cavendish university zambia schemes in zambia: a case

TRANSCRIPT

CAVENDISH UNIVERSITY ZAMBIA

A CRITICAL EVALUATION OF GOVERNANCE SUPERVISION ON PUBLIC PENSIONSCHEMES IN ZAMBIA: A CASE STUDY OF NATIONAL PENSION SCHEMEAUTHORITY.

Faculty of Business

By

Kasonde kaira

(004 - 413)

A Proposal been submitted to the Faculty of BIT of the Cavendish University Zambia in partial

fulfillment of the requirements for the award of the Degree of Bachelors in Banking and Finance

(BBF).

Cavendish University Zambia

P.O Box 34625

LUSAKA

SEPTEMBER 2020

1 | P a g e

DECLARATION

I, kasonde kaira, do solemnly declare that this piece of work has been a pure product of my own

efforts, origination and research. Even though some views may have been drawn from other

pieces of work, my conscience is very clear that enough efforts have been made to duly

acknowledge the persons and their work in all such cases. I also declare that, to the best of my

existing knowledge, this piece of work has not been previously presented at Cavendish

University Zambia for the award of bachelor’s degree in banking and finance or indeed any

other school, college or university for a similar purpose. All sections of text and results which

have been obtained from other sources have been referenced. I noted and still note that cheating

and plagiarism constitute a breach of the University`s Academic Regulations.

.......................................................... ..........................................

STUDENT (Kasonde Kaira) DATE

........................................................... ............................................

SUPERVISOR (Mrs. Pricilla Lesa) DATE

2 | P a g e

ACKNOWLEDGEMENTS

Almighty God

First and foremost, I would like to thank the lord God for the life and wisdom he has

unconditionally disposed unto me.

Supervisor

My special thanks and gratitude are also extended to my supervisor Mrs. Pricilla lesa for her

guidance, invaluable comments and unreserved intellectual assistance in undertaking this study. I

will forever remain grateful and indebted to my supervisor for making all my efforts seem so

easy and going out of her way to ensure that I reached the finishing line

Faculty and Research Staff

I am also grateful to faculty members in particular Mr. lee mahlango, Mr. Cifwala clement

Hikachila, Mr. Serenje, Mr. Beda Mwale, Mr. kawina and Mrs Elizabeth Zyambo for the endless

effort rendered in helping me to be a successful graduate and as they were true nationalists and

distinguished mentors and lecturers, who continued to inspire and encourage me in so many

ways than they realized,.

Family and Friends

I am very much thankful to my parents Mr. Stephen Kaira and Mrs.Grace Kasonde Kaira humble

and kind-hearted legends whose deeds will forever remain unmatched and whose constant

challenge for me to go an extra mile in working hard remains graphically and freshly vivid to

date. Including the Kaira’s family as a whole and my colleages for the full support rendered in

completion of this project.

Thank you sincerely!

Kasonde Kaira

3 | P a g e

DEDICATION

This research report is dedicated to all my friends, my family, and other members of the

extended family who supported me both spiritually and financially and made it possible for me

to undertake a Bachelor’s Degree in Banking and Finance at Cavendish University Zambia.

4 | P a g e

LIST OF ACCRONYMS AND ABREVIATIONS

CAPSA - Canadian Association of Pension Supervisory Authorities

IMF - International Monetary Fund

IOPS - International Organisation for Pension Supervisors,

INPRS - International Network of Pension Regulators and

Supervisors ISSA - International Social Security Association

HIPC - Highly Indebted Poor Country

LASF - Local Authorities Superannuation Fund

NAPSA - National Pension Scheme Authority

OECD - Organisation for Economic Co-operation and Development

PSPF - Public Service Pensions Fund

PSRA - Pension Schemes Regulation Act

PIA - Pensions and Insurance Authority

WB - World Bank

WCFCB - Workers Compensation Fund Control Board

ZESCO - Zambia Electricity Supply Corporation

ZNPF - Zambia National Provident Fund

ABSTRACT

A pension scheme operates on the premise that it collects part of the income from its members,

invests and grows it for future drawings by the members. On the merit of this principle, pension

benefits are classified as deferred income for the members and beneficiaries, with the pension

5 | P a g e

administrator or fund manager promising to make the benefits available immediately a claim is

made in future, subject to the rules of the scheme. The pension administrator is not only charged

with the responsibility of safe-keeping, but also multiplying the promised retirement income

through prudent investment.

However, worldwide experience has shown that the investment and general management of

pension funds is not without risk. Imprudently or improperly managed, such funds can yield

negative returns or can disappear altogether. These factors, together with the non-negotiable

element of the pension promise make it critical for pension schemes to be governed in order to

ensure that members interests are safeguarded.

Because the experts in pension matters are generally agreed that pension funds are set up with the

common objective of serving as a secure source of income funds for retirement benefits, they

have consequently adopted universal governance regulations which are designed to guide the

governance of global pension schemes, through the OECD. Countries world-wide, particularly

those affiliated to OECD, are expected to manage their pension systems within the universal

pension governance regulations.

However in the Zambian case, despite affiliating to the OECD, there is foreboding understanding

that public pension schemes are particularly faced with a governance problem, one that is clearly

manifested in and stems from the manner of supervision exerted upon these public schemes.

Using a mix of information gathering methods which included wide literature review,

unstructured interviews and questionnaires which targeted the pension scheme, Retirees and fund

managers that are supervised by Zambia’s pension regulatory authority (PIA). This study was

able to demonstrate that it is one thing to have regulations, guidelines, codes or even a regulatory

authority in place, yet quite another to enforce governance benchmarks on public pension

schemes which are basically state-sponsored. The study proves the overriding hypothesis that the

supervision, and consequently the governance, of public pension schemes in Zambia is seriously

undermined by the fact that the sponsor and the supervisor are one and the same.

6 | P a g e

It is therefore recommended that the structural arrangements relating to the supervision of public

pension schemes should be streamlined to make it more distant from government and less

susceptible to compromise due to the dependent interrelations involved.

Table of ContentsACKNOWLEDGEMENTS.........................................................................................................................3

LIST OF ACCRONYMS AND ABREVIATIONS.............................................................................5

ABSTRACT................................................................................................................................................6

7 | P a g e

1.0 BACKGROUND......................................................................................................................10

1.1 Introduction...........................................................................................................................10

1.2 Background about Zambia.....................................................................................................10

1.3 Problem statement.................................................................................................................15

1.4 Research objectives................................................................................................................17

1.5 Hypotheses.............................................................................................................................17

1.6 Research questions.................................................................................................................18

1.7 Scope of the study..................................................................................................................19

1.8 Significance of the study........................................................................................................19

1.9 Organization of the study.......................................................................................................20

2.0 LITERATURE REVIEW.......................................................................................................20

2.1 Introduction...........................................................................................................................20

2.2 Structure of the pension industry in Zambia..........................................................................21

2.3 The concept of corporate governance....................................................................................23

2.4 Historical perspective of corporate governance.....................................................................25

2.5 The governance framework for pension schemes..................................................................26

2.6 Primary elements of supervision............................................................................................30

2.7 Theoretical framework...........................................................................................................31

RESEARCH METHODOLOGY AND DESIGN..................................................................................40

3.0 Introduction...............................................................................................................................40

3.1 Research Paradigm....................................................................................................................41

3.2 Research design.........................................................................................................................42

3.2.1 Study Area.........................................................................................................................43

3.2.2 Types of measurement.......................................................................................................43

3.2.3 MEASUREMENT OF VARIABLES WILL TAKE DIFFERENT SCALES AS FOLLOWS.........43

Interval scale.............................................................................................................................................44

Ratio scale.................................................................................................................................................44

3.3 SAMPLE SIZE.........................................................................................................................44

3.4 Sampling Plan and Procedure...................................................................................................45

3.5 TYPES AND SOURCES OF DATA...............................................................................................45

3.5.1 Primary Data......................................................................................................................45

3.5.2 Secondary Data.................................................................................................................46

3.6 DATA COLLECTION METHODS AND APPROACHES............................................................46

8 | P a g e

3.6.1 questionnaire.................................................................................................................................47

reliability and validity............................................................................................................................47

ethical consideration..............................................................................................................................48

3.7 LIMITATIONS OF THE STUDY...................................................................................................49

3.8 CONCLUSION...............................................................................................................................50

4.0 PRESENTATION OF THE FINDINGS................................................................................50

4.1 Introduction...........................................................................................................................51

4.2 Analytical framework............................................................................................................51

5.0 ANALYSIS OF FINDINGS..........................................................................................................63

Figure 5.2 Total Pension Contributions (K’ Millions).......................................................................68

Figure 5.3 Self-Administered Pension Schemes’ Share of Industry Net Assets.................................68

6.0 CONCLUSIONS AND RECOMMENDATIONS.................................................................69

6.1 Introduction...........................................................................................................................69

6.3 Recommendations..................................................................................................................74

6.4 Summary of conclusions and recommendations....................................................................76

6.0 REFERENCES........................................................................................................................77

APPENDIX I........................................................................................................................................79

QUESTIONNAIRE.........................................................................................................................79

APPENDIX II......................................................................................................................................91

QUESTIONNAIRE.........................................................................................................................91

CHAPTER ONE

9 | P a g e

1.0 BACKGROUND

1.1 Introduction

This chapter lays a foundation for our study. It gives a general background about the country,

Zambia, which provides the setting for this study. It then proceeds to give a background of the

pension industry in Zambia and the regulatory framework thereof. The chapter also introduces

the problem under study and the hypotheses that this research will be attempting to prove.

1.2 Background about Zambia

Zambia is a 750,000-square-kilometers landlocked country in southern Africa. It is surrounded

by eight neighboring sovereign states and lies in a tropical belt on a fairly high plateau enjoying

a temperate climate with hardly any humidity. It has, in abundance, good agriculture soil, many

lakes and rivers, vast game parks filled with lots of wild life species and scenic beauties

including the world tourism acknowledged and famous Victoria Falls. The country has a little

over 10 million inhabitants. Zambia’s main economic activities are copper mining, agriculture

and tourism. It has rejuvenating manufacturing and energy sectors, but with a very small formal

employment sector of less than half a million people. The largest employer is the government of

the Republic of Zambia, followed by the private-sector owned and managed mining sector.

Economic growth has however been dismal with nominal Gross National Product (GNP) per

capita falling from USD 630 in 1980 to USD 450 in 1990 and USD 300 in 2000, according to

the World Bank Country Report (2002). Zambia’s per capita income is estimated at USD 230,ranking almost the lowest in the region and therefore poorly ranked on the international scene.

By 31 March 2005, Zambia had reached the HIPC decision point which has since triggered

sizeable donor financial support, both through the reduction of the debt stock and the injection of

project finance and budget support which should help stabilize the country’s macro-economic

environment. Project support and reduced debt financing will create scope for public

investments that should help generate employment.

10 | P a g e

The medium term expenditure framework 2005-2007 targets, among other goals, GDP growth of

5 per cent, single digit inflation, insulation to internal and external shocks, maintenance and

sustenance of external account deficit and stabilization of debt, improving public expenditure

management and increased operational efficiency in managing domestic borrowing, leading to

less hassled private sector delivery, and of direct effect to the pensions industry, to develop a

well-functioning financial system.

The vision of the financial services sector is to have a stable, sound and market-based financial

system that supports the efficient mobilization and allocation of resources necessary to achieve

economic diversification, sustainable growth and poverty reduction. A draft Financial Sector

Development Plan1 has been structured among others to address the following weakness:

i. low intermediation;

ii. poor credit culture;

iii. multiple and potentially conflicting government roles;

iv. the weak regulatory framework for non-banking financial institutions, insurance and

pension funds;

v. the undeveloped capital market;

vi. lack of long term development and housing finance; and

vii. a limited number of monetary policy instruments.

Stakeholders have drawn comprehensive terms of reference covering the entire sector with

benchmarks for formal commissioning of the plan, which well encompasses the pensions and

insurance industry.

1.2.1 Background of the pension industry in Zambia

The history of social security in Zambia dates back to the pre-colonial era, as early as the 1920s

when employers’ liability was introduced for work injury compensation, currently administered

by the Workers Compensation Fund Control Board (WCFCB). In 1954, LASF was established

to provide pensions for employees in the local authorities. Over the years, LASF’s coverage and

1 A draft copy of the Financial Sector Development Plan is under review, supervised by the Central Bank ofZambia.

11 | P a g e

mandate was extended to include what are known as Associated Authorities. These are

institutions that provide services that were originally provided by local authorities but have over

the years been hived off to become autonomous quasi-government institutions or have been

commercialized and/or privatized. They include the national electricity utility (ZESCO Ltd) and

some water utility companies, prominent amongst them the Lusaka Water and Sewerage

Company.

In the mainstream civil service, the earliest coverage for pensions was a remainder of the

colonial legacy – a pension scheme that was for the reserve of white employees only. However,

after the country’s independence in 1964, there was pressure to extend coverage to indigenous

Zambians working in the civil service, culminating in the creation of the Civil Service (Local

Conditions) Pensions Fund, currently operating as the Public Service Pensions Fund (PSPF).

1966, the government created the Zambia National Provident Fund (ZNPF) to cover employees

outside the civil service and the local authorities. ZNPF was transformed to the current National

Pension Scheme Authority (NAPSA) in 2000. NAPSA is a basic and compulsory scheme

covering all employees in Zambia, including those under PSPF and LASF.

Up to independence in 1964, employment under the main economic and social activities i.e.

mining, agriculture, transport and education, provided a variety of retirement terms embedded in

the employment conditions of service. Pension provisions were largely harmonized during

nationalization of companies in the early 1970s when government took over control of all major

companies and made uniform the retirement benefits for all employees in the parastatal sector.

Up to 1992, pension and insurance businesses was restricted to state owned enterprises as the

law did not allow competition except from the Mukuba Scheme for the mining industry. With

the liberalization of the economy, several new players emerged to set up and offer competitive

retirement benefit plans. A sizeable number of companies running in house retirement funds

have since introduced formal occupational schemes for their employees which, by law, are

required to be affiliated with multi-employer trustees regulated by the Pensions and Insurance

Authority (PIA).

12 | P a g e

Recent changes in Zambia’s social security have largely been driven by a number of studies

undertaken by various experts from as far back as the early 1980s, to provide a framework

within which the social security arrangements in the country could be rationalized and

strengthened. The various studies revealed a number of unhealthy conditions relating to social

security arrangements as a whole, and highlighted significant weaknesses in terms of design,

financing and administration (Hantuba, 2005).

1.2.2 Pension Funds in Zambia

There are generally two types of pension funds in Zambia - the statutory (public) pension funds

and private occupational pension funds. The statutory pension funds include the PSPF, LASF

and NAPSA. All the three schemes exist under their own respective statutes. NAPSA is a

mandatory statutory scheme under the Ministry of Labour and Social Security, whilst PSPF and

LASF fall under the Ministries of Finance and National Planning and Local Government and

Housing, respectively. All in all there are currently 240 registered pension schemes in Zambia

(Martin Libinga, registrar and CEO of Zambia PIA).

All the 240 schemes are required by the Zambian law to affiliate to multi-employer trusts

managed by dedicated Fund Managers, of which there are some registered under the Pension

Scheme Regulation Act (PSRA) No. 28 of 1996. Multi-employer trusts are the only institutions

charged with the responsibility of managing pension scheme funds, with an exception of the

public schemes, which manage the Funds on their own. Under Section 11 of PSRA, it is a

requirement that any pension scheme established under this Act in the Republic of Zambia shall

have a fund establish in a separate multi-employer trust or alternatively be affiliated to such a

trust into which all contributions, investment earnings, surpluses from insurance and other

moneys shall be paid in accordance with the relevant pension plan rules.

All the pension funds in Zambia are designed either as final salary (defined benefit) or money

purchase (defined contribution) arrangements. A small number of these pension funds are a

hybrid type, which is a combination of both, defined benefits and defined contributions types.

However, the majority of the pension schemes are defined contribution arrangements.

13 | P a g e

1.2.3 Regulation and supervision of the pension industry

Apart from NAPSA, which is more or less self-regulated through its own stand-alone legal

framework, but supervised by the Ministry of Labour and Social Security, all statutory and

private occupational pension funds, including all employer sponsored pension schemes, fall

under the regulatory framework of the Pension Scheme Regulation Act, which is under the ambit

of PIA.

The PIA was established in February 1997 to regulate the conduct of the pensions and insurance

industry through prudential supervision in order to protect the interests of pension scheme

members and insurance policy holders. Before PIA was created in 1997, the industry was

virtually unregulated, meaning that being less than ten years old, pension regulatory issues in the

country are still in infancy, so to speak.

1.3 Problem statement

The two main aims of pension regulation and supervision are to protect the rights of members

and beneficiaries and to ensure the security and sustainability of pension plans. These two basic

goals form the basis for the principles of pension regulation that have been approved by both the

Organization for Economic Co-operation and Development (OECD)2 and the International

Network of Pension Regulators and Supervisors (INPRS) and endorsed by other international

organizations such as the World Bank (WB) and the International Monetary Fund (IMF).

Pension rights and pension plans need to be protected because they provide deferred income for

the members and beneficiaries. They constitute a promise that is intended to allow the saver to

subsist without working, at a later point in life.

2 The OECD groups 30 member countries sharing a commitment to democratic government and the market economy. Bestknown for its publications and its statistics, its work covers economic and social issues from macroeconomics, to trade,education, development and science and innovation. The OECD is also prominent for its role in fostering good governance in thepublic service and in corporate activity. It helps governments to ensure the responsiveness of key economic areas with sectoralmonitoring.

14 | P a g e

At the time of accepting entry of the member, the pension administrator or fund manager

promises to make the benefits available immediately a claim is made in future, subject to the

rules of the scheme. The pension administrator is, therefore, not only charged with the

responsibility of safe-keeping, but also multiplying the promised retirement income through

prudent investment and paying it as and when required.

However, worldwide experience has shown that the investment and general management of

pension funds is not without risk. Imprudently or improperly managed, such funds can yield

negative returns or can disappear altogether. The fact that these funds are very vulnerable, on

one hand, contrasted with the fact that pension promise is non-negotiable, on the other hand,

makes it absolutely critical for pension schemes to be governed in a sustainable manner.

Although there are existing differences in the operation of pension funds in countries that belong

to the OECD, it is generally accepted that these differences should not obscure the fact that

pension funds are set up with one common objective - to serve as a secure source of income

funds for retirement benefits. In this respect, governance regulations in different countries are

designed under the guidance of this overriding objective.

Reading the inspection reports of the PIA and reviewing the literature in three of Zambia’s three

public (statutory) pension schemes3, namely LASF, PSPF and NAPSA, one develops immediate

doubts about the practicability of these governance principles amongst the public pension funds.

Interviews with officials at the supervisory authority (PIA) itself confirmed skepticism about the

commitment to the governance of public pension schemes. With such doubts, touching on the

very foundation of a pension system, it is reasonable to conclude that retirement funds under

statutory schemes in Zambia have very high exposure and as such, the pension promise is under

threat. By implication, the governance of public pension schemes in Zambia is questionable.

3 The words “Scheme” and “Fund” are used interchangeably in this document because the institutions under study, i.e. LASF, PSPF and NAPSA, are pension schemes as well as fund managers of those schemes. This must not be confused with situations where an institution could have a pension scheme whose Funds are externally managed by another entity, i.e. a dedicated financial institution called Fund Manager. In such cases, the three entities are separate and different in scope. However, in the case of LASF, PSPF and NAPSA, the schemes manage their own funds, hence the interchangeability in the use of words. In many countries, the word “Plan” is also used in place of “scheme”. The institution referred to is one and the same

15 | P a g e

An analysis of literature (mostly unpublished) from LASF and PSPF clearly indicates that the

two organizations have, for years, not been meeting PIA regulatory and supervisory benchmarks.

It is therefore assumed that measured against the OECD pension governance framework as

articulated in the literature review, both LASF and PSPF would perform negatively. Supposedly,

therefore, the pension promise has been threatened, if not broken altogether. Yet, both

institutions have continued to operate despite lacking or failing to meet particular elements of

pension governance, which would have attracted heavy supervisory action in the case of private

schemes. This therefore begs the following broad research question: to what extent does state

involvement in the ownership of public pension schemes in Zambia account for the variance in

the effectiveness of the supervisory authority of PIA over LASF and PSPF.

1.4 Research objectives

This study is intended to demonstrate that it is one thing to have regulations, guidelines, codes or

even a regulatory authority in place, yet quite another to enforce supervision compliance in the

case of public pension schemes which by virtue of being under the de jure guarantee of the state

are, in principle, also state-sponsored.

General objective

To asses measures taken into place in governance supervision on one of Zambia’s public

pension scheme NAPSA

Specific objectives

1.4.1 To establish the characteristics behind the principles of pension governance;

1.4.2 To draw conclusions about the applicability of governance principles in public pension

schemes;

1.4.3 To confirm whether or not Zambia’s public pension scheme (NAPSA) has been meeting

pension governance requirements;

1.4.4 To establish the reasons why it is difficult to arrive at effective governance for public

pensions in Zambia; and

16 | P a g e

1.4.5 To establish how the supervisory effectiveness of public pension schemes is affected by the

impact of state-ownership of the schemes.

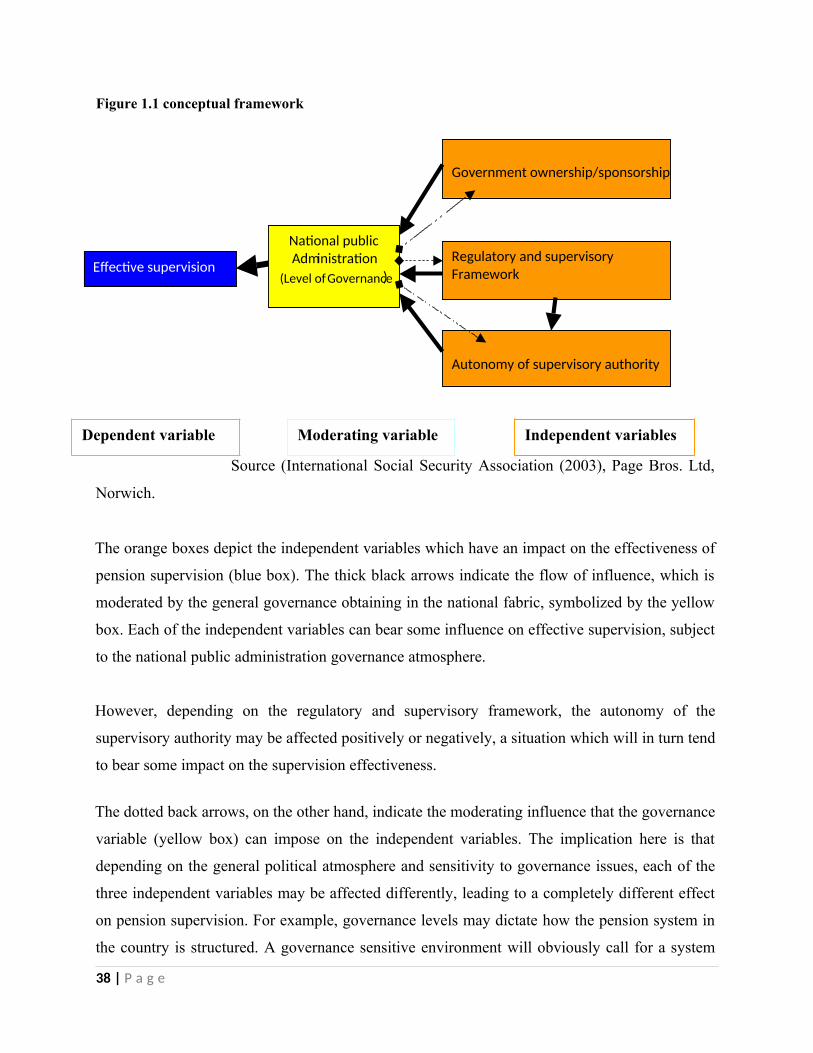

1.5 Hypotheses

The general hypothesis in this study is that one of the critical elements of governance, the

effective supervision of public pension schemes in Zambia, has been compromised through state

ownership. The working hypotheses may therefore be itemized as follows:

1.5.1 The supervision of public pension funds is negatively affected by government ownership

of the pension funds;

1.5.2 The regulatory and supervisory framework has an influence on the supervisory

effectiveness of public pension schemes;

1.5.3 The more autonomous the supervisory authority is, the more effective is its supervision of

pension funds;

1.5.4 The structure of the pension regulatory and supervisory framework has an impact on the

autonomy of the supervisory authority;

1.5.5 The level of governance in the general public administration has moderating influence on

all factors that affect pension supervision.

1.6 Research questions

Drawing strength from the above hypotheses, the study will seek to answer the following main

research question: To what extent does state involvement in the ownership of public pension

schemes in Zambia account for the variance in the effectiveness of the supervisory authority of

PIA over LASF, PSPF and NAPSA? The following are the subsidiary questions:

17 | P a g e

1.6.1 Is the Zambian pension supervisory authority adequately armed with authority to supervise

public pension schemes, such as LASF, PSPF and NAPSA, effectively?

1.6.2 What limitations does PIA have in relation to the supervision of public pension schemes?

1.6.3 Does the fact that LASF, PSPF and NAPSA are state-owned make it difficult for PIA to

enforce compliance on the two schemes?

1.7 Scope of the study

The focus of this study is on the supervision of NAPSA in relation to the supervisory regulations

of LASF and PSPF, of which these are government guaranteed pension schemes established

under their own respective statutes. NAPSA being an institution chosen specifically because it is

one of the public schemes whose conduct and governance practices have raised eyebrows on

many occasions in the past, provoking wide public criticism. Of which it tends to have an aspect

of notoriousness for failing to honour the “pension promise” to their beneficiaries raising fears

of un-sustainability, poor governance and other related controversies.

However, in order to make meaningful comparisons, the study will be extended to some private

Fund Managers4 as well as PIA which is the supervisory authority. The idea is to delve into the

actual practices of supervision of the pension schemes from the point of view of all the

supervisees and compare with what the supervisor states as the actual practices from their point

of view.

1.8 Significance of the study

This study is significant to the understanding of pension supervision, particularly as it relates to

the quest for effective pension governance. The research findings are expected to provide

guidance to policy makers by providing a basis on which they can draw experiences and lessons

to be used in future. The study is also expected to contribute to the existing body of knowledge,

4 All the private pension schemes in Zambia are affiliated to any one of the Fund Managers or multi-employer trusts, by definition.

18 | P a g e

especially having noted that the subject of governance in pension schemes appears not to have

benefited so much of research. It is therefore hoped that this study will form some basis on

which further research on the subject matter can be undertaken in future.

1.9 Organization of the study

The rest of the study is organized in four chapters. Chapter two reviews the literature and otherrelated issues expounded by many scholars on governance in general and as it specificallyapplies to pension plans. The first part of the chapter elaborates how the pension industry inZambia is organized and the framework under which it conducts business. The second part ofthe chapter examines the various literature on governance before undertaking a detailed reviewaimed at developing a theoretical framework that brings out the specific elements that are takeninto account in the supervision of pension plans, which will then be used to establish the scalefor measuring the intensity, scope and dimensions of pension supervision in Zambia. Thechapter also reviews related case studies and other experiences;

Chapter three explains the process followed in the study, including the design and

methods that the research employed.

Chapter four analyses the captured data and lays a framework for drawing inferences on

factors that have a bearing on the effective supervision of pension schemes.

Chapter five draws conclusions from the analysis of the findings. The chapter also makes

recommendations on how pension supervision in the Zambian public sector can be

improved.

CHAPTER TWO

19 | P a g e

2.0 LITERATURE REVIEW

2.1 Introduction

Chapter three explores the various studies and writings that are available on the subject matter.

The exploration begins with a focus on the organization and structure of the pension industry in

Zambia. It then reviews the concept of corporate governance in general and describes the global

governance framework for pension schemes as adopted and recommended by OECD. The

chapter goes further to identify and analyze the specific elements that are critical in the

governance framework of a pension system. Also identified in this chapter are the various

variables that impact on the supervisory effectiveness of the pension system in Zambia, which

infact forms the most critical component of this study.

2.2 Structure of the pension industry in Zambia

The various forms of literature that have attempted to catalogue and describe the organization of

financial and non-financial institutions in Zambia clearly agree that the pensions industry

exhibits characteristics of a typical three-pillar profile which comprises the compulsory,

occupational or optional and self-formalized schemes. The literature also converge on the

understanding that all of the pension schemes in Zambia are focused on covering formal

employees and none is covering the unemployed or those in the informal sector, at the moment.

One of the most apt analysis and description of this industry is authored by Muna Hantuba

(2005) who describes the first pillar as a compulsory savings pillar that provides benefits only to

contributors and, in general, provides the most benefits to those who contribute most. Hantuba

asserts that this pillar is mandatory and pre-funded in a fashion similar to a payroll tax, with

penalties for non-compliance. It is popularly known as NAPSA and is managed by a statutory

body supervised by a semi-independent board. NAPSA is a social security pension scheme for

both private sector and parastatal employees, implemented in February 2000. The scheme

operates on a defined benefit basis. Membership is compulsory for all regularly employed

persons, except for a few exceptions, at the present time. It is designed to provide a basic

pension only. NAPSA has accumulated assets of at least ZMK4 1.2 trillion (USD 262 million)

20 | P a g e

as at December 2004 for an estimated 350,000 members from 12,500 contributing employers.

The other notable statutory scheme under this pillar is the Workers and Pneumonoconosis

Compensation Funds that address disability benefits i.e. injury protection to all private and

public sector employees except the police and armed forces.

Pillar two, according to Hantuba, is basically tied up to the respective employers and is mostly

funded or underwritten. It comprises private and occupational schemes, which are expected to

augment the basic minimum pension under NAPSA. The pensions registry (PIA, 2004) reflects

that there are over 240 private or occupational pension schemes currently operating in Zambia,

covered by at least seven dedicated fund managers. Official figures indicate that the total assets

under management are estimated at ZMK 772 billion (USD 169 million) as at December 2004

for an estimated 52,577 members as at June 2004.

In addition, the two public pension schemes PSPF and LASF, which are self-managed, fall under

this pillar.

PSPF covers retirement benefits for civil servants and other qualifying quasi-government

entities. The PSPF is a funded defined benefit scheme established by Act No. 35 of 1996 Cap

260 of the Laws of Zambia. The scheme has a membership base of at least 107,241 active

members and 54,000 pensioners and beneficiaries. It is run by a Board, whose functions are to

control and administer the scheme in accordance with sound business practices and in the best

interest of the members of the scheme subject to the provisions of the Act. The scheme is

currently under severe financial stress, having a projected actuarial deficit of ZMK 3.87 trillion

as at December 2004 against an estimated asset of ZMK 437 billion.

LASF covers benefits for an estimated 22,907 local government employees and has assets of

approximately ZMK 47 billion as at December 2004. It is also believed to be in serious deficit,

although that cannot be confirmed due to lack of actuarial valuation, which the scheme has not

been subjected to in a long while.

The third pillar is a formal voluntary savings pillar available to anyone who wants to supplement

the retirement income provided by the first two pillars. The law allows operations of personal

21 | P a g e

retirement schemes such as life policies. There is insignificant activity with regard to this pillar

as it is mainly sold as an endowment product which is still unpopular, given the experience of

failed instruments by providers before liberalization of the market in the early 1990s. This pillar

also caters for individual retirement plans for professionals and generally high net worth

citizens.

The social security legislation under Income Tax Act of 1966 was recently strengthened by the

enactment of laws to oversee the operations of the market. The PIA was established in 1998 and

the social security activities are now regulated by the Pensions and Insurance Act and the

Pension Scheme Regulation Act of 1996, the Income Tax Act 1966 as amended and the Ministry

of Labor and Social Security. The investment activities are also regulated by other financial

services regulations such as the Banking and Financial Services Act and the Securities and

Exchange Commission Act. These statutes are what basically constitute the legal and

governance framework within which the pension industry operates.

2.3 The concept of corporate governance

According to the European Union’s white paper on governance, the term "governance" is a very

versatile one. It is used in connection with several contemporary social sciences, especially

economics and political science. It originates from the need of economics (as regards corporate

governance) and political science (as regards State governance) for an all-embracing concept

capable of conveying diverse meanings not covered by the traditional term "government".

Referring to the exercise of power overall, the term "governance", in both corporate and State

contexts, embraces action by executive bodies, assemblies (e.g. national parliaments) and

judicial bodies (e.g. national courts and tribunals).

The term "governance" corresponds to the so-called post-modern form of economic and political

organizations. According to the political scientist Roderick Rhodes, the concept of governance is

currently used in contemporary social sciences with at least six different meanings: the minimal

State, corporate governance, new public management, good governance, social-cybernetic

systems and self-organized networks.

22 | P a g e

The context of this paper, however, would be more interested in the meaning of "Corporate

governance” which is described more aptly by J. Wolfensohn, president of the World Bank, as

the principle of promoting corporate fairness, transparency and accountability5. Even though it

may not be representative of a universal definition, this loose description of corporate

governance highlights three key elements that have given credence to the study of this subject

matter, which are fairness, transparency and accountability. The concept of corporate

governance is defined in several ways because it potentially covers the entire gamut of activities

having direct or indirect influence on the financial health of the corporate entities. As a result,

different people have come up with different definitions, which basically reflect their special

interests in the field.

It is quite useful to recall the earliest definition of Corporate Governance by the Economist and

Noble laureate Milton Friedman. According to him, Corporate Governance is to conduct the

business in accordance with owner or shareholders’ desires, which generally will be to make as

much money as possible, while conforming to the basic rules of the society embodied in law and

local customs. This definition is based on the economic concept of market value maximization

that underpins shareholder capitalism. Apparently, in the present day context, Friedman’s

definition is narrower in scope. Over a period of time the definition of Corporate Governance

has been widened. It now encompasses the interests of not only the shareholders but also many

stakeholders and particularly the way those interests are protected.

The Cadbury Report6 of the UK, which is one of the most globally cited reports and authorities

on corporate governance, defines corporate governance as the system by which companies are

directed and controlled. Boards of directors are responsible for the governance of their

companies. The shareholders’ role in governance is to appoint the directors and the auditors and

to satisfy themselves that an appropriate governance structure is in place. The responsibilities of

the board include setting the company’s strategic aims, providing the leadership to put them into

effect, supervising the management of the business and reporting to shareholders on their

5 As quoted by an article in the Financial Times (UK), June 21, 1999 6 Chaired by Sir Adrian Cadbury, the Report was set up by the London Stock Exchange in May 1991 to draft a code of practices to assist corporations in U.K. in defining and applying internal controls to limit their exposure to financial loss

23 | P a g e

stewardship. The board’s actions are subject to the laws and regulations and the shareholders in

general meetings.

The Report further states that within that overall framework, the specific financial aspects of

corporate governance are the way in which boards set financial policy and oversee its

implementation, including the use of financial controls and the process whereby they report on

the activities and progress of the company to the shareholders. The role of the auditors is to

provide the shareholders with an external and objective check on the directors’ financial

statements which form the basis of that reporting system. Although the reports of the directors

are addressed to the shareholders, they are important to a wider audience, not least to employees

whose interests boards have a statutory duty to take into account.

2.4 Historical perspective of corporate governance

The Watergate Scandal in the United States is believed to have provided the original impetus to

the need for corporate governance. As a result of subsequent investigations, United States

regulatory and legislative bodies were able to highlight control failures that had allowed several

major corporations to make illegal political contributions and to bribe government officials. This

led to the development of the Foreign and Corrupt Practices Act of 1977 in USA that contained

specific provisions regarding the establishment, maintenance and review of systems of internal

control.

This was followed in 1979 by the Securities and Exchange Commission of USA’s proposals for

mandatory reporting on internal financial controls. In 1985, following a series of high profile

business failures in the USA, the most notable one of which being the Savings and Loan

collapse, the Treadway Commission was formed. Its primary role was to identify the main

causes of misrepresentation in financial reports and to recommend ways of reducing incidence

thereof. The Treadway report published in 1987 highlighted the need for a proper control

environment, independent audit committees and an objective Internal Audit function. It called

for published reports on the effectiveness of internal control. It also requested the sponsoring

organizations to develop an integrated set of internal control criteria to enable companies to

improve their controls.

24 | P a g e

Accordingly, the Committee of Sponsoring Organizations was born. The report produced by it in

1992 stipulated a control framework, which has been endorsed and refined in the four

subsequent UK reports: Cadbury, Rutteman, Hampel and Turnbull.

While developments in the United States stimulated debate in the UK, a spate of scandals and

collapses in that country in the late 1980s and early 1990's led shareholders and banks to worry

about their investments. These also led the Government in UK to recognize that the then existing

legislation and self-regulation were not working.

Companies such as Polly Peck, British & Commonwealth, BCCI, and Robert Maxwell’s Mirror

Group News International in UK were all victims of the boom-to-bust decade of the 1980s.

Several companies, which saw explosive growth in earnings, ended the decade in a memorably

disastrous manner. Such spectacular corporate failures arose primarily out of poorly managed

business practices.

It was in an attempt to prevent the recurrence of such business failures that the Cadbury

Committee, under the chairmanship of Sir Adrian Cadbury, was set up by the London Stock

Exchange in May 1991. The committee, consisting of representatives drawn from the top levels

of British industry, was given the task of drafting a code of practices to assist corporations in

U.K. in defining and applying internal controls to limit their exposure to financial loss, from

whatever cause.

2.5 The governance framework for pension schemes

The literature available from the world’s social security realm, including documents from the

International Social Security Association (ISSA), Canadian Association of Pension Supervisory

Authorities (CAPSA), International Monetary Fund (IMF), World Bank and OECD, do

converge on the premise that pension funds function on the basis of agency relationships

between members and beneficiaries, on the one hand, and the persons/entities involved in the

administration of or financing of the scheme, such as the scheme sponsor and scheme

administrator, on the other. The governance of these schemes consists of all the relationships

between the different entities and persons involved in the functioning of the pension scheme.

Governance also provides the structure through which the objectives of the pension scheme are

25 | P a g e

set, and the means of attaining those objectives and monitoring performance. It is the mirror

image of the corporate governance of a public limited company, which consists of the set of

relationships between the company’s management, board, shareholders and other stakeholders

(OECD, 2002).

Although there are existing differences in the operation of pension funds in OECD countries, it

has been accepted that these differences should not obscure the fact that pension funds are set up

with one common objective of serving as a secure source of income funds for retirement

benefits. In this respect, it is universally agreed that regulations on pension governance need to

be framed under this overriding objective (Sunday Times of Zambia, 2005).

OECD (2002) postulates that the central figure in the pension fund governance is the governing

body, the board of trustees – i.e. the person, group of persons, or legal entity responsible for the

management and safeguarding of the pension fund. The governing body is subject to various

forms of external oversight. At one level, the governing body may be monitored by special

committees set up specifically for this purpose (e.g. a supervisory board or oversight committee,

whose members may be elected by scheme members or beneficiaries). At another level,

regulations require independent professionals such as actuaries, auditors and custodians to

monitor and report on the compliance of the governing body with relevant legislation. Finally,

the governing body is subject to the supervision of relevant authorities. The regularity and detail

of the oversight exerted by the supervisory authorities will vary depending on the complexity of

the pension system and the specific role of actuaries, auditors and custodians (OECD, 2002).

OECD recommends two dimensions to the framework for the development of governance

guidelines or regulations, regardless of the country to country variations in the practical

implementation. These dimensions take the form of the governance structure, on one hand, and

the governance mechanisms on the other.

The governance structure should ensure an appropriate division of operational and oversight

responsibilities, and the accountability and suitability of those with such responsibilities.

Elements under governance structure include issues of mandate as well as legal and regulatory

26 | P a g e

provisions. Specifically, OECD (2002) recommends the following elements to appear in the

governance structure of a pension Fund if effective supervision is to be attained:

2.5.1 Identification of responsibilities – there should be a clear identification and assignment of

operational and oversight responsibilities in the governance of a pension fund;

2.5.2 Governing body – every pension fund must have a governing body or administrator vested

with the power to administer the pension fund and who is ultimately responsible for

ensuring the adherence to the terms of arrangement and the protection of the interests

of scheme members and beneficiaries. The responsibilities of the governing body

should be consistent with the overriding objective of a pension fund which is to serve

as a secure source of retirement income;

2.5.3 Expert advice - where it lacks sufficient expertise to make fully informed decisions and

fulfill its responsibilities, the governing body could be required to seek expert advice

or appoint professionals to carry out certain functions;

2.5.4 Auditor – an independent auditor of the pension entity, the governing body and the scheme

sponsor should be appointed by the appropriate body or authority to carry out a

periodic audit consistent with the needs of the arrangement. What is also critical here

is where that auditor reports and what mechanisms are in place to take remedial

action in cases where the pension fund is found wanting;

2.5.5 Actuary – an actuary should be appointed by the governing body for all defined benefit

plans financed via pension funds. As soon as the actuary realises, on performing his

or her professional or legal duties, that the fund does not or is unlikely to comply

with the appropriate statutory requirements and depending on the general supervisory

framework, he or she shall inform the governing body and - if the governing body

does not take any appropriate remedial action - the supervisory authority without

delay;

27 | P a g e

2.5.6 Custodian – Custody of the pension fund assets may be carried out by the pension entity,

the financial institution that manages the pension fund, or by an independent

custodian. If an independent custodian is appointed by the governing body to hold the

pension fund assets and to ensure their safekeeping, the pension fund assets should be

legally separated from those of the custodian. The custodian should not be able to

absolve itself of its responsibility by entrusting to a third party all or some of the

assets in its safekeeping;

2.5.7 Accountability – The governing body should be accountable to the pension plan members

and beneficiaries and the competent authorities. The governing body may also be

accountable to the plan sponsor to an extent commensurate with its responsibility as

benefit provider. In order to guarantee the accountability of the governing body, it

should be legally liable for its actions;

2.5.8 Suitability – The governing body should be subject to minimum suitability standards in

order to ensure a high level of integrity and professionalism in the administration of

the pension fund.

On the other hand, governance mechanisms are critical, according to the OECD model. Pension

funds should have appropriate control, communication, and incentive mechanisms that

encourage good decision making, proper and timely execution, transparency, and regular review

and assessment. Elements specified by OECD under governance mechanisms are as follows:

2.5.9 Internal controls – There should be appropriate controls in place to ensure that all persons

and entities with operational and oversight responsibilities act in accordance with the

objectives set out in the pension entity's by-laws, statutes, contract, or trust

instrument, or in documents associated with any of these, and that they comply with

the law. Such controls should cover all basic organizational and administrative

procedures; depending upon the scale and complexity of the plan, these controls will

include performance assessment, compensation mechanisms, information systems

and processes, and risk management procedures;

28 | P a g e

2.5.10 Reporting – Reporting channels between all the persons and entities involved in the

administration of the pension fund should be established in order to ensure the

effective and timely transmission of relevant and accurate information;

2.5.11 Disclosure – The governing body should disclose relevant information to all

Parties involved (notably pension plan members and beneficiaries, supervisory

authorities, etc.) in a clear, accurate, and timely fashion;

2.5.12 Redress – Pension plan members and beneficiaries should be granted access to statutory

redress mechanisms through at least the regulatory/supervisory authority or the courts

that assure prompt redress.

Clearly, the guidelines recommended by OECD provide a considerably plausible route for

acceptable governance practices and safeguarding pension interests. However, the problem with

discussing any form of governance is that no matter how attractive the model might appear, the

reality is that actual implementation usually falls below the desired quality. Various critiques of

pension governance models argue that a model that is devoid of inherent bottlenecks is yet to be

developed. Despite the comprehensiveness of the OECD model, it has also been criticized for its

lack of depth in practicality.

According to Golinowska and Kurowski (2000), the appropriateness and effectiveness of

specific risk and governance solutions in a pension system largely depends on factors that

characterise a given country’s situation: its level of economic development, the population’s

affluence, traditions of business culture and co-operation, etc. The safe and effective operation

of pension funds in a given country requires a proper set of tools that do not necessarily have to

be universal, but whose deviation from the general rules should not be so numerous as to change

the basic mechanism of the instruments’ functioning. And if these deviations do occur, they

should be rationally justified. When constructing these instruments, the legislator faces many

dilemmas. These may result from the contradiction between the goals of the system’s new

institutions and the tasks of the instruments used to safeguard against risks. What is critical

29 | P a g e

though is to ensure that the dilemmas are given detailed consideration at the point of

constructing the instruments.

2.6 Primary elements of supervision

Evidently though, not much study has been devoted to the examination of the practicalities of

pension governance models worldwide, particularly as relates to the element of supervision.

Currently, global institutions such as the IOPS, World Bank, OECD etc. Are actively engaged in

the pursuit of extended exploration and understanding of the successes and failures of pension

regulatory and supervisory structures. Although there is a growing body of work on the theory

and economics of pension systems, this tends to be focused on the financial implications and

consequences of these arrangements, rather than on understanding their operation and oversight.

Very little consideration has been given to the way schemes are supervised and to the factors

that determine relationships between the design of pension systems, the environment in which

they operate and the manner in which supervision is most effectively undertaken.

The body of literature that is well cited in the area of effective pension supervision includes

studies by Mataoanu (2004) and Hinz and Mataoanu (2005), who stress that maintaining

effective pension regulatory and supervisory structures that secure the interests of the

participants and beneficiaries is crucial for systemic stability and economic growth. Mataoanu’s

(2004) study focuses on the supervision of privately managed, defined contribution pension

systems and attempts to clarify key factors that determine the setting and operational activity of

pension supervisory structures. Hinz and Mataoanu, on the other hand, propose an approach to

classifying and measuring the primary elements of pension supervision.

Like in much other literature relating to the subject matter of pension supervision, the starting

point of both analyses is the OECD’s model on pension governance. Examined to greater detail,

the OECD’s framework brings out six basic and functional elements of supervision, namely

monitoring, licensing, communication, measurement, intervention and correction (OECD, 2004),

which are expounded in the theoretical framework that follows.

30 | P a g e

2.7 Theoretical framework

In considering the factors that influence the variations in supervisory effectiveness, it is

necessary to organize and classify the elements so as to set a framework for clearly discerning

the various variables involved and the inter-linkages at play. As earlier highlighted in preceding

paragraphs of the literature review, the activities of pension supervisors can be considered in six

primary categories, i.e. licensing, monitoring, analysis, intervention, correction and

communication. This framework will briefly describe each of the six elements of pension

supervision and proceed to discuss the potential variables there from and suggest how they

impact on supervision. A point to note is that although this framework is public-sector based, it

has been adapted from the private pension framework propounded by Hinz and Mataoanu (2005)

in their study of the international practice and country context of pension supervision. A step-by-

step theoretical framing of the six elements, in the public-domain context, follows hereunder.

2.7.1 Licensing

Licensing activities restrict and control entry to the pension market through procedural

requirements and criteria. These are commonly applied to pension funds or the entities that are

permitted to sponsor or operate them. They can also be extended to individuals who perform

important functions in the pension system, for example trustees, or to firms or individuals that

are qualified to provide services, for example, to actuaries who valuate the status of benefit

plans. The modalities in which this function is exercised differ widely across different systems,

but in essence, they all make use of a set of predetermined criteria to establish an entry barrier or

select a limited number of entrants. Licensing is differentiated among pension systems by its

restrictiveness, depth, and periodicity. Some systems have virtually no entry barriers while

others have very complex and strict standards applied by the supervisor.

31 | P a g e

2.7.2 Monitoring

Monitoring activities collect information to enable the supervisor to track the status and actions

of the pension funds within its jurisdiction. Monitoring commonly takes the form of required

submissions of information on a regular basis or periodic reports to the supervisor. It also

includes a range of other reporting requirements or more active forms of information collection.

The common attribute is the provision of information that will either provide the basis for

judgments or actions by the supervisor or through its provision or disclosure make the activities

of the pension funds more transparent. Potential recipients and users of monitoring include

supervisors as well as the members of funds.

Monitoring activities can be defined in terms of the scope and content of the information that is

collected as well as the mode of collection. Common types of information collected include

financial statements, schedules of transactions, information on individuals responsible for

important aspects of fund operations (trustees, administrators, Boards of Directors), actuarial

analyses and information on the sponsors of pension funds. Monitoring is often a passive

activity on the part of the supervisor in which information is required to be submitted by the

relevant institutions or individuals. It may also be a pro-active function in which the supervisor

periodically goes on site to collect specific or supplementary information. Supervisors may also

monitor the media for information, have regular exchanges of information or consultations with

other supervisors, and have regular programs of meetings with pension funds to collect

information. An important form of monitoring is establishing venues for individuals or fund

members to communicate with the supervisor and to request scrutiny of a particular fund or

activity. A distinctive type of this approach is the so called “whistleblower” requirements of

some systems, which assign responsibility to certain individuals or parties to report knowledge

of improprieties to the supervisor. Some monitoring systems also use independent third parties

such as auditors or credit rating agencies to produce or verify information.

Monitoring varies in terms of the type, scope, and depth of the information that supervisors seek

to utilize, as well as the parties who provide the information and the periodicity of the collection

of information.

32 | P a g e

2.7.3 Communication

Supervisors engage in a full range of activities to communicate with pension funds. These are

essentially a complement to monitoring activities, except in this case the flow of information is

from the supervisor to the funds. This can make it difficult to clearly separate the two in many

instances. Supervisors may communicate with the funds through the provision of regular reports

on the industry, by announcing their priorities and compliance strategy, or by publicizing

compliance actions. They may also engage in interactive communication by placing inspectors

on site and engaging in daily communication, by meeting regularly with the funds to discuss

issues of mutual interest or through more formal processes in which changes in the activities of

the funds are suggested and issues resolved through negotiation. Supervisors may also undertake

programs of outreach, education, and training to enhance the knowledge of the legal

requirements or operation of pension systems. Supervisors often seek to communicate with a

range of parties including fund managers, service providers, members, and the public.

Communication activities of supervisors have a wide range of goals and objectives. Some

communication programs may have the purpose of informing pension funds about the intent and

nature of the supervisor’s activities to maximize the capacity for cooperation and make the

interactions with fund more efficient. Others are intended to advance the understanding of the

regulatory structure as well as rights and responsibilities of funds and their members to facilitate

compliance with the rules or to advance the exercise of individual rights of action by members.

Communication may also be intended to leverage resources and establish a climate of deterrence

among funds by publicizing the enforcement actions of the supervisor.

Basic types of communication by supervisors are disclosure, outreach and educational activities

and training. Communication is differentiated among pension systems by the scope and purpose

of the activities. Supervisory systems that impose strong controls and have little reliance on

external or market processes are very directive in their communication with funds regarding

compliance issues, and they are likely to engage in few activities designed to facilitate

compliance or enhance deterrence. Systems with more procedurally oriented standards or a

greater reliance on external processes will engage in a more interactive communication process.

33 | P a g e

They will typically have far more extensive outreach and education programs that support

negotiated settlement of compliance issues and rely on deterrence and third party actions to

support direct compliance activities.

2.7.4 Analysis

The manner and extent to which supervisors analyze and evaluate the information they receive

from pension funds is usually closely linked to the system’s legal and regulatory approach. Legal

frameworks that are based on quantitative standards lead supervisors to extensive measurement

efforts that compare funds’ financial status and activities to normative standards. Measurement

of supervisory effectiveness using the analysis element is usually evaluated on the basis of the

purpose, frequency, and intensity of the activity.

2.7.5 Intervention

All supervisory programs are continually faced with decisions about whether and how to

intervene in the operation of pension funds. It is often difficult to separate intervention from

some of the key aspects of the communication with the funds. Interventions may take the form

of explicit requirements for the fund to either undertake, or desist from engaging in, certain

activities that carry the force of law and must be complied with immediately. In other systems

interventions may be in the form of findings that are presented to the funds for a response. The

process of intervening in these circumstances is likely to be in the form of negotiations in which

issues are resolved, or a process of litigation through the civil courts, where the ultimate

resolution is reached through a judicial process. A key issue that defines the nature of

interventions is the force of authority given to the supervisor and the nature of the process

through which interventions occur. In some countries, the supervisor simply has the authority to

intervene when a finding is made that a fund is, or may be, approaching non-compliance. Fund

managers may in some cases be provided with very little if any recourse to negotiate or appeal.

In other countries, the supervisor has little capacity to unilaterally impose sanctions and instead

intervenes through a far less directive process of consultation, notification and perhaps

negotiation. The most basic and important feature of the notification of compliance actions is the

manner in which individual funds are notified by the supervisor when they are deemed to be out

34 | P a g e

of compliance with legal requirements. This can range from regularly scheduled interaction that

may occur as often as daily in some countries, to formal notices. In some cases there are simply

directives from the supervisor to the fund to make changes. The manner of this sort of

intervention and the nature of the process that follows, whether it is completely directive or a

form of negotiated settlement, is perhaps the aspect of the supervisor’s activities that most

defines the nature and style of supervision. Another key variation is the involvement of third

parties in interventions. Some systems require that all actions be taken through the courts. Others

establish a formal process of appeal to a specially constituted group. Interventions by

supervisors are therefore differentiated partially by the degree to which they are pro-active or

occur only after conclusive evidence of non-compliance is established. They are also

distinguished by the extent to which they are directive and represent the unilateral exercise of

authority to which there is little or no appeal, or conversely are a process of negotiation and

adjudication.

2.7.6 Correction

As is the case with any form of compliance enforcement, one of the most important elements ofpension supervision is the capacity of the supervisor to take corrective actions. Three basic typesof corrective actions can be delimitate: Punitive, remedial and compensatory. Supervisoryprograms may engage in all three types or may be limited exclusively in their authority to onlyone. Punitive actions are designed to impose penalties on the funds for actions deemed to beadverse to the interest of members. They are distinguished by both form and intent. Penalties areusually fines that are paid to the supervisory and may be retained by the authority or become partof public revenues. Their intent is to establish deterrence and punish behavior outside of thestandards.

Remedial actions are those taken by a supervisory authority to remedy the consequences offailure to comply with the law. These are essentially a way to reverse the outcome of thenoncompliance. Remedial sanctions may simply be requiring the fund to return to a prior statusor to cease in certain actions. In some cases this may involve financial sanctions that are limitedto any direct result of negligence or malfeasance by responsible parties. Compensatory correctiveactions go beyond the remedial outcomes and seek to compensate aggrieved parties for both thedirect and indirect effects of violations. These types of actions have a strong deterrent intent butalso have the purpose of ensuring that harm is minimized. Corrective activities of supervisory aredistinguished by the degree to which they are solely focused on remedial outcomes, correctingproblems as they occur or whether they extend into the arena of compensation and punitiveprovisions that attempt to establish a more self-enforcing regime of deterrence.

35 | P a g e

The primary intent of these corrective actions is to rectify any direct negative outcomes and

prevent a recurrence. In our study of supervisory effectiveness, this element is critical

considering that it can singularly give us an impression on a supervisory body’s capacities and

limitations in terms of authority.

There is no doubt, generally, that given an appropriate environment, an intense application of the

six elements of pension supervision would uphold effectiveness. In developed countries, studies

have been undertaken to confirm this hypothesis, particularly in the case of private pension

schemes. Although there is no empirical evidence to show for it (which is partly reason for this

study), arguments have been advanced to claim that infact the supervision of private pension

schemes in Zambian has been very effective, to such an extent that justification has been

established to advocate for the complete privatization of the social security system in the country

(Hantuba, 2005).

2.7.7 The variables that impact on pension supervision

The theoretical argument advanced by this study is that there are four variables that influence

effectiveness of the supervising authority on public pension schemes in Zambia, three of which

are independent while the fourth one is a moderating variable. The following are the independent

variables which impact on effective supervision of public pension schemes:

2.7.7.1 Government ownership and/or sponsorship of the Fund

The fact that public pension schemes are sponsored by the state makes it practically difficult for

the supervising authority, which is also a government institution to effectively police these

schemes. In the case of PSPF, it is even worse because the superintending Ministry for the

scheme also superintends over PIA, i.e. the Minister of Finance is in charge of both the Pension

Fund and the supervisory authority. Issues of oversight are extremely difficult under such

circumstances. The influence of this dilemma may not be obvious, but it certainly is implied.

Even though neither side would want to admit it, certain actions or lack of certain actions infact

signify the dilemma that PIA is faced with.

2.7.7.2 Regulatory and supervisory framework

36 | P a g e