ceo briefing corporate priorities for...

TRANSCRIPT

CEO BriefingCorporate priorities for 2004

A report from the Economist Intelligence Unit

Sponsored by Dimension Data, HP, Nortel Networks and Oracle

© The Economist Intelligence Unit 2004 1

CEO Briefing Corporate priorities for 2004

CEO Briefing is an annual Economist IntelligenceUnit research programme designed to identify themanagement challenges that face the world’scorporate leaders. Dimension Data, HP, NortelNetworks and Oracle sponsor CEO Briefing.

The Economist Intelligence Unit bears soleresponsibility for the content of this report. TheEconomist Intelligence Unit’s editorial teamexecuted the online survey, conducted theinterviews and wrote the report. The findings andviews expressed in this report do not necessarilyreflect the views of the sponsors.

Our research drew on two main initiatives:● We conducted a wide-ranging online survey of

senior executives from around the world inDecember 2003. In total, 527 executives,including 112 chief executives, from 76countries took part.

● To supplement the survey results, theEconomist Intelligence Unit also conducted in-depth interviews with CEOs, CFOs, chairmenand other senior executives from majorcompanies in all of the world’s regions. Theobservations collected from these interviews—35 in all—cast brighter light on boardroomthinking about the insights yielded by thesurvey.

Andrew Palmer was the author of the report. Thefollowing researchers conducted interviews withexecutives around the world: Peter Baldwin,Jeanette Borzo, Rick Bullock, Wendy Cooper,Camilla Gallagher, Ben Gardner, Ross O’Brien,Alison Rea and Sara Yin.

Our thanks are due to everyone who sharedtheir time and insights during our research.

Preface

2 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

The global business environment is on the turn.Growth is upon us; earnings and share prices arepicking up. A global survey of senior executives,conducted especially for this CEO Briefing whitepaper, reveals much greater confidence at theoutset of 2004 than existed at the start of 2003.

But the lessons of the past three years havebeen well learned. Caution typifies the surveyresponses as much as confidence. Fewrespondents commit to robust growth in revenuesand profits this year; many remain preoccupied bycompetitive pressures and determined to root outfurther costs. This recovery will not be aneffervescent return to health but a slowrecuperation.

Among the key conclusions of the white paper arethe following:

The economic outlook for 2004 is reasonable;the longer-term picture is weak. The EconomistIntelligence Unit expects the world economy togrow by 4.2% in 2004, after expanding by anestimated 3.5% in 2003. But imbalances in the USand continued weakness in the euro zone andJapan represent significant concerns. Wheregrowth prospects are brighter—in China, forexample—the risks are proportionate. CEOs mustplan for continued economic fragility.

Globalisation is back. The most dynamic regionsof the world in the minds of survey respondents

are emerging markets in Asia and Eastern Europe.Outsourcing, particularly to overseas destinations,is an integral element of many companies’strategies. Technological advances continue tomake information-sharing across multiplelocations and time zones easier and safer. Andexecutives have been forced to become better atrisk management than they were.

Productivity is a critical watchword. Havingslaved to drive inefficiencies out of the business,nobody wants to lose the advantages of leanness.Companies will focus on keeping unit costs undercontrol even as they scale their activities back up.Suppliers hoping for a softer ride from theircustomers are likely to be disappointed.

Customers are turning into partners. Therelationship bit of customer relationshipmanagement is what really matters. Customerscontinue both to consolidate their supplier baseand to demand better service and more completesolutions. Businesses that actively involvecustomers in upstream product design and testingwill survive and thrive in this harsh environment.

The last downturn gave way to a period of firstsustained, and then unsustainable, growth. Thatpattern may yet repeat itself, but not if most oftoday’s corporate leaders can help it. CEOs haveacquired some hard-nosed habits over the pastthree years. Long may they be remembered.

Executive Summary

© The Economist Intelligence Unit 2004 3

CEO Briefing Corporate priorities for 2004

● Optimism has grown. Executives areconsiderably more optimistic about globalbusiness prospects this year than they wereat the start of 2003. Executives see the bestgrowth opportunities in Asia, with aparticular focus on China.

● Exuberance is strictly rational. Despite themore promising signs for 2004, the generalexpectation among respondents is formodest growth in revenues and profits,rather than for robust growth.

● Cost-cutting remains a priority. Worriesabout global political, financial andeconomic instability may have recededsince the last survey but competitivepressures remain intense—they pose thekey risk to respondents’ business. Loweringcosts remains a strategic priority as aresult.

● Outsourcing is mainstream. Outsourcinghas emerged as a key preoccupation forbusiness. More respondents identify it as acritical force in the global businessenvironment than any other.

● Governance is not a fad. Corporategovernance remains a major challenge for

executives, and concern is rising fast aboutnew regulations and a higher complianceburden.

● Financial services are set to rebound.Sentiment about financial services hasbrightened substantially compared withlast year’s survey. Private equity is an areawith particularly bright prospects.

● Technology is essential to growth. Only5% of respondents do not regardtechnology as essential or important.Improved sales and marketing has replacedreducing costs as the main aim oftechnology investment in this year’s survey.

● EU enlargement is a big deal. Respondentspicked the expansion of the EU from 15 to25 member states as the most importantscheduled event of 2004, ahead even of theUS presidential election.

● The customer remains king. Increasingcustomer satisfaction is once againrespondents’ top strategic priority.Building closer relationships with existingcustomers is regarded as the best way tomaximise growth opportunities.

Top findings from the CEO Briefing survey

4 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

Confidence and caution jostle atop thecorporate agenda for 2004. The optimistsapplaud the global economic recovery,rallying equity markets and improved

earnings. The pessimists frown at USmacroeconomic imbalances, competitive pressuresand regulatory burdens. Striking the right balancebetween these two sentiments will be the definingchallenge for CEOs over the coming months.

Both strains of thinking run through this year’sCEO Briefing, an annual Economist IntelligenceUnit survey and interview programme aimed atsenior executives around the world. Boardroomsentiment is noticeably more upbeat than lastyear—as 2004 begins, 76% of the 527 surveyrespondents regard the prospects for business asgood or very good, up from 61% twelve monthsago. Only 6% think prospects are bad or very bad,well down on the 17% of respondents who took asimilarly glum view of 2003.

But asked to rate their expectations for their owncompany’s performance in 2004, executives arewarier. Almost three in five expect only modestgrowth in revenues and profits this year; a further9% do not expect revenue growth at all but willcontinue to increase profitability through furthercost-cutting. The bottom of the cycle may havepassed, but there’s no place this time for the“irrational exuberance” that typified the late 1990s.

“Things are picking up and looking better,”agrees Esther Dyson, chairman of EDventure

Holdings and a noted technology commentator.“But it is not a question of ‘now we’re going to goback to the way it was’.” This will be a recoverystamped by the last three years of falling revenueand cost-cutting, of pension deficits andgovernance scandals, of changing regulations andgeopolitical turmoil. Like the grin (or should it befrown?) of the Cheshire Cat, the downturn willremain hanging over business long after theeconomy itself has improved.

How do you view the prospects for business in the globalmarketplace over the coming three years?

(% respondents)This year Last year

Very bad 1 1

Bad 5 16

Indifferent 18 22

Good 69 55

Very good 7 6

How well do you expect your company to perform in the 2004calendar year?

(% respondents)

We expect modest growth in revenues and profits 59

We expect robust growth in revenues and profits 26

We do not expect revenue growth but will deliver higher profits through continued cost-cutting 9

We expect a modest decline in revenues and profits 3

We expect a substantial decline in revenues and profits 1

Source: CEO Briefing survey, December 2003

Introduction

© The Economist Intelligence Unit 2004 5

CEO Briefing Corporate priorities for 2004

527 executives from 76 countries around theworld participated in this year’s CEO Briefingsurvey. The US and the UK provided the largestnumber of respondents, but a remarkablydiverse group of executives, based in locationsfrom Argentina to Vietnam, gave their views.

As well as being highly cosmopolitan, thesurvey group was very senior. Over one in fiverespondents was a CEO, up from 13% ofrespondents in the last survey; otherrespondents included 11 chairmen, 25 CFOs, 74directors and 45 senior vice-presidents.

A range of industries was represented—as inthe last survey, financial services, professionalservices, and telecoms and IT accounted for themost respondents. Participants also came froma spread of company sizes, with a thirdreporting annual revenues of over US$1bn.

Which of the following best describes your job?

(% respondents)

Chief executive 21

Director 14

Senior functional manager 10

Senior vice-president/vice-president 9

Business development manager 6

Director of strategic business unit 5

Chief finance officer 5

Regional manager 5

Chief marketing officer 3

Chief information officer 2

Chairman 2

Head of human resources 1

Other 18

Source: CEO Briefing survey, December 2003

Who took the survey?

6 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

“When all is said and done, I ammore optimistic about 2004than I was starting 2003,” saysMartin Glynn, the CEO of HSBC

Bank USA. Rightly so. The Economist IntelligenceUnit forecasts that world GDP growth (on apurchasing power parity basis) will average 4.2%in 2004, after expanding by an estimated 3.5% in2003. Latest data in many of the world’s largesteconomies suggest that growth has picked upsignificantly, with output in the third quarter of2003 rising at its fastest pace since early 2000.

In the US, economic growth has acceleratedmarkedly as tax cuts feed through into consumerdemand. Business investment is rising and jobcreation has at last resumed, albeit too sluggishlyto make a dent in the unemployment rate. Theeuro zone also seems to be recovering, with third-quarter GDP data showing that the recession seenin some countries in the first half of 2003 has cometo an end. Even the Japanese economy hasperformed far better than expected a year ago,

with GDP growth averaging an estimated 2.1% in2003.

The pick-up has already started feeding throughinto earnings, order books and share prices. MoreS&P 500 companies raised earnings estimates thanlowered them in advance of their fourth-quarterresults for 2003, the first time this ratio has beenpositive since 1999. Share prices in the world’smajor markets rose for the first time in four yearsin 2003. Increased levels of activity are visibleacross most industries. “We are seeing quite anuptick in rail volumes in almost all areas exceptautomobiles,” says Rob Ritchie from his vantage-point as CEO of Canadian Pacific Railway.

Asked to identify the industries that have thebest growth prospects over the next three years,cyclical industries are the big winners. True, surveyrespondents put a non-cyclical industry,healthcare and pharmaceuticals, at the top of thelist, just as in 2003, but its score has dropped from69% to 62%. Aerospace and defence, another non-cyclical industry, drops from second to ninth in thelist; food and beverages, a traditional safe havenduring hard times, also gets significantly fewervotes this year than last.

The stand-out performance is that of financialservices, one of the sectors hardest hit by thedownturn. This year, 49% of respondents pickedthe industry out as having excellent growthprospects, against just 29% in the previous survey.“The hangover from the technology andstockmarket bubble and from corporate bankingexcesses is pretty well gone,” says Mr Glynn atHSBC. “Most people are starting 2004 with a pretty

The global marketplace

Key points● The outlook for 2004 is reasonable; the

longer-term picture is weak● Cyclical industries are much better placed

now than they were 12 months ago● The dollar’s slide is set to continue and could

even accelerate● Excitement levels are greatest around China,

but the risks are proportionate

© The Economist Intelligence Unit 2004 7

CEO Briefing Corporate priorities for 2004

clean page.” The outlook for professional servicesfirms, the travel and tourism industry, and fortelecoms and technology is also brighter this yearthan it was in 2003.

Imbalancing actSo far, so encouraging. But with many of theworld’s largest economies still nursing significantdebt levels or other economic imbalances left overfrom the boom years of the late 1990s, therecovery carries with it significant risks. “Theglobal economy is on an upward trend”, says DavidGrigson, the finance director of Reuters, “but thereare fragilities.” Few are banking on a sustained,robust global recovery.

Although economic performance in the eurozone will continue to improve, our forecast ofaverage growth of 1.9% in 2004 is stilldisappointing. Labour markets remain weak,putting a brake on consumer spending growth.This is unlikely to change until investment picksup, which will take some time as many firms stillsuffer from excess capacity and high levels of debtfollowing the investment boom of the late 1990s.“There will be moderate economic growth, whichwill only improve slowly,” says Dr Ernst Wustinger,CEO of Pankl Racing Systems, an Austrian-headquartered supplier for high-end vehicles,aviation and motor racing. Further east, Japan’simpressive short-run performance will nottranslate into a sustained economic rebound—weexpect growth to slow to 1.3% in 2004.

It is in the US, the engine of global growth, thatthe risks are most concerning—one in every fivesurvey respondents rates it as the country thatpresents the greatest risks to their business. Evenassuming no significant widening of the war onterror, high US consumer debt will limit thewillingness of consumers to boost spendingaggressively. Looking further ahead to 2005, taxcuts will come to an end and monetary policy willalso be significantly tighter—we expect theeconomy to slow again that year, to 3.2% growth.

Meanwhile, the combination of a worryinglylarge current-account deficit and only moderatereturns on US investment has already prompted aslide in the value of the US dollar, and there is asignificant risk that the pace of dollar declinecould accelerate yet further. Breaking theUS$1.50:€1 barrier is a very real possibility. Thatwould dampen global growth, both by drivinginflation and interest rates higher in the US and bymaking life tougher for exporters trying to sell tothe US. Without hedging, it will cause particular

“It’s going to be arecovery, but not aboom, and it’s notgoing to be asprofitable a recovery asprevious cycles havebeen”Donald Brydon, chairman,AXA Investment Managers

Which industries do you believe enjoy the best growth prospects over the coming three years? (year-on-year change in % of respondents picking each industry)

Financial services +20

Professional services +8

Travel, tourism and transport +8

Electronic and electrical +7

Telecoms, software and computer +6

Construction and real estate +6

Automotive +6

Retailing +2

Leisure and entertainment +1

Agriculture +1

Utilities –1

Engineering and machinery –1

Mining, oil and gas –2

Chemicals and textiles –4

Healthcare, pharmaceuticals and biotechnology –7

Food, beverages and tobacco –10

Aerospace and defence –16Source: CEO Briefing survey, December 2003

8 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

trouble for overseas companies that are earning indollars. “We have to grow by 20% just to stayeven,” rails Mark White, CFO of SAP America, whoseresults are measured in euros back at SAP’sheadquarters in Germany.

But perhaps the worst effect of the slidingdollar is that it risks adding fuel to protectionistsentiment in the US. The combination ofsignificant job losses in the US economy over thepast few years, the forthcoming US presidentialelection, the large current-account deficit and theperceived undervaluation of Asian currenciesincreases the risk that trade protectionism willtake hold during 2004.

If so, China will be a prime target, because of amassive and rapidly rising trade deficit betweenthe world’s largest economy and its most populousone. The US has already imposed import quotas oncertain Chinese goods. Some Western companies(including a number from the US) with

manufacturing-for-export operations in Chinahave gone public to express their disquiet overgrowing US pressure on the Beijing government torevalue the yuan upwards.

China shinesWhether trade rival or offshoring destination,manufacturing base or consumer market, China’sshadow looms large over the survey results. A clearmajority of survey respondents select it as thecountry that offers their business its greatestgrowth opportunity. “Five years ago, our companyhad a debate on whether China would become ‘thecentre of the universe’,” says Peter Yin, vice-president of South Pacific operations for Fedex, aglobal logistics company. “The debate has sincebeen settled. Companies need to put their best andbrightest there, over-invest their capital and re-think their organisational structure to clearlyreflect a strong China bias. This is not to say put alleggs in one basket—just a lot more.”

Even those with no direct interest in the countrycan readily observe its influence. “What we arenoticing is the impact that China is having in theconsumption of commodities,” says Mr Ritchie atCanadian Pacific Railway. “We have been prettybusy taking coal, grain, sulphur and potash to thewest coast for export to China, and also busybringing import containers from China through thewest coast to eastern Canada and the midwesternand eastern US. We are getting a great boost fromChina.”

Yet China is clearly also prone to risk. “We areseeing our business there pick up but China is ahuge unknown,” says Marcelo Lemos, president ofDassault Systemes of America, a unit of a globalsoftware developer headquartered in Paris. “Thereis a tendency among Asian economies for thesaddle to slip off when they are riding hard,” warns

“To become a majorplayer in China, wehave to emphasisegrowth. To grow, wehave to take calculatedrisks”Paul Lau, country president,China, Novartis

Up, down (Real GDP growth; % change)

0

1

2

3

4

2003 2004 2005 2006

US

Euro zone

UK

Japan

Source: Economist Intelligence Unit

© The Economist Intelligence Unit 2004 9

CEO Briefing Corporate priorities for 2004

Of the events that are already in the calendarfor 2004, the enlargement of the EU from 15member states to 25 on May 1st is the one thatour survey respondents pick out as being mostsignificant for their business. The ten accessioncountries are Cyprus, the Czech Republic,Estonia, Hungary, Latvia, Lithuania, Malta,Poland, Slovakia and Slovenia.

Not that anything particularly dramatic willhappen that day. “We do not expect a stepchange as a result of enlargement,” says PeterKelly, president of Enterprise Networks in EMEAfor Nortel Networks, a networking services andinfrastructure firm. The new joiners have hadten years to ready themselves for accession. Themultinationals have put down deep roots, andthere is unlikely to be significant freshinvestment next year (though mid-marketinvestment flows should quicken). And becausethe accession countries are much poorer onaverage than the EU-15, the addition to theEU’s economic output will be small—total GDPwill rise by less than 5%.

But the absorption of the new members will

have several longer-term consequences.Purchasing power in the accession countrieswill rise and business environments willimprove. Procurement tenders will becomemore transparent and spending oninfrastructural projects will rise. Labour costsare likely to increase, as will competition. Inshort, swathes of Central and Eastern Europewill lose the tag of emerging markets.

Which of the following scheduled events in 2004 is likelyto have the biggest impact on your business?

(% respondents)

The eastward enlargement of the EU 38

The US presidential election 28

Conclusion of the Free Trade Area of the Americas (FTAA) talks 14

Iraq’s transition to democracy 7

EU decision on whether to start membership negotiations with Turkey 3

Presidential election in Russia 1

Other 9

Source: CEO Briefing survey, December 2003

Note: For a full discussion of the political, economic and business implications

of EU enlargement, Europe enlarged: Understanding the impact is available to

buy from the EIU’s Online Store at http://store.eiu.com.

Eastern promise

Rob Blain, CEO of CB Richard Ellis, a commercialproperty services firm, in Asia-Pacific.

Economically, the skin of a bubble may beforming: if investment in China continues to growrapidly and spare capacity continues to rise, there isa danger of a build-up of bad loans and an economicslowdown in future years as companies retrench.

Politically, tensions between China and Taiwan stillpreoccupy many executives—one Hong Kong-basedCEO sees the relationship between these twocountries as the greatest threat to his business.Within China, domestic social pressures will becomeever harder for the government in Beijing tomanage. Operationally, foreign firms are still

10 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

heavily constrained in what they can and can’t do,and the business environment is marred byinadequate infrastructure and a poor intellectualproperty regime.

China is not the only reason why the Asia-Pacific region was chosen by more respondentsthan any other as having excellent growthprospects. India’s time may—finally—be coming.William Padfield, the CEO of Datacraft Asia, an ITservices company headquartered in Singapore,thinks that Asian growth will be “supported by thetwin growth engines of India, for services, andChina, for manufacturing”. India comes third afterChina and the US as the market picked by surveyrespondents as offering the greatest growthopportunities. “There is considerable potential inthe Indian domestic market, provided regulatoryand legislative constraints are eased,” says OPLohia, managing director of Indo Rama Synthetics,the country’s largest dedicated polyestermanufacturer and exporter.

Which single country do you see as entailing the greatestrisk to your business over the next three years?

(% respondents; top five answers)

US 20

China 12

Iraq 5

UK 4

Russia 3

Source: CEO Briefing survey, December 2003

Which single country do you see as offering the greatestgrowth opportunity for your business over the next threeyears?

(% respondents; top six answers)

China 37

US 13

India 6

Russia 4

Brazil 4

UK 4

© The Economist Intelligence Unit 2004 11

CEO Briefing Corporate priorities for 2004

Twelve months ago, it was possible toconstruct a fairly cogent argument thatglobalisation was in trouble. Levels of FDIhad fallen, risk aversion had rocketed, costs

were under the microscope, and the attacks andconsequences of September 11th had encouragedmany to shrink their commercial horizons. In our2003 survey, geopolitical instability, financial andeconomic instability, and corporate governancepressures topped the list of critical forceschanging the global marketplace. This was hardlythe time for risky forays abroad.

If anything, the events of the past year shouldhave reinforced those worries. The outbreak ofSARS, the war in Iraq and its messy aftermath, andthe growing litany of terrorist incidents have allreinforced the message that this is an era foggedby uncertainty. Yet respondents’ worries aboutinstability have receded, if not disappeared;perceptions of risk in the Middle East and LatinAmerica have dropped significantly; and global FDIlevels are expected to climb again this year. In thelist of respondents’ strategic priorities for the nextthree years, globalising operations came third, upfrom sixth last year. Why?

Economic recovery clearly has something to dowith it. As boardroom thinking turns to growth,the opportunities for expansion posed byemerging and developed markets overseasnaturally come into sharper focus and investmentcapital becomes easier to find. But there are otherforces at work here too.

One is improved risk management. The surveyrespondents still recognise the threat of

Critical forces

“I’m not willing to be avictim of macro events.I always takeresponsibility for myown destiny” Lew Frankfort, CEO andchairman, Coach Inc

Key points● Worries about political, financial and

economic instability have receded● Outsourcing tops the list of critical global

forces● Governance pressures are here to stay● Corporate functions will be centralised,

operational ones decentralised

What are the greatest risks facing your company over the next three years? (year-on-year change in % of respondents picking each industry)

Tighter regulations and higher compliance burden +9

Increased competitive pressures +3

Failure to innovate +2

Macroeconomic and financial risk –5

Geopolitical risk –5

Difficulty attracting and retaining talent –8

Inability to respond quickly to changing market conditions –10Source: CEO Briefing survey, December 2003

12 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

geopolitical instability but they have had at leasttwo years to get used to it. “If there is dislocationor unrest in any of the countries in which weoperate, it could bring local operations to a halt.But this risk is mitigated by our diversegeographical footprint and we have goodcontingency plans,” says Kenneth Joyce, CFO ofAmkor, the world’s largest provider of contractsemiconductor assembly and test solutions. “So Idon’t lose any sleep over it.”

Another driving force, the most critical of all inthe eyes of the survey respondents, is the increasein outsourcing and, in particular, the relocation ofjobs overseas (a trend also known as“offshoring”).

Moving processes abroad is nothing new—companies have long parcelled out manufacturingjobs to locations elsewhere in the world. What’schanging is the nature of the jobs that are beingmoved. Increasingly, these jobs are higher up thevalue chain and based in the services sector;frequently, they are in customer contact roles.Forrester, a research group, claims that 3.3m white-collar American jobs (500,000 of them in IT) willshift offshore to countries such as India by 2015.

This is a fundamental deepening ofglobalisation, much of it enabled by advances intechnology that allow for data to be sharedsecurely and reliably across virtual networks, andfor employees, customers and partners tocommunicate seamlessly across multiple locationsand time zones.

Outsourced, not out of mindOutsourcing is not the answer to every problem, ofcourse. Even if the overall outsourcing trend isclear, the details are highly specific. Sometimesjobs are moved to different geographicaldestinations within the same company—an

approach HSBC calls global resourcing. Sometimesthey are taken over by another company.Sometimes functions are outsourced within thesame country and sometimes they are shuntedhalfway around the world. Some pundits seeregional outsourcing chains emerging, with Chinaand India being the offshore location of choice forAsian companies, Eastern Europe fulfilling thesame role for the EU and Latin America importingthe bulk of US jobs.

Pragmatism is critical. Executives must, forexample, make critical decisions on whichfunctions, if any, should be outsourced in the firstplace and which are core to the business. IT, HRand logistics are the areas where the surveyrespondents are most receptive to outsourcing.They tread more warily in areas such as finance andaccounting, customer contact roles, and researchand development.

Thomas Cook, one of the UK’s largest travelcompanies, has already gone further than most insuccessfully outsourcing its finance, IT and HRfunctions, mainly with Accenture. According to IanAilles, who is managing director of the firm’sspecialist businesses and oversees outsourcing forthe company as a whole, “We continue to look atways in which we can continually make ourbusiness more effective and cannot rule out

“Outsourcing non-corecompetencies hasbecome an establishedway of doing businessbut is not always thepanacea that peoplethink it is. It willcontinue to have merit;it won’t go away, but itwon’t end everything aswe know it” John Morphy, CFO, Paychex

Which functions does your company have no plan tooutsource? (% respondents saying no plan to outsource overnext three years)

R&D 87

Finance and accounting 72

Customer contact roles 72

Manufacturing 70

Logistics 59

IT 49

Payroll 47

Source: CEO Briefing survey, December 2003

© The Economist Intelligence Unit 2004 13

CEO Briefing Corporate priorities for 2004

further co-sourcing activities. However, given thatwe are in a service industry we will not makeoperational cost-saving decisions that are not inthe best interest of meeting our customers’needs.”

For Mr Ailles and others, cost is by no means theonly input into sourcing decisions. ChevronTexaco, a global energy company, is planning tooutsource the development and maintenance ofsome software to India in the coming months. “Ina global business, you can’t continue to developand maintain software only in the US,” saysHelmut Porkert, the company’s chief procurementofficer. But Mr Porkert is looking at far more thanjust price when making his sourcing decisions: “Weneed to look at where we can get best operationalexcellence and where we can get the best service,as well as the lowest total cost.”

Elisabetta Bigsby, head of strategic planningfor RBC Financial Group, Canada’s largestcompany, agrees: “Outsourcing to a low-costprovider is not necessarily the right solution. I’dsuggest a better way is to constantly look at yourend-to-end process and find an optimal way ofdelivering that process. Offshore may be acomponent of that or the whole of it at some point,but low cost is not the solution per se.”

That’s particularly true of a world wherecustomers want better quality and improvedservice, as well as lower prices. In 1996 Coach, anupscale US accessories maker, manufactured over96% of its output directly through company-ownedfactories. Now that proportion is down to less than1%. “Even though we have outsourced it”, says LewFrankfort, the company’s CEO and chairman, “weare very control-oriented. To maintain and evenstrengthen quality standards, we provide all theraw materials to our factories. And we havepermanent inspectors and trainers in all of our key

factories so that the quality is nevercompromised.”

The governance imperativeJust as outsourcing cannot compromise quality, soit must not jeopardise corporate governance.Operational control can be outsourced butregulatory responsibility cannot, and in thisenvironment, that’s no small consideration.Although some regard the preoccupation withgovernance as a fad, market pressures to improvegovernance remain a significant force in globalbusiness.● “I find it sad that good corporate governance

has become the new mantra,” says Mr Joyce atAmkor. “We were all supposed to have goodcorporate governance.” Despite his sense ofdisappointment, not every bad apple has yetbeen found out—witness the current travails ofParmalat, an Italian food company. Companiesin emerging markets face a particularly steeplearning curve to bring their managementprocesses up to scratch.

● Shareholders are starting to find their voice,particularly in challenging the more lavishremuneration packages. GlaxoSmithKline wasforced to scrap two-year rolling contracts forexecutive directors in the face of a shareholderrevolt; it won’t be the last to beat a retreat onpay. Implementing performance-relatedcompensation, which rewards relative successrather than absolute numbers, will be aparticular focus of remuneration committees.

● The regulatory changes that the governancegale blew in have added a non-negotiablecompliance burden in the US and elsewhere.“Becoming compliant is taking up a lot ofeffort,” says Mr Ritchie at Canadian PacificRailway. “The cost of auditors is up

“There are a lot of corebusiness benefits thatcan be had if you take aholistic view ofgovernmentregulations oncorporate governance”Pete Fiore, president,Ascential SoftwareCorporation

14 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

Blending a renewed focus on globalisation andgrowth with a continued emphasis ongovernance is no easy task. On the one hand,local units must be given the flexibility to seizeopportunities in their own markets. “In the pastthree years, we focused on strengthening ourcontrol and tightening corporate governance.But in the next three years we will push forgreater flexibility and networking, simplybecause we’re getting ready to grow,” says TerryCheng, managing director of LucentTechnologies in Asia.

On the other hand, there is the need tomaintain effective control of the business.“Decision-making will become morecentralised,” says David Grigson, financedirector at Reuters, whose structure hashistorically been very fragmented. “We aresimplifying the business model on a smallernumber of services.”

These competing imperatives seem to comethrough in the survey, with two in every fiverespondents expecting a move towards greatercommand and control in their organisation overthe next three years, but one in every fourexpecting a shift in the opposite direction.

In reality, the ebb and flow of centralisationand decentralisation is likely to take place withincompanies as well as across them, as certainfunctions become more tightly managed andothers are devolved. (Outsourcing,

interestingly, is hard to pigeonhole—is itcentralisation or not?) “You want to centralisebut you also want to be closer to your markets,”says Jaap Monte, chief operating officer ofGroenewout Consultants & Engineers, aEuropean supply chain consultancy. “Corporatefunctions you can centralise, such as finance andplanning. Sales and marketing, those kinds ofthings, will move closer to the end-customer.”

Certainly, awareness of the need forcompanies to be sensitive to local culturalconditions seems to have risen in the past fewyears. “Countries and markets will continue tobe different,” says Carlo Secchi, dean ofBocconi University in Milan. “We must learn tolive side by side, and I see this as beingfundamental to business operations as well.” MrMonte agrees: “There will be a shift ofmanagement control to the lower levels, to beable to be more flexible and responsive tomarkets.”

How will your corporate organisation change over thenext three years?

(% respondents)

There will be a move towards greater command and control 42

There will be no change 34

There will be a move away from command and control 24

Source: CEO Briefing survey, December 2003

Control and delegate

© The Economist Intelligence Unit 2004 15

CEO Briefing Corporate priorities for 2004

substantially just to be [Sarbanes-Oxleysection] 404-compliant. Then you have to hirepeople to articulate and write up all thebusiness processes around the internalcontrols of the company so you can sign off.” Ahigher compliance burden jumps up the list ofkey business risks in this year’s survey.

But improving governance has its upside. For someIT vendors, it represents a significant salesopportunity—Mr White, CFO at SAP America, citescompliance with Sarbanes-Oxley and other lawsand regulations as one of the reasons he is hopefulof increased expenditure on IT in 2004.

More importantly, overhauling governance can

drive changes in the way that business is done.Better management controls lead to more accuratedata that can be used to get a firmer handle on theway the business is going. An EconomistIntelligence Unit survey conducted in the summerof 2003 found that a majority of respondentsbelieve senior managers have a better grasp of thebusiness realities within their company as a resultof the governance focus. George Rose, CFO at BAESystems, a £12bn systems company, can also seethe advantages of the governance trend: “There’sa heightened appreciation of and attention to risk.Making people think through risk is a nice balanceto having over-optimistic managements.”

16 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

Governance and outsourcing are largelylegacies of the past five years, one areaction to the excesses of the boom, theother prompted by the cost-cutting

imperative of the downturn. There are otherlegacies, too. Lowering costs remains the second-highest strategic priority for survey respondents—behind increasing customer satisfaction—just as itwas last year.

Of course, cost-cutting alone doesn’t producegrowth. “Organisations have scaled back theiractivities, cut their discretionary budgets andtherefore don’t have the product offering to takefull advantage of the recovery,” says Mr Grigson atReuters. Product innovation will inevitably moveup the corporate agenda. But this recovery, fragileas it is, will be as much about memorising the hardlessons of the past as it will be about embracingthe opportunities of the future.

So forget a return to the wild expansionism ofthe 1990s. For one thing, the fastest way to grabmarket share, mergers and acquisition activity, isunappealing to many—survey respondents placefar more emphasis on alliances than M&A as a

means of driving growth. For another, manycompanies are still too highly leveraged. Amkor’sdebt is around 75% of its total marketcapitalisation, for example, and the company’saim is to get this down to the 25-30% range. Anequity offering in late 2003 raised US$140m to paydown debt. According to Mr Joyce, the firm’s CFO,“We are hoping—if the market conditions arethere—to do some additional equity raising toreduce debt in 2004.”

More than one in three surveyed companies hasno plans to raise capital at all in the next threeyears. Of those that are, few are looking to theequity markets for funding—bank financing is themost popular avenue, closely followed by privateequity investment. Here is evidence for anotherlegacy of the boom and bust. Going private isn’tfor everyone, but disenchantment with the short-termism of equity markets, allied to the risingcompliance pressures of public ownership, seemsto have grown. “Because we’re private, we cantake a slightly longer view,” says John Fry, CEO forArchant, a family-owned UK newspaper group.“And we can talk directly to shareholders whoactually own the company. When you talk toanalysts, they’re just people who are analysingyou, and when you go to fund managers, they’restill managing other people’s money.”

Weight on gainsPrivate or public, companies are determined thatthe focus on growth will not be allowed tocompromise the gains in efficiency that have beenrealised over the past three years. SunTrust Banks,

Corporate strategies

Key points● Companies will focus on retaining the

efficiencies and productivity gains of the pastthree years as they scale back up

● Relationships with customers will deepen andmove upstream to product design and testing

● Employee retention will be a significantchallenge as the jobs market heats up again

© The Economist Intelligence Unit 2004 17

CEO Briefing Corporate priorities for 2004

a banking group operating primarily in the south-east of the US, has cut staff and production costsby about 20% over the past two years, and addedcosts of about 5% in customer-facing areas of thebusiness. “We have pared back and become muchmore efficient in our operations and more investedin outreach,” says John Spiegel, the company’sCFO. “Now the challenge is to leverage thatstructure to take full advantage of it.”

In an ever more competitive businessenvironment, productivity will be the watchwordas companies scale back up. “We’re quite happy tosee our absolute costs rise, as long as revenues arerising as well,” says Donald Brydon, chairman ofAXA Investment Managers, part of France’s AXAGroup. “It’s unit costs that matter to us.” “Themaximisation of efficiencies is not just aboutcutting costs but about ensuring that the cost

base, once fundamentally reshaped, is trulyscaleable,” agrees Mr Grigson at Reuters.

Nor will companies cease their search for newefficiencies. “There is a recognition that we haveto be able to do more with less,” says Mr Kelly atNortel Networks, whose company is generatingmore data traffic than ever despite losing 60% ofits staff. Over at Chevron Texaco, Mr Porkert, thechief procurement officer, is implementing a newe-procurement system that currently handlesUS$2bn-worth of company spending. That figure isset to rise to US$10bn in 2004. He is also chasingUS$200m-worth of annual savings in the supplychain by reducing idle inventory.

When incremental spending does take place,particularly on technology, it will have to clearsome high hurdles first. “Six months ROI withmeasurable benefits is the new yardstick,” saysDatacraft Asia’s Mr Padfield. “Improved efficiencyis not sufficient to justify investment. There has tobe a measurable ROI.”

For those vendors and suppliers who are hopingthat recovery will mean an automatic let-up inpricing pressures, disappointment looms. Intensecompetition will help keep inflation under control.Growth in margins will depend instead onbecoming a preferred partner, ever more tightlyembedded within enterprises’ supply chains andmeeting customer needs on a bespoke basis.

According to Jim Simmons, CEO of SungardAvailability Services, a provider of informationavailability services, “We have wiser, brighterconsumers who are tending to consolidate their ITchoices to fewer vendors but asking for morecomplete solutions.” Pete Fiore, president ofAscential Software, a US-based data integrationservices provider, concurs: “Customers are lookingfor smaller numbers of partners, partners withstaying power.”

What are your company’s strategic priorities over the next three years?

(% respondents; respondents allowed to choose no more thanthree priorities)

Increasing customer satisfaction 47

Lowering costs and maximising competencies 45

Globalising operations 28

Fostering innovation 25

Improving quality 24

Should your company need to raise capital in the comingthree years, which route are you most likely to use?

(% respondents)

We will not raise capital in the next three years 26

Bank financing 21

Private equity investment 19

We will dip into reserves instead 11

Corporate bond 10

IPO/share issue 9

Sale of assets 3

Other 2

Source: CEO Briefing survey, December 2003

“Success is about beingvery customer focused.It is all about customerdelivery. It is abouteach and every one ofyour employeesbelieving in thecustomer”Ian Ailles, managingdirector, specialistbusinesses, Thomas Cook

18 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

It’s the customer, stupidIt is in this context of consolidation andcustomisation that respondents’ focus on thecustomer needs to be placed. Increasing customersatisfaction may seem like a pretty hackneyedpriority, but it’s no less important for that. “It ismore evident that the view of customers as assetsis becoming part of the boardroom agenda—afterall, that’s where the cashflows are coming from,”says Tomas Forsgård, senior vice-president forstrategy and performance at Kemira, aninternational chemicals company withheadquarters in Finland. Reuters reorganised itselfat the end of 2001, for example, to shift its focusaway from geography and onto customersegments. “Customer-segment people havedeeper insight into what the customer’s needsare,” says Mr Grigson.

Partnerships between suppliers and customerswill move upstream, to collaboration on productdesign and testing. Chevron Texaco is workingwith key suppliers to drive out costs, for example,by involving selected partners in the early phasesof equipment design. Amkor’s engineers workdirectly with customers’ engineers to ensure thatmeasures to reduce manufacturing costs do notadversely affect quality. Mr Blain of CB RichardEllis in Asia, who is also in charge of the firm’sglobal CRM initiative, is focusing relentlessly onunderstanding the needs of, and selling more to,the firm’s top 30 clients.

Partnerships will deepen in distribution andretailing, too. Continental, a German tyremakerand automotive components giant, works to bindindependent tyre dealers into the brand, forinstance, by giving them advice on how to managetheir dealer stores. “We bring in a new customerfocus to supply chain management,” says Dr AlanHippe, Continental’s CFO. Alessandro Profumo,

CEO of UniCredito Italiano, Italy’s largest bankinggroup, aims to use close, personal relationshipswith clients to achieve the bank’s goals, in retailmarkets as well as corporate ones: “Our target is toprovide highly customised services, consolidatingour leadership and exploiting the competitiveadvantage arising from specialisation.”

Technology bubbles againThe approaches above re-emphasise the humandimension of customer interaction. “The ability tosit down with clients and actually listen to whatthey need is crucial,” says Ms Bigsby at RBCFinancial. But the survey respondents also see acentral role for technology in improving customerrelationships.

Whereas in 2003 lower costs were the primarygoal of technology investment, this year improvedsales and marketing is the area where the greatestbenefits are anticipated. In part, that reflects ageneral shift in focus from costs to revenue, fromthe back- to the front-end. But it also reflects theemergence of new Internet Protocol (IP) networksolutions that can deliver the right data to theright people at the right time.

“Many previous CRM deployments failedbecause they weren’t properly integrated,” says MrKelly at Nortel Networks. “But converged IP

“Technology does notdifferentiate anymore—it’s the valueproposition thatcounts”Brett Dawson, chiefoperating officer, DimensionData

In which areas of the business do you expect to see thegreatest benefits from your investment in technology overthe next three years?

(% respondents; respondents allowed to choose as many asapply)

Improved sales and marketing 55

Improved knowledge management 51

More successful customer relationship management 46

Lower costs 45

Enhanced back-office systems and networks 45

Source: CEO Briefing survey, December 2003

© The Economist Intelligence Unit 2004 19

CEO Briefing Corporate priorities for 2004

solutions are ready for primetime and are going inright now.” This could be the year when CRMsolutions lose their “money pit” tag and regainrespectability.

What goes for CRM also applies to technology ingeneral. Ninety-five per cent of surveyrespondents regard technology as essential orimportant to their business goals, and advances intechnology and the Internet rank as the secondmost important force in the global businessenvironment. As well as CRM, here are four otherareas where technology is enabling criticalchanges to the way business is done.● Network security. Asked to choose the ways inwhich their company structures will change overthe next three years, survey respondents plumpedfor the faster, wider sharing of information and for

the increasing importance of alliances. Put simply,ever more data are being shared with ever morepeople, and the importance of network security isrising as a result. Technology is not the onlyanswer to security issues but it is an essentialenabler. ● Remote working. Remote working is sharplyon the rise, as telecommuters find it just as easy toplug into the network at home as in the office.Survey respondents rank the increasing flexibilityof working practices third highest in the list oflikely changes to company structures. The growingtake-up of broadband in people’s homes, thedevelopment of wireless hotspots and thematuring of network security solutions are allhelping to drive this change in working patterns.● Online transactions. “E-commerce”, a quaint

A sharper focus on customers must not come atthe expense of employees. Among thechallenges that a growth environment will posewill be that of retaining talent in a moredynamic jobs market. “As the recovery picks up,a significant challenge will be to manageemployee stability,” says William Padfield, CEOof Datacraft Asia. “In the IT industry especially,as demand for certain skills rises, it will becomedifficult to retain key personnel once again.”

The war for talent is being fought in emergingmarkets as well as developed ones. “Should acompany not be able to refresh its humanresource talent, no amount of technologyinfusion can protect it from stagnating,” warns

Ashwinni Bajaj, CEO of The Amrit Group, one ofIndia’s leading processors of edible oil.

Employers must be ready to act, and not justby improving compensation schemes. Moreflexible working practices is one area in whichemployers are increasingly able to satisfy staffdemands. Training is also central. “We doregular employee surveys,” says David Dupont,CFO of Pennon Group, a UK utilities group.“Employees tend to be most concerned aboutmaximising the value of training anddevelopment. We have therefore put increasingfocus on ensuring that the training programmesthat we provide are appropriate to the needs ofthe business and of the individual.”

Don’t forget your own

“People management isa fundamental successfactor in the creation ofbig internationalgroups and dependsabove all on the abilityto retain recognisedtalent, attract newtalent and nurture allpotential new talent”Alessandro Profumo, CEO,Unicredito Bank

20 © The Economist Intelligence Unit 2004

CEO Briefing Corporate priorities for 2004

phrase from the dotcom era, is reaching a newlevel of maturity as consumers find it ever easier tobuy online. According to Giancarlo Cimoli, CEO ofFerrovie dello Stato, Italy’s largest railwaycompany, 6-7% of the firm’s ticket sales arealready transacted via the Internet and callcentres, and that proportion is set to increase. ● Supply chain management. Technology hasalready had a huge impact on the efficiency ofsupply chains, and radio frequency identification

(RFID), a technology that acts like a kind of talkingbarcode, is about to make processes even leaner.Bill Bass, whose hats include running e-commerceoperations at Lands’ End, a direct clothingmerchant, looks forward to the day when RFIDtechnology is widely used in retail stores:“Customers are going to begin to expect Internet-level intelligence from point-of-sale systems. Atthe item level, self check-out becomes viable andcan change the retail experience.”

The cusp is a difficult place to be. Should CEOs seize themoment and make acquisitions while capital remainsrelatively cheap? Should they focus on further efficiencies inthe knowledge that any recovery will be fragile? “One of thebiggest challenges is going to be how to rein in enthusiasmand become growth-oriented in a controlled manner, whereyou very methodically analyse your prospects and invest inpriority areas,” says John Spiegel, CFO of SunTrust Banks.

No surprise therefore that, asked to identify the qualitiesthat will be most important in leaders of global companies inthe coming months and years, respondents put strategicvision out in front.

Next on the list comes communication and people skills,more important than ever in an environment where investorsdemand unprecedented transparency and talentedemployees need to be inspired. Striking a balance betweenlong-term goals and short-term results is critical, too—investors may want their companies to be unimpeachable interms of governance but CEOs remain under the samepressure to deliver quarter by quarter. And with recoveryupon us and globalisation back in vogue, cross-cultural skills

and innovativeness are also reckoned essential.What isn’t needed is a high public profile, bottom of the

list of leadership attributes that our respondents thinkimportant. Not that humility is particularly valued either.Profile, high or low, is irrelevant—results are what count.

What leadership qualities will be required to manage a global company inthe future?

(% respondents; respondents could choose no more than three qualities)

Strategic vision 63

Excellent communication and people skills 49

A balance between long-term goals and short-term results 43

International knowledge/ability to manage across cultures 38

Innovativeness/openness to new ideas 35

Deep knowledge of market needs and operations 34

Honesty and integrity 30

The ability to manage risk without stifling entrepreneurialism 24

A good understanding of technology 13

Humility/low public profile 5

High public profile 4

Other 1

Source: CEO Briefing survey, December 2003

Strategists needed, not celebrities

© The Economist Intelligence Unit 2004 21

CEO Briefing Corporate priorities for 2004

The battle between caution and confidence thatruns through this year’s CEO Briefing survey doesnot have a clear-cut victor. Companies areexpecting growth and are less preoccupied by risksof economic and political turmoil. Investment intechnology is no longer so geared to cost-cutting.There’s particular buoyancy around certainmarkets, such as China, and industries, such asfinancial services.

But the pressures that have been exerted onexecutives over the past three years are, ifanything, intensifying. Competition remainsbrutal. Customers are asking for better servicefrom fewer suppliers. Productivity gains will noteasily be sacrificed. Margins will remain tight.

Above all, change will be the only constant.“You need to be restless and continue to evolveyour business model and your business asconsumers evolve,” says Mr Frankfort at Coach.“You must be nimble, agile and have a culture thatembraces change.” Mr Joyce, Amkor’s CFO, is inwhole-hearted agreement: “You can’t be afraid ofchange. That is a crucial mindset.”

Conclusion

22 © The Economist Intelligence Unit 2004

Appendix: Survey results

527 respondents from a total of 76 countriesparticipated in the survey, which was administeredonline in December 2003. Our sincere thanks go toeveryone who took part in the survey.

Please note that not all answers add up to 100%,because of rounding, because respondents wereable to give multiple answers to one question, orbecause a selection of top answers is given.

Demographics

In which country are you located?

(% respondents; top twelve countries)

US 20

UK 16

Australia 6

Singapore 5

India 4

Canada 4

China 3

Spain 3

Brazil 3

Japan 2

Hong Kong 2

Germany 2

Which of the following best describes your job?

(% respondents)

Chief executive 21

Director 14

Senior functional manager 10

Senior vice-president/vice-president 9

Business development manager 6

Director of strategic business unit 5

Chief finance officer 5

Regional manager 5

Chief marketing officer 3

Chief information officer 2

Chairman 2

Head of human resources 1

Other 18

© The Economist Intelligence Unit 2004 23

Appendix: Survey resultsCEO Briefing

Corporate priorities for 2004

What industry are you in?

(% respondents)

Financial services 23

Professional services 17

Telecoms, software and computer services 12

Travel, tourism and transport 4

Leisure, entertainment, media and publishing 4

Electronic and electrical equipment 4

Consumer goods 3

Healthcare, pharmaceuticals and biotechnology 3

Chemicals and textiles 3

Mining, oil and gas 3

Food, beverages and tobacco 2

Engineering and machinery 2

Automotive 2

Construction and real estate 2

Retailing 2

Utilities 2

Aerospace and defence 1

Agriculture 1

Other 12

What are your company's annual revenues in US dollars? (% respondents)

Less than US$500m 55

US$500m to US$1bn 11

US$1bn to US$3bn 10

US$3bn to US$8bn 6

More than US$8bn 13

Not applicable 5

24 © The Economist Intelligence Unit 2004

Appendix: Survey resultsCEO Briefing Corporate priorities for 2004

The global marketplace

What are the critical forces changing the global marketplace over the coming three years?

(% respondents; respondents allowed to choose as many as apply)

Increased outsourcing and offshoring 51

Advances in technology and the Internet 48

Heightened geopolitical instability 46

Customer pressure for greater quality, cheaper products and improved service 46

Worldwide economic recovery 44

Market pressures to improve corporate governance 41

Global economic and financial instability 40

Increased competition 40

Shifting relationships between competitors, partners and customers 39

Opportunities from the opening up of new global markets 37

Pressure for improved performance from investors and shareholders 34

Impact of expanding regional trading blocs 30

The emergence of new business regulations 29

A political and regulatory backlash against globalisation 18

Other 8

How do you view the prospects for business in the global marketplace over the coming three years? (% respondents)

Very good 7

Very bad 1

Bad 5

Indifferent 18Good 69

© The Economist Intelligence Unit 2004 25

Appendix: Survey resultsCEO Briefing

Corporate priorities for 2004

Which region or regions do you see as offering the greatest growth opportunities for your business over the next three years?

(% respondents; respondents allowed to choose as many as apply)

Asia-Pacific 69

Eastern Europe 37

North America 27

Western Europe 25

Latin America 20

Middle East and North Africa 9

Sub-Saharan Africa 6

Which single country do you see as offering the greatest growth opportunity for your business over the next three years?

(% respondents; top six answers)

China 37

US 13

India 6

Russia 4

Brazil 4

UK 4

Which region or regions do you think entail the greatest risks for your business over the next three years?

(% respondents; respondents allowed to choose as many as apply)

Middle East and North Africa 33

Asia-Pacific 27

North America 25

Western Europe 19

Latin America 19

Sub-Saharan Africa 15

Eastern Europe 14

Which single country do you see as entailing the greatest risk to your business over the next three years?

(% respondents; top five answers)

US 20

China 12

Iraq 5

UK 4

Russia 3

26 © The Economist Intelligence Unit 2004

Appendix: Survey resultsCEO Briefing Corporate priorities for 2004

Which industries do you believe enjoy the best growth prospects over the coming three years?

(% respondents; respondents allowed to choose as many as apply)

Healthcare, pharmaceuticals and biotechnology 62

Financial services 49

Professional services 39

Telecoms, software and computing 39

Electronic and electrical 37

Leisure and entertainment 34

Consumer goods 29

Travel, tourism and transport 28

Aerospace and defence 24

Construction and real estate 23

Mining, oil and gas 16

Retailing 14

Utilities 13

Automotive 13

Agriculture 12

Chemicals and textiles 12

Food, beverages and tobacco 11

Engineering and machinery 11

Other 3

Which of the following scheduled events in 2004 is likely to have the biggest impact on your business?(% respondents)

The eastward enlargement of the EU 38

The US presidential election 28

Other 9

Presidential election in Russia 1

EU decision on whether to start membership negotiations with Turkey 3

Iraq’s transition to democracy 7

Conclusion of the Free Trade Area of the Americas (FTAA) talks 14

© The Economist Intelligence Unit 2004 27

Appendix: Survey resultsCEO Briefing

Corporate priorities for 2004

What are your company’s strategic priorities over the next three years?

(% respondents; respondents allowed to choose no more than three priorities)

Increasing customer satisfaction 47

Lowering costs and maximising competencies 45

Globalising operations 28

Fostering innovation 25

Improving quality 24

Accelerating time-to-market 24

Refining corporate organisation and culture 22

Upgrading internal controls and risk management 21

Striving for market dominance 21

Developing a successful e-business strategy 15

Outsourcing non-core competencies 11

Improving corporate transparency image 10

Other 5

Corporate strategy

How well do you expect your company to perform in the 2004 calendar year? (% respondents)

We expect robust growth in revenues and profits 26

We do not expect revenue growth but will deliver higher profits through continued cost-cutting 9

We expect a modest decline in revenues and profits 3

We expect a substantial decline in revenues and profits 1

Other 1

We expect modest growth in revenues and profits 59

28 © The Economist Intelligence Unit 2004

Appendix: Survey resultsCEO Briefing Corporate priorities for 2004

Which approaches will your company take to drive growth worldwide over the next three years?

(% respondents; respondents allowed to choose as many as apply)

Building closer relations with existing customers 55

Developing new products and services 55

Entering new alliance relationships 50

Penetrating new customer markets 47

Focusing on/leveraging core products and services 45

Entering new geographical markets 42

Achieving growth through mergers and acquisitions 20

Spinning off and/or starting up new companies 10

What are the greatest risks facing your company over the next three years?

(% respondents; respondents allowed to choose no more than three risks)

Increased competitive pressures 51

Macroeconomic and financial risk 37

Failure to innovate 33

Inability to respond quickly to changing market conditions 31

Geopolitical risk 24

Difficulty attracting and retaining talent 21

Tighter regulations and higher compliance burden 18

Inability to manage start-ups, alliances and acquisitions 15

Operational and reputational risk from behaviour of employees, partners and clients 12

Bankruptcy and credit risk 12

Rising cost of employee benefits 8

Rising wage pressures 8

Inability to manage outsourcing deals 6

Shareholder pressure for corporate transparency 3

Other 2

Should your company need to raise capital in the coming three years, which route are you most likely to use?

(% respondents)

We will not raise capital in the next three years 26

Bank financing 21

Private equity investment 19

We will dip into reserves instead 11

Corporate bond 10

IPO/share issue 9

Sale of assets 3

Other 2

© The Economist Intelligence Unit 2004 29

Appendix: Survey resultsCEO Briefing

Corporate priorities for 2004

Which functions, if any, does your company outsource now and which do you plan to outsource within the next three years?

(% respondents)

Now outsource Plan to outsource No plan to outsource

Payroll 35 18 47

IT 34 17 49

Logistics 23 18 59

Manufacturing 21 10 70

Finance and accounting 14 14 72

Other HR 12 19 69

Customer contact roles 10 18 72

R&D 5 8 87

Competing in the digital age

How important are technology and the Internet to achieving your corporate goals over the next three years? (% respondents)

Unimportant 5

Important 40

Essential 55

What is your preferred method for developing technology-based business solutions? (% respondents)

Buy technology and heavily customise it 16

Outsource to managed services provider 13

Other 1

Buy technology and lightly customise it 28

Build technology in-house 18

Select technology partners to develop solutions 24

30 © The Economist Intelligence Unit 2004

Appendix: Survey resultsCEO Briefing Corporate priorities for 2004

In which areas of the business do you expect to see the greatest benefits from your investment in technology over the nextthree years?

(% respondents; respondents allowed to choose as many as apply)

Improved sales and marketing 55

Improved knowledge management 51

More successful customer relationship management 46

Lower costs 45

Enhanced back-office systems and networks 45

Better quality of products and services 35

Easier collaboration with partners and suppliers 32

Better financial management 32

More efficient supply-chain management 31

Increased productivity from mobile and remote workers 28

Increased innovation 23

We don’t expect to see benefits within three years 1

Other 1

Leading the global organisation

What leadership qualities will be required to manage a global company in the future?

(% respondents; respondents allowed to choose no more than three qualities)

Strategic vision 63

Excellent communication and people skills 49

A balance between long-term goals and short-term results 43

International knowledge/ability to manage across cultures 38

Innovativeness/openness to new ideas 35

Deep knowledge of market needs and operations 34

Honesty and integrity 30

The ability to manage risk without stifling entrepreneurialism 24

A good understanding of technology 13

Humility/low public profile 5

High public profile 4

Other 1

© The Economist Intelligence Unit 2004 31

Appendix: Survey resultsCEO Briefing

Corporate priorities for 2004

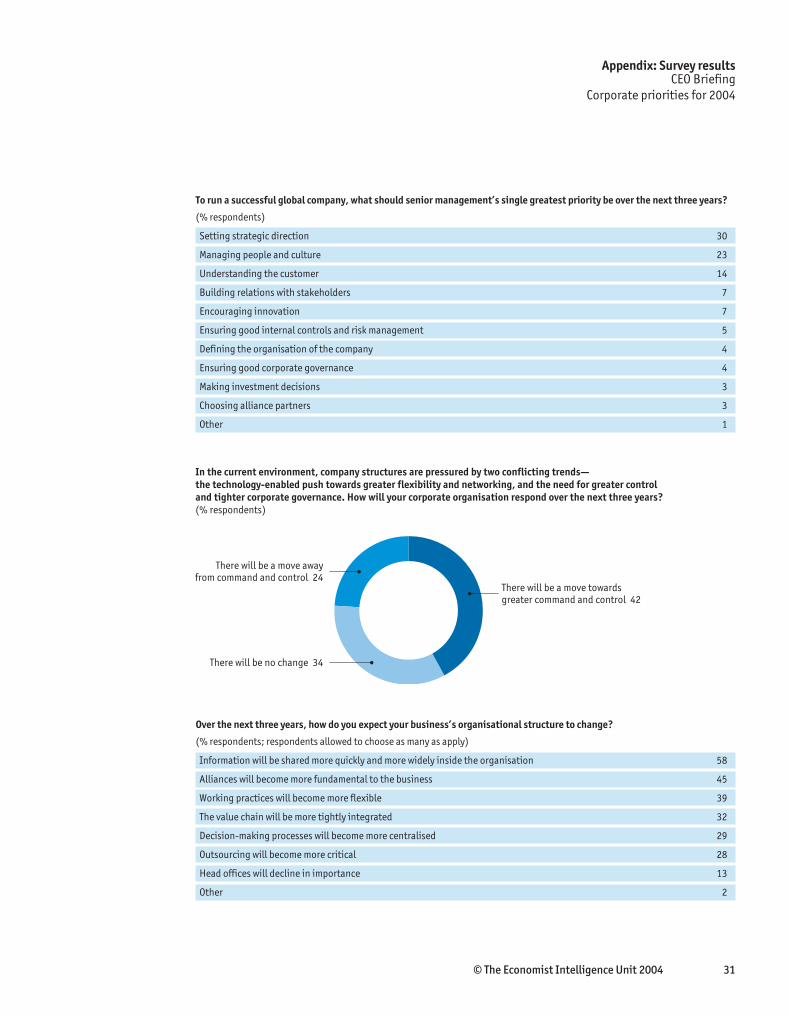

To run a successful global company, what should senior management’s single greatest priority be over the next three years?

(% respondents)

Setting strategic direction 30

Managing people and culture 23

Understanding the customer 14

Building relations with stakeholders 7

Encouraging innovation 7

Ensuring good internal controls and risk management 5

Defining the organisation of the company 4

Ensuring good corporate governance 4

Making investment decisions 3

Choosing alliance partners 3

Other 1

Over the next three years, how do you expect your business’s organisational structure to change?

(% respondents; respondents allowed to choose as many as apply)

Information will be shared more quickly and more widely inside the organisation 58

Alliances will become more fundamental to the business 45

Working practices will become more flexible 39

The value chain will be more tightly integrated 32

Decision-making processes will become more centralised 29

Outsourcing will become more critical 28

Head offices will decline in importance 13

Other 2

In the current environment, company structures are pressured by two conflicting trends—the technology-enabled push towards greater flexibility and networking, and the need for greater control and tighter corporate governance. How will your corporate organisation respond over the next three years? (% respondents)

There will be a move towards greater command and control 42

There will be a move awayfrom command and control 24

There will be no change 34

32 © The Economist Intelligence Unit 2004

Whilst every effort has been taken to verify theaccuracy of this information, neither TheEconomist Intelligence Unit Ltd. nor the sponsorsof this report can accept any responsibility orliability for reliance by any person on this whitepaper or any of the information, opinions orconclusions set out in the white paper.

January 2004

LONDON

15 Regent Street

London

SW1Y 4LR

United Kingdom

Tel: (44.20) 7830 1000

Fax: (44.20) 7499 9767

E-mail: [email protected]

NEW YORK

111 West 57th Street

New York

NY 10019

United States

Tel: (1.212) 554 0600

Fax: (1.212) 586 1181/2

E-mail: [email protected]

HONG KONG

60/F, Central Plaza

18 Harbour Road

Wanchai

Hong Kong

Tel: (852) 2585 3888

Fax: (852) 2802 7638

E-mail: [email protected]