chapter 1: important accounting concepts

TRANSCRIPT

1

Chapter 1: Important Accounting Concepts

Activity 1:

1 Who is known as the “Father” of Accounting”? ___Luca Pacioli.___

2 What does the double entry principle mean? __It means that for each debit entry there

will be an equal credit entry and for each credit entry there wil be an equal debit entry.___

3 Give the correct name for each of the following in the space provided:

a b c d e f Month Day Details Fol Rand-value c

… (g)-side Credit-side

A ___Month___

B ___Day___

c ___Details___

d ___Folio___

e ___Rand-value___

f ___Cents___

g ___Debit side___

Activity 2:

Use the following table and complete the missing information:

Account Definition/description

Classification of the account, it is

owner’s equity, non-current

asset/current asset, non-current

liability/current liability, income or

expense

EXAMPLE:

Equipment

Used to produce goods in a

manufacturing business

Non-current assets

Fuel Petrol or diesel for vehicles Expense

Trading inventory

Goods bought by the business to be sold at

a profit

Current asset

Loan: Name of the

bank, eg. Loan:

ABSA

A loan (money) received by the business.

Long term – payable over a period more

than one year.

Short term – payable over a period less

than one year.

Non-current liability

Current liability

2

Wages Paid weekly or bi-weekly to workers for

the work done by them

Expense

Mortgage Loan A long term loan for the purchase of Land

and Buildings

Non-current liability

Water and

Electricity

A cost (expense) paid to the municipality

for the use of water and electricity

Expense

Petty cash When the business must pay a small

amount (eg batteries or stationery) and it

is not worth the cost to write a cheque or

do a EFT

Current asset

Vehicles

Give FIVE examples of different kinds of

vehicles that can be used in a business:

a Busses

b Pick-ups

c Passenger vehicles

d Trucks

e Motorbikes

Non-current asset

Current Income Income for services rendered Income

Insurance

Monthly payment (premium) to insure

(cover/protect) assets against theft and

damage

Expense

Float

Cash (change) in the cash register Current asset

Debtors

Clients that buy on credit from the business

(on account) . They owe the business money.

Current asset

Drawings

The owner takes cash from the business or

something else (like trading inventory) for

personal use

Owner’s equity

Sales

Trading inventory sold for cash or on

credit

Income

Bank overdraft The business spends (make more

payments) as the money available in the

bank account

Current liability

Banking fees

Service fees paid to the bank for banking Expense

3

services rendered to the business

Creditor’s control Money owed to suppliers for goods

bought or services rendered to the

business on credit (on account)

Current liability

Interest on

overdraft

When the business’s bank account is in

overdraft, the business has to pay interest

on the overdraft (money owed to the

bank)

Expense

Fixed deposit

An investment made by the business

(normally with a bank) for a fixed period

Non-current asset

Interest on Fixed

deposit

Interest on Fixed deposit (investment) Income

Interest on loan

Interest paid on loan – interest on the

amount of money borrowed

Expense

Rent income

Income received for rental of a building or

part of a building

Income

Rent expense Payment of the rent for the office or shop Expense

Bank Money in the business’s bank account Current asset

Wages Weekly or bi-weekly payments to

employees for their work

Expense

Consumables Products used in the business to render a

service, eg. champoo in a hair salon or

cleaning materials

Expense

Activity 3

1 What is the difference between debtors en creditors?

Debtors buy from the business on credit/account and therefor owe the business money.

Creditors are people or other enterprises to whom the business owe money because goods or services

were bought on credit/account.

2 Name four accounts classified as non-current assets.

Land and Buildings

Vehicles

Equipment

Fixed deposit

4

3 What is the difference between capital en drawings?

Both are Owner’s equity accounts. Capital is the account that is used when the owner transfer

money or something else (eg a computer) to the business… that way he/she increases the

investment in the business.

Drawings is the account used when the owner withdraw money or something else (eg trading

inventory) for personal use.

4 Name THREE current assets and give a short description of each.

(a) Trading inventory: Goods bought by the business to be sold at a profit.

(b) Petty cash: Cash held by the business for smaller payments (eg batteries, some stationery or

refreshments).

(c) Float: Cash placed in the cash register as change.

5 What is the difference between salaries and wages?

Both are paid to employees as payment/compensation for their services (work) rendered..

Wages are paid weekly or bi-weekly and salaries are paid monthly.

6 Name FOUR kinds of income.

Current Income Sales

Rent Income Interest Income

Commission Income Donations received

7 Name SIX kinds of expenses.

Advertising Fuel

Banking fees Water and Electricity

Telephone Stationery

Packaging Insurance

8 Name FOUR people / groups interested in the financial statements of the business.

Owner Prospective investors

Creditors South African Revenue Services

9 Explain the double entry principle.

For each debit there should be an equivalent credit en vice versa. In other words for each credit

there should be an equivalent debit.

5

Chapter 2: The Accounting Equation

Activity 4

Classify the accounts as one of the following: Owner’s equity, Non-current asset, Current asset, Non-

current liability or Current liability, Income of Expense.

Account name Classification

Bank CURRENT ASSET

Banking fees EXPENSE

Fuel EXPENSE

Debtor’s control CURRENT ASSET

Donations made EXPENSE

Donations received INCOME

Land and Buildings NON-CURRENT ASSET

Trading inventory CURRENT ASSET

Repairs and maintenance EXPENSE

Rent income INCOME

Rent expense EXPENSE

Capital OWNER’S EQUITY

Petty cash CURRENT ASSET

Short term loan CURRENT LIABILITY

Creditor’s control CURRENT LIABILITY

Wages EXPENSE

Current Income from services rendered INCOME

Drawings OWNER’S EQUITY

Bank overdraft CURRENT LIABILITY

Postage EXPENSE

Interest on current bank account INCOME

Interest on overdraft EXPENSE

Interest on Fixed deposit INCOME

Stationery EXPENSE

Savings account CURRENT ASSET

Telephone EXPENSE

Equipment NON-CURRENT ASSET

6

Fixed deposit NON-CURRENT ASSET

Mortgage loan NON-CURRENT LIABILITY

Consumables EXPENSE

Packaging EXPENSE

Insurance EXPENSE

Vehicles NON-CURRENT ASSET

Water and electricity EXPENSE

Float (Change) CURRENT ASSET

Activity 5

Assets Owner’s equity Liabilities

Nr Amount Reason Amount Reason Amount Reason

1 +125 000 BANK ↑ +125 000 CAPITAL ↑

2 - 65 000 BANK ↓

+65 000 BANK ↑

3 - 9 600 BANK ↓

+9 600 EQUIPMENT ↑

4 - 13 450 BANK ↑

+13 450 EQUIPMENT ↑

5 - 2 800 BANK ↓ - 2 800 EXPENSES/WAGES ↑

6 - 4 600 BANK ↓ - 8 146 EXPENSES/INSURANCE ↑

7 +8 146 BANK ↑ +8 146 CURRENT INCOME ↑

8 - 1 800 BANK ↓ - 1 800 DRAWINGS ↑

9 - 1 580 BANK ↓ - 1 580 STATIONERY ↑

10 +1 800 BANK ↑ +1 800 RENT INCOME ↑

7

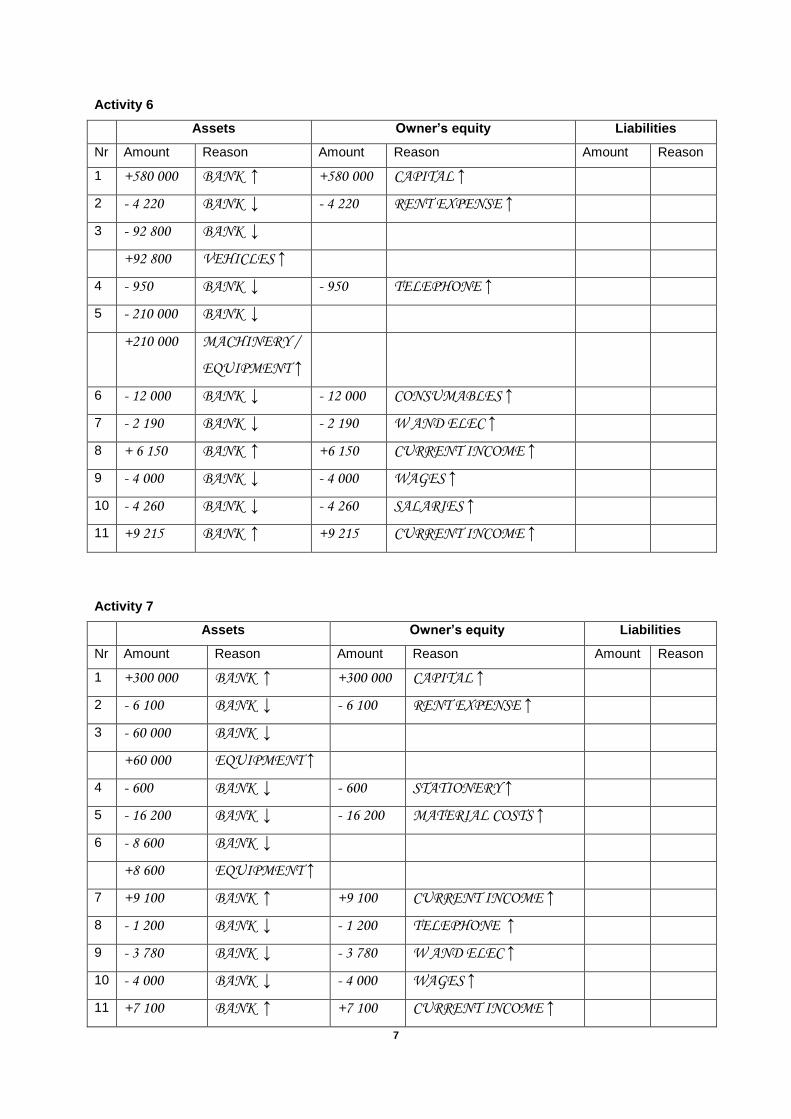

Activity 6

Assets Owner’s equity Liabilities

Nr Amount Reason Amount Reason Amount Reason

1 +580 000 BANK ↑ +580 000 CAPITAL ↑

2 - 4 220 BANK ↓ - 4 220 RENT EXPENSE ↑

3 - 92 800 BANK ↓

+92 800 VEHICLES ↑

4 - 950 BANK ↓ - 950 TELEPHONE ↑

5 - 210 000 BANK ↓

+210 000 MACHINERY /

EQUIPMENT ↑

6 - 12 000 BANK ↓ - 12 000 CONSUMABLES ↑

7 - 2 190 BANK ↓ - 2 190 W AND ELEC ↑

8 + 6 150 BANK ↑ +6 150 CURRENT INCOME ↑

9 - 4 000 BANK ↓ - 4 000 WAGES ↑

10 - 4 260 BANK ↓ - 4 260 SALARIES ↑

11 +9 215 BANK ↑ +9 215 CURRENT INCOME ↑

Activity 7

Assets Owner’s equity Liabilities

Nr Amount Reason Amount Reason Amount Reason

1 +300 000 BANK ↑ +300 000 CAPITAL ↑

2 - 6 100 BANK ↓ - 6 100 RENT EXPENSE ↑

3 - 60 000 BANK ↓

+60 000 EQUIPMENT ↑

4 - 600 BANK ↓ - 600 STATIONERY ↑

5 - 16 200 BANK ↓ - 16 200 MATERIAL COSTS ↑

6 - 8 600 BANK ↓

+8 600 EQUIPMENT ↑

7 +9 100 BANK ↑ +9 100 CURRENT INCOME ↑

8 - 1 200 BANK ↓ - 1 200 TELEPHONE ↑

9 - 3 780 BANK ↓ - 3 780 W AND ELEC ↑

10 - 4 000 BANK ↓ - 4 000 WAGES ↑

11 +7 100 BANK ↑ +7 100 CURRENT INCOME ↑

8

12 - 3 100 BANK ↓ - 3 100 INSURANCE ↑

13 - 815 BANK ↓ - 815 CONSUMABLES↑

Total income Total Expenses

9 100 6 100

7 100 600

16 200

1 200

3 780

4 000

3 100

815

16 200 35 795

Activity 8

Assets Owner’s equity Liabilities

Nr Amount Reason Amount Reason Amount Reason

2 - 55 500 BANK ↓

+55 500 EQUIPMENT ↑

3 - 180 000 BANK ↓

+180 000 VEHICLES ↑

4 +25 000 BANK ↑ +25 000 CURRENT INCOME ↑

5 - 2 000 BANK ↓ - 2 000 WAGES ↑

6 +50 000 BANK ↑ +50 000 CAPITAL ↑

7 - 2 900 BANK ↓ - 950 STATIONERY ↑

+1 950 EQUIPMENT ↑

8 - 550 BANK ↓ - 550 FUEL ↑

9 - 2 200 BANK ↓ - 2 200 WAGES ↑

10 +30 125 BANK ↑ +30 125 CURRENT INCOME ↑

16 1615

Income – expenses = nett profit /loss

16 200 – 35 795 = -19 595

Loss

9

Total income Total Expenses

25 000 2 000

30 125 950

550

2 200

55 125 5 700

Activity 9

Assets Owner’s equity Liabilities

Nr Amount Reason Amount Reason Amount Reason

1 +100 000 BANK ↑ +100 000 CAPITAL ↑

2 - 15 900 BANK ↓ - 15 900 MATERIAL COSTS ↑

3 - 46 000 BANK ↓

+46 000 EQUIPMENT ↑

4 +10 000 BANK ↑ +10 000 LOAN: Barclays ↑

5 - 9 600 BANK ↓ - 9 600 RENT EXPENSES ↑

6 - 1 710 BANK ↓ - 1 710 STATIONERY ↑

7 - 12 000 BANK ↓

+12 000 EQUIPMENT ↑

8 - 1 900 BANK ↓

+1 900 DEPOSIT:

Water and

electricity ↑

10 - 125

+125

DRAWINGS ↑ MATERIAL COSTS ↓

11 +19 200 BANK ↑ +19 200 CURRENT INCOME ↑

12 - 8 110 BANK ↓ - 8 110 WAGES ↑

13 - 1 555 BANK ↓ - 1 555 W AND ELEC ↑

14 - 10 000 BANK ↓ - 10 000 DRAWINGS ↑

Income - expenses = nett profit

55 125 – 5 700 = 49 425

Profit

10

Activity 10

Total income Total Expenses

19 200 15 900

9 600

1 710

8 110

1 555

19 200 36 875

Assets Owner’s equity Liabilities

Nr Amount Reason Amount Reason Amount Reason

1 +40 000 BANK ↑ +40 000 CAPITAL ↑

2 +50 000 BANK ↑ +50 000 LOAN: FNB↑

3 - 3 600 BANK ↓ - 3 600 WAGES ↑

4 - 5 000 BANK ↓ - 5 000 DRAWINGS ↑

5 - 9 000 BANK ↓ - 9 000 RENT EXPENSE ↑

6 - 1 900 STATIONERY ↑ +1 900 CREDITORS

CONTROL ↑

7 +5 910 BANK ↑ +5 910 CURRENT INCOME ↑

8 - 910 BANK ↓ - 910 INTEREST ON LOAN ↑

9 +19 195 BANK ↑ +19 195 CURRENT INCOME ↑

10 - 1 900 BANK ↓ - 1 900 CREDITORS

CONTROL ↓

11 +2 600 BANK ↑ +2 600 RENT INCOME ↑

12 +1 390 BANK ↑ +1 390 CURRENT INCOME ↑

Income - Expenses = Nett Profit/Loss

19 200 – 36 875 = -17 675

Loss

11

Income – Expenses = Nett profit/Loss

Activity 11

1 F

2 I

3 A

4 B

5 G

6 O

7 L

8 F

9 Q

10 M

11 R

12 T

13 S

14 J

15 H

16 K

Total income Total Expenses

5 910 3 600

19 195 9 000

2 600 1 900

1 390 910

29 095 15 410

29 095 – 15 410 = 13 685

Profit

12

Chapter 3: Transactions and source documents

Activity 12

Explain the following terms in your own words.

Terms Explanation

Current bank account The current bank account (cheque account) is the account by the bank

in the name of the business wherein the business receives cash on a

daily basis and from which payments are made on a daily basis.

Receipt This is the source document given as proof of cash received. The

duplicate is used by the bookkeeper to record the transaction in the

Cash Receipt Journal.

Cash register roll This is the source document used to keep record of cash sales and

services rendered for cash.

Deposit slip The Deposit slip is completed when cash received is deposited in the

business’s current account at the bank.

Overdraft When the business do not have enough funds in it’s bank account to

make all necessary payments, the business can apply for an overdraft

facility from the bank. Payments can then be made from funds made

available by the bank. The business then owes the bank. It is a

current liability.

Cheque counterfoil The business uses cheques to make payments. The cheque counterfoil

with detail of the payment is the source document that is used to

record the payment in the Cash Payments Journal.

Banking fees This is the cost for the business to have a current account. Examples

of fees charged by the bank are: Administrative fees, deposit fees and

cost of cheques ect. Interest on the bank overdraft is NOT banking

fees and is shown separately of banking fees.

Electronic funds transfer (EFT) Electronic funds transfer: When payments are done electronically (via

internet) or cash is received electronically.

13

Chapter 4: General Ledger

Activity 13

General Ledger of Connie Modiste

Balance sheet section

Capital B1

Month Day Details / Contra-

account Fol Rand c Month Day Details / Contra-account Fol Rand C

Feb 1 Bank 60 000 00

Bank B2

Feb 1 Capital 60 000 00 F Feb 2 Rent expense 1 230 00

12 Current income 3 110 00 Equipment 25 600 00

19 Current income 7 146 00 4 Telephone 920 00

8 Water and electricity 1 256 00

Wages 1 600 00

13 Consumables 525 00

23 Wages 1 800 00

25 Salaries 8 900 00

28 Balance c/f 28 425 00

70 256 00 70 256 00

Mch 1 Balance b/d 28 425 00

Equipment B3

Month Day Details / Contra-

account Fol Rand C Month Day Details / Contra-account Fol Rand c

Feb 2 Bank 25 600 00

Nominal section

Rent Expense N1

Feb 2 Bank 1 230 00

Telephone N2

Feb 4 Bank 920 00

Water and electricity N3

Feb 8 Bank 1 256 00

14

Wages N4

Feb 8 Bank 1 600 00

23 Bank 1 800 00

3 400 00

Current Income N5

Feb 12 Bank 3 110 00

19 Bank 7 146 00

10 256 00

Consumables N6

Feb 13 Bank 525 00

Salaries N7

Feb 25 Bank 8 900 00

Activity 14

General Ledger of Sorbet Hair Salon

Balance sheet section

Capital B1

Month Day Details / Contra-

account Fol Rand C Month Day Details / Contra-account Fol Rand c

Mch 1 Bank 300 000 00

Bank B2

Mch 1 Capital 300 000 00 Mch 2 Rent expense 6 100 00

15 Current income 9 100 00 4 Equipment 60 000 00

21 Current income 7 100 00 Stationery 600 00

4 Consumables 16 200 00

11 Equipment 8 600 00

19 Telephone 1 200 00

Water and electricity 3 780 00

25 Salaries 14 900 00

31 Balance c/f 204 820 00

316 200 00 316 200 00

Apr 1 Balance b/d 204 820 00

15

Equipment B3

Month Day Details / Contra-

account Fol Rand C Month Day Details / Contra-account Fol Rand c

Mch 4 Bank 60 000 00

11 Bank 8 600 00

68 600 00

Nominal section

Rent Expense N1

Mch 2 Bank 6 100 00

Stationery N2

Mch 4 Bank 600 00

Water and electricity N3

Mch 19 Bank 3 780 00

Current Income N4

Mch 15 Bank 9 100 00

21 Bank 7 100 00

16 200 00

Telephone N5

Mch 19 Bank 1 200 00

Consumables N6

Mch 6 Bank 16 200 00

16

Activity 15

General Ledger of Urban Fitness

Balance sheet section

Capital B1

Month Day Details / Contra-

account Fol Rand C Month Day Details / Contra-account Fol Rand C

Feb 1 Bank 1 000 000 00

19 Bank 200 000 00

1 200 000 00

Bank B2

Feb 1 Capital 1 000 000 00 Feb 4 Equipment 800 000 00

6 Current income 112 500 00 Rent expense 35 000 00

19 Current income 10 120 00 10 Wages 3 000 00

19 Capital 200 000 00 12 Equipment 19 000 00

15 Drawings 6 000 00

16 Water and electricity 2 300 00

21 Telephone 1 890 00

23 Stationery 610 00

25 Wages 3 000 00

28 Balance c/f 451 820 00

1 322 620 00 1 322 620 00

Mch 1 Balance b/d 451 820 00

Equipment B3

Month Day Details / Contra-

account Fol Rand C Month Day Details / Contra-account Fol Rand C

Feb 4 Bank 800 000 00

12 Bank 19 000 00

819 000 00

Drawings B4

Feb 15 Bank 6 000 00

Nominal section

Rent Expense N1

Feb 4 Bank 35 000 00

17

Total of all amounts on the

debit side

=

Total of all amount on the

credit side

=

Current Income N2

Feb 6 Bank 112 500 00

19 Bank 10 120 00

122 620 00

Wages N3

Mch 10 Bank 3 000 00

25 Bank 3 000 00

6 000 00

Water and electricity N4

Mch 16 Bank 2 300 00

Telephone N5

Mch 21 Bank 1 890 00

Stationery N6

Mch 23 Bank 610 00

18

Activity 16

Nr General Ledger Accounting Equation

Account debited

Account credited

Assets Owner’s equity

Liabilities

1 Bank Capital +100 000 +100 000

2 Rent expense Bank - 4 500 - 4 500

3 Wages Bank - 4 000 - 4 000

4 Equipment Bank +9 000 - 9 000

5 Bank Current income +5 200 +5 200

6 Equipment Bank +9 400 - 9 400

7 Drawings Bank - 1 600 - 1 600

8 Float Bank - 600 +600

9 Bank Rent income +900 +900

10 Consumables Bank - 840 - 840

11 Bank Capital +50 000 +50 000

12 Salaries Bank - 12 400 - 12 400

13 Bank Loan: Absa +80 000 +80 000

Activity 17

Nr General Ledger Accounting Equation

Account debited

Account credited

Assets Owner’s equity

Liabilities

1 Bank Capital +250 000 +250 000

2 Equipment Bank - 19 000

+19 000

3 Wages Bank - 3 000 - 3 000

Float Bank - 5 000

+5 000

4 Bank Current income +15 200 +15 200

5 Bank Capital +600 000 +600 000

6 Rent expense Bank - 6 250 - 6 250

7 Wages Bank - 3 300 - 3 300

8 Vehicles Loan: FNB +50 000 +50 000

9 Packaging Bank - 2 100 - 2 100

10 Drawings Bank - 650 - 650

11 Refreshments Bank - -

19

Chapter 5: Susidiary journals and General Ledger

Activity 18

Cash Receipts Journal of Betsie’s Aftercare Centre - February 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts Bank

Current Income

Sundry

Amount Fol Details

001 01 Betsie Bell 1 780 000 00 1 780 000 00 1 780 000 00 Capital

B/S 06 Nedbank 300 000 00 300 000 00 Mortgage loan: Nedbank

CRR Services rendered 12 000 00 12 000 00 12 000 00

CRR 15 Services rendered 9 800 00 9 800 00 9 800 00

CRR 21 Services rendered 10 300 00 10 300 00

002 Sandra Ramage 3 000 00 13 300 00 3 000 00 Rent income

CRR 28 Services rendered 7 800 00 7 800 00 7 800 00

2 122 900 00 39 900 00 2 083 000 00

20

Activity 19

Cash Receipts Journal of Rita’s Salon – February 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts Bank Current Income

Sundry

Amount Fol Details

001 1 Rita Viljoen 250 000 00 250 000 00 250 000 00 Capital

CRR 8 Services rendered 7 813 00 7 813 00 7 813 00

CRR 16 Services rendered 5 316 00 5 316 00 5 316 00

002 25 Rita Viljoen 100 000 00 100 000 00 Capital

CRR Services rendered 8 110 00 108 110 00 8 110 00

003 26 Max Marais 8 000 00 8 000 00 8 000 00 Rent income

CRR 28 Services rendered 15 230 00 15 230 00 15 230 00

394 469 00 36 469 00 358 000 00

21

Activity 20

Cash Receipts Journal of Bruto Herstellers – January 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts Bank

Current Income

Sundry

Amount Fol Details

B/S 1 T. Bruto 105 000 00 105 000 00 Capital

001 7 Jaco Crock 4 252 00 4 252 00 4 252 00

002 14 Minaars Inc 3 120 00 3 120 00 3 120 00 Commission-income

003 19 Elfie Green 2 169 00 2 169 00 2 169 00

B/S T. Bruto 45 000 00 45 000 00 Capital

B/S 25 Tin Man 9 800 00 9 800 00

169 341 00 16 221 00 153 120 00

22

Activity 21

Cash Receipts Journal of Hi Flyers Garden Services – April 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts Bank

Current Income

Sundry

Amount Fol Details

105 5 Freddie Flyer 150 000 00 150 000 00 150 000 00 Capital

CRR 11 Services rendered 8 475 00 8 475 00 8 475 00

106 20 Freddie Flyer 50 000 00 50 000 00 Capital

CRR Services rendered 12 235 00 62 235 00 12 235 00

B/S 25 Gunter Simon 15 000 00 15 000 00 Rent income

CRR 28 Services rendered 11 985 00 11 985 00 11 985 00

B/S ABSA 55 00 55 00 Interest on current account

247 750 00 32 695 00 215 055 00

23

Activity 22

Cash Receipts Journal of Boma Plants – September 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts Bank

Current Income

Sundry

Amount Fol Details

685 1 Fabulous Plants 7 582 00 7 582 00 7 582 00 Commission-income

B/S 6 FNB 35 120 00 35 000 00 Fixed deposit: FNB

120 00 Interest on Fixed deposit

686 Joe Soap 6 950 00 6 950 00 6 950 00

687 19 Gary Hitsy 20 000 00 20 000 00 Capital

CRR Services rendered 8 350 00 28 350 00 8 350 00

B/S 21 Trix Thompson 12 000 00 12 000 00 Rent income

90 002 00 15 300 00 74 702 00

24

Activity 23

General Ledger of Betsie’s Aftercare Centre

Balance sheet section

Capital B1

2016 Feb

1

Bank

CRJ

1 780 000 00

Bank B2

2016 Feb

28

Total receipts

CRJ

2 122 900 00

Mortgage Loan B3

2016 Feb 6 Bank CRJ 300 000 00

Nominal section

Current Income N1

2016 Feb

28

Bank

CRJ

31 080 00

Rent income N2

2016 Feb

21

Bank

CRJ

3 000 00

Analyze the transactions in activity 21 according to the Accounting Equation:

Nr General Ledger Accounting Equation

Account debited

Account credited

Assets Owner’s equity

Liabilities

1 Bank Capital +1 780 000 +1 780 000

6 Bank Mortgage Loan: Nedbank +300 000 +300 000

Bank Current income +12 000 +12 000

15 Bank Current income +9 800 +9 800

21 Bank Current income +10 300 +10 300

Bank Rent income +3 000 +3 000

28 Bank Current income +7 800 +7 800

25

Activity 24

General Ledger of Rita’s Salon

Balance sheet section

Capital B1

2016 Feb

1

Bank

CRJ

250 000 00

Bank B2

2016 Feb

28

Total receipts

CRJ

294 559 00

Nominal section

Current Income N1

2016 Feb

28

Bank

CRJ

36 559 00

Rent income N2

2016 Feb

28

Bank

CRJ

8 000 00

Activity 25

General Ledger of Bruto Herstellers (Repairers)

Balance sheet section

Capital B1

2016 Jan

1

Bank

CRJ

105 000 00

19 Bank CRJ 45 000 00

Bank B2

2016 Jan

31

Total receipts

CRJ

169 341 00

Nominal section

Current income N1

2016 Jan

31

Bank

CRJ

16 221 00

Commission income N2

2016 Jan

14

Bank

CRJ

3 120 00

26

Activity 26

General Ledger of Hi Flyer Garden Services

Balance sheet section

Capital B1

2016 Apr

5

Bank

CRJ

150 000 00

20 Bank CRJ 50 000 00

200 000 00

Bank B2

2016 Apr

30

Total receipts

CRJ

247 750 00

Nominal section

Current Income N1

2016 Apr

30

Bank

CRJ

32 695 00

Rent income N2

2016 Apr

25

Bank

CRJ

15 000 00

Interest on current account N3

2016 Apr

28

Bank

CRJ

55 00

Analyze the transactions of activity 22 according to the Accounting Equation:

Nr General Ledger Accounting Equation

Account debited

Account credited

Assets Owner’s equity

Liabilities

5 Bank Capital +150 000 +150 000

11 Bank Current income +8 475 +8 475

20 Bank Current income +12 235 +12 235

25 Bank Rent income +15 000 +15 000

28 Bank Current income +11 985 +11 985

Bank Interest on current

account +55 +55

27

Activity 27

General Ledger of Boma Plants

Balance sheet section

Capital B1

2016 Sept

1

Balance

b/d

140 000 00

19 Bank

CRJ

20 000

00

160 000 00

Fixed deposit: FNB B2

2016 Sept

1

Balance

b/d

35 000 00

2016 Sept 6

Bank

CRJ

35 000 00

Bank B3

2016 Sept

30

Total receipts

CRJ

90 002 00

Nominal section

Current income N1

2016 Sept

30

Bank

CRJ

15 300 00

Commission income N2

2016 Sept 1

Bank

CRJ

7 582 00

Rent income N3

2016 Sept

21

Bank

CRJ

12 000 00

Interest on Fixed deposit N4

2016 Sept

6

Bank

CRJ

120 00

28

Activity 28

Cash Receipts Journal of Bakkie Winkels – May 2016

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

001 01 Ben Bakkie 150 000 00 150 000 00 Capital

CRR 04 Services rendered 4 000 00 4 000 00

002 Belinda Burger 800 00 4 800 00 800 00 Rent income

CRR 10 Services rendered 6 200 00 6 200 00 6 200 00

B/S 15 Ben Bakkie 20 000 00 20 000 00 Capital

B/S Services rendered 9 800 00 9 800 00

B/S 25 Services rendered 1 500 00 1 500 00

B/S 28 Absa 110 00 110 00 Interest on current account

192 410 00 21 500 00 170 910 00

29

General Ledger of Bakkie Winkels

Balance sheet section

Capital B1

2016 May

1

Bank

CRJ

150 000 00

15 Bank

CRJ

20 000 00

Bank B2

2016 May

31

Total receipts

CRJ

192 410 00

Nominal section

Current income N1

2016 May

30

Bank

CRJ

21 500 00

Rent income N2

2016 May

4

Bank

CRJ

800 00

Interest on current account N3

2016 May

28

Bank

CRJ

110 00

30

Activity 29

Cash Payments Journal of Betsie’s Aftercare Centre – February 2016 CPJ

Doc

D

Name of

beneficiary

Fol Bank Wages Consumables

Sundry

Amount Fol Details

001 01 Attorney -Cash 1 350 000 00 1 350 000 00 B3 Land and Buildings

002 12 Makro 80 000 00 80 000 00 B4 Equipment

003 17 Pick ‘n Pay 910 00 910 00

004 Cash 3 600 00 3 600 00

B/S 24 Caxton Paper 1 600 00 1 600 00 N4 Advertising

005 CNA 630 00 630 00 N5 Stationery

006 Cash 3 960 00 3 960 00

B/S 29 Mutual & Federal 1 800 00 1 800 00 N6 Insurance

1 442 500 00 7 560 00 910 00 1 434 030 00

B5 N2 N3

31

General Ledger of Betsie’s Aftercare Centre

Balance sheet section

Land and Buildings B3

2016 Feb

1

Bank

CPJ

1 350 000 00

Equipment B4

2016 Feb

12

Bank

CPJ

80 000 00

Bank B5

2016 Feb

29

Total Payments

CPJ

1 442 500 00

Nominal section

Wages N2

2016 Feb

29

Bank

CPJ

7 560 00

Consumables N3

2016 Feb

29

Bank

CPJ

910 00

Advertising N4

2016 Feb

24

Bank

CPJ

1 600 00

Stationery N5

2016 Feb

24

Bank

CPJ

630 00

Insurance N6

2016 Feb

29

Bank

CPJ

1 800 00

32

Activity 30

Cash Payments Journal of Rita’s Salon – February 2016 CPJ

Doc

D

Name of

beneficiary

Fol Bank Wages Consumables

Sundry

Amount Fol Details

B/S 01 Dwayne Smith 6 525 00 6 525 00 N4 Rent expense

001 03 Honda Motors 125 000 00 125 000 00 B3 Vehicles

002 Makro Traders 59 200 00 59 200 00 B4 Equipment

003 07 Cash 3 700 00 3 200 00 500 00 B6 Float

004 08 L’Oreal Suppliers 9 160 00 9 160 00

B/S 21 Municipality 3 160 00 3 160 00 N5 Water and electricity

005 23 Globe Ltd 4 950 00 4 950 00 N6 Advertising

006 Rita Viljoen 8 000 00 8 000 00 B2 Drawings

219 695 00 3 200 00 9 160 00 207 335 00

B4 N2 N3

- 33 -

General Ledger of Rita’s Salon

Balance sheet section Drawings B2

2016 Feb

23

Bank

CPJ

8 000 00

Vehicles B3

2016 Feb

3

Bank

CPJ

125 000 00

Equipment B4

2016 Feb

3

Bank

CPJ

59 200 00

Bank B5

2016 Feb

29

Total Payments

CPJ

219 695 00

Float B6

2016 Feb

7

Bank

CPJ

500 00

Nominal section

Wages N2

2016 Feb

29

Bank

CPJ

3 200 00

Consumables N3

2016 Feb

29

Bank

CPJ

9 160 00

Rent expense N4

2016 Feb

1

Bank

CPJ

6 525 00

Water and electricity N5

2016 Feb

21

Bank

CPJ

3 160 00

Advertising N6

2016 Feb

12

Bank

CPJ

4 950 00

34

Activity 31

Cash Receipts Journal of Jakkals Plumbers – February 2016 CRJ 1

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

B/S 1 Dave Jakkals 500 000 00 500 000 00 Capital

01 12 Tina Zack 11 250 00 11 250 00 11 250 00

02 14 Sam Jolie 11 390 00 11 390 00 11 390 00

B/S 19 Zola Budd 5 110 00 5 110 00

03 24 Sally Peters 4 318 00 4 318 00 4 318 00

532 068 00 32 068 00 500 000 00

35

Cash Payments Journal of Jakkals Plumbers - February 2016 CPJ 1

Doc

D

Name of beneficiary

Fol Bank Wages Material cost

Sundry

Amount Fol Details

B/S 2 Muller Properties 3 600 00 3 600 00 Rent expense

001 3 Ford Motors 125 600 00 125 600 00 Vehicles

B/S 4 Ekhuruleni Municipality 1 600 00 1 600 00 Water and electricity

002 Dion Wired 7 200 00 7 200 00 Equipment

003 Waltons 960 00 960 00 Stationery

004 6 Mega Mica 6 100 00 6 100 00

005 Pick ‘n Pay 1 300 00 1 300 00 Consumables

006 Cash 3 100 00 3 100 00

007 12 Makro 1 860 00 1 860 00 Equipment

008 14 Cash 3 100 00 3 100 00

009 21 Cash 3 100 00 3 100 00

B/S Telkom 1 240 00 1 240 00 Telephone

010 28 Cash 3 348 00 3 348 00

011 Dave Jakkals 9 000 00 9 000 00 Drawings

B/S Rina Scholtz 14 300 00 14 300 00 Salaries

185 408 00 12 648 00 6 100 00 166 660 00

36

Activity 32

Cash Receipts Journal of Jakkals Plumbers - March 2016 CRJ 2

Doc D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

04 3 Dave Jakkals 275 000 00 275 000 00 275 000 00 Capital

05 4 Mary Moolman 4 720 00 4 720 00 4 720 00

06 10 Nols Nortje 3 149 00 3 149 00 3 149 00

07 18 Delia Badenhorst 14 925 00 14 925 00 14 925 00

CRR 24 Services rendered 9 114 00 9 114 00 9114 00

306 908 00 31 908 00 275 000 00

37

Cash Payments Journal of Jakkals Plumbers – March 2016 CPJ 2

Doc

D

Name of beneficiary

Fol Bank Wages Material cost

Sundry

Amount Fol Details

B/S 4 Muller Properties 3 600 00 3 600 00 Rent expense

012 6 Cash 900 00 900 00 Petty cash

013 7 Cash 3 348 00 3 348 00

014 10 Jack’s Paints 5 163 00 5 163 00

015 14 Cash 5 000 00 5 000 00

016 18 Makro 2 077 00 2 077 00

B/S Old Mutual

Insurers 5 170 00 5 170 00 Insurance

017 Simmons Ltd 9 195 00 9 195 00 Equipment

B/S 21 Telkom 1 473 00 1 473 00 Telephone

B/S Ekhuruleni Municipality 1 872 00 1 872 00 Water and electricity

017 Cash 5 500 00 5 500 00

018 28 Cash 5 500 00 5 500 00

B/S Cell C 910 00 910 00 Drawings

B/S 31 Rina Scholtz 14 300 00 14 300 00 Salaries

019 Dave Jakkals 6 000 00 6 000 00 Drawings

70 008 00 19 348 00 7 240 00 43 420 00

38

Activity 33

Balance the following Bank accounts in the General Ledger:

Bank B1

Aug 31 Total receipts CRJ 520 369 00 Aug 31 Total Payments CPJ 340 598 00

Balance c/f 179 771 00

520 369 00 520 369 00

Sep 1 Balance b/d 179 771 00

Next month the bank account will open with a balance of R179 771,00 .

Bank B1

Aug 31 Total receipts CRJ 995 212 00 Aug 31 Total Payments CPJ 452 125 00

Balance c/f 543 087 00

995 212 00 995 212 00

Sept 1 Balance b/d 543 087 00

Next month the bank account will open with a balance of R995 212,00.

Bank B1

Aug 31 Total receipts CRJ 455 101 00 Aug 31 Total Payments CPJ 234 587 00

Balance c/f 220 514 00

455 101 00 455 101 00

Sept 1 Balance b/d 220 514 00

Next month the bank account will open with a balance of R220 514,00.

.

Bank B1

Aug 31 Total receipts CRJ 148 951 00 Aug 31 Total Payments CPJ 896 548 00

Balance c/f 747 597 00

896 548 00 896 548 00

Sept 1 Balance b/d 747 597 00

Next month the bank account will open with a negative (overdraft) balance of R747 597,00 .

39

Bank B1

Aug 31 Total receipts CRJ 852 369 00 Aug 31 Total Payments CPJ 258 963 00

Balance c/f 593 406 00

852 369 00 852 369 00

Sept 1 Balance b/d 593 406 00

Next month the bank account will open with a balance of R593 406,00 .

Bank B1

Aug 31 Total receipts CRJ 789 654 00 Aug 31 Total Payments CPJ 654 123 00

Balance c/f 135 531 00

789 654 00 789 654 00

Sept 1 Balance b/d 135 531 00

Next month the bank account will open with a balance of R135 531,00.

- 40 -

Activity 34

Cash Receipts Journal of Erik Electricians – June 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

01 1 Erik Loots 150 000 00 150 000 00 150 000 00 B1 Capital

CRR 5 Services rendered 3 400 00 3 400 00

02 Peter Rich 900 00 4 300 00 900 00 N2 Commission Income

CRR 6 Services rendered 6 100 00 6 100 00 6 100 00

CRR 14 Services rendered 1 240 00 1 240 00

03 Erik Loots 9 000 00 10 240 00 9 000 00 B1 Capital

CRR 21 Services rendered 9 180 00 9 180 00

04 Peter Rich 610 00 9 790 00 610 00 N1 Commission Income

CRR 25 Services rendered 2 960 00 2 960 00 2 960 00

183 390 00 22 880 00 160 510 00

B5 N1

- 41 -

Cash Payments Journal of Erik Electricians – June 2016 CPJ

Doc

D

Name of

beneficiary

Fol Bank Wages Material cost

Sundry

Amount Fol Details

001 2 Sanlam 3 200 00 3 200 00 N5 Rent expense

002 3 Manlo Traders 10 400 00 10 400 00 B4 Equipment

B/S Telkom 1 340 00 1 340 00 N6 Telephone

003 4 Hyandai 115 000 00 115 000 00 B3 Vehicles

004 6 Ekhuruleni 2 100 00 2 100 00 N7 Water and electricity

005 Cash 3 000 00 3 000 00

006 11 Sasol Motors 625 00 625 00 N8 Fuel

007 13 Checkers 910 00 910 00 N9 Consumables

008 Cash 3 300 00 3 300 00

009 14 PNA 621 00 621 00 N10 Stationery

010 Cash 350 00 350 00 B2 Drawings

011 19 Sasol Motors 510 00 510 00 N8 Fuel

012 20 Cash 3 300 00 3 300 00

013 21 Caxton 4 218 00 4 218 00 N11 Advertising

B/S 22 Sanlam 1 450 00 1 450 00 N12 Insurance

014 25 Cash 8 000 00 8 000 00 B2 Drawings

015 26 Gary Ntumba 6 100 00 6 100 00 N13 Salaries

B/S Jacks Paints 8 620 00 8 620 00

173 044 00 9 600 00 8 620 00 154 824 00

B5 N3 N4

42

General Ledger of Erik Electricians

Balance sheet section

Capital B1

2016 June 1 Bank CRJ 150 000 00

14 Bank CRJ 9 000 00

159 000 00

Drawings B2

2016 June 14 Bank CPJ 350 00

25 Bank CPJ 8 000 00

8 350 00

Vehicles B3

2016 June 4 Bank CPJ 115 000 00

Equipment B4

2016 June 3 Bank CPJ 10 400 00

Bank B5

2016 June 30 Total receipts CRJ 183 390 00

2016 June 30 Total Payments CPJ 173 044 00

Balance c/f 10 346 00

183 390 00 183 390 00

July 1 Balance b/d 10 346 00

Nominal section

Current income N1

2016 June 30 Bank CRJ 22 880 00

Commission Income N2

2016 June 5 Bank CRJ 900 00

21 Bank CRJ 610 00

1 510 00

43

Wages N3

2016 June 30 Bank CPJ 9 600 00

Material costs N4

2016 June 30 Bank CPJ 8 620 00

Rent expense N5

2016 June 2 Bank CPJ 3 200 00

Telephone N6

2016 June 3 Bank CPJ 1 340 00

Water and electricity N7

2016 June 6 Bank CPJ 2 100 00

Fuel N8

2016 June 11 Bank CPJ 625 00

19 Bank CPJ 510 00

1 135 00

Consumables N9

2016 June 13 Bank CPJ 910 00

Stationery N10

2016 June 14 Bank CPJ 621 00

Advertising N11

2016 June 21 Bank CPJ 4 218 00

Insurance N12

2016 June 22 Bank CPJ 1 450 00

Salaries N13

2016 June 26 Bank CPJ 6 100 00

44

Activity 35

Cash Receipts Journal of Jojo Salon – April 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

001 1 Simon Jojo 150 000 00 150 000 00 Capital

CRR 18 Services rendered 11 500 00 11 500 00 11 500 00

CRR 22 Services rendered 17 800 00 17 800 00 17 800 00

CRR 26 Services rendered 12 150 00 12 150 00 12 150 00

191 450 00 41 450 00 150 000 00

45

Cash Payments Journal of Jojo Salon – April 2016 CPJ

Doc

D

Details

Fol Bank Wages Material cost

Sundry

Amount Fol Details

001 1 Mac’s Furniture

65 000 00 65 000 00 Equipment

002 Duo Bros

4 500 00 4 500 00 Rent expense

003 2 Cash

500 00 500 00 Float

004 4 L’Oreal

15 900 00 15 900 00

005 7 Cash

8 000 00 8 000 00

006 Telkom

2 100 00 2 100 00 Telephone

007 14 Cash

8 000 00 8 000 00

B/S 19 First for Women

1 100 00 1 100 00 Drawings

008 21 Cash

8 000 00 8 000 00

009 Checkers

1 498 00 1 498 00 Consumables

010 29 Ekhuruleni 2 280 00 2 280 00 Water and electricity

011 Cash

8 000 00 8 000 00

B/S 30 Tina Turner

8 440 00 8 440 00 Salaries

133 318 00 15 900 00 32 000 00 85 418 00

46

General Ledger of Jojo Salon

Balance sheet section

Capital B1

2016 April

1

Bank

CRJ

150 000 00

Drawings B2

2016 April

19

Bank

CPJ

1 100 00

Equipment B3

Bank B4

2016 April

30

Total receipts

CRJ

191 450 00

2016 April

30

Total Payments

CPJ

133 318 00

Balance c/f 58 132 00

191 450 00 191 450 00

May 1 Balance b/d 58 132 00

Float B5

2016 April

19

Bank

CPJ

1 100 00

Nominal section

Current income N1

2016 April

30

Bank

CRJ

41 450 00

Material costs N2

2016 April

21

Bank

CPJ

32 000 00

Wages N3

2016 April

30

Bank

CPJ

15 900 00

Rent expenses N5

2016 April

1

Bank

CPJ

4 500 00

Telephone N6

2016 April

7

Bank

CPJ

2 100 00

Consumables N7

2016 April

21

Bank

CPJ

1 498 00

Water and electricity N8

2016 April

29

Bank

CPJ

2 280 00

Salaries N9

2016 April

30

Bank

CPJ

8 440 00

47

Activity 36

Cash Receipts Journal of Pieter Herstellers (Repairers) – March 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

001 1 Pieter Venter 100 000 00 100 000 00 Capital

CRR 12 Services rendered 12 600 00 12 600 00

002 Absa Bank 100 000 00 112 600 00 100 000 00 Loan: Absa

CRR 25 Services rendered 9 000 00 9 000 00 9 000 00

003 30 Pieter Venter 50 000 00 50 000 00 Capital

CRR Services rendered 12 150 00 62 150 00 12 150 00

283 750 00 33 750 00 250 000 00

48

Cash Payments Journal of Pieter Herstellers – March 2016 CPJ

Doc

D

Details

Fol Bank Wages Consumables

Sundry

Amount Fol Details

001 2 Simon’s Shop 58 000 00 58 000 00 Equipment

002 3 Wouter & Seun 9 000 00 9 000 00 Rent expense

003 Cash 900 00 900 00 Float

004 4 Micro Traders 46 400 00 46 400 00

005 7 Cash 4 000 00 4 000 00

006 Feldman & Kie 5 190 00 5 190 00 Packaging

007 14 Cash 4 000 00 4 000 00

008 Pieter Venter 2 500 00 2 500 00 Drawings

009 19 Budget Insurance 4 100 00 4 100 00 Insurance

B/S Telkom 1 899 00 1 899 00 Telephone

010 21 Cash 4 400 00 4 400 00

011 27 Willis Wholesalers

14 640 00

6 100 00

8 540 00

Equipment

012 28 Cash 4 400 00 4 400 00

013 Pick ‘n Pay 350 00 350 00 Packaging

014 29 BMW 8 250 00 8 250 00 Drawings

B/S 30 Heidi Dirks 14 300 00 14 300 00 Salaries

B/S Ben Burges 5 100 00 5 100 00 Salaries

187 429 00 16 800 00 52 500 00 118 129 00

- 49 -

General Ledger of Pieter Herstellers (Repairers)

Balance sheet section

Capital B1

2016 Mch 1 Bank CRJ 100 000 00

30 Bank CRJ 50 000 00

150 000 00

Drawings B2

2016 Mch 14 Bank CPJ 2 500 00

29 Bank CPJ 8 250 00

10 750 00

Equipment B3

2016 Mch 2 Bank CPJ 58 000 00

27 Bank CPJ 8 540 00

66 540 00 Loan: Absa B4

2016 Mch 1 Bank CRJ 100 000 00

Bank B5

2016 Mch 31 Total receipts CRJ 283 750 00

2016 Mch 31 Total Payments CPJ 187 429 00

Balance c/f 96 321 00

283 750 00 283 750 00

April 1 Balance b/d 96 321 00

Float B6

2016 Mch 3 Bank CPJ 900 00

Nominal section

Current income N1

2016 Mch 31 Bank CRJ 33 750 00

Rent expense N2

2016 Mch 3 Bank CPJ 9 000 00

Packaging N3

2016 Mch 7 Bank CPJ 5 190 00

28 Bank CPJ 350 00

5 540 00

- 50 -

Consumables N6

2016 Mch 31 Bank CPJ 52 500 00

Telephone N7

2016 Mch 19 Bank CPJ 1 899 00

Salaries N8

2016 Mch 30 Bank CPJ 14 300 00

Bank CPJ 5 100 00

19 400 00

Insurance N4

2016 Mch 10 Bank CPJ 4 100 00

Wages

N5

2016 Mch 31 Bank CPJ 16 800 00

- 51 -

Activity 37

Cash Receipt Journal of Suzie’s Salon – June 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

001 1 Suzie Phili 90 000 00 90 000 00 90 000 00 Capital

CRR 9 Services rendered 4 610 00 4 610 00

002 J. Bullie 1 900 00 6 510 00 9 994 00 1 900 00 Rent income

CRR 14 Services rendered 9 994 00 9 994 00

003 16 Betty Blue 1 680 00 1 680 00 11 460 00 1 680 00 Commission-income

CRR 25 Services rendered 11 460 00 11 460 00 8 165 00

CRR 30 Services rendered 8 165 00 8 165 00 34 229 00

127 809 00 34 229 00 93 580 00

- 52 -

Cash Payment Journal of Suzie’s Salon – June 2016 CPJ

Doc

D

Name of

beneficiary

Fol Bank Consumables Wages

Sundry

Amount Fol Details

001 1 JJ Beperk 6 440 00 6 440 00 Rent expense

002 Telkom 2 220 00 2 220 00 Telephone

003 2 Cash 600 00 600 00 Float

004 Hanna & Kie 51 900 00 51 900 00 Equipment

005 5 L’Oreal 24 000 00 24 000 00

B/S 7 Outsurance 3 195 00 3 195 00 Insurance

006 Cash 6 000 00 6 000 00

007 11 PNA 901 00 901 00 Stationery

008 14 Cash 6 000 00 6 000 00

B/S 19 Dove & Kie 11 180 00 11 180 00

009 21 Cash 6 100 00 6 100 00

010 28 Cash 6 100 00 6 100 00

011 29 Cash 9 000 00 9 000 00 Drawings

012 Pick ‘n Pay 1 210 00 1 210 00 Consumables

B/S 30 Cyli Marais 7 100 00 7 100 00 Salaries

141 946 00 35 180 00 24 200 00 82 566 00

General Ledger of Suzie’s Salon

Balance sheet section

Capital B1

June 1 Bank CRJ 90 000 00

Drawings B2

June 29 Bank CPJ 9 000 00

Equipment B3

June 2 Bank CPJ 51 900 00

Bank B4

June 30 Total receipts CRJ 127 809 00 June 30 Total Payments CPJ 141 946 00

Balance c/f 14 137 00

177 175 00 177 175 00

Julie 1 Balance b/d 14 137 00

Float B5

June 2 Bank CPJ 600 00

Nominal section

Current income N1

June 30 Bank CRJ 34 229 00

Rent income N2

June 9 Bank CRJ 1 900 00

Commission-income N3

June 16 Bank CRJ 1 680 00

Material costs N4

June 30 Bank CPJ 69 409 00

Wages N5

June 30 Bank CPJ 24 200 00

Rent expense N6

June 1 Bank CPJ 6 440 00

Telephone N7

June 1 Bank CPJ 2 220 00

Insurance N8

June 7 Bank CPJ 3 195 00

Stationery N9

June 11 Bank CPJ 901 00

Consumables N10

June 29 Bank CPJ 1 210 00

Salaries N11

June 30 Bank CPJ 7 100 00

Analyze the following transactions according to the Accounting Equation:

Date General Ledger Accounting Equation

Account

debited

Account

credited

Assets Owner’s

equity

Liabilities

CRJ: 1st Bank Capital +90 000 +90 000

CRJ: 16th Bank Commission-income +1 680 +1 680

CPJ: 2nd Float Bank +600

- 600

CPJ: 2nd Equipment Bank +51 900

- 51 900

CPJ: 29th Drawings Bank - 9 000 - 9 000

CPJ: 29th Consumables Bank - 7 100 - 7 100

Chapter 6: The General Ledger with opening Balances and/or Totals

Activity 38

Cash Receipts Journal of Gogo Salon - September 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

112 3 Diane Gogo

25 000 00 25 000 00

Capital

CRR 12 Services rendered

18 800 00 18 800 00 18 800 00

CRR 18 Services rendered

10 980 00 10 980 00 10 980 00

CRR 25 Services rendered

9 220 00 9 220 00 9 220 00

64 000 00 39 000 00 25 000 00

Cash Payments Journal of Gogo Salon - September 2016 CPJ

Doc

D

Name of

beneficiary

Fol Bank Wages Material cost

Sundry

Amount Fol Details

314 5 Diane Gogo

1 200 00 1 200 00

Drawings

B/S 7 Cash

4 800 00 4 800 00

B/S Sage

3 100 00 3 100 00

Rent expense

315 9 Makro

12 100 00 12 100 00

Equipment

316 14 Cash

4 800 00 4 800 00

B/S Municipality

1 460 00 1 460 00

Water and electricity

317 16 Lanie & Kie

3 160 00 3 160 00

318 21 Cash

4 800 00 4 800 00

319 23 Cash

2 000 00 2 000 00

Drawings

320 25 CNA

610 00 610 00

Stationery

321 28 Cash

4 800 00 4 800 00

B/S 31 ABSA

320 00 320 00

Banking fees

43 150 00 19 200 00 3 160 00 20 790 00

General Ledger of Gogo Salon

Balance sheet section

Capital B1

Sept 1 Balance b/d 100 000 00

3 Bank CRJ 25 000 00

125 000 00

Drawings B2

Sept 1 Balance b/d 6 500 00

5 Bank CPJ 1 200 00

23 Bank CPJ 2 000 00

9 700 00

Equipment B3

Sept 1 Balance b/d 6 500 00

9 Bank CPJ 12 100 00

18 600 00 Bank B4

Sept 1 Balance b/d 6 500 00 Sept 30 Total Payments CPJ 43 150 00

30 Total receipts CRJ 64 000 00 Balance c/f 27 350 00

70 500 00 70 500 00

Oct 1 Balance b/d 27 350 00

Nominal section

Current income N1

Sept 1 Total b/d 123 800 00

30 Bank CRJ 39 000 00

162 800 00

Material costs N2

Sept 1 Total b/d 22 960 00

30 Bank CPJ 3 160 00

26 120 00

Wages N3

Sept 1 Total b/d 24 800 00

30 Bank CPJ 19 200 00

44 000 00

Rent expenses N4

Sept 1 Total b/d 36 400 00

7 Bank CPJ 3 100 00

39 500 00

Water and electricity N5

Sept 1 Total b/d 13 360 00

14 Bank CPJ 1 460 00

14 820 00

Stationery N6

Sept 1 Total b/d 4 320 00

25 Bank CPJ 610 00

4 930 00

Banking fees N7

Sept 1 Total b/d 1 830 00

31 BanK CPJ 320 00

2 150 00

Analyze the following transactions according to the Accounting Equation:

Date General Ledger Accounting Equation

Account debited

Account credited

Assets Owner’s equity

Liabilities

CRJ: 3rd Bank Capital +25 000 +25 000

CRJ: 12th Bank Current income +18 800 +18 800

CPJ: 5th Drawings Bank - 1 200 - 1 200

CPJ: 7th Wages Bank - 4 800 - 4 800

CPJ: 7th Rent expense Bank - 3 100 - 3 100

CPJ: 9th Equipment Bank +12 100

- 12 100

CPJ: 31st Banking fees Bank - 320 - 320

Activity 39

Cash Receipts Journal of Gavin ‘s Plumbers – October 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

195 2 Gavin Hacks

136 000 00 136 000 00

Capital

CRR 14 Services rendered

16 900 00 16 900 00 16 900 00

CRR 21 Services rendered

35 698 00 35 698 00 35 698 00

CRR 30 Services rendered

19 412 00 19 412 00 19 412 00

208 010 00 72 010 00 136 000 00

Cash Payments Journal of Gavin ‘s Plumbers – October 2016 CPJ

Doc

D

Details

Fol Bank Wages Consumables

Sundry

Amount Fol Details

404 3 Diane Gogo

5 400 00 5 400 00

Drawings

B/S 9 Cash

10 500 00 10 500 00

B/S 10 SafeSure

6 200 00 6 200 00

Insurance

405 11 Billies Vehicles

112 100 00 112 100 00

Vehicles

406 16 Cash

10 500 00 10 500 00

B/S Vodacom

2 555 00 2 555 00

Cellphone

407 18 Tersia’s Traders

3 160 00 3 160 00

408 23 Cash

10 500 00 10 500 00

409 25 Cash

12 000 00 12 000 00

Drawings

410 PNA

2 610 00 2 610 00

Stationery

411 30 Cash

10 500 00 10 500 00

B/S Nedbank

120 00 120 00

Banking fees

186 145 00 42 000 00 3 160 00 140 985 00

General Ledger of Gavin ‘s Plumbers

Balance sheet section

Capital B1

Oct 1 Balance b/d 250 000 00

2 Bank CRJ 136 000 00

386 000 00

Drawings B2

Oct 1 Balance b/d 13 450 00

3 Bank CPJ 5 400 00

25 Bank CPJ 12 000 00

30 850 00

Vehicles B3

Oct 1 Balance b/d 95 250 00

11 Bank CPJ 112 100 00

207 350 00

Bank B4

Oct 1 Balance b/d 194 092 00 Oct 31 Total Payments CPJ 186 145 00

31 Total receipts CRJ 208 010 00 Balance c/f 215 957 00

402 102 00 402 102 00

Nov 1 Balance b/d 215 957 00

Nominal section

Current income N1

Oct 1 Total b/d 225 200 00

31 Bank CRJ 72 010 00

297 210 00

Consumables N2

Oct 1 Total b/d 35 210 00

31 Bank CPJ 3 160 00

38 370 00

Wages N3

Oct 1 Total b/d 55 600 00

31 Bank CPJ 42 000 00

97 600 00

Insurance N4

Oct 1 Total b/d 42 000 00

10 Bank CPJ 6 200 00

48 200 00

Cellphone N5

Oct 1 Total b/d 25 698 00

16 Bank CPJ 2 555 00

28 253 00

Stationery N6

Oct 1 Total b/d 12 980 00

25 Bank CPJ 2 610 00

15 590 00

Banking fees N7

Oct 1 Total b/d 920 00

30 Bank CPJ 120 00

1 040 00

Analyze the following transactions according to the Accounting Equation:

Date General Ledger Accounting Equation

Account debited

Account credited

Assets Owner’s equity

Liabilities

CRJ: 2nd Bank Capital +136 000 +136 000

CRJ:

30th

Bank Current income +19 412 +19 412

CPJ: 3rd Drawings Bank - 5 400 - 5 400

CPJ:

10th

Insurance Bank - 6 200 - 6 200

CPJ:

11th

Vehicles Bank +112 100

- 112 100

CPJ:

16th

Wages Bank - 10 500 - 10 500

CPJ:

16th

Cellphone Bank - 2 555 - 2 555

Activity 40

Cash Receipts Journal of Paula’s Playschool – March 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank

Current Income

Sundry

Amount Fol Details

CRR 1 Services rendered

33 250 00 33 250 00 33 250 00

33 13 Paula Plessis

136 000 00 136 000 00 136 000 00

Capital

CRR 14 Services rendered

29 850 00 29 850 00 29 850 00

CRR 31 Services rendered

19 412 00 19 412 00 19 412 00

218 512 00 82 512 00 136 000 00

Cash Payments Journal of Paula’s Playschool – March 2016 CPJ

Doc

D

Name of

beneficiary

Fol Bank Wages Stationery

Sundry

Amount Fol Details

40 5 Cash

6 850 00 6 850 00

B/S 7 Cash

10 000 00 10 000 00

B/S 12 Toys R Us

11 100 00 11 100 00

Equipment

B/S Bouwerke

22 000 00 22 000 00

Land and Buildings

41 14 Cash

6 850 00 6 850 00

B/S 15 Telkom

1 235 00 1 235 00

Telephone

42 16 Pen & Pencil

4 560 00 4 560 00

43 19 Cash

6 850 00 6 850 00

B/S 24 Paula Plessis

13 000 00 13 000 00

Drawings

B/S 25 Municipality

3 510 00 3 510 00

Water and electricity

45 26 Cash

8 000 00 8 000 00

46 30 SA Post Office

99 00 99 00

Postage

94 054 00 28 550 00 14 560 00 50 944 00

General Ledger of Paula’s Playschool

Balance sheet section

Capital B1

Mch 1 Balance b/d 897 084 00

13 Bank CRJ 136 000 00

1 033 084 00

Drawings B2

Mch 1 Balance b/d 136 820 00

24 Bank CPJ 13 000 00

149 820 00

Land and Buildings B3

Mch 1 Balance b/d 995 250 00

12 Bank CPJ 22 000 00

1 017 250 00

Bank B4

Mch 1 Balance b/d 71 042 00 Mch 31 Total Payments CPJ 94 054 00

31 Total receipts CRJ 218 512 00 Balance c/f 195 500 00

289 554 00 289 554 00

April 1 Balance b/d 195 500 00

Equipment B5

Mch 1 Balance b/d 55 000 00

12 Bank CPJ 11 100 00

66 100 00

Nominal section

Current income N1

Mch 1 Total b/d 450 000 00

31 Bank CRJ 82 512 00

532 512 00

Water and electricity N2

Mch 1 Total b/d 24 250 00

25 Bank CPJ 3 510 00

27 760 00

Wages N3

Mch 1 Total b/d 22 987 00

31 Bank CPJ 28 550 00

51 537 00

Telephone N4

Mch 1 Total b/d 5 125 00

15 Bank CPJ 1 235 00

6 360 00

Stationery N5

Mch 1 Total b/d 35 410 00

31 Bank CPJ 14 560 00

49 970 00

Postage N6

Mch 1 Total b/d 1 200 00

30 Bank CPJ 99 00

1 299 00

Answer the following questions on this exercise:

1 What must be written on the 15th in the CRJ in the details column? Services rendered

2 What must be written on the 14th in the CPJ in the name of beneficiary column? Cash

Motivate your answer. The owner cashes a cheque at the bank to pay employees who are on cash

wages.

3 Cheque nr 44 has not been used in the CPJ. Is that a problem? Why / why not?

It will be a problem if the cheque is not in the owner’s possession. It could be that a mistake was

made on the cheque en that it has therefor been cancelled.

4 Give TWO possible reasons why cheque nr 44 does not appear in the CPJ.

Reason 1: A mistake has been made on the cheque and it couldn’t be used.

Reason 2: The cheque was stolen.

5 On the 24th the owner, Paula Plessis was paid a salary of R13 000, but it was recorded as

“Drawings”. It is not a mistake. Why not? Anything (cash or other things) taken from the

business by the owner is drawings.

6 In the CRJ (on the 13th), Paula’s capital contribution is recorded in the analysis of receipts

column. In most of the previous activities this was not the case.

6.1 Explain when the capital contribution will be recorded in the analysis of receipts column.

The owner writes a personal cheque to be deposited in the current account of the business. A receipt

is issued.

6.2 Explain when the capital contribution will not be written in the analysis of receipts column.

The owner does an electronic (internet) transfer directly from his personal account to the current

account of the business.

7 Why do businesses prefer to receive funds electronically and to make their payments

electronically? It is easy to check electronic transactions on the bank statement. It is a relatively

safe method.

Chapter 7: Trial Balance

Activity 41

Trial Balance of Tenpin Bowling Club on 30 April 2016

Fol Debit Credit

Balance sheet section

Capital B1 150 000

Drawings B2 1 100

Equipment B3 65 000

Bank B4 58 132

Float B5 500

Nominal section

Current income N1 41 450

Material costs N2 15 900

Wages N3 32 000

Rent expenses N4 4 500

Telephone N5 2 100

Consumables N6 1 498

Water and electricity N7 2 280

Salaries N8 8 440

191 450 191 450

Activity 42

Trial Balance of Salon Maria on 31 May 2016

Fol Debit Credit

Balance sheet section

Capital B1 190 955

Drawings B2 24 980

Vehicles B3 95 000

Equipment B4 135 900

Bank B5 9 460

Petty cash B6 800

Float B7 300

Nominal section

Current income N1 460 000

Stationery N2 3 100

Insurance N3 14 900

Telephone N4 7 845

Wages N5 102 000

Commission Income N6 6 130

Rent expense N7 36 000

Material costs N8 42 800

Salaries N9 184 000

657 085 657 085

Activity 43

Trial Balance of Timothy’s Garden Service on 31 Augustus 2016

Fol Debit Credit

Balance sheet section

Capital B1 400 000

Drawings B2 42 900

Land and Buildings B3 800 000

Equipment B4 69 200

Mortgage Loan B5 500 000

Fixed deposit: Citibank B6 10 000

Bank B7 5 192

Float B8 500

Nominal section

Current income N1 348 000

Advertising N2 3 990

Rent expense N3 66 000

Wages N4 64 000

Material costs N5 47 924

Salaries N6 72 240

Stationery N7 3 154

Telephone N8 18 240

Insurances N9 19 060

Water and electricity N10 25 600

1 248 000 1 248 000

Activity 44

Trial Balance of Great Gardens on 31 July 2016

Fol Debit Credit

Balance sheet section

Capital B1 1 450 000

Drawings B2 102 000

Land and Buildings B3 600 000

Vehicles B4 85 000

Equipment B5 1 200 000

Bank B6 6 432

Petty cash B7 600

Mortgage Loan: FNB B8 300 000

Fixed deposit: Absa B9 5 000

Creditor’s control B10 5 440

Debtor’s control B11 17 147

Nominal section

Current income N1 698 099

Water and electricity N2 23 996

Insurance N3 25 200

Consumables N4 4 440

Telephone N5 11 400

Stationery N6 3 160

Salaries N7 292 000

Interest on Mortgage Loan N8 36 000

Wages N9 68 000

Commission Income N10 15 000

Rent income N11 14 400

Repairs and maintenance N12 2 564

2 482 939 2 482 939

Activity 45

Trial Balance of Nixie Dixie Dealers on 30 April 2016

Fol Debit Credit

Balance sheet section

Capital B1 390 195

Drawings B2 10 730

Vehicles B3 320 000

Equipment B4 287 000

Bank B5 9 959

Loan: Absa Bank B6 96 000

Nominal section

Current income N1 446 000

Insurance N2 12 000

Material costs N3 5 000

Rent expense N4 72 000

Interest on loan N5 1 800

Repairs and maintenance N6 31 582

Salaries N7 95 000

Telephone N8 6 250

Water and electricity N9 27 891

Stationery N10 13 725

Wages N11 39 258

932 195 932 195

Chapter 8: Financial Statements

Activity 46

Statement of Comprehensive Income of Urban Sport Club for the year ended 28 February 2016

Current Income 698 090

Other income 29 400

Rent income 14 400

Commission Income 15 000

Gross operating income 727 490

Minus: Operating Expenses: (466 760)

Insurance 25 200

Wages 68 000

Salaries 292 000

Stationery 3 160

Consumables 4 440

Telephone 11 400

Water and electricity 23 996

Repairs and maintenance 2 564

Advertising 36 000

Nett profit for the year 260 730

Statement of Financial Position of Urban Sport Club on 28 February 2016

ASSETS Notes

Non-Current assets 1 890 000

Tangible Assets 1 1 885 000

Fixed Deposit: Absa 5 000

Current assets 24 170

Trade and other receivables 17 147

Cash and cash equivalents 2 7 023

TOTAL ASSETS 1 914 170

EQUITY AND LIABILITIES

Owner’s equity 3 1 608 730

Non current Liabilities 300 000

Mortgage Loan: FNB 300 000

Current liabilities 5 440

Trade and other payables 5 440

TOTAL EQUITY AND LIABILITIES 1 914 170

Notes to the Statement of Financial Position

1 Tangible Assets:

Land and Buildings 600 000

Equipment 1 200 000

Vehicles 85 000

1 885 000

2 Cash and cash equivalents

Bank 6 423

Petty cash 600

7 023

3 Owner’s equity:

Capital at the beginning of the year 1 450 000

Nett profit for the year 260 730

Drawings (102 000)

Capital at the end of the year 1 608 730

Activity 47

Statement of Comprehensive Income of Rikus Rekenmeester (Accountant) for the year ending

30 June 2016

Current Income 610 000

Other income 25 900

Commission Income 25 900

Gross operating income 635 900

minus Operating Expenses: (535 554)

Stationery 5 900

Insurance 18 200

Wages 62 000

Consumables 6 154

Water and electricity 10 800

Rent expense 91 900

Telephone 28 600

Salaries 312 000

Nett profit for the year 100 346

Statement of Financial Position of Rikus Rekenmeester (Accountant) on 30 June 2016

ASSETS Notes

Non-Current assets 212 000

Tangible Assets 1 212 000

Current assets 75 115

Trade and other receivables 61 000

Cash and cash equivalents 2 14 115

Total Assets 287 115

EQUITY AND LIABILITIES

Owner’s equity 3 230 115

Non current liabilities 25 000

Loan: Nedbank 25 000

Current liabilities 32 000

Trade and other payables 32 000

Total Equity and Liabilities 287 115

Notes to the Statement of Financial Position

1 Tangible Assets:

Vehicles 121 000

Equipment 91 000

212 000

2 Cash and Cash equivalents

Bank 14 115

14 115

3 Owner’s equity:

Capital at the beginning of the year 273 769

Nett profit for the year 100 346

Drawings (144 000)

230 115

Activity 48

Statement of Comprehensive Income of Scott-Droogskoonmakers (Dry Cleaners) for the year ending 28

February 2016

Current Income 618 810

Other income -

-

Gross operating income 618 810

Operating Expenses: (447 700)

Insurance 8 500

Wages 38 440

Material costs 51 970

Salaries 165 000

Rent expense 59 950

Telephone 18 040

Water and electricity 24 210

Stationery 33 760

Advertising 18 000

Repairs and maintenance 29 830

NETT PROFIT FOR THE YEAR 171 110

Statement of Financial Position of Scott-Droogskoonmakers (Dry-Cleaners) on 28 February 2016

ASSETS Notes

Non-Current assets 537 000

Tangible Assets 1 537 000

Current assets

Trade and other receivables -

Cash and cash equivalents 2 26 000

TOTAL ASSETS 563 000

EQUITY AND LIABILITIES

Owner’s equity 3 463 000

Non current Liabilities 100 000

Loan: Absa Bank 100 000

Current liabilities -

Trade and other payables -

TOTAL EQUITY AND LIABILITIES 563 000

Notes to the Statement of Financial Position

1 Tangible Assets:

Vehicles 250 000

Equipment 287 000

537 000

2 Cash and cash equivalents

Bank 26 000

26 000

3 Owner’s equity:

Capital at the beginning of the year 391 890

Nett profit for the year 171 110

Drawings (100 000)

Capital at the end of the year 463 000

Activity 49

Statement of Comprehensive Income of Jumping Jack for the year ending

28 February 2016

Current Income 420 125

Other income 36 449

Commission income 36 449

Gross operating income 456 574

Operating Expenses: (356 675)

Stationery 1 894

Insurance 35 120

Telephone 11 412

Wages 55 200

Rent expense 44 555

Material costs 12 258

Salaries 196 236

Nett profit for the year 99 899

Statement of Financial Position of Jumping Jack on 28 February 2016

ASSETS Notes

Non-Current assets 297 974

Tangible Assets 1 297 974

Current assets 165 345

Trade and other receivables -

Cash and cash equivalents 2 165 345

TOTAL ASSETS 463 319

EQUITY AND LIABILITIES

Owner’s equity 3 463 319

Non current Liabilities

-

Current liabilities

Trade and other payables -

TOTAL EQUITY AND LIABILITIES 463 319

Notes to the Statement of Financial Position

1 Tangible Assets:

Vehicles 203 320

Equipment 94 654

297 974

2 Cash and cash equivalents

Bank 163 095

Petty cash 950

Float 1 300

165 345

3 Owner’s equity:

Capital at the beginning of the year 400 000

Nett profit for the year 99 899

Drawings (36 580)

Capital at the end of the year 463 319

Activity 50

Statement of Comprehensive Income of Riets-Herstellers for the year ending 28 February 2016

Current income 439 770

Operating Expenses: (254 839)

Trading licence 1 760

Stationery 2 054

Wages 86 539

Telephone 12 490

Fuel 11 337

Material costs 44 660

Water and electricity 21 130

Insurance 9 870

Salaries 65 000

Nett profit for the year 184 931

Statement of Financial Position of Riets-Hestellers on 28 February 2016

ASSETS Notes

Non-Current assets

Tangible Assets 1 941 375

Current assets 20 850

Trade and other receivables -

Cash and cash equivalents 2 20 850

TOTAL ASSETS 962 225

EQUITY AND LIABILITIES

Owner’s equity 3 462 225

Non current liabilities 500 000

Mortgage Loan 500 000

Current liabilities -

Trade and other payables -

TOTAL EQUITY AND LIABILITIES 962 225

Notes to the Statement of Financial Position

1 Tangible Assets:

Land and Buildings 800 000

Vehicles 92 500

Equipment 48 875

941 375

2 Cash and cash equivalents

Bank 20 850

20 850

3 Owner’s equity:

Capital at the beginning of the year 312 999

Nett profit for the year 184 931

Drawings (35 705)

462 225

Chapter 9: Trading business

Activity 51

Calaulate the selling price. Show your calculations:

Cost

price

Profit

margin

Selling price Calculations

1 R 800 100 % R1 600 800 x 200 % (800 x 100 % = 800 + 800 = R1 600)

2 R 25 25 % R31,25 25 x 125 % (25 x 25 % = 6,25 + 25 = R31,25

3 R 3 100 75 % R5 425 3 100 x 175 % (3 100 x 75 % = 2 325 + 3 100)

4 R 700 50 % R1 050 700 x 150 % (700 x 50 % = 350 + 700)

5 R 150 150 % R375 150 x 250 % (150 x 150 % = 225 + 150)

6 R 610 14 % R695,40 610 x 114 % (610 x 14 % = 85,40 + 610)

7 R12 900 175 % R35 475 12 900 x 275 % (12 900 x 175 % = 22 575 + 12 900)

8 R 99 33⅓ % R132 99 x 133,333 % (99 x 33⅓ % = 33 + 99)

9 R 120 66⅔ % R200 120 x 166,666 % (120 x 66⅔ % = 80 + 120)

10 R 4 800 250 % R16 800 4 800 x 350 % (4 800 x 250 % = 12 000 + 4 800)

11 R 100 300% R400 100 x 400 % (100 x 300 % = 300 + 100)

12 R 99,95 125 % R224,89 99,95 x 225 % (99,95 x 125 % = 124,94 + 99,95)

13 R 9 250 20 % R11 100 9 250 x 120% (9250 x 20 % = 1 850 + 9 250)

14 R 12,50 125 % R28,13 12,50 x 225 % (12,50 x 125 % = R15,63 + 12,50)

15 R 8 300 100 % R16 600 8 300 x 200 % (8 300 x 100 % = 8 300 + 8 300)

16 R 1 000 60 % R1 600 1 000 x 160 % (1 000 x 60 % = 600 + 1 000)

17 R 220 10 % R242 220 x 110 % (220 x 10 % = 22 + 220)

18 R 15 50 % R22,50 15 x 150 % (15 x 50 % = 7,50 + 15)

19 R 16,40 25 % R20,50 16,40 x 125 % (16,40 x 25 % = 4,10 + 16,40)

20 R200,50 200 % R601,50 200,50 x 300 % (200,50 x 200 % = 401 + 200,50

Activity 52

Complete the table:

Cost

price

Percentage

profit on cost

price

Profit in

Rand

Selling price Calculations

R900 100 % *R900 *R1 800 900 x 200 %

*R1 000 50 % *R500 R1 500 1 500 x 100/150

R600 75 % *R450 *R1 050 600 x 75 % = 450 + 600

*R800 150 % *R1 200 R2 000 2 000 x 100/250

R750 *33⅓ % R250 *R1 000 250/750 x 100

*R1 500 200 % R3 000 *R4 500 3 000 x 100/200

R210 125 % *R262,50 *R472,50 210 x 225 %

*R400 *50 % R200 R600 600 – 200 (200/400 x 100)

R580 25 % *R145 *R725 580 x 25 %

R320 *50 % *R160 R480 480 – 320 (160/320 x 100)

Activity 53

Cash Receipts Journal of Rooi Handelaars (Traders) - July 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank Sales Cost of sales

Sundry

Amount Fol Details

001 1 Vian Rooi 75 000 00 75 000 00 Capital

CRR 7 Sales 1 860 00 1 860 00 930 00

002 J. Blou 2 100 00 3 960 00 2 100 00 Rent income

CRR 12 Sales 6 320 00 6 320 00 6 320 00 3 160 00

003 15 Vian Rooi 50 000 00 50 000 00 50 000 00 Capital

B/S 21 Absa 62 00 62 00 Interest on current account

CRR 22 Sales 4 580 00 4 580 00 4 580 00 2 290 00

CRR 31 Sales 12 900 00 12 900 00 6 450 00

152 822 00 26 660 00 12 830 00 127 162 00

General Ledger of Rooi Handelaars (Traders)

Balance sheet section

Trading inventory B6

July 01 Balance b/d 75 000 00 July 31 Cost of sales CRJ 12 830 00

Balance c/f 62 170 00

75 000 00 75 000 00

Aug 01 Balance b/d 62 170 00

Nominal section

Sales N1

July 31 Bank CRJ 26 660 00

Cost of sales N2

July 31 Trading inventory CRJ 12 830 00

Activity 54

Nr Account

debited

Account

credited

Assets Owner’s equity Liabilities

Debit Credit Debit Credit Debit Credit

1 Trading inventory Bank 15 600 15 600

2 Bank Sales 8 500 8 500

Cost of sales Trading

inventory

4 250 4 250

Activity 55

Cash Receipt Journal of Bobo Handelaars - October 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank Sales Cost of sales

Sundry

Amount Fol Details

001 1 Tom Bobo 100 000 00 100 000 00 100 000 00 Capital

CRR 8 Sales 8 700 00 8 700 00 8 700 00 5 800 00

CRR 11 Sales 12 900 00 12 900 00 8 600 00

002 Tom Bobo 50 000 00 62 900 00 50 000 00 Capital

CRR 25 Sales 14 700 00 14 700 00 14 700 00 9 800 00

186 300 00 36 300 00 24 200 00 150 000 00

B7 N1 B6/N2

Cash Payments Journal of Bobo Handelaars - October 2016 CPJ

Doc

D

Details

Fol Bank Wages

Trading inventory

Sundry

Amount Fol Details

001 2 Hertz 35 900 00 35 900 00 Equipment

002 3 Trek & Bros 45 600 00 45 600 00

003 Waltons 4 960 00 4 960 00 Stationery

004 Hoover Ltd 13 900 00 13 900 00 Rent expense

005 5 Cash 500 00 500 00 Float

006 6 Cash 6 100 00 6 100 00

007 Caxton Ltd 8 195 00 2 280 00 Advertising

5 915 00 Packaging

008 13 Cash 6 100 00 6 100 00

B/S AB Wholesalers 28 600 00 28 600 00

009 15 Tom Bobo 8 000 00 8 000 00 Drawings

010 Municipality 1 200 00 1 200 00 Water and electricity

011 18 Sanlam 1 890 00 1 890 00 Insurance

012 Makro 9 800 00 9 800 00 Equipment

013 The Beeld 6 800 00 6 800 00 Advertising

014 20 Cash 6 100 00 6 100 00

015 27 Cash 6 100 00 6 100 00

B/S Tracy Bothma 6 320 00 6 320 00 Salaries

B/S Sally Katz 5 100 00 5 100 00 Salaries

201 165 00 24 400 00 74 200 00 102 565 00

General Ledger of Bob Traders

Balance sheet section

Trading inventory B6

Oct 31 Bank CPJ 74 200 00 Oct 31 Cost of sales CRJ 24 200 00

Balance c/f 50 000 00

74 200 00 74 200 00

Nov 1 Balance b/d 50 000 00

Bank B7

Oct 31 Total receipts CRJ 186 300 00 Oct 31 Total Payments CPJ 201 165 00

Balance c/f 14 865 00

201 165 00 201 165 00

Nov 1 Balance b/d 14 865 00

Nominal section

Sales N1

Oct 31 Bank CRJ 36 300 00

Cost of sales N2

Oct 31 Trading inventory CRJ 24 200 00

Activity 56

Cash Receipts Journal of Toto Wholesalers - October 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts

Bank Sales Cost of sales

Sundry

Amount Fol Details

01 1 Pieter Toto 400 000 00 400 000 00 400 000 00 Capital

02 5 Cash 2 100 00 2 100 00 2 100 00 Commission income

CRR 6 Sales 19 800 00 19 800 00 19 800 00 9 900 00

CRR 11 Sales 26 900 00 26 900 00 26 900 00 13 450 00

CRR 19 Sales 15 760 00 15 760 00 15 760 00 7 880 00

03 24 Cash 4 900 00 4 900 00 4 900 00 Commission income

CRR 25 Sales 18 440 00 18 440 00 18 440 00 9 220 00

CRR 31 Sales 22 510 00 22 510 00 22 510 00 11 255 00

510 410 00 103 410 00 51 705 00 407 000 00

B7 N1 B6/N2

Cash Payments Journal of Toto Wholesalers – October 2016 CPJ

Doc

D

Details

Fol Bank Wages

Trading inventory

Sundry

Amount Fol Details

001 2 Ford Motors 115 000 00 115 000 00 Vehicles

002 Fox Manufacturers 190 000 00 190 000 00

B/S 3 Outsurance 2 610 00 2 610 00 Insurance

003 4 Sanlam Ltd 10 900 00 10 900 00 Rent expense

004 5 Municipality 3 120 00 3 120 00 Water and electricity

005 6 Cash 4 100 00 4 100 00

006 8 Pick ‘n Pay 822 00 822 00 Consumables

007 15 Balance 625 00 625 00 Fuel

008 Cash 4 100 00 4 100 00

009 19 Telkom 1 930 00 1 930 00 Telephone

010 Vodacom 747 00 747 00 Drawings

011 25 Cash 4 100 00 4 100 00

B/S 26 Joe Black 9 155 00 9 155 00 Salaries

012 30 Waltons 1 348 00 1 348 00 Stationery

348 557 00 12 300 00 190 000 00 146 257 00

B7 B6

General Ledger of Toto Groothandelaars (Wholesalers)

Balance sheet section

Trading inventory B6

Oct 31 Bank CPJ 190 000 00 Oct 31 Cost of sales CRJ 51 705 00

Balance c/f 138 295 00

190 000 00 190 000 00

Nov 1 Balance b/d 138 295 00

Bank B7

Oct 31 Total receipts CRJ 510 410 00 Oct 31 Total Payments CPJ 348 557 00

Balance c/f 161 853 00

510 400 00 510 400 00

Nov 1 Balance b/d 161 853 00

Nominal section

Sales N1

Oct 31 Bank CRJ 103 410 00

Cost of sales N2

Oct 31 Trading inventory CRJ 51 70 00

Activity 57

Cash Receipts Journal of Bilbao Traders - October 2016 CRJ

Doc

D

Details

Fol

Analysis of receipts