“changes in propane supply - muse, stancil & co.€¦ · minnesota propane supply ... another...

TRANSCRIPT

“CHANGES IN U.S. PROPANE SUPPLY”

Presented by:

Ajey ChandraMuse, Stancil & Co.

January 21, 2015

2

MUSE, STANCIL & CO. Independent energy consulting firm founded in 1984, providing industry

expertise from wellhead to end-user; www.musestancil.com

Energy Sectors Served– Crude Oil– Refining – Refined Products– Natural Gas– Natural Gas Liquids– Petrochemicals– Biofuels– Power/Cogeneration

Representative Assignments– Market Studies– Project Development– Transactional Due

Diligence– Insurance Claims

(Property & Business Interruption)

– Contract Negotiation/Dispute Resolution

Energy Sectors Served– Crude Oil– Refined Products– Natural Gas Liquids– Power/Cogeneration

– Refining – Natural Gas– Petrochemicals– Biofuels

– Litigation Support– Asset Valuation– New Technology

Assessment– Royalty

Negotiation/Auditing

3

AGENDA How the Shale Revolution is changing the NGL landscape in North America

Current and Projected Propane Production

Minnesota Propane Supply– Where does it come from – How does it get to here

Export markets and their effect on propane markets

Impact of the Panama Canal Expansion

4

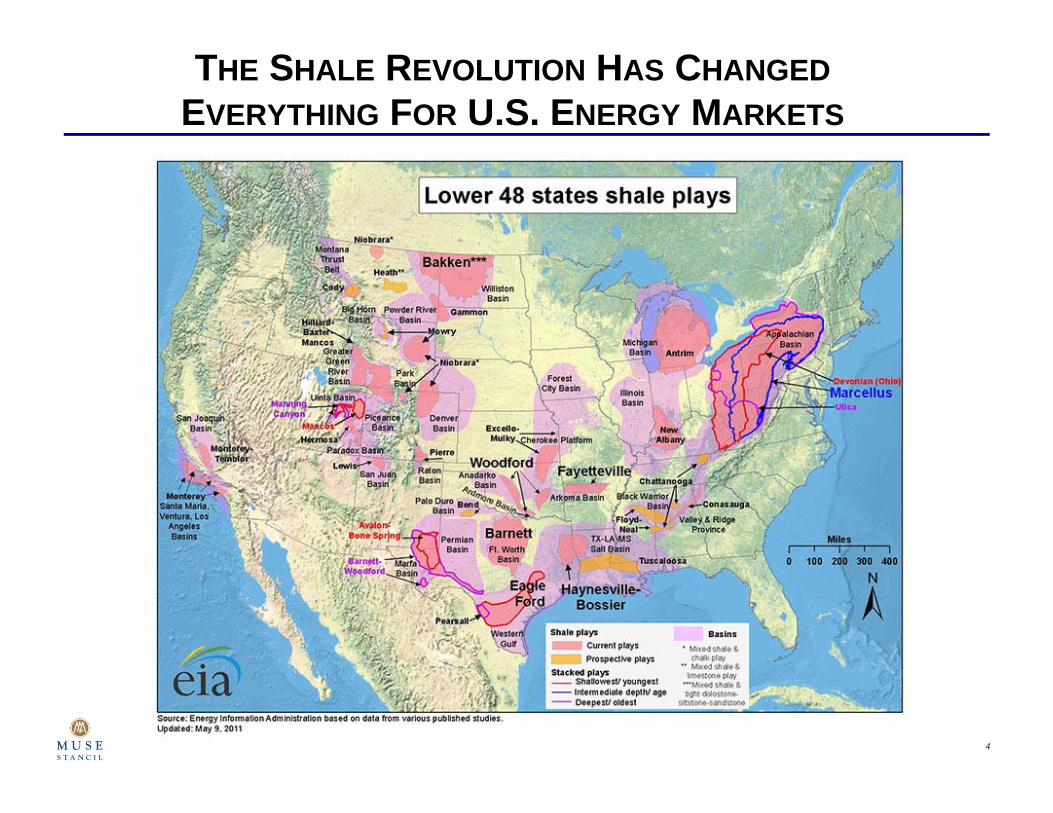

THE SHALE REVOLUTION HAS CHANGEDEVERYTHING FOR U.S. ENERGY MARKETS

5

U.S. GAS PRODUCTION FORECASTS HAVE CHANGED

Source: EIA

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

Trillion Cu

bic Feet

2009 Dry Gas Production Forecast 2014 Dry Gas Production Forecast

6

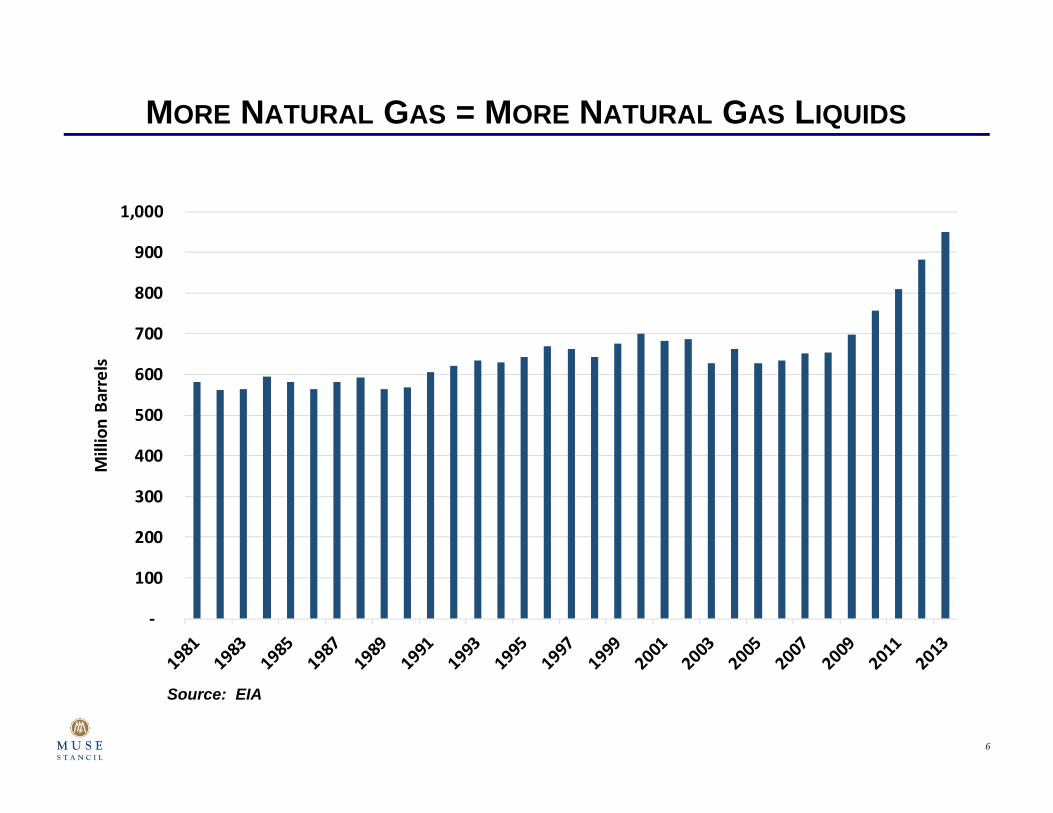

MORE NATURAL GAS = MORE NATURAL GAS LIQUIDS

Source: EIA

‐

100

200

300

400

500

600

700

800

900

1,000

Million Ba

rrels

7

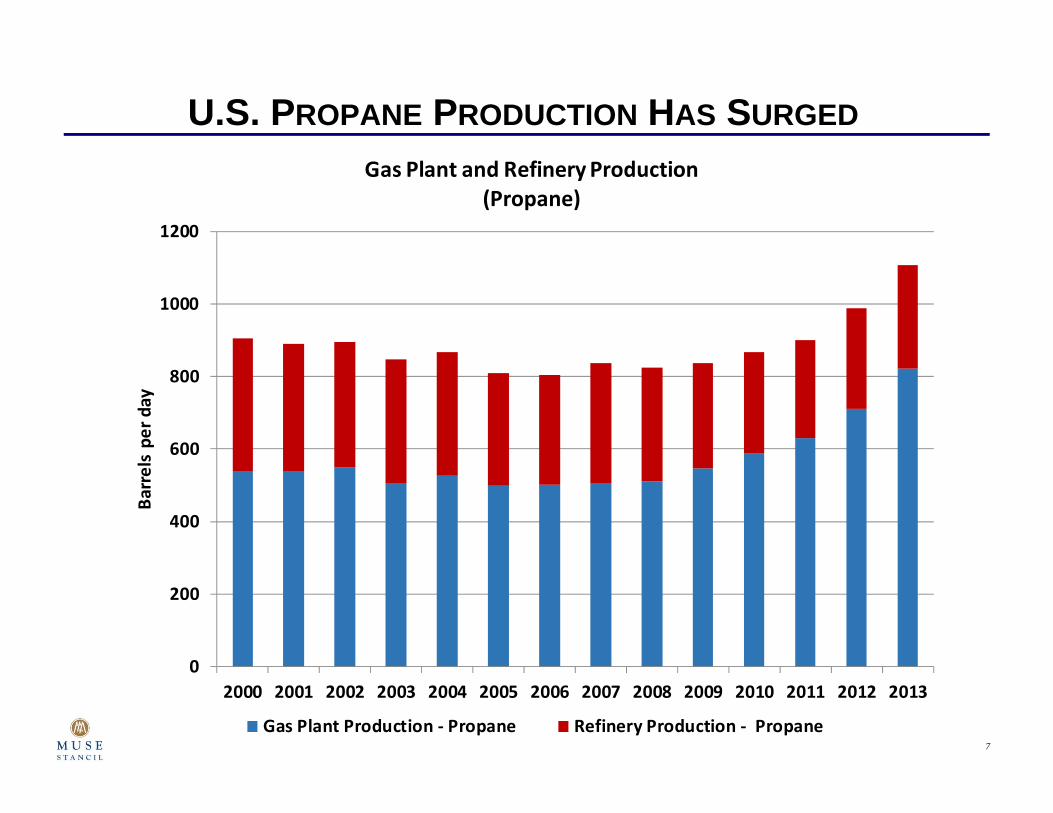

U.S. PROPANE PRODUCTION HAS SURGED

0

200

400

600

800

1000

1200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Barrels pe

r day

Gas Plant and Refinery Production (Propane)

Gas Plant Production ‐ Propane Refinery Production ‐ Propane

8

U.S. GAS PLANT PROPANE PRODUCTIONCONTINUES TO GROW

0

200

400

600

800

1000

1200

1400Jan‐2010

Mar‐201

0

May

‐201

0

Jul‐2

010

Sep‐2010

Nov

‐201

0

Jan‐2011

Mar‐201

1

May

‐201

1

Jul‐2

011

Sep‐2011

Nov

‐201

1

Jan‐2012

Mar‐201

2

May

‐201

2

Jul‐2

012

Sep‐2012

Nov

‐201

2

Jan‐2013

Mar‐201

3

May

‐201

3

Jul‐2

013

Sep‐2013

Nov

‐201

3

Jan‐2014

Mar‐201

4

May

‐201

4

Jul‐2

014

Sep‐2014

Thou

sand

Barrels pe

r Day

Refinery and Gas Plant Propane Production

Refineries Gas Plants

9

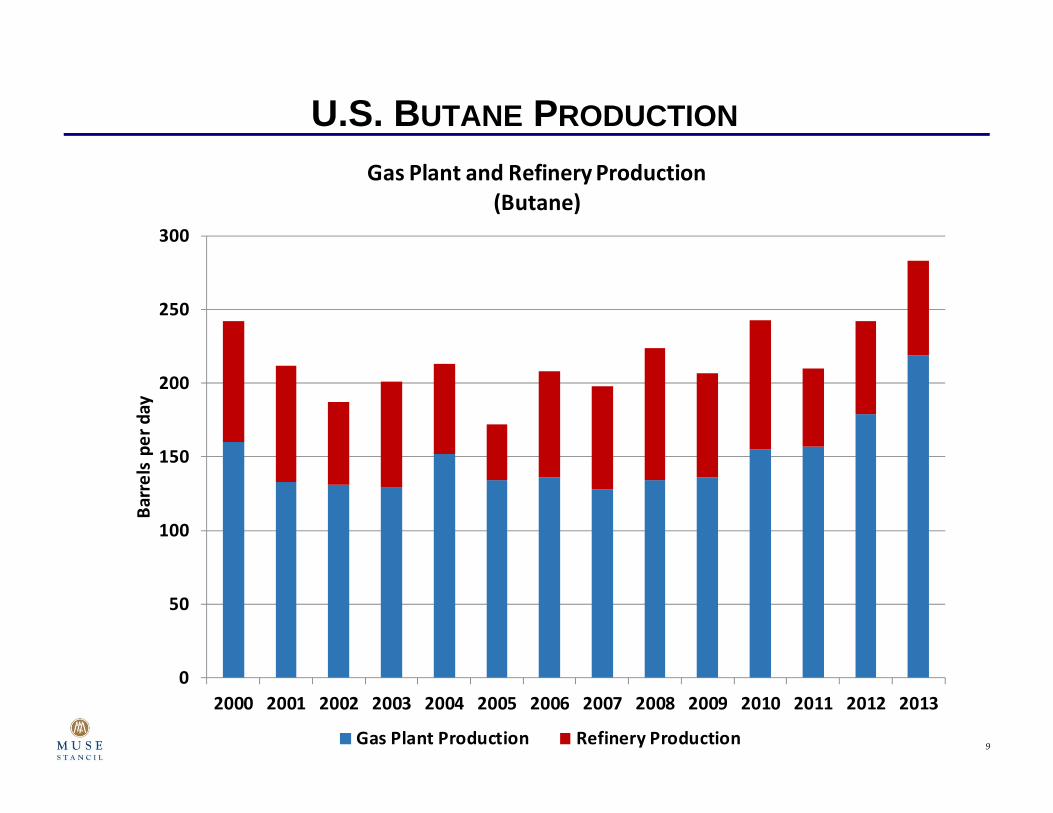

U.S. BUTANE PRODUCTION

0

50

100

150

200

250

300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Barrels pe

r day

Gas Plant and Refinery Production (Butane)

Gas Plant Production Refinery Production

10

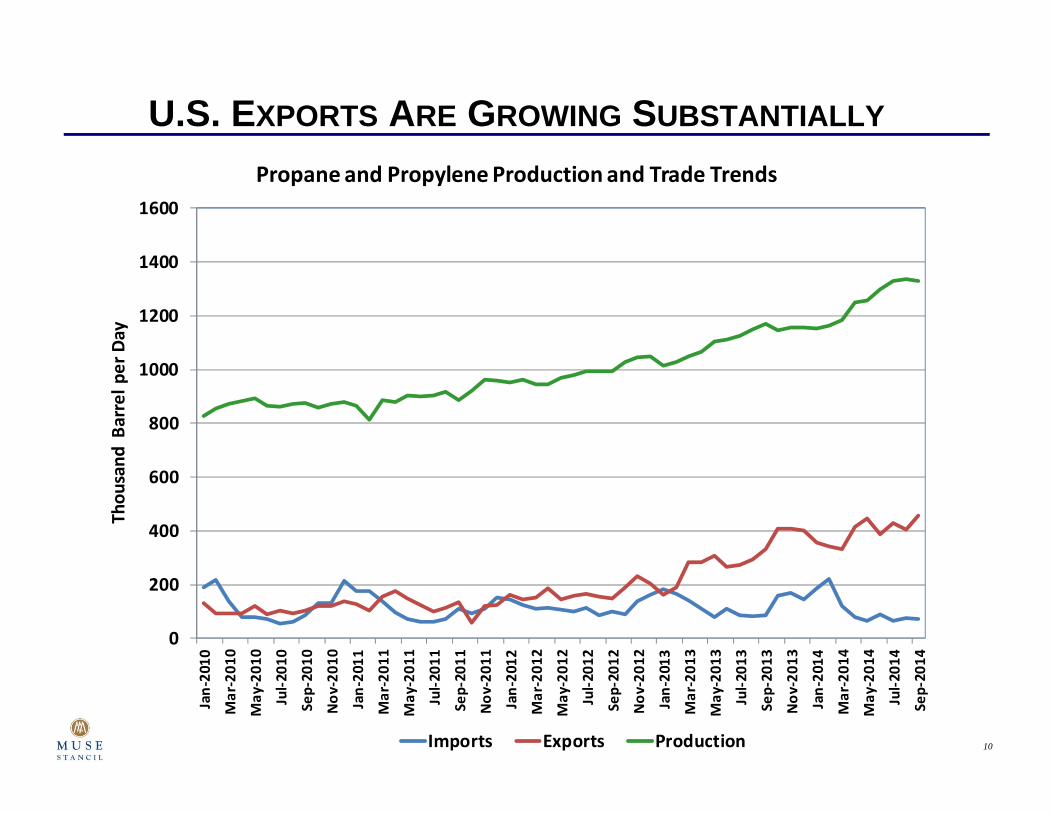

U.S. EXPORTS ARE GROWING SUBSTANTIALLY

0

200

400

600

800

1000

1200

1400

1600Jan‐2010

Mar‐201

0

May

‐201

0

Jul‐2

010

Sep‐2010

Nov

‐201

0

Jan‐2011

Mar‐201

1

May

‐201

1

Jul‐2

011

Sep‐2011

Nov

‐201

1

Jan‐2012

Mar‐201

2

May

‐201

2

Jul‐2

012

Sep‐2012

Nov

‐201

2

Jan‐2013

Mar‐201

3

May

‐201

3

Jul‐2

013

Sep‐2013

Nov

‐201

3

Jan‐2014

Mar‐201

4

May

‐201

4

Jul‐2

014

Sep‐2014

Thou

sand

Barrel p

er Day

Propane and Propylene Production and Trade Trends

Imports Exports Production

11

Mont Belvieu

Hobbs

Conway

NM

TXLA

MSAL

AR

GA

FL

SC

TN

KY

NC

VAWV

PA

NJ

NY

ME

VT

NH

MACT RI

OHIN

IL

MO

WIMI

MN

ND

SDWY

CO

NE

KS

MT

MD DE

OK

KANEBOverland PassONEOKMAPL

NGL Pipelines

DCP Sand Hills

ArbuckleSterling IIISterling I & IIONEOK BakkenMariner EastMariner WestMAPL (Rockies)Seminole

CentennialTEPPCO

U.S. DISTRIBUTION INFRASTRUCTURECONTINUES TO EXPAND

12

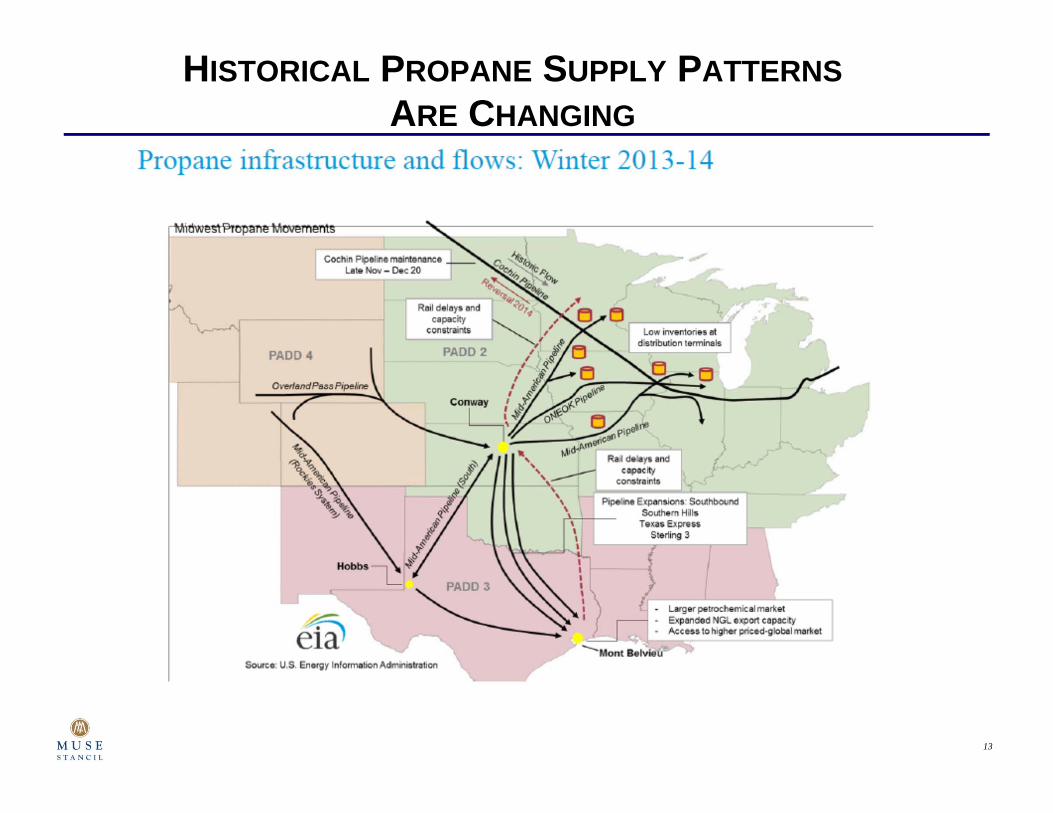

PROPANE DISTRIBUTION FLOWS

13

HISTORICAL PROPANE SUPPLY PATTERNSARE CHANGING

14

2014 SUPPLY INFRASTRUCTURE HAS CHANGED

15

Mont Belvieu

Hobbs

Conway

NM

TXLA

MSAL

AR

GA

FL

SC

TN

KY

NC

VAWV

PA

NJ

NY

ME

VT

NH

MACT RI

OHIN

IL

MO

WIMI

MNND

SDWY

CO

NE

KS

MT

MD DE

OK

KANEBOverland PassONEOKMAPL

NGL Pipelines

DCP Sand Hills

ArbuckleSterling IIISterling I & IIONEOK BakkenMariner EastMariner WestMAPL (Rockies)Seminole

CentennialTEPPCO

Carrington

New Hampton

Hannaford

Fairmont BensonRockville

Glenwood

Mankato Hixton

Iowa City Clinton Channahon

Milford

Sarnia

Rapid River

Superior

Tioga/BakkenGas Processors

Former Cochin TerminalDepropanizerRail Loading (fractionator or processor

Market hubRail Unloading (new or expanding)

Y‐grade Pipeline Flow

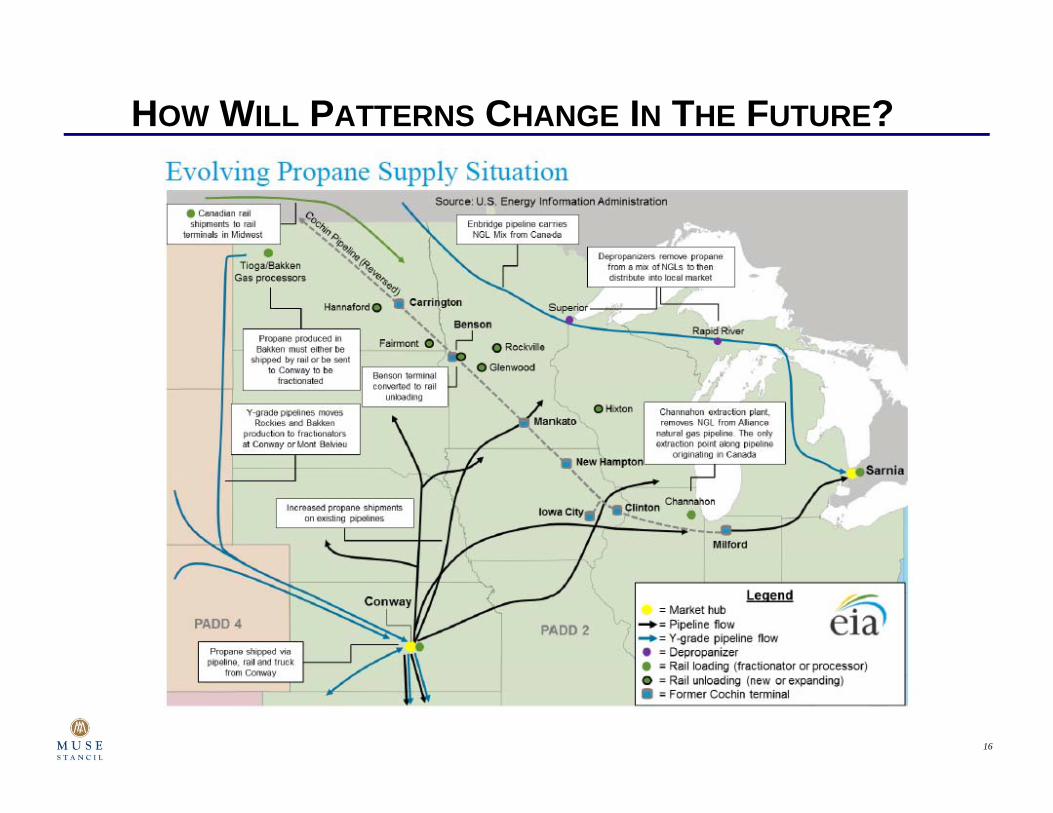

PROPANE DISTRIBUTION INFRASTRUCTURE

16

HOW WILL PATTERNS CHANGE IN THE FUTURE?

17

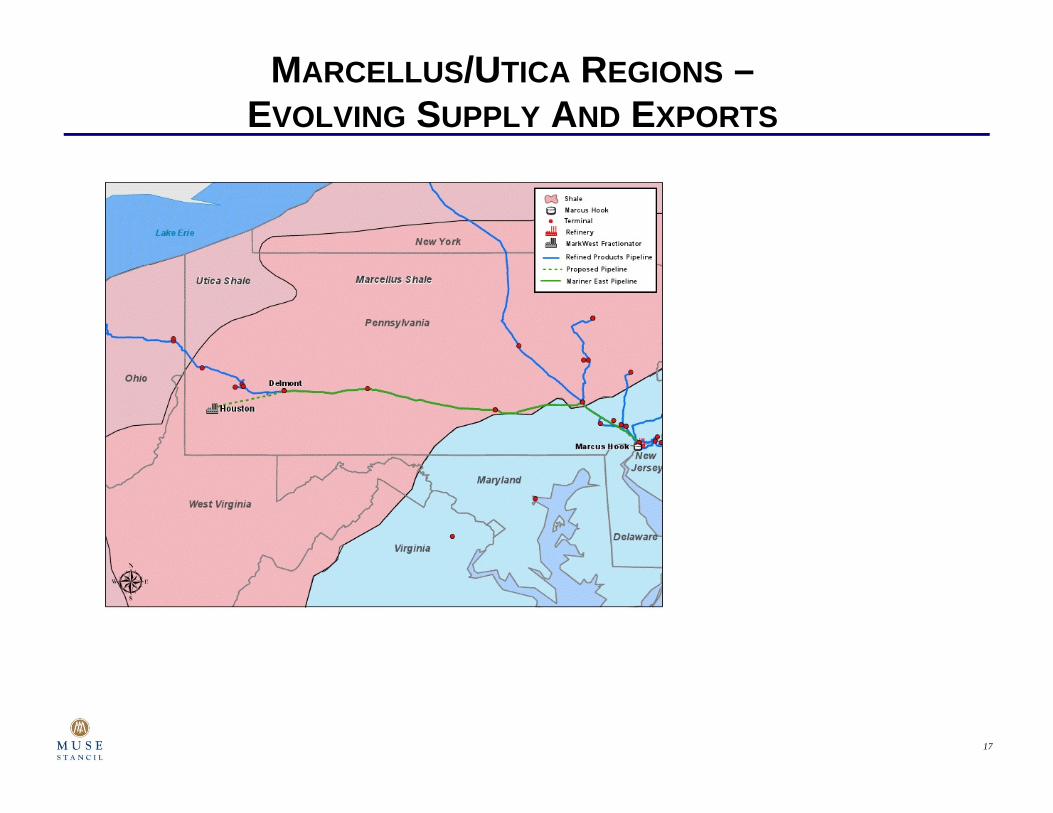

MARCELLUS/UTICA REGIONS –EVOLVING SUPPLY AND EXPORTS

18

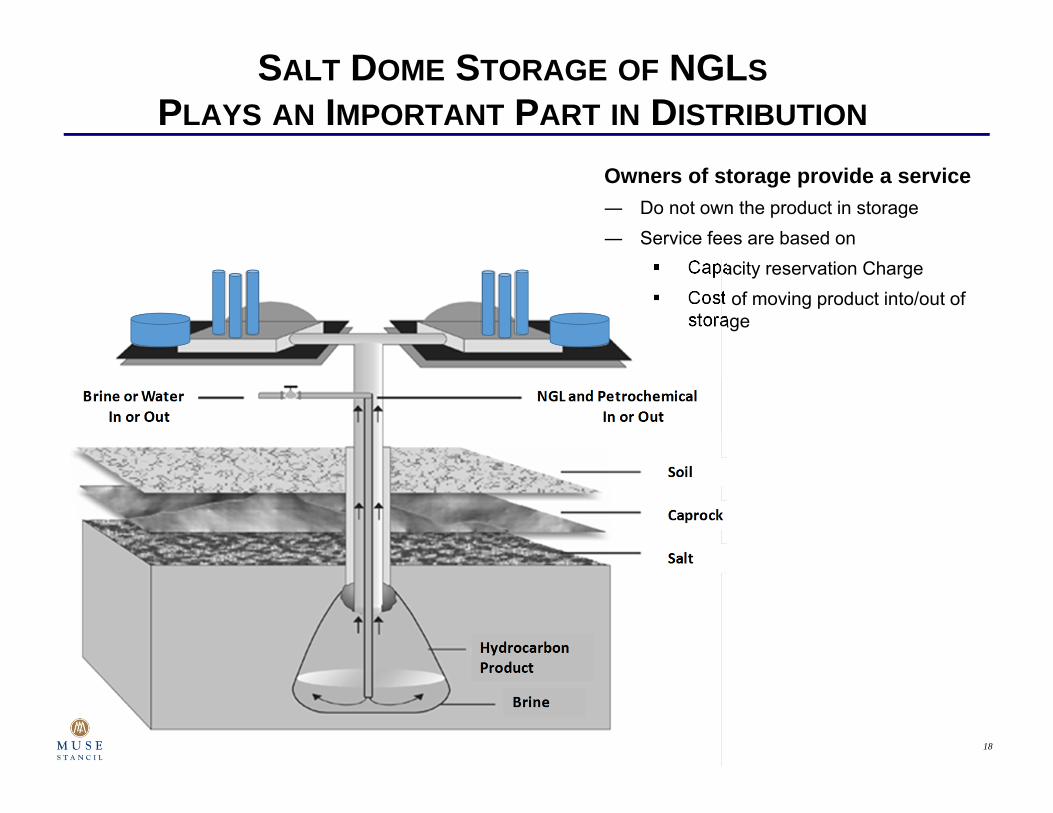

SALT DOME STORAGE OF NGLSPLAYS AN IMPORTANT PART IN DISTRIBUTION

Owners of storage provide a service― Do not own the product in storage― Service fees are based on

Capacity reservation Charge Cost of moving product into/out of

storage

19

ALLOCATION OF PRODUCT Why do pipelines go on “allocation”

– Need to balance supply and demand

What does this mean for the propane distributor– Why can’t you get all the propane that you need when you need it?

Who determines how much propane you get?– Key elements of pipeline allocation

What is the total capacity of the system? When capacity is limited, what is a “fair” way to distribute this capacity? Who has paid for the capacity? Who has historically used the capacity? What about “new” shippers

Will rail shipments play a larger role in the future?

20

EIA – U.S. NATURAL GAS LIQUIDS FORECAST

‐

200

400

600

800

1,000

1,20019

8119

8319

8519

8719

8919

9119

9319

9519

9719

9920

0120

0320

0520

0720

0920

1120

1320

1520

1720

1920

2120

2320

2520

2720

2920

3120

3320

3520

3720

39

Million Ba

rrels

Actual Production 2014 Forecast

Source: EIA

21

INCREASE IN PDH PLANTS WILL ABSORBPROPANE PRODUCTION

As more petrochemical producers have switched to ethane for ethylene production, the amount of propylene produced has been reduced

Propylene consumption continues to grow faster than GDP growth

Another method for propylene production is propane dehydrogenation (PDH)

Multiple PDH plants are being constructed in the U.S.

This will provide a growing use for “excess” propane in North America

China is planning another 14 PDH plants over the next three-four years– Propane demand in China expected to continue to grow

22

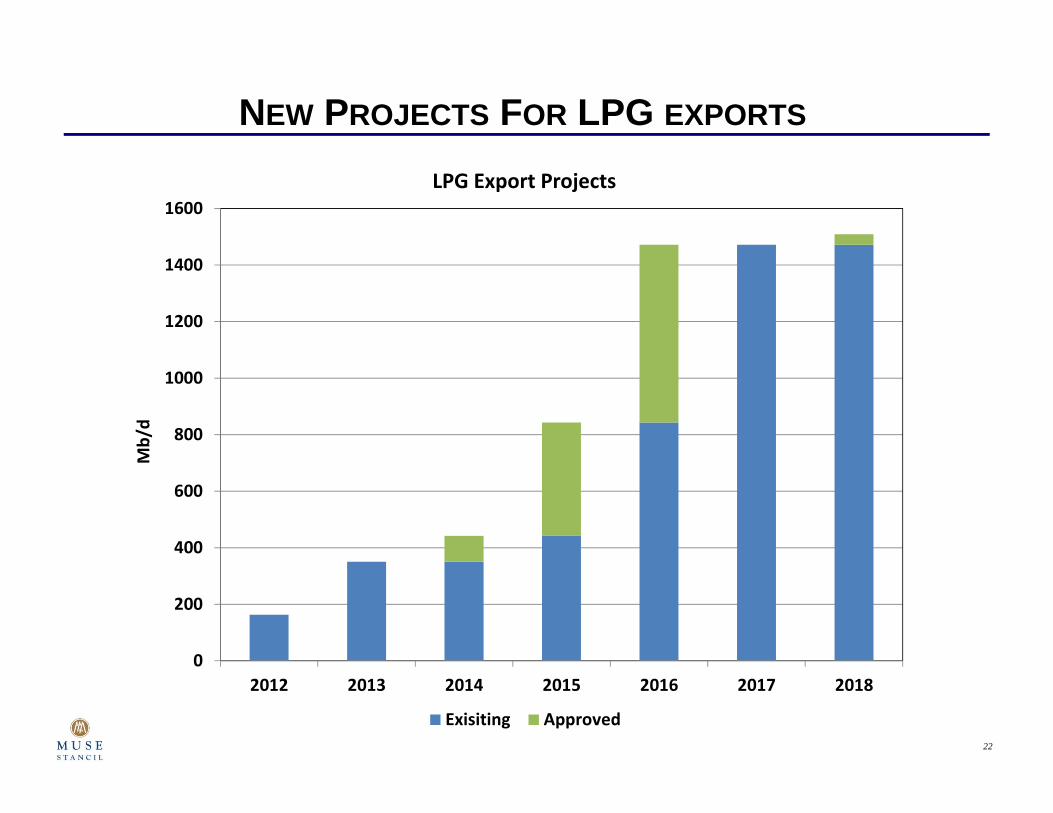

NEW PROJECTS FOR LPG EXPORTS

0

200

400

600

800

1000

1200

1400

1600

2012 2013 2014 2015 2016 2017 2018

Mb/d

LPG Export Projects

Exisiting Approved

23

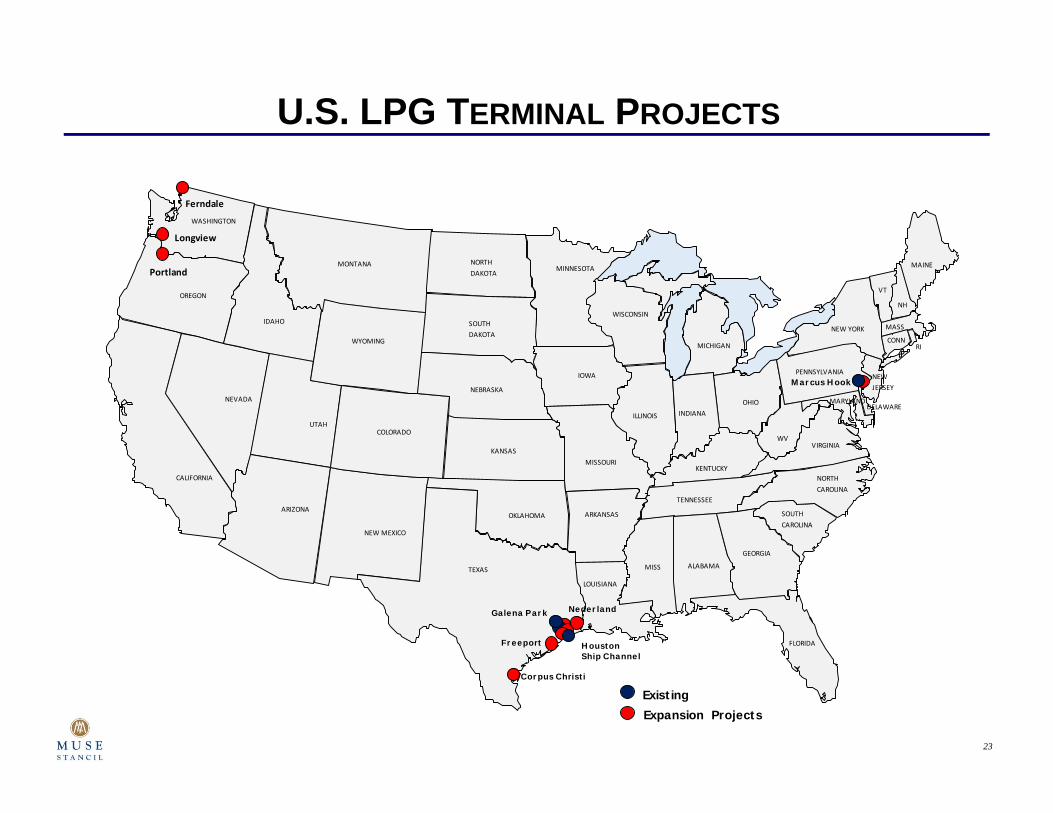

U.S. LPG TERMINAL PROJECTS

Corpus Christi

PortlandMONTANA

WYOMING

IDAHO

WASHINGTON

OREGON

NEVADA

UTAH

CALIFORNIA

ARIZONA

NORTH DAKOTA

SOUTH DAKOTA

NEBRASKA

COLORADO

NEW MEXICO

TEXAS

OKLAHOMA

KANSAS

ARKANSAS

LOUISIANA

MISSOURI

IOWA

MINNESOTA

WISCONSIN

ILLINOIS INDIANA

KENTUCKY

TENNESSEE

MISS ALABAMA

GEORGIA

FLORIDA

SOUTHCAROLINA

NORTH CAROLINA

VIRGINIAWV

OHIO

MICHIGAN

NEW YORK

PENNSYLVANIA

MARYLANDDELAWARE

NEWJERSEY

CONNRI

MASS

MAINE

VT

NH

Freeport Houston Ship Channel

Galena Park Nederland

Longview

Ferndale

Marcus Hook

Existing

Expansion Projects

24

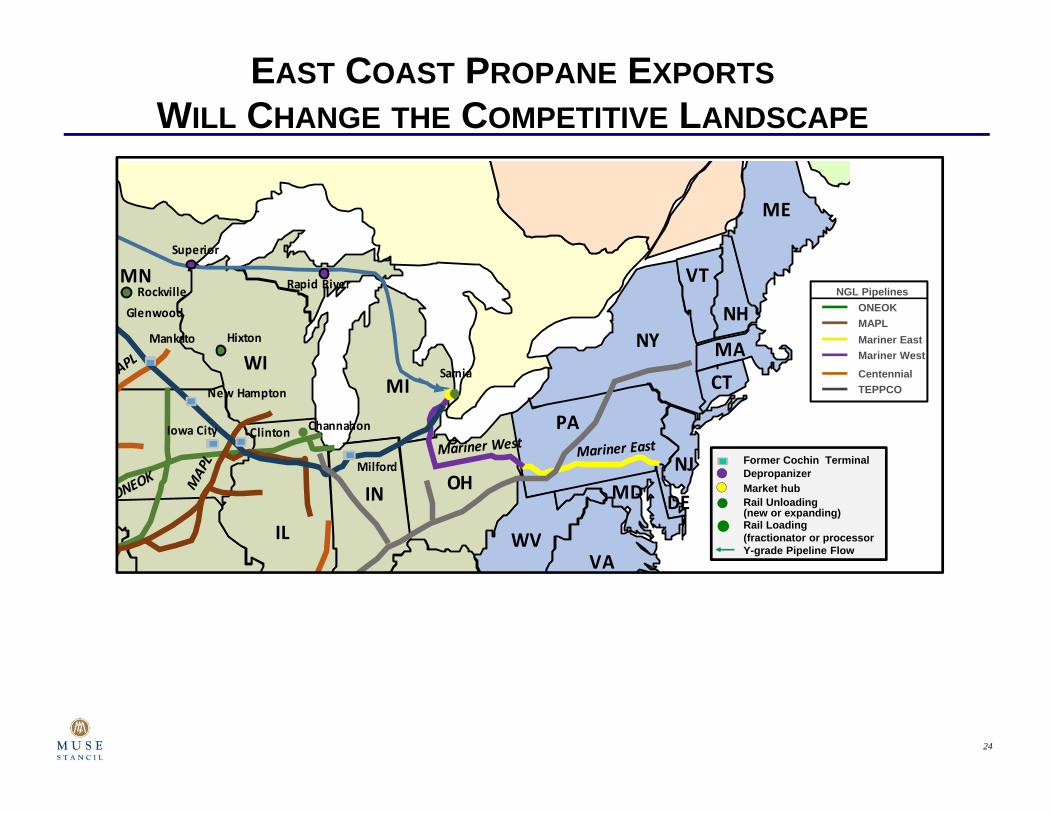

EAST COAST PROPANE EXPORTSWILL CHANGE THE COMPETITIVE LANDSCAPE

VAWV

PA

NJ

NY

ME

VT

NH

MACT

OHIN

IL

WIMI

MN

MD DE

New Hampton

Rockville

Glenwood

Mankato Hixton

Iowa City Clinton Channahon

Milford

Sarnia

Rapid River

Superior

ONEOKMAPL

NGL Pipelines

Mariner EastMariner WestCentennialTEPPCO

Former Cochin TerminalDepropanizer

Rail Loading (fractionator or processor

Market hubRail Unloading (new or expanding)

Y-grade Pipeline Flow

25

U.S. LPG EXPORTS HAVE GROWN DRAMATICALLY

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Mb/d

LPG Exports by Destination

Other South America Central America Asia Caribbean

26

WHERE ARE U.S. LPG EXPORTS HEADED?

27

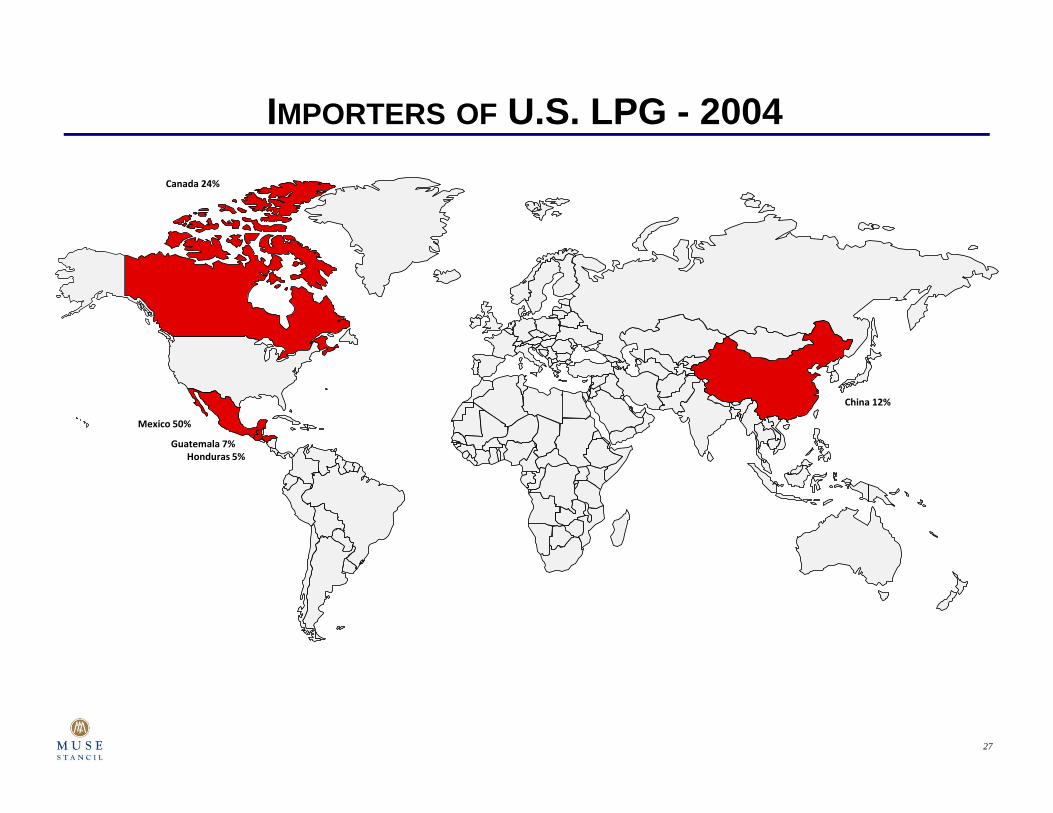

IMPORTERS OF U.S. LPG - 2004

Mexico 50%

Canada 24%

China 12%

Guatemala 7%Honduras 5%

28

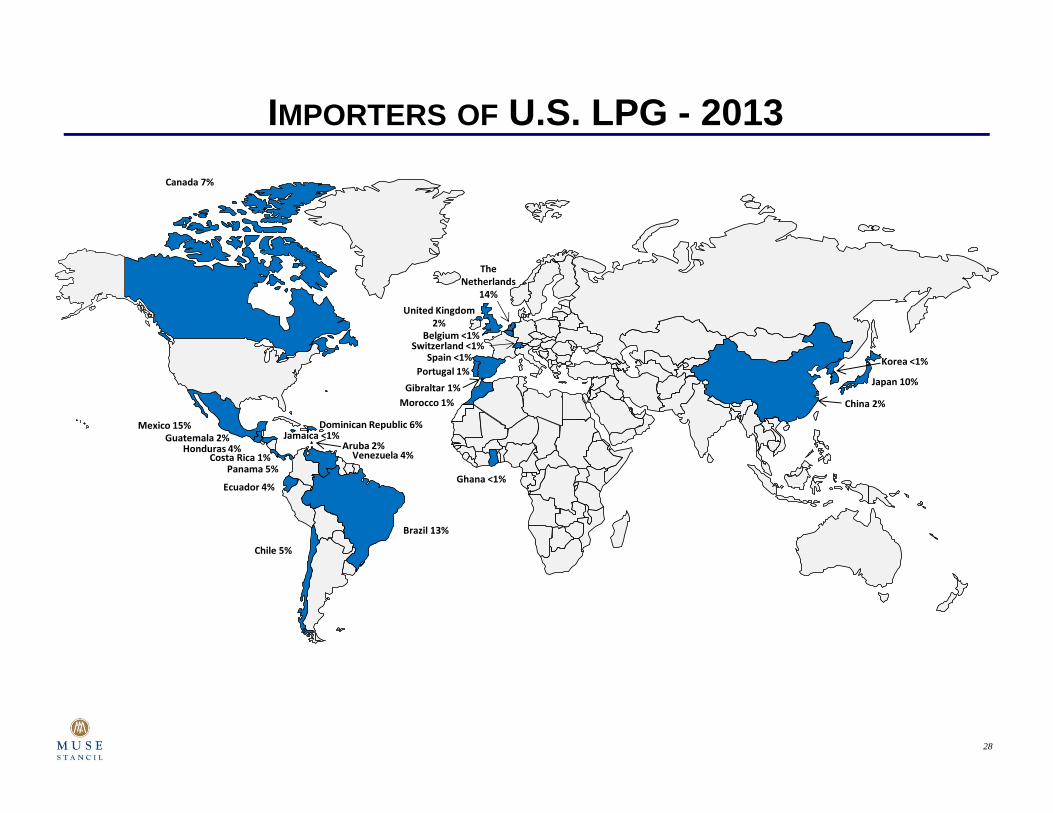

IMPORTERS OF U.S. LPG - 2013

Japan 10%

Brazil 13%

Mexico 15%

The Netherlands

14%

Canada 7%

Dominican Republic 6%

Chile 5%

Panama 5%

Ecuador 4%

Venezuela 4%Aruba 2%

China 2%

Guatemala 2%

United Kingdom 2%

Gibraltar 1%Morocco 1%

Portugal 1%

Belgium <1%

Costa Rica 1%

Ghana <1%

Jamaica <1%

Korea <1%Spain <1%Switzerland <1%

Honduras 4%

29

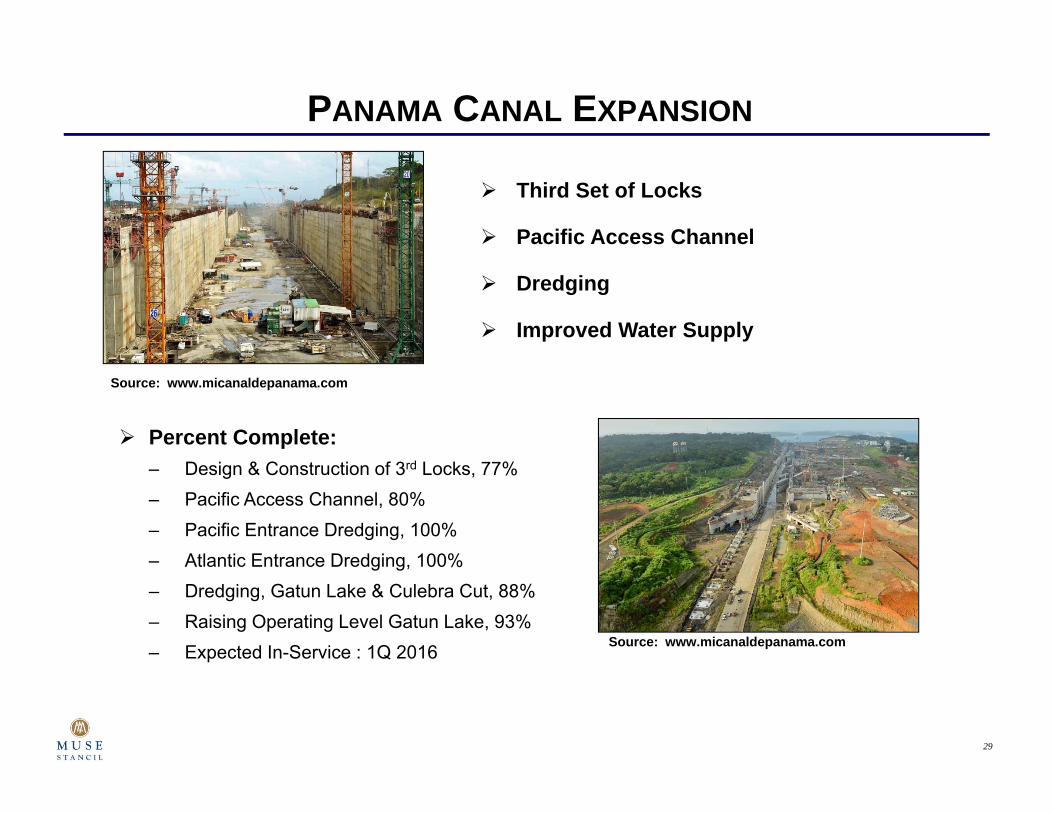

PANAMA CANAL EXPANSION

Source: www.micanaldepanama.com

Third Set of Locks

Pacific Access Channel

Dredging

Improved Water Supply

Source: www.micanaldepanama.com

Percent Complete:– Design & Construction of 3rd Locks, 77%– Pacific Access Channel, 80%– Pacific Entrance Dredging, 100%– Atlantic Entrance Dredging, 100%– Dredging, Gatun Lake & Culebra Cut, 88%– Raising Operating Level Gatun Lake, 93%– Expected In-Service : 1Q 2016

30

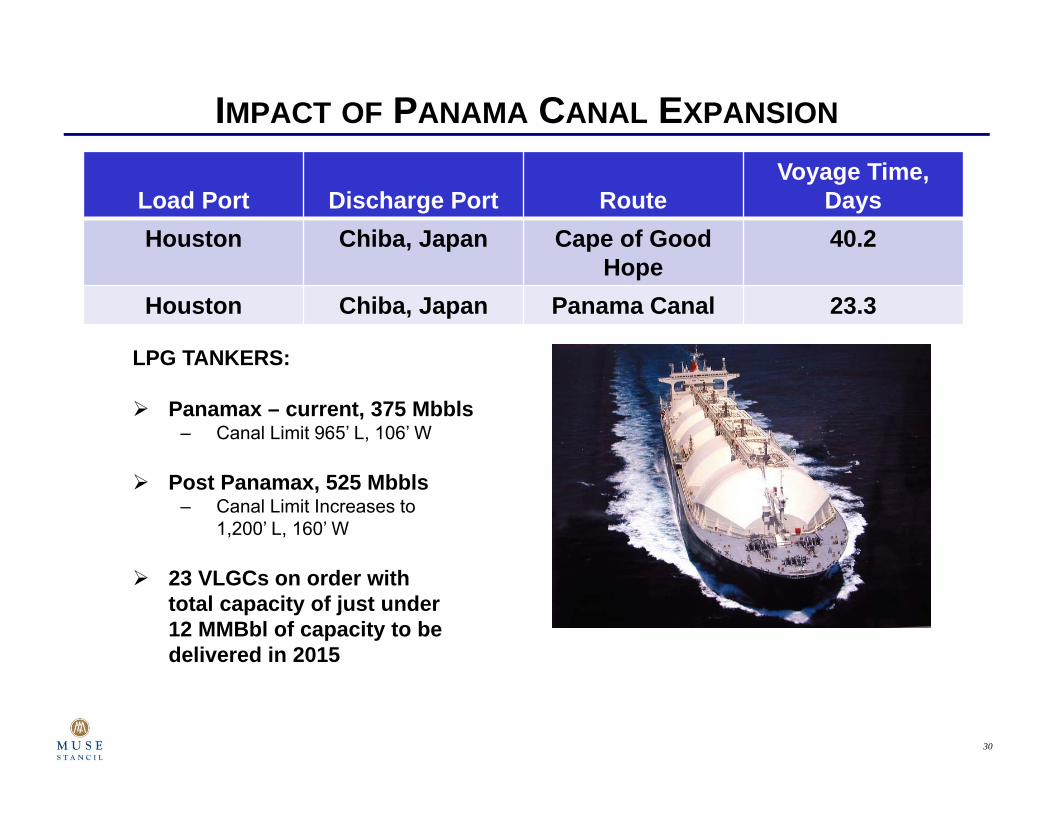

IMPACT OF PANAMA CANAL EXPANSION

Load Port Discharge Port RouteVoyage Time,

DaysHouston Chiba, Japan Cape of Good

Hope40.2

Houston Chiba, Japan Panama Canal 23.3

LPG TANKERS:

Panamax – current, 375 Mbbls– Canal Limit 965’ L, 106’ W

Post Panamax, 525 Mbbls– Canal Limit Increases to

1,200’ L, 160’ W

23 VLGCs on order with total capacity of just under 12 MMBbl of capacity to be delivered in 2015

31

IMPACT OF THE PANAMA CANAL EXPANSION Significant reduction in transportation costs

– Larger ships will be able to transit the locks– Significantly shortens transit time to the Asia Pacific region– Thus, overall transport costs will see a large reduction

Will allow large refrigerated cargos to move to Japan, China, and India– All of these economics continue to grow and are importing more LPG for domestic use

Asia Pacific region continues to require new supply sources

Security of supply is an issue– U.S. is politically more stable that other LPG producing areas of the world

32

CONCLUSIONS U.S. Propane continues to grow dramatically due to increase in shale oil and gas

production

Infrastructure to move additional NGLs is rapidly catching up in the new shale areas

U.S. propane consumption is not increasing as quickly as production, and exports will be needed to balance supply and demand

Timing of these exports are lining up well with the new export terminal projects and expansion of Panama Canal

Economies in Asia are looking for supply security through diversification of sources