challenges arising from alternative investment management

TRANSCRIPT

Banque de France • Financial Stability Review • No. 3 • November 2003 1

Challenges arising from alternativeinvestment management

François HAASBanque de France

Market and Financial Stability ResearchDivision

Noël AMENCProfessor of Finance, EDHEC

Misys Asset Management Systems

Mathieu VAISSIÉResearch Engineer, EDHEC

Over the past few years the alternativeinvestment industry has developedspectacularly, attracting so much investor

interest that it appears at times to have taken on theproportions of a “fad”. This article sets out to chart thedevelopment of this phenomenon. We will start out byattempting to define the broad outlines and trends ofthis rapidly evolving industry. We will then try to show

why this style of management requires specific riskanalysis techniques and performance indicators. Thiswill enable us to assess the impact of alternativeinvestment management on financial market dynamics,and identify the conditions under which thesemanagement strategies might “usefully” contribute tothe functioning of financial markets and become a lastingfeature in the world of asset management.

Alternative investment management differs from traditional asset management in a number ofrespects. First, it is distinct in terms of both its targets – aiming to achieve an absolute performance,regardless of trends in underlying markets – and its strategies, in particular exploiting inefficienciesin the valuation of financial assets via opportunistic and discretionary positions. It also differs interms of the financial techniques implemented, e.g. the extensive use made of leverage, derivativesand short selling, and the specific investment vehicles used (ad hoc structures such as hedge fundsthat are not bound by ordinary law in the way traditional investment vehicles are). Theseparticularities, alongside the fact that the alternative investment universe is somewhat opaque,make it difficult to measure a fund’s risks or a fund manager’s performance. Specific measurementtools are therefore required, which differ from those commonly used in traditional asset management.

Over the past few years, the alternative investment management, a diverse and rapidly-evolvinguniverse, has enjoyed a spectacular development, which is illustrated by the sharp rise in the amountsunder management and the proliferation of investment vehicles offered to an increasingly broadinvestor base. In view of the specific nature of alternative fund managers’ modus operandi, theflourishing of the alternative investment industry raises questions as to its implications in terms offinancial stability. It also raises new issues regarding the division of roles between market participantsand supervisory authorities in the organisation and monitoring of this asset management sector.

Challenges arising from alternative investment management

2 Banque de France • Financial Stability Review • No. 3 • November 2003

1| The universe of alternative investment management

Given the diversity and evolving nature ofthis industry, it is not easy to define what iscommonly understood by “alternative investmentmanagement”. Before analysing the trends currentlycharacterising this universe, we will attempt todetermine its contours.

1|1 An attempted definition

Alternative investment management can be definedin terms of how it differs from “traditional” assetmanagement: the targets set, the instruments andtechniques used, and the investment strategiesimplemented.

Investment targets

In “traditional” asset management, as practisedby mutual funds and institutional fund managers,the investment rationale is typically arelative performance approach: investments undermanagement in this form are essentially, if notexclusively, allocated to pre-specified financial assetclasses, at a medium- to long-term horizon.Consequently, the performance of a portfoliomanaged in this way, and the risk to which it isexposed, will depend primarily on the trends of theunderlying markets and, secondly, on the fundmanager’s ability to allocate assets appropriately.This performance will be measured against anoverall or sectoral benchmark index, considered tobe representative of the markets in which the assetsare invested (money markets, bond markets, equitymarkets, domestic or international markets). Thefund manager aims to achieve a performance that iseither as close as possible to that of the benchmarkindex (index-linked or passive management) or tobeat this index (active management).

Conversely, in alternative investment management,an absolute positive performance target is set,i.e. a performance uncorrelated with that of theunderlying asset classes. In principle, managers setout to achieve a performance that is (at leastpartially) independent of the intrinsic performanceof financial markets: investors forgo structuralreturns associated with “long-only” investmentpositions (the risk premium adjusted for the level ofmarket exposure – beta 1), in exchange for protectionagainst adverse movements in markets (directionalrisk). Investors are thus directly exposed to thequality of the fund manager 2.

While the traditional asset management approach isbased on efficient market and optimal marketportfolio hypotheses, the alternative investmentapproach looks for inefficiencies in financial marketswith a view to exploiting them: the alternativeinvestment approach aims to capture alpha ratherthan beta, i.e. to outperform the market.

Techniques and instruments

Alternative investment management, like traditionalasset management, uses conventional financialinstruments such as money market paper, bonds andequities. However, it also uses less conventional, andgenerally less liquid, categories of assets (unlistedsecurities, commodities, or even real estate assets).Furthermore it employs, in the usual manner, andsometimes in significant proportions, a completerange of outright and conditional derivatives, as wellas specific financial techniques such as short selling.While leverage 3 is not specific to alternativeinvestment, nor systematically used 4, it is part ofalternative fund managers’ array of everydaytechniques.

1 Broadly speaking, beta is the measure of the volatility of an individual (portfolio) security compared with that of the market as a whole, i.e. itssystematic risk. Alpha represents the excess returns on an individual (portfolio) security, which is not explained by the model. For a moredetailed definition, see Box 1 below.

2 Hence, the performance structure of hedge fund managers is directly linked to their performance: on average, on the basis of a number of marketsources, we can estimate that fund managers receive almost 18% of profits generated, as well as management fees of 1% to 1.5% of the amountof assets under management.

3 In this paper, we define leverage as the use of borrowed resources or the use of the above-mentioned financial techniques and instruments witha view to increasing the size of the positions taken.

4 In particular when exploiting minor arbitrage opportunities.

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 3

Strategies

Alternative funds implement a wide range ofinvestment strategies. While these strategies areflexible, and many different combinations exist, wecan basically identify four major investment styles,of which there are numerous variations.

– Long/short strategies involve taking simultaneouslyshort and long positions in different securities,some considered undervalued and othersovervalued on the basis of a fundamental ortechnical analysis, and then exploiting thismarket anomaly. The overall position can bedirectional – skewed in favour of one or other ofthe positions, or non-directional (market neutral).In the latter case, the profit generated is notdependent on the performance of the market asa whole (both securities may appreciate ordepreciate simultaneously) but solely on therelative performance of each of the positions.

– Arbitrage 5 and relative value strategies are focusedon detecting and exploiting perceived anomaliesin the relative pricing of financial assets or inthe statistical relationships linking differentassets. On the basis of this principle, arbitragestrategies between different segments of the yieldcurve or bond markets exploit yield differentialsand, in particular, the mean return tendency ofthese spreads. Also of note are convertiblesecurities arbitrages, which aim to exploitpotential pricing differences between the securityitself and its different components 6 or takeposition in the underlying factors that determinethe value of these particular securities. Anothertechnique employed is “capital structurearbitrage”, whose objective is to exploit anydifferences in the pricing of an issuer’s liabilities(between its debts according to their ranking, orbetween debt and equity securities). As differentas they may be, these strategies share onecommon feature: the intensive use of quantitativetechniques and sophisticated mathematicalmodelling to identify arbitrage opportunities. Thelatter are systematically exploited by the takingof both long positions and short selling. Giventhat arbitrage opportunities are often minor, thepositions taken by these funds are frequentlyhighly leveraged.

– Event-driven and special situation strategies can bedefined as positions taken on the developmentsof a situation of a particular company, or on theprobability of the occurrence of a particular eventin the life of a company. Some funds, sometimesknown as “vulture funds”, specialise in the debtof restructuring companies (distressed debt),which is often undervalued due to the fact thatmany investors find it impossible to hold thistype of paper in their portfolio. These funds mayalso specialise in merger and acquisition (M&A)operations, which entails taking positions in thesecurities of the target company, and whereappropriate taking an opposite position in thesecurities of the company initiating theoperation.

– Directional strategies and tactical approaches differconsiderably from the theoretical frameworkdescribed above to outline the principles ofalternative investment management. Here,positions are taken that either follow a markettrend or “lean against the wind”, depending onwhether the fund manager expects the trend tocontinue or to turn around. By definition, thesepositions are unhedged. Implemented by “globalmacro” funds, these strategies are not based on atechnical financial market approach, but ratheron a financial and macroeconomic analysis of thesituation of a country, sector of activity oreconomic area. Trading funds, “market timing”and “trend followers” funds, futures funds andCommodity Trading Advisers implement theseinvestment strategies. They are closer toconventional “speculative” position-taking thanto other alternative investment strategies thattake advantage of valuation inefficiencies.

5 The notion of arbitrage should not be interpreted here in the usual sense of “risk free” arbitrage, but rather as a position aiming to exploit a“temporary” divergence between the movements of two assets that is not typical of their long-term relationship (see Part 3).

6 Convertible bonds are frequently undervalued in relation to their theoretical value. The most conventional arbitrage technique consists in takinga long position in a convertible bond and a short position in the underlying stock, so as to exploit the price difference while remaining protectedagainst fluctuations in the stock itself.

seigetartstrohs/gnoL %7

eulavevitalerdnaegartibrA %63

seigetartsnoitautislaicepsdnanevird-tnevE %9

seigetartslanoitceriD %03

)seigetartscitsinutroppodnadenibmoc(srehtO %81

latoT %001

.setamitseecnarFedeuqnaB:ecruoS

Table 1The alternative investment industry:relative share of different investment styles

Challenges arising from alternative investment management

4 Banque de France • Financial Stability Review • No. 3 • November 2003

– As different as they may be, the investmentstyles described above all require the fundmanager to be extremely proactive and adoptan opportunistic and discretionary approach.These particularities, and the constraints theyimpose on investors, especially in terms of theliquidity of their investment, explain why thealternative investment industry has developedwithin the framework of ad hoc structures thatare not subject to prudential rules (risk divisionratios, strict rules covering the use of derivatives,short selling, etc.) and transparency rules(valuation) imposed on standard investmentvehicles, and are accessible only to a minorityof qualified investors. These investment fundsare commonly known as “hedge funds” or“highly leveraged institutions” (HLI). However,no statutory definition exists for these terms, nordo market participants unanimously agree onone 7. In very broad terms, from an operationalstandpoint, hedge funds can be qualified as allinvestment vehicles not bound by ordinary lawin terms of protection of savings and/or that areliable to use a complete range of available

financial market instruments and techniques.In the rest of this paper we will employ the terms“hedge fund” and “alternative fund”indifferently.

1|2 An evolving industry

Investment structures and customer bases:from global macro fundsto alternative multi-management

Over the past 15 years, the hedge fund industry hasevolved significantly. In quantitative terms, despitethe fact that alternative investment funds still onlyaccount for a small proportion of funds invested inthe asset management industry, the number ofalternative funds has increased dramatically,growing by a factor of around five since 1988, toexceed 7,000 units. In particular, over the sameperiod, the amounts under management look to haveincreased by a factor of almost 20, to reachUSD 650 billion at end-2002.

7 A document published in the light of American Supervising Authority, the Securities and Exchange Commission (SEC), hearings on hedge fundsin May 2003 offers fourteen different definitions.

Chart 1Hedge funds: number of vehicles and assets under management

(USD billions)

Source: Van Hedge Fund Advisors International Inc.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 20031988

Number of funds (left-hand scale)Assets under management (right-hand scale)

0

100

200

300

400

500

600

700

800

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 5

This booming industry has also radicallyrestructured.

– Global macro funds, which symbolised thedevelopment of this industry during the 1990s,from the sterling crisis of 1992 to the Asian andRussian crises of 1997-1998, no longer dominatethe universe of alternative funds. Strictlyspeaking, these funds currently account for lessthan 5% of assets under management (comparedwith almost 70% at the start of the 1990s) withinan industry dominated by arbitrage funds andcharacterised by small specialised structures:according to a number of market sources, 80% ofhedge funds currently manage assets worth lessthan USD 100 million.

Chart 2Breakdown of assets under management(by portfolio size, in USD millions)

25-100(32%)

100-500(17%)

> 500(3%)

0-5(18%)

5-25(30%)

Source: Banque de France estimates.

– The customer base of hedge funds, initiallyconcentrated on wealthy private investors, inparticular in the United States, steadilybroadened, to encompass institutional investors

(pension funds, insurance corporations, etc.), andlater on all individual investors. Thedevelopment of multi-management and “fundsof funds”, and the popularisation of alternativefunds offering capital guarantees plainlyillustrate the current “democratisation” trend ofalternative investment products.

There are several reasons behind institutional andindividual investors’ recent enthusiasm foralternative investment funds, some of which arecyclical, and others more structural.

– In addition to the decline in bond yields sincethe start of the 1980s, equity markets have fallensubstantially over the past few years. The formertrend prompted investors to seek new sources ofhigh returns, while the latter highlighted therelevance of approaches aiming to achieveabsolute performance, regardless of trends in theunderlying markets.

– The propensity of traditional asset classes toexhibit, particularly in bear markets, a highcorrelation, and the limitations of internationaldiversification stemming from the increasingglobalisation of financial markets, have alsocontributed to this trend.

– The alternative investment industry has alsoexpanded as a result of “deviations” in traditionalmanagement, in particular the practice of “closetindexing” in benchmarked asset management.

– Lastly, over the most recent period, the increasein volatility in all markets may have contributedto the more commonplace use of alternativeinvestment management.

Challenges arising from alternative investment management

6 Banque de France • Financial Stability Review • No. 3 • November 2003

2| Performance measures and alternative risk strategies

2|1 The difficulties entailed inmeasuring risks in alternativeinvestment strategies

Alternative investment strategies are infinitely morecomplex than those implemented by traditionalfunds, such as buy-and-hold strategies, as, in additionto identifying the markets in which funds takepositions (i.e. the location factor), it is also necessaryto calculate their net exposure and leverage (i.e. thestrategy factor). Measuring their performance isrendered all the more difficult.

Traditional measurement tools ...

There are two main approaches used to measureperformance: “absolute” measures, which areindependent of any benchmark, and “relative”measures, which compare an asset’s performanceto that of a benchmark portfolio. The first categoryincludes indicators such as the Sharpe ratio and theTreynor ratio. These measures consist in calculatingthe excess return of an asset minus the risk-freerate over the risk indicator. The latter can be definedas the standard deviation of the asset’s return series(i.e. return volatility, see the Sharpe ratio), or thesensitivity of the asset to market movements(i.e. beta, see the Treynor ratio), or a measure ofmaximum loss (i.e. Value-at-Risk or VaR 8). Amongthe tools for measuring the relative performanceadjusted for risk, Jensen’s alpha (1968), the bestknown, is defined as the average return on aportfolio over and above that predicted by themarket model, given the portfolio’s beta and theaverage market return.

... which are poorly suited to measuringthe specific nature of hedge fund performance

Exposure to multiple risk factors

Given that they are free to invest dynamically in alarge range of assets, hedge funds are exposed tomultiple risk factors (market, volatility, credit,liquidity, etc.). Consequently, even though somestrategies are non-directional, the risk-free rate

cannot be an appropriate benchmark and theabsolute performance measures discussed above arenot suitable for measuring hedge fund performance.Among the relative performance measures, onlythose using a benchmark that takes account of allthe sources of risk to which hedge funds are exposedare apposite for measuring the risk-adjustedperformance of alternative strategies. Manydifficulties are still encountered in measuring theserisk factors and apprehending their interdependence(e.g. liquidity and credit risks). This explains whyonly a few strategies have, to date, given rise torelatively robust models (such as trend-following,merger arbitrage, and more recently bondstrategies).

Dynamic and non-linear exposures to risk factors

Most performance evaluation methods currentlyimplemented use one-factor linear or multifactorialmodels 9. The effectiveness of these modelsdepends, inter alia , on the linearity of therelationships between the dependent variable andthe explanatory variables. Unfortunately, threefactors contribute to the non-linearity of theexposure of hedge fund performance to thedifferent risk factors.

– A number of risk factors underlie each alternativestrategy. For a given strategy, the best funds arethose which succeed in correctly over- orunderweighting their exposure to different riskfactors. Because they use this “tactical factorallocation” strategy, and “market timing” or “riskfactor timing”, their exposure to the different riskfactors changes over time.

– Moreover, given that markets are relativelyefficient, there are not an infinite amount ofarbitrage opportunities. In order to maintain theirperformance, some hedge funds therefore tendto seize any opportunities that arise, even if itmakes them deviate from the strategy they claimto implement. These one-off changes in style,known as “tactical style allocation” by fundmanagers and “style drift” (see Lhabitant, 2001)by investors, also result in variations in exposuresto risk factors. The exposure of hedge funds torisk factors is hence doubly dynamic.

8 VaR expresses the portfolio risk as the maximum amount of loss that can be incurred for a set confidence threshold at a given time horizon.9 CAPM, a three-factor model developed by Fama and French; a four-state model by Carhart; Arbitrage Pricing Theory (APT), etc.

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 7

Box 1

Traditional performance measures

Absolute measures

Sharpe ratio : E (RP) – RF

σ (RP) ; Treynor ratio :

Where E(Rp ) is the expected portfolio return, σ (RP ) its volatility, RF the risk-free rate, and βP the sensitivityof the portfolio return to market variations.

Relative measures

Jensen’s alpha is calculated by the following regression: RPt – RFt = αP + P (RMt – RFt) + εPt β

Where RPt , RFt et RMt

are the return on the portfolio, the risk-free asset and the market at date t, βP the sensitivity

of the portfolio return to market variations and εPt an error term.

Contrary to the Sharpe and Treynor ratios, Jensen’s measure contains a benchmark. However, Jensen’s alphacannot be used to compare portfolios with different risks, as the value of alpha is proportionate to the level of risktaken.

To solve this problem, Modigliani and Modigliani (1997) proposed M 2 or Risk adjusted performance (RAP). Thismeasure evaluates the performance adjusted for the risk of a portfolio against the market benchmark, expressedas the return per unit of risk:

RAPP = (E (RP) – RF) + RFσ (RM)σ (RP)

where E (Rp ) is the expected portfolio return, σ (RP) its volatility, σ (RM) that of the market and RF the risk-freerate.

Lobosco (1999) then further developed RAP to SRAP, to take account of the effect of management style on anasset’s performance. The SRAP is defined as the difference between the asset’s RAP and the benchmark’s RAP,representative of the asset’s management style.

Lastly, in the Sortino ratio, which is very close to the Sharpe ratio, the risk-free rate is replaced by the benchmarkreturn (or the Minimum acceptable return – MAR) and the standard deviation by the square root of thesemi-variance. This indicator can then be used to evaluate the performance of an asset whose return distributionfunction is not symmetrical.

Sortino ratio :

where E(Rp ) is the expected portfolio return, MAR is the Minimum acceptable return and RPt the portfolioreturn at date t.

∑

E (RP) – MAR

(RPt – MAR) 21T

T

t = 0RPt < MAR

E (RP) – RF

Pβ

Challenges arising from alternative investment management

8 Banque de France • Financial Stability Review • No. 3 • November 2003

– The asset portfolios held by hedge funds (inparticular derivatives) are themselves sources ofnon-linear exposures to the different risk factors.

– The remuneration system of hedge fundscomprises a fixed part (management fees)and a variable part (incentive fees). Thisremuneration is therefore asymmetrical as thereturn pattern of the variable part is similar tothat of a call option on the fund’s performance 10.Since the performance of hedge funds isreported net-of-fees, this introduces de facto anon-linear component.

Traditional indicators for measuring absoluteperformance assume that the (total or systematic)risk is constant over the whole analysis period.Likewise, standard mono- and multi-factorialmodels do not take into account risk factorexposure dynamics, as the stability of thecoefficients is one of the central assumptions ofthese models. They simply measure the averageexposure to different risk factors over the analysisperiod. Naturally, this distorts the evaluation ofhedge funds’ risk-adjusted performance.

Extreme risks

Most traditional tools for measuring performanceand risks assume the normality of the distributionof returns on the evaluated asset. The asset’s risk istherefore characterised by its volatility (i.e. thestandard deviation). However, many studies haveshown the significance of third-order moments(asymmetry coefficient) and fourth-order moments(flattening coefficient) of the distribution functionsof hedge fund returns. Hedge fund performancetherefore cannot be analysed using the mean-variance framework.

Taking into account exceptional events exacerbatesthe statistical estimation problems that arise fromusing VaR 11. To overcome these difficulties, investorsand fund managers have implemented someinteresting solutions: stress tests, scenario analyses,more complex modelling of distribution tails withextreme value theory. Nevertheless, although theyare theoretically more robust, there are still practicaldifficulties in applying them due to gaps inknowledge about the underlying factorial structureof the different alternative strategies (above all

scenario analyses and stress tests) and the limitednumber of observations (especially in the case ofthe “block maxima” method and the peaks-over-threshold method, or more simply for expansionsof Cornish-Fisher-type – VaR approach) 12.

Relative measures of the performanceof alternative strategies

Despite the fact that they are unsuitable forevaluating hedge fund performance, absolutemeasures of performance have been used in manystudies. While there is no doubt that the evaluationof the performance of alternative strategies needsto take account of the risk factors to which they areexposed, the best method for doing this has yet to bedetermined. Where some authors used a single-factormodel, others employed multi-factorial models totake better account of the diversity of risk sources.For all that, the factors in hedge fund returns remaindifficult to identify; the risk being that incorrectfactors may be included or correct ones left out.

Implicit factorial analysis

Hedge funds do not generate the majority of theirreturns from allocation between different assetclasses, as is the case for traditional funds, but fromthe dynamic strategies implemented by theirmanagers. However, Sharpe’s model for analysingmanagement styles does not take into account theactive component of hedge fund returns. The resultsyielded are therefore not very significant whenapplying the model to hedge funds. According to thestudy by Fung and Hsieh (1997) the explanatorypower (R 2) of Sharpe’s model is indeed below 25%for 48% of hedge funds, whereas it exceeds 75% for47% of mutual funds). Therefore, in order to improvethe explanatory power, it is necessary to integratethe factors reflecting the specific nature of hedgefund strategies (i.e. trading factors). The best solutionfor identifying these, without being exposed to a highdegree of model risk, is to carry out a factorialanalysis of hedge fund returns in order to determinethe predominant styles. This method is based onthe assumption that managers investing in the sameasset classes and using the same managementstrategies must generate correlated returns. Thisanalysis method can be used to explain the variationsin hedge fund returns, but it does not provide a clear

10 The strike price is therefore equal to the “hurdle rate”, i.e. the return above which the fund is paid incentive fees.11 Historical VaR calculations require a large number of variables to obtain a significant event sample; VaR calculations based on a

Monte Carlo approach are complex and cumbersome; parametric analyses are oversimplified.12 See Jorion (2001) for further details on VaR and Lhabitant (2003) for a presentation of extreme value theory.

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 9

view of the dynamics of hedge fund returns overtime. Furthermore, a significant part of thevariation in hedge fund returns in the samplestudied is not explained by the main factorsidentified (e.g. over 50% according to the studyby Fung and Hsieh, 1997).

Analysis using a linear model with non-linear regressors

In order to compensate for the lack of traditionallinear factorial models for analysing hedge fundperformance, models have been developed in theliterature that make it possible to take account ofthe non-linearity of these funds’ returns. Newregressors (or explanatory variables) are used thathave a non-linear exposure to traditional assetclasses, so as to approximate dynamic managementstrategies in a linear regression. Option portfolios orhedge fund indices are natural candidates for thesenew regressors.

Given that the management strategies implementedby hedge fund managers are not known withprecision, some authors have attempted to describethem using simple optional strategies. Byimplementing models comprising call and put optionportfolios of certain location factors (equity indices,bond indices,), a default factor (i.e. credit spread),Fama and French factors (size, value/growth) and aCarhart factor (momentum), they managed toexplain a significant proportion of the variability inhedge fund returns over time 13.

Another possibility would be to use hedge fundindices. This approach is based on an extension ofthe style analysis model developed by Sharpe (1992)for traditional funds. By extending this model it ispossible to take into account specific hedge fundstrategies, i.e. the use of short-selling and leverage.With this choice of factors we can eliminatenon-linearity problems, which are taken intoaccount in the indices themselves. The accuracy ofresults depends directly on the quality of the hedgefund indices used. It is therefore highlyrecommended to use style indices that are bothrepresentative and with little bias (see the box onEDHEC indices below). This model can be used tocompare the performance of hedge funds with anappropriate benchmark, without knowing with

precision the management strategy applied by thehedge fund. This model is simple to implement anduses only hedge fund returns. Its main weakness isthat it assumes coefficients allocated to the differentindices are constant over the whole analysis period.It is therefore difficult to capture the dynamics ofexposures to risk factors.

Non-linear analysis: payoff distribution pricing model

A final approach involves using a non-linear modelto explain hedge fund returns. In order to correctlyevaluate the performance of portfolios withnon-normal return distributions and a non-zeroasymmetry coefficient, the distribution as a wholemust be considered. Ideally, this should be donewithout specific assumptions regarding thedistribution pattern. This approach thereforeproposes an efficiency test whose theoreticalfoundations are based on the payoff distributionpricing model (PDPM) by Dybvig (1988a, 1988b).Dybvig’s model attributes a price to a givenconsumption distribution function (i.e. the price isequal to the cost of the least expensive portfoliogenerating the consumption function). Thedifference between the cost of the investor’s realportfolio and the cost of the least expensive portfoliogenerating the same consumption function seemsthe natural measure in monetary units of theefficiency loss. The advantage of this evaluationmodel is that it does not require assumptions on thedistribution of the returns of the funds considered.

The results of an empirical study carried outon a sample of 1,500 hedge funds obtainedfrom the MAR/CISDM database 14 and using allthe above-mentioned performance measurementmodels show that traditional mono- ormulti-factorial models find significantly positivealphas for hedge funds. However, when the wholedistribution of returns is taken into account or onlyimplicit factors are included in the model, hedgefunds no longer, on average, have significantlypositive alphas. All in all, the alpha of a hedge fundmay have a dispersion of over 40% between thedifferent methods! This reminds investors that,above and beyond the financial and operational risksto which hedge funds are exposed, model risks mustalso be taken into account.

13 This approach is perfectly illustrated in studies by Fung and Hsieh (1997) for trend following strategies, Mitchell and Pulvino (2001) for mergerarbitrage strategies, Fung and Hsieh (2002c) for bond strategies and Agarwal and Naik (2003).

14 Amenc et al. (2003a).

Challenges arising from alternative investment management

10 Banque de France • Financial Stability Review • No. 3 • November 2003

2|2 The difficultiesof benchmarking in alternativeinvestment management

Given that the risk-free rate is not a suitablebenchmark for all types of hedge funds, anappropriate benchmark remains to be determined.It appears that the alternative investment industryis shifting from an absolute return approach to arelative return approach. The principle involvescomparing a given fund’s returns with those of aportfolio of a fund implementing the same strategy(peer benchmarking), or with those of abenchmarking index. Already difficult in thetraditional universe, compiling appropriate indicesis much more complicated for the alternativeinvestment industry, due to problems associatedwith both representativity and the purity(i.e. homogeneity) of data.

Impact of biases in databases

The use of a specific data sample, from a universe ofhedge funds that cannot be observed as a whole,introduces a bias in the measure of performance.There are essentially three sources of differencebetween the performance of hedge funds calculatedusing this type of database and the performance ofhedge funds as a whole. These different biases, whichare described in Fung and Hsieh (2000 and 2002a),are: the survivorship bias, the selection bias and theinstant history bias.

The survivorship bias occurs because poor managersleave the industry, and good managers remain.Furthermore, the funds in databases tend to bethose whose return exceeds the average return forall hedge funds, as databases only contain thereturns of good managers, or at least those ofmanagers present at the time of measuring. Thestandard procedure for measuring the survivorshipbias is described by Malkiel (1995). It involvesdetermining the difference over the period underreview between the average return for all hedgefunds and the average return from surviving funds.

As the composition of indices varies significantlybetween the different data providers, thesurvivorship bias will not have the same effect onthe different hedge fund indices.

The selection bias results from the fact that theselection criteria of databases may differsignificantly, and the data provided by thesedatabases are not necessarily representative of thesame management universe and of the real hedgefund universe. Yet again, the impact of this biaswill depend on the databases’ selection criteria.The selection bias will therefore not be the samefor all indices.

Furthermore, data on hedge funds are not easilyaccessible. Reporting the performance of analternative fund in one of the competing databasesis purely voluntary and only some funds choose todo so. This results in a “self reporting” bias. As fundsnot reporting their performance in any database areby definition unobservable 15, it is impossible toevaluate the impact of this bias.

The instant history bias (see Park, 1995) resultsfrom the difference in the dates when hedge funddata are entered in databases. Yet, when a fund isadded to a database, some or all of its history mustbe back filled. This can be done by extrapolatingthe fund’s recent performance data. In general, asnewly-entered funds are likely to perform well, itis probable that their average performance overthe incubation period will be better than that offunds that have been in the database for a longtime (upward bias on returns of newly-enteredfunds). If funds are not entered on the same datein two different databases, they will not be equallyexposed to this bias.

The heterogeneity of hedge fund indices

Competing indices are compiled using differentdatabases and a variety of construction methods.Consequently, they are not affected in the sameway by the measurement biases described above.Differences in performance therefore arise.

15 Some funds chose not to report their performance because it is not satisfactory, and others because they have already reached critical size.

saiB nnamzteoGdnanworB,kraP)9991(

heisHdnagnuF)0002(

pihsrovivruS %6.2 %0.3noitceleS %9.1 %4.1

latoT %5.4 %4.4

Table 2Survivorship bias and selection biasin hedge fund returns

Sources: authors quoted

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 11

Major disparities in performance are often observedin the various competing indices for a givenmanagement style. This phenomenon is particularlymarked in crisis periods, in particular betweenAugust 1998 and October 1998 (see Table 2). Dataprovided by the different index providers differsubstantially: by over 20% in the case of theperformance of the Zurich and EACM (EvaluationAssociates Capital Markets) long/short equityindices in February 2000 (see Amenc and Martellini,2003). An analysis of mean and median correlations

between the performance of different competingindices confirms this lack of homogeneity. Themean correlation between competing indices on agiven type of strategy (equity market neutral: 0.43,long/short equity: 0.46) may be less than 0.5. Theincreasing number of index providers andconstruction methods result in a greaterheterogeneity of data. If we consider that theheterogeneity indicator HI=1 – mean correlation 16,it is obvious that hedge fund indices do not providethe representativity conditions necessary to offerinvestors a homogenous vision of alternative funds.

In order to document the heterogeneity ofdifferent indices we can also consider thedifferences in exposure to the main risk sourcesof these strategies. The results given in Table 4speak for themselves. Once again, we clearly

observe that the different competing indices arevery heterogeneous. In view of the differentexposures to the various risk factors, the resultswill differ according to the competing index chosenas the benchmark.

16 Perfect heterogeneity of indices is expressed as HI=1.

Table 4Sensitivity to the main risk factors – the fixed income strategy(from January 1998 to December 2000)

dexiFemocni

egartibra

tekraMksir 0

0

ytilitaloVksir 00

00

etartseretnIksir 000

0

ehtfoepolSevrucdleiy

egnahcxEksiretar

seitidommoCksir 0000

tiderCksir 0

ytidiuqiLksir 0

0

BFSC 00.0 21.0 51.0 32.0 24.0 50.0 83.0- 01.0-RFH 61.0- 41.0 52.0 91.0 75.0 70.0 42.0- 81.0-

egdeHnaV 35.0 74.0- 90.0 20.0 31.0- 41.0 61.0- 50.0-eessenneH 73.0 73.0- 60.0 91.0 62.0 21.0 22.0- 21.0-

teNFH 01.0- 02.0 22.0 02.0 24.0 30.0 73.0- 10.0-

NB: Market risk: relative variations in the Standard and Poor’s 500 Price Index; Volatility risk: relative price variations in the VIX contract; Interest rate risk: variationsin the three-month Treasury bill yield; Exchange rate risk: USD exchange rate against a basket of foreign currencies; Commodities risk: relative price variations ina barrel of crude oil; Liquidity risk: changes in the volumes of securities traded on the New York Stock Exchange (NYSE); Credit risk: relative changes in the spreadbetween yields on bonds rated BAA and AAA by Moody’s; slope of the yield curve: spread between the yield on a 30-year bond and a three-month T-Bill.

Source: Armenc and Martellini (2003).

selytstnemtsevnI )secidnidnasetadhtiw(secnereffidmumixaM

egartibraelbitrevnoC 0 %67.4 )%80.0(eessenneH/)%86,4-(BFSC:8991rebotcOseitirucesdessertsiD %19.6 )%22.8(hcirüZ/)%13.1(MCAE:0002yraurbeF

stekramgnigremE %54.91 )%02.7-(tsevtlA/)%56.62-(RAM:8991tsuguAlartuentekramytiuqE %00.5 )%02.5(egdeHnaV/)%02.0(eessenneH:9991rebmeceD

nevirdtnevE %60.5 )%17.6-(tsevtlA/)%77.11-(BFSC:8991tsuguAegartibraemocnidexiF %03.11 )%02.0(egdeHnaV/)%01.11-(teNFH:8991rebotcO

sdnuffosdnuF 0 %10.8 )%24.01(tsevtlA/)%14.2(RAM:9991rebmeceDorcamlabolG %71.41 )%26.2(tsevtlA/)%55.11-(BFSC:8991rebotcO

ytiuqetrohs/gnoL %40.22 )%84.02(hcirüZ/)%65.1-(MCAE:0002yraurbeFegartibraregreM %78.1 )%59.2(tsevtlA/)%80.1(teNFH:8991yraurbeF

eulavevitaleR %74.01 )%04.4(egdeHnaV/)%70.6-(MCAE:8991rebmetpeSgnillestrohS %02.12 /)%03.42-(egdeHnaV:0002yraurbeF )%01.3-(MCAE

.)3002(inilletraMdnacnemA:ecruoS

Table 3Differences in maximum performance observed beween representative indices of a given style(from January 1998 to December 2000)

Challenges arising from alternative investment management

12 Banque de France • Financial Stability Review • No. 3 • November 2003

Just as in the traditional management universe, thedifferent indices published are neither collectivelyexhaustive nor mutually exclusive. However, in the caseof the alternative investment universe, the lack of

Box 2

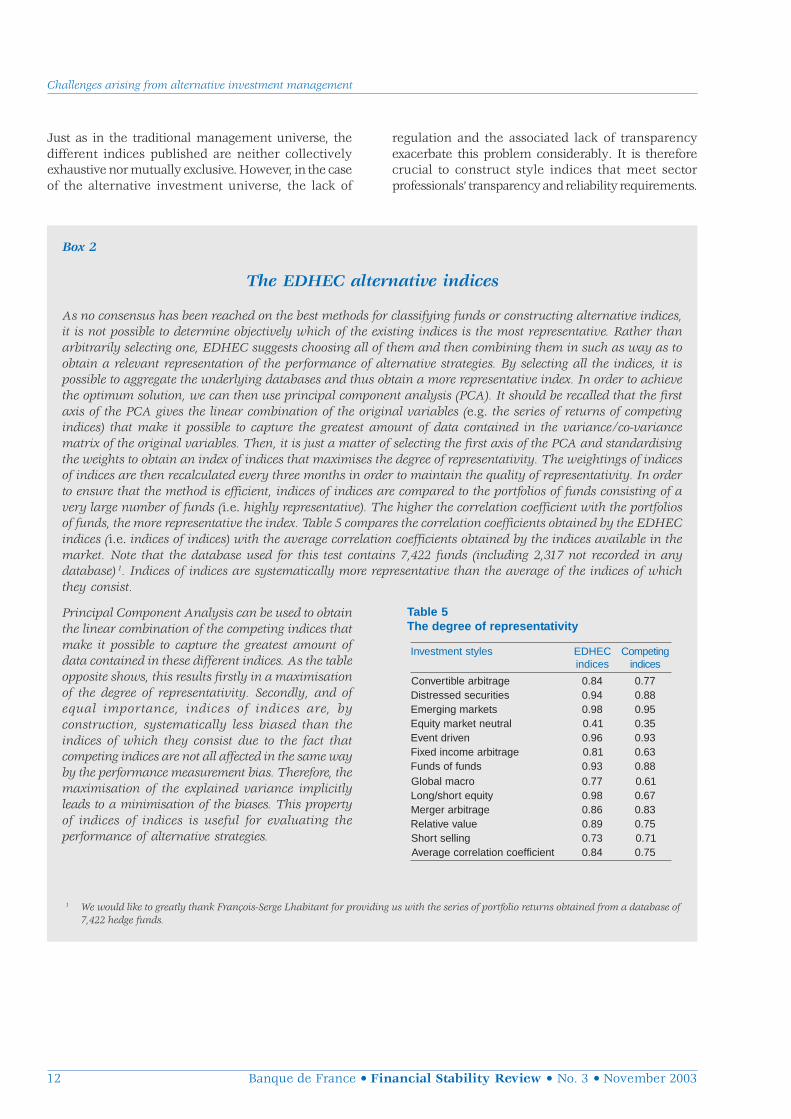

The EDHEC alternative indices

As no consensus has been reached on the best methods for classifying funds or constructing alternative indices,it is not possible to determine objectively which of the existing indices is the most representative. Rather thanarbitrarily selecting one, EDHEC suggests choosing all of them and then combining them in such as way as toobtain a relevant representation of the performance of alternative strategies. By selecting all the indices, it ispossible to aggregate the underlying databases and thus obtain a more representative index. In order to achievethe optimum solution, we can then use principal component analysis (PCA). It should be recalled that the firstaxis of the PCA gives the linear combination of the original variables (e.g. the series of returns of competingindices) that make it possible to capture the greatest amount of data contained in the variance/co-variancematrix of the original variables. Then, it is just a matter of selecting the first axis of the PCA and standardisingthe weights to obtain an index of indices that maximises the degree of representativity. The weightings of indicesof indices are then recalculated every three months in order to maintain the quality of representativity. In orderto ensure that the method is efficient, indices of indices are compared to the portfolios of funds consisting of avery large number of funds (i.e. highly representative). The higher the correlation coefficient with the portfoliosof funds, the more representative the index. Table 5 compares the correlation coefficients obtained by the EDHECindices (i.e. indices of indices) with the average correlation coefficients obtained by the indices available in themarket. Note that the database used for this test contains 7,422 funds (including 2,317 not recorded in anydatabase) 1. Indices of indices are systematically more representative than the average of the indices of whichthey consist.

1 We would like to greatly thank François-Serge Lhabitant for providing us with the series of portfolio returns obtained from a database of7,422 hedge funds.

selytstnemtsevnI CEHDEsecidni

gnitepmoCsecidni

egartibraelbitrevnoC 48.0 77.0seitirucesdessertsiD 49.0 88.0

stekramgnigremE 89.0 59.0lartuentekramytiuqE 14.0 53.0

nevirdtnevE 69.0 39.0egartibraemocnidexiF 18.0 36.0

sdnuffosdnuF 39.0 88.0orcamlabolG 77.0 16.0

ytiuqetrohs/gnoL 89.0 76.0egartibraregreM 68.0 38.0

eulavevitaleR 98.0 57.0gnillestrohS 37.0 17.0

tneiciffeocnoitalerrocegarevA 48.0 57.0

Table 5The degree of representativity

Principal Component Analysis can be used to obtainthe linear combination of the competing indices thatmake it possible to capture the greatest amount ofdata contained in these different indices. As the tableopposite shows, this results firstly in a maximisationof the degree of representativity. Secondly, and ofequal importance, indices of indices are, byconstruction, systematically less biased than theindices of which they consist due to the fact thatcompeting indices are not all affected in the same wayby the performance measurement bias. Therefore, themaximisation of the explained variance implicitlyleads to a minimisation of the biases. This propertyof indices of indices is useful for evaluating theperformance of alternative strategies.

regulation and the associated lack of transparencyexacerbate this problem considerably. It is thereforecrucial to construct style indices that meet sectorprofessionals’ transparency and reliability requirements.

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 13

3| Alternative investment managementfrom the financial stability perspective

From the financial stability perspective, thedevelopment of the alternative investment industryraises two sets of questions. First, to what extent doesthis management approach and the techniquesinvolved impact on the functioning and dynamicsof financial markets? Second, in view of the specificrisks associated with the alternative investmentindustry, how should roles be divided betweenmarket participants and supervisory authorities forthe oversight of this activity and its development?

3|1 Contribution to the functioningof financial markets

Given the diversity of alternative investmentstrategies, it is not possible to unequivocally assessthe impact of the alternative investment industryon the functioning of financial markets. An approachby management style and an analysis of techniquesused by alternative fund managers prove to be morefruitful, and also make it possible to pinpoint thespecific risk factors associated with alternativeinvestment management.

More complete financial markets

A detailed examination of the functioning of financialmarkets reveals that “pockets” of inefficiency, asdefined in financial theory, i.e. situations in whichasset prices do not reflect all available fundamentaldata, are likely to develop. These anomalies leadin fine to asset price misalignments. A number ofinvestment strategies implemented by alternativeinvestment firms, in particular non-directionalstrategies, aim to exploit these situations 17:

– by providing market liquidity when there appears tobe a lack. In general, given that alternative fundsare not subject to the constraints governing mostother market participants, they can deal withmarket shocks better, and therefore provideliquidity when markets are unbalanced. On

“distressed” debt markets, or high-yield bondmarkets, which are narrow and fragile marketsbecause they do not have a broad natural investorbase, demand from alternative funds maycontribute to limiting excessive pricemisalignments. Likewise, the spectaculardevelopment of the convertible bond market inrecent years is largely due to the capacity of fundsspecialising in this type of arbitrage to absorb anincreasing supply of paper;

– by actively participating in the financial asset pricediscovery process. “Long/short” strategies andarbitrage strategies contribute to ensuring theoverall consistency of financial asset prices.Alternative funds’ strategies are very different inthis area from those of traditional fund managersand may also have, ceteris paribus, a greaterimpact: on the one hand, in their allocationdecisions, they do not face the constraint of notbeing allowed to deviate excessively from abenchmark portfolio and, on the other, they canshort sell securities deemed to be overvalued.

Fuelling destabilising dynamics?

The fear that hedge funds’ strategies may be fuellingdestabilising market dynamics would appear tocontradict the “merits” often attributed to them,i.e. that they are thought to reduce volatility andfoster greater financial market stability. Thecontinuing debates over short selling, and its useby hedge funds, illustrate the complexity of thisissue. There is no doubt that short selling may, inthe context of fragile markets, amplify an imbalanceand facilitate the development of cumulativedepreciation 18. However, this technique, which is notonly used for speculating on the fall in the price of aspecific security, is also implemented by otherplayers. Furthermore, it is often combined with longpositions (i.e. in long/short strategies and arbitragestrategies). Lastly, it should be noted that shortselling can be replicated synthetically using standardmarket instruments such as swaps.

17 It should be noted that the operating methods of these funds do not differ fundamentally from those of the proprietary traders of commercial andinvestment banks.

18 The same argument can be put forward for leveraged securities purchases and the use of derivatives for leveraging a long position, which fuelcumulative appreciation.

Challenges arising from alternative investment management

14 Banque de France • Financial Stability Review • No. 3 • November 2003

More generally, most academic studies carried outon this subject do not attribute an intrinsicallydestabilising role to alternative investment strategies:it does not appear that hedge funds’ positions onmarkets systematically fuel deviations in asset pricefrom “fundamentals” 19, nor do they seem to lead toherd or mimetic behaviour among other marketparticipants or “positive feedback trading” 20.

This diagnosis can be refined by breaking downthe impact of alternative strategies according to:

– type of management style: directional strategies,in particular “trend following” strategies, are bynature more prone to exacerbate sharp pricemovements and amplify the short-term trendsprevailing on markets. The fact that thesestrategies rely to a large extent on leverageaggravates this problem (see below);

– the overall configuration of the markets: whenmarkets are stressed, they are more likely tobecome unbalanced by participants that takespeculative positions, that use a large array ofinstruments or that can more easily make use ofleverage;

– type of underlying market: the successive exchangerate crises of the 1990s, in both developedcountries (ERM) and emerging countries (Asiaand Latin America) have demonstrated that insome circumstances a speculative attack on acurrency may be self-fulfilling if the marketbecomes convinced that, in the short run, it willbe too costly for the authorities to defend theexchange rate, even if it had initially beensustainable. These episodes have also showedthat, even though it is traditionally considered tobe one of the most deep and liquid markets, theforeign exchange market is not immune to suchincidents.

Irrespective of the potential destabilising effects ofalternative investment strategies, it should berecalled that the investment mechanisms used intraditional assets management may also have adestabilising impact (short-termism, strictbenchmarking, etc.) 21.

3|2 Exposure to specific risks

Alternative investment management is oftenpresented as offering investors protection againstadverse market movements (i.e. against the risk of afall in prices). This argument should however bequalified. Furthermore, a possible protection againstmarket risk does not mean that no risks exist, butrather that specific risks are present.

Market risk is not systematically absentfrom alternative strategies

Aside from directional strategies, which, clearly, arefully exposed to this form of risk, it is interesting tonote that alternative funds exhibit not only verydifferent correlation levels with traditional assetclasses (equities and bonds), but also that thesecorrelation levels change in line with the directionof markets: studies on conditional correlations havedemonstrated that the correlation levels with thestock market of many alternative strategies increasedduring periods of sharp falls in the market, i.e. exactlywhen decorrelation would be most useful.

Not only does the alternative investment industry facepersistent market risk, but also more specific risks.

Operational risks

The strategies deployed by alternative fundmanagers are often extremely complex, requiring theextensive use of mathematical modelling andsophisticated quantitative techniques. Model risk,whether arising from the definition or theassessment of the risks incurred (see Part 2), is ofparticular relevance. While it is not the only factorresponsible for the spectacular collapse of LTCM(Long Term Capital Management) in autumn 1998,the unsuitability of risk measurement tools(inadequate calibration of the parameters used tocalculate VaR, insufficient records of data used andnon-stationarity of series) is one of the main reasonsbehind this failure 22. The fact that the relative valuestrategies implemented by hedge funds have to beanalysed as statistical convergence strategies ratherthan arbitrages in the strict sense of the term makesit is even more important to focus on model risk.

19 Fung and Hsieh (2000): “Measuring the Market Impact of Hedge Funds”, Journal of Empirical Finance.20 Eichengreen (1999).21 Committee on the Global Financial System (CGFS) (2003).22 Jorion (2000).

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 15

“Manager risk” may also be considered, amongoperational risks, as a specific risk that includescomponents such as the quality of the decision-makingprocess and the actual expertise of the fund manager,which is a crucial factor in the alternative universe.

From liquidity risk to risks associated with leverage

This risk, while it is not specific to alternative funds,takes on a particular relevance and form in thecontext of alternative investment. It is especiallyrelevant because these funds invest in assets whosesecondary markets lack depth and liquidity 23. It isalso significant because alternative vehiclesfrequently finance their positions using borrowedfunds or, to a greater degree, using leverage. Leveragetakes many forms: bank loans, derivatives or repotransactions, short selling techniques and buying onmargin. Yet again, we should stress that alternativefunds are not the only market participants that usethese techniques or leverage. What sets them apartis that they are not constrained by regulatory limitsgoverning this practice. All other things being equal,the use of leverage exacerbates the different risksincurred by funds and reduces their resilience to dealwith unforeseen shocks. In particular, it increasesmarket risk, via the collateralisation mechanismsassociated with debt financing and derivativestransactions: a fall in the price of underlying assetswill trigger margin calls and/or the rapid liquidation,under probably unfavourable conditions, of positionsrefinanced in this way. This is one of alternativefunds’ factors of fragility, and a potential source ofcontagion of the difficulties of some of its participantsto the market as a whole.

It is nevertheless difficult to accurately assess the scaleof the use of leverage by alternative funds: they donot have any mandatory disclosure requirements inthis area, and the available data is patchy as it onlyrefers to leverage recorded in the balance sheet.According to available market data 24, it appears thatalmost three-quarters (74%) of alternative funds mayhabitually use leverage in their transactions (fundsspecialising in defaulted bonds make the least use,with only 52% resorting to this technique, while macroand arbitrage funds are the main users with 89% and82% respectively). The amount of leverage remainslimited, with average leverage ratios of around 2 to 1for hedge funds as a whole, and only exceeds this valuefor 30% of funds. This is a far cry from the extremevalues registered by LTCM (50 to 1).

3|3 The regulatory frameworkof the alternative investmentindustry: a division of rolesbetween market participantsand supervisory authorities

The alternative investment industry has developedin an environment very largely free from theregulatory constraints that limit “traditional” marketparticipants. It could also be said that the industrygrew as a reaction to the restrictions that theseregulations imposed on its participants and toexploit the effects of these limitations.Developments to date have shown that alternativeinvestment management, according to the form ittakes, may contribute positively, to differingdegrees, to the functioning of financial markets. Wecannot however conclude that the development ofthis industry should necessarily be unregulated.Attention should be squarely focused on theconditions in which the alternative investmentindustry is developing for two main reasons.

– The LTCM episode in 1998 illustrated how thethreat of a systemic crisis arising from the failureof a key player, but whose importance on thesemarkets was only realised when it collapsed,could weigh on financial markets.

– The alternative investment industry is currentlyopening up to new types of investors: on the onehand, individual investors (in addition to its initialwealth management and private banking clientele)and, on the other, institutional investors, both ofwhom the law sets out to protect.

The prevention of systemic risk and the protectionof savings are the two main reasons forimplementing regulations to frame thedevelopment of the alternative investmentindustry. As it stands today, this framework is builtaround the close co-operation of marketparticipants and the public authorities, combiningthe self-discipline of the former and the limitedregulatory constraints of the latter. In the mediumterm, the more effective the implementation ofmarket discipline, the less need there will be toextend this regulatory framework.

23 “Congestion risk” is a particular expression of this liquidity risk liable to affect the conduct of an investment strategy: a strategy that is profitablewill gain in popularity and attract new funds until the initial opportunities are exhausted for all those except participants willing to accept anever-increasing amount of risk.

24 Van Hedge Fund Advisors International.

Challenges arising from alternative investment management

16 Banque de France • Financial Stability Review • No. 3 • November 2003

Market discipline

Above and beyond the concerns that had alreadybeen voiced by regulators, even before the collapseof LTCM, this major shock gave rise to a salutaryrealisation on the part of the hedge funds themselves,the institutions financing them and investors, aboutthe need to substantially improve the operatingprocedures of this type of activity and thesupervision to which it should be subject by theircounterparties as well as by their customers.

This realisation led to the development of codes ofgood practices 25 that attempt to establish standardsfor the industry as a whole. The recommendationsthey propose target in particular the internalorganisation of funds (identifying responsibilities,organising risk monitoring), the rules applicable tothe management of different risks (valuation methodsand resources to be implemented) and disclosure ofinformation (to investors, credit suppliers, and evenregulators). While these codes represent a significantstep forward in terms of the governance andtransparency of funds, they are not however legallybinding 26, and their effectiveness therefore remainsuncertain. While the Financial Stability Forumsubscribes to this notion of self-discipline, itnevertheless regularly assesses, together with theJoint Forum, the progress made in these areas, inparticular in the light of recommendations in theReport of the Fisher Group on enhancing disclosure.

Aside from the funds themselves, theircounterparties and investors have a key role to playin the implementation of efficient mechanisms ofdiscipline and self-regulation.

– Credit institutions that finance alternative fundsare at the centre of the market’s self-regulationmechanism. This is particularly the case for primebrokers that provide a complete financial andlogistical service to hedge funds, from thefinancing, executing and post-market managementof transactions (settlement, delivery versuspayment, accounts holding and custody services),to the management of margin calls, organisationof securities borrowing/lending, and even externalinformation and organisation of marketingprogrammes. They are the only players to have acomplete view, in real time, of the situation ofhedge funds.

– The opening up of the alternative investmentindustry to institutional investors also transfersto the latter a specific responsibility in terms ofmonitoring. Because they themselves are subjectto strict reporting requirements and must followa rigorous investment process, these investors arein a position to lend significant momentum toincreasing the transparency of the alternativeinvestment industry. There is no longer anydoubt as to the beneficial effects of the ”disciplineof transparency”. As regards hedge funds, we shallconfine ourselves to the results of a recent studyanalysing the reported performance of thesefunds in the light of their accounts auditingpractices: alternative funds are not usuallysubject to disclosure and auditing requirements.Their performance reporting, recorded in anumber of specialised databases, is also carriedout on a voluntary basis. A study by Bing Lianghighlights the fact that the differences inperformance of the same fund from one databaseto the next (in itself an anomaly) are lesssignificant for audited funds than for others. Thepaper also shows that there is a positiverelationship between the size of the fund and itsuse of auditors, and that funds which make theleast use of leverage on the one hand, and thosewith the largest investor bases on the other, aremost likely to have their accounts audited.Investors and alternative fund managers havestarted fruitful discussions that would bebeneficial to build upon.

A regulatory framework that remains limited

To date, intervention by supervisory authorities hasremained fairly limited. Banking supervisors havealso favoured an indirect monitoring of hedge fundsby stressing, on the one hand, the principles of soundrisk management that should guide relationshipsbetween credit institutions and their counterpartiesof this type, and, on the other hand, by enhancingwhere appropriate the disclosure of their exposuresrequested from credit institutions: in France, forexample, for poorly-rated or unrated counterparties,regulations on reporting large exposures have beenmodified, with credit institutions now being requiredto report exposures in gross rather than net terms.

25 “Sound Practices for Hedge Fund Managers” (February 2000); “Guide to Sound Practices for European Hedge Fund Managers” (August 2002).26 It should be noted however that in France, the guide to sound professional practices currently being drawn up by the Association française de

gestion shall have, after approval by the Commission des opérations de bourse (COB), the status of professional standard.

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 17

Market supervisors, for their part, have focused ondefining (restrictively) the conditions for the sellingof investment products offered by alternativeinvestment funds, with a view to protectingindividual investors.

In this exercise, market authorities must take intoaccount individual investors’ growing appetite forthese types of funds as well as the increasinglydiversified range of alternative products offered bymulti-management or structured investment funds.Without pronouncing on the outcome of thesedeliberations by the market authorities in differentcountries, they appear, at present, to be opting for achange in the access conditions to these products,and a clarification of the regulatory regime, in orderto prevent in particular an uncontrollable off-shoredevelopment of these products. In practice, theseregulatory developments result in promoting theindirect access to alternative products, throughmulti-management and alternative funds of funds.

The development of the multi-management industry

In brief, multi-management gives investors theopportunity to invest in a selection of alternativefunds offering different risk profiles rather than onespecific alternative fund with a particular riskprofile. Alternative funds of funds are the mostdynamic segment of the alternative investmentindustry: they currently account for USD 200 billionin assets under management, i.e. more than a thirdof the assets managed by this industry. Funds offunds have significant advantages for “new”alternative investors given that they selectindividual funds from within an expanding rangeof products, while taking charge of monitoringperformance and relations with alternative fundmanagers. These funds offer a diversification of riskbetween several management styles, and alsoreduce the risk of loss associated with the highhedge fund mortality rate. The multi-managementapproach shares some common characteristics withthe traditional management universe; using amulti-fund manager is a way of managing theagency and asymmetry of information problemsthat underlie the development of the assetmanagement industry. When selecting funds themulti-management fund manager plays a similarrole to that of the traditional fund manager inhis/her asset allocation decisions.

Technically, therefore, funds of funds appear to beone of the favoured vehicles for the large-scaledevelopment of the alternative investment industry.In a number of countries, regulatory developmentsalso lend impetus to this trend.

Regulatory developments

The notion of qualified investor is used in mostjurisdictions to restrict access to alternative productsto investors considered capable of assessing the risksinherent in this management approach and bearingthe potential losses. This restriction may take theform of a minimum subscription requirement (as isthe case most frequently) and/or a minimum incomeor wealth requirement.

These types of restrictions exist both on direct accessto alternative funds and on investment in funds offunds. The more recent regulations on access tofunds of funds are generally much less restrictivethan those on direct access to individual funds. InFrance, for example, access to organismes deplacement collectif en valeurs mobilières (OPCVM) àprocédure allégée, the closest asset managementvehicle to what is usually understood by a hedgefund, is reserved for qualified investors, with aminimum subscription requirement of EUR 500,000.“Contractual funds” 27, created under the financialsecurity bill, will in due course become part ofthis range of funds. However, new regulations onmulti-management funds (see Box 3), set theminimum subscription requirement at EUR 10,000.In Italy, direct access to fondi speculativi, alsorestricted to certain investor categories, is subjectto an initial subscription of EUR 500,000, andEUR 25,000 for funds of funds, accessible toindividual investors. In Germany, a bill currentlyunder review would restrict direct access to hedgefunds to institutional investors, and give individualinvestors the possibility to invest in funds of funds.These rules are equivalent to those in place in theUnited States, where investors are subject to aninitial subscription of USD 25,000 for accessingmulti-management investment products, andUSD 200,000 (or net wealth of USD 1 million) forhedge funds stricto sensu. In the United Kingdom,alternative funds of funds can be marketed withoutrestriction to individual investors as long as theyare listed, but can only invest in funds actuallyapproved by the Financial Services Authority (FSA).

27 These funds, restricted to qualified investors, will operate without an authorisation from the supervisory authority (on the basis of simpledeclaration), and will not be subject to any constraints in terms of division of risk. Nor will they face constraints in terms of asset types. They willbe free to establish the frequency and method of calculating net asset value.

Challenges arising from alternative investment management

18 Banque de France • Financial Stability Review • No. 3 • November 2003

Box 3

Regulating alternative multi-management investments(COB press release of 3 April 2003)

In France, management strategies seeking to deliver absolute returns, uncorrelated with a benchmark index havedeveloped only marginally. They are not widely distributed and account for limited amounts under management.Amid difficult market conditions, demand for these products has grown, mirroring the international developmentof hedge funds. Today, these management strategies are commonly referred to as “alternative”, although this termhas no standard international definition and its substance varies significantly.

In France, alternative investments primarily consist of alternative funds of funds, i.e. French funds invested inoffshore funds or French funds with a specialist bias, such as futures or options). It is therefore necessary to establisha precise legal framework which can be applied to an activity that France has tolerated for almost a decade.

Investment management companies that choose French or foreign funds relying on complex managementtechniques much follow due diligence procedures, which need to be formalised and included in a special programmeof operations (for discretionary management and collective investment fund management). Furthermore, investorsmust be informed of the special characteristics of such products and techniques through the marketing programmeand appropriate informational materials. In order for them to make an informed decision about a particularproduct, prospective fund subscribers and discretionary clients must be clearly informed by means of thefund’s prospectus, discretionary mandate and any promotional literature, of the type of investment involved andthe specific risks inherent in it.

Following several months of industry-wide discussions, the COB recently adopted a series of positions (...) thatestablishes a framework for contributing to the development of alternative investment activity and ensuringproper security. The main rules are as follows 1.

– Management companies managing a fund or a mandate invested in an alternative fund must update theirprogramme of operations accordingly (companies seeking authorisation to exercise this activity must submitthis amended programme beforehand).

– General purpose funds with less than 10 per cent of their assets vested in alternative funds must updatetheir prospectus accordingly (and the management company must update its programme of operations).

– General purpose funds with more than 10% of their assets invested in alternative funds must update theirprospectus. Management companies must supplement their programme of operations with a marketingprogramme (for newly formed funds, these documents must be submitted to the COB as a prerequisite forauthorisation.

The COB will review programmes of operations to ensure that management companies have the necessaryskills and ressources to manage these products.

Existing regulations will be adapted to cover alternative investment funds — notably via the creation of a newclassification: “funds invested in alternative funds” — in 2003. This will be part of an overall regulatory overhaulaimed at taking into account the issues dealt with by the COB (e.g. the working group on management fees andcharges, chaired by Philippe Adhémar) as well as new European directives.

In addition, discussions are still underway with the French Investment Management Association, AFG, with awiew to approving a code of professional conduct for market participants involved in alternative investmentstrategies.

These discussions will be extended, in collaboration with the industry as a whole, to determine the bestarrangements for implementing direct alternative strategies in funds organised under French law.

1 The decision statement and special programme of operations are available on the COB website at www.cob.fr.

Challenges arising from alternative investment management

Banque de France • Financial Stability Review • No. 3 • November 2003 19

All in all, the alternative investment industry does not deserve to be excessively praised or maligned.Looking to it to find the solution for the difficulties recently encountered in traditional asset managementwould be just as simplistic as branding it a systematic factor of financial market destabilisation:alternative investment can indeed be an instrument for risk diversification and, in this respect, auseful tool in overall portfolio management, while contributing to greater market efficiency. But itcan also contribute to, or even amplify market imbalances. More than simply a new asset class,alternative investment management should be seen for what it really is: an ensemble of unconventionalinvestment strategies, often very different from one another, involving traditional asset classes, andcarrying its own specific risks. The spectacular movements observed on financial markets overrecent years, and the disappointment of investors, have accelerated the recognition of the alternativeinvestment industry and just as spectacularly fuelled its development. This first hurdle has nowbeen overcome but many more challenges still face the alternative investment industry: how can aniche activity become a mature industry without losing its particular features? How, over time, canperformance and standardisation be reconciled? In the long term, the answer to these questions willdepend, in particular, on the balance struck between market discipline and the regulatory framework,as well as on the alternative investment industry’s capacity to open up and enhance transparency.We have seen how crucial the complex issue of measuring performance and risk is in this area. Itwill also depend on the developments that the “traditional” asset management universe will necessarilyundergo: if it evolves towards a “core-satellite model”, this would reinforce the position of alternativeinvestment management alongside a more systematic index-linked approach. Conversely, if traditionalfund managers return to a more pro-active approach, this would no doubt limit the alternativesector’s growth margin.

A recent study by the FSA has shown that individualinvestors have little appetite for direct access tohedge fund products.

As the new regulatory regime for alternativemulti-management in France shows (see Box 3), thisindirect access to alternative investment productsis often coupled with the implementation of a newregulatory framework. The latter aims to ensure thatnot only investors are protected (specific monitoringof sales and marketing conditions, restricting access

to alternative investment products, banning directmarketing of underlying funds and updatingprospectuses) but also, more broadly, that theoperational risk associated with this managementapproach is prevented (management firmsconcerned are required to submit a specialprogramme of operations to the COB for approval,with a view, in particular, to ensuring the expertiseof management teams, the suitability of specific riskcontrol procedures, the existence of technicalresources, etc.).

Challenges arising from alternative investment management

20 Banque de France • Financial Stability Review • No. 3 • November 2003

Ackermann (C.), McEnally (R.) and Ravenscraft (D.)(1999): “The Performance of Hedge Funds: Risk,Return and Incentives”, Journal of Finance, vol. 54,n°3, p. 833-874

Agarwal, (V.) (2000): “Generalized Style Analysis ofHedge-funds”, The Journal of Asset Management,vol. 1, n°1, p. 93-109, July

Agarwal (V.) and Naik (N. Y.) (2000a): “On taking the‘Alternative’ Route: Risks, Rewards Style andPerformance Persistence of Hedge Funds”, Journalof Alternative Investments, 2, p. 6-23, Spring

Agarwal (V.) and Naik (N. Y.) (2000b): “Multi-PeriodPerformance Persistence Analysis of Hedge Funds”,Journal of Financial and Quantitative Analysis, 35,p. 327-342

Agarwal (V.) and Naik (N. Y.) (2003): “Risks and PortfolioDecisions Involving Hedge Funds”, Working paper

Alternative Investment Management Association(2002): Guide to Sound Practices for European HedgeFund Managers, August

Amenc (N.) and Martellini (L.) (2003): “The BraveNew World of Hedge Fund Indices”, Working paper,EDHEC, Misys Risk and Asset ManagementResearch Centre

Amenc (N.), Curtis (S.) and Martellini (L.) (2003a):“The Alpha and Omega of Hedge Fund PerformanceMeasurement”, Working paper, EDHEC, Misys Riskand Asset Management Research Centre

Amenc (N.), Martellini (L.) and Vaissié (M.) (2003b):“Benefits and Risks of Alternative InvestmentStrategies”, Journal of Asset Management, vol. 4, n°2,p. 96-118

Amin (G.) and Kat (H.) (2003): “Hedge FundPerformance 1990-2000: Do the Money MachinesReally add Value?”, Journal of Financial andQuantitative Analysis, vol. 38, n°2, June

Asness (C.), Krail (R.) and Liew (J.) (2000): “DoHedge Funds Hedge?”, Working paper, AQR CapitalManagement

Association française de la gestion financière(AFG-ASFFI) (2002): “Gestion alternative : recueild’opinions”

Basel Committee on Banking Supervision (BCBS)(2000): “Banks’ interactions with Highly LeveragedInstitutions: Implementation of the BaselCommittee’s sound practices paper”, January

Brealey (R.) and Kaplanis (E.) (2001): “Hedge Fundsand Financial Stability: An Analysis of their FactorExposures”, International Finance 4:2,p. 161-187