chapter 11 depreciation, impairments, and depletion acct-30301

TRANSCRIPT

Chapter 11

Depreciation, Impairments, and Depletion

ACCT-3030 1

1. Theory of DepreciationDefinition

◦ the systematic and rational allocation of the cost of a fixed asset

Depreciation is an allocation method – not a valuation method

Justification◦matching◦fluctuations in market value too difficult

to determineACCT-3030 2

2. Depreciation FactorsCost – covered in Chapter 10Salvage value – estimatedUseful life

◦useful life vs. physical life◦ functional factors

changes in environment, asset inadequate for intended purpose, obsolescence, supersession

◦physical factors routine wear and tear, deterioration, effects of

continual usage, etc.ACCT-3030 3

3. Selecting Appropriate MethodFactors

◦expected use, expected obsolescence, expected pattern of decline in usefulness of asset, expected contribution of asset to revenue, etc.

Conceptually◦method that most clearly reflects net income

Practically◦method that minimizes bookkeeping expenses◦method that reports highest net income

ConsistencyACCT-3030 4

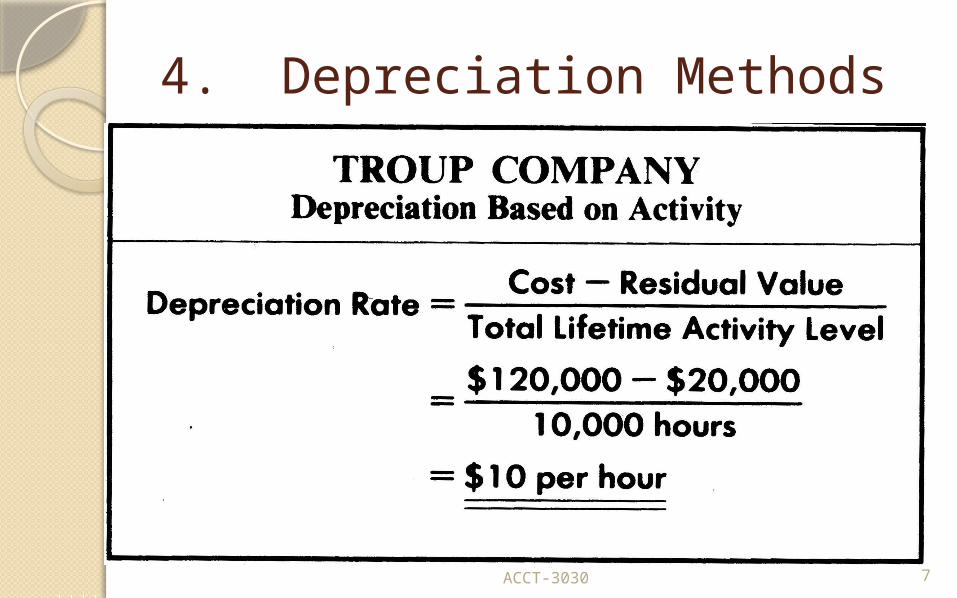

4. Depreciation MethodsActivity method

◦can be based on output (e.g., units produced)

◦can be based on inputs (e.g., operating hours or miles)

Depr = Cost – Salvage x Productive ServiceExp Life in Units

ACCT-3030 5

4. Depreciation Methods

ACCT-3030 6

4. Depreciation Methods

ACCT-3030 7

4. Depreciation MethodsStraight Line

◦most commonly used method◦easy to use

ACCT-3030 8

4. Depreciation Methods

ACCT-3030 9

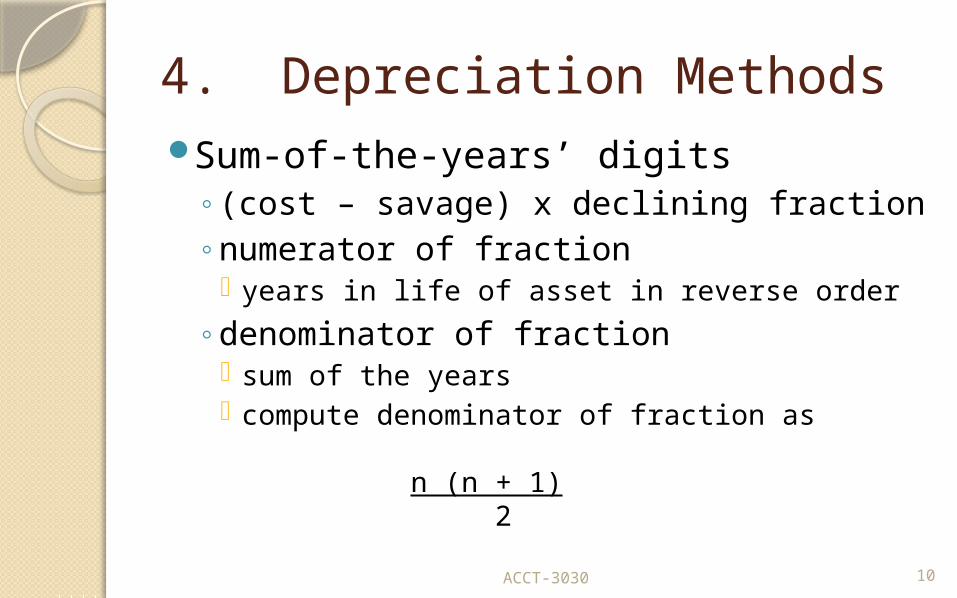

4. Depreciation MethodsSum-of-the-years’ digits

◦(cost – savage) x declining fraction◦numerator of fraction

years in life of asset in reverse order

◦denominator of fraction sum of the years compute denominator of fraction as

n (n + 1) 2

ACCT-3030 10

4. Depreciation Methods

ACCT-3030 11

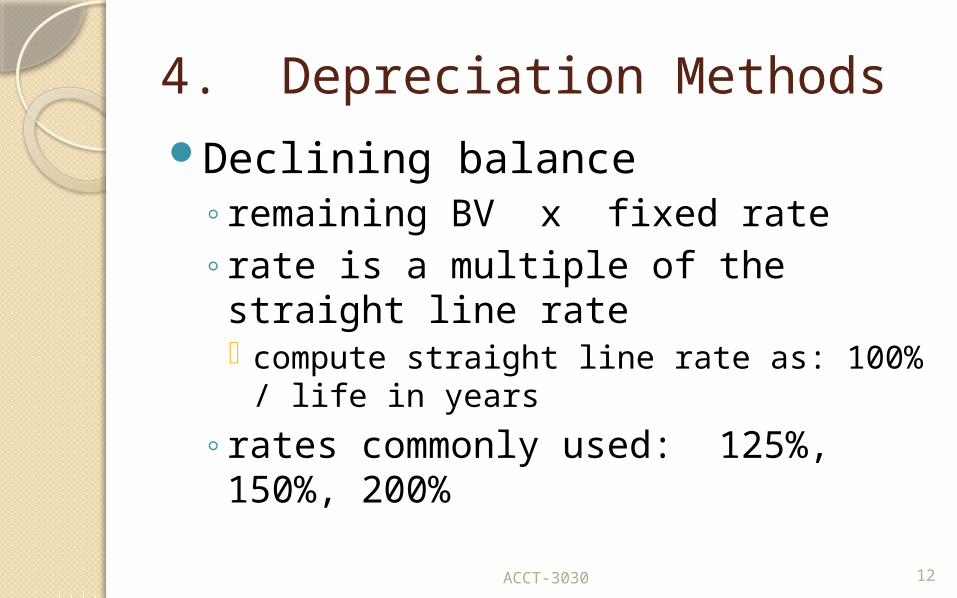

4. Depreciation MethodsDeclining balance

◦remaining BV x fixed rate◦rate is a multiple of the straight line

rate compute straight line rate as: 100% / life

in years

◦rates commonly used: 125%, 150%, 200%

ACCT-3030 12

4. Depreciation Methods

ACCT-3030 13

4. Depreciation Methods Group and Composite methods

◦ assets grouped by common characteristics

◦ average depreciation rate used as if a single unit

◦ depreciation expense = group cost x average rate

Composite◦ refers to collection of dissimilar assets

Group◦ refers to collection of similar assets

Use straight line depreciation method No gain or loss recorded on disposals until entire group

disposed of◦ debit accumulated depreciation for difference between asset’s cost

and the proceeds

Example BE 11-6 ACCT-3030 14

4. Depreciation Methods

ACCT-3030 15

BRIEF EXERCISE 11-6

Asset Depreciation Expense A ($70,000 – $7,000) / 10 = $ 6,300 B ($50,000 – $5,000) / 5 = 9,000 C ($82,000 – $4,000) / 12 = 6,500 $202,000 $16,000 $21,800

Composite rate = $21,800/$202,000 = 10.8%

Composite life = ($202,000 – 16,000) / $21,800 = 8.53 years

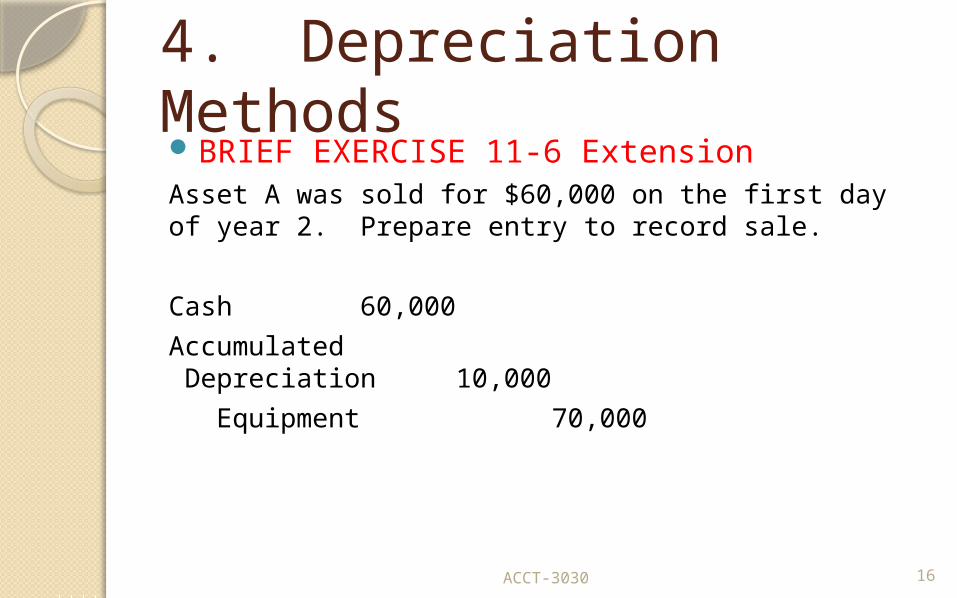

4. Depreciation MethodsBRIEF EXERCISE 11-6 ExtensionAsset A was sold for $60,000 on the first day of year 2. Prepare entry to record sale.

Cash 60,000

Accumulated Depreciation 10,000

Equipment 70,000

ACCT-3030 16

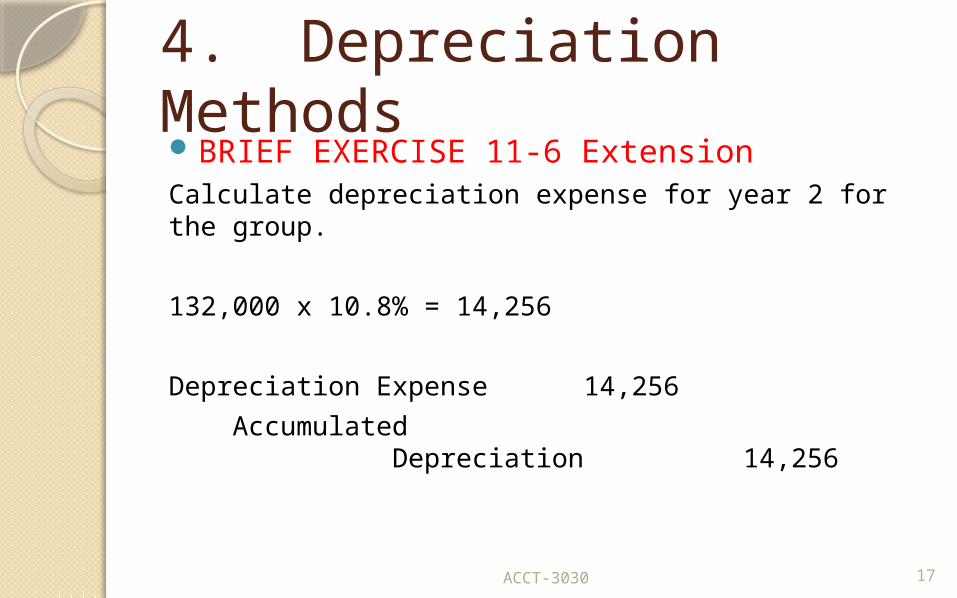

4. Depreciation MethodsBRIEF EXERCISE 11-6 ExtensionCalculate depreciation expense for year 2 for the group.

132,000 x 10.8% = 14,256

Depreciation Expense 14,256

Accumulated Depreciation 14,256

ACCT-3030 17

4. Depreciation MethodsOther methods Inventory method

◦ sometimes used for large numbers of low cost assetsRetirement and Replacement methods

◦ sometimes used if have large number of similar assets replaced on constant schedule

◦ Retirement method FIFO approach

◦ Replacement method LIFO approach

ExamplesACCT-3030 18

4. Depreciation MethodsPartial years

◦ conventions – must be used consistently half year in first and last year full year in first year and none in last year none in first year and full year in last year nearest month

◦ SYD prorate 12-month blocks of depreciation between years

◦ DB use partial year fraction in first year only

◦ ExampleACCT-3030 19

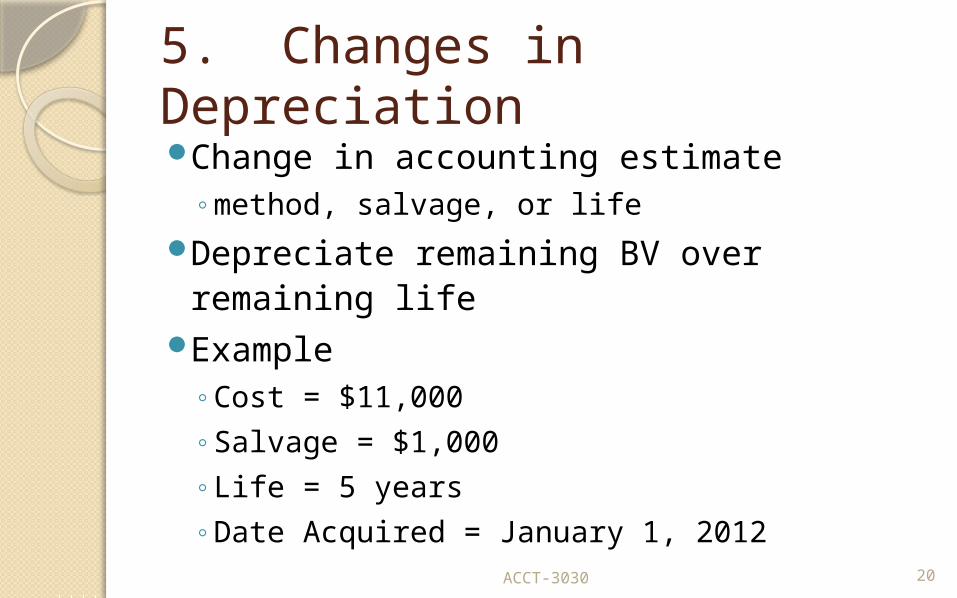

5. Changes in DepreciationChange in accounting estimate

◦method, salvage, or lifeDepreciate remaining BV over remaining

lifeExample

◦Cost = $11,000

◦Salvage = $1,000

◦Life = 5 years

◦Date Acquired = January 1, 2012ACCT-3030 20

5. Changes in DepreciationSL depreciation: 11,000 – 1,000 / 5

= 2,000During 2015, changed life from 5

years to 7New depreciation used for 2015 and

forward

ACCT-3030 21

BV on 1/1/2015

Cost $ 11,000

Accum Depr (2000 x 3) $ 6,000

BV $ 5,000

New Depreciation Amount

5,000 - 1000 / 4 = 1,000

6. Depletion Depreciable assets retain their physical characteristics

as used Natural resources (coal, gas, oil) are used up

◦ as natural resources used up cost of natural resources allocated to units extracted

Use the units-of-production method◦ determine depletion base (acquisition cost, development

cost, carrying cost)

◦ estimate recoverable units

◦ calculate depletion rate:

Cost of Natural Resource – Residual Value Estimated Recoverable Units

ACCT-3030 22

6. Depletion

Example◦ABC Mining acquired a tract of land

containing ore deposits. Total costs of acquisition and development were $1,100,000. ABC estimated the land contained 40,000 tons of ore, and that the land will be sold for $100,000 after the coal is mined. What is ABC’s depletion rate?

ACCT-3030 23

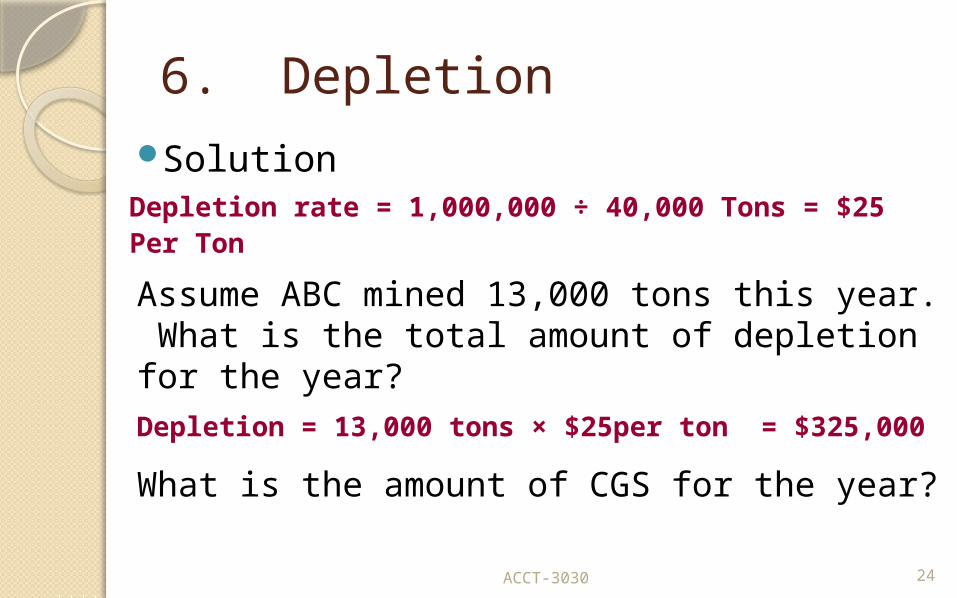

6. DepletionSolutionDepletion rate = 1,000,000 ÷ 40,000 Tons = $25 Per Ton

Assume ABC mined 13,000 tons this year. What is the total amount of depletion for the year?Depletion = 13,000 tons × $25per ton = $325,000

What is the amount of CGS for the year?ACCT-3030 24

7. ImpairmentsAn impairment occurs when

expected future net cash flows (undiscounted) of an asset are less than the asset’s carrying amount

ACCT-3030 25

7. ImpairmentsTest for impairment

◦ review events for possible impairment◦apply recoverability test to determine if

impairment has occurred impairment occurs if sum of expected future net cash

flows (undiscounted) is less than asset’s carrying amount

◦ if impairment has occurred recognize impairment loss for amount by which the

carrying amount of the asset exceeds fair value of asset fair value is market price if active market exists if no market, use present value of expected future net cash flows

ACCT-3030 26

7. Impairments◦ if impaired asset is held for use

new cost basis of asset is the reduced carrying amount

depreciation is taken on new cost basis over asset’s remaining useful life

write-ups of asset’s value are not allowed

◦ if impaired asset is intended to be disposed of reported at the lower-of cost-or-net realizable value recovery of impairment loss is allowed but write-up

cannot exceed carrying amount of asset before impairment

ACCT-3030 27

7. Impairments

ACCT-3030 28