ch. chancery division. 303 - formatevi.com paulings settlement...1 ch. chancery division. 303 ......

TRANSCRIPT

1 Ch. CHANCERY DIVISION. 303

C. A. In re PAULING'S SETTLEMENT TEUSTS. 1963

YOUNGHUSBAND AND OTHERS V. COUTTS & CO. March 6, 7, 8, l l , 12, 13, 14,15,18,19,

[1958 P. 2540.] 20,21,22,25, Trusts—Breach of trust—Consent of beneficiary—Whether beneficiary

26,27. May 29.

entitled to relief against trustees — Advancement to beneficiary— Willmer, Payment to third party. upjohnVjj.

Trusts — Breach of trust — Professional trustees — Trustees' duty in conflict with interest—Whether entitled to relief—Trustee Act, 1925 (15 & 16 Geo. 5, c. 19), s. 61.

Trusts—Power of advancement—Exercise of power—Settlement—Power to advance far beneficiary's absolute use—Whether power fiduciary —Particular purpose specified—Duty of trustee-

Undue Influence — Gift by child to parent — Presumption of undue influence—Requirements to support valid gift.

Acquiescence—Breach of trust—Delay by beneficiary in bringing action —Beneficiary's knowledge of his rights essential.

Limitation of Action—Trust—Action by beneficiary—"Future inter-" est"—Advancements in breach of trust—Limitation Act, 1939 (2 & 3 Geo. 6. c. 21), s. 19 (2), proviso.

Teaches — Statutory period of limitation — Action by beneficiary for breach of trust—Doctrine inapplicable.

By clause 11 of a marriage settlement made in 1919 upon the marriage of the plaintiffs' parents, it was provided that the trustees (the defendant bank) might with the written consent of the wife, who was the life tenant, raise any part not exceeding one-half of the expectant, presumptive or vested share of any child of the wife in the trust fund and pay the same to him or her for his or her own absolute use or pay or apply the same for his or her advancement or otherwise for his or her benefit in such manner as the trustees should think fit.

The plaintiffs, Francis, George, Ann and Anthony, were the four children of the marriage who attained their majorities on October 15, 1941, October 11, 1946, March 24, 1949, and June 15, 1951, respectively. The family were a united family, who, at all material times, lived beyond their means and were continually in grave financial difficulties. The mother had a current account with the defendant bank, which was between September, 1948, and August, 1959, continuously overdrawn by some £2,000 or more.' At all material times the children knew of the family's financial difficulties.

Between 1948 and 1954, the bank, in purported exercise of their powers under clause 11, made a number of advances to the children, who, on some though not on every occasion, received independent legal advice as to their rights under the settlement. The mother's

[Reported by T. C. C. BARKWORTH, Esq., Barrister-at-Law.]

304 CHANCERY DIVISION. [ 1 9 6 4 ]

C A. consent was obtained in every case. Those advances were as follows : lg6„ in September and November, 1948, two advances, totalling £8,450

_; : to Francis and George who authorised the bank to apply them for PAULING'S the purchase of a house for the family in the Isle of Man: the sons

SETTLEMENT received no independent legal advice. Subsequently, on October 26, IRUSTS, 1948, the house was purchased and on the father's instructions and

' • without the consent or knowledge of the sons, the bank caused the conveyance to be made in favour of the parents. On September 13, 1948, an advance of £1,000 to Francis and George, which, on the authority of a " c h i t " signed by the sons, the bank paid directly into the mother's overdrawn account; as to this sum, the bank was told that the sons proposed to use it for the purchase of furniture for the house in the Isle of Man. No furniture was in fact bought, and the bank took no steps to inquire whether any had been bought. On September 13, 1948, an advance to Francis and George of £2,600 which the bank applied in discharge of a loan known as " the " Hodson Loan " on the mother's life interest under another settlement : the sons received independent legal advice. On May 13, 1949, an advance of £2,000 to Francis and George, which was paid directly into the mother's overdrawn current account. This payment was made on the authority of a memorandum prepared by the bank and signed by the sons stating that the money was to be used for "improvements" to the house in the Isle of Man. On June 3, 1949, an advance to Ann of £2,986 Is. 9d. applied by her in the purchase of a house in London, to which objection was not taken, and between August 26, 1949, and June 12, 1950, nine advances and part of a tenth to Ann of together £1,803 12s. 8d. for work and improvements to the house in London to none of which objection was taken. Between September 12, 1949, and August 21, 1950, six advances and part of another totalling £3,260 to Ann nominally for the purchase of furniture for the house in London, but which were transferred either to the father or to the mother's overdrawn account. Of this sum some £300 only was spent on furniture for Ann's house. Between July 11, 1951, and February 7, 1952, five advances to Anthony, together amounting to £6,500 of which all but £1,000 was paid directly into the mother's account, the £1,000 being used to pay off a loan charged on his sister's house in London. Anthony had an account with the bank, which was replenished from his mother's account whenever he was overdrawn by an arrangement made long before the advances. Finally there were eight advances between September 25, 1953, and June 17, 1954, four to Francis, totalling £2,475, two to George totalling £1,425, and two to Ann totalling £1,450, all of which were paid straight into the mother's account. I t was the policy of the bank to allow the mother's overdraft to be restored to its former figure so that any moneys paid in might be used.

The plaintiffs issued a writ against the bank claiming that they had wrongfully and in breach of trust paid out by way of advancement to beneficiaries who were presumed to be subject to undue influence and who were not emancipated from parental control, the sum of £29,160, and that they were liable to make good that sum,

1 C h . CHANCERY DIVISION. 305

together with the fees charged in respect of the advances and claiming if necessary the appointment of new trustees. The defendant bank pleaded, inter alia, the Limitation Act, 1939, laches and acquiescence.

Wilberforce J . held that when considering whether it was fair and equitable for a beneficiary who had concurred in such transactions to sue the trustee for breach of trust the court must consider all the circumstances in which the concurrence was given, and that subject to that, it was not necessary that the beneficiary should know that what he was concurring in was a breach of trust provided that he fully understood what he was concurring in, and that it was not necessary that the beneficiary himself should have benefited by the breach of trust. He accordingly held the bank liable to make good £14,950 subject to certain deductions, if any, which should be found on inquiry to be deductible in respect of the advances to Anthony and also repayment of the fees of £20 6s. 6d. charged on the advances. The plaintiffs appealed and the bank cross-appealed : —

Held, (1) that, having regard to the very wide interpretation placed by the House of Lords upon the statutory power of advancement, which approximated to the second limb of the power contained in clause 11 of the settlement, the ambit of the two limbs of the power did not substantially differ from each other; that in both cases the power was a fiduciary one, the power under the first limb as under the second limb being exercisable only if it were for the benefit of the child or remoter issue to be advanced (post, p. 333); and that therefore the trustees before an exercise thereof must weigh the benefit to the proposed advancee against the rights of those who were or might become interested under the settlement.

In re Pilkington's Will Trusts [1964] A.C. 612; [1962] 3 W.L.R. 1051; [1962] 3 All E.R. 622, H-L.<E.) applied.

(2) That the power was exercisable, if the circumstances warranted it, either by an out and out payment to the person advanced or by a payment for a particular purpose specified by the trustees, the advancee being then under a duty to carry out that purpose and the trustees being under a duty to see that he did so and under a duty not to leave the advancee free to spend it in any way he chose (post, p. 334).

(3) That if an advance were a proper exercise of the power the consent of a beneficiary, although an adult, was unnecessary in the absence of any express provision to the contrary in the settlement (post, p. 335). If an advance were made to or for the benefit of a beneficiary in an improper exercise of the power, but that beneficiary is suing only to compel the trustees to replace sums wrongly advanced to him or applied for his benefit, then, if the trustees could establish a valid request or consent to the advance in question, such request or consent affords a good defence to that beneficiary's claim even though the advance was made in breach of trust (post, p. 335). .

In re Pilkington's Will Trusts (supra) applied.

C. A.

1963

PAULINO'S SETTLEMENT

TRUSTS, In re.

306 CHANCERY DIVISION. [ 1 9 6 4 ]

C- A. (4) That where the presumption of undue influence existed a .gg„ gift by a child could not be retained by a parent unless he could

show first, that the gift was the spontaneous act of the child, and PAULINO'S secondly, that the child knew what his rights were. I t was also

SETTLEMENT desirable that the child should have had independent and, if /n*8*8 possible, professional advice (post, p. 336).

' Dictum of Cotton L.J. in Allcard v. Skinner (1887) 36 Ch.D. 145, 171; 3 T.L.R. 751, C.A.; Huguenin v. Baseley (1807) 14 Ves. 273, and dictum of Farwell J. in Fowell v. Powell [1900] 1 Ch. 243, 246 considered.

(5) That where a banker undertook to act as a paid trustee of a settlement created by a customer and so deliberately placed himself in a position where his duty as trustee conflicted with his interest as banker, the court should be slow to relieve him under section 61 of the Trustee Act, 1925 (post, p. 339).

(6) That where a beneficiary rightly sued trustees for breaches of trust, he was under no obligation to account for any benefit incidentally received by him but that where he had consented to such breach he must give credit for the property that he had in fact received as a result; that this principle, however, did not apply in the circumstances of this case to the advance of £2,600 used to pay off the Hodson Loan since Francis and George to whom the advance was made were wholly ignorant of and had never consented to the transaction as it was in fact carried out (post, pp. 357, 358); that since, however, the bank had received a letter from the sons' solicitors stating that the transaction was satisfactory, they ought fairly to be relieved under section 61, but (Willmer L.J. dissenting) such relief should be limited to the extent of the surrender value of the four insurance policies transferred to the sons (post, pp. 358, 359).

(7) That, on the facts, (i) the advance of £8,450 for the purchase of the house in the Isle of Man was a breach of trust to which the sons never consented and the bank was liable to restore that amount to the trust fund; (ii) the advance of £1,000 for the purchase of furniture for the house in the Isle of Man was a plain breach of trust in which the bank placed themselves in a position where their interest as bankers conflicted with their duty as trustees, and no question of relief under section 61 arose; (iii) the advance of £2,000 for improvements to the house in the Isle of Man was, likewise, a plain breach of trust, but, in the circumstances of the case, the bank had a good defence in that they obtained consents from both George and Francis, the two children concerned, who were emancipated from parental control; (iv) the advances of £3,260 to Ann, nominally for furniture for the house in London, were clearly breaches of trust, but, though Ann had independent advice as to the purchase of the house that did not extend to these advances and consequently the bank could not rely on her consent as a defence since she was still presumed to be acting under the undue influence of her parents. However, having in fact received about £300 worth of furniture, Ann was bound to give credit for this sum, but the bank having behaved unreasonably no question of relief under

1 Ch. CHANCERY DIVISION. 307

section 61 of the Trustee Act, 1925, arose; (v) the advances of £6,500 to Anthony were clearly breaches of trust for which the bank was liable and relief under section 61 of the Trustee Act, 1925, was out of the question. Though Anthony, who was still under the presumed undue influence of his father, might have received some indirect benefit, in the circumstances there was nothing to entitle a defaulting trustee to demand that he should account for such benefit; (vi) the eight advances amounting to £5,350 in all, to Francis, George and Ann between September, 1953, and June, 1954, were all clear breaches of trust but they were assented to by the beneficiaries concerned, who were all by that time emancipated from parental control and accordingly these sums were not recoverable.

(8) That (post, p. 353) (affirming Wilberforce J . [1962] 1 W.L.R. at p. 115) the plaintiffs' rights were preserved by the proviso to section 19 (2) of the Limitation Act, 1939, since they undoubtedly had a " future interest " which did not fall into possession when the trustees by an ex hypothesi invalid advance raised a sum of money out of the capital, the mother's consent not being equivalent to a release of her life interest.

(9) That (affirming Wilberforce J. ibid.) there being an express statutory provision of a period of limitation for the plaintiff's claims, there was no room for the doctrine of laches (post, p. 353).

(10) That a party could not be said to have acquiesced unless he knew, or ought to have known, what his rights were (post, p. 353); and on the facts of this case the plaintiffs could not be criticised for failing to realise what these rights were until 1954, when they were advised that the advances might have been improper, and accordingly, the writ having been issued in 1958, it would not be right to debar the plaintiffs by acquiescence from bringing an action which otherwise was justified.

Allcard v. Skinner (1887) 36 Ch.D. 145; 3 T.L.R. 751, C.A. considered.

Decision of Wilberforce J . [1962] 1 W.L.R. 86; [1962] 3 All E.R. 713 upheld in part.

APPEAL from Wilberforce J . 1

The following s ta tement of facts is taken from the judgment of Wilberforce J .

The plaintiffs, Francis George Arthur Younghusband, George Oswald Younghusband, Ann Margaret Madeleine Broadbent and Anthony Arthur David Younghusband, were the four children of the marriage between Violet Pauling (now Violet Younghusband) and Commander Francis Charles Eobert Eomer Younghusband. The defendants, Coutts & Co., were the trustees of the marriage settlement made in 1919 on the marriage of the plaintiffs' parents.

The trusts of the sett lement, dated December 30, 1919, after

C. A.

1963

PAULINO'S SETTLEMENT

TRUSTS, In re.

i [1962] 1 W.L.B. 86; [1962] 3 All E.E. 713.

308 CHANCERY DIVISION. [ 1 9 6 4 ]

C. A. reciting that the wife was entitled to certain investments, pro-igg3 vided by clause 5 that the trusteee might during the life of the

;— wife raise sums not exceeding £10,000 and pay the same to the SETTLEMENT w ^ e f°r ^er absolute use and benefit. That power had been

TRUSTS, exercised in full at some time prior to the date of the transactions " complained of in the action. By clause 6 the income of the

trust fund was payable to the wife for life without power of anticipation and after her death there was provision for an annuity to the husband of £500 a year during his life but determinable as therein mentioned. Clause 7 contained a power for the wife by will or codicil to appoint an interest to a surviving husband. Clause 8 contained trusts of capital in favour of the wife's children or remoter issue whether by the intended or any future marriage as the wife should appoint, and in default of such appointment to such children who should attain twenty-one, or, being female, marry under that age. Clause 11 contained a power of advancement in the following terms: " It " shall be lawful for the trustees at any time or times after the " death of the wife or in her lifetime with her consent in writing, " to raise any part or parts not exceeding in the whole one half of " the then expectant or presumptive or vested share of any child " or more remote issue of the wife in the said trust premises " under the trusts hereinbefore contained and to pay the same to '' him or her for his or her own absolute use or to pay or apply the " same for his or her advancement or otherwise for his or her " benefit in such manner as the trustees shall think fit . . . " By clause 14 the trustees were given power at any time during the life of the wife with her consent in writing to expend a sum not exceeding £10,000 in purchasing a house, with the limitation that the house or premises should be situated in England, Wales, Scotland or Ireland. Lastly provision was made for the bank to act as bankers in respect of the trust funds without being liable to account for profits and to be remunerated for their services in accordance with their published scale of fees. Charles Eussell & Co. were the solicitors acting for the trust and the bank's own solicitors were Farrer & Co. In addition to the income from the settlement the mother enjoyed a small life interest under the will of her deceased uncle, and there were also certain shares standing in the joint names of the commander and his mother but apart from this the family were solely dependent on the income from the settlement.

The plaintiffs between them were entitled to the capital of the trust fund. Their dates of birth were : Francis, October 15,

1 C h . CHANCERY DIVISION. 309

1920, George, October 11, 1925, Ann, March 24, 1928 and C. A. Anthony, June 15, 1930. 1963

Before the transactions complained of in the action, the ~~ ; family had been living,in Gloucestershire at Clifford Manor, SETTLEMENT where they maintained a considerable establishment. At all TRUSTS, material times they lived beyond their means and were con- ' tinually in grave financial difficulties. The wife had a current account with the bank, on which her husband, the commander, could draw and which between September, 1948, and August, 1950, was continuously overdrawn by some £2,000 or more. The family was a united one and the children knew of the family's financial difficulties. In 1947 the financial difficulties turned into crisis. Clifford Manor was sold and the furniture was stored. The commander and the mother went to the United States of America, where the commander had obtained employment, leaving their children to pursue their education and spend their holidays with friends and relations, but before the end of the year they returned, the commander having given up any idea of living permanently in the United States, and having formed the idea of settling in the Isle of Man. Under the settlement, however, it appeared that there was no power to purchase land in the Isle of Man, and advice was accordingly sought from Charles Eussell & Co., who in turn sought counsel's opinion. Counsel confirmed the view that there was no power under clause 14 to purchase a house in the Isle of Man but advised that the desired object could be achieved by making use of the power of advancement under clause 11 to advance money to the two eldest sons, Francis and George, who were of age and who could thus purchase the house and settle it voluntarily upon the mother for life with remainder to themselves. Counsel emphasised, however, that this could only be done by a voluntary act on the part of the two sons who should be separately advised. Francis and George agreed to this course but said they fully understood the matter and disclaimed any desire to be separately advised. Accordingly, in September, 1948, the trustees raised £8,450 from capital and made an advance (Advances Nos. 1 & 4) to Francis and George and this was applied in the purchase of Oakhill Lodge, Douglas, Isle of Man. The house, however, was conveyed in October without the consent or knowledge of the sons, to their parents absolutely, and was not settled as had been suggested. Shortly afterwards, the house was mortgaged by the commander for £5,000, and was eventually sold for less than was needed to pay off the mortgage debt. The

310 CHANCERY DIVISION. [1964]

C. A.

1963

PAULING'S SHTTLBMBNT

TRUSTS, In re.

only benefit that the sons derived from it was that the house became the family home for seven years.

Having become aware of the extent of the possible advances, the commander suggested that it would be advantageous to make advances to the full possible amount and to pay off a loan on the mother's life interest under her uncle's will and the overdraft at the bank. On September 13, 1948, an advance of £1,000 (Advance No. 2) was made to Francis and George, supposedly to enable furniture to be bought for Oakhill, on the authority of a " chit " signed by them, the money being paid directly into their mother's overdrawn account. In fact hardly any furniture was bought. The sons received no independent advice. Similarly, on May 13, 1949, there was an advance of £2,000 (Advance No. 3) to Francis and George which went directly to the mother's account, on the authority of a memorandum prepared by the bank and signed by the sons, stating that the money was to be used for " improvements etc." to Oakhill. Again the sons received no independent advice.

On September 13, 1948, the bank, as trustees, had also advanced to Francis and George a sum of £2,600 (Advance No. 5) which was applied in discharging a loan, which the bank, as trustee of a settlement of another customer of the bank, a Mrs. Hodson, had made to their mother and which had been charged as a mortgage on their mother's life interest under her uncle's will. This loan (known as the Hodson loan) was also secured by four life insurance policies on the mother's life of a total nominal value of £3,000, whose surrender value was then about £650. On this transaction the sons did have separate advice. Charles Eussell & Co. advised that it would be a proper exercise of the power of advancement provided that Francis and George received an adequate quid pro quo in the shape of the assignment to them of the four policies, coupled with covenants by the mother to maintain the premiums and to pay interest on the money advanced. However, the assignment of the life policies, as executed, contained no such covenants by the mother. Bur-rell of Farrer & Co. approved the draft assignment on behalf of the sons without ever consulting them. The sons retained the life policies till 1953 when they gave them back to their mother, on joining with their mother in executing a mortgage dated March 18, 1953, by the mother to the bank of her life interest under her uncle's will for the sum of £2,000. Apparently this was for the purpose of enabling the commander to raise further sums by charging them again. This brought the advances, so far, to

1 C h . CHANCERY DIVISION. 311

£14,050, and thus exhausted the amount which could be advanced to the two eldest sons, according to the initial calculations made by the bank in 1948.

The next child to attain 21 was Ann and shortly before her 21st birthday, when she was in her first year at Oxford, the commander was planning advances to her. On June 3, 1949, a sum of £2,986 Is. 9d. (Advance No. 6) was raised and paid into Ann's account with the bank, this being the only advance that was ever paid into the banking account of a beneficiary who was being advanced. This was applied by her in the purchase of a house at 28, Gunter Grove, Chelsea, the house being conveyed to her, and though it was used as a family home in London, it was legally hers and when it was sold she retained the proceeds of sale. Ann received separate advice and no complaint was made as to this advance. Then followed 16 further advances for Ann's " benefit." These can be divided into two groups, the first consisting of nine advances and part of a tenth, totalling £1,803 12s. 8d. were used as payment for work and improvements to Gunter Grove and no complaint was made with regard to them. These were as follows:

C. A.

1963

PAnLINO'S SETTLEMENT

TRUSTS, In re.

Date Amount Advance No

£ s. d. August 26, 1949 85 10 9 7 October 14, 1949 225 0 0 9 December 13, 1949 200 0 0 11 January 25, 1950 100 0 0 13 January 26, 1950 41 8 6 14 February 18, 1950 14 19 0 15 February 18, 1950 8 12 6 16 May 6, 1950 400 0 0 19 May 17, 1950 200 0 0* 20 June 12, 1950 528 1 11 21

Total £1,803 12 8

* (N.B. This was one half only of the advance made on this date.)

The remainder of the 16 advances, amounting to £3,260, were transferred in most cases on the same day from Ann's account either to the commander or into the mother's overdrawn account, in some cases purportedly for the purchase of furniture for Gunter Grove.

312 CHANCERY DIVISION. [1964]

C A. These advances were as follows: 1963 Date Amount

£ « d. Advance No.

PAULINO'S SETTLEMENT

TRUSTS,

September 12, 1949 November 1, 1949

660 400

0 0

0 0

8 10

In re. January 14, 1950 400 0 0 12 March 8, 1950 300 0 0 17 March 10, 1950 300 0 0 18 May 17, 1950 200 0 Of 20 August 22, 1950 1,000 0 0 22

Total £3,260 0 0

t (N.B. The other half of thiB advance is referred to above.)

Ann asked for these sums to be advanced and in each case did so in writing, representing that they were for furniture, etc., well knowing that in fact only about £300 was so expended from start to finish. The bank made a few protests and asked to see bills, but never in fact did so. Some of the money went into the family's general living expenses through the mother's account. Although Ann received independent advice as to the purchase of the house, she received none as to the expenditure on furniture. This completed the amount which could be advanced to Ann on the initial calculation.

Anthony, the fourth child, attained 21 on June 15, 1951, whilst he was serving with his regiment in Germany. On June 18 the commander called on the bank and told them that he wanted £2,000 raised. A solicitor's letter was to be written to Anthony, giving him separate advice, and then the money was to be raised. Burrell of Farrer & Co. wrote a most perfunctory letter to Anthony and thereafter between July 11, 1951, and February 7, 1952, £6,500 was raised and paid straight into the mother's account.

The advances were as follows: Date

July 11, 1951 August 3, 1951 October 30, 1951 January 19, 1952 February 7, 1952

Amount Advance No. £ s. d.

2,000 0 0 23 1,000 0 0 24 2,000 0 0 25 1,130 0 0 26

370 0 0 27

Total £6,500 0 0

1 C h . CHANCERY DIVISION. 313

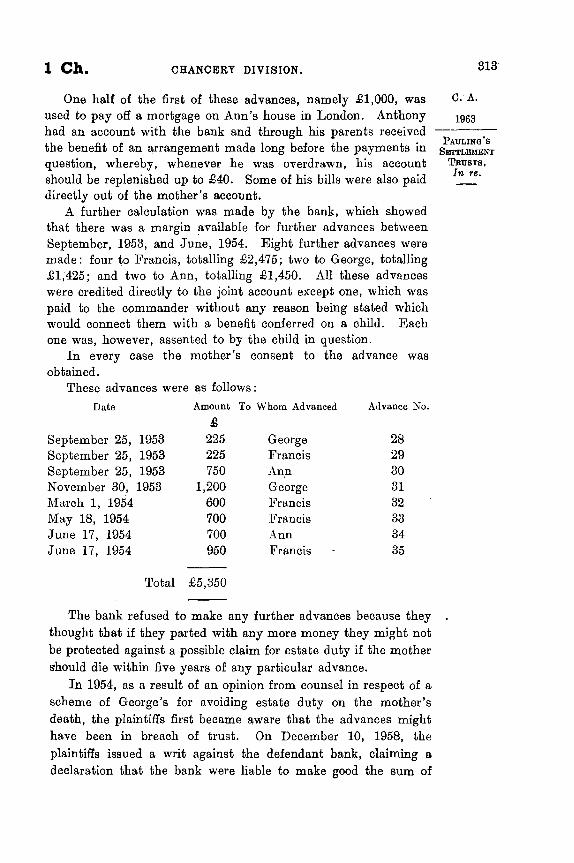

One half of the first of these advances, namely £1,000, was used to pay off a mortgage on Ann's house in London. Anthony had an account with the bank and through his parents received the benefit of an arrangement made long before the payments in question, whereby, whenever he was overdrawn, his account should be replenished up to £40. Some of his bills were also paid directly out of the mother's account.

A further calculation was made by the bank, which showed that there was a margin available for further advances between September, 1953, and June, 1954. Eight further advances were made: four to Francis, totalling £2,475; two to George, totalling £1,425; and two to Ann, totalling £1,450. All these advances were credited directly to the joint account except one, which was paid to the commander without any reason being stated which would connect them with a benefit conferred on a child. Each one was, however, assented to by the child in question.

In every case the mother's consent to the advance was obtained.

These advances were as follows:

C. A. 1963

Date Amount

£ 225.

To Whom Advanced Advance No.

September 25, 1953

Amount

£ 225. George 28

September 25, 1953 225 Francis 29 September 25, 1953 750 Ann 30 November 30, 1953 1,200 George 31 March 1, 1954 600 Francis 32 May 18, 1954 700 Francis 33 June 17, 1954 700 Ann 34 June 17, 1954 950 Francis 35

Total £5,350

Francis

PAULING'S SETTLEMENT

TRUSTS, In re.

The bank refused to make any further advances because they thought that if they parted with any more money they might not be protected against a possible claim for estate duty if the mother should die within five years of any particular advance.

In 1954, as a result of an opinion from counsel in respect of a scheme of George's for avoiding estate duty on the mother's death, the plaintiffs first became aware that the advances might have been in breach of trust. On December 10, 1958, the plaintiffs issued a writ against the defendant bank, claiming a declaration that the bank were liable to make good the sum of

314 CHANCEEY DIVISION. [1964]

C. A. £29,160 which it was alleged the defendants as trustees had 1963 wrongfully and in breach of trust paid out by way of advancement

;— from the trust fund. SETTLEMENT ^ n e statement of claim set out the 35 advances referred to

TECSTS, above, but no claim was made in respect of Nos. 6, 7, 9, 11, 13, ' 14, 15, 16, 19, 21 and part of 20. By clause 10 of the statement of

claim it was alleged that the plaintiffs did not know that the advances were breaches of trust, and that where any consent was given it was given under undue influence whilst the plaintiffs were unemancipated from parental control. In answer to a request for further and better particulars of the statement of claim it was alleged that, except as respected Ann after her marriage, the control and undue influence alleged were such as the. law presumes to exist between a parent and child until emancipation. In regard to Francis, it was further alleged that the control and influence were such as the law presumed to exist between a person suffering from mental ill-health and the person with whom he resides, and that Francis had suffered a complete nervous breakdown in 1940 from which he had never wholly recovered, which disabled him from earning his living and attending to business matters. In Ann's case it was alleged that the control and influence continued after her marriage in respect of her interests under the settlement in that she received no advice or guidance from her husband or anyone else in relation thereto and had become accustomed to comply with her father's wishes. The defence pleaded the Limitation Act, 1939, laches and acquiescence, and claimed relief under section 61 of the Trustee Act, 1925.

Wilberforce J. held (1) that when considering whether it was fair and equitable for a beneficiary, who had concurred in such transactions, to sue the trustees for breach of trust the court must consider all the circumstances in which the concurrence was given, and that, subject to that, it was not necessary that the beneficiary should know that what he was concurring in was a breach of trust provided that he fully understood what he was concurring in, and that it was not necessary that the beneficiary himself should have directly benefited from the breach of trust. Accordingly, the trustees were liable to make good (i) the sum of £8,450 advanced to Francis and George for the purchase of the house in the Isle of Man, and (ii) the sum of £6,500 advanced to Anthony, less such sum as should on inquiry be found to be deductible in respect of benefits indirectly received by him. (2) That the plaintiffs' rights were preserved by the proviso to

1 Ch. CHANCERY DIVISION. 315

section 19 (2) of the Limitation Act, 1939. (3) That there being an express statutory provision providing a period of limitation for the plaintiffs' claims, there was no room for the equitable doctrine of laches. Both sides appealed.

W. A. Bagnall Q.C. and S. L. ~Newcom.be for the plaintiffs. In so far as the bank can establish that the sums advanced were paid away in proper exercise of the power of advancement the plaintiffs have no claim. In so far as the bank fails to do so, it is liable to make good to the trust fund. The power of advancement in the settlement is wider than the ordinary power contained in such settlements. Clause 11 contains two limbs; the first is a power to pay whatever is raised to the beneficiary for his or her own absolute use; and the second (the more usual one) " to pay or apply the same for his or her advancement or " otherwise for his or her benefit." I t is a discretionary power and accordingly the trustees must consciously exercise that discretion to see whether in all the circumstances it is right that capital sums should be advanced. See In re Powlcs, deed.2 In re Pilkington's Will Trusts3 does not affect the question as to the width of the power in this case.

The claims here are really four several and independent claims by the four plaintiffs. The basic question is how far the presumption of undue influence which equity presumes a parent to exercise upon children just of age is rebutted by independent advice, or by the child becoming emancipated. The bank purported to exercise the first limb of the power of advancement and never directed its mind to the second limb, i.e., to the aspect of paying or applying the money for the advancement or benefit of the child. In the case of the advances to George and Francis for the purchase of the house in the Isle of Man, the money was never paid to the beneficiaries at all but to their mother at their direction, and the question is whether their consent was real. A further question is whether, when the money leaves the trustees' control, it can be said to have been paid to the beneficiary or for his absolute use, if, when it is paid, he is under the presumed undue influence of his parents. If the trustees can show a really free and uninfluenced direction to

C. A.

1963

PAULINO'S SBTTLBMBNT

TRUSTS, In re.

2 [1954] 1 W.L.B. 336; [1954] All E.E. 516.

3 [1964] A.C. 612; [1962] 3 W.L.B. 1051; [1962] 3 All E.E. 662, H.L.(E.).

316 CHANCERY DIVISION. [ 1 9 6 4 ]

C. A. pay to someone else, that would be a defence. But here not a igg3 penny ever was at the absolute disposal of any of the beneficiaries.

~~ ; Their consents or requests were never freely given. SETTLEMENT Here, the bank acted in three capacities: (1) As trustee.

TRUSTS, (2) As bankers to the mother, to Ann, and to Anthony, and at In T€* ' some time to George also. (3) They were also trustees of the

Hodson settlement which had lent money to the mother. Professional trustees may well owe a higher duty than the ordinary trustee. I t is not alleged that the bank here acted dishonestly or that they ever consciously exercised the power to benefit themselves or the other trust. They tried to do their duty but did not come up to the high standard required of a professional trustee. They were unduly influenced by the fact that the tenant for life was always in desperate straits for money and nearly always overdrawn, and they were looking to her interests at the expense of those of the remaindermen. [Cf. In re Northcliffe's Settlements.*]

In regard to the initial advances for the purchase of the house in the Isle of Man, the advice of Charles Eussell & Co. was unexceptionable, and if it had been followed and correctly understood, none of the trouble would have occurred. The judge correctly summed up the matter with the words " video meliora " proboque deteriora sequor." The solicitors employed to give independent advice misappreciated the problem and thought that what they had to do was to give an independent explanation, but that is not sufficient: see Powell v. Powell.5 In the case of the advances to Ann the bank knew that no consent would protect them unless she were competently independently advised. They knew that advice was being given to her by their own solicitors, but took no steps to see that it was competent. It is not suggested that they could have asked what advice was given,' but independent advice is not there for the protection of the young person, but for that of the person who takes the benefit, because otherwise equity will not allow him to retain the benefit, if in fact the advice is inadequate: see Lancashire Loans Ltd. v. Black.*

All the first group of advances, to Francis and George, occurred in 1948. (i) On the advance of £8,450 for the purchase of the house in the Isle of Man the sons were not separately advised, nor was the transaction carried out as advised by

" [1937] 3 All E.E. 804. « [1934] 1 K.B. 380, C.A. s [1900] 1 Ch. 243, 246. '-

1 C h . CHANCERY DIVISION. 317

counsel. There was no authority from the sons; such authority C. A. as there was, was given for a totally different scheme; namely, ±g&3

for a house to be bought in their names and settled upon their ■— mother for life with remainder to them. The judge rightly held gprTLBUBHT that it was not a proper exercise of the power, (ii) On the TRUSTS, advance of the £2,600, though the sons received a transfer of n re' the life insurance policies and the mother made a codicil to her will in their favour, giving them a legacy equal to the duty on the policy moneys, and though they were separately advised by solicitors, who were also the bank's own solicitors, the advice given was inadequate. The transaction was not carried out as advised and contained no covenant by the mother to keep up the premiums, and the advance was accordingly not a proper one. The transaction as carried out was never consented to by the sons, (iii) On the advances of £1,000 and £2,000 (ostensibly for furniture and for improvements to the house in the Isle of Man, but which were in fact paid direct into the mother's overdrawn account with the bank), the bank owed a duty to see that the money was actually spent on the purposes specified and can only establish a defence if they can show a truly independent request by the sons, and that they cannot do. No consideration was ever given by the bank as to whether it was for the sons' benefit, and no steps were taken to see that the furniture was bought or the improvements carried out.

As to the second group, namely, those advances made to Ann between June, 3, 1949, and August 21, 1950 (i.e., from six weeks after her majority for the next 14 months), £4,789 was advanced for the purchase of a house in London and for repairs and improvements to it, Ann being separately advised. The house was put into Ann's name. No complaint is made as to those advances, but advances of £3,260 ostensibly for furniture for the London house were in fact paid to Ann's account at the bank and thereafter at once transferred to the mother's account, Ann's account being a mere conduit pipe, and as to these advances, Ann was never independently advised. Such advice as she had was directed to the wrong question, namely, as to the merits of the house as an investment for money already in Ann's hands; it ought to have been directed to the question whether she wanted money taken out of settlement at all.

In regard to Ann: (1) the bank never took any steps to see that the money advanced, ostensibly for the purchase of furniture, was in fact spent on furniture. (2) The bank never exercised any discretion as to these advances, amounting to £3,260, and

1 C H . 1964. 22

318 CHANCERY DIVISION. [ 1 9 6 4 ]

C. A. took no steps to see that the amount advanced bore any relation' s ship to the quantity of furniture purchased. (3) If the advances

—~ ; were to be for Ann's absolute use, then in no real sense could SETTLEMENT ^ be said that she ever obtained the absolute use of it—its

TRUSTS, destination was already fixed before it was advanced to her. ' (4) The bank in her case cannot rely on any request or consent

by her, since the advances were made within the first year of her attaining her majority, whilst she was still under the presumed influence of her parents. (5) Ann received no separate advice in connection with the advances for the purchase of furniture; the advice which she received in respect of the house in London was not adequate even for that purpose, far less was it adequate to cover the advances for the purchase of furniture. (6) There was no evidence on which the judge could hold that Ann was completely emancipated at the time. Such evidence as there was, was all the other way. The knowledge of the financial pressure to which the family was subject was such as to prevent the children becoming freed from undue influence. In Allcard v. Skinner,7 it is said that where there is a presumption of undue influence the court will set aside a voluntary gift unless it is proved that in fact the gift was the spontaneous act of the donor, acting under circumstances which enable the donor to exercise an independent will. I t is conceded that £300 was in fact spent upon furniture and that Ann's claim should accordingly be reduced by that amount.

As to the third group of advances, i.e., those to Anthony between July 11, 1951, and February 17, 1952 (i.e., from a month after his 21st birthday for the next seven months), though some attempt was made at giving independent advice, it was very perfunctory and inadequate, and the judge rightly so held. He ought not, however, to have ordered an inquiry as to how much benefit Anthony had received indirectly from the advances that were at first paid into his mother's account, but from which account he received certain subventions. The judge sought to base his judgment on this matter on Raby v. Ridehalgh* and Chillingworth v. Chambers," but those cases do not support the principle he sought to deduce. They were cases where the beneficiaries had clearly instigated the breach. There is no legal principle on which Anthony should be made to account.

As to the fourth group, namely, those advances made to

' (1887) 36 Ch.D. 145, 171. » [1896] 1 Ch. 685; 12 T.L.E. « (1855) 7 De G-.M. & G. 104. 217.

1 C h . ■ CHANCERY DIVISION. ■319

George, Francis and Ann between September 25, 1953, and June 17, 1954, £5,350 was paid directly into the mother ' s account. Though authority was obtained from the various beneficiaries, the process had become a routine. The real question in issue, namely, whether the child really wished to have the money taken out of sett lement, was never raised at all. The advice given was wholly inadequate. Where there is an atmosphere of perpetual financial strain it is impossible to say that emancipation was effective.

The question of the extent and duration of undue influence is admittedly one of fact and degree. I t is partly a mat ter of fact and partly of inference. The judge found that the children were then " fully informed " of the circumstances and that knowledge was the determining factor, but tha t does not mean tha t they were emancipated. The judge was wrong in thinking that if one child was emancipated the others were too; even if George had knowledge of the facts in 1953 there is no evidence that the others had. If the children are of such an age that the law presumes undue influence to exist, the trustees mus t show not merely that the children acted on advice, but also tha t that advice was proper. For example, though the two eldest boys consented de facto to the Hodson loan transaction, their consent cannot be relied on by the bank because the presumption of undue influence still applied, and though they received independent legal advice such advice was inadequate. The transaction as completed was not the one proposed, but even as proposed it was not for their benefit. The presumption of undue influence certainly continues until shortly after the child has attained majority. Indeed, if the child is living in association with his or her parents, 10 years is not too long a period for its continuance. I t is put t ing it too high to say that marriage automatically breaks the parental connection; nor does leaving the parental home automatically do so : see Lancashire Loans Ltd. v . Black.10

The power of advancement is fiduciary and the trustees m u s t exercise their discretion whether the advance would be for the benefit of the person to be advanced. The interests of the other beneficiaries under the set t lement mus t also be considered. The exercise of the power for the benefit of the mother was clearly a wrong exercise of the power: see In re Moxon's Will Trusts11

and In re Pilkington's Will Trusts.12 The trustees must exercise

C. A.

1963

PAULINO'S SETTLEMENT

TRUSTS, In re.

1° [1934] 1 K.B. 380, C.A. " [1958] 1 W.L.B. 165; [1958]

All E.B. 386.

12 [1964] A.C. 612; [1962] 3 -W.L.B. 1051; [1962] 3 All E.B. 622, H.Ii.(E.).

320 CHANCERY DIVISION. [1964]

C- A. their discretion in the light of all the relevant circumstances 1963 "ght UP to the moment of actual loss of control of the money

~~ ; advanced. Here everybody knew that the money was going to SETTLEMENT ^n e mother, and there would have been nothing wrong in that,

TRUSTS, provided that the person advanced could have been shown to have ' had absolute use of the money. Where the presumption of

undue influence remains, the provision of independent advice is the only way in which the presumption can be removed. The money must be unfettered in the hands of the beneficiary, or there can be no real consent. There must be a spontaneous act of will by the child: see Billage v. Southee 13 and Bainbngge v. Browne.u The bank, as trustee, is in no better position than that of a volunteer and in any case it had notice.

Independent advice, to be adequate, must not merely explain the position to the intending donor, it must also express a view as to the propriety of the transaction. In all these advances each child's case must be considered separately: there is a vast distinction between Francis's case and the others in view of his mental condition. A trustee's duty is to find out those matters relevant to the exercise of the power, and a person's mental state is one of those matters.

In summary the following propositions of law are advanced: (1) Every advance was made under the first limb of the power, i.e., to pay to the beneficiary for his or her absolute use. The other limb was never considered by the bank. (2) This was a fiduciary power requiring a conscious exercise of discretion by the bank. (3) If a payment is made to a third party at the request or with the consent of the beneficiary, that request or consent must amount to a really voluntary disposition of that which has become the beneficiary's own property. (4) Where the relationship of parent and child exists, so that undue influence is presumed, the bank trustee must show either complete emancipation from control generally, or that independent advice was given to the beneficiary, having full knowledge of his right and of the facts. The presumption of undue influence certainly extends for a short period after the child attains majority— marriage, of itself, does not necessarily amount to emancipation. (5) The last two submissions (3) and (4) apply equally where a payment is made to a beneficiary, the trustee knowing full well that the beneficiary intends at once to transfer the money to

is (1852) 9 Hare 534; 21 L.J.Ch. 472.-

" (1881) 18 Ch.D. 188.

1 Ch. CHANCERY DIVISION. 321

his or her parents. The parents in such a case must show a c- A-real voluntary disposition. (6) The independent advice which is 1953 given must be given by an adviser who has full knowledge of all ;— the relevant circumstances, and it must be such as a competent SETTLEMENT and honest adviser would give if acting solely in the interests of TRUSTS, the beneficiary. It must be advice, mere explanation or informa- ' tion is inadequate. See Inche Noriah v. Shaik Allie Bin Omar.1* In Powell v. Powell16 Farwell J. went so far as to say that no protection was afforded by independent advice unless it was acted upon. Some course of conduct must be advised. If the trustees know that independent advice has been given advising against a transaction, then they ought not to carry out the transaction. (7) Looking at the question from the beneficiary's point of view, the person who seeks to rely on such a voluntary gift must show that it is the spontaneous act of the donor, in circumstances which enable him to exercise an independent will: see per Cotton L.J. in Allcard v. Skinner" and also Huguenin v. Baseley.1*

The question must be decided by an objective test, looking at the facts in each case. The judge looked at each advance to decide whether or not it was a breach of trust and then went on to consider whether the beneficiary had precluded himself from complaining. I t is submitted that the only question is whether the consent was a real one.

Though there are similarities between the exercise of a power of advancement and a power of appointment, the principles governing the exercise of the latter do not really apply here. The judge overlooked the vital question of who was complaining.

[UPJOHN L.J. I regard this analogy to powers of appointment as dangerous and misleading.]

[Eeference was also made to Reade v. Beade " ; Dyer v. Dyer20; Vatcher v. Paull21; Molyneux v. Fletcher22; McMackin v. Hibernian Bank23; In re Salting, Baillie Hamilton v. Morgan2*; Wright v. Carter.25]

Sir Milner Holland Q.C. and B. Cohens-Hardy Home for the bank. Each case of advancement raises different questions

" [1929] A.C. 127; 45 T.L.E. 1, P.C.

" [1900] 1 Ch. 243, 246. " (1887) 36 Ch.D. 145, 171. « (1807) 14 Ves. 273. 19 (1889) 9 Ir.L.R. 409. *« [1903] 1 Ch. 27; 19 T.L.E. 29, 20 (1788) 2 Cox Eq.Caa. 92. C.A.

21 [1915] A.C. 372, P.C. 22 [1898] 1 Q.B. 648; 14 T.L.E.

211. 23 [1905] 1 I.E. 296. 24, [1932] 2 Ch. 57.

322 CHANCERY DIVISION. [1964]

C- A- because of the differing ages' and character of the children, the 1963 surrounding circumstances and the interventions of solicitors, all

~~ ; of which affect the position of the bank as trustees. I t is not a SBTTLBMBNT c a s e °f undue influence or nothing. Clause 11 of the settlement

TBTOT8, contains a dichotomy: there are two limbs to it. The first is ___' much wider than the second and under it the beneficiary can

go to the trustee and ask for an advance for a particular purpose. The power is admittedly fiduciary, but under the first limb there is no duty upon the trustee to see that the advance is for the benefit of the person to be advanced. Under the second.limb the trustee must see that the object is carried out. The plea that the children did not consent when money was paid for the benefit of other beneficiaries and was thus misapplied, has been withdrawn.

In the case of the Hodson loan transaction the bank thought that Francis and George should be separately advised. So long as the transaction, as actually carried out, was approved by independent solicitors acting for them that is sufficient to absolve the bank from any liability. The two boys agreed to what was proposed. If the solicitors did not carry out the transaction as instructed, that did not render the bank as trustees, liable. There was no need for the bank to check to see that the money was properly applied. The bank would probably be liable only if they actually knew that the money was. being paid out for another purpose. I t is not suggested that the bank was instigated to commit breaches of trust. It was, however, conceded before Wilberforce J. that the children had consented to things they knew to be breaches of trust. The children were anxious that their parents should receive bounty.

[UPJOHN L.J. You cannot give trust money away to charity at the expense of the beneficiaries.]

The plaintiffs appear to think that no breach of trust can be cured, but that is not so. In the pleadings it is alleged that the plaintiffs were unemancipated from parental control, but no allegation is made that the bank knew or ought to have known that that was so. No one told the bank that there was anything wrong with Francis's mental capacity or suggested that he could not understand what was going on. Nor is there any plea of undue influence, other than that which the law presumes. .

The law as stated in Underhill on Trusts, 10th ed., p. ,581, is that if a beneficiary has assented to or concurred in a breach of trust or has acquiesced in it, he cannot afterwards charge the

1 C h . CHANCERY DIVISION. 323

trustees with the breach; provided (1) that he was sui juris at c- A-the time, (2) that with full knowledge of the facts and of what 1963 he was doing and its legal effect he has retained the benefit of ;

"PAITT ran A

the breach, and (3) that no actual undue influence was brought SETTLEMENT to bear upon him. Crichton v. Crichton26 does not support the TRUSTS, contention for which it was there cited. '

The questions that arise are: (a) What is the legal presumption and does it apply here? (b) If it applies, is it displaced? (c) If, contrary to the judge's finding, it is not displaced, what is the position of a trustee who acts upon the authority or consent of an adult beneficiary? :

If the bank did not know that consent was obtained by undue influence they would not be liable. Perhaps the best and most accurate statement of the law as to the presumption of undue influence;is to be found in White and Tudor on Equity, 8th ed., p. 237. The court must be sure that the child was able to form an independent judgment free from influence: see Lancashire Loans Ltd. v. Black27; Smith v. Kay2S; Archer v. Hudson2*.; In re Coombes.30 These cases show that the presumption only applies when the child is just over 21 and is living at home.

The. view expressed by Farwell J. in Powell, v. Powell31 as to the nature of the advice to be given is disposed of by Inche Noriah v. Shaik Allie Bin Omar,32 where the Privy Council held that independent legal advice was not the only way in which the presumption can be rebutted, nor were they prepared to hold that independent advice was ineffective unless the advice was taken. It is sufficient if a full and independent explanation of the nature of the act is given. The court has to decide whether there has been a free exercise of an independent will and whether the explanation given was a proper one. Here in fact the plaintiffs had the position fully explained to them. The fact that Ann said that had she known that it was her money she was dealing with she would never have agreed, is evidence that she was not under the domination of her father at all. In Ann's case it is conceded that the presumption applies, but it has been displaced. She was a woman of full age who knew that if she said certain things, the bank would pay out money;, she cannot now be allowed to recover that money by. coming to a court of

=» [1896] l C h . «Y0, C.A. ■»» [1911] 1 Ch. 723, C.A. « [1934] 1 K.B. 380, C.A. « [1900] 1 Ch. 243. " (1859) 7 H.L.Cas. 750. " [1929] A.C. 127; 45 T.L.E. 1. =» (1844) 7 Beav. 551. ■

324 CHANCERY DIVISION. [1964]

C. A. equity and saying that what she told the bank was quite untrue 1963 an(* *kat *^e D a n k ought not to have believed her.

I n considering the application of the presumption to the par-SMTLBMBNT ti°u'ar facts of each case the following conclusions can be drawn.

In re. As to the first advances to George and Francis, Francis was one ' month short of 27 when the first advance was made, he was not

living at home but with his grandmother, and was attending Edinburgh University. I t is not sufficient for him to say the presumption applies. Admittedly for a t ime it is for the father to disprove undue influence, but thereafter it is for the son to allege and prove it affirmatively. If it is to be at tempted to prove actual undue influence the bank would be seriously prejudiced. As pleaded, the plaintiffs' case alleges no actual undue influence by the father or mother, and the presumption alone is relied upon. Where a person is mentally weak, there is no presumption of undue influence by the person with whom he lives, though actual undue influence may not be hard to prove. I t is agreed that Francis suffered from a nervous breakdown before the events complained of. There is no presumption in his case, and in any case Wilberforce J . found that he was quite capable of understanding business mat ters . A trustee can rely on the consent of an adult beneficiary unless he knew or ought to have known that the consent was vitiated in some way. No actual undue influence was pleaded in his case.

In September, 1948, when the first advances were made, George was one month short of 23, and shortly after in January, 1949, he took a job in Liverpool. H e was living independently of his parents and the presumption does not apply. I n Ann's case, when the first group of advances to her were made she was living at home and it is conceded tha t since she had only just attained 21 and was living at home the presumption applies. The advances to Anthony were made when he was a regular soldier serving with his regiment in Germany, and though no doubt he spent his leaves at home it is extremely doubtful whether the presumption would apply to him. H e too was living independently of his parents. There is no finding that he was subject to undue influence when the final batch of advances to Francis, George and Ann were made. George was working for the Solicitor to the Inland EevenUe and was then about 28, Francis was at home, but was by then 33, and Ann was over 25, was married and was no longer living at home, so that in such a complete : change of circumstances the law would certainly not presume undue influence and no actual influence was alleged.

1 Ch. CHANCERY DIVISION. 325,

In re.

It is not true to say that only independent advice suffices c- A-to displace the presumption. The question for the court is: Did X963 the person express a free and independent will or was his will ;— dominated? The onus can be discharged without showing that SETTLEMENT the person had independent advice: see Allcard v. Skinner,33 TRUSTS, per Cotton L.J. I t is possible for advice to be given, but yet for the influence not to be removed. The task of the solicitor giving advice is not actually to advise a specific course of action; it is sufficient if he sees that the donor understands what he is doing and intends to do it; he need not advise him to do it or not to do it: see In re Coombes.3*

The judge set himself the right questions, namely: What was the nature and quality of the consent given? Was it given freely? Was the child freed from parental influence? Was separate independent advice required? If so, was it given, and was it adequate to impart to any consent given the necessary quality of freedom? There is no duty to inquire into the beneficiary's psychology or state of mind before making an advance.

Cozens-Hardy Home following. Unless the plaintiffs' right of action is preserved by the proviso to section 19 of the Limitation Act, 1939, section 19 (2) must apply to all the advances to the plaintiffs and bars their claims except for the fourth group of advances. See also section 8 of the Trustee Act, 1888, and section 29 of the Limitation Act, 1939. A future interest falls into possession when the trust interest under which it arises falls into possession, i.e., when it is paid to, or according to the direction of, the person beneficially interested. See Fry v. Inland Revenue Commissioners.35 There is no difference between an interest in expectancy under the Finance Act, 1894, and a future interest under section 19 of the Limitation Act, 1939.

[HARMAN L.J. You are saying that by committing a breach of trust the trustees caused the interests to fall into possession?]

The interests here fell into possession because they coalesced. Everything was done with the consent of the persons interested.

[UPJOHN L.J. When an advancement is made a sum is taken out of settlement, but there is no coalescing of the interests at all. ]

Even if the Limitation Act does not apply that does not preclude the doctrine of laches from applying, as a valid defence.

« (1887) 36 Ch.D. 145. 35 [1959] ch. 86; [1958] 3 3* [19111 1 Ch. 723, C.A. W.L.B. 381; [1958] 3 All E.R. 90,

C.A.

326 CHANCERY DIVISION. [1964]

C. A. The plaintiffs' inaction lulled the bank into a state of inactivity X963 whereby they were losing their right to impound the income, and

; — therefore the longer the delay the greater the loss. As to laches SETTLEMENT ^e following propositions are. advanced: (1) Laches involves

TRUSTS, delay, and acquiescence by the plaintiffs, or a change of position ' by either party such that it would render it inequitable for the

plaintiffs to succeed. (2) A plaintiff is treated as having acquiesced when a violation of his rights of which he did not know is brought to his notice, and he still takes no action. (If a plaintiff knows the facts he is presumed to know his rights.) (3) Acquiescence will readily be inferred if the plaintiff benefits by keeping quiet. A benefit to the plaintiff coupled with delay is sufficient to constitute laches, even if there is no actual acquiescence. (4) Apart from acquiescence the defence of laches will readily be applied where the defendant's position has changed as a result of the delay in such a way as to prejudice him, as might be the case here in that (i) the longer the delay the greater the difficulty of getting rebutting evidence, and (ii) the delay may result in financial loss in that the defendants lose the right to impound the income of the beneficiary during the period of delay. (5) Where the plaintiff's claim is based on undue influence, the plaintiff must take steps immediately the influence ceases for the claim to lie. See Turner v. Collins,38 per Lord Hatherley. [Smith v. Kay37 and Erlanger v. New Sombrero Phosphate Company 3S were also referred to.]

In this case the plaintiffs knew their rights under the settle^ ment in 1952 and the writ was not issued until 1958. It is immaterial that they did not know that the advances had been in breach of trust: see Allcard v. Skinner39 and Stafford v. Stafford.*0

In applying the doctrine of laches to the present case the court ought also to pay attention to certain considerations very material to this case, viz.: (1) The plaintiffs were relying on the presumption rather than on actual undue influence, which meant.that it was more difficult to produce evidence in 1961 as to what happened in 1948. (2) The court ought to be particularly suspicious of allegations of undue influence made long after the influence ceased, when the donor sues.the trustee without joining the donee as a party.

When George gave his consent to the purchase of Oakhill,

se (1871) 7 Ch.App. 329. »» (1887) 36 Ch.D. 145. , : " (1859) 7 H.L.Cas. 750. « (1857) 1 De &. A J. 193 . »» (1878) 3 App.Cas. 1218, H.D. ,

1 C h . CHANCERY DIVISION. 327

he knew the financial advantages to the family of buying a house c- A-in the Isle of Man; he knew what was happening and acquiesced 1963 in it.. , The judge found that he was emancipated. On his own ~ evidence when he signed the consent to the advance of £2,000 SEMEMES he understood what was happening. Prom 1950 onwards, when TRUSTS,

Ifl T6.

he started reading for the bar, he understood that the capital ■ ■ ■ ' belonged to him, the reason why he did not institute proceedings earlier was that he thought the defendants had protected themselves by the provision of separate advice, it is submitted that he was aware that he might have rights to complain and that he decided not to act upon them. Once the plaintiffs stood by and allowed further advances without objection that was clearly acquiescence: see Stafford v. Stafford.*0 As to the purchase of Oakhill, the bank had directions from Francis and George to pay the money to whomsoever the mother directed, and she directed them to pay it to Kneale & Co., whom the bank wrongly assumed to be acting as solicitors for Francis and George. [Williams v. Johnson41 and Clarke v. Edinburgh and District. Tramways Co.42 were also referred to.]

Bagnall Q.C: in reply. The trustees must consider the interests of all the beneficiaries; the exercise of the power must not be capricious. So far as the second limb of the power in clause 11 is concerned there must be a specific purpose, so far as the- first limb is concerned, even though the money is advanced to the beneficiary absolutely, it must be for his benefit. I t is not right for the trustee to leave the application of the funds to a third person, but money can be rightly left in the hands of a third person if that third person is carrying out the purpose for which the money is to be advanced. Sir Milner Holland adopts a wrong approach in treating the matter as if it were one between a tenant for life and a remainderman, whereas it is purely as a result of the exercise of the power that the beneficiaries here were entitled to anything at all.

The Hodson loan transaction could not possibly have been a proper exercise of the power: the fact that the beneficiaries got something in return so that it was not quite so improper as it might have been is neither here nor there. George and Francis must, it is clear, give credit for something. It might be strictly correct to treat the loss to the trust fund as £2,600 less the surrender value of the policies as at August 18, 1948, the date

" 1 Deft. & J. 193. «. 1919 S.C.(H.L.) 35; 56 Sc.L.E. 41 [1937] 4 All E.B. 34, P.C. 303.

328 CHANCERY DIVISION. [1964]

C. A. when they were assigned to the sons, but it is submitted that they ought not to be in a worse position than if they had sold the policies at the date they in fact gave them away, namely,

PAULINO'S March 18, 1953. It cannot be said that they have no claim at all TBUSTS simply because they got something which in certain circumstances In re. might have produced the required value.

As to the question of relief under section 61, four conditions must be satisfied: (i) the trustees must have acted honestly; (ii) they must have acted reasonably; (iii) the facts must be such that they ought fairly to be excused; and (iv) such that the court in its discretion ought to relieve them. There has been no case where a professional trustee had been granted relief.

[WILLMER L.J. If the trustees acted honestly and reasonably, what other test is there that should be applied in considering whether they ought fairly to be excused?]

The sort of case where trustees might be relieved is if a proposal to use capital, held in trust for a child, in payment of a parent's debts, is acceded to by trustees on condition that the parent provided a policy on his life with a covenant to keep up the premiums and to replace the capital at his death, and the parent falls upon evil days and his other income failing through wholly extraneous circumstances the parent is unable to keep up the policies so that they lapse. In such a case the trustees might well be excused, but here the scheme was wholly improper! Belief under the section is discretionary. The fact that reliance was placed on a solicitor is no defence. Maybe if the act were a ministerial one, reliance on a solicitor might afford some defence, but here the trustees virtually delegated their discretion to the solicitors. Section 61 of the Trustee Act, 1925, merely enables relief to be granted where nothing is wrong save that the court's direction has not been sought. It is almost a matter of principle that relief under section 61 is not open to professional trustees: see National Trustees Company of Australasia Ltd. v. General Finance Company of Australasia Ltd.,4,3 which was followed and applied in In re Windsor Steam Coal Company Ltd.** The circumstances must be wholly extraordinary before the court will intervene to relieve a professional trustee.

As to the advance to Francis and George of £1,000 for the purchase of furniture, the bank ought at least to have paid the sum into a separate account in their joint names, and not into the

« [1905] A.C. 373; 21 T.L.B. « [1929] 1 Ch. 151, C.A. 522, P.C.

1 C h . CHANCERY DIVISION. 329

overdrawn account. The bank never exercised any discretion C. A. as trustees as to the amount of the advance, and they never exer- 1953 cised any control over how it was spent. As to the advance of ; — £2,000 to Francis and George, the bank are at least in no better SETTLEMENT position than that of volunteers; they clearly had knowledge of TBUSTS, the facts. '

The presumption of undue influence is not one of law, but of facts assumed by the law to exist. I n the case of a child shortly after attaining majority it is presumed to exist unless the contrary is proved: see Shephard v. Cartwright.45 Those who say tha t no influence exists mus t show tha t the presumption has ceased to apply. If there is any ground for suspicion the trustees should always refuse to act. This is "illustrated by the cases dealing with fraud on a power: see King v . King46 and Lloyd v . Attwood*7 and Halsbury 's Laws of England, 3rd ed., Vol. 30, pp. 276, 27T.

Emancipation is an abstract conception and is a question part ly of law and partly of inference from facts. The correspondence in this case provides as good a guide as seeing the children in the witness box 10 years after the events in question. No exception is taken to the judge's findings of fact except in regard to Francis 's state of mind and the inferences which the judge drew from the facts. This court is in just as good a position as was the trial court to draw inferences: see Powell v. Streatham Nursing Home, per Lord Sankey L.C.4 8 The judge drew the wrong inferences in this case, and his findings on Francis were contradictory; there was no evidence on which the judge could have held that Francis knew all about the transactions. The knowledge imputed to George bore no relation to the realities of the case. There is very little in the judge's judgment to show tha t he considered the question of emancipation as distinct from that of knowledge. H e did not refer to the well-known passages on the subject: see Wright v . Vanderplank.4* The judge wrongly regarded intelligence plus knowledge as amounting to emancipation, and appears to have thought that for undue influence there had to be something equivalent to overbearing conduct. Normally at 28 Francis would have been emancipated. I t was not a trustee 's duty to find out about his mental state, bu t it was in

*s [1955] A.C. 431; [1954] 3 «» [1935] A.C. 243; 51 T.L.K. W.L.E. 967; [1954] 3 All E.E. 649, 289, H.L.(E.). H.L. 49 (1856) 8 De G.M. & G. 133,

« (1857) 1 De G. & J. 663. affirming (1855) 2 K. & J. 11. " (1859) 3 De G. & J. 614.

330 CHANCERY DIVISION. [1964]

C. A. their interest so to do, since if they failed any advances which i g 6 3 they made would be at their peril : see Shephard v . Cartwright.50

As to Ann, but for family loyalty she would have had nothing to SETTLEMENT ^0 w ^ * n e scheme of advances. The judge makes no finding

TRUSTS, tha t she was emancipated but merely that she had received " adequate advice. Ann is asking the bank to restore the money

they applied improperly—which they were paid to apply properly. As to the last group of advances, the only argument tha t can be put forward is that they were still following the pattern set by the earlier transactions in 1948.

Gozens-Hardy Home in reply. Beneficiaries who are of full age are entitled to ask trustees for assistance, and in those circumstances the trustees are freed from responsibility if the beneficiaries give their consent: see Phillipson v . Gatty 61 and also section 61 of the Trustee Act, 1925.

As regards the Hodson loan transaction the trustees knew that separate advice was being given and if that was so there was no need for them to ask what such advice was. As to Ann, there was no reason to suppose that she was not telling the truth over the transactions in connection with her house. There was no reason to know of the mental condition of Francis. As to Anthony, though the money was paid into his mother ' s account, much of it came back into his own account when he drew cheques in view of the arrangement made by his mother.

Cur. adv. vult.

May 29, 1963. WILLMEK L . J . The judgment which I am about to read is the judgment of the court, which deals with and resolves all the points which have been argued except one, and in relation to that one there is, unhappily, a disagreement between the members of the court, and on that one point we will deliver separate judgments when I have read the judgment of the court.

This is indeed a sorry story, and one which reflects no credit at all on any of the parties to it. When Miss Pauling, the plaintiffs' mother (and we shall refer to her throughout as " the " mother ") married their father (to whom we shall refer as " the commander ") she was a young lady of considerable fortune. She was marrying a naval officer who had almost no fortune at all, and by the wisdom, no doubt, of her parents, it was decided

5 0 [1955] A.C. 431; [1954] 3 5 1 (1850) H. & Tw. 459, on appeal W.L.E. 967; [1954] 3 All B.E. 649, from (1848) 7 Hare 516. H.L.

1 C h . CHANCERY DIVISION. 331

to vest her fortune in trustees on the trusts of a marriage settlement. The whole object of this transaction was to prevent the use (or rather misuse) of the lady's capital for the very purposes for which in fact it has been very largely frittered away, that is, in the ordinary living expenses of the family. Apart from a power to raise £10,000 out of the settlement (which had been exercised long before the history of this action starts) it was intended that the mother should have nothing more than the income during her life, and she was restrained from anticipating that.

In June, 1948, the trust funds were intact, and amounted to over £70,000. By June, 1954, the bank (the trustees of the settlement) had raised and paid away over £29,000 from the capital of these funds in purported exercise of a power of advancement, and there was nothing whatever left to show for it. How had this melancholy event happened? It was in part due to a misunderstanding of a power of advancement contained in the settlement, which was in rather unusual form, and later on to its plain misuse, but also was largely due to the charm of manner and powers of persuasion of the commander. The trial judge has found the bank liable to replace nearly £15,000 as having been expended in breach of trust for which they can be compelled to account. Both parties appeal.

The relevant transactions over this period of six years are many, and involve each of the four children of the marriage. Different questions arise in respect of most of these transactions, and accordingly we propose in this judgment first to set out the basic facts, then to state our view of the legal questions that have been argued before us, and finally to deal seriatim with the facts of each advance and to apply the law accordingly.

The plaintiffs, the children of the commander and the mother, are: (1) a son, Francis, born on October 15, 1920; (2) a son, George, born on October 11, 1925; (3) a daughter, Ann (now Mrs. Broadbent), born on March 24, 1928; (4) a son, Anthony, bom on June 15, 1930. As already stated, the marriage settlement was of funds supplied entirely by the mother. The defendants, Coutts & Co. (to whom we shall refer as " the bank "), have all along been the sole trustees. Apart from the special power to raise £10,000 for the mother's use which we have already mentioned, the settlement followed the usual lines of such an instrument. The mother had the income of the trust fund for life without power of anticipation and after her death her husband was to have an annuity of £500 a year. Provision was also made

C. A. 1963

PAULINO'S SETTLEMENT

TRUSTS, In re.

332 CHANCERY DIVISION. [1964] C. A.

1963

PAULINO'S SETTLEMENT

TRUSTS, In re.

for the mother to have power to appoint a life interest in half of the trust fund to any surviving husband. Subject thereto, the trust fund was to be held in trust for the children or remoter issue of the mother, whether by the intended or any future marriage, in such shares as the mother might appoint, and in default of appointment the children were to take in equal shares on attaining the age of 21, or being female marrying under that age. Clause 11 of the settlement, under which the bank purported to act in making the advances complained of, provided as follows: " It shall be lawful for the trustees at any time or times " after the death of the wife or in her lifetime with her consent " in writing to raise any part or parts not exceeding in the whole " one-half of the then expectant or presumptive or vested share " of any child or more remote issue of the wife in the said trust " premises under the trusts hereinbefore contained and to pay

the same to him or her for his or her own absolute use or to pay " or apply the same for his or her advancement or otherwise for " his or her benefit in such manner as the trustees shall think fit " . . . " By clause 14 power was conferred on the trustees during the life of the mother, and with her consent in writing, to lay out a sum not exceeding £10,000 in the purchase of a house as a residence for the wife, and in its decoration, repair or improvement, provided that such house was situated in England, Wales, Scotland or Ireland. Lastly, provision was made for the bank to act as bankers in respect of the trust funds without being liable to account for profits, and to be remunerated for their services in accordance with their published scale of fees. Charles Eussell & Co. were nominated as solicitors to the trust with permission to the bank to consult its own solicitors in any case in which it should think fit. These were Farrer & Co. It should at this stage be stated that at all material times the mother had an account with the bank. The commander did not have any separate bank account with the bank, but he was authorised to draw on the mother's account, and it appears that it was he who largely controlled it. During most of the time with which we are concerned this account was substantially overdrawn.