cash management group solvency ii and money … · overview solvency ii is a risk-based framework...

TRANSCRIPT

Managing cash and short term investments is an essential

component of the portfolio asset allocation strategy for many

insurance companies. Under Solvency II, the new regulatory

framework for the European insurance industry, levels of

money market or cash investments held by insurance firms

may increase due to the likelihood that longer-term assets

considered to carry greater risk may attract higher capital

charges. As a result we believe it may be less “expensive” in

capital terms for insurance firms to carry relatively higher

levels of cash.

Today insurance companies are often familiar with triple-A

rated money market funds (MMFs) and many firms use them

to manage their short-term cash exposures; as a result

insurers will need to understand and consider the

implications of Solvency II for their MMF holdings.

Whilst regulatory regimes within the financial services

industry often allow cash investments to attract zero capital

charges, Solvency II will require new levels of differentiation

and capital weighting between cash instruments. This new

framework is intended to apply a more granular approach to

the various market risks associated with cash investments

and measure these exposures within an industry-recognised

capital framework.

At the time of writing, final clarification around the treatment

of certain instruments, including cash, remains outstanding.

Despite this uncertainty, this note aims to reflect our current

understanding of the Solvency II requirements as they

apply to MMFs and provide a number of observations that

we believe may be helpful to cash investors in the

insurance industry.

BlackRock and Solvency II

As a leading provider of asset management, risk management

and advisory services to institutional, intermediary and

individual clients worldwide, BlackRock is focused on assisting

its clients in understanding regulatory change wherever it

impacts the financial markets. With respect to Solvency II, we

believe BlackRock is uniquely positioned to help insurance firms

in understanding both its wider impact and targeting the

expected treatment of specific asset classes.

Through the expertise provided to investors via the BlackRock

Cash Management and BlackRock Financial Institutions

Groups, combined with the analytics, systems and technology

provided by the BlackRock Solutions® business we stand

ready to support the insurance industry as it adapts to

changing regulation.

In this paper we combine the insight and capabilities of these

businesses through both outlining our interpretation of how

BlackRock’s MMFs would be treated under Solvency II and

additionally highlighting our systems’ ability to support the

calculation and reporting of key measures.

BlackRock Solutions’ Green Package® analytics platform

already facilitates the full analysis of investments across asset

classes and the calculation of specific market risk exposures

based on our interpretations of the technical specifications of

QIS5 ,a component of the new regulations. BlackRock

recognises that the draft Level 2 text within the Solvency II

framework provides the most up-to-date definitions at this

time, but is potentially subject to amendment. As a result

content within this paper may be updated when the Level 2

text is finalised.

Examples in this note are provided to demonstrate the reporting

and calculation of MMF holdings through Green Package based

on the current QIS51 configuration. In the meantime BlackRock

would be pleased to work with any insurers who may be

completing analyses or preparing submissions based on the

current draft text.

Cash Management Group Solvency II and Money Market Funds

ThE oPInIonS ExPRESSED ARE AS oF JUnE 2012 AnD MAy ChAnGE AS SUBSEQUEnT ConDITIonS vARy.

1 At the request of the European Commission, CEIoPS – the Committee of European Insurance and occupation Pensions Supervisors (replaced by EIoPA – the European Insurance and occupational Pensions Authority as of January 1, 2011) – surveyed various European insurers between August and november 2010 in order to solicit quantitative input for the establish-ment of the Solvency II Framework Directive. This survey was called the fifth Quantitative Impact Study, or QIS5, and is the foundation for the calculations in Pillar 1. QIS5 provides detailed specifications for the valuation of assets and liabilities on an insurer’s balance sheet as well as the methodology for calculating capital requirements.

Overview

Solvency II is a risk-based framework denoting a collection of

regulatory requirements for insurance firms domiciled in

Europe, and including the European operations of

overseas insurers.

A key premise of the Solvency II framework is that a full

understanding of the risks inherent in an insurer’s businesses

(both assets and liabilities) is critical and an insurer should

allocate enough capital to cover these risks. Although this is by

no means a new concept, Solvency II looks to provide to

regulators a more extensive and detailed picture of the financial

situation of insurance companies and provide for appropriate

levels of capital allocation relative to the risks inherent within

their business models.

In summary, Solvency II aims to provide the European insurance

market with a comprehensive and consistent method to

measure the solvency margin of an insurance company where

the solvency margin is defined as the amount of regulatory

capital required to protect against unanticipated events.

How does Solvency II apply to MMFs?Under Solvency II, the Solvency Capital Ratio (SCR) is a key

indicator that ensures that insurance companies are able to

continue their operations and make good on their obligations

even in the event that they experience significant losses. In

calculating the SCR a number of risk modules are considered

including the Market Risk module which happens to be of most

relevance to MMFs.

Within the Market Risk module a number of factors are

considered and insurers must provide reporting for their

cash holdings for the risk areas listed below as part of their

SCR calculation:

a) Interest Rates – sensitivity of assets and liabilities to

changes in the term structure of interest rates or interest

rate volatility.

BlackRock’s MMF portfolios typically hold short-dated fixed

income instruments which tend to have relatively lower sensitivity

to changes in interest rates than longer-dated securities. As a

result the impact to the SCR calculation for this market risk factor

is expected to be low.

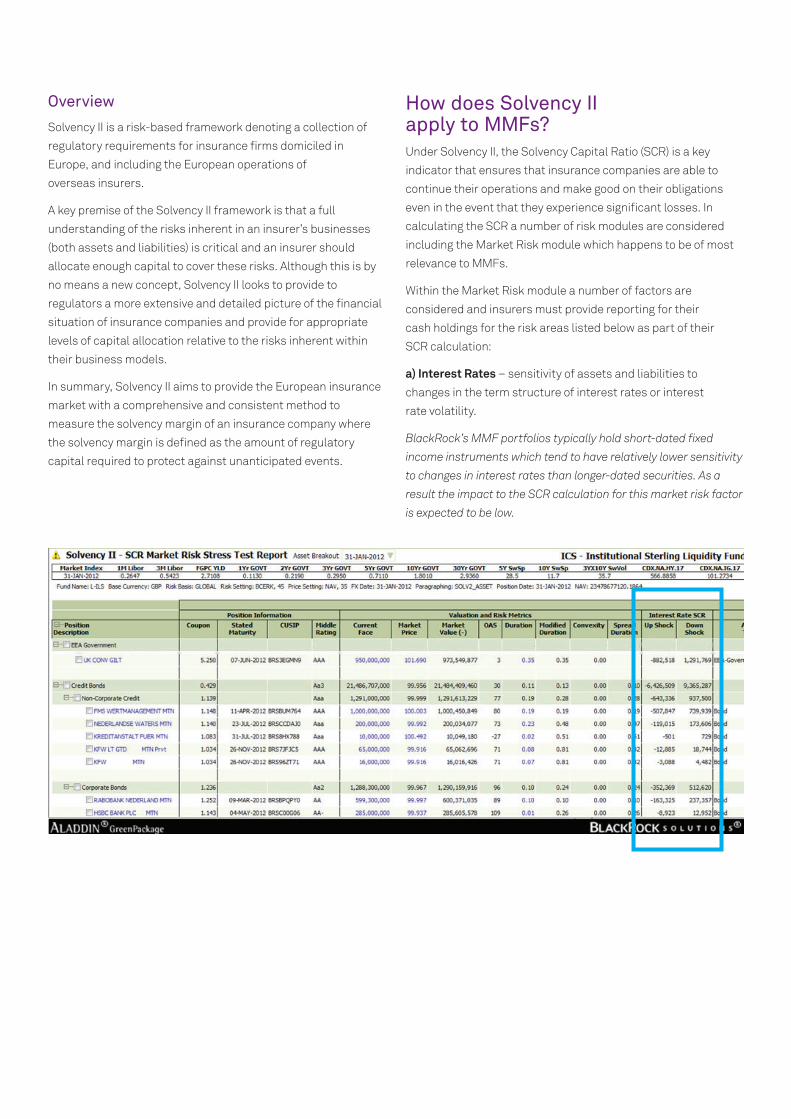

An example of interest rate SCR for the BlackRock ICS –

Institutional Sterling Liquidity Fund (calculated by BlackRock

Solutions on Green Package) can be seen below:

Analysis: The Interest Rate SCR column highlighted reflects the

impact to the levels of capital held against individual portfolio

securities should interest rates move up or down.

b) Credit Spreads – sensitivity to changes in the level or

volatility of credit spreads over the risk free interest rate term

structure. Instruments included within a MMF portfolio are

generally considered to carry lower credit risk than other

instruments. Typically they include money market instruments

such as certificates of deposit, time deposits, sovereign debt,

commercial paper and repurchase agreements.

Instruments held within BlackRock’s MMF portfolios are

generally of high credit quality and short term in duration2 and

these features are typically expected to result in relatively low

levels of price volatility. As a result the impact to the SCR

calculation for this market risk factor is expected to be minimal.

c) Currency Rates – sensitivity to the level or volatility of

currency exchange rates. Solvency II regulations denote that the

local currency defined as the currency in which the entity

prepares its financial statements will attract a zero capital

charge. All other reported currencies are referred to as

foreign currencies.

Foreign currency investments into MMFs will have a higher capital

charge than local currency. Our understanding is that these

investments will still benefit from the diversification provided by a

MMF when compared with other cash alternatives.

BlackRock MMFs typically do not take foreign currency

exposure and only invest in securities issued in the base

currency of the fund.

d) Issuer Concentration – assesses balance sheet exposure to

individual issuers. Debt that is issued or guaranteed by a

European Economic Area (EEA) national government in an EEA

currency or by an approved multilateral development bank or

international organisation does not receive a capital charge.

BlackRock’s MMFs are well diversified and adhere to strict

regulatory restrictions surrounding issuers, we therefore expect

that there will be a relatively lower capital charge for this risk

factor within our funds.

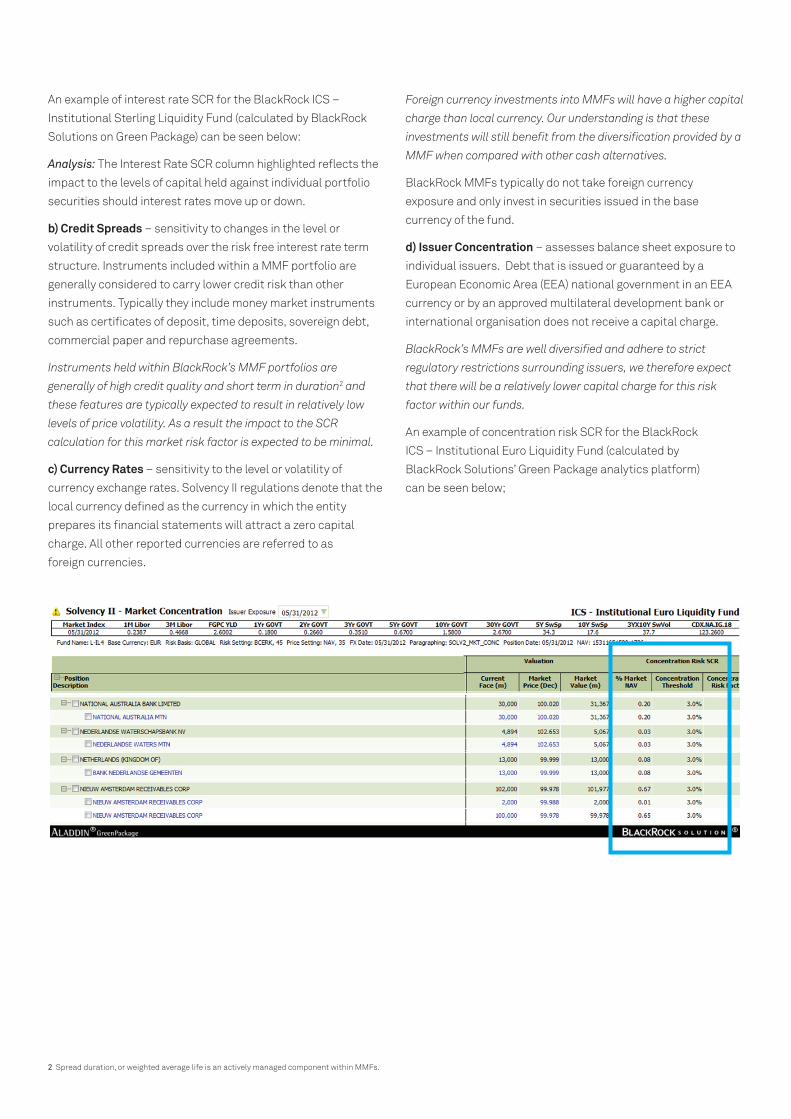

An example of concentration risk SCR for the BlackRock

ICS – Institutional Euro Liquidity Fund (calculated by

BlackRock Solutions’ Green Package analytics platform)

can be seen below;

2 Spread duration, or weighted average life is an actively managed component within MMFs.

Analysis: The highlighted box above highlights key data-points in

measuring concentration risk including; % Market nAv – the

percentage of a portfolio held in an individual security

Concentration threshold – the maximum permitted level within

a portfolio held in an individual security

Concentration risk factor – the ratio weighting resulting from the

concentration level of an individual portfolio security

Other relevant risks considered under Solvency II;

e) Counterparty Risk – features alongside the market risk

factors and focuses on the likelihood of a counterparty default.

BlackRock’s MMF portfolios have high levels of diversification

across counterparties regarded to be of high credit quality

including both non-government and government entities. We think

this should result in reduced levels of capital charge relative to

portfolios comprised of longer-dated and higher risk instruments.

In fact we believe there may well be an improvement in the SCR

due to this diversification.

There are additional risk factors stated within the QIS5

specifications which are not relevant to MMFs and relate to

equity markets, real estate and illiquidity premium risk.

In addition to Pillar I requirements for Solvency II, Insurers will

need to consider the Pillar III reporting guidelines with regards to

their MMF holdings. In particular the Complementary

Identification Code (CIC) is a Solvency II 4-character

alphanumeric security identification code. 3The CIC code is part

of Pillar III Quantitative Reporting Templates (QRT) and is

intended to classify investment securities characteristics and

risk exposures. The Quantitative Reporting Templates aim to

harmonize the Solvency II process and provide disclosure and

transparency into insurers’ Solvency Capital Requirements

calculated in Pillar I.

The CIC codes will need to be part of the security holdings input

data feeding into insurers SCR calculation engine and will be

relevant to the underlying holdings of MMF portfolios.

How is the SCR for MMFs reported?Given the requirement within the SCR to look at the market risk

factors of an insurer’s cash portfolio, it is prudent to assume

that MMFs will require modelling on a fully transparent look

through basis.

With reference to QIS5 there are three methodology options for

determining market risk under Solvency II:

Security level look-through – applies the market risk

factors mentioned previously to every security in the relevant

MMF portfolio

Portfolio level look-through – looks at the MMF prospectus

in order to determine the SCR calculation

No look-through – the investment has the potential to be

classified as other equities and would therefore be subject to a

49% capital charge

We believe that the most accurate representation of market risk

and the least capital intensive option will be via a full security

level look-through. As such, we feel that following this

methodology would result in a lower capital charge being applied

to a MMF allocation.

For example: Blackrock’s MMFs often invest in overnight

repurchase agreements that are 102% collateralised with highly

rated government bonds. Our interpretation is that these holdings

would not be subject to counterparty risk given the collateral

comprises government bonds and therefore should be viewed

favourably under any market factor risk assessment.

How can BlackRock’s Cash Management Group assist?In order to support our insurance client base in relation to the

security level look through, we are taking steps to expedite the

production of our schedule of investment (SoI) reports to satisfy

the reporting requirements connected with Pillar III.4 In addition,

we are exploring the development of online capabilities for a full

security level look through via a bespoke platform solution.

Through these steps and our on-going client dialogue our

objective is to ensure that we are as prepared as we can be to

assist our customers when Solvency II is implemented.

Additionally, through the BlackRock Solutions’ Green Package®

analytics platform we are working to assist the insurance

market through helping to facilitate the calculation of specific

market risk exposures for SCR.

3, 4 It was introduced in EIoPA’s draft pre-consultation proposal for Level 3 guidelines on Public Disclosure, Regular Supervisory Reporting and Predefined Events, which was circulated in January 2011.

Green Package will support a full range of risk assessments

based on QIS5 including interest rate, credit spread, currency,

equity market, and issuer concentration risk stress testing

components.

BlackRock remains committed to adapting our MMF range to

support our insurance investor base in this continually evolving

regulatory environment.

BlackRock Financial Institutions Group (FIG)

The BlackRock FIG team have produced a range of materials

supporting Solvency II including assessments of the treatment

of other non-cash asset classes under the regime. In particular,

“Balancing Risk, Return and Capital Requirements: The effect of

Solvency II on Asset Allocation and Investment Strategy”

(published by BlackRock - February 2012) has been created by

the FIG business in conjunction with the Economist Intelligence

Unit to help investors and others in the insurance industry in

their preparations.

For more information from the FIG group or to share your views,

please contact us through your Cash Management relationship

manager or by e-mail to: [email protected]

Conclusion

BlackRock is uniquely positioned to assist cash investors in

the insurance industry through its cash management

expertise, insurance specialisation and analytics platforms

While regulators are still finalising a number of questions

related to Solvency II, adopting a wait and see approach is not

an option

BlackRock remains ready to engage with investors to assist

them in their preparations

With respect to cash investments we believe the following

are key:

•Portfoliolevellook-throughwillresultinalowercapital

charge than zero portfolio look-through

•FulllookthroughonMMFportfoliosmayreducelevelsof

capital charge relative to single counter-party direct cash

deposits or other cash equivalents

•Concentrationriskistobeviewedacrossassetsand

liabilities in unison

•ForeigncurrencyinvestmentsintoMMFswillhaveahigher

capital charge than local currency

•ReportingrequirementsunderSolvencyIIwillincreasewith

an specific focus on transparency

BlackRock remains ready to support its insurance industry

clients throughout the transition to the new Solvency II regime.

We look forward to working with investors to develop effective

solutions serving their needs.

About BlackRock

BlackRock is a premier provider of asset management, risk

management, and advisory services to institutional,

intermediary, and individual clients worldwide. As of 30 June

2012, the firm manages USD 3.56 trillion across asset classes in

separate accounts, mutual funds, other pooled investment

vehicles, and the industry-leading iShares® exchange-

traded funds.

BlackRock Cash Management Group

BlackRock is an expert in liquidity management, managing an

estimated USD239 billion5 in short term cash assets for our

global client base and considers cash management a unique

investment discipline requiring a distinct skill set for effective

management. While our investment strategy is conservative in

nature, we strive to deliver competitive returns over time. We

understand the importance of putting safety and liquidity

first – not as a marketing message, but as the code of our

investment philosophy.

BlackRock Solutions®

Through BlackRock Solutions, the firm offers risk management

and advisory services that combine capital markets expertise

with proprietarily-developed analytics, systems, and technology.

BlackRock Solutions currently provides risk management and

enterprise investment services for USD 12 trillion in assets.

BlackRock serves clients in north and South America, Europe,

Asia, Australia, Africa, and the Middle East. headquartered

in new york, the firm maintains offices in 27 countries

around the world.

BlackRock Financial Institutions Group

BlackRock has unrivalled insights into the management of

insurance company assets. Its Financial Institutions Group

managed USD202 billion in unaffiliated general account assets

for 125 insurers in 22 countries as at the end of June 2012.

In addition to these asset management relationships, BlackRock

also provides risk management services to 75 insurers through

BlackRock Solutions.

5 As of 30 June 2012.

Please do not hesitate to contact us should you require any further information

Andrew [email protected]+44 (0) 20 7743 1105

This material is for distribution only to those types of recipients as provided below and should not be relied upon by any other persons. This material is provided for informational purposes only and does not constitute a solicitation in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. Moreover, it neither constitutes an offer to enter into an investment agreement with the recipient of this document nor an invitation to respond to it by making an offer to enter into an investment agreement.

one should consider the investment objectives, risks, charges and expenses of a money market fund carefully before investing. A fund’s prospectus contains this and other information and is available, along with information on all BlackRock Funds, by accessing the website at www.blackrock.com/cash. The prospectus should be read carefully before investing.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of yields or returns, and proposed or expected portfolio composition. Moreover, where certain historical information of any investment vehicles managed by BlackRock, Inc. and/or its subsidiaries (together, “BlackRock”) has been included in this material such performance information is presented by way of example only. Any changes to assumptions that may have been made in preparing this material could have a material impact on the market outlook that is presented herein by way of example.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of June 2012 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

This document contains general information only and is not intended to represent general or specific investment advice. The information does not take into account your financial circumstances. An assessment should be made as to whether the information is appropriate for you having regard to your objectives, financial situation and needs.

Issued by BlackRock Investment Management (UK) Limited, authorised and regulated by the Financial Services Authority. Registered office: 12 Throgmorton Avenue, London, EC2n 2DL. Tel: 020 7743 3000. Registered in England no. 2020394. For your protection telephone calls are usually recorded. BlackRock is a trading name of BlackRock Investment Management (UK) Limited.

Past performance is not a guide to future performance. The value of investments and the income from them can fall as well as rise and is not guaranteed. you may not get back the amount originally invested. Changes in the rates of exchange between currencies may cause the value of investments to diminish or increase. Fluctuation may be particularly marked in the case of a higher volatility fund and the value of an investment may fall suddenly and substantially. Levels and basis of taxation may change from time to time.

Any research in this document has been procured and may have been acted on by BlackRock for its own purpose. The results of such research are being made available only incidentally. The views expressed do not constitute investment or any other advice and are subject to change. They do not necessarily reflect the views of any company in the BlackRock Group or any part thereof and no assurances are made as to their accuracy.

This document is for information purposes only and does not constitute an offer or invitation to anyone to invest in any BlackRock funds and has not been prepared in connection with any such offer.

This material is for distribution to Professional Clients (as defined by the FSA Rules) and should not be relied upon by any other persons.

ThIS MATERIAL IS hIGhLy ConFIDEnTIAL AnD IS noT To BE REPRoDUCED oR DISTRIBUTED To PERSonS oThER ThAn ThE RECIPIEnT.

© 2012 BlackRock, Inc. All Rights reserved. BLACKRoCK, BLACKRoCK SoLUTIonS, ALADDIn, iShARES, LIFEPATh, So WhAT Do I Do WITh My MonEy, InvESTInG FoR A nEW WoRLD, and BUILT FoR ThESE TIMES are registered and unregistered trademarks of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

www.blackrock.co.uk/cash

004718–12 Jul

Please do not hesitate to contact us should you require any further information.

James [email protected]+44 (0) 20 7743 2231