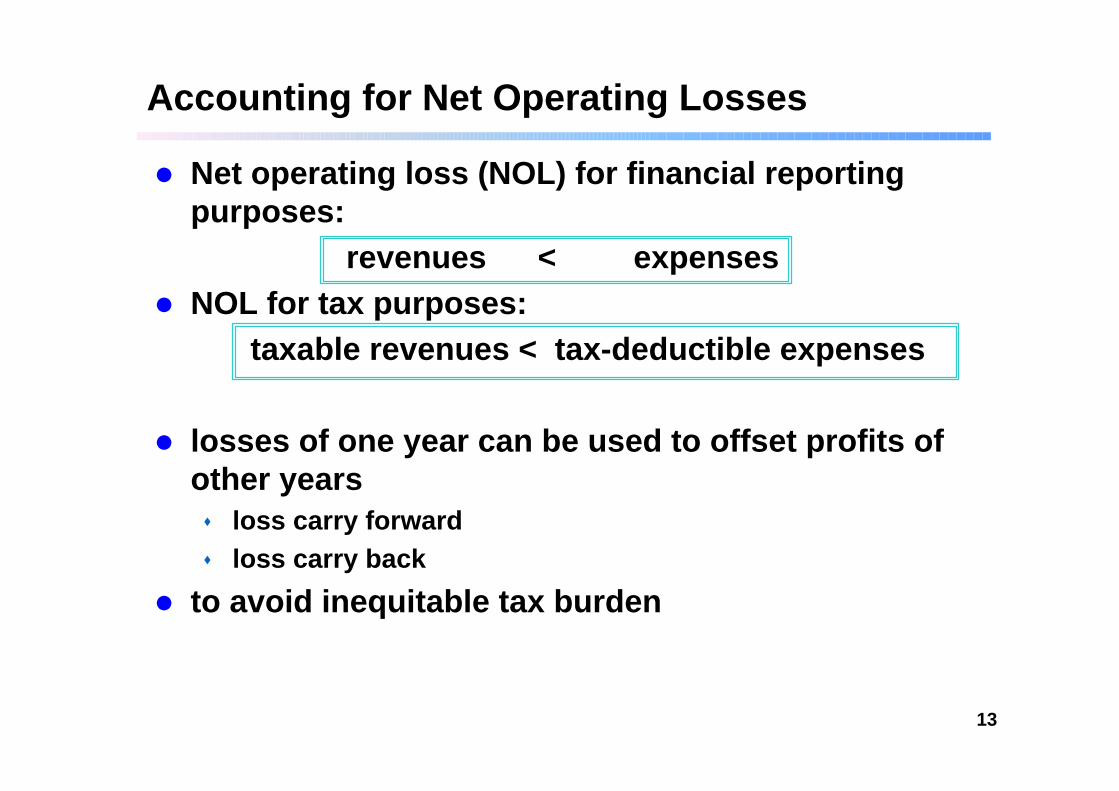

Accounting for Net Operating Losses

� Net operating loss (NOL) for financial reporting purposes:

revenues < expenses� NOL for tax purposes:

taxable revenues < tax-deductible expenses

� losses of one year can be used to offset profits of other years� loss carry forward� loss carry back

� to avoid inequitable tax burden

14

Loss Carryback and Loss Carryforward

� Loss carryback� NOL is carried back two years [US-GAAP] ���� tax refund

• loss is applied to earlier year first and then to the second year

� remaining losses may be carried forward

� Loss carryforward� losses had been recorded in previous two years ���� no loss

carryback, just loss carryforward

Net Operating Loss

Loss carryback Loss carryforward 2 years back 20 years forward

2000 2002 2003 2004 2005 20222001

15

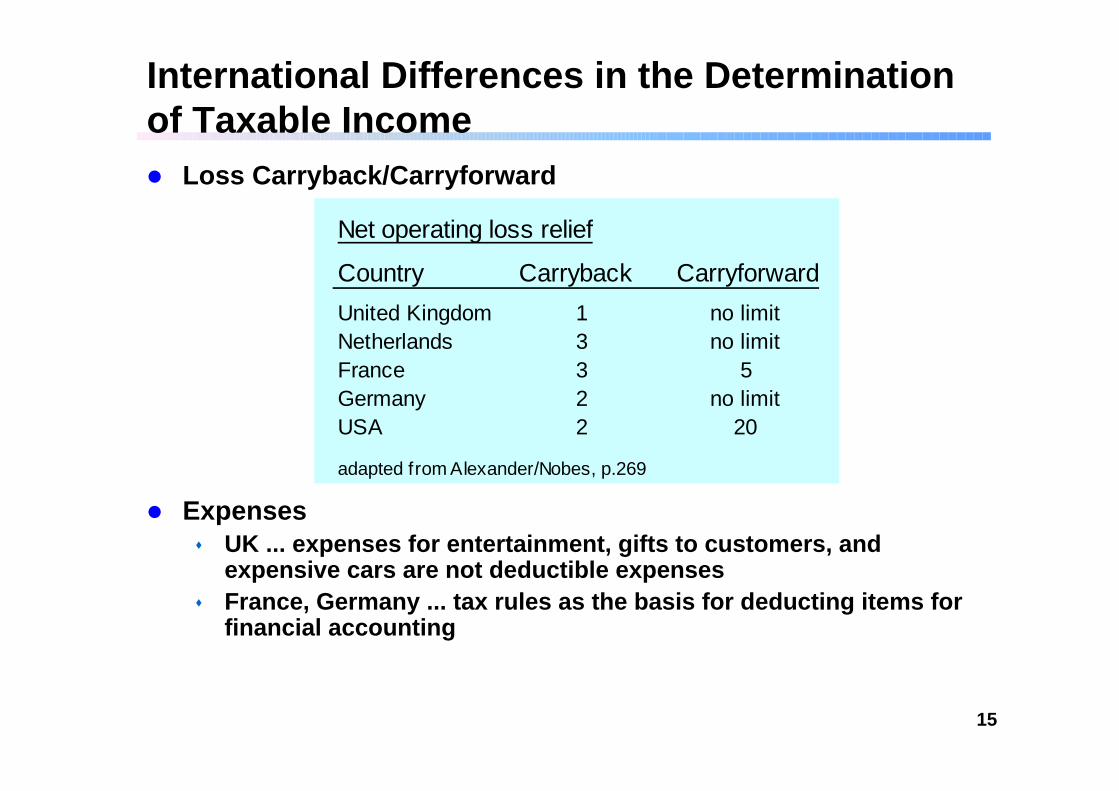

International Differences in the Determination of Taxable Income� Loss Carryback/Carryforward

� Expenses� UK ... expenses for entertainment, gifts to customer s, and

expensive cars are not deductible expenses� France, Germany ... tax rules as the basis for deduct ing items for

financial accounting

Net operating loss relief

Country Carryback Carryforward

United Kingdom 1 no limitNetherlands 3 no limitFrance 3 5Germany 2 no limitUSA 2 20

adapted from Alexander/Nobes, p.269