chapter 11 business combinations. financial information analysis2 copyright 2006 john wiley &...

TRANSCRIPT

Chapter 11

Business Combinations

Financial Information Analysis 2Copyright 2006 John Wiley & Sons Ltd

Business Combinations (Groups)

• Most large UK plc’s are Groups• i.e., companies combined together in

various ways and forms• Anglo-American governance culture

favours this means of ‘growth’• Usually achieved by:

• Acquisition, or• Merger

• IAS 27; IFRS 3

Financial Information Analysis 3Copyright 2006 John Wiley & Sons Ltd

Acquisition

• Company buys shares in another directly or indirectly

• This gives in “an interest”• If it acquires a controlling interest then

this creates parent/subsidiary relationship

• A company is a parent of another if it:• holds a majority of voting rights, or• has right to appoint majority of board, or• governs its financial and reporting

policies, or• can cast majority of votes at board

meeting

Financial Information Analysis 4Copyright 2006 John Wiley & Sons Ltd

Company Relationships

C om pany A100%

Suffic ient fo r controlW holly-ow ned

C om pany B51%

Suffic ient fo r controlPartly-ow ned

C om pany C49%

C ontro l?If 'Yes ' = Partly-ow ned

C om pany D25%

Significant In fluenceAssocia te

Parent companyVarious investm ents in other com panies

Relationship depends on criteria for Control

Financial Information Analysis 5Copyright 2006 John Wiley & Sons Ltd

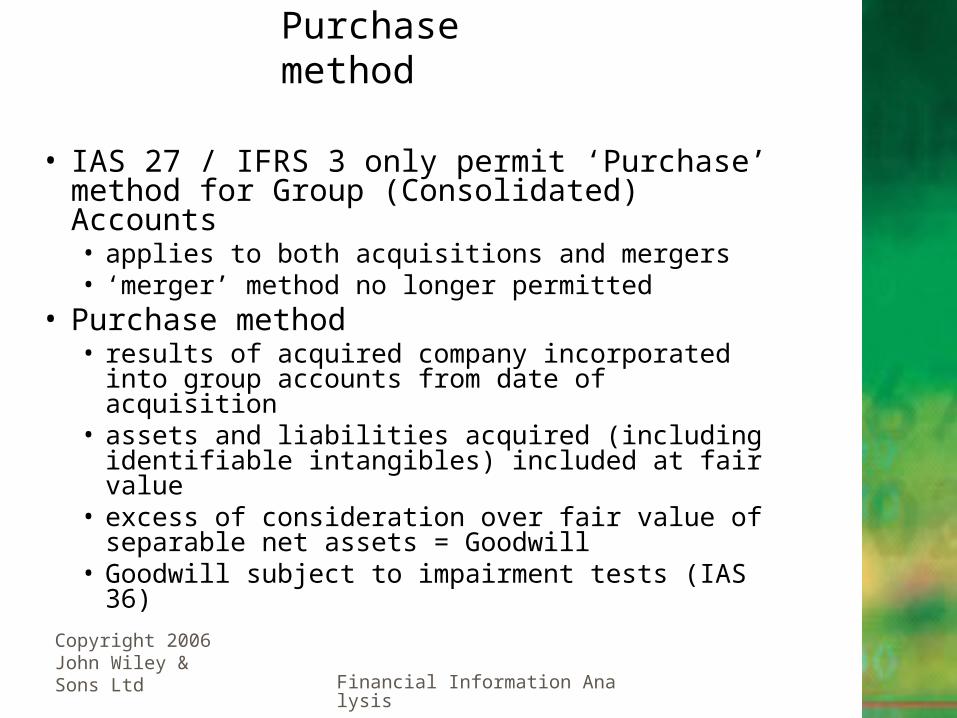

Purchase method

• IAS 27 / IFRS 3 only permit ‘Purchase’ method for Group (Consolidated) Accounts• applies to both acquisitions and mergers• ‘merger’ method no longer permitted

• Purchase method• results of acquired company incorporated into

group accounts from date of acquisition• assets and liabilities acquired (including identifiable

intangibles) included at fair value• excess of consideration over fair value of separable

net assets = Goodwill• Goodwill subject to impairment tests (IAS 36)

Financial Information Analysis 6Copyright 2006 John Wiley & Sons Ltd

Purchase method ctd.

• 2 basic principles• 1. Amalgamate

• e.g., where P and S have Fixed Assets of £150k and £100k, Group a/cs will show £250k

• 2. Cancel out corresponding items• e.g., where P shows ‘Investment in S’ of £200k

and S shows Share Capital of £200k they cancel each other

Financial Information Analysis 7Copyright 2006 John Wiley & Sons Ltd

Purchase Method ctd.

• Group Balance Sheet: • amalgamate those of parent and subsidiaries• partly-owned subsidiary: un-cancelled Share

Capital in subsidiary = Minority Interest • Revenue Reserves in subsidiary at date of

acquisition cannot be distributed• Goodwill = excess of consideration over fair

values of separable net assets

Financial Information Analysis 8Copyright 2006 John Wiley & Sons Ltd

Purchase method ctd.

• Group Income Statement: • amalgamate those of parent and subsidiaries• Minority Interest’s share of profits must be

indicated• inter-company dividends will cancel• unrealised profits on inter-company trading

must be eliminated

Financial Information Analysis 9Copyright 2006 John Wiley & Sons Ltd

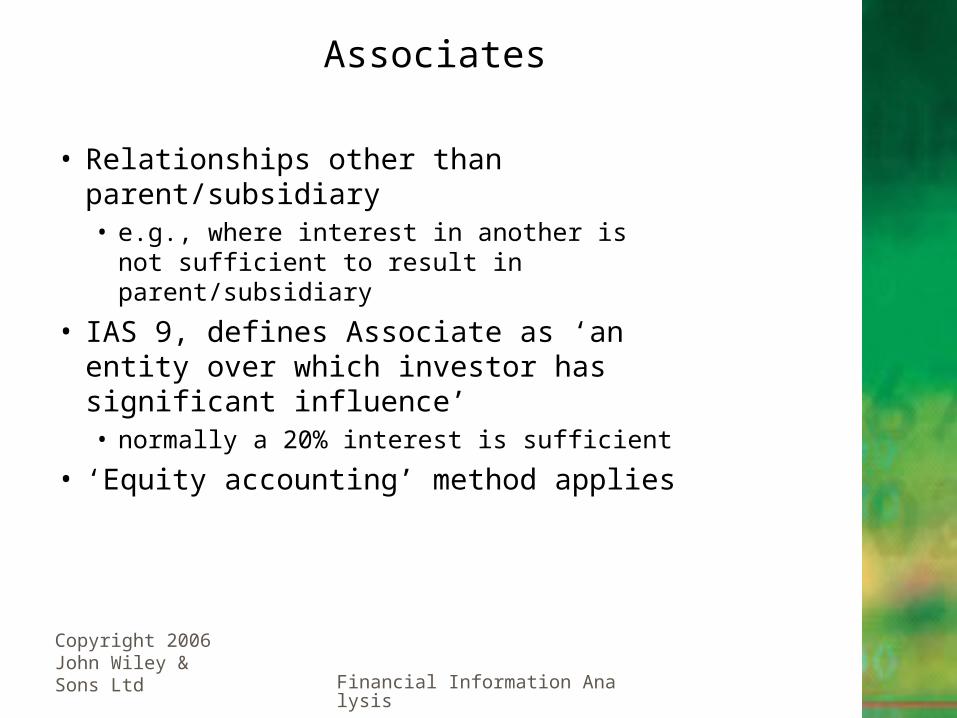

Associates

• Relationships other than parent/subsidiary• e.g., where interest in another is not

sufficient to result in parent/subsidiary

• IAS 9, defines Associate as ‘an entity over which investor has significant influence’• normally a 20% interest is sufficient

• ‘Equity accounting’ method applies

Financial Information Analysis 10Copyright 2006 John Wiley & Sons Ltd

Equity Accounting method

• Investor must reflect relationship with Associate in own accounts

• Equity accounting method:• investment shown as non-current asset • goodwill identified and grouped with

other goodwill• carrying amount adjusted annually for

gains, losses• share of associate’s profits included in IS• CFS shows flows between investor and

investee

Financial Information Analysis 11Copyright 2006 John Wiley & Sons Ltd

Joint Ventures

• Companies often join together to carry out projects, contracts, etc.

• IAS 31: ‘contractual arrangement whereby entities undertake economic activity subject to joint control’• e.g.: collaborative manufacture of aircraft

• IAS 31 allows Equity Accounting or Proportionate Consolidation methods

• Favours latter because results in line for line incorporation into group accounts

Financial Information Analysis 12Copyright 2006 John Wiley & Sons Ltd

Related-Party Transactions

• Not all transactions at ‘arms-length’• e.g., company granting loan to a

director

• Such ‘related party’ transactions require disclosure

Financial Information Analysis 13Copyright 2006 John Wiley & Sons Ltd

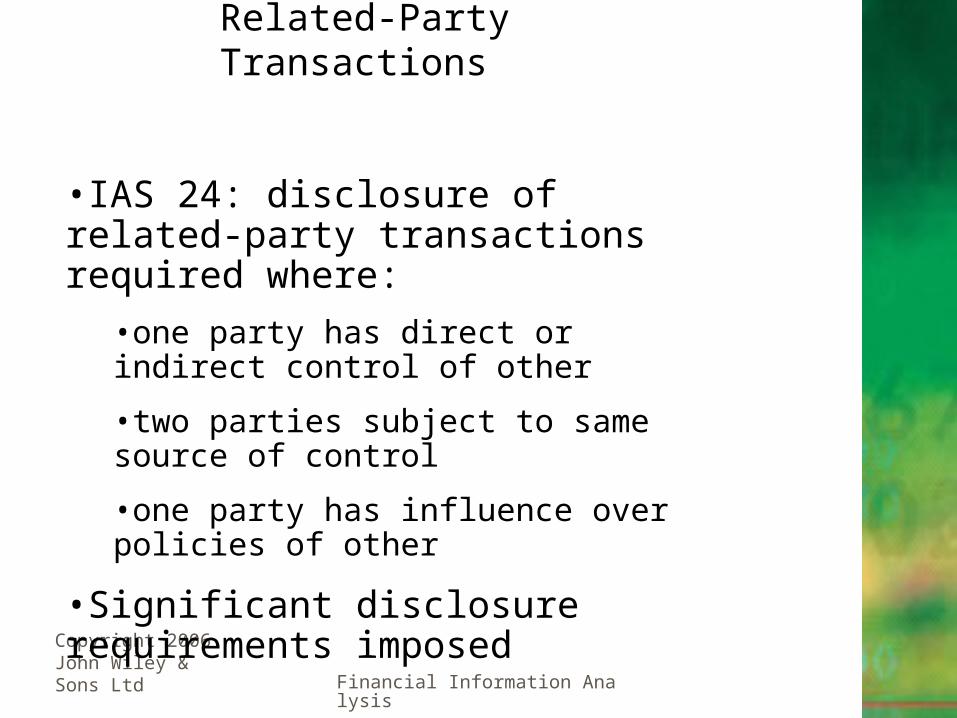

•IAS 24: disclosure of related-party transactions required where:

•one party has direct or indirect control of other

•two parties subject to same source of control

•one party has influence over policies of other

•Significant disclosure requirements imposed

Related-Party Transactions

Financial Information Analysis 14Copyright 2006 John Wiley & Sons Ltd

Summary

• Various forms of business combination exist• Relationship usually depends on nature of

investment• parent/wholly-owned subsidiary

• parent/partly-owned subsidiary

• investor/associate

• joint venture

• Accounting method used depends on nature of relationship