ccar 2018: ey regulatory alert, february 2018 · · 2018-02-06ccar 2018 5 february 2018 | 1 on...

TRANSCRIPT

1CCAR 2018 5 February 2018 |

On Thursday, February 1, 2018, the Federal Reserve Board (FRB or Fed) published the 2018 Comprehensive Capital Analysis and Review (CCAR) instructions and the related supervisory scenarios for the annual stress tests required under the Dodd-Frank Act Stress Testing (DFAST) rules and the capital plan rule.

Day one Tax Reform impacts coupled with a more severe supervisory scenario are key drivers to firms’ capital strategies and distributions for this CCAR cycleThe 2018 CCAR instructions confirmed that provisions of the Tax Cut and Jobs Act (Tax Reform) have to be reflected in firms’ projections. The change in US corporate tax rate, effects from the one-time Transition tax, and other Tax Reform provisions have already been incorporated into CCAR firms’ December 31, 2017 balance sheets and capital ratios.

This year’s supervisory severely adverse scenario is generally more severe than last year. Shocks to certain variables (US equity markets, BBB spreads, and CRE index) represent the most severe assumptions in any CCAR cycle. These scenario features plus other Tax Reform provisions will put additional pressure on CCAR firms’ stress projections, but impact will differ based on business model and asset mix.

Capital distribution strategies will need to consider any resulting changes in required stress buffers. For CCAR 2018, the FRB has included a new provision that CCAR firms can, as part of the one-time adjustment to planned capital actions, increase planned common stock issuances – in addition to reducing their planned capital distribution.

CCAR 2018EY Regulatory AlertFebruary 2018

Highlights

Tax Reform Tax Cuts and Jobs Act likely to have direct and indirect effects on net income projections and stress capital ratios

Scenario Severity Certain key variables represent the most severe CCAR stress ever required by the FRB

2 | CCAR 2018 5 February 2018

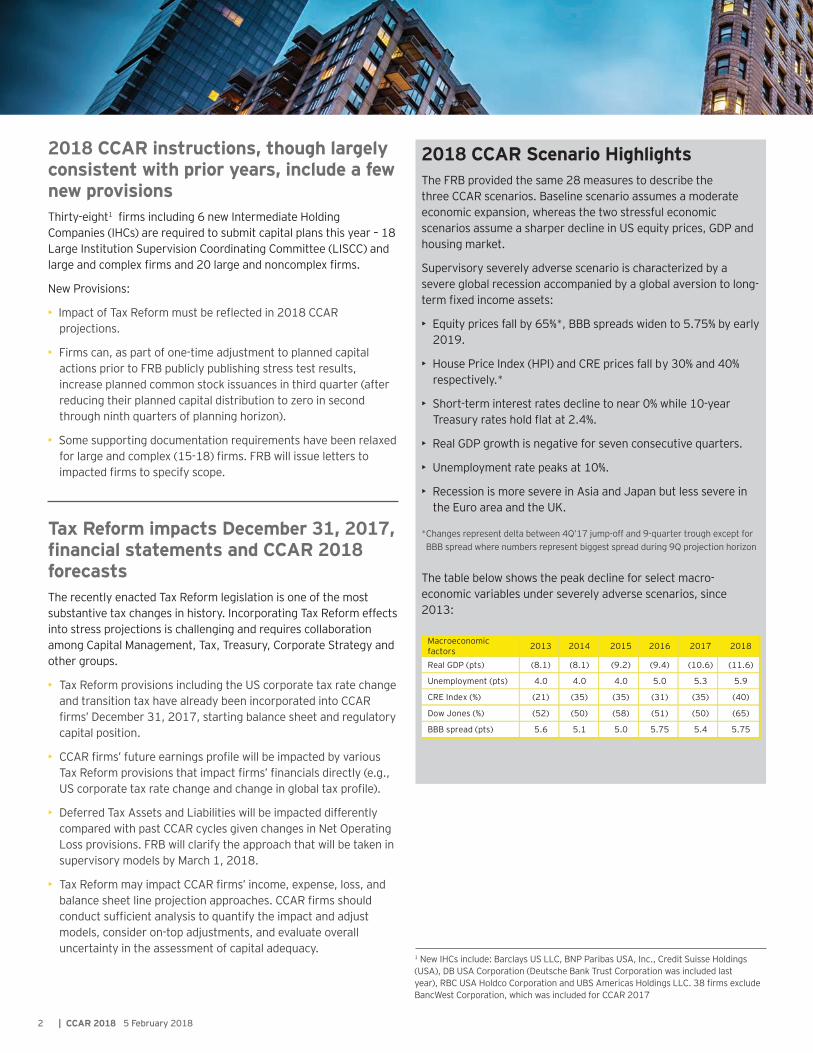

2018 CCAR instructions, though largely consistent with prior years, include a few new provisions Thirty-eight1 firms including 6 new Intermediate Holding Companies (IHCs) are required to submit capital plans this year – 18 Large Institution Supervision Coordinating Committee (LISCC) and large and complex firms and 20 large and noncomplex firms.

New Provisions:

• ►►►Impact of Tax Reform must be reflected in 2018 CCAR projections.

• ►Firms can, as part of one-time adjustment to planned capital actions prior to FRB publicly publishing stress test results, increase planned common stock issuances in third quarter (after reducing their planned capital distribution to zero in second through ninth quarters of planning horizon).

• ►►Some supporting documentation requirements have been relaxed for large and complex (15-18) firms. FRB will issue letters to impacted firms to specify scope.

Tax Reform impacts December 31, 2017, financial statements and CCAR 2018 forecastsThe recently enacted Tax Reform legislation is one of the most substantive tax changes in history. Incorporating Tax Reform effects into stress projections is challenging and requires collaboration among Capital Management, Tax, Treasury, Corporate Strategy and other groups.

• Tax Reform provisions including the US corporate tax rate change and transition tax have already been incorporated into CCAR firms’ December 31, 2017, starting balance sheet and regulatory capital position.

• CCAR firms’ future earnings profile will be impacted by variousTax Reform provisions that impact firms’ financials directly (e.g., US corporate tax rate change and change in global tax profile).

• Deferred Tax Assets and Liabilities will be impacted differently compared with past CCAR cycles given changes in Net Operating Loss provisions. FRB will clarify the approach that will be taken insupervisory models by March 1, 2018.

• Tax Reform may impact CCAR firms’ income, expense, loss, and balance sheet line projection approaches. CCAR firms should conduct sufficient analysis to quantify the impact and adjustmodels, consider on-top adjustments, and evaluate overalluncertainty in the assessment of capital adequacy.

2018 CCAR Scenario HighlightsThe FRB provided the same 28 measures to describe the three CCAR scenarios. Baseline scenario assumes a moderate economic expansion, whereas the two stressful economic scenarios assume a sharper decline in US equity prices, GDP and housing market.

Supervisory severely adverse scenario is characterized by a severe global recession accompanied by a global aversion to long-term fixed income assets:

• ►Equity prices fall by 65%*, BBB spreads widen to 5.75% by early 2019.

• ►House Price Index (HPI) and CRE prices fall by 30% and 40% respectively.*

• ►Short-term interest rates decline to near 0% while 10-year Treasury rates hold flat at 2.4%.

• ►Real GDP growth is negative for seven consecutive quarters.

• ►Unemployment rate peaks at 10%.

• ►Recession is more severe in Asia and Japan but less severe in the Euro area and the UK. ►

* Changes represent delta between 4Q’17 jump-off and 9-quarter trough except forBBB spread where numbers represent biggest spread during 9Q projection horizon

The table below shows the peak decline for select macro-economic variables under severely adverse scenarios, since 2013:

1 New IHCs include: Barclays US LLC, BNP Paribas USA, Inc., Credit Suisse Holdings (USA), DB USA Corporation (Deutsche Bank Trust Corporation was included lastyear), RBC USA Holdco Corporation and UBS Americas Holdings LLC. 38 firms exclude BancWest Corporation, which was included for CCAR 2017

CCAR 2018 | 5 February 2018 Page 2 of 6

2018 CCAR instructions, though largelyconsistent with prior years, include a fewnew provisionsThirty-eight1 firms including 6 new Intermediate HoldingCompanies (IHCs) are required to submit capital plans this year – 18 Large Institution Supervision CoordinatingCommittee (LISCC) and large and complex firms and 20large and noncomplex firms.

New provisions:

► Impact of Tax Reform must be reflected in 2018 CCARprojections.

► Firms can, as part of one-time adjustment to plannedcapital actions prior to FRB publicly publishing stresstest results, increase planned common stock issuancesin third quarter (after reducing their planned capital distribution to zero in second through ninth quarters ofplanning horizon).

► Some supporting documentation requirements havebeen relaxed for large and complex (15-18) firms. FRBwill issue letters to impacted firms to specify scope.

Tax Reform impacts December 31, 2017 financial statements and CCAR 2018forecastsThe recently enacted Tax Reform legislation, is one of the most substantive tax changes in history. Incorporating TaxReform effects into stress projections is challenging andrequires collaboration among Capital Management, Tax, Treasury, Corporate Strategy and other groups.

► Tax Reform provisions including the US corporate tax rate change and transition tax have already beenincorporated into CCAR firms’ December 31, 2017 starting balance sheet and regulatory capital position.

► CCAR firms’ future earnings profile will be impacted byvarious Tax Reform provisions that impact firms’ financials directly (e.g., US corporate tax rate change and change in global tax profile).

► Deferred Tax Assets and Liabilities will be impacteddifferently compared with past CCAR cycles givenchanges in Net Operating Loss provisions. FRB will

1 New IHCs include: Barclays US LLC, BNP Paribas USA, Inc., Credit Suisse Holdings(USA), DB USA Corporation (Deutsche Bank Trust Corporation was included last

clarify the approach that will be taken in supervisorymodels by March 1, 2018.

► Tax Reform may impact CCAR firms’ income, expense,loss, and balance sheet line projection approaches. CCAR firms should conduct sufficient analysis toquantify the impact and adjust models, consider on-topadjustments, and evaluate overall uncertainty in the assessment of capital adequacy.

year), RBC USA Holdco Corporation and UBS Americas Holdings LLC. 38 firmsexclude BancWest Corporation, which was included for CCAR 2017

Image caption – Banner picture TBD (to use EY branding type pictures, not any people that may distract, otherwise delete)

2018 CCAR Scenario HighlightsThe FRB provided the same 28 measures to describe the three CCAR scenarios. Baseline scenario assumes amoderate economic expansion, whereas the two stressfuleconomic scenarios assume a sharper decline in US equity prices, GDP and housing market.

Supervisory severely adverse scenario is characterized bya severe global recession accompanied by a globalaversion to long-term fixed income assets:

► Equity prices fall by 65%*, BBB spreads widen to 5.75% by early 2019

► House Price Index (HPI) and CRE prices fall by 35% and40% respectively*

► Short-term interest rates decline to near 0% while 10-year Treasury rates hold flat at 2.4%

► Real GDP growth is negative for seven consecutive quarters

► Unemployment rate peaks at 10%► Recession is more severe in Asia and Japan but less

severe in the Euro area and the UK► USD weakens against EUR and JPY* Changes represent delta between 4Q’17 jump-off and 9-quarter trough except for BBB spread where numbers represent biggest spread during 9Q projection horizon

The table below shows the peak decline for select macro-economic variables under severely adverse scenarios, since 2013:

Macroeconomic factors 2013 2014 2015 2016 2017 2018

Real GDP (pts) (8.1) (8.1) (9.2) (9.4) (10.6) (11.6)

Unemployment (pts) 4.0 4.0 4.0 5.0 5.3 5.9

CRE Index (%) (21) (35) (35) (31) (35) (40)

Dow Jones (%) (52) (50) (58) (51) (50) (65)

BBB spread (pts) 5.6 5.1 5.0 5.75 5.4 5.75

3CCAR 2018 5 February 2018 |

Other key FRB guidance • ►New accounting standards should not be incorporated in

projections unless effective or adopted by December 31, 2017.

• ►In particular, changes to current expected credit loss impairment standard (CECL)2 should not be incorporated for CCAR 2018 and 2019.

• ►No changes set for qualitative assessment categories: governance, risk management, internal control, capital policy, incorporating stressful conditions and events and estimating the impact on capital positions.

• ►Existing requirements reiterated: 1) Required supplementary leverage ratio (SLR) minimum of 3% for advanced approaches BHCs and IHCs subject to SLR, 2) CFO attestation for LISCC firms for FR Y-14 reports as-of December 31, 2017, now also includes effectiveness of internal controls (in addition to 2017 attestations for material correctness of actual submitted data and conformance with FR Y-14 instructions).

• ►Extension set for certain transition provisions in the capital rules for non-advanced approaches firms, applicable for 2017 for certain items (mortgage servicing assets, certain deferred tax assets, investments in the capital instruments of unconsolidated financial institutions, and minority interest).

The CCAR 2018 Global Market Shock (GMS)3 severely adverse scenario highlights a general sell-off of US assets with significant curve steepening• ►The 2018 GMS severely adverse scenario is characterized by a

sharp increase in US inflation (1M +87bps), bear steepener in US rates (10Y Treasury +175bps), and depreciation of the US dollar (EUR/USD +17%). The scenario also features a general increase in risk premia, and asset sell-off that is more severe in the US market.

• ►The 2018 GMS severely adverse scenario shock calibration is generally more severe than the 2017 severely adverse scenario. For example, whereas the 2017 GMS shocks were -19% and 9 vol points for US equity spot and 1Y volatility, the 2018 GMS shocks are -28% and 31 vol points respectively. The return of larger shocks for certain asset classes such as equities may result in larger trading losses than 2017 for unhedged portfolios and gains for portfolios with downside hedges.

2 New IHCs include: Barclays US LLC, BNP Paribas USA, Inc., Credit Suisse Holdings (USA), DB USA Corporation (Deutsche Bank Trust Corporation was included last year), RBC USA Holdco Corporation and UBS Americas Holdings LLC. 38 firms exclude BancWest Corporation, which was included for CCAR 20173 FRB will provide further guidance on reflecting CECL in CCAR 2020. The six LISCC and large and complex bank holding companies (BHCs) subject to the GMS are Bank of America Corporation; Citigroup Inc.; The Goldman Sachs Group, Inc.; JPMorgan Chase & Co.; Morgan Stanley; and Wells Fargo & Company.

4 GMS ‘as-of’ date has been communicated to be December 4, 2017, and banks can use data as of the date that corresponds to their weekly internal risk reporting between December 4 to December 85 Applicable to any firm subject to supervisory stress test that (1) has aggregate trading assets and liabilities of $50b or more, or aggregate trading assets and liabilities equal to 10% or more of total consolidated assets, and (2) is not a “large and non-complex firm” under the Board’s capital plan rule

• Consistent with the traditional safe-haven status of the US, the flow of funds out of the US corresponds with rallies in alternative safe havens such as gold, which is up 16% in 2018 vs. down 11% in 2017.

• Given the 2018 shock sizes, credit and securitized products asset classes will likely continue to contribute towards large portion of trading losses.

• The USD rate sell-off may result in larger counterparty credit losses, particularly for banks that facilitate hedging against rises in long-term interest rates for their clients.

Six IHCs are subject to interim market risk components in lieu of the GMS• ►►Six IHCs will become subject to GMS in CCAR 2019 as a result of

modified threshold for applicability of GMS component.

• ►The 2018 supervisory scenarios in the IHC’s company-run stress test must reflect trading and counterparty losses using market risk components tailored to firms’ risks as individually communicated to these firms.

• ►For supervisory stress test, FRB will use a simplified version of GMS and large counterparty default scenario component and apply defined loss rates to the applicable exposures from the FR Y-9C reporting as of December 31, 2017. Loss rates for the severely adverse scenario are shown in the table below:

• For LISCC IHCs, FR Y-14Q schedules F (Trading) and L (Counterparty) are now subject to the CFO attestation requirements starting with December 31, 2017, as-of date schedules.

CCAR 2018 | 5 February 2018 Page 3 of 6

Other key FRB guidance ► New accounting standards should not be incorporated in

projections unless effective or adopted by December 31, 2017.

► In particular, changes to current expected credit loss impairment standard (CECL)2 should not be incorporated for CCAR 2018 and 2019.

► No changes set for qualitative assessment categories: governance, risk management, internal control, capital policy, incorporating stressful conditions and events and estimating the impact on capital positions.

► Existing requirements reiterated: 1) Required supplementary leverage ratio (SLR) minimum of 3% for advanced approaches BHCs and IHCs subject to SLR, 2) CFO attestation for LISCC firms for FR Y-14 reports as-of December 31, 2017 now also includes effectiveness of internal controls (in addition to 2017 attestations for material correctness of actual submitted data and conformance with FR Y-14 instructions).

► Extension set for certain transition provisions in the capital rules for non-advanced approaches firms, applicable for 2017 for certain items (mortgage servicing assets, certain deferred tax assets, investments in the capital instruments of unconsolidated financial institutions, and minority interest).

The CCAR 2018 Global Market Shock (GMS)3 severely adverse scenario highlights a general sell-off of US assets with significant curve steepening ► The 2018 GMS4 severely adverse scenario is

characterized by a sharp increase in US inflation (1M +87bps), bear steepener in US rates (10Y Treasury +175bps), and depreciation of the US dollar (EUR/USD +17%). The scenario also features a general increase in risk premia, and asset sell-off that is more severe in the US market.

► The 2018 GMS severely adverse scenario shock calibration is generally more severe than the 2017 severely adverse scenario. For example, whereas the 2017 GMS shocks were -19% and 9 vol points for US equity spot and 1Y volatility, the 2018 GMS shocks are -28% and 31 vol points respectively. The return of larger shocks for certain asset classes such as equities may result in larger trading losses than 2017 for unhedged portfolios and gains for portfolios with downside hedges.

2 FRB will provide further guidance on reflecting CECL in CCAR 2020 3 The six LISCC and large and complex bank holding companies (BHCs) subject to the GMS are Bank of America Corporation; Citigroup Inc.; The Goldman Sachs Group, Inc.; JPMorgan Chase & Co.; Morgan Stanley; and Wells Fargo & Company. 4 GMS ‘as-of’ date has been communicated to be December 4, 2017, and banks can use data as of the date that corresponds to their weekly internal risk reporting between December 4 to December 8

► Consistent with the traditional safe-haven status of the US, the flow of funds out of the US corresponds with rallies in alternative safe havens such as gold, which is up 16% in 2018 vs. down 11% in 2017.

► Given the 2018 shock sizes, credit and securitized products asset classes will likely continue to contribute towards large portion of trading losses.

► The USD rate sell-off may result in larger counterparty credit losses, particularly for banks that facilitate hedging against rises in long-term interest rates for their clients.

Six IHCs are subject to interim market risk components in lieu of the GMS ► Six IHCs will become subject to GMS in CCAR 2019 as a

result of modified threshold for applicability5 of GMS component.

► The 2018 supervisory scenarios in the IHC’s company-run stress test must reflect trading and counterparty losses using market risk components tailored to firms’ risks as individually communicated to these firms.

► For supervisory stress test, FRB will use a simplified version of GMS and large counterparty default scenario component and apply defined loss rates to the applicable exposures from the FR Y-9C reporting as of December 31, 2017. Loss rates for the severely adverse scenario are shown in the table below:

► For LISCC IHCs, FR Y-14Q schedules F (Trading) and L (Counterparty) are now subject to the CFO attestation requirements starting with December 31, 2017 as-of date schedules.

5 Applicable to any firm subject to supervisory stress test that (1) has aggregate trading assets and liabilities of $50b or more, or aggregate trading assets and liabilities equal to 10% or more of total consolidated assets, and (2) is not a “large and non-complex firm” under the Board’s capital plan rule

Loss measures Loss rates

(severely adverse scenario)

Applicable exposures

Securitized products

losses 46.4%

Certain loans and credits held for

trading Trading MtM and trading IDR losses

1.8% Market RWA

CVA losses 2.8% OTC derivatives RWA

Large counterparty default losses

1.5% Repo-style

transactions, OTC derivatives RWA

4 | CCAR 2018 5 February 2018

Supervisory focus on efficiency, transparency and simplification will continue to drive changes in expectations for capital planning while core capabilities will remain criticalThe FRB continues to further differentiate expectations for LISCC and large and complex firms versus large and non-complex Firms. A series of recent regulatory and administrative announcements, speeches and proposals have provided insight into the regulatory focus on efficiency, transparency and simplification of post-crisis financial regulation.

While there are indications of potential changes ahead as regulators assess the overall stress testing framework, a recent proposal related to supervisory rating system for firms with more than $50b in assets indicate how capital planning will continue to be a key factor in evaluating the financial and operational strength and resilience of financial institutions.

Fed Vice Chairman Randal Quarles in his recent speech on “Early Observations on Improving the Effectiveness of Post-Crisis Regulation” summarized the major supervisory focus for 2018 to include:

• ►Tailoring supervision and regulation to the size, systemic footprint, risk profile, and business model of banks through:

• ► Reduction in CCAR frequency

• ► Recalibration of leverage ratio

• ► Further simplification of capital requirements for small and medium-sized banking firms

• ► Increase in current $50b asset threshold for the enhanced prudential standards

• ► Elimination of advanced approaches risk-based capital requirements and one or more ratios in stress testing

• ► Simplification of total loss absorbing capacity (TLAC) requirements

• ► Simplification of Volcker Rule and resolution planning

• ►Improving transparency of the FRB stress testing program specifically for economic conditions and models used in FRB’s stress tests.

As regulators formalize the changes to the stress testing program, CCAR firms should continue to focus on the further integration of core capital planning processes with risk management and strategic planning.

Key Upcoming dates• Next few weeks - FRB letter to LISCC and large and complex

firms specifying planned scope for supporting documentation for CCAR 2018

• March 1, 2018 - FRB letter describing material enhancements to the supervisory models, including those related to tax law

• April 5, 2018 - 2018 capital plan and FR Y-14A submissions

• June 30, 2018, or earlier - FRB disclosure of DFAST results and CCAR 2018 quantitative and qualitative assessments for large and complex firms

5CCAR 2018 5 February 2018 |

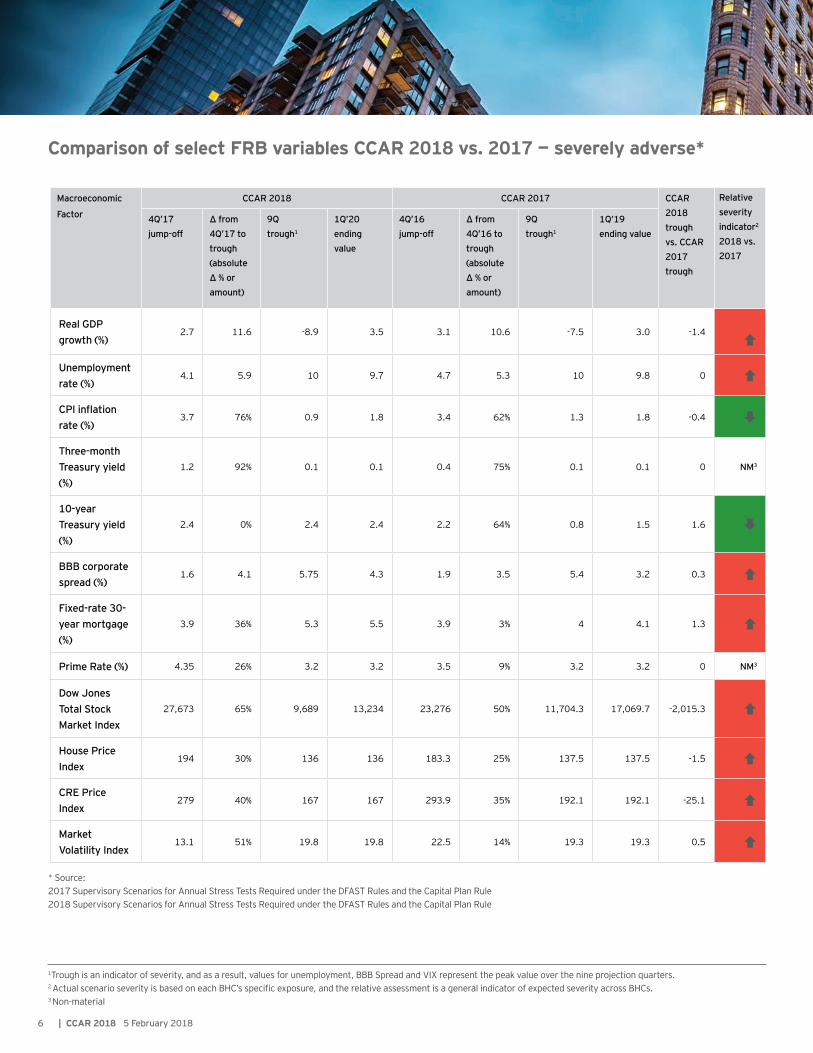

Comparison of select FRB variables CCAR 2018 vs. 2017 — severely adverse*

* Source:2017 Supervisory Scenarios for Annual Stress Tests Required under the DFAST Rules and the Capital Plan Rule2018 Supervisory Scenarios for Annual Stress Tests Required under the DFAST Rules and the Capital Plan Rule

CCAR 2018 | 5 February 2018 Page 5 of 6 ►

Comparison of select FRB variables CCAR 2018 vs. 2017 — severely adverse Table 1: Real GDP growth Table 2: Unemployment

Table 3: CRE index Table 4: Fixed-rate 30-year mortgage

Table 5: BBB corporate spread Table 6: 10 Year Treasury Yield

Table 7: Dow Jones Industrial Average Table 8: VIX

Table 9: Comparison of select FRB variables CCAR 2018 vs. 2017 — severely adverse scenario

Macroeconomic factor

CCAR 2018 CCAR 2017 CCAR 2018 trough vs.

CCAR 2017 trough

Relative severity

indicator2 2018 vs.

2017

4Q'17 jump-off

Δ from 4Q'17 to trough

(absolute Δ % or amount)

9Q trough1

1Q'20 ending value

4Q'16 jump-off

Δ from 4Q'16 to trough

(absolute Δ % or amount)

9Q trough1

1Q'19 ending value

Real GDP growth (%) 2.7 11.6 -8.9 3.5 3.1 10.6 -7.5 3.0 -1.4 Unemployment rate (%) 4.1 5.9 10 9.7 4.7 5.3 10 9.8 0 CPI inflation rate (%) 3.7 76% 0.9 1.8 3.4 62% 1.3 1.8 -0.4 3-month treasury yield (%) 1.2 92% 0.1 0.1 0.4 75% 0.1 0.1 0 NM3 10-year treasury yield (%) 2.4 0% 2.4 2.4 2.2 64% 0.8 1.5 1.6 BBB corporate spread 1.6 4.1 5.75 4.3 1.9 3.5 5.4 3.2 0.3 Mortgage rate (%) 3.9 36% 5.3 5.5 3.9 3% 4 4.1 1.3 Prime rate (%) 4.3 26% 3.2 3.2 3.5 9% 3.2 3.2 0 NM3 Dow Jones index 27673 65% 9689 13234 23276 50% 11704.3 17069.7 -2015.3 House price index 194 30% 136 136 183.3 25% 137.5 137.5 -1.5 CRE price index 279 40% 167 167 293.9 35% 192.1 192.1 -25.1 Market volatility index (VIX) 13.1 51% 19.8 19.8 22.5 14% 19.3 19.3 0.5 1 Trough is an indicator of severity, and as a result, values for unemployment, BBB Spread and VIX represent the peak value over the nine projection quarters.

2 Actual scenario severity is based on each BHC’s specific exposure, and the relative assessment is a general indicator of expected severity across BHCs. 3 Non-material

-10.0

-5.0

0.0

5.0

10.0 Real GDP Growth (17 V 18)

2017 Sev Adv

2018 Sev Adv0.0

2.0

4.0

6.0

8.0

10.0

12.0 Unemployment (17 V 18)

2017 Sev Adv

2018 Sev Adv

100

150

200

250

300

350 CRE Index (17 V 18)

2017 Sev Adv 2018 Sev Adv 0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0 30-Year Mortgage Rate (17 V 18)

2017 Sev Adv2018 Sev Adv

0.0

1.0

2.0

3.0

4.0

5.0

6.0BBB Corporate Spread (17 V 18)

2017 Sev Adv2018 Sev Adv

0.0

0.5

1.0

1.5

2.0

2.5

3.0 10 Year Treasury Yield (17 V 18)

2017 Sev Adv

2018 Sev Adv

0

5

10

15

20

25

30 DJIA (17 V 18)

2017 Sev Adv

2018 Sev Adv0

20

40

60

80 VIX (17 V 18)

2017 Sev Adv

2018 Sev Adv

6 | CCAR 2018 5 February 2018

Macroeconomic

Factor

CCAR 2018 CCAR 2017 CCAR 2018 trough vs. CCAR 2017 trough

Relative severity indicator2 2018 vs. 2017

4Q’17jump-off

Δ from 4Q’17 to trough (absolute Δ % or amount)

9Qtrough1

1Q’20 ending value

4Q’16 jump-off

Δ from 4Q’16 to trough (absolute Δ % or amount)

9Qtrough1

1Q’19ending value

Real GDP growth (%)

2.7 11.6 -8.9 3.5 3.1 10.6 -7.5 3.0 -1.4 Ç

Unemployment rate (%)

4.1 5.9 10 9.7 4.7 5.3 10 9.8 0 Ç

CPI inflation rate (%)

3.7 76% 0.9 1.8 3.4 62% 1.3 1.8 -0.4 È

Three-month Treasury yield (%)

1.2 92% 0.1 0.1 0.4 75% 0.1 0.1 0 NM3

10-year Treasury yield (%)

2.4 0% 2.4 2.4 2.2 64% 0.8 1.5 1.6 È

BBB corporate spread (%)

1.6 4.1 5.75 4.3 1.9 3.5 5.4 3.2 0.3 Ç

Fixed-rate 30-year mortgage (%)

3.9 36% 5.3 5.5 3.9 3% 4 4.1 1.3 Ç

Prime Rate (%) 4.35 26% 3.2 3.2 3.5 9% 3.2 3.2 0 NM3

Dow Jones Total Stock Market Index

27,673 65% 9,689 13,234 23,276 50% 11,704.3 17,069.7 -2,015.3 Ç

House Price Index

194 30% 136 136 183.3 25% 137.5 137.5 -1.5 Ç

CRE Price Index

279 40% 167 167 293.9 35% 192.1 192.1 -25.1 Ç

Market Volatility Index

13.1 51% 19.8 19.8 22.5 14% 19.3 19.3 0.5 Ç

Comparison of select FRB variables CCAR 2018 vs. 2017 — severely adverse*

1Trough is an indicator of severity, and as a result, values for unemployment, BBB Spread and VIX represent the peak value over the nine projection quarters.2 Actual scenario severity is based on each BHC’s specific exposure, and the relative assessment is a general indicator of expected severity across BHCs.3 Non-material

* Source:2017 Supervisory Scenarios for Annual Stress Tests Required under the DFAST Rules and the Capital Plan Rule2018 Supervisory Scenarios for Annual Stress Tests Required under the DFAST Rules and the Capital Plan Rule

7CCAR 2017 EY Regulatory Alert |

EY contacts

Capital planningAdam GirlingPrincipalErnst & Young LLP+ 1 212 773 [email protected]

Tom JacksonPrincipalErnst & Young LLP+1 704 331 [email protected]

Jefrey RoblesPrincipalErnst & Young LLP+1 212 773 [email protected]

Marc SaidenbergPrincipalErnst & Young LLP+1 212 773 [email protected]

Preston ThompsonExecutive DirectorErnst & Young LLP+1 617 585 [email protected]

Trading and counterparty Mike SheptinPrincipalErnst & Young LLP+1 212 773 [email protected]

Sumit MalikPrincipalErnst & Young LLP+1 212 773 [email protected]

Ari CohenExecutive DirectorErnst & Young LLP+1 212 360 [email protected]

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2018 Ernst & Young LLP.All Rights Reserved.

SCORE no. 00700-181US

1801-2574216

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com