challenge bibendum 2010 guest forum the marketplace for e-mobility rio de janeiro, june 2, 2010

TRANSCRIPT

Challenge Bibendum 2010Guest Forum

The Marketplace for E-Mobility

Rio de Janeiro, June 2, 2010

Copyright © 2010 IHS Global Insight. All Rights Reserved.

2

Global Drivers for Future Mobility Solutions

• Economy/Per Capita Income

• Population

• Wealth Distribution

• Oil Prices

• World CO2 Regulations

• Values

• IT/Technology Use

Copyright © 2010 IHS Global Insight. All Rights Reserved.

3

Mobility has Traditionally Been Measured by the Level of Motorization. Motorization is Primarily a Function of Wealth

• Mature markets• Very wealthy• Established industry• Motorization rate leveling off

• Growth markets• Wealth is building• Growing local industry• Rate of motorization is increasing rapidly as a

function of wealth

• Emerging markets• Breaking the $5,000 per capita threshold• Indigenous industry just beginning to emerge• Motorization will increase rapidly 0

100

200

300

400

500

600

700

800

900

0 10 20 30 40 50

Per Capita GDP @ PPP

Ve

hic

les

Pe

r 1

00

0 P

eo

ple

0

100

200

300

400

500

600

700

800

900

0 10 20 30 40 50

Per Capita GDP @ PPP

Ve

hic

les

Pe

r 1

00

0 P

eo

ple

Vehicle Density vs. Income(for 2002 and 2007)

Singapore

Hong Kong

United States

W. Europe & Japan

Copyright © 2010 IHS Global Insight. All Rights Reserved.

4

• If our current model of mobility is maintained, there will be demand for the equivalent of three billion vehicles on the roads of the world by 2035

• Imagine what this world will be like, considering the mobility challenges we face today when there are only 800 million vehicles in-use globally

• Clearly, this model of mobility can not be maintained. The scenarios will explore different pathways for the evolution of motorization

1) Gott, Philip; Is Mobility As We Know It Sustainable? International Automotive Mobility Forum, 2008, Geneva, Switzerland

…It is Only the Day After Tomorrow!

Just Imagine! 2030 is Only One Platform Cycle Away

Copyright © 2010 IHS Global Insight. All Rights Reserved.

5

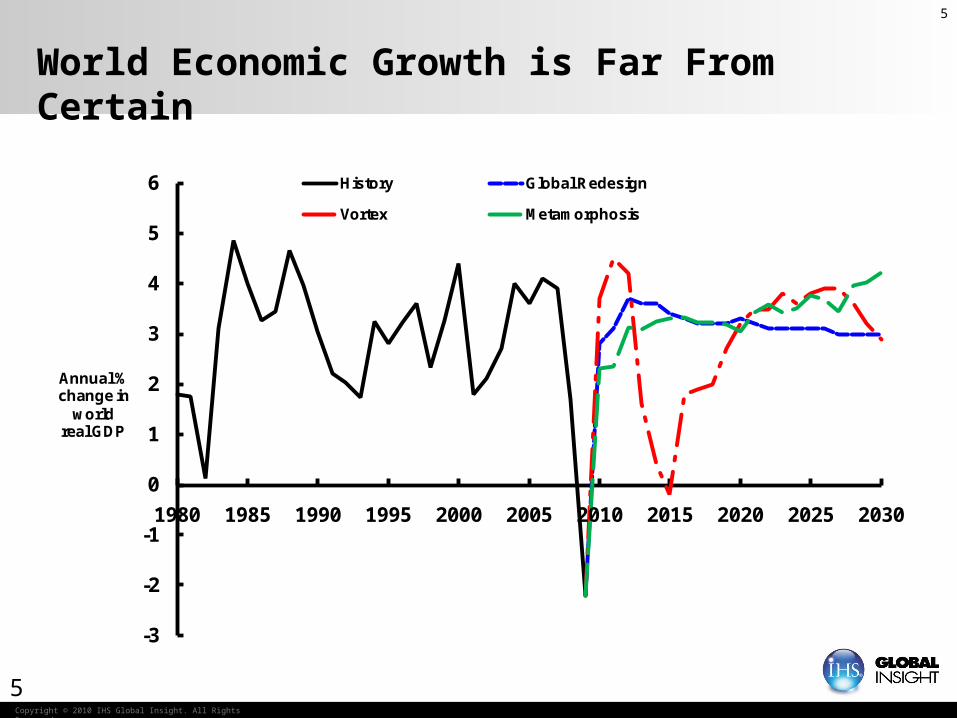

World Economic Growth is Far From Certain

-3

-2

-1

0

1

2

3

4

5

6

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Annual % change in

world real GDP

History Global Redesign

Vortex Metamorphosis

5

Copyright © 2010 IHS Global Insight. All Rights Reserved.

6

Population Trends are More Predictable: An Aging Consumer Living More and More in Urban Areas…

Source: World Urbanization Prospects: The 2007 Revision, United Nations Economic and Social Affairs, 2007

World Population Trends to 2050

Source: World Urbanization Prospects: The 2004 Revision

The Share of Population Over 65 Years Is Growing

Urban Areas

Today

Copyright © 2010 IHS Global Insight. All Rights Reserved.

7

… With a Rising Old Age Dependency Ratio

Sources: US Census, UN Population Prospects 2008. Note: Ratio is calculated by dividing population aged 65 years and older by population aged 15–64.

7

0%

10%

20%

30%

40%

50%

60%

1980 1990 2000 2010 2020 2030

DependencyRatio

Old Age Dependency Ratio, 1980-2030Global Redesign

China Japan

India United States

Note: Ratio is calculated by dividing population aged 65 years and older by population aged 15-64.Source: IHS Global Scenarios, US Census, UN Population Prospects 2008.

W. EuropeW. Europe

Copyright © 2010 IHS Global Insight. All Rights Reserved.

8

… And Increasingly “Eco-aware”

• Future indications point towards more ‘awareness’ with the consumer, potentially resulting in pressure for mobility providers to offer more eco-acceptable transport solutions

• The ‘Eco Sensor’ Concept from Finnish cell phone maker Nokia features a sensor that measures CO, CO2, particulate matter, and ground-level ozone.

• Real-time consumption measurement Source: Nokia

Copyright © 2010 IHS Global Insight. All Rights Reserved.

9

Locally Determined Drivers for Future Global Mobility Solutions

Market Dependant Mobility Solution Drivers

• Energy

• Attitudes (Resource Conservation)

• Mobility Regulations

• Lifestyle

• Free-Time

• LD Infrastructures

• Local Infrastructures

• Technology and Safety

Copyright © 2010 IHS Global Insight. All Rights Reserved.

10

Megacity

• >10 million population

• 19 in 2007

• 27 in 2025

Lifestyle Is A Function Of Where People Live

Urban

• Includes suburban areas

• >400 people/km2

Rural

Source: Courtesy of, Alexander Augst

Copyright © 2010 IHS Global Insight. All Rights Reserved.

11

Planning for Mobility in the Future:

2030

20102008

20252015

Disruptive

Business As Expected

Cornutopia

MarketsMature

Growth

Emerging

Economic, Regulatory & Energy Environment

CornutopiaAs Expected

Disruptive

Lifestyle

Mega Cities

Urban

Rural

Possible Future Business Environments

Market Type PCGDP@PPP 2007 2030Pre-Emergent <$5,000 83 53Emerging $5K - $10K 39 30Growth $10 - $20K 41 32Mature >$20K 44 92

Social Consciousness

Energy Costs

Demographics

Per Capita Income

Natural Resources Available

Economic Well-Being

Politics

Social Stability

Use of Information Technologies

Copyright © 2010 IHS Global Insight. All Rights Reserved.

12

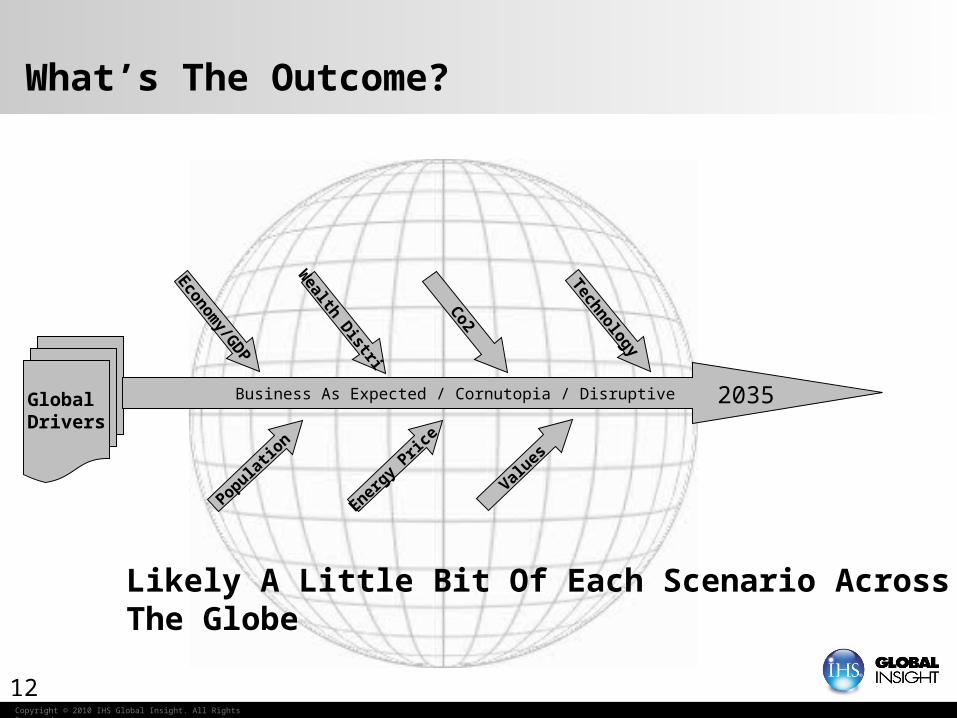

What’s The Outcome?

Global Drivers

Business As Expected / Cornutopia / Disruptive

Economy/G

DP

Wealth D

istri

Co2

2035Technology

Populatio

n

Energy

Price

Values

Likely A Little Bit Of Each Scenario Across The Globe

Copyright © 2010 IHS Global Insight. All Rights Reserved.

13

Today’s Conventional Wisdoms Are Challenged

• We currently purchase vehicles that are excessive for their most frequent missions

• Downsizing with greater flexibility for vehicle functionality is needed

• The Car of the Future will be more tuned to its intended use/mission profile

• As long as the user is assured access to more versatile vehicles when needed

• More people will accept a truly small car (Nano, Fiat 500, Smart and smaller) as long as access to more versatile vehicles can be assured when they are needed

• Accident prevention is essential

• Emotions will play a less important role in the purchase decision• The more urbanized an area, the less emotions are tied to ownership

• Emotions are independent of car size

• Shared fleets will be purchased based on a balance of business criteria and emotional appeal to car share members/users

Copyright © 2010 IHS Global Insight. All Rights Reserved.

14

The Role of the Car Will Be Altered!

• Forces Driving Change Include• Aging population

• Vehicle usage rethink

• Vehicle design/powertrain rethink

• Do I need to ‘own’ the vehicle?

• Virtual mobility

• A need for “Integrated Mobility Services” to cover various phases of travel seamlessly

• Car sharing meets the “integrated mobility” needs very well. It will be encouraged

• How will this be provided?

Copyright © 2010 IHS Global Insight. All Rights Reserved.

15

Implications

The Urban Car of the Future will be:

• Largely used in urban areas for relatively short trips

• Managed by car-sharing fleets

• Fueled by a diversity of energy forms

• Compatible with dense traffic conditions and a potentially compromised driver

Source: Ford Motor Co

Source: MIT

Copyright © 2010 IHS Global Insight. All Rights Reserved.

16

0

100

200

300

400

500

600

700

800

900

0 10 20 30 40 50

Mobility Will Mean Far More Than Access to a Car

• Mobility has always been an extension of humankinds boundaries

• Physical mobility has always been paramount, and will remain a strong component of mobility

• Personal

• Shared

• Collective

• It will be joined by other forms of mobility

Motorization Compared to Internet Density vs. Income

Motorization

0

100

200

300

400

500

600

700

800

900

0 10 20 30 40 50

Per Capita GDP @ PPP

e-mobility

Per

100

0 P

eop

le

Source: iphone.wareseeker.comSource: Internet World Stats

Copyright © 2010 IHS Global Insight. All Rights Reserved.

17

“Business-as-usual” is the least-likely scenario!

• To sum it up, while the Car of the Future is likely to be predominantly smaller, right-sized and electric and fleet-owned to facilitate sharing, the future car is to play a much less important role in the lifestyle of tomorrow's city-dweller.

• The change in ownership, size and energy source will help mitigate the impact of each vehicle on its physical surroundings; the sheer reduction in its use will be the most effective way to ensure that the mobility provided is sustainable.

Source: Toyota

Source: General Motors

Source: PSA

Thank you!Thank you!

Phil Gott, Managing DirectorAutomotive Science and TechnologyIHS Automotive Consulting