chapter 10 - capital budgeting. capital budgeting a major part of the financial management of the...

TRANSCRIPT

Chapter 10 - Capital Budgeting

Capital BudgetingA major part of the financial management of the firm

Kinds Of Spending In BusinessShort term - to support day to day operations

Long term - to support long lived equipment and projects

Long term money and the things acquired with it are both called capital

Capital BudgetingPlanning and Justifying How Capital Dollars Are Spent On Long

Term ProjectsProvides methods for evaluating whether projects make financial sense and for choosing among them

Capital Budgeting

Capital budgeting involves planning and justifying large expenditures on long-term projects– Projects can be classified as:

Replacement – low risk

Expansion – moderate risk

New venture – high risk

3

Characteristics of Business Projects

Project Types and Risk– Capital projects have increasing risk according to

whether they are replacements, expansions or new ventures

Stand-Alone and Mutually Exclusive Projects– Stand-alone project has no competing alternatives– Mutually exclusive projects involve selecting one

project from among two or more alternatives

4

Characteristics of Business Projects

Project Cash Flows– Reduce projects to a series of cash flows:

C0 $(50,000)

C1 (10,000)

C2 15,000

C3 15,000

C4 15,000

C5 5,000

– Business projects: early cash outflows and later inflows

– C0 is the Initial Outlay and usually required to get started

5

Characteristics of Business Projects

The Cost of Capital– The average rate a firm pays investors for

use of its long term moneyFirms raise money from two sources: debt and equity

6

Capital Budgeting Techniques

Payback Period– How many years to recover initial cost

Net Present Value – Present value of inflows less outflows

Internal Rate of Return – Project’s return on investment

Profitability Index – Ratio of present value of inflows to outflows

7

Capital Budgeting TechniquesPayback

Payback period is the time it takes to recover early cash outflows– Shorter paybacks are better

Payback Decision Rules– Stand-alone projects– Mutually Exclusive Projects

Weaknesses of the Payback Method– Ignores time value of money– Ignores cash flows after payback period

8

Concept Connection Example 10-1 Payback Period

9

Payback period is easily visualized by the cumulative cash flows

Example 10-2: Weakness of the Payback Technique

10

Use the payback period technique to choose between mutually exclusive projects A and B.

Project A’s payback is 3 years as its initial outlay is fully recovered in that time. Project B doesn’t fully recover until sometime in the 4th year. Thus, according to the payback method, Project A is better than B. But project B is clearly better because of the large inflows in the last two years

NET PRESENT VALUE (NPV)The present value of future cash flows is what counts

when making decisions based on value.

The Net Present Value of all of a project's cash flows is its expected contribution

to the firm's value and shareholder wealth

PVs are taken at k, the cost of capital

Calculate NPV usingNPV = C0 + C1[PVFk,1] + C2[PVFk,2] + · · · + Cn[PVFk,n]

Outflows are Ci with negative values and tend to occur first

NPV: Difference between the present values of positives and negativesProjects with positive NPVs increase the firm’s value

Projects with negative NPVs decrease the firm’s value

nn

221

)k1(

C...

)k1(

C

)k1(

C

0C =NPV

Net Present Value (NPV)

NPV and Shareholder Wealth– A project’s NPV is the net effect that it is

expected to have on the firm’s value

– To maximize shareholder wealth, select the capital spending program with the highest NPV

12

Net Present Value (NPV)

Decision Rules

– Stand-alone ProjectsNPV > 0 accept

NPV < 0 reject

– Mutually Exclusive ProjectsNPVA > NPVB choose Project A over B

13

Concept Connection Example 10-3 Net Present Value (NPV)

14

Project Alpha has the following cash flows. If the firm considering Alpha has a cost of capital of 12%, should the project be undertaken?

Concept Connection Example 10-3 Net Present Value (NPV)

15

The NPV is found by summing the present value of the cash flows when discounted at the firm’s cost of capital.

Since Alpha’s NPV<0, it should

not be undertaken.

)30.377($

70.622,4$000,5$

40.2135$40.594,1$90.829$000,5$

)7118(.000,3$)7972(.000,2$)8929(.000,1$000,5$

000,5312.1

000,3212.1

000,2)12.1(

000,1

1

AlphaNPV

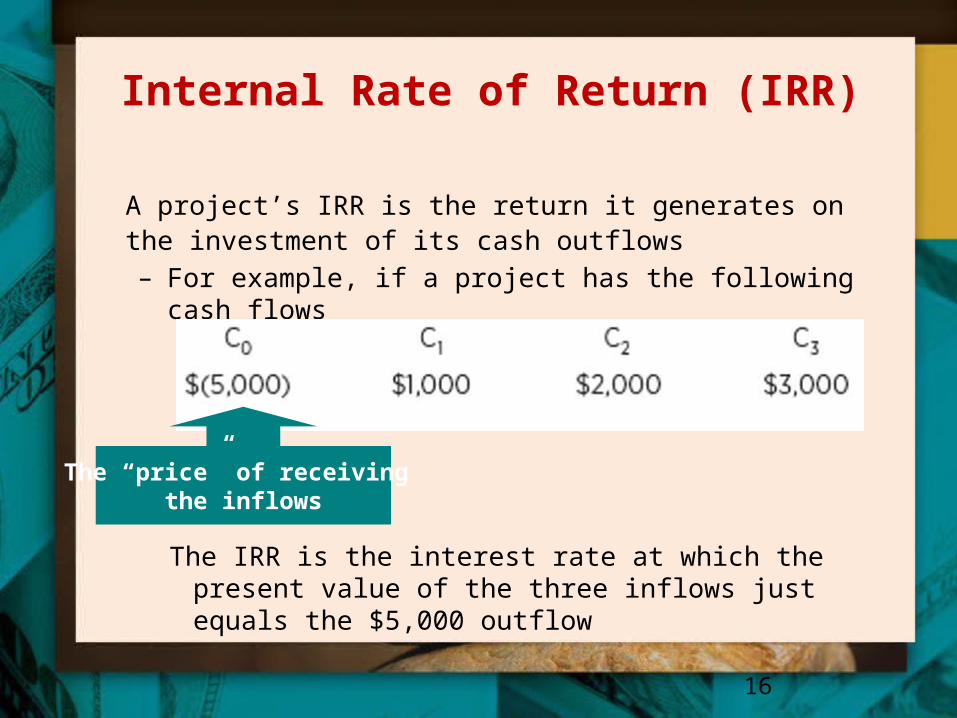

Internal Rate of Return (IRR)

A project’s IRR is the return it generates on the investment of its cash outflows– For example, if a project has the following cash flows

16

The IRR is the interest rate at which the present value of the three inflows just equals the $5,000 outflow

The “price” of receiving the inflows

Defining IRR Through the NPV Equation

At the IRR the PVs of project inflows and

outflows are equal, so NPV = 0

Set NPV=0 and substitute IRR for k

0 = C0 + C1[PVFIRR,1] + C2[PVFIRR,2] + · · + Cn[PVFIRR,n]

IRR is the solution to this equation for a given set of Ci

Requires an iterative approach if the Ci are irregular

0 = C0

C

IRR

C

IRR

C

IRR

nn

1 221 1 1( ) ( )

...( )

nn

221

)k1(

C...

)k1(

C

)k1(

C

0C =NPV

Internal Rate of Return (IRR)

Decision Rules

– Stand-alone ProjectsIf IRR > cost of capital (k) accept

If IRR < cost of capital (k) reject

– Mutually Exclusive ProjectsIRRA > IRRB choose Project A over Project B

18

Internal Rate of Return (IRR)

Calculating IRRs– Finding IRRs usually requires an iterative,

trial-and-error techniqueGuess at the project’s IRR

Calculate the project’s NPV using this interest rate

– If NPV = zero, guessed interest rate is the project’s IRR

– If NPV > 0, try a higher interest rate– If NPV < 0, try a lower interest rate

19

Concept Connection Example 10-5IRR – Iterative Procedure

20

Find the IRR for the following series of cash flows:

If the firm’s cost of capital is 8%, is the project a good idea? What if the cost of capital is 10%?

Example 10-5 IRR – Iterative Procedure

21

Start by guessing IRR = 12% and calculate NPV.

NPV = C0 + C1[PVFk,1] + C2[PVFk,2] + · · · + Cn[PVFk,n] NPV = -5,000 + 1,000[PVF12,1] + 2,000[PVF12,2] + 3,000[PVF12,3] NPV = -5,000 + 1,000[.8929] + 2,000[.7972] + 3,000[.7118] NPV = -5,000 + 892.90 + 1,594.4 + 2,135.40 NPV = -$377.30

Since NPV<0, the project’s IRR must be < 12%.

Figure 10-1 NPV Profile

22

A project’s NPV profile is a graph of its NPV vs. the cost of capital. It crosses the horizontal axis at the IRR.

Concept Connection Example 10-5 IRR – Iterative Procedure

23

We’ll try a different, lower interest rate, say 10%. At 10%, the project’s NPV is ($184). Since the NPV is still less than zero, we need to try a still lower interest rate, say 9%. The following table lists the project’s NPV at different interest rates.

Since NPV becomes positive somewhere between 8% and 9%, the project’s IRR must be between 8% and 9%. If the

firm’s cost of capital is 8%, the project is marginal. If the

firm’s cost of capital is 10%, the project is not a good idea.

$1307

$228

($83)9

($184)10

($377)12%

Calculated NPV

Interest Rate Guess

Techniques: Internal Rate of Return (IRR)

Technical Problems with IRR– Multiple Solutions

Unusual projects can have more than one IRR

The number of positive IRRs to a project depends on the number of sign reversals to the project’s cash flows

– The Reinvestment AssumptionIRR method implicitly assumes cash inflows will be reinvested at the project’s IRR

24

Comparing IRR and NPV

NPV and IRR do not always select the same project in mutually exclusive decisions

A conflict can arise if NPV profiles cross in the first quadrant

In the event of a conflict The selection of the NPV method is preferred

25

Figure 10-2 Projects for Which IRR and NPV Can Give Different Solutions

26

At a cost of capital of k1, Project A is better than Project B, while at k2 the opposite is

true.

PROJECTS WITH A SINGLE OUTFLOW AND REGULAR INFLOWS

Many projects are characterized by an initial outflow and a series of equal, regular inflows:

PV of annuity formula makes the pattern easy to work with

NPV: NPV = C0 + C [PVFAk,n]

IRR: 0 = C0 + C [PVFAIRR,n]

Example 10-6 – Regular Cash InflowsFind the NPV and IRR for the following project if the cost of capital is

12%.

C0 C1 C2 C3

($5,000) $2,000 $2,000 $2,000

Solution: For NPVNPV = C0 + C[PVFAk,n]

= -$5,000 + $2,000[PVFA12,3] = -$5,000 + $2,000(2.4018) = -$196.40

For IRR

0 = C0 + C[PVFAIRR,n]

= -$5,000 + $2,000[PVFAIRR,3]

PVFAIRR,3 = $5,000 / $2,000 = 2.5000

From which IRR is between 9% and 10%

Profitability Index (PI)

Is a variation on the NPV method

A ratio of the present value of a project’s inflows to the present value of a project’s outflows

Projects are acceptable if PI>1

29

Profitability Index (PI)

Also known as the benefit/cost ratio– Positive future cash flows are the benefit– Negative initial outlay is the cost

30

1 2 n

1 2 n

0

C C C

1+k 1+k 1+kPI

C

or

present value of inflowsPI

present value of outflows

Profitability Index (PI)

Decision Rules– Stand-alone Projects

If PI > 1.0 accept

If PI < 1.0 reject

– Mutually Exclusive ProjectsPIA > PIB choose Project A over Project B

Comparison with NPV– With mutually exclusive projects the two

methods may not lead to the same choices

31

Comparing Projects with Unequal Lives

If a significant difference exists between mutually exclusive projects’ lives, a direct comparison is meaningless

The problem arises due to the NPV method– Longer lived projects almost always have

higher NPVs

32

Comparing Projects with Unequal Lives

Two solutions exist– Replacement Chain Method

Extends projects until a common time horizon is reached

– Equivalent Annual Annuity (EAA) MethodReplaces each project with an equivalent perpetuity that equates to the project’s original NPV

33

Concept Connection Example 10-8 Replacement Chain

34

Thus, choosing the Long-Lived Project is a better decision than choosing the Short-Lived Project twice.

The IRR method argues for undertaking the Short-Lived Project while the NPV method argues for the Long-Lived Project. We’ll correct for the unequal life problem by using both the Replacement Chain Method and the EAA Method. Both methods will lead to the same decision.

Concept Connection Example 10-8 Replacement Chain

35

Which of the two following mutually exclusive projects should a firm purchase?

Concept Connection Example 10-9 Equivalent Annual Annuity (EAA)

36

The EAA Method equates each project’s original NPV to an equivalent annual annuity. For the Short-Lived Project the EAA is $167.95 (the equivalent of receiving $432.82 spread out over 3 years at 8%); while the Long-Lived Project has an EAA of $187.58 (the equivalent of receiving $867.16 spread out over 6 years at 8%).

Concept Connection Example 10-9 Equivalent Annual Annuity (EAA)

37

Because the Long-Lived Project has the higher EAA, it should be chosen. This is the same decision reached by the Replacement Chain Method.

Capital Rationing

Used when capital funds for new projects are limited

Generally rank projects in descending order of IRR and cut off at the cost of capital

However this doesn’t always make the best use of capital so a complex mathematical process called constrained maximization can be used

38

Figure 10-6 Capital Rationing

39