chapter 1 the accounting equation. 1-22 general info accounting is the language of business!...

TRANSCRIPT

Chapter 1Chapter 1The Accounting Equation

1-2 2

General InfoGeneral Info

• Accounting is the language of business!

• Understanding accounting helps managers & owners make better business decisions.

• Failure to understand accounting info. can result in poor business decisions.

• Inaccurate accounting records often contribute to business failure and bankruptcy.

ENRON!

LESSON 1-1LESSON 1-1

What does an accountant do?•Plans, records, analyzes, and interprets financial records

•Handles a broad range of responsibilities•These are skills successful businesses cannot do without.

•If you are good, the sky’s the limit.

1-2 4

Is Accounting Boring?Is Accounting Boring?

• Will it lead you to a career in the spotlight?

• Brad Pitt staring in an action thriller about a jet setting accountant???

• Who develops and approves the budget for his films to go into production?

• Who advises Mr. Pitt how to invest his salary?

1-2 5

1-1 New Vocabulary1-1 New Vocabulary• Service Business

– A business that performs an activity for a fee• Examples: • Dr. Moser• Marcy Allen-Klaus, Attorney

• Sole Proprietorship—Proprietor means “owner”.– A business owned by one person.

• Examples:• Tresses• Dr. Haines• Mike’s Landscaping

1-2 6

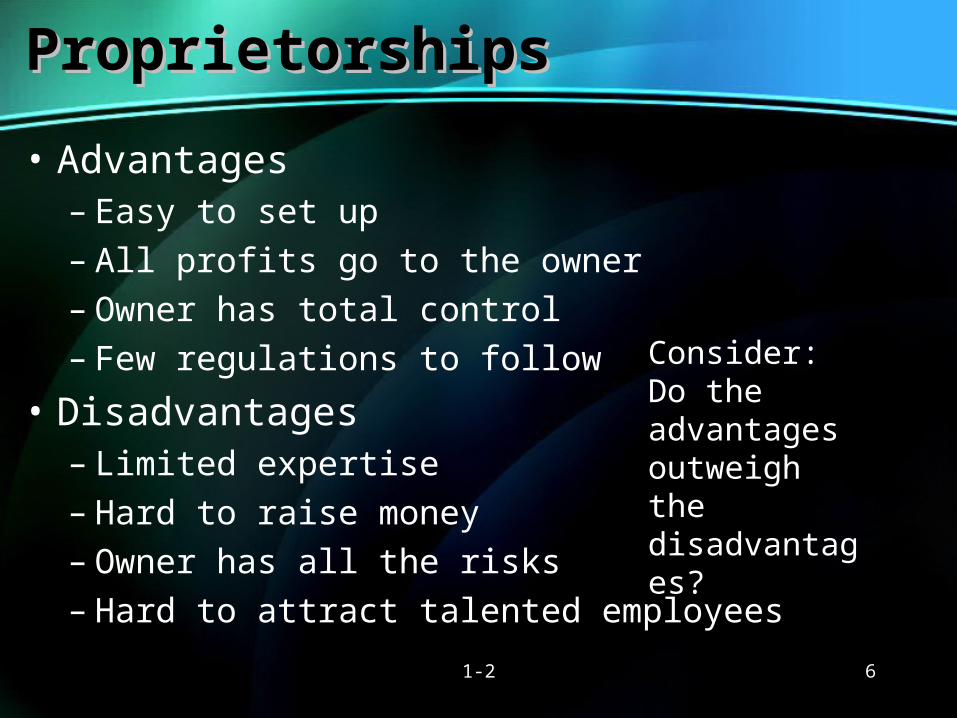

ProprietorshipsProprietorships

• Advantages– Easy to set up– All profits go to the owner– Owner has total control– Few regulations to follow

• Disadvantages– Limited expertise– Hard to raise money– Owner has all the risks– Hard to attract talented employees

Consider: Do the advantages outweigh the disadvantages?

1-2 7

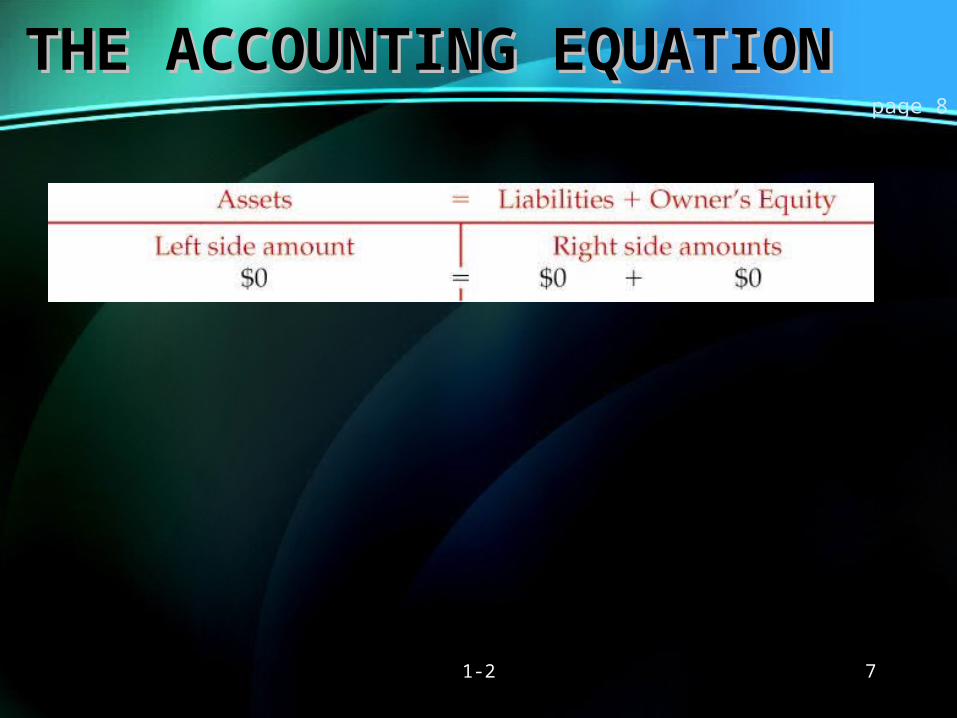

THE ACCOUNTING EQUATIONTHE ACCOUNTING EQUATIONpage 8

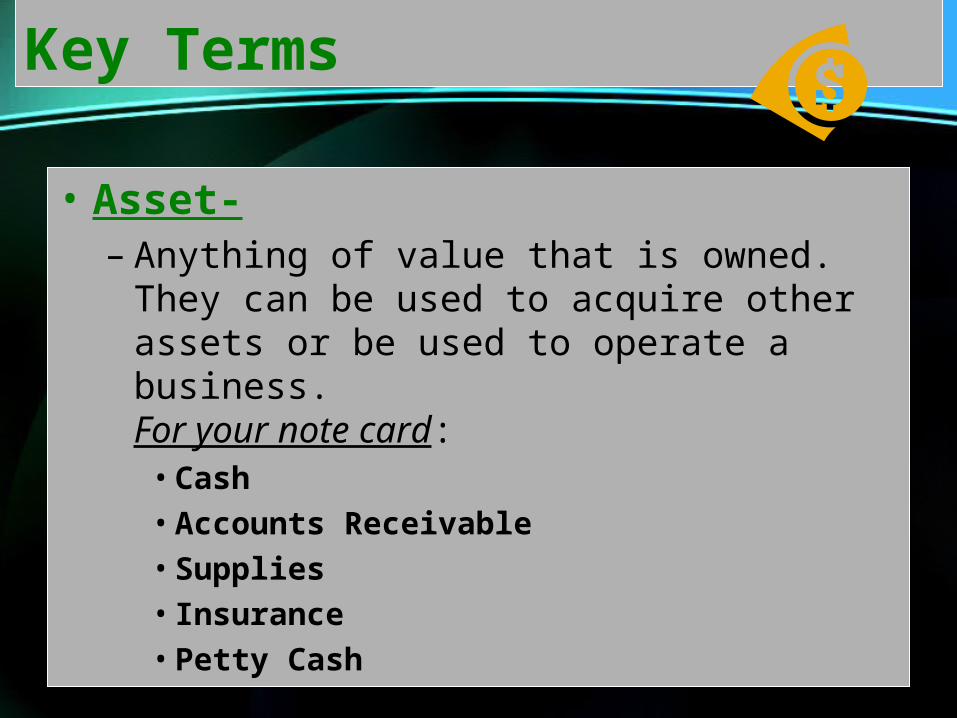

Key Terms

• Asset-– Anything of value that is owned. They can be

used to acquire other assets or be used to operate a business.For your note card:

• Cash• Accounts Receivable• Supplies• Insurance• Petty Cash

Key Terms

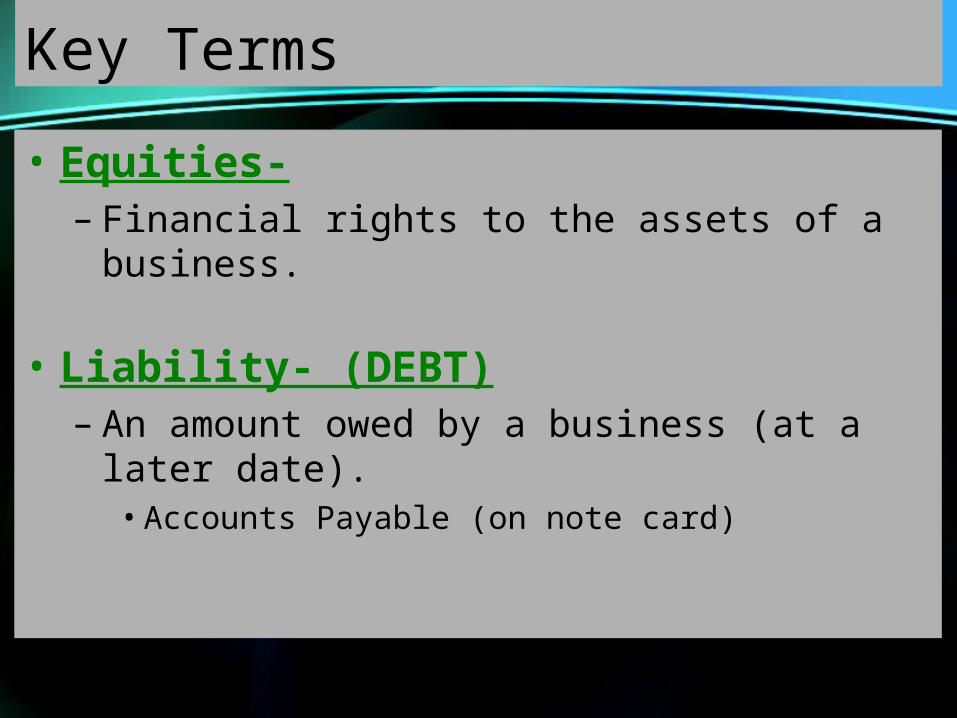

• Equities-– Financial rights to the assets of a business.

• Liability- (DEBT)– An amount owed by a business (at a later date).

• Accounts Payable (on note card)

Yes, More Terms

Owner’s Equity-

(the value of ownership)

• The amount remaining after the value of all liabilities is subtracted from the value of all assets.

• Assets-Liabilities = Owner’s Equity

1-2 11

Financial ClaimsFinancial Claims

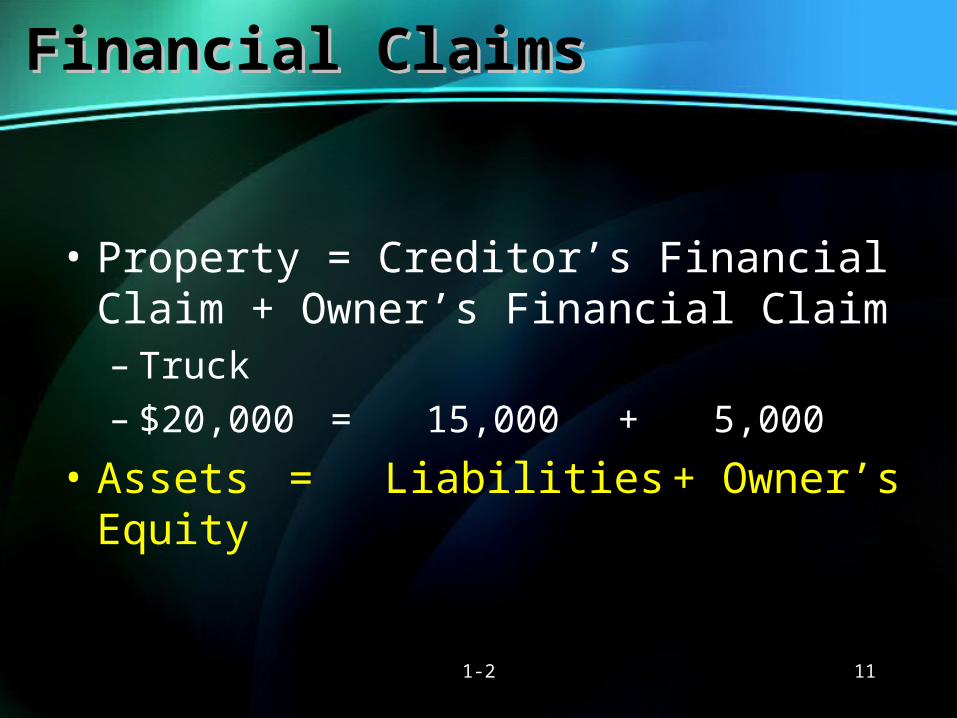

• Property = Creditor’s Financial Claim + Owner’s Financial Claim– Truck– $20,000 = 15,000 + 5,000

• Assets = Liabilities + Owner’s Equity

1-2 12

The Accounting EquationThe Accounting Equation

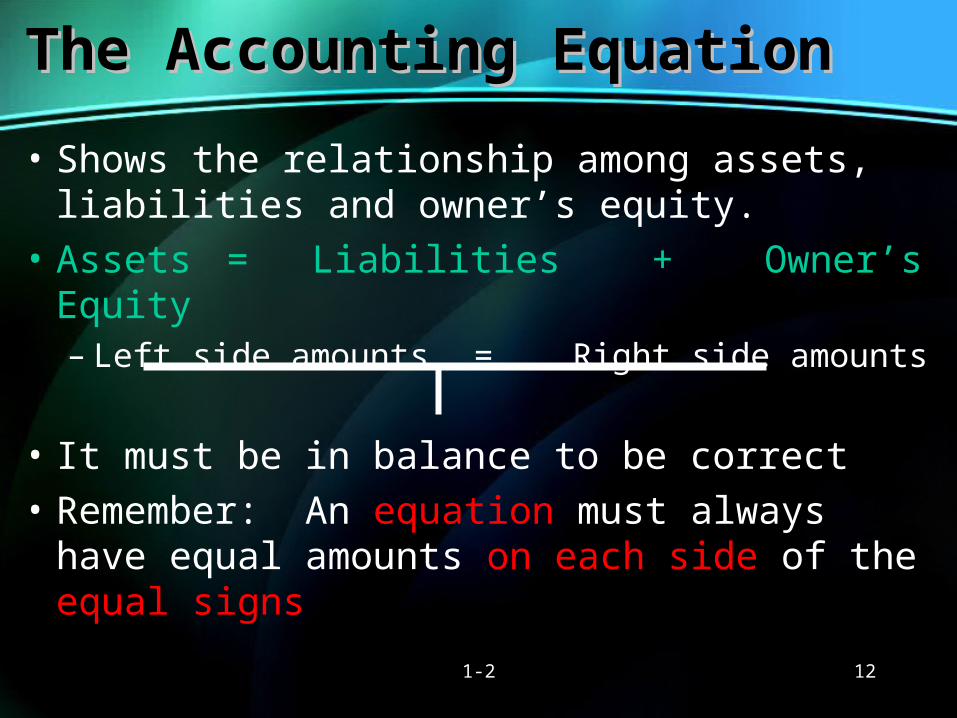

• Shows the relationship among assets, liabilities and owner’s equity.

• Assets = Liabilities + Owner’s Equity– Left side amounts = Right side amounts

• It must be in balance to be correct

• Remember: An equation must always have equal amounts on each side of the equal signs

1-2 13

The Accounting EquationThe Accounting Equation

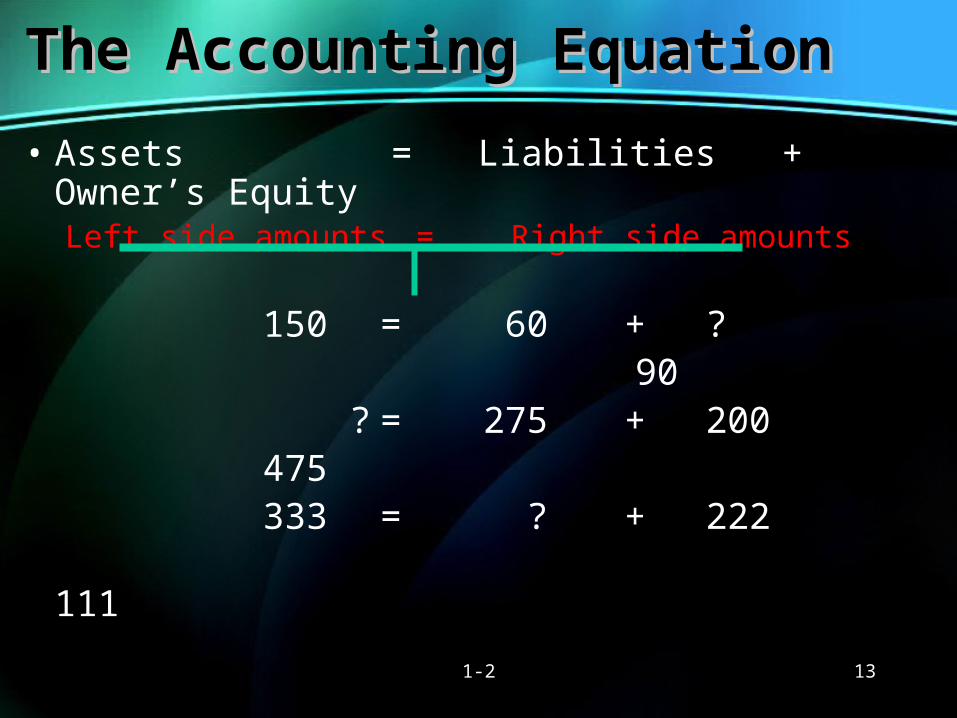

• Assets = Liabilities + Owner’s EquityLeft side amounts = Right side amounts

150 = 60 + ? 90 ? = 275 + 200 475 333 = ? + 222 111

1-2 14

Audit Your UnderstandingAudit Your Understanding

• Give examples of service businesses– Dry Cleaners– Doctor’s Office– Auto Repair

• What is a proprietorship?– A business owned by one person

• State the accounting equation– Assets = Liabilities + Owner’s Equity

1-2 15

Work Together 1-1Work Together 1-1

• On the O: drive– We will do this together

ON YOUR OWN– Just like it says, you will be doing this by yourself

LESSON 1-2LESSON 1-2

How Business Activities

Change the Accounting Equation

Quick ReviewQuick Review

• What is the Accounting Equation?

• What is a Proprietorship?

1-2 – Notecard Time!!!1-2 – Notecard Time!!!

• Note card #1

–Assets• Cash

• Petty Cash

• Accounts Receivable

• Supplies

• Prepaid Insurance #1

1-2 – Notecard Time!!!1-2 – Notecard Time!!!

• Note card #2

–Liabilities• Accounts Payable

#2

1-2 – Notecard Time!!!1-2 – Notecard Time!!!

• Note card # 3

–Owner’s Equity• Capital

• Drawing

#3

1-2 21

Accounting ConceptsAccounting Concepts• Business Entity: This concept is applied when a

business’s financial information is recorded and reported separately from the owner’s personal financial information.

– Example: house, personal car, personal belongings

• Unit of measurement: Business transactions are stated in numbers that have common values; that is, using a common unit of measurement.

– Example: Canadian dollar

• Realization of Revenue: Revenue is recorded at the time goods or services are sold.—even if it is a charge sale

1-2 22

New VocabularyNew Vocabulary

• Transaction: A business activity that changes assets, liabilities, or owner’s equity. Example: paid cash for supplies

• Account: A record summarizing all the information pertaining to a single item in the accounting equation. Example: Cash

• Account Title: The name given to an account.• Account Balance: The amount in an account.• Capital: The account used to summarize the

owner’s equity in a business. Example: Travis Smith, Capital

1-2 23

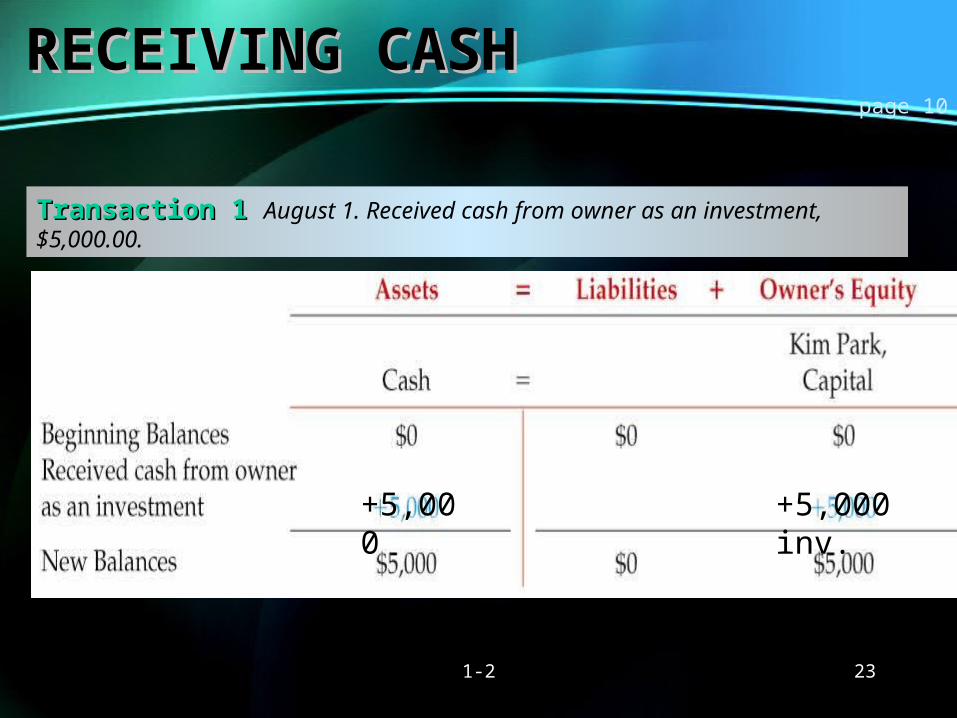

RECEIVING CASHRECEIVING CASH

Transaction 1Transaction 1 August 1. Received cash from owner as an investment, $5,000.00.

page 10

+5,000 +5,000 inv.

1-2 24

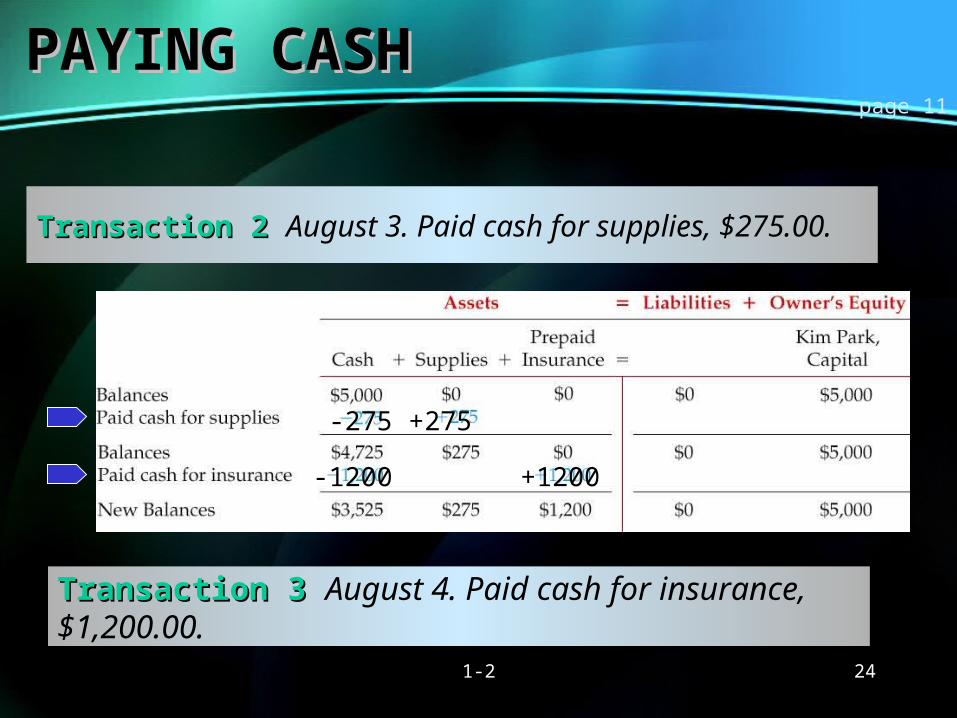

PAYING CASHPAYING CASH

Transaction 2Transaction 2 August 3. Paid cash for supplies, $275.00.

Transaction 3Transaction 3 August 4. Paid cash for insurance, $1,200.00.

page 11

-275 +275

-1200 +1200

1-2 25

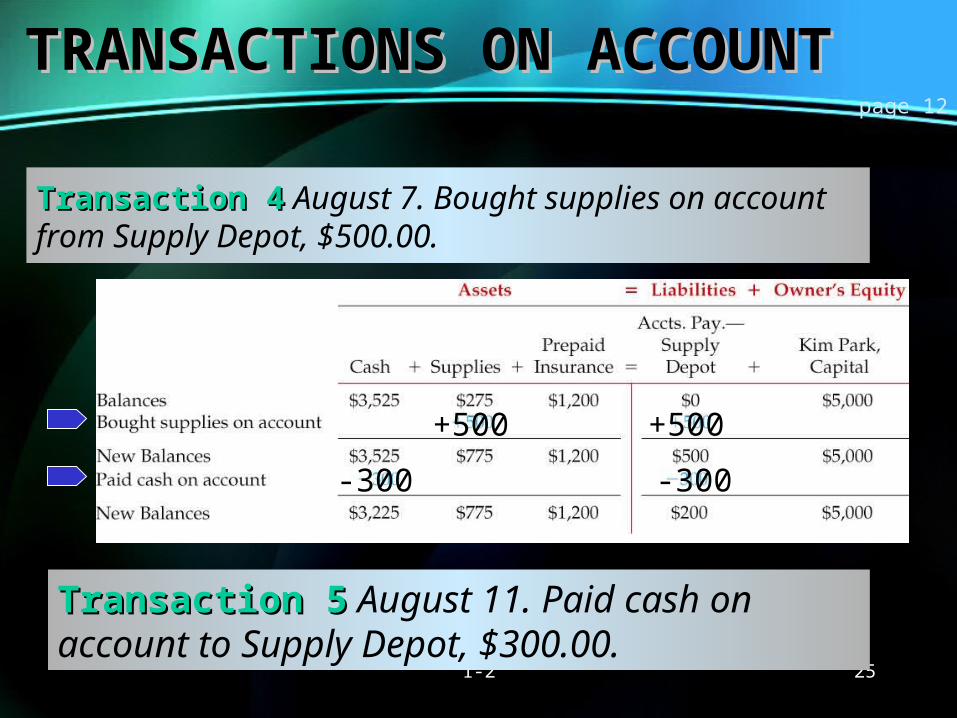

TRANSACTIONS ON ACCOUNTTRANSACTIONS ON ACCOUNT

Transaction 4Transaction 4 August 7. Bought supplies on account from Supply Depot, $500.00.

Transaction 5Transaction 5 August 11. Paid cash on account to Supply Depot, $300.00.

page 12

+500 +500

-300-300

1-2 26

Audit Your UnderstandingAudit Your Understanding

What must be done if a transaction increases the left side of the accounting equation?

• The right side must also be increased

How can a transaction affect only one side of the accounting equation?

• If one account is increased, another account on the same side of the equation must be decreased by the same amount.

To what does the phrase “on account” refer?• Buying items and paying for them at a later date.

LESSON 1-3LESSON 1-3

How Transactions Change Owner’s Equity

in an Accounting Equation

1-2 28

New Vocabulary

• Revenue: An increase in owner’s equity resulting from the operation of a business.

• Sales on Account: A sale for which cash will be received at a later date. (A.K.A. charge sale)

• Expense: A decrease in owner’s equity resulting from the operation of a business.

• Withdrawals: Assets taken out of the business for the owner’s personal use. (decreases Owner’s Equity)

1-2 29

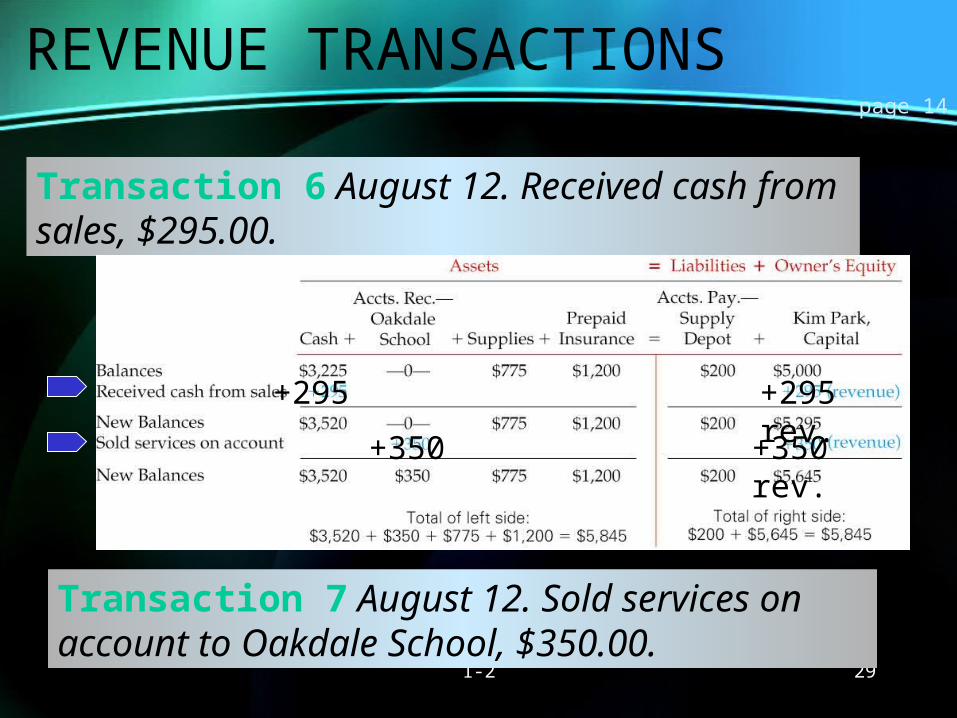

REVENUE TRANSACTIONS

Transaction 6 August 12. Received cash from sales, $295.00.

Transaction 7 August 12. Sold services on account to Oakdale School, $350.00.

page 14

+295

+350 +350 rev.

+295 rev.

1-2 30

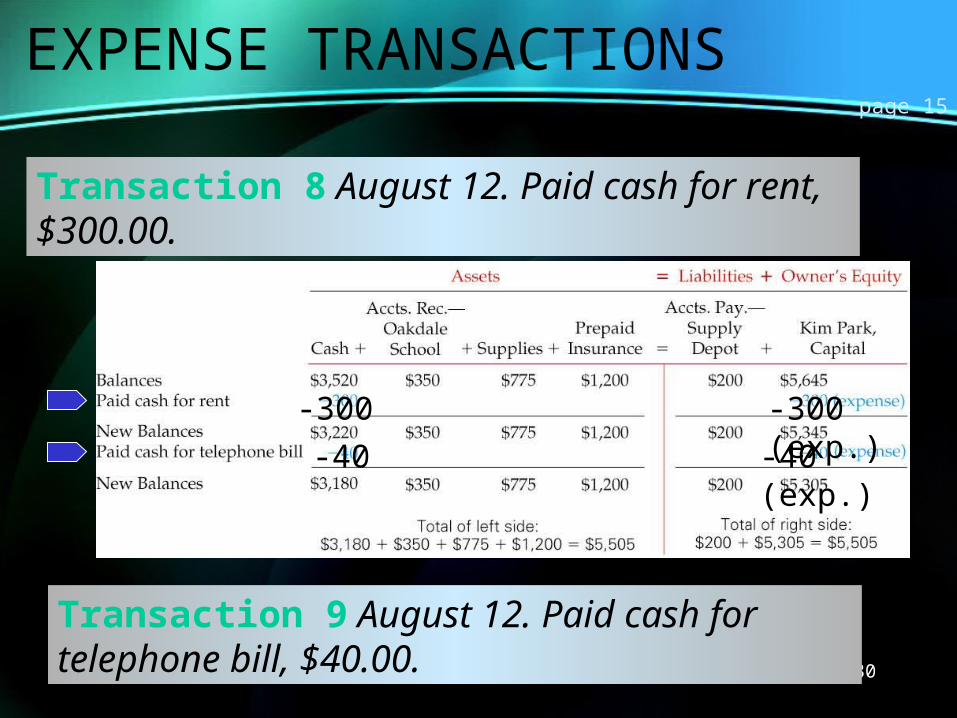

EXPENSE TRANSACTIONS

Transaction 8 August 12. Paid cash for rent, $300.00.

Transaction 9 August 12. Paid cash for telephone bill, $40.00.

page 15

-300

-40 -40 (exp.)

-300 (exp.)

1-2 31

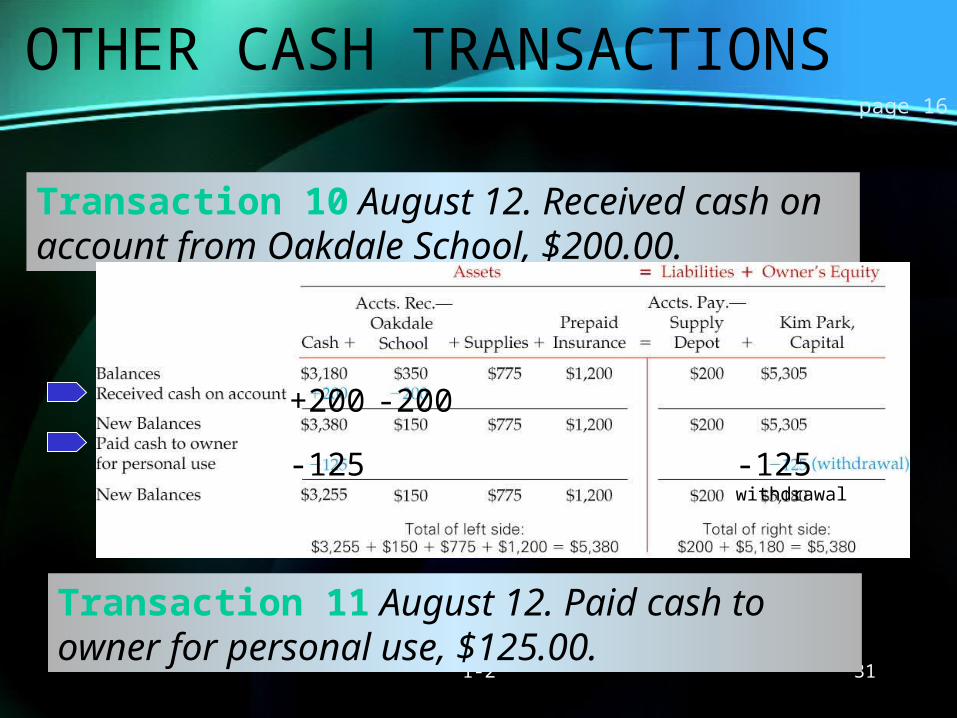

OTHER CASH TRANSACTIONS

Transaction 10 August 12. Received cash on account from Oakdale School, $200.00.

Transaction 11 August 12. Paid cash to owner for personal use, $125.00.

page 16

+200

-125 -125 withdrawal

-200

1-2 32

Audit Your Understanding

How is owner’s equity affected when cash is received from sales?

• increased

How is owner’s equity affected when services are sold on account?

• increased

How is owner’s equity affected when cash is paid for expenses?

• decreased

1-2 33

Work Together

• Download it from my site