certain provisions relating to companies act. · managerial remuneration ... on and after the...

TRANSCRIPT

CNK & Associates LLP

Chartered Accountants

Manish Sampat

June 16, 2018

Certain provisions relating to Companies Act.

Sub Regional Conference -

Vadodara

2CNK

Disclaimer

• Views expressed herein may not necessarily reflect the views of the firm.

• A presentation which raises ideas and concepts does not amount to anopinion of the firm or of the author, but should be merely viewed as mattershaving potential possibility.

• Presentations are intended to be dissuasive and not conclusive

• A presentation is not a replacement for a formal opinion on a point of lawwhich may require to be addressed.

• The information and views contained in this presentation are to be viewedwith caution and should be appropriately considered.

• Information provided herein is only for the benefit of the recipients, and is notto be shared with any other person without our or ICAI’s consent

3CNK

Today’s Agenda

• Provisions relating to:

Acceptance of Deposits by Companies [Sec 73 to 76 Chapter V]

Loans to Directors [Sec 185 Chapter XII]

Related Parties Transactions [Sec 188 Chapter XII]

Managerial Remuneration [Sec 197-199 Chapter XIII]

Declaration of Dividend [Sec 123-127 Chapter VIII]

CNK & Associates LLP

Chartered Accountants

Provisions Regarding

Acceptance of Deposits by Companies [Chapter V]

5CNK

Acceptance Of Deposits By Companies w.e.f. 01.04.2014 (Section – 73)

Section 73 Corresponding to Sec 58A

(1) On and after the commencement of this Act, no company shall

invite, accept or renew deposits under this Act from the public

except in a manner provided under this Chapter.

Exclusions:

(a) Banking Company

(b) Non- Banking Finance Company registered with RBI

(c) Any other Company specified by CG after consultationwith RBI

6CNK

Deposit Definitions:

• Section 2(31) : "deposit" includes any receipt of money by way ofdeposit or loan or in any other form by a company, but does not includesuch categories of amount as may be prescribed* in consultation withthe Reserve Bank of India;

• Rule 2(c) - “deposit includes any receipt of money by way of deposits orloan or in any other form, by a company, but does not include thefollowing: …..”

• Therefore , the three elements which will constitute as deposit

– Any receipt of money by way of deposit;

– Any loan; and

– Any receipt of money in any other form .

7CNK

Deposit: Rule 2(c) of CAD Rules 2014

Certain types of monies received by a company are excluded from the

definition of 'deposit'- Following amount received shall not be

considered as "Deposit“

i. From Central Government /State Government/ local authority ;

ii. Foreign or international banks/multilateral financial institution,

foreign authorities and persons resident outside India subject to

provisions of FEMA,1999 ;

iii. Banking Companies and Banking Institution notified under Banking

Regulation Act including co-operative banks;

iv. Public Financial Institution /Regional Financial Institutions /

Insurance Companies / Scheduled Banks ;

v. Commercial paper or any other instruments issued in accordance

with the guidelines of Reserve Bank of India.

8CNK

vi. any other Company

vii. Subscription for securities including share application money

viii. a director or relative of director of private company

ix. issue of bonds or debentures secured by first charge on any assets / listed unsecured NCDs

ixa any listed NCD issued without any charge on assets

x. an employee of the company not exceeding his annual salary in the nature of non interest bearing security.

xi. a Non- interest bearing amount received and held in trust

xii. Any amount received in the course of or the purpose of the business for the following:

(a) As advance for the supply of goods or provision of services

Deposit: Rule 2(c) of CAD Rules 2014

9CNK

b) As advance received in connection with consideration for immovable property under an agreement or arrangement,

c) As security deposit for the performance of the contract for supply of goods or provision of services.

d) As advance received under long term projects for supply of capital goods.

e) As advance towards consideration for providing future service

f) As advance Received and as allowed by any sectoral regulator from CG/SG

g) advance for subscription towards publication

xiii. Any amount brought in by the promoters themselves or their relatives by way of unsecured loan in pursuance of a stipulation of any lending institution on the promoters

Deposit: Rule 2(c) of CAD Rules 2014

10CNK

xiv. any amount accepted by a Nidhi Company in accordance withrules made U/s 406 of the Act

xv. any amount received by way of subscription by Chit fund company

xvi. any amount received by company under collective investmentscheme framed by SEBI

xvii.an amount of twenty five lakh rupees or more received by a start-up company, by way of a convertible note in a single tranche, froma person.

xviii. any amount received by a company from Alternate InvestmentFunds, Domestic Venture Capital Funds, Infrastructure InvestmentFunds and Mutual Funds registered with the SEBI in accordancewith regulations made by it.

Deposit: Rule 2(c) of CAD Rules 2014

11CNK

Deposit accepted under Co's Act,1956 and renewed after 01.04.2014

Issue: Whether deposit accepted under Co's Act, 1956 renewed

after 01.04.2014 need to comply with the provision of this

section?

- Clarification regarding applicability of Act in Circular 5 /2015

dated 30.03.2015

12CNK

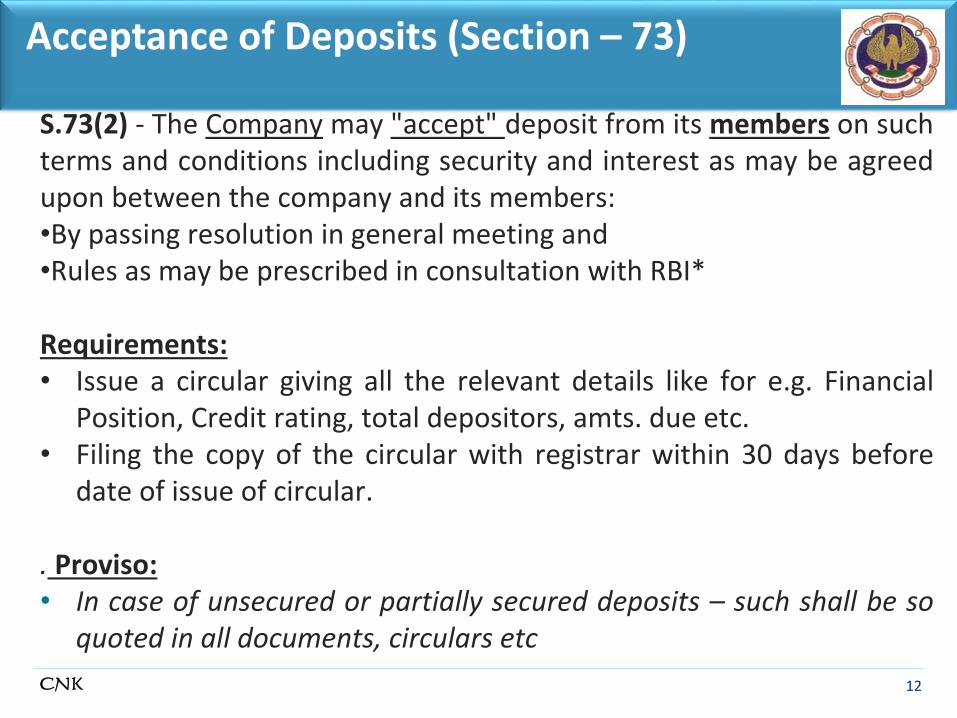

Acceptance of Deposits (Section – 73)

S.73(2) - The Company may "accept" deposit from its members on suchterms and conditions including security and interest as may be agreedupon between the company and its members:•By passing resolution in general meeting and•Rules as may be prescribed in consultation with RBI*

Requirements:• Issue a circular giving all the relevant details like for e.g. Financial

Position, Credit rating, total depositors, amts. due etc.• Filing the copy of the circular with registrar within 30 days before

date of issue of circular.

. Proviso:• In case of unsecured or partially secured deposits – such shall be so

quoted in all documents, circulars etc

13CNK

Additional Requirements (As amended by Companies (Amendment)Act, 2017 - Yet to be notified by Central Government):

Depositing before the 30th April each year not less than 20% 15%maturing during following two FY - separate bank account of ascheduled - deposit repayment reserve account

Insurance as may be prescribed

Certification - no default in the repayment of deposits & interest- before or after the commencement of this Act and where adefault had occurred, the company made good the default and aperiod of five years had lapsed since the date of making good thedefault

providing security, if any and creation of charge on the propertyor assets of the company

Acceptance of Deposits (Section – 73)

14CNK

Provisions - Private Companies

Notification dated 13th June, 2017

Clauses (a) to (e) of Sec 73 (2) – not applicable to a Private Co:

Accepts monies from members not exceeding 100% (PSC+ FR+SP); OR

Is a ‘start-up’, for five years from date of its incorporation; OR

Which fulfils the following:

(a) which is not an associate or a subsidiary company of any other company;

(b) if the borrowings of such a company from banks or financial institutions or

any body corporate is less than twice of its paid up share capital or fifty

crore rupees, whichever is lower; and

(c) such a company has not defaulted in the repayment of such borrowings

subsisting at the time of accepting deposits under this section:

Such company shall file the details of monies so accepted to the Registrar

in such manner as may be specified

15CNK

Provisions – Specified IFSC Public Company

Notification dated 4th January 2017

Clauses (a) to (e) of subsection (2) of section 73 Shall not apply to a

Specified IFSC public company which accepts from its members,

monies not exceeding one hundred per cent. of aggregate of the

paid up share capital and free reserves, and such company shall file

the details of monies so accepted to the Registrar in such manner

as may be specified

16CNK

Deposit from members (Section 73)

Conditions:

S. 73(3) - repay with interest in accordance with the terms and conditions

S. 73(4) - Failure - the depositor may apply to the NCLT repayment or for

any loss or damage

S. 73(5) - Deposit repayment reserve account not be used for any purpose

other than repayment of deposits.

17CNK

Repayment of deposits, etc., accepted before commencement of this Act (Section – 74)

• Section 74 new provision enforced on 01.04.2014

Clause (1) - any deposit accepted by a company beforecommencement of the Act, the amount of deposit or any interestdue thereon remains unpaid on such commencement or becomesdue at any time thereafter, the company shall:

a) file within a period of three months from such commencementor from the date on which such payments, are due, with theregistrar, a statement*, and;

b) repay within three years from such commencement or on orbefore expiry of the period for which the deposits wereaccepted, whichever is earlier repay within one year from suchcommencement or from the date on which such payments aredue, whichever is earlier - yet to be notified.

18CNK

(2) The Tribunal may on application made by the Company, afterconsidering financial condition of the company, allow further timeas considered reasonable to the company to repay the deposit.

(3) If company fails to repay the deposit or interest thereon within atime specified in sub section (1) and (2), be punishable with:

– For Company - Fine – Rs. 1 crore to Rs. 10 crore

– For every officer in default – imprisonment upto 7 years or withthe fine of Rs. 25 lakhs to Rs. 2 crores or with both.

Repayment of deposits, etc., accepted before commencement of this Act (Section – 74)

19CNK

Damages for Fraud (Section 75)

• Section 75 new provision enforced w.e.f. 01.06.2016

1) It is proved that deposit accepted with intent to defraud thedepositors or for any fraudulent purposes, every officerresponsible for accepting deposits, will be personally liablewithout any limitation of liability, for all or any of the losses ordamages that may have been incurred by the depositor.

2) Any suit, proceedings or other action may be taken by anyperson or any group of persons or any association of persons.

20CNK

Acceptance of Deposits by certain companies (Section 76) Notwithstanding anything contained in Section 73, a public company,

having such net worth or turnover as may be prescribed, may acceptdeposits from persons other than its members subject to compliancewith the requirement provided in sub-section (2) of Section 73 andsubject to rules as the CG may prescribe.

First Proviso:

"such company need to obtain rating from recognized credit ratingagency at the time of inviting the deposit and the rating shall beobtained every year during the tenure of deposit“*

Second Proviso:

"Every company accepting secured deposit from the public shall createa charge on its assets within 30 days from acceptance to the extent ofamount of deposit accepted"

•

21CNK

Section 76 r.w. CAD Rules 2014

Eligible company (Rule 2(e) of CAD Rules 2014):

• Net worth –not less than INR 100 cr. OR

• Turnover – not less than INR 500 cr. AND

• Prior consent of the company in General meeting (Special Resolution)

• Filed a copy of Resolution before registrar before making invitation

• Ordinary Resolution of the deposit is within the limit of Section180(1)(c)

Term of Deposit (Rule 3 of CAD Rules 2014): Members + Public

• Repayable on demand OR

• Upon receiving notice in less than 6 months* OR

• Upon receiving notice in more than 36 months

• From the date on which such deposits were taken

* Certain exception for short term requirement of funds

22CNK

Section 76 r.w. CAD rules, 2014

Limit * on quantum of Deposits (Rule 3 of CAD Rules 2014):

Limit on Deposit from Members:

• A company can take deposit from its members up to 25 35%** of the aggregate of the paid up share capital, free reserves and Securities Premium Account of the company

• Specified IFSC Co. and Pvt. Co.- 100% of PSC + FR + SP

Limit on deposits for Eligible Company:

• From company’s members – up to 10 % of PSC+FR+SP

• From Public- up to 25% of PSC + FR + SP

Limit on deposit from public for Govt. Company:

• Up to 35% of PSC + FR + SP

23CNK

Section 76 r.w. CAD rules, 2014

• Deposits from members & public - Maximum interest rate

brokerage regulated by RBI

• Alteration in terms and conditions (prejudice or disadvantage of

the depositor) not possible

24CNK

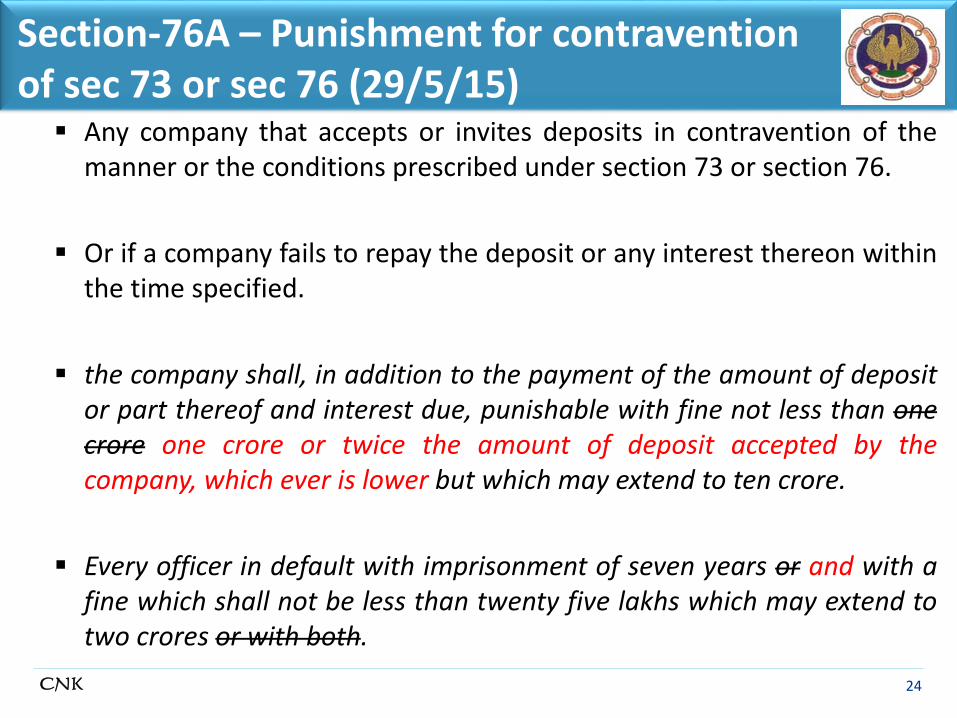

Section-76A – Punishment for contravention of sec 73 or sec 76 (29/5/15) Any company that accepts or invites deposits in contravention of the

manner or the conditions prescribed under section 73 or section 76.

Or if a company fails to repay the deposit or any interest thereon withinthe time specified.

the company shall, in addition to the payment of the amount of depositor part thereof and interest due, punishable with fine not less than onecrore one crore or twice the amount of deposit accepted by thecompany, which ever is lower but which may extend to ten crore.

Every officer in default with imprisonment of seven years or and with afine which shall not be less than twenty five lakhs which may extend totwo crores or with both.

25CNK

Rule 16A (29/6/16)

Disclosures in the financial statement.-

(1) Every company, other than a private company, shall disclose in itsfinancial statement, by way of notes, about the money receivedfrom the director.

(2) Every private company shall disclose in its financial statement, byway of notes, about the money received from the directors, orrelatives of directors.”.

•

26CNK

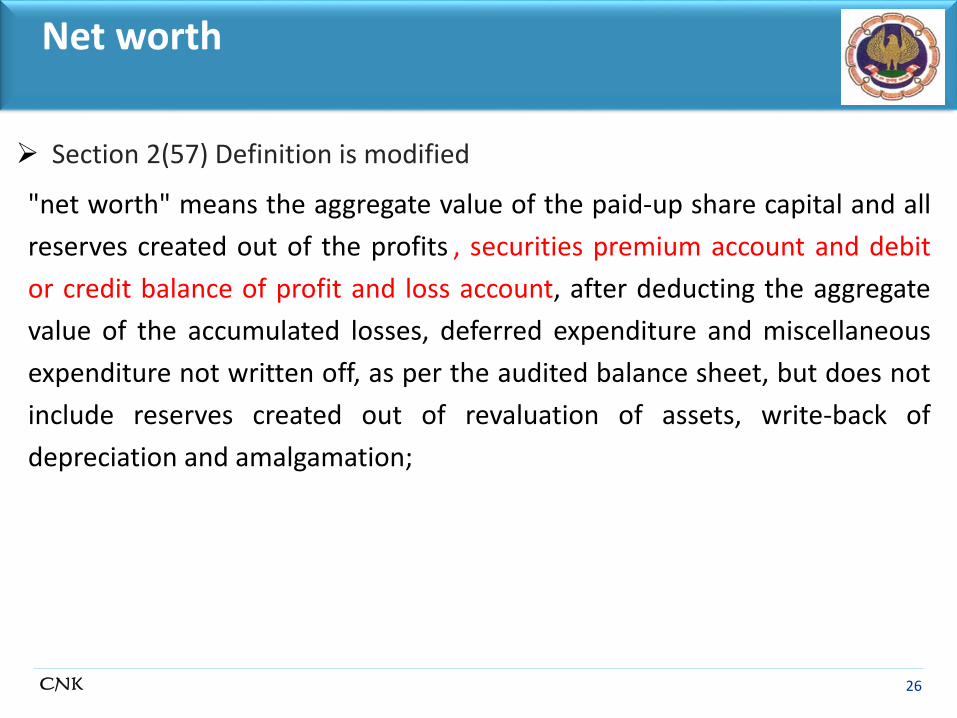

Section 2(57) Definition is modified

"net worth" means the aggregate value of the paid-up share capital and all

reserves created out of the profits , securities premium account and debit

or credit balance of profit and loss account, after deducting the aggregate

value of the accumulated losses, deferred expenditure and miscellaneous

expenditure not written off, as per the audited balance sheet, but does not

include reserves created out of revaluation of assets, write-back of

depreciation and amalgamation;

Net worth

27CNK

Free Reserves

Section 2(43) Definition is modified

“free reserves” means such reserves which, as per the latest audited

balance sheet of a company, are available for distribution as dividend;

Provided that:

i. any amount representing unrealised gains, notional gains or

revaluation of assets, whether shown as a reserve or otherwise, or

ii. any change in carrying amount of an asset or of a liability recognised

in equity, including surplus in profit and loss account on

measurement of the asset or the liability at fair value,

shall not be treated as free reserves.

28CNK

Section 2(91) New Definition

“turnover" means the gross amount of revenue recognised in the profit

and loss account from the sale, supply, or distribution of goods or on

account of services rendered, or both, by a company during a financial

year”

Turnover

29CNK

FAQs

• Can a Private Company Accept deposit from its members?

– If yes – upto what limit?

– What are the compliances required?

• Can a Private Company Accept deposit from its directors and/or

relatives of such directors?

– If yes – upto what limit?

– What are the compliances required?

• Can a Private Company Accept deposit from public?

– What is the maximum limit

30CNK

• Does deposits provisions cover debentures?

• Secured CCDs/OCDs/NCD – not a deposit

• Unsecured CCDs/OCDs/NCDs issued to a co.- not a deposit

• Unsecured CCDs/OCDs/NCDs issued to a resident - not a deposit if

converted within 10 years

• Unsecured CCDs/OCDs/NCDs issued to a resident - not a deposit if

listed otherwise deposit

• Unsecured CCDs/OCDs/NCDs issued to a foreign body - not a deposit

FAQs

CNK & Associates LLP

Chartered Accountants

Loans to Directors[Sec. 185 Chapter XII]

33CNK

Loans to Directors (section 185) (As Amended)

• Corresponding to Sec. 295 & 296 of the 1956 Act

• Entire provision of Section 185 of the Act substituted by

Companies (Amendment) Act, 2017 and has been made effective

from May 7, 2018.

• In Clause (1) the words “Save as otherwise provided in this Act,”

have been deleted.

34CNK

No company shall directly or indirectly advance any loan, includingany loan represented by a book debt to, or give any guarantee orprovide any security in connection with any loan taken by,—

Any director of company; or Any Director of holding company; or Any partner or relative of any such director; or firm in which any such director or relative is a partner.

Loans to Directors (section 185) (As Amended)

35CNK

A company may advance any loan including any loan represented by abook debt or give any guarantee or provide any security in connectionwith loan taken by: any private company of which such director is a director or member; Any body corporate at GM of which not less than 25% is controlled

by any such director; Any body corporate- BOD are accustomed to act in accordance with

instruction of the lending company.

Condition for granting loan to above 3 parties:

special resolution is passed by the lending company [with explanatory details to disclose full details];

the loans are utilised by the borrowing company for its principal business activities.

Loans to Directors (section 185) (As Amended)

36CNK

Exemptions:

giving any loan to a managing director or whole time director;

as part of the conditions of service extended by the company to all its employees; or

pursuant to any scheme approved by the members by a Special Resolution

Ordinary course of business to provide loans and interest at GSec rates of comparable tenor;

Loan/Security/Guarantee by holding to subsidiary for any loan taken by Subsidiary company;

Security/Guarantee by holding to subsidiary for any loan taken by Subsidiary company from Banks/ Financial Institution;

Loans to Directors (section 185) (As Amended)

37CNK

Penal provision in contravention of section 185:

The company shall be punishable with fine which shall not be lessthan five lakh rupees but which may extend to twenty five lakhs;

Director or other person to whom any loan is advanced orguarantee or security is given or provided in connection with anyloan by him or other person- imprisonment of six months withminimum fine of five lakhs.

Loans to Directors (section 185) (As Amended)

38CNK

Loans to Directors (Section 185)

Exemption to Private Companies:*

Section 185 will not apply to Private Company -

In whose share capital no other "body corporate" has invested anymoney ;

If borrowing from Banks or FI's or any body corporate is less thantwice of paid up capital or fifty crore, whichever is lower ;

Such a company has no defaults in repayment of such borrowingsubsisting at the time of making transactions under this section.

39CNK

Other Exemption :

Section 185 shall not apply to Government company-*

In case such company obtains approval of the Ministry orDepartment of the Central Government/State Government beforemaking any loan or giving any guarantee or providing any securityunder the section ;

Section 185 shall not apply to Nidhi company-**

The loan is given to a director or his relative in their capacity as members and such transaction is disclosed in the annual accounts by a note.

Loans to Directors (Section 185)

40CNK

Other Exemption (Notification Dated 4th January, 2017) :

Explanation to clause (c) of Sec 185 (1)

In case of Specified IFSC Public Company & In case of Specified IFSC Private Company

any private company of which any such director is a director ormember in which director of the lending company do not have director indirect shareholding through themselves or through their relativesand a special resolution is passed to this effect;”;

International Financial Services Centre (IFSC)

Loans to Directors (Section 185)

41CNK

• A Ltd. has two directors PM and AM , both holds 50% share each ofcompany. A Ltd. wish to give loan to following and have asked your viewson same.

Loan to Director PM

Loan to a relative of Director AM

Director of D Ltd. which is holding company of A Ltd.

A Partner of Director of Holding Company

A Partner of Director of A Ltd.

To a firm in which Mr. PM is partner

To a firm in which relative of Mr. AM is a Partner

To a LLP in which PM is partner

Case Study

42CNK

• Sec 2(77) - ‘‘relative’’, with reference to any person, means

anyone who is related to another, if—

■ (i) they are members of a Hindu Undivided Family;

■ (ii) they are husband and wife; or

■ (iii) one person is related to the other in such manner as may be

prescribed*;

*- Father, mother, son, son’s wife, daughter, daughter’s husband,

brother, sister, (including step relations)

Relative

43CNK

• No distinction between Private & Public company initially

• Certain exemptions for Private coms brought back

• Even if a loan etc. obtained in contravention of the above

provisions is repaid, the contravener would still be exposed to

punishment by way of imprisonment

• Applicable prospectively and should not affect existing loans etc.

• Renewals of loan etc. needs to be in conformity with the 2013

Act

• Section does not contain any remedial proviso

Key takeways

44CNK

Issues & solutions:

• What happen to existing loans?

• Shares held by directors as “nominee”

• Rearrange or realign – shareholding and/or directorship

• Appoint new directors

• Convert to LLP

• Use of dependent relatives

CNK & Associates LLP

Chartered Accountants

Related Parties

[Sec 188 Chapter XII]

47CNK

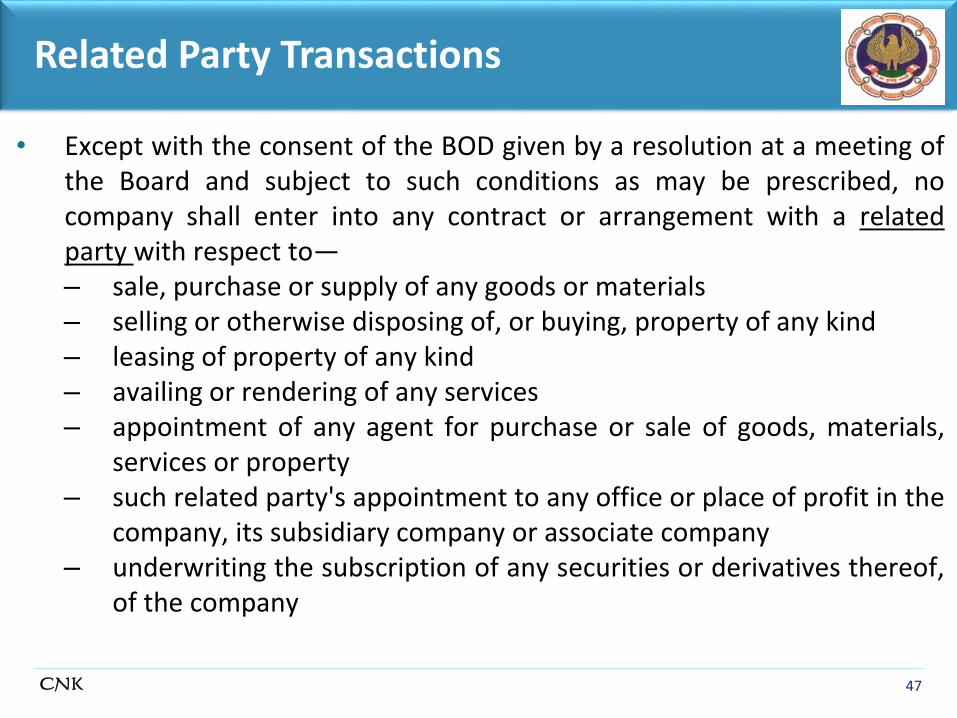

Related Party Transactions

• Except with the consent of the BOD given by a resolution at a meeting ofthe Board and subject to such conditions as may be prescribed, nocompany shall enter into any contract or arrangement with a relatedparty with respect to—– sale, purchase or supply of any goods or materials– selling or otherwise disposing of, or buying, property of any kind– leasing of property of any kind– availing or rendering of any services– appointment of any agent for purchase or sale of goods, materials,

services or property– such related party's appointment to any office or place of profit in the

company, its subsidiary company or associate company– underwriting the subscription of any securities or derivatives thereof,

of the company

48CNK

Section 2(76) related party” with reference to a company, means —

i. director or his relative;ii. KMP or his relative;iii. firm, in which a director, manager or his relative is a partner;iv. private company in which a director or manager or his relative is a

member or director ;v. public company in which a director or manager is a director and

holds along with his relatives, more than 2% of its paid-up sharecapital;

vi. any body corporate whose BoD, MD, or manager is accustomed toact in accordance with the advice, directions or instructions of adirector or manager;

Related Party

49CNK

Section 2(76) related party” with reference to a company, means —

vii. any person under whose advice, directions or instructions a director ormanager is accustomed to act;

viii. any company which is –i. a holding, subsidiary or an associate company of such company;ii. a subsidiary of a holding company to which it is also a subsidiary oriii. An investing company or the venturer of the company

the investing company or the venturer of a company - means a body corporate

whose investment in the company would result in the company becoming an

associate company of the body corporate

ix. such other persons as may be prescribed

Related Party

50CNK

Sec 2(51) - ‘‘key managerial personnel’’, (KMP) in relation to acompany, means –

– Chief Executive Officer or the managing director or the manager– company secretary– whole-time director– Chief Financial Officer; and– such other officer, not more than one level below the directors

who is in whole-time employment, designated as key managerialpersonnel by the Board; and

– such other officer as may be prescribed

Key Managerial Person

51CNK

Section 2(77) ‘‘relative’’, with reference to any person, means anyonewho is related to another, if—

■ (i) they are members of a Hindu Undivided Family;■ (ii) they are husband and wife; or■ (iii) one person is related to the other in such manner as may be

prescribed*;

*- Father, mother, son, son’s wife, daughter, daughter’s husband,brother, sister, (including step relations)

Relative

52CNK

Coverage of Relative

Cases of Relative Co. Act,

1956

Co. Act,

2013

IT Act,

1961

Cases of Relative Co.

Act,

1956

Co.

Act,

2013

IT Act,

1961

Members of HUF Yes Yes Yes Mother’s father Yes No No

Husband/Wife Yes Yes Yes Son’s son/ daughter Yes No Yes

Father (including

step-Father)

Yes Yes Yes Daughter’s husband Yes Yes Yes

Mother (including

step-mother)

Yes Yes Yes Son’s daughter’s husband Yes No No

Son (including step-

son)

Yes Yes Yes Daughter’s son Yes No No

Daughter (including

step-daughter)

Yes Yes Yes Daughter’s Son’s wife Yes No No

Son’s son’s wife Yes

Brother (including

step-brother)

Yes Yes Yes Daughter’s daughter Yes No No

Sister (including

step-sister)

Yes Yes Yes Daughter’s daughter’s

husband

Yes No No

Son’s Wife Yes Yes Yes Son’s daughter’s husband Yes No No

Father’s father Yes No Yes Daughter’s son’s wife Yes No No

Father’s mother Yes No Yes Brother’s wife Yes No Yes

Mother’s mother Yes No No Sister’s husband Yes No Yes

53CNK

Section 2(68) -“private company” means a company having a minimumpaid-up share capital of Rs.1 Lakh or such higher paid-up share capital asmay be prescribed, and which by its articles, -

i. Restricts the rights to transfer its shares;

ii. Except incase of one person company, limits the number of itsmembers to 200; and

iii. Prohibits any invitation to the public to subscribe for any securities

of the company.

Private Company

54CNK

Section 2(87)- “subsidiary company” or “subsidiary”, in relation to anyother company (that is to say the holding company), means a companyin which the holding company—

i. controls the composition of the Board of Directors; or

ii. exercises or controls more than one-half of the total voting powereither at its own or together with one or more of its subsidiarycompanies

Provided that such class or classes of holding companies as may beprescribed shall not have layers of subsidiaries beyond such numbers asmay be prescribed.

Subsidiary Company

55CNK

Sec 2(6) - ‘‘associate company’’, in relation to another company, meansa company in which that other company has a significant influence, butwhich is not a subsidiary company of the company having such influenceand includes a joint venture company.

Explanation.—For the purposes of this clause,a) “significant influence” means control of at least twenty per cent. of

total voting power, or of control of or participation in businessdecisions under an agreement;

b) the expression "joint venture" means a joint arrangementwhereby the parties that have joint control of the arrangementhave rights to the net assets of the arrangement;

Associate Company

56CNK

A transaction with a related party is

i. not in the ordinary course of business or

ii. is in the ordinary course of business but not on an arm’s length basis:

Prior consent of the BOD by a resolution at a board meeting and subject to such conditions as may be prescribed ;

Prior approval of the shareholders by a special resolution where paid-up capital of company or transaction amount exceeds prescribed limit;

• Not applicable to Government Companies* ,

• Not applicable to transactions between holding and its wholly owned subsidiary whose accounts are consolidated and placed before shareholders at the general meeting

Approvals for RPT

57CNK

Related party who is a member of such a company cannot voteon such a special resolution

• not applicable to Government Companies*, Specified IFSCPublic Company and Private Companies

• Shall not apply to a company in which 90% or moremembers , in numbers, are relatives of promoters or arerelated parties

Approvals for RPT

58CNK

• A company shall enter into any contract or arrangement with a related party subject to the following conditions, namely: The agenda of the Board meeting at which the resolution is proposed to

be moved shall disclose-• name of the related party and nature of relationship• the nature, duration of the contract and particulars of the contract or

arrangement;• the material terms of the contract or arrangement (incl. value)• any advance paid or received for the contract• the manner of determining the pricing and other commercial terms• whether all factors relevant to the contract have been considered, if not,

the details of factors not considered with the rationale for not considering those factors; and

• any other information relevant or important for the Board to take a decision on the proposed transaction.

Interested director not to be present during discussion

Prior Consent of BOD

59CNK

• Prior Approval of Members required for

a) contracts or arrangements with criteria as mentioned below-– sale, purchase or supply of any goods or materials, directly or through

appointment of agent, amounts to 10% of Turnover or Rs. 100 crorewhichever is lower.

– selling or otherwise disposing of, or buying, property of any kind ,directly or through appointment of agent, amounts to 10% of Networth or Rs. 100 crore whichever is lower.

– leasing of property of any kind amounts to 10% of Net worth or 10%of Turnover or Rs. 100 crore whichever is lower.

– availing or rendering of any services , directly or through appointmentof agent, amounting to 10% of turnover or Rs. 50 crore whichever islower.

The limits specified above shall apply for transaction or transactions to beentered into either individually or taken together with the previoustransactions during a financial year.

Prior Approval of Members

60CNK

• Prior Approval of Members required for b) appointment to any office or place of profit in the company, its

subsidiary company or associate company at a monthly remmunerationexceeding two and a half lakh rupees;

c) remuneration for underwriting the subscription of any securities orderivatives thereof, of the company exceeding one percent.of the networth

The turnover or net worth referred in the above sub-rules shall becomputed on the basis of the audited financial statement of the precedingfinancial year.

In case of wholly owned subsidiary, the 2[resolution] is passed by theholding companyshall be sufficient for the purpose of entering intothe transaction between the wholly owned subsidiary and theholding company

Prior Approval of Members

61CNK

The turnover or net worth referred in the above sub-rules shall becomputed on the basis of the audited financial statement of thepreceding financial year.

In case of wholly owned subsidiary, the resolution is passed by theholding company shall be sufficient for the purpose of enteringinto the transaction between the wholly owned subsidiary and theholding company

The explanatory statement to be annexed to the notice of ageneral meeting convened pursuant to section 101 shall containthe necessary particulars

Prior Approval of Members

62CNK

Section 188(2) - Board Report to contain mention of everycontract or arrangement entered with RP along with thejustification for entering into such contract or arrangement

• Section 188(3) - contract with RP without prior approval to beratified by BOD/general members within 3 months - else voidableat the option of the Board or, as the case may be, of theshareholders

• Section 188(4) - Company to recover loss against any such party in case of loss sustained due to contract

• Section 188(5) - Punishable offence with fine for listed co & other cos.

Other Provisions

CNK & Associates LLP

Chartered Accountants

Managerial Remuneration

[Sec 196-198 Chapter XIII]

64CNK

Section 2(78) defines remuneration as any money or its equivalent givenor passed to any person for services rendered by him and includesperquisites as defined under the Income-tax Act, 1961.

Section 197(1) – Total Managerial Remuneration payable to publiccompany (not applicable to Government Company or Specified IFSCPublic Company)

Total Remuneration paid to directors including MD + WTD + Manager<= 11% of the net profits computed in the manner laid down in Sec198 (remuneration shall not be deducted from gross profits)

Remuneration exceeding 11% can be given subject to authorisationby the company in general meeting and approval of the CentralGovernment - yet to be notified.

Managerial Remuneration

66CNK

Further, with the approval of the Company in general meeting by a specialresolution, the remuneration payable To any on MD, WTD or manager <= 5% and if there is more than one

such director , remuneration <=10%

To any directors who are neither MD, WTD or Manager <=1% if there isa MD, Manager or WTD

To any directors who are neither MD, WTD or Manager <=3% in anyother case.

Prior approval of the bank or public financial institution or the non-convertible debenture holders or other secured creditor shall be obtainedby the company before obtaining approval in the general meeting – yet tobe notified

Managerial Remuneration payable by Companies having adequate profits

67CNK

Percentages stated earlier shall be exclusive of Fees for attending meetings of the Board or Committee

–Sitting fees shall be the sum as may be decided by the Board ofdirectors thereof which shall not exceed one lakh rupees permeeting of the Board or committee thereof:

–Sitting Fees paid to Independent Directors and Women Directors,shall not be less than the sitting fee payable to other directors

Fees for any other purpose whatsoever as may be decided by theBoard

Managerial Remuneration payable by Companies having adequate profits

68CNK

In computing the net profits of a company in any financial year for the purposeof section 197,—

credit shall be given for the bounties and subsidies received from anyGovernment, or any public authority unless and except in so far as the CentralGovernment otherwise directs.

credit shall not be given for the following sums profits, by way of premium on shares or debentures of the company (unless

the company is an investment company as referred to in clause (a) of theExplanation to section 186] – not yet notified

profits on sales by the company of forfeited shares; profits of a capital nature including profits from the sale of the undertaking(s) profits from the sale of any immovable property or fixed assets of a capital

nature any change in carrying amount of an asset or of a liability recognised in equity

reserves including surplus in profit and loss account on measurement of the asset or the liability at fair value

any amount representing unrealised gains, notional gains or revaluation of assets- not yet notified

Calculation of profits under Section 198

69CNK

Following sums shall be deducted all the usual working charges; directors’ remuneration; bonus or commission paid or payable to any member of the company’s staff,

or to any engineer, technician or person employed or engaged by thecompany, whether on a whole-time or on a part-time basis;

any tax notified by the Central Government as being in the nature of a tax onexcess or abnormal profits;

any tax on business profits imposed for special reasons or in specialcircumstances and notified by the Central Government in this behalf;

interest on debentures issued by the company; interest on mortgages executed by the company and on loans and advances

secured by a charge on its fixed or floating assets; interest on unsecured loans and advances; expenses on repairs, whether to immovable or to movable property, provided

the repairs are not of a capital nature;

Calculation of profits under Section 198

70CNK

Following sums shall be deducted outgoings inclusive of contributions made under section 181; depreciation to the extent specified in section 123; the excess of expenditure over income, which had arisen in computing the net

profits in accordance with this section in any year 2[Omitted], in so far as suchexcess has not been deducted in any subsequent year preceding the year inrespect of which the net profits have to be ascertained;

any compensation or damages to be paid in virtue of any legal liabilityincluding a liability arising from a breach of contract;

any sum paid by way of insurance against the risk of meeting any liability suchas is referred to in clause (m);

debts considered bad and written off or adjusted during the year of account.

Calculation of profits under Section 198

71CNK

Where in any financial year - A company has no profits or its profits areinadequate, it may, without Central Government approval, payremuneration to the managerial person not exceeding, the limits specifiedas under :-

• Limits shall be doubled if special resolution passed by the shareholders

• For a period less than one year, the limits shall be pro-rated

Managerial Remuneration payable by Companies having nil or inadequate profits

Effective Capital Limit of yearly remuneration payableshall not exceed (Rupees)

i) Negative < Rs.5 crore 60 Lakhs

ii) >Rs. 5 crore <= Rs. 100 crores 84 Lakhs

iii) >Rs. 100 crores <= Rs.250 crores 120 Lakhs

iv) >Rs.250 crores 120 lakhs plus 0.01% of the effectivecapital in excess of Rs. 250 crores:

72CNK

• “effective capital” means the aggregate of the paid-up share capital(excluding share application money or advances against shares);amount, if any, for the time being standing to the credit of sharepremium account; reserves and surplus (excluding revaluation reserve);long-term loans and deposits repayable after one year (excludingworking capital loans, over drafts, interest due on loans unless funded,bank guarantee, etc., and other short-term arrangements) as reduced bythe aggregate of any investments (except in case of investment by aninvestment company whose principal business is acquisition of shares,stock, debentures or other securities), accumulated losses andpreliminary expenses not written off.

Managerial Remuneration payable by Companies having nil or inadequate profits

73CNK

• Central Government approval also not required if such managerial person (Professional Director)

– is functioning in a professional capacity

– possesses graduate level qualification with expertise and specialised knowledge in the field in which the company operates:

– is not having any interest in the capital of the company or its holding company or any of its subsidiaries directly or indirectly or through any other statutory structures and

– Does not having any, direct or indirect interest or related to the directors or promoters of the company or its holding company or any of its subsidiaries at any time during the last two years before or on or after the date of appointment

Managerial Remuneration payable by Companies having nil or inadequate profits

74CNK

• Limit specified on the basis of Effective Capital and for Professional Director above shall apply only if:

■The payment of remuneration is approved by Nomination and Remuneration Committee.

■The Company has not committed any default in repayment of any of any debts (including public deposits) or debentures or interest payable thereon for a continuous period of 30 days in the preceding financial year before the date of appointment of such managerial personnel.

■Special Resolution has been passed by the Company for payment of remuneration for a period not exceeding 3 years.

■Explanatory Statement along with Notice calling the general meeting shall contain prescribed information.

Managerial Remuneration payable by Companies having nil or inadequate profits

75CNK

A. Where the remuneration in excess of the limits specified in Section I or Section II can be paid to Managerial Personnel by following companies:

• Foreign Company

• Any other Company subject to following conditions –

– obtain the approval of its shareholders to make such payment;

– treats this amount as managerial remuneration for the purpose of section 197 and

– the total managerial remuneration payable is within permissible limits under section 197.

Managerial Remuneration payable in special Circumstances in case of nil or inadequate profits

76CNK

B. Managerial remuneration up to two times the amount permissible under Section II can be paid in following class of Company:

• Newly incorporated company, for a period of seven years from the date of its incorporation, or

• is a sick company, for which a scheme of revival or rehabilitation has been ordered by the Board for Industrial and Financial Reconstruction (BIFR) or National Company Law Tribunal (NCLT), for a period of five years from the date of sanction of scheme of revival, or

• Company in relation to which resolution plan has been approved by NCLT under Insolvency and Bankruptcy Code, 2016 for a period of 5 years from such approval.

Managerial Remuneration payable in special Circumstances in case of nil or inadequate profits

77CNK

C. Where remuneration of a managerial person exceeds the limits inSection II but the remuneration has been fixed by the BIFR or the NCLTsubject to certain conditions.

D. A company in a Special Economic Zone as notified by Department ofCommerce from time to time may pay remuneration up to Rs.2,40,00,000 per annum if it:

– has not raised any money through public issue of shares ordebentures in India, and

– has not made any default in India in repayment of any of its debts(including public deposits) or debentures or interest payable thereonfor a continuous period of thirty days in any financial year.

Managerial Remuneration payable in special Circumstances in case of nil or inadequate profits

78CNK

• Following perquisites not be included in the remuneration mentioned inSection II and Section III– Contribution to PF, Superannuation fund or annuity fund to the extent not

taxable under Income tax Act, 1961.– Gratuity payable at a rate not exceeding half a month’s salary for each

completed year of services; and– Encashment of leave at the end of tenure.

• In the case of Expatriate managerial personnel the following perquisite shall notbe included :

• Children’s education allowance of Rs. 12000 per annum per child or Actualexpenses incurred whichever is lower, subject to the maximum of 2 Children.

• Holiday passage for children studying outside India or family stayingabroadonce in a year by economy class or once in 2 years by first class tochildren and to the family members

• Leave travel concession: Return passage for self and family for spending leave inaccordance with the rules specified

Perquisites not included in Managerial Remuneration

79CNK

197(6) - A director or manager may be paid remuneration either byway of a monthly payment or at a specified percentage of the netprofits of the company or partly by one way and partly by the other.

197(7) - Notwithstanding anything contained in any other provision ofthis Act but subject to the provisions of this section, an independentdirector shall not be entitled to any stock option and may receiveremuneration by way of fees provided under sub-section (5),reimbursement of expenses for participation in the Board and othermeetings and profit related commission as may be approved by themembers

Other Conditions

80CNK

197(9) If any director draws or receives, directly or indirectly, by way ofremuneration any such sums in excess of the limit prescribed by thissection or without approval required under this section, he shall refundsuch sums to the company, within two years or such lesser period as maybe allowed by the company, and until such sum is refunded, hold it in trustfor the company. – yet to be notified

197(10) – Recovery of any sum refundable under Section 197(9) cannotbe waived unless approved by the company by special resolution withintwo years from the date the sum becomes refundable. - yet to be notified

Prior approval of the bank or public financial institution or the non-convertible debenture holders or other secured creditor shall be obtainedby the company before obtaining approval in the general meeting - yet tobe notified

Other Conditions

CNK & Associates LLP

Chartered Accountants

Dividends

[Sec 197-199 Chapter VIII]

82CNK

Dividend Declaration

No dividend shall be declared or paid by a company for any financial yearexcept

Out of the profits of the company for current year arrived at afterproviding for depreciation in accordance 123(2); or

Out of the profits of the company for any previous financial year oryears arrived at after providing for depreciation in accordance inaccordance with 123(2); or

Out of both;

Out of money provided by the Central Government or a State Government for the payment of dividend by the company in pursuance of a guarantee given by that Government.

Section 2(35) on Dividend – Dividend includes any interim dividend

83CNK

Provisions to be taken care of while ascertaining profits for distribution Provided that in computing profits any amount representing unrealised gains,

notional gains or revaluation of assets and any change in carrying amount ofan asset or of a liability on measurement of the asset or the liability at fairvalue shall be excluded; or

For the purposes of Section 123(1)(a), depreciation shall be provided inaccordance with the provisions of Schedule II.

Provided that a company may, before the declaration of any dividend in anyfinancial year, transfer such percentage of its profits for that financial year as itmay consider appropriate to the reserves of the company.

Provided also that no dividend shall be declared or paid by a company from itsreserves other than free reserves.

Provided also that no company shall declare dividend unless carried overprevious losses and depreciation not provided in previous year or years are setoff against profit of the company for the current year – effective 29th May 2015

84CNK

Dividend in case of Inadequacy or absence of profitsIn the event of inadequacy or absence of profits in any year, a company maydeclare dividend out of free reserves subject to the fulfillment of the followingconditions, namely:-

1. The rate of dividend declared shall not exceed the average dividend rate of immediately preceding 3 years. - Provided that this sub-rule shall not apply to a company, which has not declared any dividend in each of the 3 preceding financial

year.

2. Amount drawn from such accumulated profits <= 10% of the paid-up share capital + free reserves as appearing in the latest audited financial statement.

3. The amount so drawn in Point 2) shall first be utilised to set off current year losses

4. The balance of reserves after such withdrawal shall not fall below 15% per cent of its paid up share capital as appearing in the latest audited financial statement.

85CNK

Interim Dividend

• BOD can declare interim dividend

– during any financial year

– or at any time during the period from closure of financial year till holding of the AGM

– out of the surplus in the P&L

– or out of profits of the financial year for which such interim dividend is sought to be declared

– or out of profits generated in the financial year till the quarter preceding the date of declaration of the interim dividend:

• In case Company has incurred loss during the current financial year up to the end of the quarter immediately preceding the date of declaration of interim dividend, such interim dividend shall not exceed the average dividend rate of immediately preceding 3 years.

86CNK

Other Points

• The amount of the dividend, including interim dividend, shall be deposited in a scheduled bank in a separate account within five days from the date of declaration of such dividend.

– Not Applicable to Government Companies

• No dividend shall be paid by a company in respect of any share therein except to the registered shareholder of such share or to his order or to his banker and shall not be payable except in cash.

– No prohibition of capitalisation of profits or reserves of a company for the purpose of issuing fully paid-up bonus shares or paying up any amount for the time being unpaid on any shares held by the members of the company:

– Dividend payable in cash may be paid by cheque/ warrant / electronic mode

• If Company has failed to comply with provisions of Section 73 & 74 it cannot declare dividend on its Equity Shares till such failure continues.

87CNK

Unpaid Dividend

• Dividend not paid or claimed within 30 days from the date of thedeclaration shall, within 7 days from expiry of 30 days be transferred to aspecial account with any scheduled bank to be called the Unpaid DividendAccount.

• Statement containing details of unpaid dividend to be placed on theCompany website or any other web-site approved by the CentralGovernment within 90 days from transfer.

• Any default in making the transfer to Unpaid Dividend Account shall beliable to interest at the 12% p.a. and the interest accruing on such amountshall ensure to the benefit of the members of the company in proportionto the amount remaining unpaid to them.

88CNK

IEPF

• Any person claiming to be entitled to any money transferred under sub-section (1) to the Unpaid Dividend Account of the company may apply tothe company for payment of the money claimed.

• Amount lying in Unpaid Dividend + Interest Accrued + Shares in respect ofwhich dividend is not claimed shall after a period of 7 years from date oftransfer be transferred to the Investor Education and Protection Fund andthe company shall send a statement in the prescribed form of the details ofsuch transfer to the authority which administers the said Fund and thatauthority shall issue a receipt to the company as evidence of such transfer.

89CNK

IEPF

• Any claimant of shares transferred to IEPF shall be entitled to claim the transfer of shares from IEPF in accordance with such procedure and on submission of such documents as may be prescribed.

• Explanation.—For the removal of doubts, it is hereby clarified that in case any dividend is paid or claimed for any year during the said period of seven consecutive years, the share shall not be transferred to Investor Education and Protection Fund.

• Failure to comply with requirements of provisions

– Company shall be punishable with fine between Rs. 5 lakh – Rs. 25 Lakhs

– Officer of Company shall be punishable with fine between Rs. 1 lakh –Rs. 10 Lakhs