ch02 ppt brighamfm1ce

TRANSCRIPT

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 1/45

PowerPoint Presentationprepared by

Traven ReedCanadore College

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 2/45

chapter 2Financial Statements, Cash

Flow, and Taxes

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 3/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-3

Corporate Valuation andFinancial Statements

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 4/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-4

Topics in Chapter

Balance sheet

Income statement

Statement of retained earnings

Accounting income versus cash flow

Statement of cash flows

MVA and EVA Personal taxes

Corporate taxes

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 5/45

CH2

Financial Statements and

Reports Company annual report describes

the operating results from the past

year and new plans for the comingyear with four financial statements:

± Balance sheet

± Income statement ± Statement of retained earnings

± Statement of cash flows

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-5

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 6/45

CH2

Balance Sheet

Provide a snapshot of the firm¶sfinancial position at a particular point

in time. Show assets on the left-hand size or

at the top and liabilities/equity (i.e.claims against assets) on t

he rig

ht-

hand size or at the bottom.

Record with book values when assets

are pur chased or liabilities are issued.Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-6

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 7/45

CH2

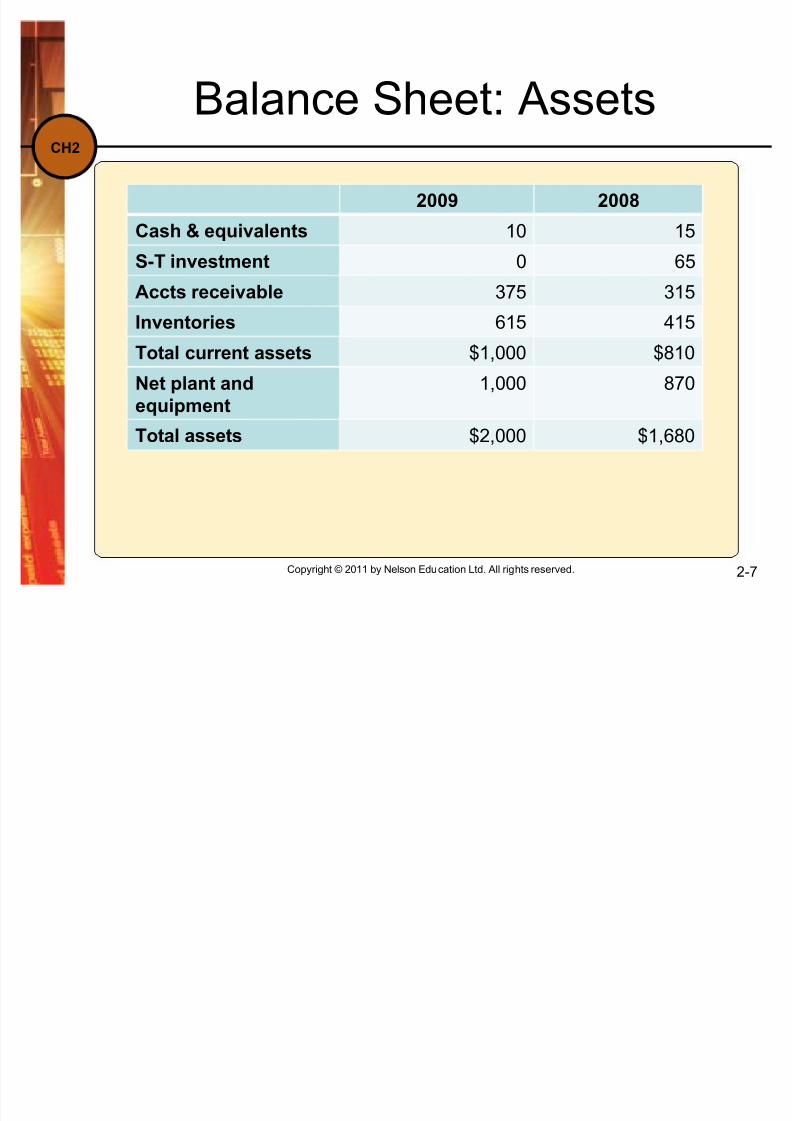

Balance Sheet: Assets

2009 2008

Cash & equivalents 10 15

S-T investment 0 65

Accts receivable 375 315

Inventories 615 415

Total current assets $1,000 $810

Net plant and

equipment

1,000 870

Total assets $2,000 $1,680

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-7

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 8/45

CH2

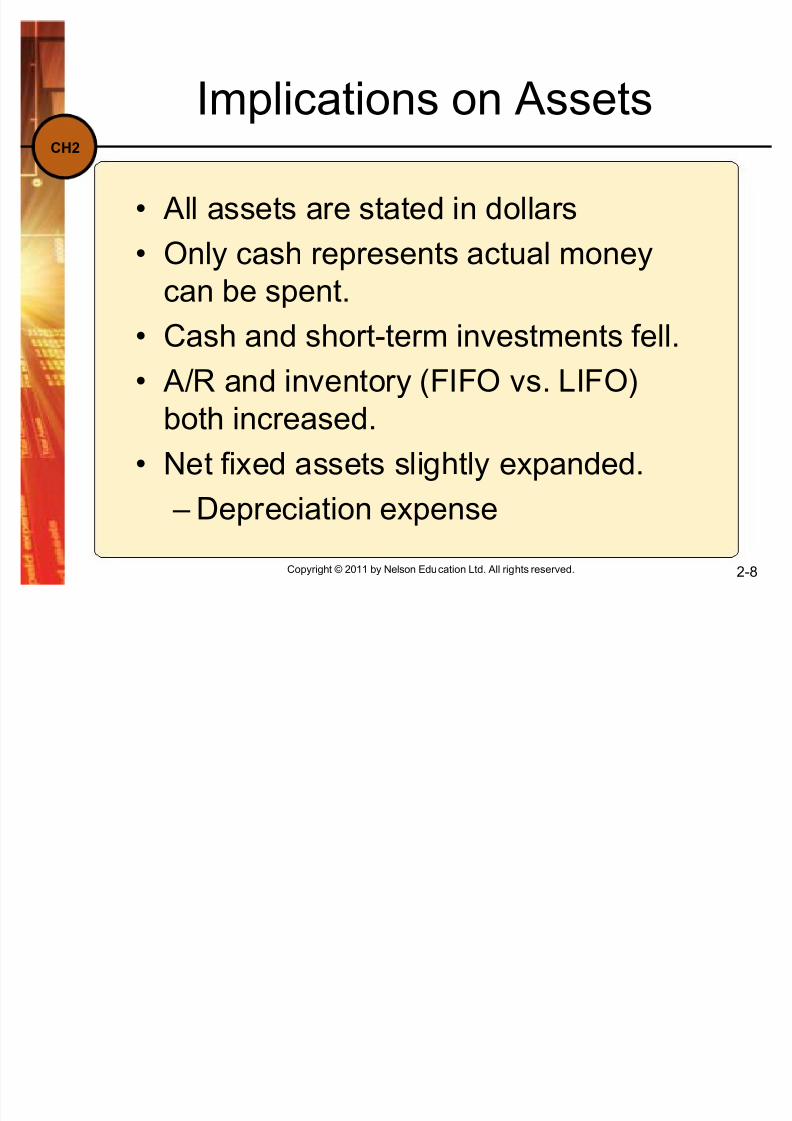

Implications on Assets

All assets are stated in dollars

Only cash represents actual moneycan be spent.

Cash and short-term investments fell.

A/R and inventory (FIFO vs. LIFO)

both increased. Net fixed assets slightly expanded.

± Depreciation expense

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-8

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 9/45

CH2

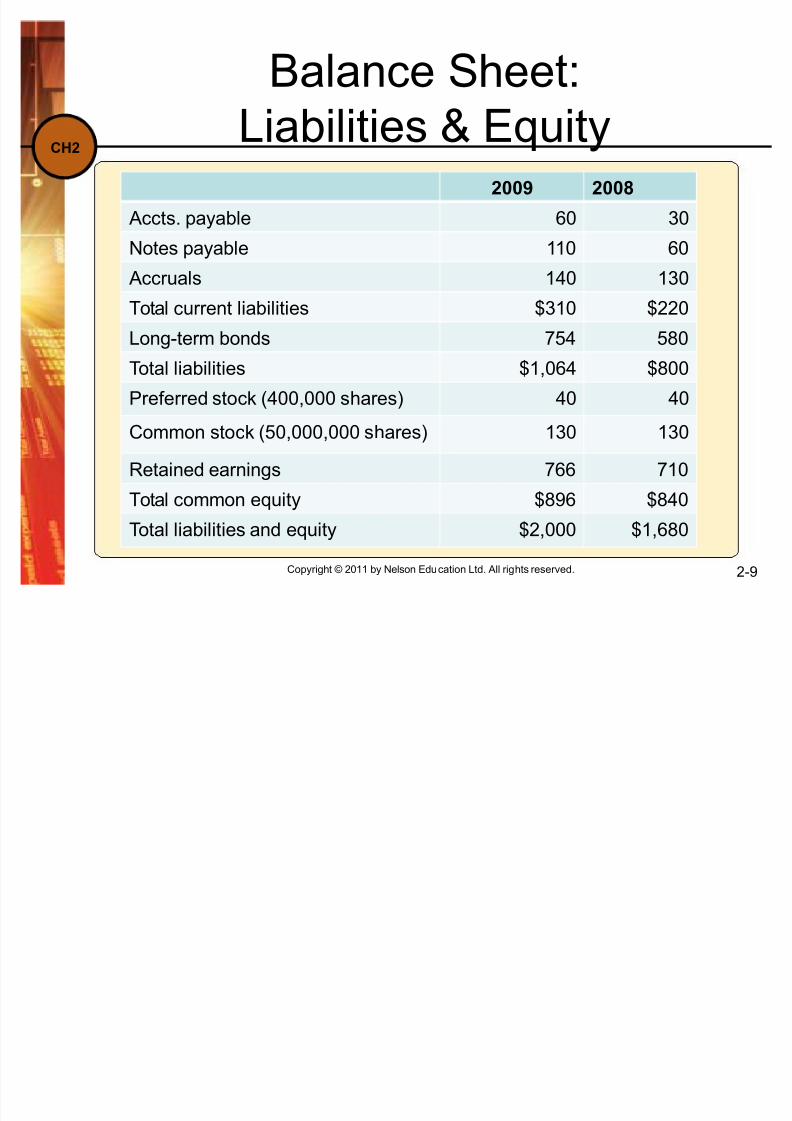

Balance Sheet:

Liabilities & Equity2009 2008

Accts. payable 60 30

Notes payable 110 60

Accruals 140 130Total current liabilities $310 $220

Long-term bonds 754 580

Total liabilities $1,064 $800

Preferred stock (400,000 shares) 40 40

Common stock (50,000,000 shares) 130 130

Retained earnings 766 710

Total common equity $896 $840

Total liabilities and equity $2,000 $1,680

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-9

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 10/45

CH2

Implications on Liabilities &

Equity CL increased as creditors and

suppliers ³financed´ part of the

expansion. Long-term debt increased to help

finance the expansion.

Thecompany didn¶t issue any newstock.

Retained earnings went up, due tono dividend payment.

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-10

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 11/45

CH2

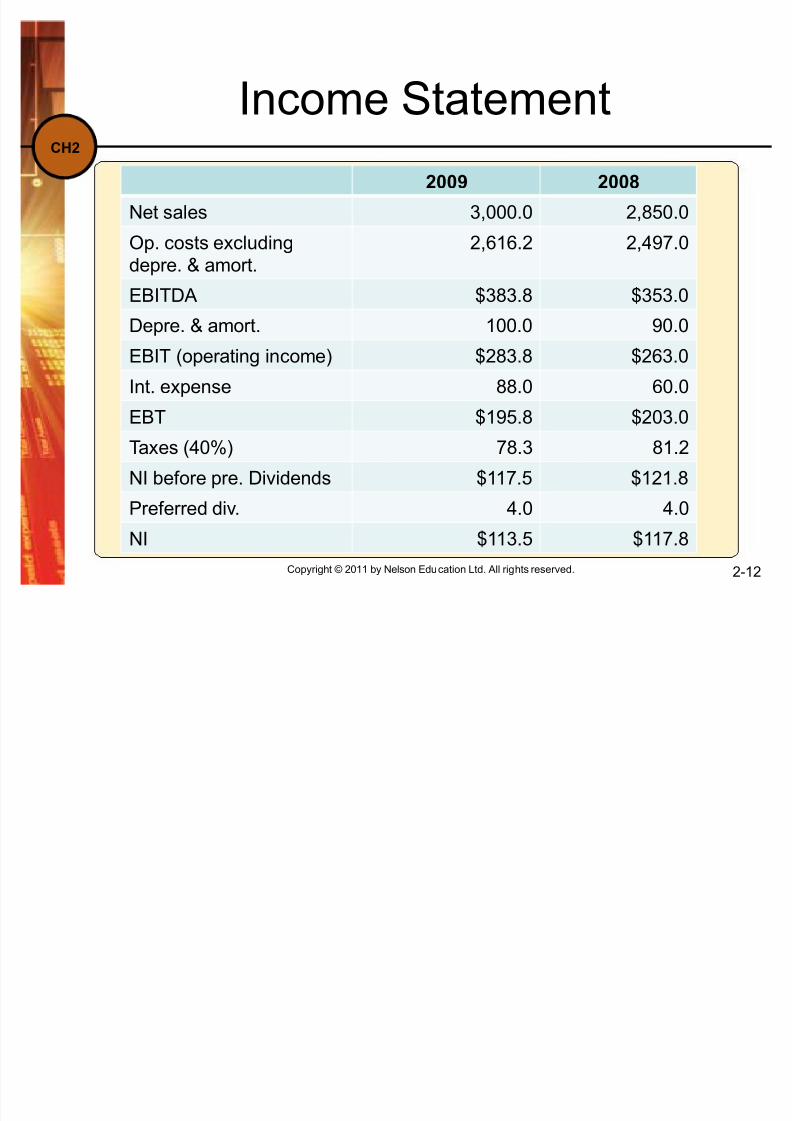

Income Statement

Show a firm¶s performance over aperiod of time such as a month, a

quarter or a year

Although NI (i.e. profit or earnings)is an important item, EBITDA can

be a better measure of financialstrength

EBITDA is not as important as FCF

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-11

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 12/45

CH2

Income Statement

2009 2008

Net sales 3,000.0 2,850.0

Op. costs excludingdepre. & amort.

2,616.2 2,497.0

EBITDA $383.8 $353.0

Depre. & amort. 100.0 90.0

EBIT (operating income) $283.8 $263.0

Int. expense 88.0 60.0

EBT $195.8 $203.0Taxes (40%) 78.3 81.2

NI before pre. Dividends $117.5 $121.8

Preferred div. 4.0 4.0

NI $113.5 $117.8

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-12

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 13/45

CH2

Stock Price and Other Data

2009 2008

Common stock price $23.00 $26.00

# of shares 50,000,000 50,000,000

EPS $2.27 $2.36

DPS $1.15 $1.06

BVPS $17.92 $16.80

CFPS $4.27 $4.16

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-13

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 14/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-14

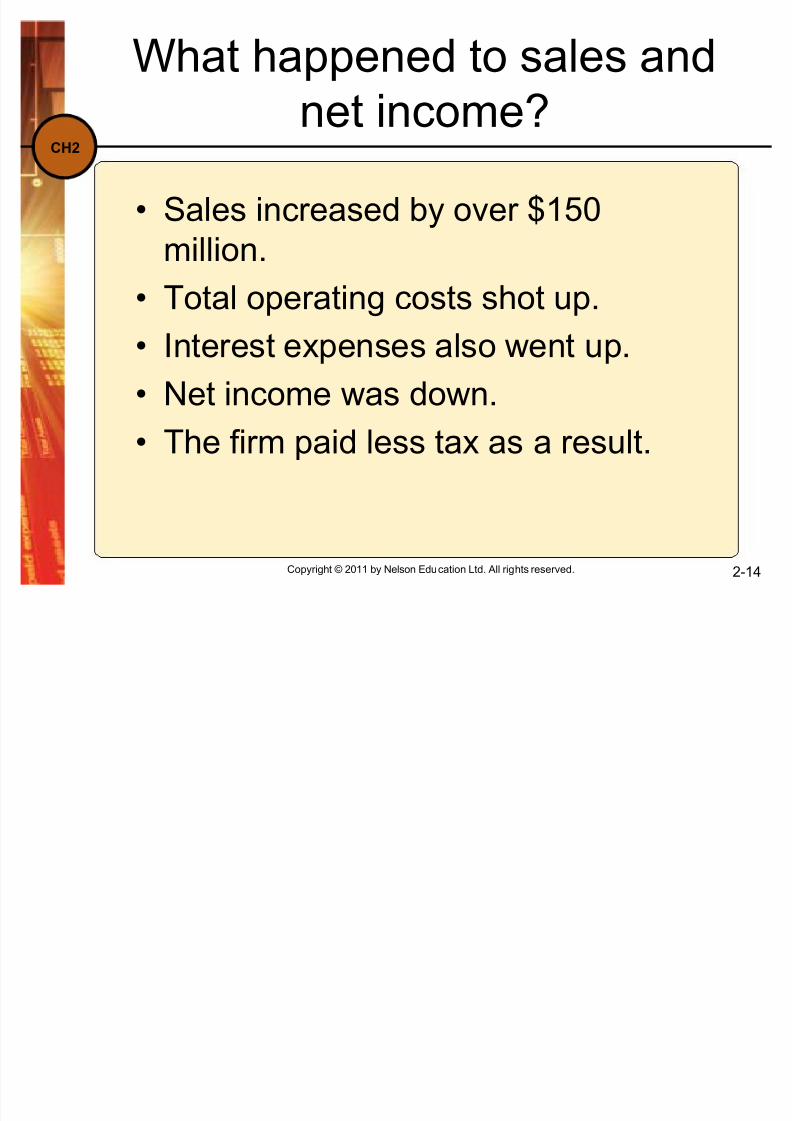

What happened to sales andnet income?

Sales increased by over $150million.

Total operating costs shot up.

Interest expenses also went up.

Net income was down.

The firm paid less tax as a result.

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 15/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-15

Statement of RetainedEarnings, 2009

Balance of retained earnings,12/31/2008 $710.0

Add: Net income, 2009 113.5

Less: Dividends paid, 2009 (57.5)Balance of retained earnings,12/31/2009 $766.0

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 16/45

CH2

Net Cash Flow

Net cash flow accounting profitsince some revenues and expenses

are not received or paid in cash

NCF = NI ± noncash revenues +noncash charges

NCF = NI + Depreciation andamortization

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-16

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 17/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-17

Statement of Cash Flows: 2009

Operating Activities

Net Income $117.5

Adjustments:Depreciation 100.0

Change in A/R (60.0)

Change in inventories (200.0)

Change in A/P 30.0

Change in accruals 10.0

Net cash provided by op. act. ($2.5)

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 18/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-18

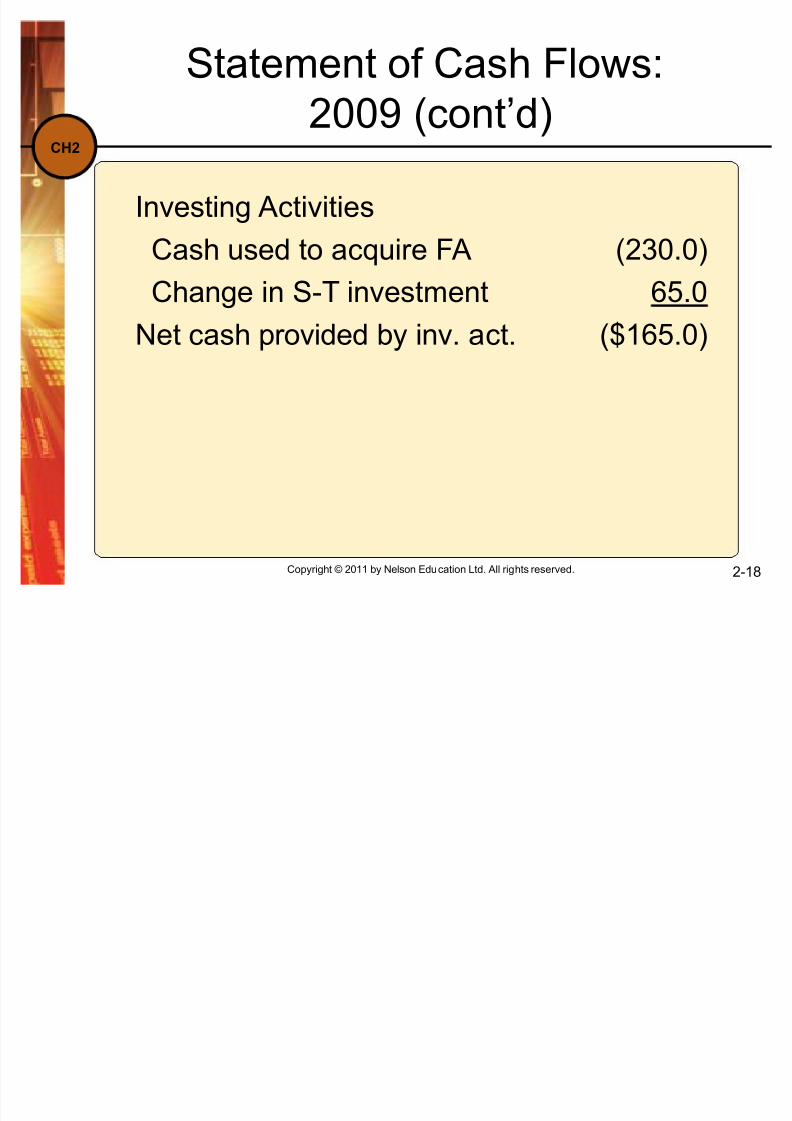

Statement of Cash Flows:2009 (cont¶d)

Investing Activities

Cash used to acquire FA (230.0)

Change in S-T investment 65.0

Net cash provided by inv. act. ($165.0)

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 19/45

CH2

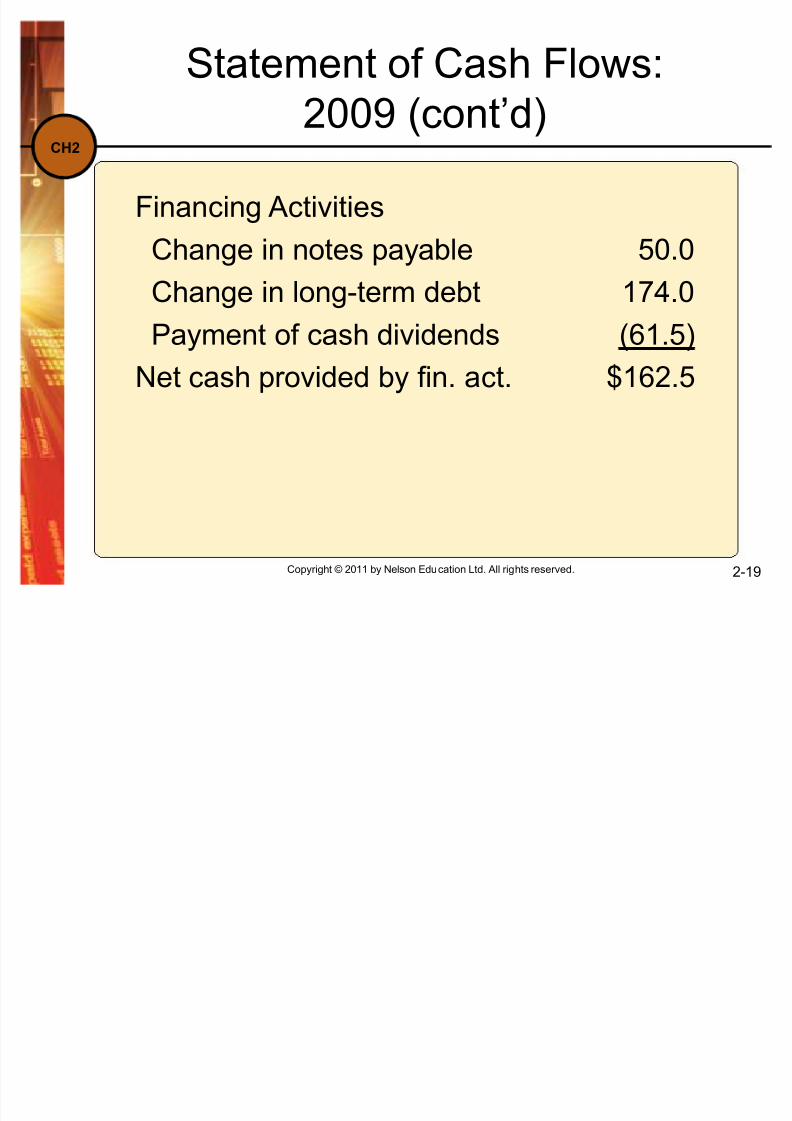

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-19

Financing Activities

Change in notes payable 50.0

Change in long-term debt 174.0

Payment of cash dividends (61.5)

Net cash provided by fin. act. $162.5

Statement of Cash Flows:2009 (cont¶d)

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 20/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-20

Summary of Statement of CF

Net cash provided by op. act. (2.5)

Netc

ash

provided by inv. ac

t. (165.5)Net cash provided by fin. act. 162.5

Net change in cash ($5.0)

Cash at beginning of year 15.0

Cash at end of year $10.0

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 21/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-21

What can you conclude fromthe statement of cash flows?

Net CF from operations = -$2.5 million,because of reduction net income and big

increases in working

capital. The firm spent $230 million on fixed

assets.

The firm borrowed heavily and sold

bonds to meet itscash

requirements. Even after borrowing, the cash account

fell by $5m.

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 22/45

CH2

What are operating current

assets? Operating current assets are the

CA needed to support operations.

± Op CA include: cash, inventory,receivables.

± Op CA exclude: short-term

investments, because t

hese are not apart of operations.

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-22

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 23/45

CH2

What are operating current

liabilities? Operating current liabilities are the

CL resulting as a normal part of

operations. ± Op CL include: accounts payable and

accruals.

± Op CL exclude: notes payable,because this is a sour ce of financing,not a part of operations.

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-23

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 24/45

CH2

Net Operating Working

Capital (NOWC) NOWC = Operating current assets

± Operating current liabilities

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-24

NOWC2009 = ($10 + $375 + $615)

- ($60 + $140)

= $800 millionUse (Cash + A/R + inventories) ± (A/P + accruals)

to try NOWC2008.

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 25/45

CH2

Total net operating capital

(also called operating capital) Total net operating capital = NOWC

+ operating long-term assets.

(TN)OC2009 = $800 + $1,000 =$1,800 million

(TN)OC2008 = $585 + $870 = $1,455

million

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-25

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 26/45

CH2

Net Operating Profit after

Taxes (NOPAT)NOPAT = EBIT(1 - Tax rate) =

Operating income × ( 1 ± Tax rate)

NOPAT2009 = $283.8 ×(1 - 0.4)

= $170.3 million

NOPAT2008 = $157.8 million

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-26

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 27/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-27

What is free cash flow (FCF)?Why is it important?

FCF is the amount of cash availablefrom operations for distribution to all

investors (including stockholdersand debtholders) after making thenecessary investments to support

operations. A company¶s value depends upon

the amount of FCF it can generate.

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 28/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-28

What are the five uses of FCF?

1. Pay interest on debt.

2. Pay back principal on debt.

3. Pay cash dividends.

4. Buy back stock.

5. Buy non-operating assets (e.g.,marketable securities, investmentsin other companies, etc.)

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 29/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-29

Free Cash Flow (FCF) for 2009

FCF = NOPAT - Net investment in

operating capital

= $170.3 - ($1,800 - $1,455)

= $170.3 - $345.0

= -$174.7 million

How do you suppose investors reacted?

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 30/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-30

Free Cash Flow (FCF) for 2009

FCF = Operating cash flow ± grossinvestment in operating capital

OCF = NOPAT + depreciation

Gross investment in operating capital = netinvestment in op. capital + depreciation

= ($170.3 + $100) - ($345 + $100)= $270.3 - $445.0

= -$174.7 million (same as before)

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 31/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-31

Return on Invested Capital (ROIC)

ROIC = NOPAT / operating capital

ROIC2009 = $170.3 / $1,800 = 9.46%

Is this enough to cover the firm¶s cost of

capital?

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 32/45

CH2

Market Value Added (MVA)

MVA = Market Value of the Firm -Book Value of the Firm

Market Value = (# shares of stock)(price per share) + Value of debt

Book Value = Total common equity+ Value of debt

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-32

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 33/45

CH2

MVA (cont¶d)

If the market value and book valueof debt are close, then MVA is:

MVA = Market value of equity ±book value of equity

MVA = (Shares outstanding)(Stock

price) ± total common equity MVA = Total market value ± total

investors supplied capital

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-33

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 34/45

CH2

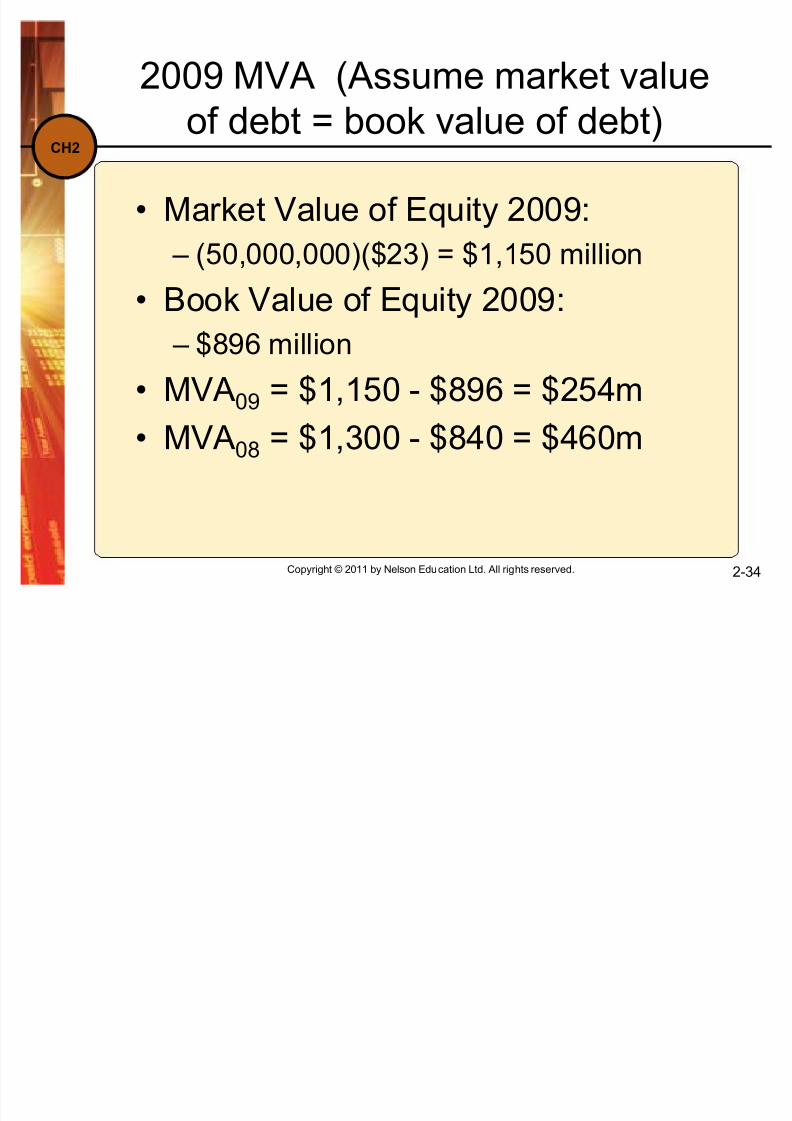

2009 MVA (Assume market valueof debt = book value of debt)

Market Value of Equity 2009:

± (50,000,000)($23) = $1,150 million

Book Value of Equity 2009:

± $896 million

MVA09 = $1,150 - $896 = $254m

MVA08 = $1,300 - $840 = $460m

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-34

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 35/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-35

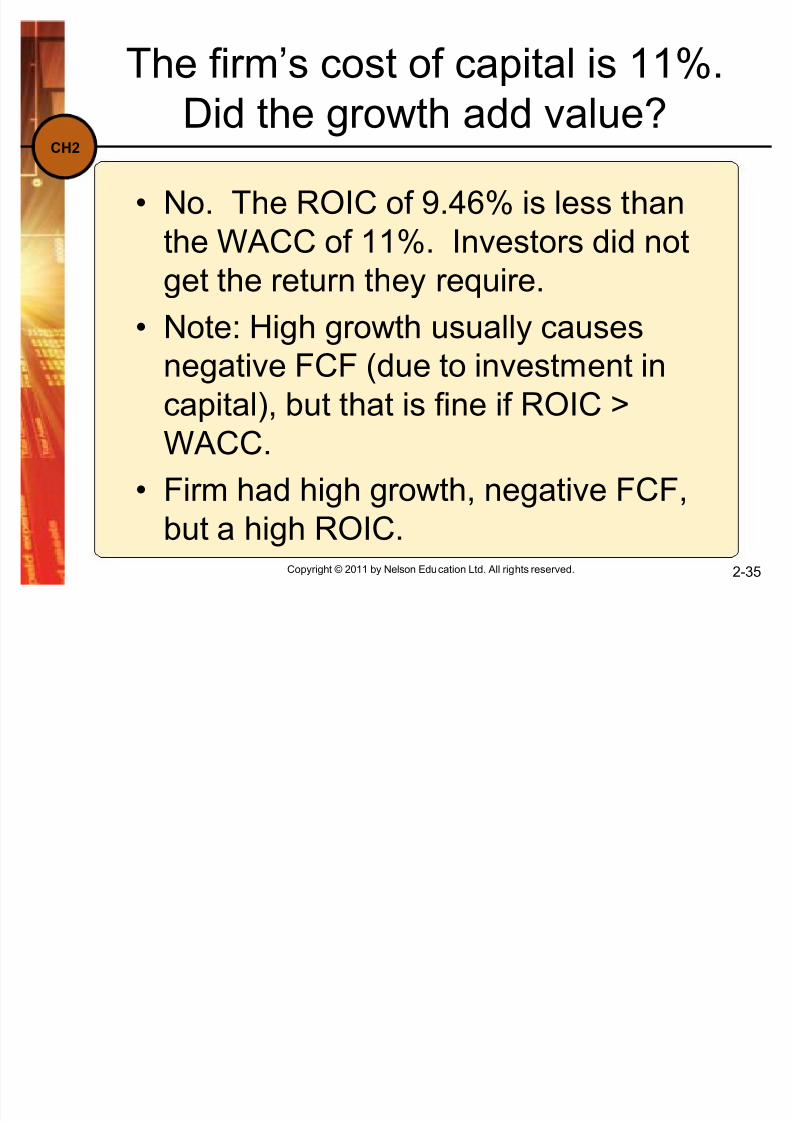

The firm¶s cost of capital is 11%.Did the growth add value?

No. The ROIC of 9.46% is less thanthe WACC of 11%. Investors did not

get the return they require. Note: High growth usually causes

negative FCF (due to investment inc

apital), but th

at is fine if ROIC >WACC.

Firm had high growth, negative FCF,but a high ROIC.

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 36/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-36

Economic Value Added (EVA)

WACC is weighted average cost of capital

EVA = NOPAT- [(WACC)(Capital)]

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 37/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-37

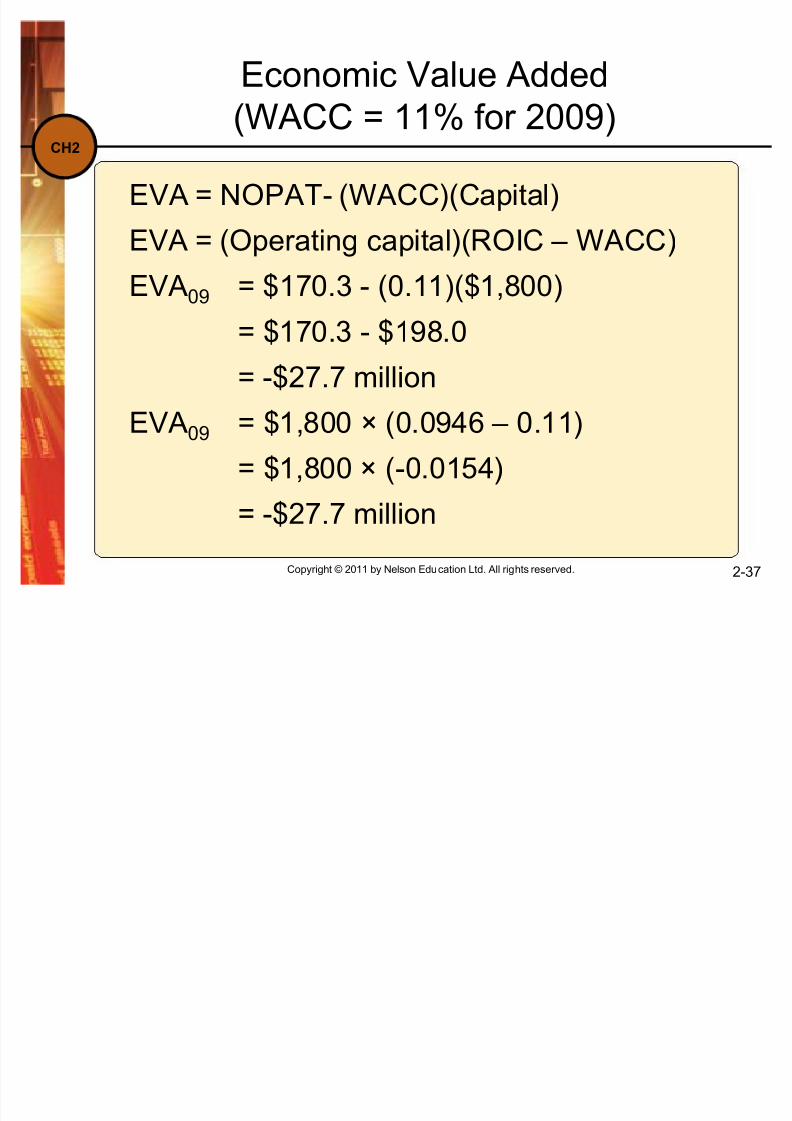

Economic Value Added(WACC = 11% for 2009)

EVA = NOPAT- (WACC)(Capital)

EVA = (Operating capital)(ROIC ± WACC)

EVA09 = $170.3 - (0.11)($1,800)

= $170.3 - $198.0

= -$27.7 million

EVA09 = $1,800 × (0.0946 ± 0.11)= $1,800 × (-0.0154)

= -$27.7 million

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 38/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-38

Key Features of the Tax Code

Corporate Taxes ± Rate vary with firm size, location, and type of

income being earned ± Both the federal and provincial governments

tax companies

Individual Taxes ± Rate are progressive

± Income tax must be paid at the federal andprovincial level

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 39/45

CH2

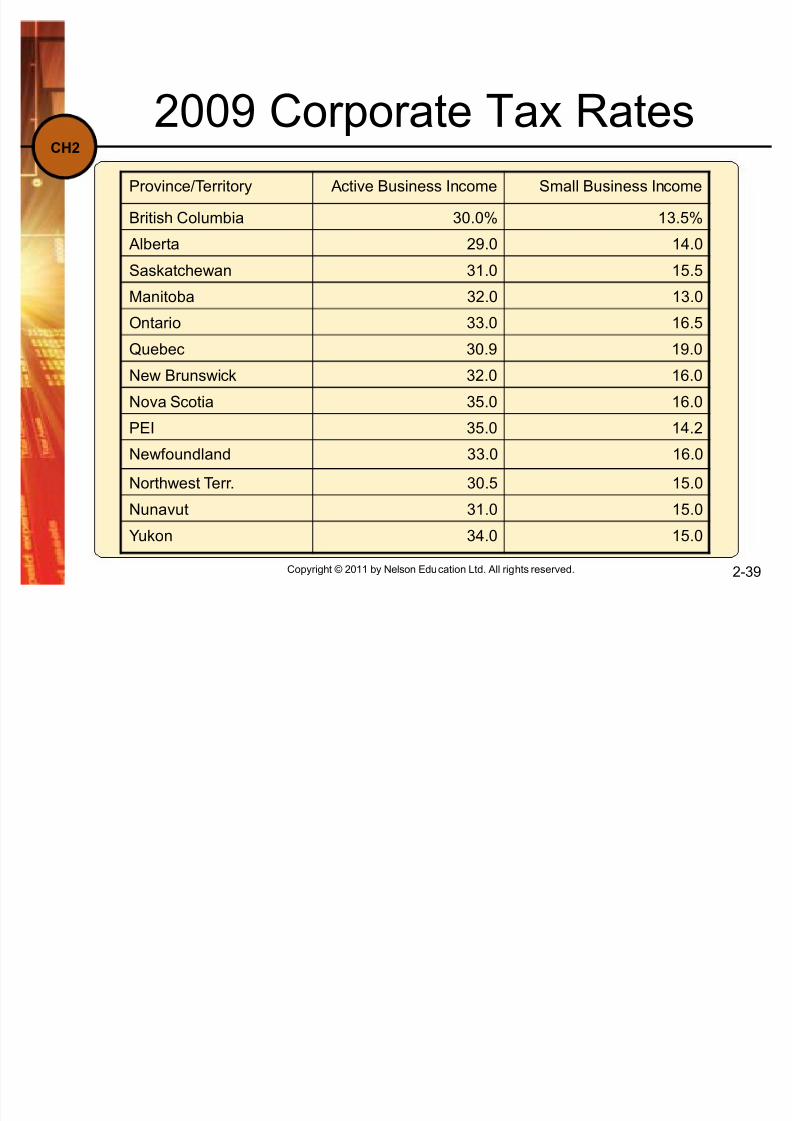

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-39

2009 Corporate Tax Rates

Province/Territory Active Business Income Small Business Income

British Columbia 30.0% 13.5%

Alberta 29.0 14.0

Saskatchewan 31.0 15.5

Manitoba 32.0 13.0

Ontario 33.0 16.5

Quebec 30.9 19.0

New Brunswick 32.0 16.0

Nova Scotia 35.0 16.0

PEI 35.0 14.2

Newfoundland 33.0 16.0

Northwest Terr. 30.5 15.0

Nunavut 31.0 15.0

Yukon 34.0 15.0

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 40/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-40

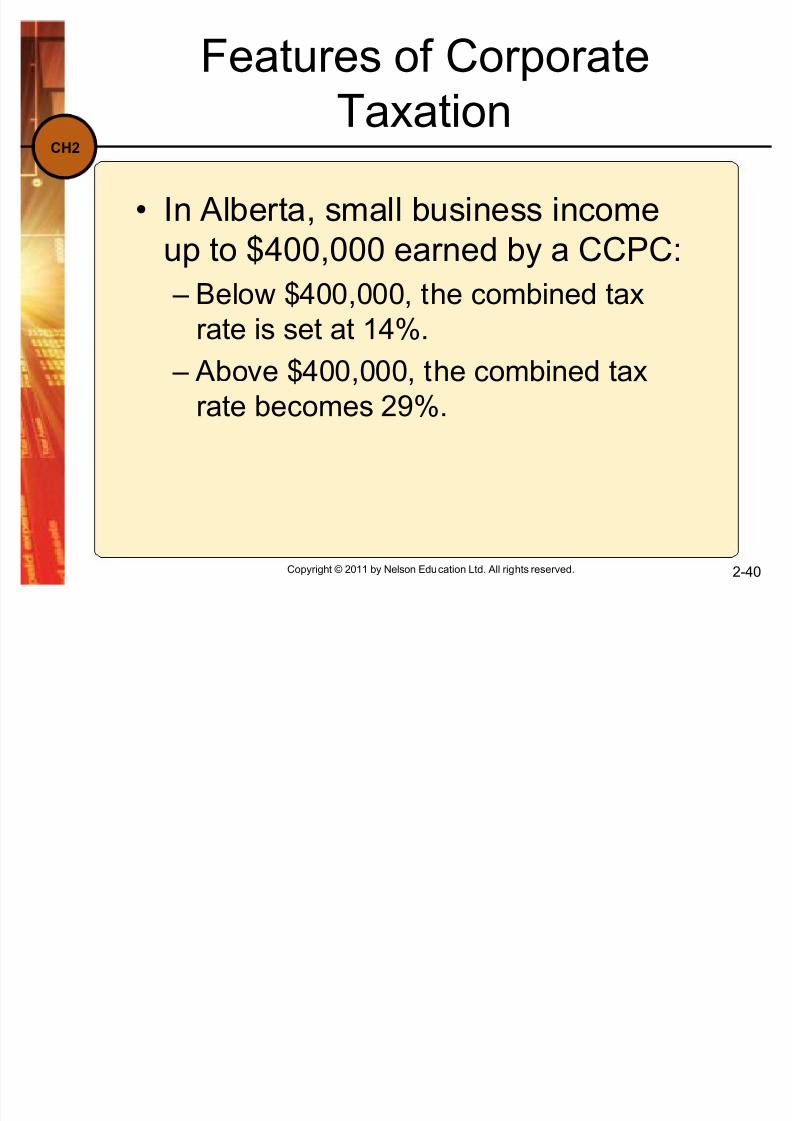

Features of CorporateTaxation

In Alberta, small business incomeup to $400,000 earned by a CCPC:

± Below $400,000, the combined taxrate is set at 14%.

± Above $400,000, the combined tax

rate bec

omes 29%.

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 41/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-41

Features of Corporate Taxes (cont¶d)

A corporation can:

± deduct its interest expenses but not its

dividend payments. ± carry back losses for 3 years, carry forward

losses for 10 years.*

± Exclude 100% of dividend income if received

from anoth

er Canadianc

orporation*The loss treatment is to avoid penalizing corporationswhose incomes fluctuate substantially from year toyear.

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 42/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-42

Example

Assume a small Alberta Canadian-controlled private corporation

(CCPC) has $500,000 of taxableincome from operations, $25,000 of interest income, and $50,000 of

dividend income. What is its tax liability?

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 43/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-43

Operating income $500,000

Interest income 25,000Taxable dividend

income0*

Taxable income $525,000

*Dividend earned from Canadian companies faces no taxation

Example (cont¶d)

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 44/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-44

Taxable Income = $525,000

Tax on base @14% = $56,000= $400,000×0.14

Amount over base = $525,000 - $400,000

= $125,000

Total Tax = $56,000 + 0.29 ($125,000)= $92,250

Example (cont¶d)

8/3/2019 Ch02 Ppt Brighamfm1ce

http://slidepdf.com/reader/full/ch02-ppt-brighamfm1ce 45/45

CH2

Copyright © 2011 by Nelson Education Ltd. All rights reserved. 2-45

Key Features of IndividualTaxation

Individuals face progressive taxrates, from 15% to 29%.

The rate on capital gains is one half the rate of ordinary income. Dividends consist of a gross up of

the actual dividend, calculating tax

on the grossed up dividend andthen taking a tax credit on thegrossed up amount.