cgiar indirect cost allocation...

TRANSCRIPT

CGIAR INDIRECT COST ALLOCATION GUIDELINES

FINANCIAL GUIDELINES SERIES, NO. 5

August 2001

Consultative Group on International Agricultural Research (CGIAR)

40592P

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

ed

Financial Guidelines Series

No.1 CGIAR Financial Management (Revised 1999) No.2 CGIAR Accounting Policies and Reporting Practices Manual (Revised 1999)

No. 3 CGIAR Auditing Guidelines Manual (Revised 1995) No. 4 CGIAR Resource Allocation: Developing and Financing the CGIAR

Research Agenda (Revised 1998) No. 5 CGIAR Indirect Cost Allocation Guidelines (August 2001) No. 6 CGIAR Procurement of Goods, Works and Services (August 2001)

These policy guidelines have been prepared by the CGIAR Secretariat to assist the International Agricultural Research Centers supported by the Consultative Group on International Agricultural Research. Each IARC is encouraged to draw up its own policies and procedures manuals for its internal use. Questions or suggestions about these guidelines should be sent to:

CGIAR Secretariat

(Attn: Shey Tata, Senior Financial Officer)

1818 H. Street, N.W.

Washington, D.C. 20433, USA

This guideline was prepared by Ernst & Young – India, under the leadership of Mr. Anjani Agarwal, Partner. Mr. Kwame Akufo-Akoto (ICRISAT) managed the project for the CGIAR.

273 Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

3

INDEX

Section Description Page No.

SECTION 1 Objectives, Scope, Evolution and Implementation 1

SECTION 2 Cost Allocation Framework

Exhibit 1: Cost Pool Structure

Exhibit 2: Il lustrative Indirect Cost Ratios based on 1999 Financial

Data

3

SECTION 3 Definitions and Principles

Exhibit 3: Overview of classification

Description of Functional Groups

Exhibit 4: Functional Groups and their treatment

Mapping resource user units to Functional Groups

Exhibit 5: Indicative List of Operating Expenses and Resource User

Units

Resource Cost Drivers

Exhibit 6: List of Resource Drivers

Exhibit 6.1: Depreciation

7

SECTION 4 Implementing the Methodology

Exhibit 7: Developmental Phase

Exhibit 8: Application Phase

Exhibit 9: Cost Pool Sheet

Exhibit 10: Expense Matrix Summary

Exhibit 11: Grouping Matrix

Reporting on Direct and Indirect Cost

Exhibit 12: Statement of Operating Expenses (Center level

consolidation)

Exhibit 13: Statement of Operating Expenses (Location wise summary)

16

Exhibit 14: Risk Management 21

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

1

SECTION 1 OBJECTIVES, SCOPE, EVOLUTION & IMPLEMENTATION

1. Objective :

CGIAR has adopted a policy of full cost recovery in financing the centers research programs/activities through grants restricted to specific activities or projects. The intention of the policy is to ensure that all donors to centers pay their fair share of the indirect costs. This manual provides principles and procedures for defining and computing indirect costs. Their application should ensure transparency, consistency and comparability of indirect costs for all CGIAR centers. By establishing these procedures, centers and donors of restricted grants can have a common understanding of the resulting rates of indirect cost recovery built in the project proposals.

The Manual describes the cost pooling and value chain framework to be used for developing indirect cost ratios. The concepts, principles and methodology embodied in this manual aim at establishing harmonious practices among CG Centers in attributing an operating expense as direct or indirect and developing a model of uniform reporting system on cost ratios.

The purpose of the manual is not to define a common indirect cost recovery rate for all centers or for that matter a fixed rate over time for an individual center. Actual ratios of indirect cost to direct cost by applying this methodology will vary across the centers due to differences, for example, in their cost structure, location, size of infrastructure, area of operation and business methods. Furthermore, rates will vary over time even at an individual center due to changes, for example, in host country environment, changes in research agenda and organization structure.

2. Scope :

The manual applies to all CGIAR Centers. Its scope covers all operating expenses [i.e. capital items excluded] that form part of the Statement of Activities and are relevant in establishing indirect costs.

The Manual

* provides a standard set of cost management principles and operating guidelines for pooling of costs and classifying them into direct and indirect categories on a logical and credible basis, to be followed uniformly by all CGIAR Centers for reporting of direct and indirect costs.

* includes procedures for collection, classification, allocation/apportionment and pooling of operating expenses to the resource user units, grouping of resource user units under certain functional categories of costs as well as treatment thereof as direct or indirect.

* covers principles for recording and pooling costs that are intra- center but inter locations (i.e. locations outside of Headquarters).

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

2

The methodology is defined in terms that allow individual centers to maintain their own nomenclature for expense account heads and cost centers (or resource user units) and tailor the methodology to suit their individual circumstances.

The Manual does not address modalities for recovery of pooled costs and inter center transfer pricing issues. It also does not provide normative ranges of indirect cost ratios for CGIAR. Detailed methods for applying specific cost drivers to expenses pooled under resource user units for final computation of individual project cost are not covered in this manual.

3. Evolution :

The preparation of this manual follows extensive discussions among finance practitioners in the CGIAR based on the following analytical work done by Ernst and Young, India.

* Cost studies in context of harmonizing the various cost accounting methods followed by the CGIAR Centers,

* Development of a costing framework for attributing and assigning expenses to research projects in the creation, support & delivery of value,

* On-site pilot studies at five centers for application of the suggested system and testing of the results, on-site test application of methodology at one center and off-site review of such exercises carried out at rest of the centers

The results of these activities have been reviewed by center management. They were also presented to the CGIAR Finance Committee who have endorsed the adoption of the methodology.

4. Application and Implementation:

Beginning 2001, a one page summary of the computation of indirect cost based on current year data should be included in the audited financial statements.

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

3

SECTION 2 COST ALLOCATION FRAMEWORK

Purpose:

The underlying objective of accounting practices is that each research project, independent of funding sources, should bear a fair share of indirect costs as well as directly identifiable costs to determine the total research cost of the project. Appropriate classification of costs, pooling them under resource users and grouping the resource users on homogeneous functions for creation and delivery of value, is an approach towards that end.

Principles:

* Under the GAAP accounting frame-work expenses are reported by functional as well as natural classification. The functional classifications describe the major classes of program services and supporting activities of the organization. Natural classification describes the major classes (line items) of expenditures, for example, personnel costs, travel. Hence, the methodology described in the Manual is subsidiary to the accounting system framework.

* The resources costs grouped under functional categories are defined as direct or indirect depending upon whether they are attributable and assignable to research projects from the point of view of creation and delivery of value stream.

* The system of classification of projects by donor related conditions has no bearing on the principles of pooling costs to resource user units and recovery of costs on research projects. Financing an expense with donor-restricted resources does not make the expense restricted considering the nature and the amount as incurred.

* In developing principles for pooling, impact of transfer pricing policies of charging the service users at pre-determined rates by the management at respective centers for intra- and inter-center usage of resources/services is presumed to be neutral.

Overview of the framework: and methodology

The methodology for pooling of direct and indirect costs is based on the principle of attribution and assignability as shown in Exhibit 1.

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

4

Exhibit 1- Cost Pool Structure

Steps in applying the methodology:

a) Line item expenditures at the lowest possible level, for example from voucher, are pooled to different resource user units (cost centers) by direct identification and/or by establishing a linkage. These resource user units (cost centers) may either be the research projects, intermediate service providers (e.g. Utilities etc) or common departments e.g, Security service (providing services to various resource users). Examples of costs to be pooled by direct identification are: Factor Inputs, Consumables, Utilities, Personnel Cost, Professional Services/Visiting Scientist Services, Other line items of operating expenses and Depreciation. Illustrative format is given at Exhibit 9.

b) Expenditure, or a part thereof, for which no linkage can be established with any resource user units, is retained separately and grouped. Both (a) and (b) have been displayed in Exhibit 1.

c) The costs thus pooled to the intermediate service providers and common departments are allocated to other resource user units according to their assignability. It is possible that a cost center may perform a number of activities of different nature. In such cases, the total cost should be allocated reasonably and grouped under appropriate Resource User Units

Directly Chargedto Resource User

Unit

Operating ExpenseVoucher

Apportion toResource User

Units

Residual &Unlinked

Items

By DirectIdentification

Treated as a partof Common Sustenance

Services

Utilities By ResourceDriver

By ResourceDriver

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

5

d) Where line items costs and costs of certain common departments / utilities are not directly allocable, these should be apportioned on the basis of resource drivers. An illustrative list of resource cost drivers is shown in Exhibit 6.

e) The different pooled costs as stated at (b), (c) and (d) should be grouped into following functional categories based on the definitions and explanations in Section 3. Research, Research Support, Operations, Management and Common Sustenance Services

f) The costs thus aggregated under these five categories are treated as direct/indirect as described below:

RESEARCH: Direct

RESEARCH SUPPORT: Direct

OPERATIONS: Direct/Indirect

MANAGEMENT: Indirect

COMMON SUSTENANCE SERVICES: Indirect g) The ratio of Indirect Costs to the Direct Costs is the rate to be used for recovery of indirect costs. An illustration list of ratios for each individuals center based on 1999 financial data is shown in Exhibit 2 below. Exhibit 2: Illustrative Indirect Cost Ratios based on 1999 Financial Data

Indirect/Direct Indirect/Total(%) (%)

CIAT 22 18CIFOR 21 17CIMMYT 21 17CIP 27 21ICARDA 24 19ICLARM 19 16ICRAF 23 19ICRISAT 22 18IFPRI 17 14IITA 23 19ILRI 22 18IPGRI 18 15IRRI 21 18ISNAR 19 16IWMI 22 18WARDA 27 21

Center Ratios

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

6

SECTION 3 DEFINITIONS AND PRINCIPLES

Introduction

The methods and principles of cost pooling and grouping do not require changes in the codification of accounts, method of grouping of expenses for financial statement presentation, definitions of different groups of operating expenses and method of presentation of Statement of Activity and Balance Sheet under the financial accounting system. The process of grouping operating expenses into certain functionally homogeneous segments is illustrated in Exhibit 3.

Exhibit 3.

I. Description of Functional Grouping:

Principles of grouping expenses and resource user units (cost centers) into five functional segments and treatment of costs under respective functional segments as direct/indirect are described below and summarized in Exhibit 4.

Exhibit 4.

Bloc

k

Cost Principles Treatment

I Research Attribution

Activities engaged in or attributed to research programs/projects to fulfill the missions of

the Center. End results are expected to benefit the beneficiaries/project proponents and

members.

Direct

II Research

Support

Attribution and Assignability.

Inputs may be attributable / assignable to specific project / projects or shared by a

number of projects.

Direct

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

7

‘End’ produces a result that directly contributes the Research function

Bloc

k

Cost Principles Treatment

III Operations Assignability

Facilitating - (i) research and research support, (ii) management.

Direct/Indirect

IV Management Designs, plans, guides, governs and/or maintains a facilitating environment for the

Center. Not linked directly to transformation process.

Indirect

V Common

Sustenance

Services

Support the performance of center’s activities (including research) on an institutional

basis.

This also includes residual of operating expenses after allocation/apportionment to

Research, Research Support, Operations and Management groups.

Indirect

(A) Utilities Assignability

Intermediate service providers.

Resources consumed by user units in the same group(Utilities) and/or by users in any

one or more of the above five groups.

i) Pooled under

Blocks I, II

& III - Direct

ii) Rest -

Indirect

(B) Depreciation Attribution i) Relating to

Block I, II, III

and A(i) -

Direct

ii) Rest -

Indirect

Research:

Research function comprises activities, grouped as projects, whose end results are distributed/disseminated to beneficiaries, project proponents and members for fulfillment of the missions for which the center exists. Typically, these research activities are defined in context of the CGIAR research agenda. Expenses under this group relate to activities engaged in and directly attributed to research projects. This is a managerial definition and hence the projects should be at least at the level of aggregation corresponding to the projects described in the center medium term plan. These costs are direct.

Research Support:

This comprises of such resource user units whose 'end' produces a result that directly contributes to the performance of the research function. The resource user units under this group are directly identifiable and linked with research activities of the center. Thus activities that provide intellectual and technical inputs and any other direct input, and are dedicated to enable performance of research activities are covered under this functional segment. Such inputs may be creative/knowledge based/enabling. These costs are direct.

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

8

Operations:

This function comprises of different resource user units which provide facilities mainly to the Research and Research Support functions in the transformation of input knowledge into research projects into outputs and also delivery of research results, though not directly improving or affecting the working of research function. These resource user units are facilitators and are not directly identifiable or linked with any discrete research activities. The cost of services of Resource User Units providing facilities to users under Research and Research Support groups are grouped under the functional segment - Operations. These costs are direct.

Operations function also provides facilities and services to Management function. Costs of activities providing such services to Resource User Units under Management will be grouped under the functional segment - Management. Since Management is an indirect cost, this portion of Operation Cost is indirect.

Management:

Management function is the stewardship and governance of the center creates, plans, governs, guides, ensures quality control and/or maintains a facilitating environment but is not directly linked to the transformation process. The cost of management function is shown as the functional segment – Management.

Common Sustenance Services:

This group comprises of such Resource User Units that do not fall under any of the four segments as above but costs thereof are incurred to support the performance of center's activities (including research) on an institutional basis. These activities are performed to sustain the center. This heading also includes residual expenses after allocation/apportionment to respective user units. These costs are indirect.

II. Mapping Resource User Units to the Functional Groups: Examples

An indicative list of Resource User Units (departments/cost centers) and certain expenses of the nature of institutional sustenance that are required to be so grouped, is provided in Exhibit 5 below for guidance and reference. The list draws on the terminology commonly used at various centers, the meaning assigned to them and the nature of activities performed under such nomenclature.

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

9

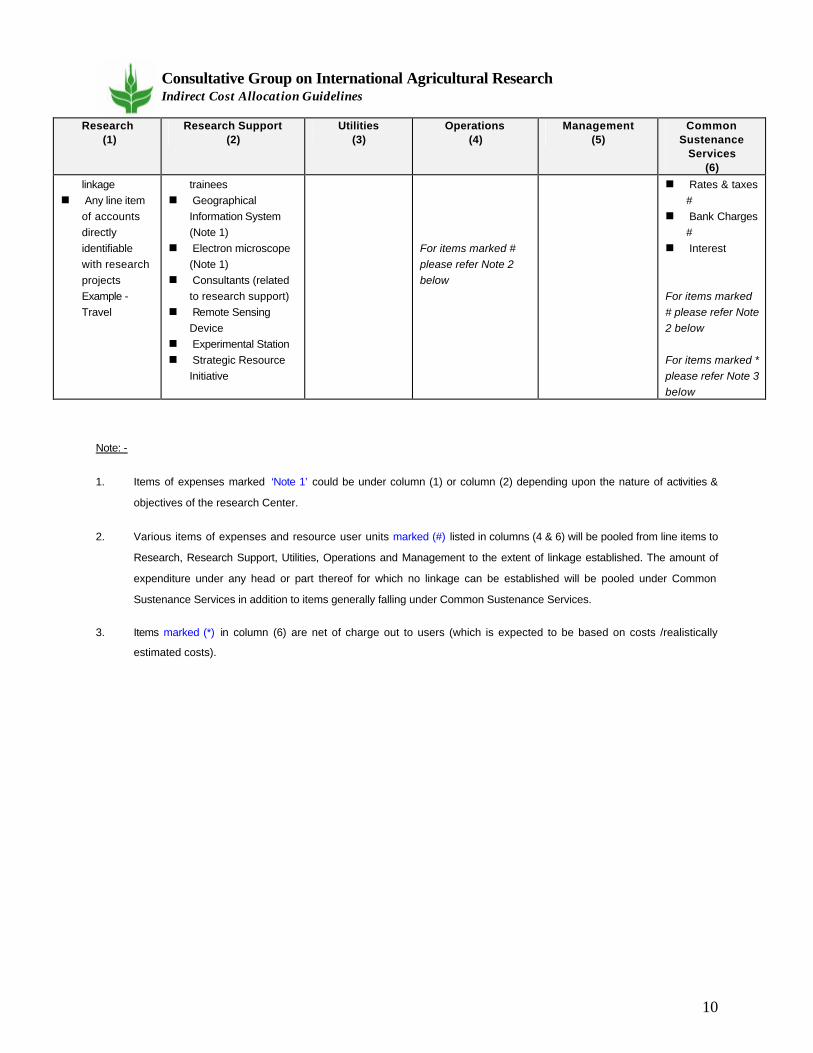

Exhibit 5 - Indicative List of Operating Expenses/Resource User Units

Research

(1) Research Support

(2) Utilities

(3) Operations

(4) Management

(5) Common

Sustenance Services

(6)

n This represents activities relating to research in accordance with the missions of the respective Centers. Certain activities, accordingly may be grouped under col. (2) in one Center, whereas they may be grouped under col. (1) in another Center.

Examples : n Training (Note

1) Research related Training

n Fellowship n Visiting

Scientists n Scientists

n Office of Director of Research

n Office of Director of out reach

n Laboratory Services n Publication / technical

bulletins contributing inputs to research (Note 1)

n Library n Partnership &

Information Management Service / workshop

n Farm administration n Plant growth facilities n Training (Note 1) n Farm operations /

services n Glass house

operations / plant growth facilities

n Research related computer services

n Electricity n Water Maintenance : n Farm

equipment. n Water

treatment n Diesel

Generator Sets / Power House

n Instrumentation

n Other equipment. engaged in research support

n Computer and Network etc.

n Ecological Maintenance Service

n Procurement Service (Purchase Department.)

n Supply Service (Stores Department.)

n Medical unit services

n Management Services / Computer Services

n Communications Services Department. #

n Rent (ground rent, lease rent, hire charge relating to research, research support & operations) #

n Transportation Department. Services (including motor vehicles exp.) #

n Rates & taxes # n Office Support

Services

n Board of Governors / Trustees

n Office of Director General

n Human Resource Development

n Donor Relations Department.

n Personnel Department

n Finance & Accounts Department

n Administration Department.

n Office of Finance Director

n Internal Audit Department.

n Liaison office n Corporate Office n Staff

Development

n Security n Canteen* n Cafeteria * n Hostel

Operations* n Housing

Services* n Laundry* n Swimming

Pool* n Cleaning n Garden n Visitor

Services / Reception Unit

n Transportation Department Services (including motor vehicles exp.) #

Rent (ground rent, lease rent, hire charge relating to research, research support & operations) #

n Research Information Management

n Identifiable activity for research policy, structure &

n Research related Information System

n Research Planning n Biometrics services n Gene Bank n Animal Unit n Green houses n Research associates,

n Insurance # n Printing &

stationery # n License fees #

n Insurance # n Printing &

stationery # n Communicatio

n services costs #

n License fees #

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

10

Research (1)

Research Support (2)

Utilities (3)

Operations (4)

Management (5)

Common Sustenance

Services (6)

linkage n Any line item

of accounts directly identifiable with research projects

Example - Travel

trainees n Geographical

Information System (Note 1)

n Electron microscope (Note 1)

n Consultants (related to research support)

n Remote Sensing Device

n Experimental Station n Strategic Resource

Initiative

For items marked # please refer Note 2 below

n Rates & taxes #

n Bank Charges #

n Interest For items marked # please refer Note 2 below For items marked * please refer Note 3 below

Note: -

1. Items of expenses marked ‘Note 1’ could be under column (1) or column (2) depending upon the nature of activities &

objectives of the research Center.

2. Various items of expenses and resource user units marked (#) listed in columns (4 & 6) will be pooled from line items to

Research, Research Support, Utilities, Operations and Management to the extent of linkage established. The amount of

expenditure under any head or part thereof for which no linkage can be established will be pooled under Common

Sustenance Services in addition to items generally falling under Common Sustenance Services.

3. Items marked (*) in column (6) are net of charge out to users (which is expected to be based on costs /realistically

estimated costs).

2711 Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

11

III. Resource Cost Drivers In the cost pooling hierarchy analysis the identification of resource drivers is an important exercise as drivers provide logical and credible basis for pooling the costs and allocating them to the users of resources. Resource drivers should be used where expense (i.e., cost of resources used) and specific Resource User Unit cannot be directly linked. Costs not assignable to any discrete function after direct identification and/or pooling through resource drivers should be grouped under Common Sustenance Services. Applicability: Resource drivers for pooling of cost are typically used in the following situations: a)Pooling of expenses to various Resource User Units (including utilities). b)Apportionment of cost of cross functional services in Utilities group.

c)Pooling of cost of Utilities to end users (i.e. various Resource User Units consuming the utilities).

d)Pooling of cost of Resource User Units under one or more of the functional groups; i.e.; Research, Research Support, Operations, Management, Common Sustenance Services. e)Pooling of cost of certain operating expenses like depreciation under one or more of the five functional groups.

Validity & Reliability of resource drivers: The system of application of resource drivers has two components - (a) driver that causes consumption of resources, and (b) weight/base for application of the selected driver. Both these aspects need to be considered before selecting the applicable resource drivers for pooling, to ensure validity, and both should be reviewed periodically for reliability of the system. Illustrative list of risk factors is shown in Exhibit 14. Indicative list of resource drivers: Individual centers are the best judge of the appropriateness of specific resource drivers. Exhibits 6 and 6.1 are indicative lists of resource drivers for typical common service providers. The preferred alternatives are given in italics. Alternative resource drivers have been indicated in certain cases for selection of any one depending upon reasonability and availability of data at a center.

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

12

Exhibit 6: List of Resource Drivers (excluding depreciation)

Functional Areas Resource Drivers Remarks

Procurement Function

(Staff Cost & Other Expenses)

n Number of Purchase Indents received

n Number of Purchase Orders raised

n Value of Purchase

Pooled under different functional groups; i.e.;

Research, Research Support, Operations and

Management

Stores or Internal Supply

Services/warehousing,

receiving & shipping

(Staff Cost & Other Expenses)

n Number of Requisitions

n Value of Issuance/Consumption

Pooled under different functional groups; i.e.;

Research, Research Support, Operations and

Management

Computer Services n Estimated/Actual Throughput time

n No. of terminals in resource user unit

n Value of Hardware located at a Resource User

Units

n Estimated Time Sharing by users of central network

system

Pooled under different functional groups; i.e.;

Research, Research Support, Operations and

Management

Communications n Direct identification with Resource User Units

n Time Sharing of Specific Medium by the Respective

resource user unit

n Estimated/Actual/Predetermined usage time by

respective User Units

Pooled under different functional groups; i.e.;

Research, Research Support, Operations and

Management

Residual and Unassignable portion of fixed cost to

be pooled under Common Sustenance Services.

Transportation Services n Direct identification with Resource User Units

n By KM traveled

n By Passenger-KM combined weight

n By department wise spread of no. of users served

by the Transportation Department.

Pooled under different functional groups; i.e.;

Research, Research Support, Operations and

Management

Residual and Unassignable cost is pooled under

Common Sustenance Services

Vehicle Maintenance (In

House/ Outsource)

n Direct identification with Resource User Units for

earmarked vehicles

n By no. of Persons belonging to a department

carried in case of mass transit vehicles

Pooled under different functional groups; i.e.;

Research, Research Support, Operations and

Management

Residual and Unassignable cost is pooled under

Common Sustenance Services

Publications

(Other than cost of factor

inputs for bringing out

publications)

n Ratio of direct cost of technical/and non-technical

publications

n Time (Estimated/or Actual) of key personnel shared

by (a) technical & (b) Non technical publications/

advertisement/ printing/ corporate brochure etc.

Cost identified for technical publications pooled to

Resource User Units will be treated as ‘Research

Support’ or ‘Research’ depending upon the missions

of the Center.

Cost identified for non-technical (e.g., corporate

brochure, annual report, plans, annual accounts

etc.) publications, advertisement, publicity will be

pooled as publications and treated as Management

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

13

function.

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

14

Functional Areas Resource Drivers Remarks

PIM & Public Awareness n Time (Estimated/Actual) of key personnel shared by

(a) technical & (b) Non technical

publications/advertisement / printing / corporate

brochure

Cost identified for PIM pooled to Resource User Unit

will be treated as ‘Research Support’ or ‘Research’

depending upon the missions of the Center.

Treatment of Public Awareness will however

depend upon nature and objective of the functions

performed by a Center.

Rent n Floor area Cost pertaining to common (unallocable) facilities

may be reapportioned on floor area ratio among

Resource User Units OR included under Common

Sustenance Services.

Non Research Training /

Conference / Seminars and

Staff Development Programs

n Number of Participants from respective resource

user units

This refers to direct expenses incurred in a program.

Personnel and other cost of the training department

will be apportioned on similar basis.

Insurance n To be identified with related

n Assets

n Objects

n Persons

n and pooled under respective resource user units.

Depreciation Please refer to Exhibit 6. 1 on Depreciation

Electricity (Purchased /

Captive)

kWh Electricity used for Research and Research Support,

as Process Power is to be identified and pooled;

balance for general use to be pooled under

respective user units and grouped under Operations

and Management respectively. Electricity consumed

by self-sustaining ancillary services will generally be

pooled under the costs of such units. Costs of such

service units, net of charge out to users, will be

grouped under Common Sustenance Services.

Water KL Consumed Pending installation of flow meter, to be treated as

Operations. Once flow meter data are available, by

KL consumed

Maintenance (equipment) Time Sharing by Resource User Units except for directly

identifiable element like spares, tools, consumables etc.

which will be charged directly to the users

Maintenance expenses of equipment (field/farm &

laboratory) may be grouped under Research Support

without pooling through Resource User Units

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

15

Maintenance (building) Direct identification with Building and floor area of

respective departments in each building for materials

and engagement time

Unallocable portion to be under CSS

Exhibit 6.1: Depreciation

• Depreciation on various items of Fixed Assets should be identified with a Resource User Unit - direct - on the basis of physical location data available from Property, Plant and Equipment Card / Fixed Asset Registers. Such items of fixed assets would be plant and equipment; mobile equipment of farmhouse; glass house equipment; laboratory equipment / instruments; electrical and instrumentation items; motor vehicles and garage equipment; office equipment; computer configuration; buildings / sheds etc. Generally equipment/instrument of farmhouses, glass house, gene bank, laboratory will be pooled under Research Support.

• Where use of Fixed Assets is shared by a number of Resource User Units, depreciation should be pooled on suitable basis (e.g. time sharing ratio; observed / estimated throughput time; identified bus lines of network system, gross/net block of the asset dedicated to a Resource User Unit etc.)

• Depreciation on Building for respective user units should be on the basis of floor area.

• Alternatively, for the limited purpose of reporting direct and indirect costs, depreciation on various items of Fixed Assets identified separately with Research, Research Support and Operations Function, may be collected under the three broad functional congregation and treated as - Direct, instead of department-wise pooling, maintaining the same principles.

• Depreciation on equipment belonging to Utilities group should be separately identified and pooled and treated as Direct or Indirect depending on the nature of User Units of utilities.

• Depreciation relating to fixed assets used by Management and Common Sustenance Services should be treated as indirect and exhibited separately under Management or Common Sustenance Services according to use.

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

16

SECTION 4 IMPLEMENTING THE METHODOLOGY

This Section describes the steps in implementing the methodology by providing detailed step by step procedures as well as documentation and reporting work sheets.

Developmental Phase:

• Create and codify the five functional groups (Research, Research Support, Operations, Management and Common Sustenance Services).

• Identify and codify Resource User Units (RUU s) using examples provided in exhibit 5. Names of Cost Centers used in the chart of accounts should be reviewed to ensure clear understanding of the nature of activities performed by the cost center.

• Select appropriate resource drivers for respective RUU s. An explanatory list of resource drivers is given in Exhibits 6 and 6.1.

• Ascertain values / weights (number, volume, weight, value, technical data etc.) for selected resource drivers. Identify the responsibility within the center for consistent source data.

Exhibit 7 - Developmental Phase

Codify

Identify & Codify

Select

Develop & Update

A. Functional Groups, i.e. R, RS, O & M

B. Resource User Units Center Specific Activities

C. Resource Drivers

D. Values for application of Resource Drivers

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

17

Exhibit 8: Application Phase

i) Assign Operating expense items, from source document if necessary, to appropriate RUU if fully identifiable with specific RUU.

ii) Apportion expenses of shared resources to RUUs on the basis of selected resource drivers and the corresponding value / weight for application.

iii) Retain items of operating expense, or a part thereof, unlinked to any RUU under the account head of line item as residual balance for further treatment.

iv) Prepare a cost pool sheet for each RUU indicating the elements of expenses, amounts, basis of pooling and explanatory notes as required. An indicative Cost Pool Sheet is given at Exhibit 9.

v) Prepare Expense Matrix Summary. Illustrative format is at Exhibit 10.

vi) Group Pooled costs under RUU s and residual balances as per Expense Matrix under the five functional segments-Research, Research Support, Operations, Management and Common Sustenance Services [Exhibit 11].

Enter

Apportion

Retain

Financial group/RUU reference on Source Document if fully identifiable with RUUS

Shared Expenses to RUUs on the basis of resource drivers & their values

Expenses not linkable to any discrete RUUs

Expense Matrix

Expense Matrix (Line Items vs BUUs) (Exam. Exhibit 7)

Expense Matrix Exhibit Expense Summary & Cost

Ratios

Grouping Matrix (Exhibit 8)

Pool the RUUS under 5 functional groups: (Follow Definition and Principles for treatment of Cost.)

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

18

Exhibit 9: Cost Pool Sheet (Composition of Cost of a Resource User Unit)

(Indicative only)

Items of Cost A/C Code Amount Basis of Pooling Remarks

Factor Inputs Direct Identification

(From line items/Source Record)

Applicable to relevant user unit like

research program, Lab, farmhouse, gene

bank, animal unit, glass house, FESP,

PPS etc.

Consumable Do Do

Personnel Cost Do Applicable to all RUU s

Professional Services/

Visiting Scientist

Services

Do Generally directly identified with the

concerned user

Utilities i) Direct Identification

ii) Through resource drivers

Please refer to list of resource drivers

Exhibit 6

Other line items of

Operating Expenses

(i) Direct Identification

(ii) Apportionment through resource

drivers

Please refer to list of resource drivers

Exhibit 6

Depreciation

(Asset Wise)*

Do Please refer to list of resource drivers

Exhibit 6.1

* Alternatively, as suggested in Exhibit 6.1 depreciation asset group wise may be directly reported under

functional classification of Research, Research Support, Operations, Management and Common Sustenance Services.

Exhibit 10: - Expense Matrix Summary (Example)

Programs/ Activities/Resource

User Units IRS Costs NRS Costs

Other staff costs

Training Travel costs Supplies General expenses

Total

Residual balance Total

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

19

Documentation and Reporting:

To ensure consistency and replicability, a series of reporting formats are outlined in exhibits 11 and 12. Each report should be supported by explanatory Notes which, as a minimum, should specify the following: i) The list of RUU s/expenses where apportionment is made, resource cost drivers used for apportionment and weights applied. ii) When resource cost drivers and corresponding weights were last reviewed. iii) Note on matters which are unique for the center and are significant along with amount and treatment given. iv) Confirmation whether treatment of direct/indirect cost is according to the principles & methodology as per the Manual. v) Whether costs reported are independent of transfer pricing mechanism adopted by the center and its impact.

Exhibit 11: - Grouping Matrix

Resource User Units

and Unallocated

expenses

Research Research Support Operations Management Common

Sustenance

Services

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

20

Exhibit 12: Statement of Operating Expenses (Center level consolidation)

Exhibit 13: Statement of Operating Expenses (Location wise Summary)

Locations è HQ Total

Research

Research Support

Operations

Direct Operating Expenses

Management

Common Sustenance Services

Indirect Operating Expenses

Total Operating Expenses

Cost Ratios

Direct/Total

Indirect/Total

Particulars Total

Research

Research Support

Operations

Direct Operating Expenses

Management

Common Sustenance Services

Indirect Operating Expenses

Total Operating Expenses

Cost Ratios

Direct/Total

Indirect/Total

Indirect/Direct

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

21

Indirect/Direct

2722 Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

22

Exhibit 14: Risk Management considerations Knowledge of risks, so far as cost pooling module is concerned, is the understanding of events / absence of events or actions / non-actions that may cause hindrance in achieving the intended objectives of cost pooling methodology and purposes of cost management in general. The following table highlights the selected risk areas, and methods to minimize risks.

Sl. # Risk Areas Action / in-action Risk Implications Risk Management

1. Departmental

activities & cost

allocation process

Automatic allocation to cost

/ budget centers by

preconceived subjective &

traditional criteria.

i. Relevance of cost for RUU s is

not identified.

ii. Responsibility for cost is

diffused throughout the

organization

iii. Relationship of cost with

creation / delivery of value is

not established.

? Costs are to be analyzed by

drivers that determine how

resources are consumed by

resource users for activities

performed so that relevance of

cost is established.

? Managers should be responsible

for resources consumption by their

respective departments.

? Activities performed by RUUs

should be analyzed to establish

relationship with research missions

by identifying how they contribute

to / facilitate creation / delivery of

value.

2. Tools &

Technique –

Selection of

Resource Cost

Drivers & Weights

for application of

Drivers

a) Selection without

analysis of relevance,

accessibility,

justification & benefits,

and

b) Without reference to

list of resource drivers

commonly applicable

as per manual.

i. Cost allocation is unrealistic

ii. Incongruity between cost and

benefits in the selection

process

iii. Pooled costs are not relevant

iv. Heterogeneous basis

Steps :

? Make a provisional selection first

? Eensure accessibility of base data

on regular basis for application of

drivers

? Whether collection of base data

(weights) justify cost & time

? Carryout similar additional analysis

with alternative drivers

? Examine whether composite driver

is more relevant

? Finalize selection of driver which

suits best in terms of causal

relationship, easy accessibility &

cost-benefit of collection of data.

3. Tools &

Techniques of

allocation –

review of

resources cost

drivers & weights

Lack of periodic review and

update

i. Allocated costs are unrealistic

ii) Results of cost ratios are

distorted & unreliable

iii. No improvement agenda for

cost performance

? Resource cost drivers should be

reviewed periodically – at least

once in two years – for credibility.

l ‘Weights’ i.e. basis for application

of drivers should be on data for the

period for which operating

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

23

Sl. # Risk Areas Action / in-action Risk Implications Risk Management

for application of

drivers

expenses & cost ratios are

reported.

l If cost expensed in one period

benefit two or more interim periods

suitable deferrals/accruals may be

used to avoid distortion of cost

ratios.

4. Environmental

changes, mission

changes,

organisational

changes,

changing donor

needs &

expectations

Non response to change;

non review of reporting

system; poor internal

information system

i) Reporting System does not

meet financial planning needs

& strategies

ii) Likely adverse effect on ability

to raise funds

iii) Negative effect on reputation &

image

? Regular review & update of

reporting system

? Ensuring that internal

information system is quick,

undisrupted and focused

? Regular assessment of risks

arising out of poor systems.

5. Documentation &

Pooling

Error in documentation

resulting in incorrect

identification, attribution &

assignability

i) Incorrect cost data & cost

ratios

ii) Discordant note among

resource users for the cost

reported for respective

departments

iii) Pooled costs results are not in

harmony with the results of

other Centers having similar

infrastructure & activities.

? Principles outlined in the guidelines of

should be followed for

documentation & pooling costs

? Close co-ordination is required

among managers responsible for

accounting framework, financial (&

budgeting) framework and cost

pooling framework.

? Effective monitoring system should

be in position to ensure compliance.

Ravi Tadvalkar

Consultative Group on International Agricultural Research Indirect Cost Allocation Guidelines

24

N:\FINANCE\FG Series\Financial Guidelines Series No 5.doc August 13, 2001 12:30 PM