challenges and prospects of real estate investment trusts

TRANSCRIPT

i

CHALLENGES AND PROSPECTS OF REAL ESTATE

INVESTMENT TRUSTS (REITs) FINANCING OF REAL

ESTATE IN KENYA

KEVIN MBURU KAMAU

D61/79235/2015

A RESEARCH PROJECT SUBMITTED IN PARTIAL

FULFILMENT OF THE REQUIREMENTS FOR THE DEGREE

OF MASTER OF BUSINESS ADMINISTRATION OF THE

UNIVERSITY OF NAIROBI 2016

ii

DECLARATION

This research project is my original work and has not been presented for

examination in any other University. I further declare that I followed all the

applicable ethical guidelines in the conduct of the research project.

Signature: ……………………… Date: ………………...............

Kamau Kevin Mburu

Reg. No.: D61/79235/2015

This research project has been submitted for examination with my approval as the

University Supervisor.

Signature: ……………………… Date: ………………...............

Supervisor: Mr James M. Karanja

Lecturer School of Business

Department of Accounting and Finance

University of Nairobi.

iii

DEDICATION

I would like to dedicate this Research project to my family, most especially my parents for

their effort, who have helped me throughout my studies in Nairobi University with proper

support and encouragement to proceed and succeed.

I would also like to dedicate this project to my friends who have also helped me in various

stage in the project to facilitate the completion of this project.

iv

ACKNOWLEDGEMENT

I am grateful to my research supervisor Mr. James Karanja for her professional support and

guidance throughout the stages of the project I was undertaking. I am also grateful to my

parents for their continuous support and encouragement.

v

ABSTRACT

A REIT (real estate investment trust) is a real estate firm which acquires,

constructs or manages different types of buildings that are put up in various

locations. REITs are a form of financing instruments from firms that source

funds to build or acquire real estate assets which they sell or rent to generate

income for the investors whom invested their funds in the firm. The income

that is generated by the firm over the period is then distributed to the

shareholders at the end of the financial year. The main aim of this study is to

investigate the various challenges and prospects that such an investment can

attain within the real estate sector in the country. This is a new

venture/investment that has been introduced in the Kenyan market and this

study will be able to identify the various challenges that affect the REITs and

prospects that such an investment holds once it picks up in the country.

Based on the type of research to be carried out the best research design that

would be appropriate for this research is an exploratory study research design

approach due to the fact that this is a very new investment that has been

introduced into the Kenyan market. The population of the study was 156

developing firms within Nairobi and a sample of 70 was selected for a

representative of the population. Both primary data through the use of

questionnaires and secondary data was used in the study.

The challenges that have been identified are policy, regulations and

procedures, high dividend pay-out, culture of capital structure within the

organization and market awareness of the investment vehicle. The prospects

that have also been identified by this study were increased commercial and

residential properties as a result to increased supply of real estate properties

within the country, new pool of investors in real estate, huge source of capital

for various real estate projects that require high source of income funding and

high liquidity in the real estate sector. Interest rates, inflation rate and market

capitalization were analyzed and concluded that these factors have a

significant effect of on the REITs financing of real estate in Kenya. Further

studies should be done on the various factors that affect the REITs financing of

real estate in Kenya.

vi

Table of Contents DECLARATION .................................................................................................................................... ii

DEDICATION ....................................................................................................................................... iii

ACKNOWLEDGEMENT ..................................................................................................................... iv

ABSTRACT ............................................................................................................................................ v

LIST OF ACRONYMS ....................................................................................................................... viii

CHAPTER ONE ..................................................................................................................................... 1

INTRODUCTION .................................................................................................................................. 1

1.1 Background of the Study .............................................................................................................. 1

1.1.1 Real estate investment trust (REIT) Financing of real estates ............................................... 4

1.1.2 Challenges and prospects of REITs ....................................................................................... 4

1.1.3 Challenges and prospects of REITs financing of real estate .................................................. 5

1.1.4 Real estate in Kenya ............................................................................................................... 6

1.2 Research problem .......................................................................................................................... 6

1.3 Research objectives ................................................................................................................. 7

1.4 Value of the study ......................................................................................................................... 8

CHAPTER TWO .................................................................................................................................... 9

LITERATURE REVIEW ....................................................................................................................... 9

2.1 Introduction ................................................................................................................................... 9

2.2 Theoretical Review ....................................................................................................................... 9

2.2.1 Trade off theory ..................................................................................................................... 9

2.2.2 The bird-in-the-hand theory of dividends .............................................................................. 9

2.2.3 Theory of financial access .................................................................................................... 10

2.3 Determinants of REITs financing the real estate sector ............................................................. 10

2.3.1 Market capitalization............................................................................................................ 10

2.3.2 Interest rates ......................................................................................................................... 11

2.3.3 Inflation ................................................................................................................................ 11

2.3.4 Challenges of REITs financing ............................................................................................ 11

2.3.5 Prospects of REITs financing .............................................................................................. 11

2.4 Empirical studies ......................................................................................................................... 12

2.4 Conceptual Framework ............................................................................................................... 17

2.6 Chapter Summary ................................................................................................................. 18

CHAPTER THREE .................................................................................................................................... 19

RESEARCH METHODOLOGY .................................................................................................................. 19

3.1 Introduction ................................................................................................................................. 19

vii

3.2 Research design .......................................................................................................................... 19

3.3 Population ................................................................................................................................... 19

3.4 Sample design ............................................................................................................................. 20

3.5 Data collection ............................................................................................................................ 20

3.6 Validity and Reliability ............................................................................................................... 20

3.7 Data analysis ............................................................................................................................... 20

CHAPTER FOUR ..................................................................................................................................... 22

DATA ANALYSIS AND PRESENTATION ................................................................................................... 22

4.1 Introduction ................................................................................................................................. 22

4.2 Response Rate ............................................................................................................................. 22

4.2 Data findings ............................................................................................................................... 23

4.2.1 Challenges of REITs financing of real estate ....................................................................... 23

4.2.2 Prospects of REITs financing of real estate ......................................................................... 24

4.2.3 Model Results on interest rates, inflation rate and market capitalization ............................ 25

4.3 Summary and Interpretation of Findings .................................................................................... 27

CHAPTER FIVE ....................................................................................................................................... 29

SUMMARY, CONCLUSION AND RECOMMENDATIONS ......................................................................... 29

5.1 Summary ..................................................................................................................................... 29

5.2 Summary findings and conclusion .............................................................................................. 29

5.3 Recommendations ....................................................................................................................... 30

5.5 Limitations of the study .............................................................................................................. 30

5.6 Suggestions for further study ...................................................................................................... 30

REFERENCES: ......................................................................................................................................... 31

APPENDICES ...................................................................................................................................... 33

QUESTIONNAIRE ...................................................................................................................... 33

viii

LIST OF ACRONYMS

REITs: Real estate investment trust(s)

UPREIT - Umbrella partnership real estate investment trusts

NSE- Nairobi securities exchange

IPO- Initial public offer

NOI- Net operating income

ANOVA- Analysis of variance

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

REITs are used as a financing vehicle for companies in the sourcing of funds

for various real estate projects. They have been used in various countries in the

various real estate projects. REITs are real estate financing vehicles that are

modelled after mutual (or unit trust) funds. REITs own, and in most cases,

operate income-producing real estate projects. The REITs structure are created

to provide all type of investors (private individuals and institutions) an

opportunity to invest in the real estate sector through purchase of the REITs

firm’s shares and getting a share of the income earned from the various

properties at the end of a given period once income is distributed in form of

dividends. Public REITs are listed into stock exchanges. As of mid-2012, there

were more than 410 real estate companies from more than 37 stock exchanges

representing an equity market capitalization of more than US$ 1 trillion with a

large share from REITs.

The genesis of the REITs can be traced back in 1960 where through a

legislative action the U.S Congress gave all Americans, the opportunity to

invest in income producing real estates in a manner similar to how individual

and institutional investors invests in shares and bonds. Income producing real

estate refers to land and the improvements on it such as construction of

apartments, offices, industrial facilities and hotels. REITs may invest in

various construction or acquisition of buildings thereby generating income

through collection of rent. They may also advance in the mortgage sector or

mortgage backed securities which are secured to properties, helping to finance

the properties and generating interest income from lending.

In most emerging and developed economies REITs own many forms of the

shopping malls, apartment building, student’s hostels, homes, medical

2

facilities, office building, hotels, cell towers, etc. In these markets REITs

contribute significantly in jobs creation and investment income to national

economies.

REITs can be classified into two different categories which are equity REITs

or mortgage REITs. Equity REITs get most of their income from rent from

either leasing or renting out their properties. Mortgage REITs grow most of

their income from interest earned on their investment in mortgages or

mortgage-backed securities. REITs have many potential advantages to those

who have interest in the real estate sector i.e. real estate developers, investors,

and the economy.

There are various regulatory frameworks that are set up to which emphasize

how the REITs should be managed and run so as to raise finances and capital

for the various real estate projects that the REITs want to undertake. This is

normally a legal framework, which emphasizes and provides rules relating to

eligibility, responsibility, key players, listing procedures, operationalization of

REITs and many more in relation to REITs.

The legal framework and the infrastructure enable the operationalization of the

publicly listed REITs availability, therefore property and mortgage developers

such as the National Housing Corporation, Pension funds, and other such

institutions may consider making use of this platform to facilitate not only in

enabling private individuals and professional institutional investors to invest

and have ownership in the vibrant real estate industry but also enable real

estate developers to access more efficient, effective, better priced and less

costly public funding for speedier development of properties and mortgage,

being either housing, commercial or industrial properties. In actual fact, less

costly funding means lower cost for houses and commercial or industrial

properties and hence more affordable houses, office space and industrial

properties in our economy.

Once the initial public offer (IPO) is under taken in the primary market the

securities will be traded in the secondary market thereby enhancing liquidity of

3

the investments in the REITs market. REITs are highly liquid method of

investing in real estate. Private individuals can invest in REITs by investing in

the shares at the IPO or through acquiring the shares or securities in the

secondary market or investing in various mutual funds that specialize in the

REITs investment market. This enables retail investors and also institutions to

become active participators in the real estate industry through owning shares in

such REITs firms. For pension funds, this may also be one of the effective

mechanisms to enable their members to participate in the ownership of assets

created by their contributions.

In other African countries with relatively similar economic aspects, Ghana’s

Home Finance Company (now HFC Bank) established its first REIT in 1994.

HFC Bank, as the forefront of mortgage financing in Ghana has successfully

been using various collective investment scheme, of which REIT is part of,

and are regulated by the Securities & Exchange Commission of Ghana.

In 2007 the Securities & Exchange Commission (SEC) of Nigeria set and

issued guidelines for the registration, issuance and operationalization of REIT.

The first successful REIT was launched in 2008 enabling the Union Homes

Hybrid Real Estate Investment Trust to raise close to 50 billion. REITs have

existed globally for the past 50 years, however the modern day REIT era can

only be traced to the early 1990s and since that time, in which the real estate

sector has seen various changes which were driven by the shift from privately

to publicly owned real estate and the resulting migration of assets and talent

into the public markets (Smotrich et al. 2012).

In Kenya, the capital markets regulator –CMA- have from December 2013 to

date licensed five companies to manage REITs in their preparations to launch

REITs products in the Nairobi Stock Exchange later this year. REITs were

introduced in the Kenyan market through the Nairobi securities exchange

(NSE) on 22 October 2015 with the launch of the first ever REITs by Stanlib

Fahari I REIT. This was the launch of the REITs investment through the initial

public offer (IPO) at the NSE.

4

1.1.1 Real estate investment trust (REIT) Financing of real estates

Real estate investment trusts (REITs) are pass-through vehicles designed to

facilitate the flow of rental income and/or mortgage interest to investors,

(Smotrich et al. 2012). A real estate investment trust (REIT) is a company that

acquires or constructs and operates, income-producing real estate properties.

The real estate properties can be in form of commercial properties such

as offices, small business establishments and residential properties such as

apartments and also warehouses, hospitals, shopping centers, hotels and

even timberlands. Some REITs also engage in financing real estate and

therefore setting up various buildings for both commercial and residential

purposes. REITs normally in most cases raise finances via equity and have a

special tax status which allows them to avoid corporate taxation if all or most

the income earned from such real estate properties is paid out to the

shareholders in form of dividends at the end of a specific period. This REIT

structure enables small business transactions with a high liquidity and a

transparent price in real estate investment.

Legal notice no.116 (2013) states a real estate investment trust scheme may be

structured as a D-REIT or an I-REIT. D-REIT is a type of REIT in which the

investors pool their money together for purposes of acquiring real estate with a

view of undertaking development and construction projects and associated

activities and the return is the sales proceeds. I–REIT is a type of REIT in

which the investors pool their money for purposes of acquiring long term

income generating real estate including housing, commercial and other real

estate and the return is rental income. These are the two types of REITs

currently established in Kenya by Stanlib Fahari I–REIT which introduced the

I-REIT and Fusion capital which has just recently introduced the D-REIT.

1.1.2 Challenges and prospects of REITs

They are various challenges and prospects with relation to the REITs

investment that can be identified. The study will analyze four of the major

challenges and four of the major prospects in relation to REITs in the market.

5

The challenges will be the reason as to why the REITs in the country have not

properly taken off and the issued REITs in the NSE have not yet properly

taken of due to the undersubscription for both issues. The I-REIT which was

issued by Stanlib Fahari in 22nd October 2015 was highly undersubscribed.

Kenya’s first Income-Real Estate Investment Trust (I-REIT) issued by Stanlib

Investments was only able to raise Sh3.6 billion of the targeted Sh12.5 billion.

Fusion Capital failed to raise Sh2.3 billion it targeted from its Development

Real Estate Investment Trust (D-REIT), the firm only achieved a 38 per cent

subscription collecting Sh873 million with only four investors against the

requirement of seven. This highlights that their various challenges that are

hindering the REITs financing vehicle from being used in the country.

There are also various advantages of using such an investment as a means of

financing that can be seen from the various other countries in which the REITs

have been successfully been implemented. This has been able to sole the

demand crisis by increasing the supply of both commercial and residential

properties in various countries such as Ghana and Nigeria in which the REITs

has been able to be successful.

1.1.3 Challenges and prospects of REITs financing of real estate

In this study the challenges that have been experienced in using REITs for

sourcing of funds for financing of the real estate projects for both commercial

and residential will be determined and carefully analyzed. The real estate

sector in Kenya has a huge demand for both commercial and residential

properties however the supply of the same cannot meet the demand and one of

the major issues is real estate finance which is a key issue for most developers.

This study has examined one of the possible means of sourcing funds for the

real estate and the challenges of using REITs as a means of sourcing funds in

the Kenyan market.

This study also examined the various prospects that are available through the

use of REITs as a means of finance in the real estate sector. Various real

estates have been funded through the use of REITs in various countries and

this has assisted in meeting the demand for the same. The REITs can bridge

6

the gap between demand and supply in the country. This can see many

residential and commercial properties set up in the country with the use of the

finances acquired through IPOs for the REITs companies.

1.1.4 Real estate in Kenya

Real property was defined as all the interests, benefits, rights and

encumbrances inherent in ownership of physical real estate, where real estate

is land together with all improvements that are permanently affixed to it and

all appetences associated thereto (Robert & Johnson, 1996). The number of

properties in comparison to the demand in the country is not at all equal to the

supply of such properties due to the fact that the growth rate of demand

outweighs the supply. This was an opportunity that many investors have taken

up in the real estate sector properties in Kenya. The real estate period of boom

in which it was performing at its peak survived the 2008 Post Election

Violence and global economic downturn that crippled other sectors such as

tourism and agriculture which showed that this sector was very strong in the

country and was very profitable. The construction sector is approximated to

have created 82,000 private sector jobs in 2010 (Mulupi, 2012).

In the period for 2011 and part of 2012 the real estate sector growth had a

server negative effect this was due to the high interest rates that were

experienced during the period. This lead to a lot of construction of properties

been postponed and left hanging for some time due to the mortgage interests at

the time going to as high as 30%. However, with the fall of interest rates the

sector picked up and the growth rate increased. This was from a study carried

out by knight Frank for the 3rd quarter for the year ended 2012.

1.2 Research problem

Ogedengbe and Adesopo (2003) did a study which showed very that such

problems as interest rates, inflation rates and the red tape in the borrowing of

loans affected the financing of such properties in Nigeria to a great extent

which lead to a weakening in the real estate development in the country. This

clearly shows there are clearly financing issues in the real estate sector in

which REITs can be used as an alternative source of financing.

7

Kenya’s economy expanded overall by 4.9 per cent in the first quarter 2011

compared to 4.3 per cent in the same period in 2010; the real estate sector,

renting and business services grew by 3.8 per cent in the same period which

analysts attribute to a more vibrant property market and shifting consumer

demands (Waithaka, 2011). The Kenyan economy is growing at a high rate

with comparison to the real estate sector. This means that real estate properties

are not matching the rate at which the economy is growing at and one of the

various reasons is due to finances. The challenges in the up taking of REITs in

the country has to be identified and corrective measures put in place so as to

enable a vibrant financing for the supply of real estate properties. This will

enable the growth of the real estate sector and demand of real estate properties

both residential and commercial will be met.

This study0 took a closer look at the challenges and prospects of REITs as an

investment which focuses on the real estate properties. They are various

challenges that are affecting the REITs investment and this is hindering on the

prospects of such an investment being fully realized in the country. The

question that this study focused on is what are the challenges and prospects of

using the REITs for the financing of real estate projects and developments

within the country plus also the factors that affect REITs financing of the real

estate in Kenya?

1.3 Research objectives

i) To identify the challenges and ascertain the level/degree in which

these challenges affect the REITs financing of real estate in

Kenya.

ii) To identify the prospects and ascertain the level/degree in which

the prospects affect the REITs financing of real estate in Kenya.

iii) To analyze the effect of the determinants of REITs on the

financing of real estate in Kenya with the use of REITs

8

1.4 Value of the study

This study enabled us to properly understand the REITs financing of the real

estate sector and the various challenges that are being faced in the up taking of

the REITs as a source of financing in Kenya. These challenges that were

hindering the fully utilization of the EITs investment in the country should be

known so as corrective measures can be set up to find solutions to some of

these major challenges. This study will therefore enable us to identify some of

the challenges that affect the REITs being used as a source of financing for the

real estate sector.

It also enabled us to clearly outline the various opportunities that such an

investment could bring if various investors are encouraged to invest in the

same. There are various potential prospects that can be realized from the

REITs financing. This is still quite a new investment market in Kenya but it

has a lot of potential to meet the current high demand for real estate sector.

This study would benefit the developers of such real estate. It would be able to

allow developers look for various kinds of finance depending on the various

developments that they are undertaking given the fund requirement for such

developments.

This study would also be useful to various investors in the identification of

various areas in which the can be able to invest their funds and earn good

returns.

9

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

REITs are investments in the business world and have significant impact on

business activity in relation to real estate properties both commercial and

residential. Globally, various studies on REITs have been done and several

theories have been proposed and tested for empirical validation.

The area of focus in this chapter will be the various challenges and prospects

of REITs financing real estate in Kenya. The areas covered here are theoretical

review, empirical review both local and international and discusses the

literature gaps.

2.2 Theoretical Review

2.2.1 Trade off theory

Murray and Vidhan (2005) did a study on trade-off theory where it is used by

different authors to describe a family of related theories and in all of these

theories, a decision maker running a firm evaluates the various costs and

benefits of alternative leverage plans.

From this theory REITs can be evaluated as a means of financing real estate

and as an alternative better option. This is in terms of cheap financing or

adequate capital requirement required for financing of various real estate

projects within the country both commercial and residential. The trade-off

theory assumes that there are benefits to leverage within a capital structure up

until the optimal capital structure is reached.

2.2.2 The bird-in-the-hand theory of dividends

Popescu and Visinescu (2009) did a review on the capital structure theories

and identified this theory of bird in the hand is a by-product of the MM

irrelevance argument in that stockholders are indifferent between dividends

today and capital gains tomorrow. The investors are indifferent between the

10

dividends they gain today and the capitals gains that they could gain in future.

They thus prefer the dividends that is for certain that they will gain today

rather than the uncertain capital gains to be gained in the future.

The capital gains that are paid in future can be discounted to the equivalent

amount to the dividends paid out today given the risk of uncertainty of future

gains. This is why investors would prefer a firm that pays out high dividends

against a firm that pays out low dividends in light of future capital gains. A

lower required return results in a higher stock price for firms that match the

high current payout pattern desired by bird-in-the-hand investors. Basically for

investors that prefer investments that payout huge dividend from the incomes

that are earned from a company ten the REITs is such an investment for such

investors as it pays out almost all income earned from such real estate

properties as dividends.

2.2.3 Theory of financial access

Theory suggests that financial exclusion acts as a brake on economic

development, this basically points out that the lack of proper access to

financial financing can lead to the hindrance of real estate development in a

particular area which relies on financing to be able to acquire the resources for

development of various properties.

This is why financial instruments such as REITs would assist in the sourcing

of new funds for various projects in the real estate sector that require a huge

source of funds to be able to be undertaken. The various investors will earn

value for their investments through returns in form of dividends.

2.3 Determinants of REITs financing the real estate sector

2.3.1 Market capitalization

Olanrele (2014) did a study on factors that affect REITs whether they remain

constant or not and found that market capitalization is a factor that determines

the performance of the REITs investment. Market capitalization refers to the

total dollar market value of a company's outstanding shares. The capitalization

rate is the rate of return on a real estate investment property based on the

11

income that the property is expected to generate. The capitalization rate could

be calculated by dividing the net operating income (NOI) by the current

market price of the shares of the gives firm. This is one of the determinants of

having a vibrant REITs market in a given economy since the market

capitalization of the properties which are owned by such REITs companies

will be essential for the performance of REITs.

2.3.2 Interest rates

Interest rate increases are likely to be met by REIT price declines. The

increase in the interest rates will require huge returns from REITs and this will

make REITs unattractive if they will not be able to meet the returns of their

investors during periods of huge interest rates.

2.3.3 Inflation

Earliest study by Chan, Hendershott, and Sanders (1990) indicate that there are

three factors driven of REIT and general stock market, i.e. changes in the risk,

term structure and unexpected inflation. Inflation will affect the returns of the

REITs due to the fact that investments will yield a low income returns due to

the cost of revenue going up thereby reducing the returns of various

investments. This basically means with high inflation the will be little or no

capital to invest in such REITs thereby reducing the overall income and

returns of the investment.

2.3.4 Challenges of REITs financing

The major challenges that are currently being faced by REITs on a global scale

are current policy, institutional and regulatory framework, tax incentives for

the REITs investment, high capital requirement so as to get into the REITs for

issuance of the IPO, lack of proper awareness of the investment vehicle and

high dividends payout which results into low plough back into the company

for further investments.

2.3.5 Prospects of REITs financing

The major prospects of the REITs investment on a global scale are infusion of

additional capital which could reduce the supply gap of real estate assets both

residential and commercial, it would open up real estate investing to a whole

new pool of investors and bring up a more equitable ownership structure for

12

real estate assets, would expand the range of financing for the real estate

developers and this would create more liquidity in that one can easily liquidate

their shares and get their funds.

2.4 Empirical studies

Gumbs (2001) did a study on the viability of the REIT structure as a vehicle

for real estate development. This paper reviewed industry articles, past studies

on the effects of development on REIT performance, and interviews with key

personnel of the REITs and private development firms profiled in this thesis.

The thesis concluded that the REIT format is an effective vehicle for real

estate development although skilled management is vital to exploiting its

inherent potential. This study basically identifies REITs as an investment that

could be used in financing real estate sector in the developing and construction

of both commercial and residential properties.

Lee and Stevenson (2004) did a research on the case for REITS in the mixed-

asset portfolio in the short and long run. Poor performance of the U.S stock

market in the period of 2003 resulted into REITs been seen as an attractive

addition to the mixed-asset portfolio. The time period of the study was from

1980 to 2002 and investigated if REITs had a position in the efficient portfolio

over varying time horizons which were estimated over a range of four

alternative rolling periods. The results highlighted that REITs do play a

significant role over both different time horizons and holding periods. The

findings show that REITs attractiveness as a diversification asset increase as

the holding period increases. This study basically views REITs as a diversified

investment for the various investors and could be used as an investment plan in

various mixed-asset portfolios and earn returns for such portfolios. For

investors who normally have a diversified portfolio REITs investment could

act like a diversified investment.

Muchiri (2006) did a study that examines the attitudes of Kenyans towards real

estate securitization. The research design used in the study was an exploratory

study and was mainly qualitative in nature. This design was chosen since the

concept is relatively new and had not taken root in the country. The population

13

for this study consists of every potential investor in the stock exchange in

Kenya. All owners of real estate whose value is equal to, or exceeds the

minimum required share capital and net asset value for listing at the Nairobi

stock exchange qualify as potential promoters of a securitized real estate IPO.

The sample of the study consisted of both institutional investors would be the

most conveniently placed to provide insight into the questions raised, property

consultants, in their capacity as advisors, this group has the ability to influence

investment in a particular direction and trustees of some of the pension funds

and officials of co-operatives that hold substantial property. This information

was obtained using an in-depth interview. Such an interview provided

opportunities to probe answers and allowed the interviewee to build on their

answers. The qualitative data was used in the analysis of the findings from this

research. The study concluded that professionals and ordinary investors would

be ready to put their money in securitized real estate. However, the readiness

to invest in shares of property companies went down as the amount involved

went up. In addition, compared to owning a property most of the respondents

favored owning a rental house to shares in a property company. This study

basically states that given the amount required to invest in REITs investors

would actually invest in the issues of REITs IPO.

Konagai (2009) did a research on Japan-REIT performance which intended to

recognize the performance of REITs in Japan (J-REITs). This was done by

conducting two kinds of studies the to do “factor loadings” being the first

which sort to identify systematic risks of long run investment performance in

J-REITs and the second being to demonstrate “Pure Play Indices,” segment-

specific indices of REIT-based property market returns by tracking monthly

REIT return data and property holding data. The first study employed the

Fama-French three-factor model for monthly J-REIT returns from

September2001 to September 2008. The model resulted in a limited

explanatory power for the J-REIT performance, which was probably due to too

short a market history, as in the past research. The second study applied the

Pure Play Indices to the J-REITs for office, residential, and retail segments

since January 2006 when the J-REIT market became sizable enough for the

study. The study concluded that as the market matures with more data

14

accumulated this two-fold study that shows demonstration of returns from J-

REITs will become more valuable to derive risk of J-REITs and different types

of information of properties. The performance of REITs can only be seen once

they become mature with a good history background on the same.

Muchuki (2010) did a study on real estate as an important investment asset

class but it posed considerable problems for portfolio managers in valuing

direct real estate investment. Real estate illiquid nature increases transaction

costs yet it is assumed to be a safer asset for long term investment. Real estate

can be purchased (direct investment) or the investment can take place through

land held by listed or unlisted companies (indirect investment). REITs are the

only truly liquid assets related to real estate investment. Indirect investment in

real estate investment trusts (listed REITs) transforms the illiquid nature of

direct real estate and offer more liquid investment vehicles thus forms part of a

well-diversified investment portfolio. Public REITs did not exist in Kenya at

the time. This study investigated whether there exits REITs needs among

institutional investors trading at Nairobi Stock Exchange. A sample of 30

institutional investors consisting of pension fund managers and unit trusts was

used. The findings showed that investors would invest in REITs if they were to

be introduced at the exchange and therefore confirmed that REITs needs do

exist among institutional investors at the NSE.

Alias and Tho (2011) did an analysis on the performance of REITS

comparison between M-REITS and UK-REITS. The United Kingdom was one

of the recent countries to enter into the tax efficient REITs regime. This took

place early in the year 2007. At the moment, it ranks fourth in terms of market

capitalization based on the Global REITs report 2008. Malaysia, with a long

history of Unit Trust Funds with some recently converting to REIT, has yet to

achieve the size of UK-REITs. This research analyzed the performance of six

selected REITs in both countries. Nevertheless, prior to the performance

analysis, the mechanism as well as the legislation adopted in regulating the

respective REITs regime was discussed. In addition, factors which contributed

to the variance of performance of REITs are presented and further discussions

are made based on the performance analysis done. The findings and analysis of

15

the study showed that the total revenue was the main factor affecting the

performance for both the largest M-REITs and UK-REITs. Furthermore, the

study views demonstrated that for every billion increase in market

capitalization, the profit margins generated by the REITs will raise by

approximately 9%. This study was a basic comparison of REITs growth in the

various countries since it took off in the U.S. and has concluded that’s the

REITs investment is quickly catching up in the various countries.

Hoesli and Oikarinen (2012) did a study and the aim of this study is to

examine whether securitized real estate returns reflect direct real estate returns

or general stock market returns using international data for the U.S., U.K., and

Australia. In the U.S., the research included four real estate sectors which were

apartments, offices, industrial, and retail while for the U.K. it included just two

real estate sectors which were offices and retail in the study analysis. For the

Australian market, the research used the overall REIT and direct market

indices given that no reliable sector data were available. For securitized real

estate, the FTSE/NAREIT Equity REIT sector level indices are used for the

U.S. and the S&P/ASX 200 A-REIT index for Australia. For the U.K., the

study constructed the REIT indices from the company level price, dividend

and market cap data provided by EPRA. It estimated the vector error-

correction models and investigate the forecast error variance decompositions

and impulse responses of the assets. Both the variance decompositions and

impulse responses suggest that the long-run REIT market performance is much

more closely related to the direct real estate market than to the general stock

market. Consequently, REITs and direct real estate should be relatively good

substitutes in a long-horizon investment portfolio. This study was basically

testing the securitizing of real estate assets and if such a venture would

generate returns in the public as it does in the private sector. The two sectors

both private and public are closely linked and through the private sector one

can be able to analysis if the securitizing of such real estate assets would

generate returns to the public investors.

Nzalu (2013) did an assessment which lloked at the factors that affected the

growth of the real estate sector in Kenya. The study investigated factors such

16

as GDP Growth, the influence of interest rate, inflation rates and population

growth. The design of the study used both quantitative and descriptive

research design to obtain information. The study therefore, investigated the

contribution on the current status of the phenomenon. The population in this

study was real estate investors while the target population included private and

public property investors. Data for analysis was based on the real estate and

renting businesses as sourced from the various Economic Surveys and Kenya

Statistical Abstracts Issues. The data obtained was analyzed by use of the

Statistical Package for Social Sciences (SPSS) to obtain descriptive statistics

and a regression model. From the results the contribution of the factors

affecting real estate growth as measured by Pearson correlation coefficients

indicated that GDP took the highest share with a value of 83% followed by

inflation growth at 78% while interest rate came third with value of 75%.

Population growth contributed the least to the growth in real estate investment

with a value of 29%. The study hypothesis that GDP is the most significant

contributor to the growth in real estate was supported by the data. In addition,

GDP growth, interest rate variation and growth in inflation were found to be

statistically significant determinant of real estate growth. A summary of the

regression results showed that the variables considered could explain up to

about 70% of variations in the investment growth. The study recommended

that Policy measures geared toward improving the economic growth and

curbing rising inflation rates and interest rates should be undertaken as they

increase the investment levels. This shows the need for growth is the real

estate developments across the country and this can be facilitated with the use

of REITs as a financing vehicle for such properties that are required.

Mwathi (2013) did a study on the effect of financing sources on real estate

development in Kenya. The purpose of this study was to establish the sources

of financing real estate in Kenya. In specific terms the study reviewed whether

financing in the real estate originates from; mortgage financing, savings,

venture capital and equity financing. This study employed the descriptive

survey design since it was conducted to describe the present situation, what

people currently believe, what people were doing at the moment and so forth.

The population of the study was all the real estate firms in Nairobi. This study

17

used secondary data for five years. Data was analyzed using Statistical

Package for Social Sciences (SPSS) and results were presented in frequency

tables and charts. The findings indicated that mortgage financing is the most

used source of financing, with equity and venture capital being the least source

of financing used. The findings also indicated that there is a significantly

positive relationship between mortgage financing and real estate development.

However, the findings recommended that to increase use of equity and venture

capital as a source of financing will require businesses to sell their ideas to

people who have money to invest. Equity and venture capital financing can be

a good source of financing if well implemented in the country.

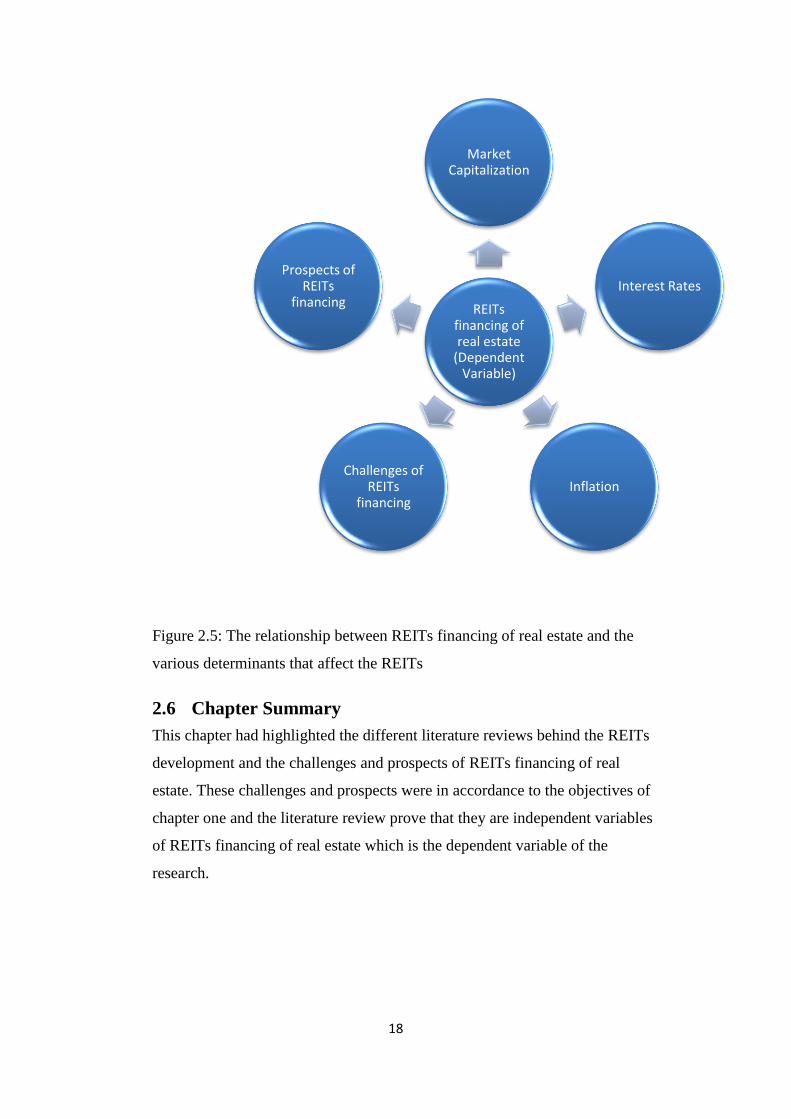

2.4 Conceptual Framework

The conceptual framework for this study would show the various determinants

for the REITs financing the real estate in the country. It was used to show the

independent variables and the dependent variables and the relationship

between such variables as stated in the above literature review.

The various determinants of REITs financing of real estate that this study will

focus on are as follows:

i) Market capitalization

ii) Interest rates

iii) Inflation

iv) Challenges of REITs financing

v) Prospects of REITs financing

18

Figure 2.5: The relationship between REITs financing of real estate and the

various determinants that affect the REITs

2.6 Chapter Summary

This chapter had highlighted the different literature reviews behind the REITs

development and the challenges and prospects of REITs financing of real

estate. These challenges and prospects were in accordance to the objectives of

chapter one and the literature review prove that they are independent variables

of REITs financing of real estate which is the dependent variable of the

research.

REITs financing of real estate

(Dependent Variable)

Market Capitalization

Interest Rates

InflationChallenges of

REITs financing

Prospects of REITs

financing

19

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

This chapter contains how the project will be carried out in terms of research

design to be used for the study, population of the study from where the data is

to be collected, data collection method to be used, analysis of the data

collected, sample to be used in the research and the method which is to be used

in carrying out the analysis. This is basically the architecture or the layout of

the research framework.

3.2 Research design

This research design that was chosen to undertake this study was an

exploratory design. An exploratory design study is a research that aims to seek

new insights into phenomena, to ask questions, and to assess the phenomena in

a new light, (Saunders et al, 2003). This design was chosen since the concept

is relatively new and had not taken root in the country. This will enable to

conduct the research on the new investment that has been started in the country

just recently in the ear 2015.

3.3 Population

We currently had only two REITs companies in Kenya, this study will gather

data from various developing firms across Nairobi. The population of this

research will be the various developing companies/firms in Nairobi County.

There is a huge population of various developing firms in Nairobi a total of

156 companies and due to time limit a sample will be chosen to represent the

vast population. These are the institutions that source for the various funds to

be used in the construction of such real estate properties the challenges and

prospects that they could experience from the REITs investment.

Secondary data collected will be on a monthly basis till June 2016 since the

existence of REITs in Kenya.

20

3.4 Sample design

Due to the large number of various developing companies located within

Nairobi, the research will collect data from 70 developing companies within

Nairobi to be the representative data and also various articles and statements

that will have data containing to the determinates of the performance of REITs

in Kenya.

3.5 Data collection

Data would be collected from a sample selected through convenience

sampling. The main research instruments to be used in the collection of data

are questionnaires. The design of the questionnaire would include multiple-

choice questions; fill in questions and also questions that required ranking of

answers. This would make it easier to do the analysis of the findings from the

data collected. The questionnaires would be printed and handed to various

developers and developing companies within Nairobi.

There will also be the use of secondary data for a proper analysis from the

various financials that are available currently so as to cover all the relevant

areas in which data can be collected and analysed.

3.6 Validity and Reliability

The validity of the data collected would be validated by the primary source of

data collection through the interviews and questionnaires from developers and

developing companies within Nairobi. This would also assist with the

reliability since the source of the information would be a primary source of

data.

3.7 Data analysis

This is the analysis of the data collected from the questionnaires and secondary

data. This involves interpreting information collected from respondents when

the questionnaires would be completed by the respondents. Also data from

secondary sources will be used in the analysis so as to capture all the relevant

data for the study.

21

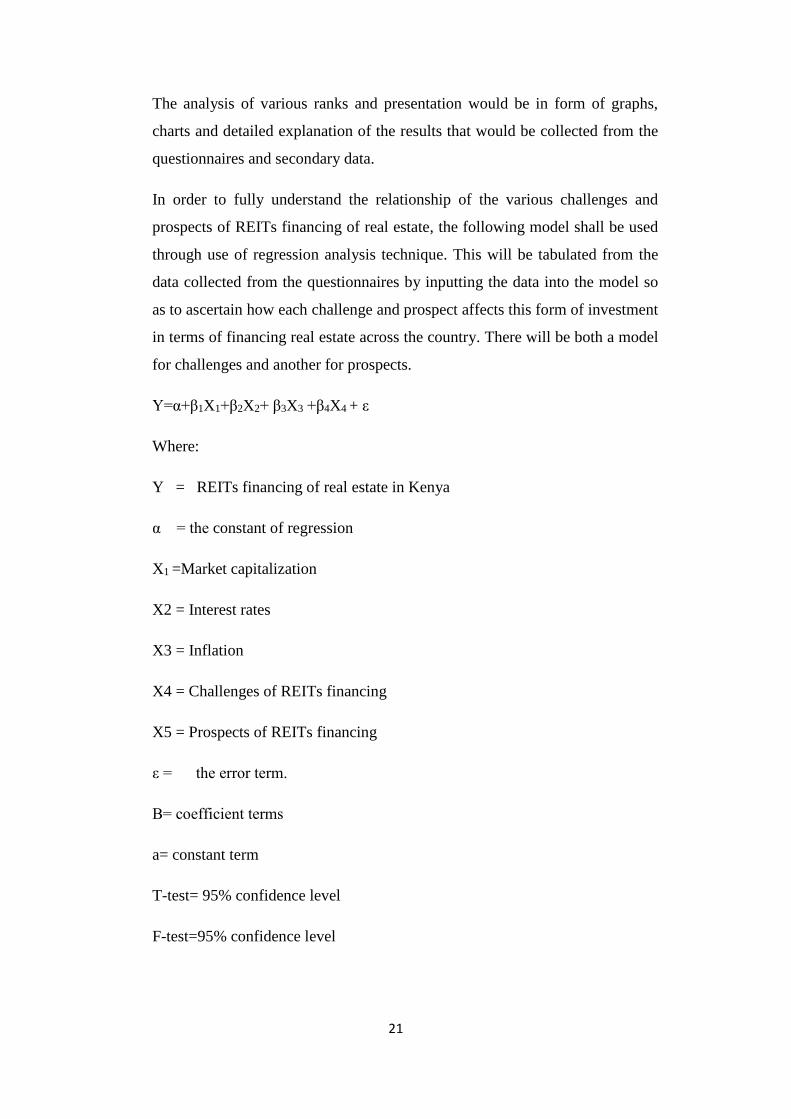

The analysis of various ranks and presentation would be in form of graphs,

charts and detailed explanation of the results that would be collected from the

questionnaires and secondary data.

In order to fully understand the relationship of the various challenges and

prospects of REITs financing of real estate, the following model shall be used

through use of regression analysis technique. This will be tabulated from the

data collected from the questionnaires by inputting the data into the model so

as to ascertain how each challenge and prospect affects this form of investment

in terms of financing real estate across the country. There will be both a model

for challenges and another for prospects.

Y=α+β1X1+β2X2+ β3X3 +β4X4 + ε

Where:

Y = REITs financing of real estate in Kenya

α = the constant of regression

X1 =Market capitalization

X2 = Interest rates

X3 = Inflation

X4 = Challenges of REITs financing

X5 = Prospects of REITs financing

ε = the error term.

Β= coefficient terms

a= constant term

T-test= 95% confidence level

F-test=95% confidence level

22

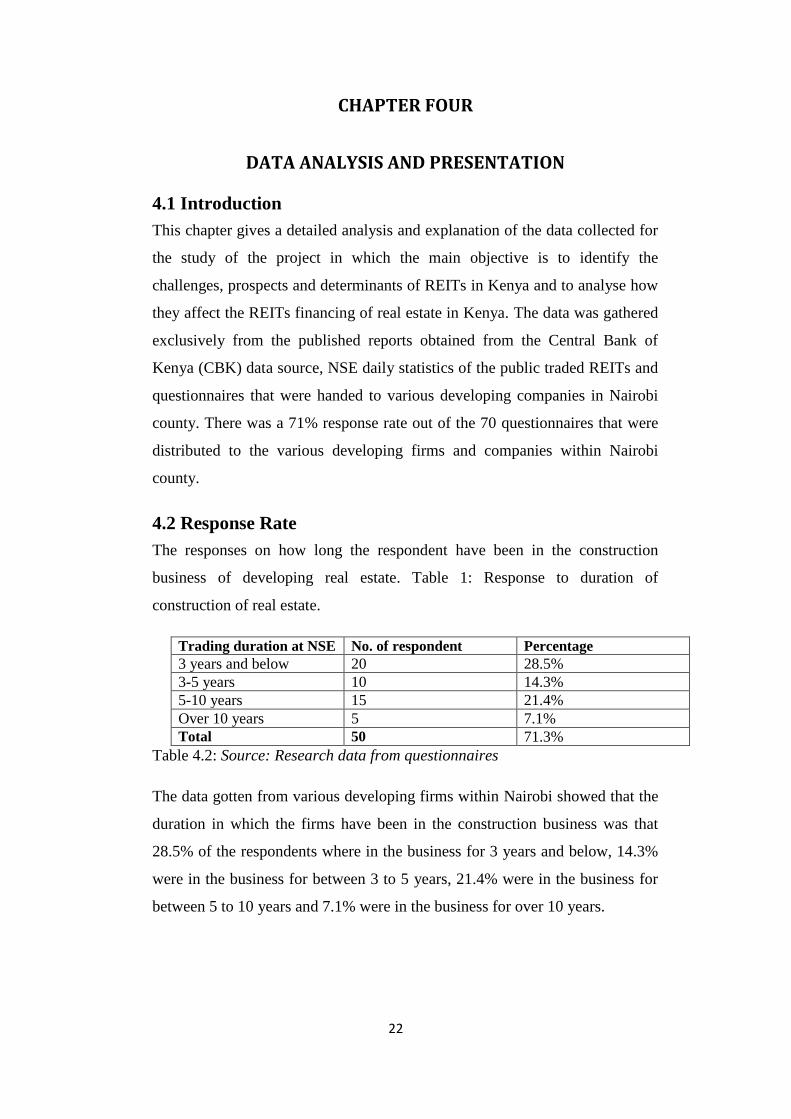

CHAPTER FOUR

DATA ANALYSIS AND PRESENTATION

4.1 Introduction

This chapter gives a detailed analysis and explanation of the data collected for

the study of the project in which the main objective is to identify the

challenges, prospects and determinants of REITs in Kenya and to analyse how

they affect the REITs financing of real estate in Kenya. The data was gathered

exclusively from the published reports obtained from the Central Bank of

Kenya (CBK) data source, NSE daily statistics of the public traded REITs and

questionnaires that were handed to various developing companies in Nairobi

county. There was a 71% response rate out of the 70 questionnaires that were

distributed to the various developing firms and companies within Nairobi

county.

4.2 Response Rate

The responses on how long the respondent have been in the construction

business of developing real estate. Table 1: Response to duration of

construction of real estate.

Trading duration at NSE No. of respondent Percentage

3 years and below 20 28.5%

3-5 years 10 14.3%

5-10 years 15 21.4%

Over 10 years 5 7.1%

Total 50 71.3%

Table 4.2: Source: Research data from questionnaires

The data gotten from various developing firms within Nairobi showed that the

duration in which the firms have been in the construction business was that

28.5% of the respondents where in the business for 3 years and below, 14.3%

were in the business for between 3 to 5 years, 21.4% were in the business for

between 5 to 10 years and 7.1% were in the business for over 10 years.

23

4.2 Data findings

4.2.1 Challenges of REITs financing of real estate

This was the data collected on the various challenges that affect the REITs

financing of real estate projects in Kenya. The challenges that were identified

and data gathered on were policy, regulations and procedures which had a

huge weight of the response indicating a 56% agreement of this being a

challenge to a great extent. The other challenge was high dividend pay-out that

prevents the ploughing back of income generated into the business which got a

huge weight of the response indicating a 54% agreement of this being a

challenge to a great extent. The other challenge that was identified was the

lack of proper tax incentives in such a business for the attraction of various

investors which had a huge weight of the response indicating a 40% agreement

of this being a challenge to an average extent.

The other challenge that was identified was culture of capital structure within

the organisation which can be a problem with new concepts of financing a

rising that may be overlooked. This challenge had most of its weight of the

response indicating a 70% agreement of this being a challenge to a great

extent. The other challenge that was identified was high cost of setting up of

the IPO for the organisation in which it had to meet various requirements of

the CMA for it to go public in such a business venture. The weight of the

response indicated a 36% agreement of this being a challenge to a little extent.

The other challenge that was identified was the market awareness of the

investment vehicle, which basically states that REITs knowledge is yet to be

widely spread out within the country. The weight of the response indicated a

60% agreement of this being a challenge to a great extent.

Where 1 – Great extent, 2- Some extent, 3 – Average, 4 – Little extent and 5 –

No extent

Challenges Response Counts

1 2 3 4 5

Policy, regulations and procedures 28 6 5 5 6 50

High dividend pay-out. 27 7 7 0 7 50

Lack of proper tax incentives 15 8 20 3 4 50

24

Culture of capital structure within the

organization. 35 10 5 0 0 50

High cost of setting up an IPO 7 9 7 18 9 50

Market awareness of the investment

vehicle. 30 10 5 5 0 50

Table 4.2.1

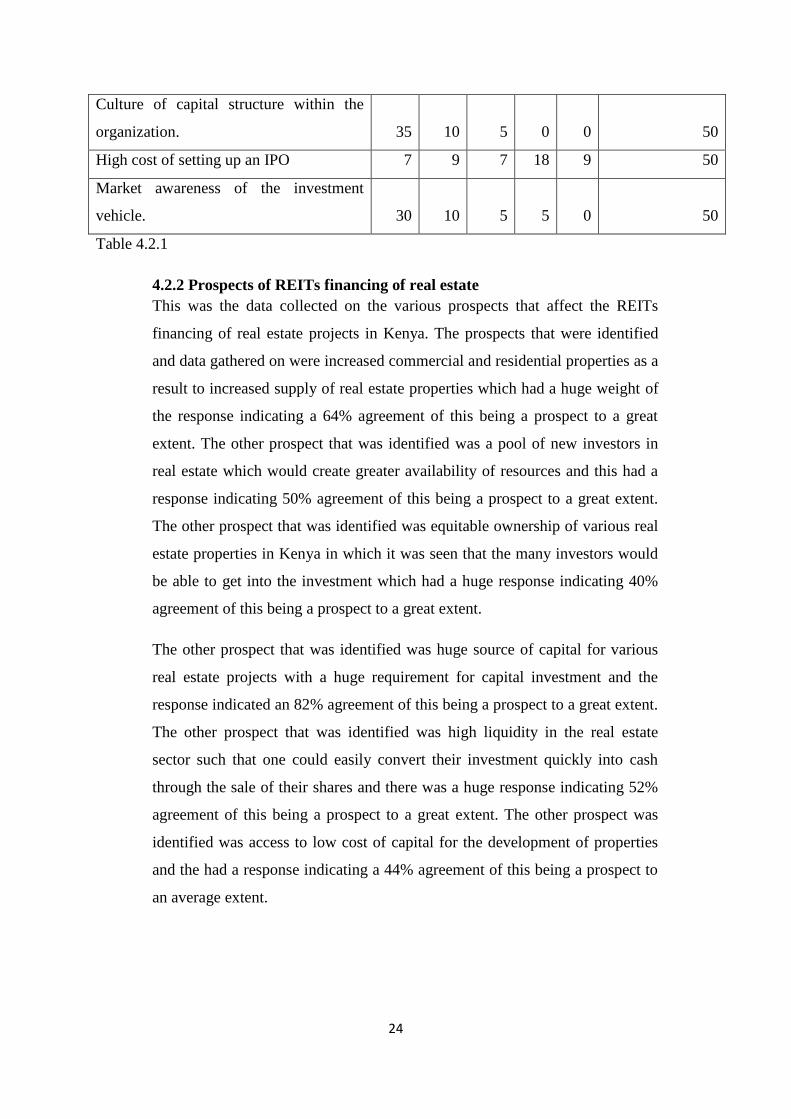

4.2.2 Prospects of REITs financing of real estate

This was the data collected on the various prospects that affect the REITs

financing of real estate projects in Kenya. The prospects that were identified

and data gathered on were increased commercial and residential properties as a

result to increased supply of real estate properties which had a huge weight of

the response indicating a 64% agreement of this being a prospect to a great

extent. The other prospect that was identified was a pool of new investors in

real estate which would create greater availability of resources and this had a

response indicating 50% agreement of this being a prospect to a great extent.

The other prospect that was identified was equitable ownership of various real

estate properties in Kenya in which it was seen that the many investors would

be able to get into the investment which had a huge response indicating 40%

agreement of this being a prospect to a great extent.

The other prospect that was identified was huge source of capital for various

real estate projects with a huge requirement for capital investment and the

response indicated an 82% agreement of this being a prospect to a great extent.

The other prospect that was identified was high liquidity in the real estate

sector such that one could easily convert their investment quickly into cash

through the sale of their shares and there was a huge response indicating 52%

agreement of this being a prospect to a great extent. The other prospect was

identified was access to low cost of capital for the development of properties

and the had a response indicating a 44% agreement of this being a prospect to

an average extent.

25

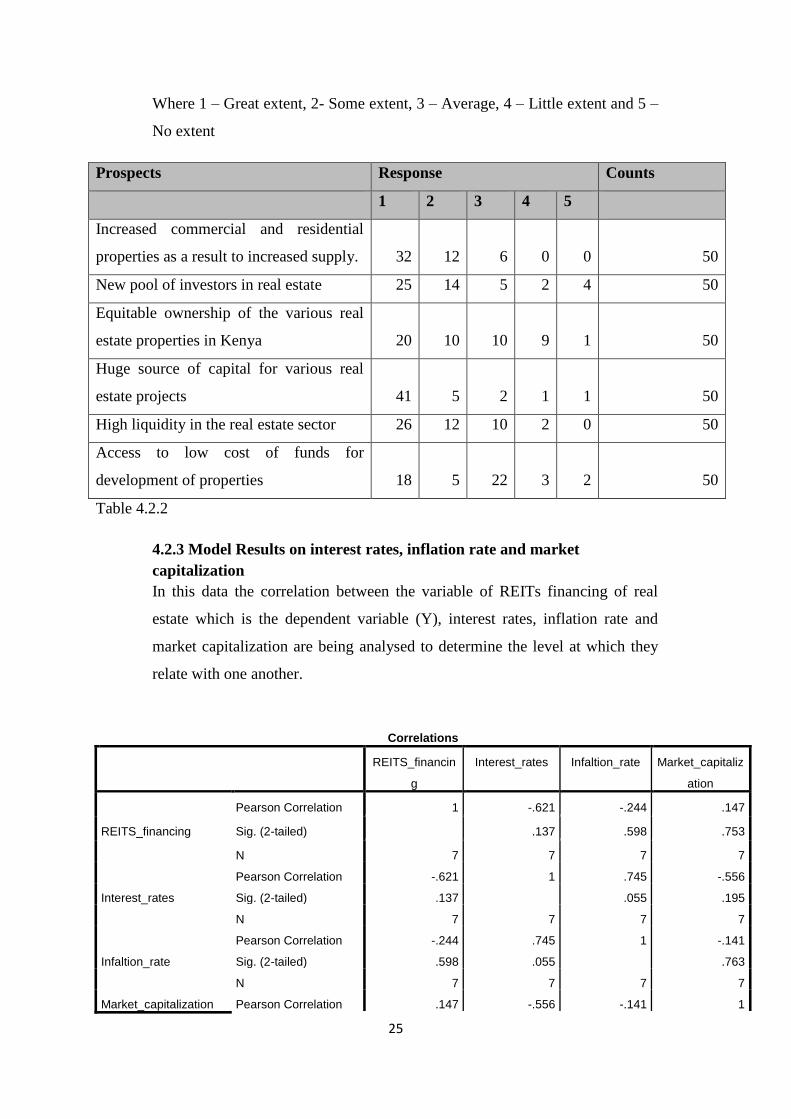

Where 1 – Great extent, 2- Some extent, 3 – Average, 4 – Little extent and 5 –

No extent

Prospects Response Counts

1 2 3 4 5

Increased commercial and residential

properties as a result to increased supply. 32 12 6 0 0 50

New pool of investors in real estate 25 14 5 2 4 50

Equitable ownership of the various real

estate properties in Kenya 20 10 10 9 1 50

Huge source of capital for various real

estate projects 41 5 2 1 1 50

High liquidity in the real estate sector 26 12 10 2 0 50

Access to low cost of funds for

development of properties 18 5 22 3 2 50

Table 4.2.2

4.2.3 Model Results on interest rates, inflation rate and market

capitalization

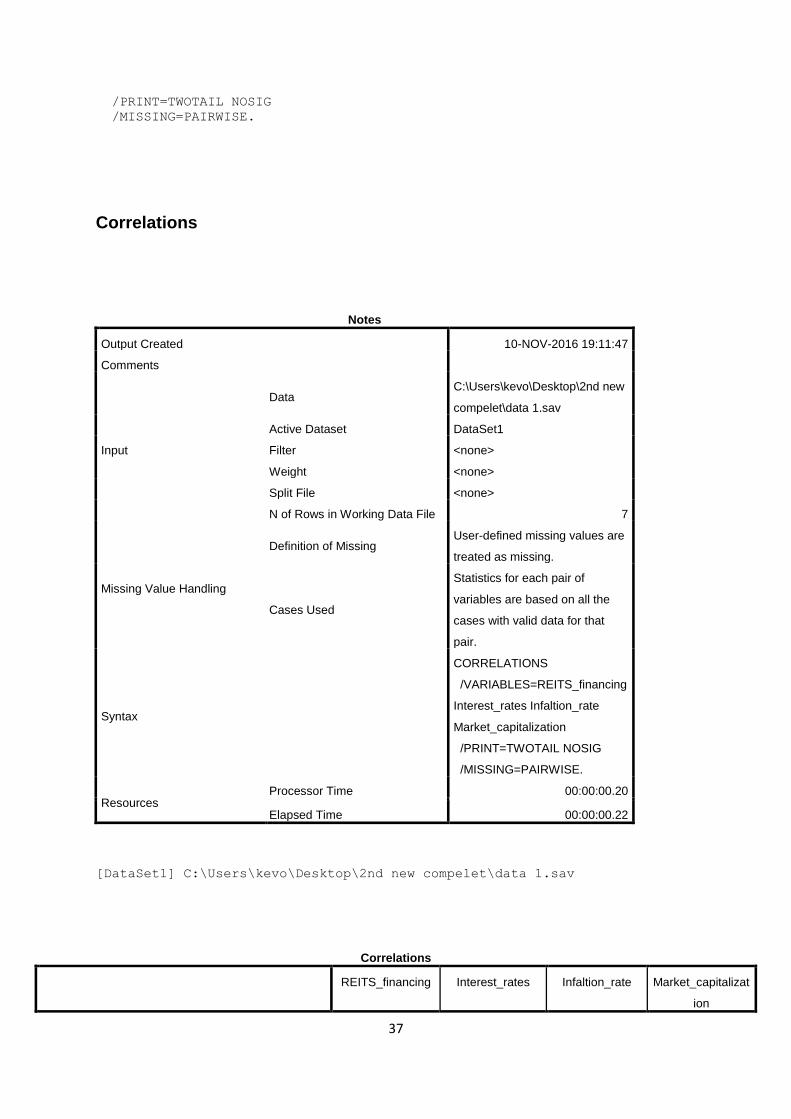

In this data the correlation between the variable of REITs financing of real

estate which is the dependent variable (Y), interest rates, inflation rate and

market capitalization are being analysed to determine the level at which they

relate with one another.

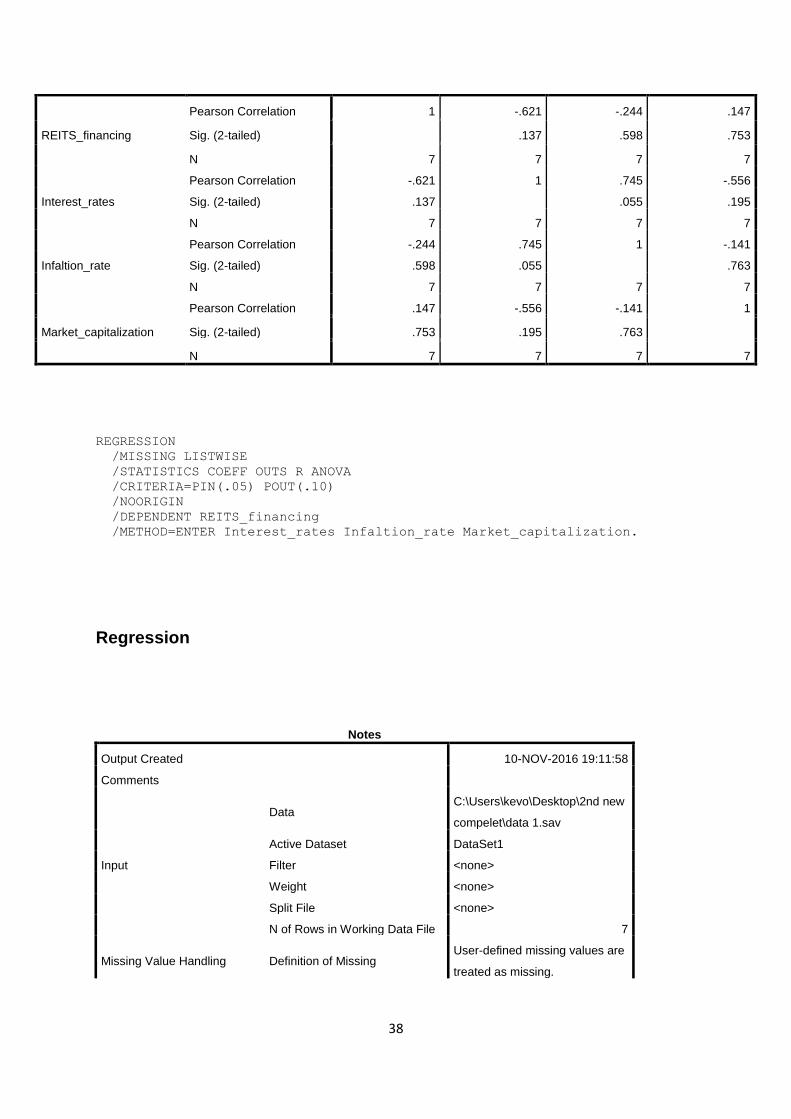

Correlations

REITS_financin

g

Interest_rates Infaltion_rate Market_capitaliz

ation

REITS_financing

Pearson Correlation 1 -.621 -.244 .147

Sig. (2-tailed) .137 .598 .753

N 7 7 7 7

Interest_rates

Pearson Correlation -.621 1 .745 -.556

Sig. (2-tailed) .137 .055 .195

N 7 7 7 7

Infaltion_rate

Pearson Correlation -.244 .745 1 -.141

Sig. (2-tailed) .598 .055 .763

N 7 7 7 7

Market_capitalization Pearson Correlation .147 -.556 -.141 1

26

Sig. (2-tailed) .753 .195 .763

N 7 7 7 7

Table 4.2.3

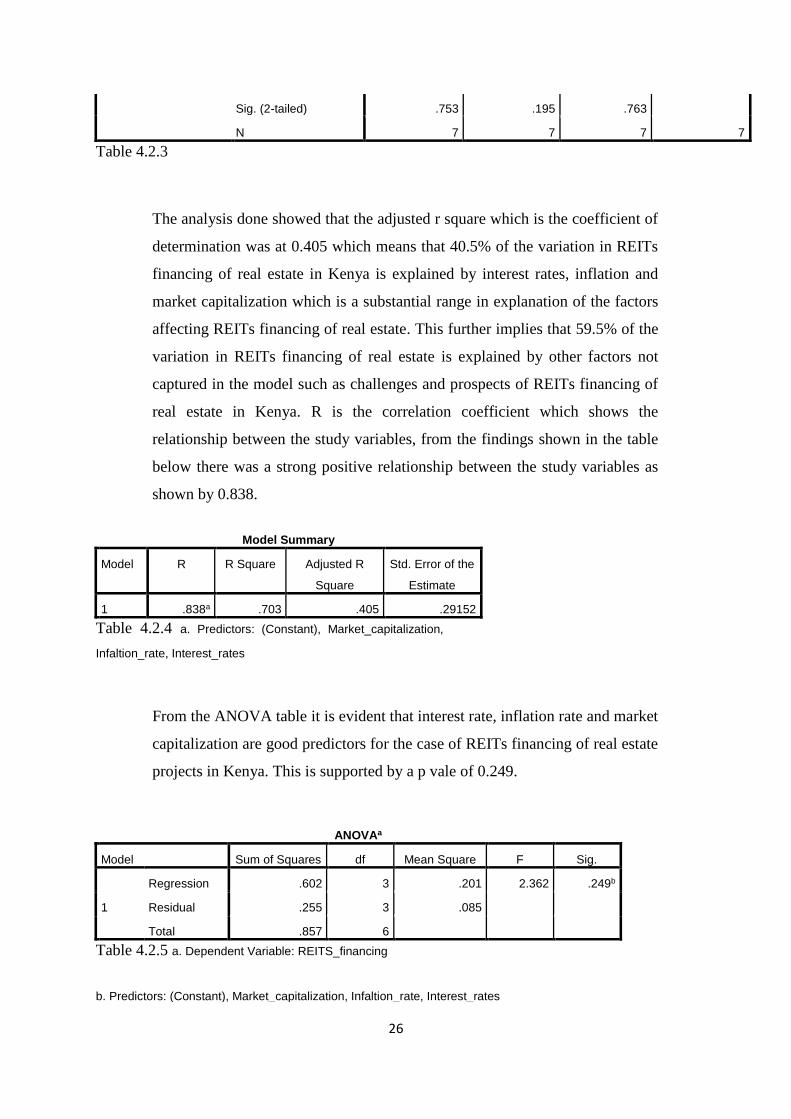

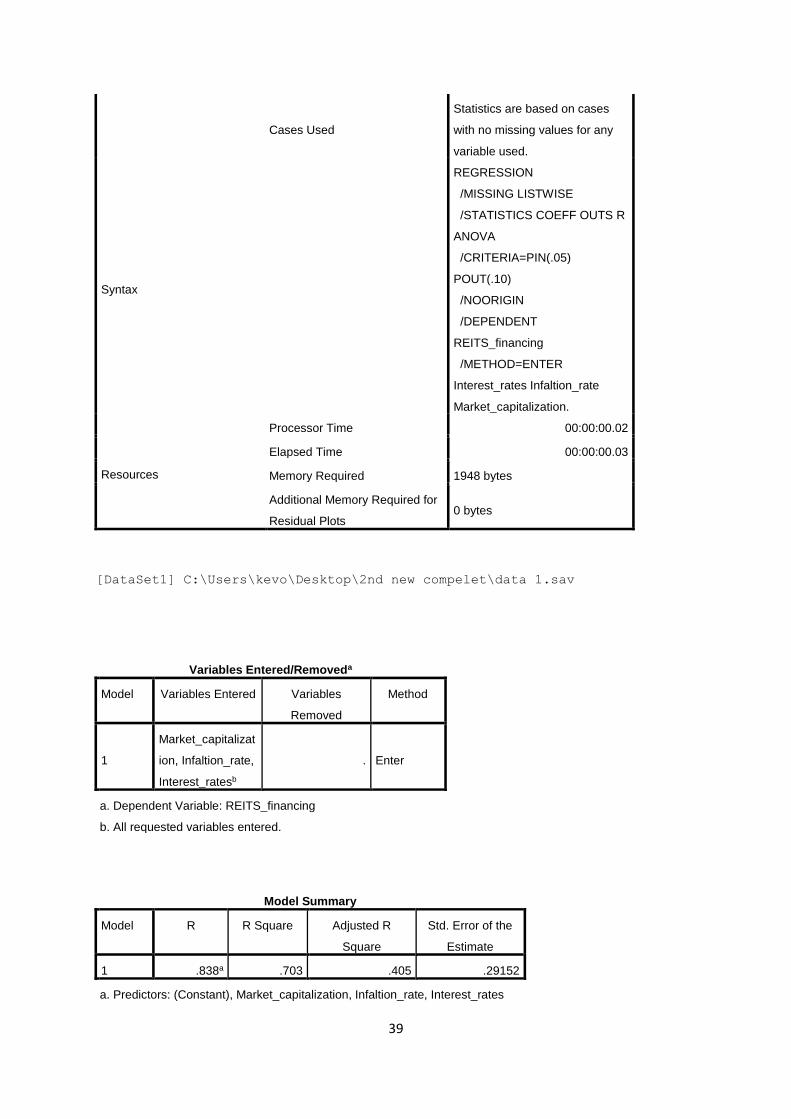

The analysis done showed that the adjusted r square which is the coefficient of

determination was at 0.405 which means that 40.5% of the variation in REITs

financing of real estate in Kenya is explained by interest rates, inflation and

market capitalization which is a substantial range in explanation of the factors

affecting REITs financing of real estate. This further implies that 59.5% of the

variation in REITs financing of real estate is explained by other factors not

captured in the model such as challenges and prospects of REITs financing of

real estate in Kenya. R is the correlation coefficient which shows the

relationship between the study variables, from the findings shown in the table

below there was a strong positive relationship between the study variables as

shown by 0.838.

Model Summary

Model R R Square Adjusted R

Square

Std. Error of the

Estimate

1 .838a .703 .405 .29152

Table 4.2.4 a. Predictors: (Constant), Market_capitalization,

Infaltion_rate, Interest_rates

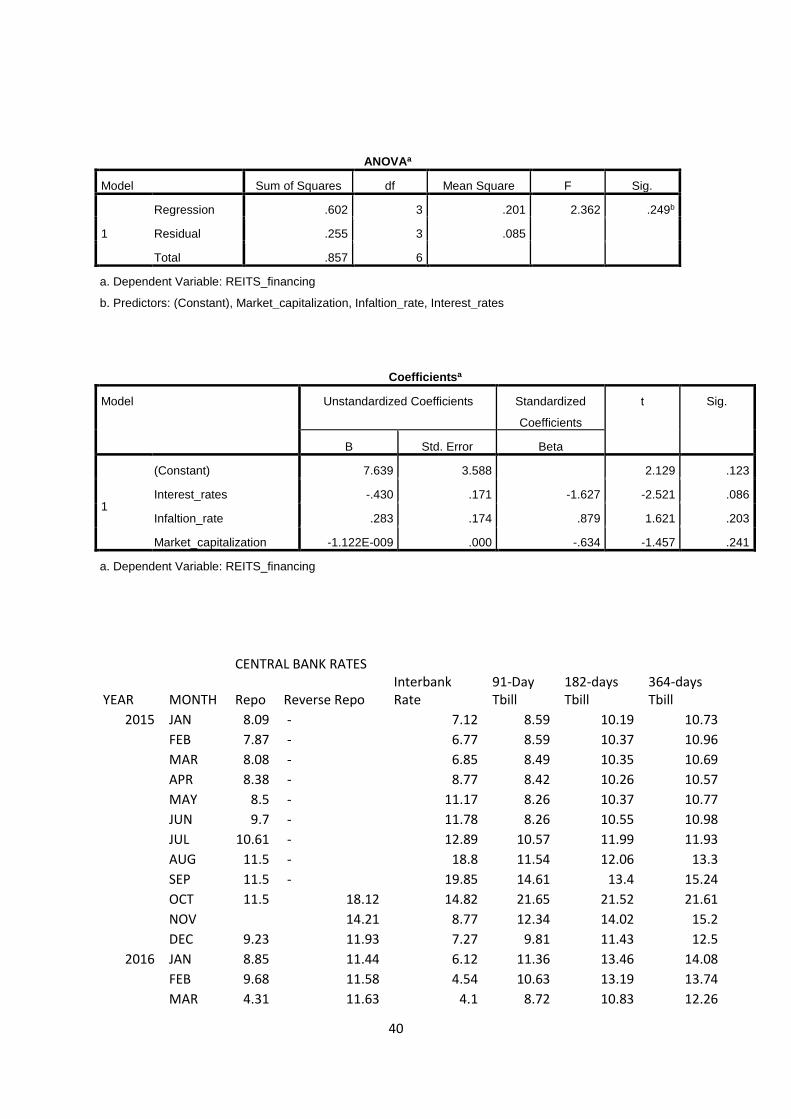

From the ANOVA table it is evident that interest rate, inflation rate and market

capitalization are good predictors for the case of REITs financing of real estate

projects in Kenya. This is supported by a p vale of 0.249.

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1

Regression .602 3 .201 2.362 .249b

Residual .255 3 .085

Total .857 6

Table 4.2.5 a. Dependent Variable: REITS_financing

b. Predictors: (Constant), Market_capitalization, Infaltion_rate, Interest_rates

27

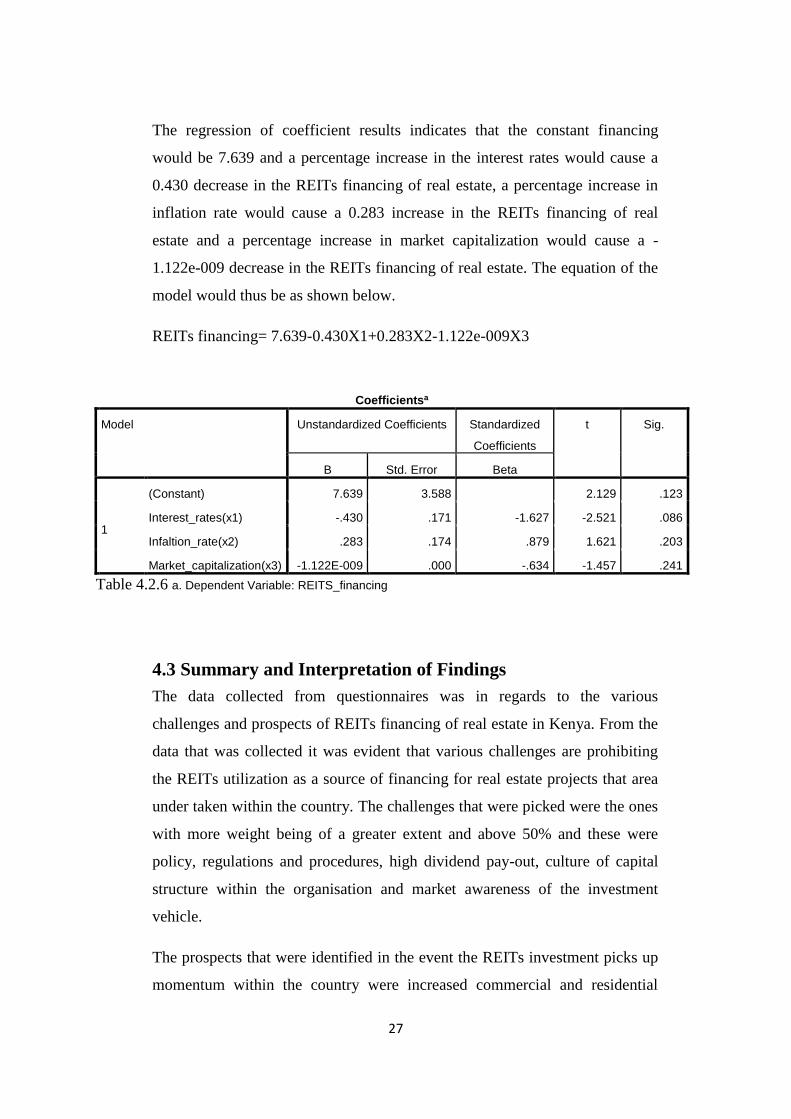

The regression of coefficient results indicates that the constant financing

would be 7.639 and a percentage increase in the interest rates would cause a

0.430 decrease in the REITs financing of real estate, a percentage increase in

inflation rate would cause a 0.283 increase in the REITs financing of real

estate and a percentage increase in market capitalization would cause a -

1.122e-009 decrease in the REITs financing of real estate. The equation of the

model would thus be as shown below.

REITs financing= 7.639-0.430X1+0.283X2-1.122e-009X3

Coefficientsa

Model Unstandardized Coefficients Standardized

Coefficients

t Sig.

B Std. Error Beta

1

(Constant) 7.639 3.588 2.129 .123

Interest_rates(x1) -.430 .171 -1.627 -2.521 .086

Infaltion_rate(x2) .283 .174 .879 1.621 .203

Market_capitalization(x3) -1.122E-009 .000 -.634 -1.457 .241

Table 4.2.6 a. Dependent Variable: REITS_financing

4.3 Summary and Interpretation of Findings

The data collected from questionnaires was in regards to the various

challenges and prospects of REITs financing of real estate in Kenya. From the

data that was collected it was evident that various challenges are prohibiting

the REITs utilization as a source of financing for real estate projects that area

under taken within the country. The challenges that were picked were the ones

with more weight being of a greater extent and above 50% and these were

policy, regulations and procedures, high dividend pay-out, culture of capital

structure within the organisation and market awareness of the investment

vehicle.

The prospects that were identified in the event the REITs investment picks up

momentum within the country were increased commercial and residential

28

properties as a result to increased supply of real estate properties within the

country, new pool of investors in real estate, huge source of capital for various

real estate projects that require hi source of income funding and high liquidity

in the real estate sector.

Interest rates as a macro-economic factor were found to having a negative

relationship in that a percentage increase in the interest rates would cause a -

0.430 percent decrease in the financing of real estate by REITs this can also be

seen from the correlation which is negatively correlated at -0.621. The

correlation between interest rate and the other variables showed that interest

rates are positively correlated to inflation rate at 0.745 and negatively

correlated to market capitalization at -0.556.

Inflation rates as another macro-economic factor were found to having a

positive relationship in that a percentage increase in the inflation rates would

cause a -0.283 percent increase in the financing of real estate by REITs. The

correlation between inflation rate and the other variables showed that interest

rates are positively correlated to interest rate at 0.745 and negatively correlated

to market capitalization at -0.141.

Market capitalization was found to having a negative relationship in that a

percentage increase in the market capitalization would cause a -1.122e-009

percent decrease in the financing of real estate by REITs. The correlation

between market capitalization and the other variables showed that market

capitalization are negatively correlated to interest rate at -0.556 and negatively

correlated to inflation rates at -0.141.

29

CHAPTER FIVE

SUMMARY, CONCLUSION AND RECOMMENDATIONS

5.1 Summary

This chapter provides the summary of the findings, the limitations and the

recommendation for further studies on REITs.

5.2 Summary findings and conclusion

The research that was done through questionnaires and secondary data

collected data that was analysed in chapter four and the findings were as

follows. The challenges that have been identified are policy, regulations and

procedures, high dividend pay-out, culture of capital structure within the

organisation and market awareness of the investment vehicle.

The prospects that have also been identified by this study were increased

commercial and residential properties as a result to increased supply of real

estate properties within the country, new pool of investors in real estate, huge

source of capital for various real estate projects that require high source of

income funding and high liquidity in the real estate sector.

The regression analysis that was carried out on the macro-economic factors of

interest rates, inflation rates and market capitalization concluded that the level

at which these factors affect the financing of real estate projects by REITs was

quite at a significant level as from the results drawn from chapter four. The

goodness in fit for the model was at 0.405 which is at 40.5% which is a

significant representation of the variables as factors for determining the REITs

financing of real estate. The analysis of variance (ANOVA) indicated that the

overall model was significant. This was supported by a p value of 0.249. The

ANOVA results demonstrated that the variables of interest rates, inflation rates

and market capitalization are good predictors of REITs financing of real estate

projects in Kenya.

In conclusion the project has been able to identify that there are various

challenges that need to be addressed for the proper utilization of REITs as a

source of financing for real estate projects in the country to be actualized and

30

the prospects attained. This project also concludes that interest rates, inflation

rates and market capitalization are significant variables at 40.5% that affect the

REITs financing of real estate in Kenya at the moment.

5.3 Recommendations

The recommendations of this project are that REITs should be further looked

at as a good economic investment into the real estate sector and developers

should take full advantage of the financing source so as to be able to undertake

various real estate projects within the country so as to be able to meet the

growing demand in the country at the moment and the growing demand in the

future.

The other factors that affect REITs financing should also be properly identified

so as to manage such factors to enable the uptake and growth of REITs with

the country to become possible.

5.5 Limitations of the study

The main limitations of the study were the time given for the study was short

and not enough data was collected for the analysis stage.

The budget allocation for the study did not enable us to travel to other counties

for the collection of data for a proper representative sample of the population.

5.6 Suggestions for further study

The area that can be further studied are the main factors that affect the REITs

financing of real estate in Kenya so as to ascertain the variable that affect the

REITs within the country.

31

REFERENCES:

Saunders, M. N., P. Lewis, A. Thornhill, (2003).Research Methods for Business

Students. 3rd Ed. New York: FT Prentice Hall,

Smotrich R. L., Bennett, R. H., Lazarevic K., Lewis, M. R., & Rand M. (2012).

Equity research U.S. REITS: Barclays Capital Inc.

Jagodic D., Dobrojevic G., Suljic S., (2011). REIT Regimes in EU Countries –

Institutional Environment versus Attractiveness of Real Estate Investment

Vehicles

Legal notice no.116. (2013). The capital markets (real estate investment trusts)

(collective investment schemes) regulations. Kenya Gazette Supplement

No. 90

Robert, P. W., & Johnson, A. C. (1996). Dallas Business Journal. Journal of

Small Business Management, Vol.32; PP.27-35.

Mulupi, D. (2012, June 20). Venture Africa. Retrieved August Friday, 2016,

from Investing, Marketing, Real estate: http://www.ventures-

africa.com/2012/06/kenyas-real-estate-sector-boom-or-doom/

Ogedengbe, P. S., & Adesopo, A. A. (2003). Problems of Financing Real

Estate Developmentin Nigeria.

Waithaka, J. (2011, July, 6 Wednesday). The Star. Retrieved August Friday,

2016, from The Star: http://www.the-star.co.ke/news/article

58189/construction-top-performing-industry-kenyas-

economy#sthash.y1oikATs.dpuf

Murray, Z. F. & Vidhan, K. G. (2005). Trade-off and pecking order theories of debt

Popescu, L. & Visinescu S. (2009). A review of the capital structure theories

Hilgen, M. (2014). The impact of cultural clusters on capital structure decisions:

Evidence from European retailers.

Menyah, K. and Paudyal, K. (2002). IPO decisions and the costs of going public.

32

U.S. securities and exchange commission-Office of investor education and advocacy.

Investor bulletin: real estate investment trusts(REITs)

Hoesli, M. & Oikarinen, E. (2012). International real estate securities, Journal of

international money and finance., Vol 31; pp 1823-1850.

Lee, S. & Stevenson, S. (2004). The case for REITS in the mixed-asset portfolio in the short

and long run. Journal of Real Estate Portfolio Management., Vol 11; pp. 55-80.

Gumbs, B. (2001). The Viability of the REIT Structure as a Vehicle for Real Estate Development. U.S.: Massachusetts Institute of Technology

Konagi, R. (2009). Two Studies of Japan-REIT Performance: Modeling Risk and Tracking

Property Level Performance. U.S.: Massachusetts Institute of Technology

Michuki, D. W., (2010). The existence of real estate investment trusts (REITS) needs by

institutional investors at the Nairobi stock exchange. Nairobi: University of Nairobi.

Muchiri, S. K., (2006). An assessment of the viability of real estate securitization in Kenya. Nairobi: University of Nairobi.

Nzalu, F. M., (2013). An Assessment of the Factors Affecting the Growth in Real Estate

Investment in Kenya. Nairobi: University of Nairobi. Mwathi, J. K., (2013). The effect of financing sources on real estatedevelopment in Kenya.

Nairobi: University of Nairobi. Alias, A. & Thou, S., (2011). Performance analysis of REITS: Comparison between M-REITS

and UK-REITS. Journal of Surveying, Construction and Property. Vol 2; pp. 38-61 Olanrele, O. O., (2014). REIT PERFORMANCE ANALYSIS: ARE OTHER FACTOR

DETERMINANTS CONSTANT? Journal of Asian Economic and Financial Review. Vol 4; pp. 492-502

Modigliani, F. & M. Miller, (1961). The Cost of Capital, Corporation Finance, and the Theory

of Investment, American Economic Review, 48, 3, 261-297.

Pham, T. H. H., (2010). Performance and return determinants of REIT and Non-REIT real

estate stocks in selected Asian markets. Amsterdam: University of Amsterdam

Chan, K.C., Hendershott, P.H., and Sanders. A.B. (1990).Risk and Return on Real Estate:

Evidence from Equity REITs, The Journal of American Real Estate and Urban

Economics Association, Vol 18; pp 431-52

33

APPENDICES

QUESTIONNAIRE

A SURVEY ON CHALLENGES AND PROSPECTS OF REAL ESTATE

INVESTMENT TRUSTS (REITs) FINANCING OF REAL ESTATE IN KENYA.

Please complete this questionnaire honestly by ticking the answer from the given

options. Some questions will require a bit of explanation and clarification.

Information collected from this questionnaire will be handled with high

confidentiality and will strictly be used for academic purposes by the researcher.

Your cooperation will be highly appreciated.

SECTION A: Background Information

a) The name of the respondent?

b) How long has your company or yourself been in the development of real estate

property business?

Length Below

3

Years

3-5

years

5-10

years

Above

10

years

Response

c) The number of real estate projects the company has done across Nairobi?

d) Do you have prior knowledge of the REITs investment in Kenya or in other

countries where the same has been established?

e) Do you know of any REITs that are in Kenya?

34

SECTION B: CHALLENGES OF REITs FINANCING REAL ESTATE IN

KENYA.

a) Which challenges do you know of that are affecting the REITs being used as a

financing vehicle of real estate in Kenya?

b) Has your company ever used REITs or equity as a financing vehicle for the real

estate properties that have been developed?

c) To what extent do agree with the following as challenges to the use of REITs as a

financing vehicle in Kenya? (Tick as appropriate)