cash and funding management for sponsored research business services division cross functional...

TRANSCRIPT

Cash and Funding Management for

Sponsored Research

Business Services Division

Cross Functional Training

March 31, 2004

Welcome

Jeff Weiner

Sponsored Projects Office

Introduction

March 31, 2004

Jeffrey Fernandez

Interim Chief Financial Officer

4

A Cross Functional Approach

• Recent audit findings and concerns raised by the University and DOE made it clear that proactive steps on LBNL’s part are necessary.

• Today’s session is designed to:–Strengthen financial management internal controls–Provide a formal structure for managing awards – Identify the specific roles and responsibilities of each

group (i.e. Division, SPO, CFO).

• The information presented for the most part is not new. It will however, require a strong partnering between Divisions, SPO, and AR.

• As we move toward making the Business Services Division world class, we must ensure that our policies and practices are compliant, documented, and LBNL staff has the proper training tools available.

Cross Functional TeamCross Functional TeamMarch 31, 2004

Chuck Axthelm

6

Working Group Objective

WFO Audit - Management Response #5 and #6:

• To improve Principal Investigators and Business Manager’s knowledge and awareness of DOE and LBNL procedures and requirements…A working group was tasked by the CFO to develop a responsibility matrix which will establish WFO roles and responsibilities.

7

Matrix – A Cross-Functional Product

• Starting with process notes from unbilled cost management activities

• Starting last April…Working both offline and in meetings with ASD (EETD & LSD) and FSD…an initial draft matrix of roles & responsibilities was developed

• Starting last October…RAPID Functional Team met weekly for 6 months to rework the matrix and create a “final” draft for management review

–Chaired by Phyllis Gale, the Functional Team is comprised of both ASD, SPO and FSD subject matter experts

Functional and Role MatricesFunctional and Role Matrices

Phyllis Gale

9

Cross Functional Matrices Handout

• Cross Functional Roles and Responsibilities Matrices – Summary and BSD Detailed Roles and Responsibilities

–Advance Payments–Billing the Sponsor–Invoicing and Collections–Costs Exceed Award Funding (Contract Value)

or Occur After the Period of Performance–A Word on Cash Management–Award Expiration and Closeout–E-mail Alerts

10

Summary – FunctionalRoles and Responsibilities Handout

• Summary Functional Roles and Responsibilities Matrices by Role

–Principal Investigator–Division Analyst–Accounts Receivable–Sponsored Projects Office–E-Notifications

Advances

Lisa Rebrovich

12

Advances

• Advances for non-federal awards are required under DOE WFO Orders and the DOE Accounting Handbook. The purpose of an Advance is to ensure that a positive cash balance is maintained between the times that a PI incurs expenses and the receipt of sponsor invoice payments covering these expenses.

• Advance is defined as the 4 highest months of cost (including the start up, equipment, and 4 months of operations costs) of the research award.

–This is a clarification of the ongoing practice of obtaining a 4 month advance payment.

13

Advances

• The PI and Division Analyst determines the Advance Invoice amount as part of budget formulation.

–This amount is recorded in RAPID (Proposal Header) under Additional Information.

• The SPO CO uses this information for the Advance Invoice and negotiations with the Sponsor.

• Once the Award is authorized, Accounts Receivable applies the advance payment to the award.

Billing the Sponsor

Jerry Kekos

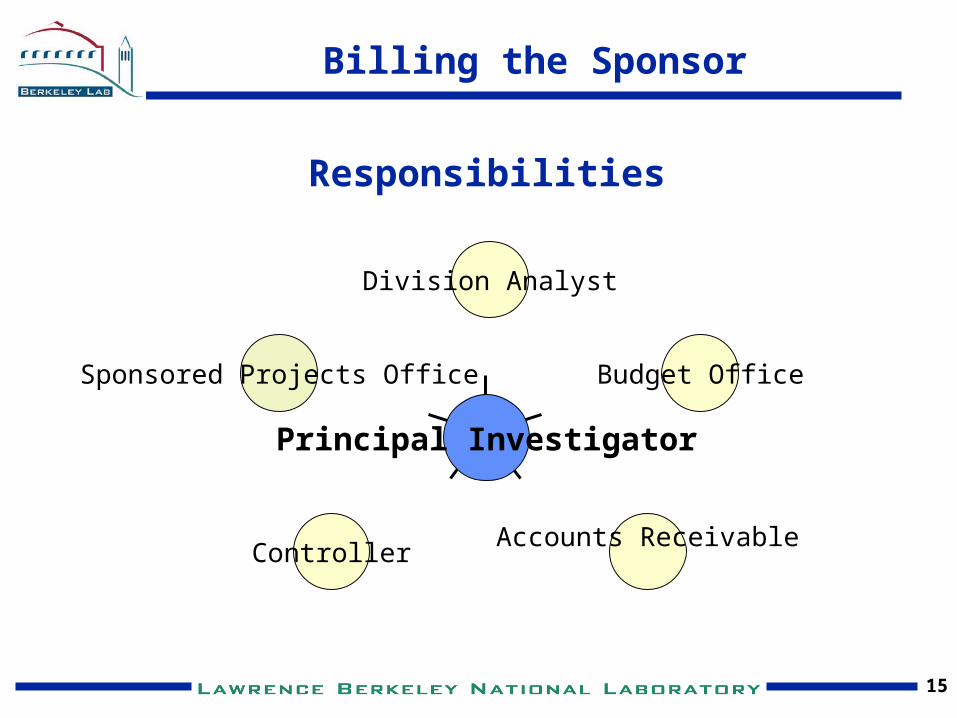

15

Sponsored Projects Office

ControllerAccounts Receivable

Budget Office

Division Analyst

Principal Investigator

Responsibilities

Billing the Sponsor

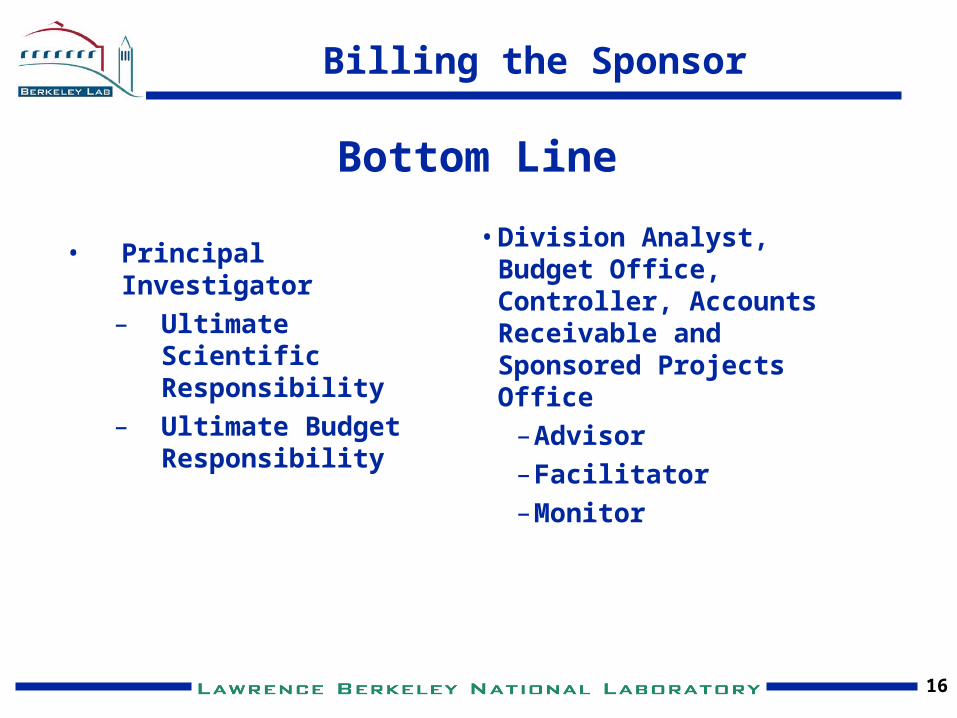

16

Bottom Line

• Principal Investigator– Ultimate Scientific

Responsibility– Ultimate Budget

Responsibility

• Division Analyst, Budget Office, Controller, Accounts Receivable and Sponsored Projects Office

–Advisor–Facilitator –Monitor

Billing the Sponsor

17

Principal Investigator• Manages award within funding and time limits

• Assures charges are allowable & reasonable

• Responsible for personnel assignments

• Approves the Subcontract requisition – Agreement– Payment

• Ensures Sponsor pre-approvals are in place before event execution:

– Re-budgeting– Key personnel– Human/Animal

• Exercises responsible fiscal control

• Ensures compliance and reports non-compliance

• Responsible for training:– Financial– Administrative

Billing the Sponsor

18

Division Analyst

Serves as an Advisor:– Reviews and understands the Awards

Terms and Conditions.– Assures the that all award costs are

treated consistently with regard to direct and indirect allocation and Cost Accounting Standards.

– Transactions are within the award funding (contract value), available cash balances, and period of performance.

– Reasonableness of cost of the transactions

– Reasonable allocation of the cost – Reports instances of Financial non-

compliance

Billing the Sponsor

19

Division Analyst

Serves as a Facilitator:– Processes financial transactions (i.e. certifies invoices).– Reviews and analyzes financial reports for sponsored awards – Prepares documents and provides information for re-budgeting if

required by Sponsor.– Prepares requests for Resource Adjustments (cost transfers) and

validates for posting by Accounting. – Prepares documents and provides information for compliance with

effort reporting (such as "NIH Other Support") on the sponsored award

Billing the Sponsor

20

Division Analyst

Serves as a Monitor:• One of the Division Analyst’s most important role is

working with the PI and others to get the costs associated with an award right before it is invoiced.

• Ensures the correct burden codes and other attributes are assigned to the proposal and the project.

• Tools to Manage

– Cost Browser on IRIS

– Award Management Report on IRIS

– Future reports and other tools will be developed in BLIS

Billing the Sponsor

21

• Budget Office– Pre-audit selected

financial transactions– Provide institutional

oversight on resource adjustments

– Perform risk analysis ensure compliance

– Reports instances of financial non-compliance

• Controller/Accounts Receivable– Prepare invoices to

sponsors in timely basis– Prepare interim financial

reports (with Divisions)– Approve or recommend

approval of unexpended fund carry-forward

– Assists P.I. & Divisions with procedural questions (billing & payments)

– Reports instances of Financial non-compliance

Billing the Sponsor

22

Sponsored Projects Office

• Authorizes Award Funding in RAPID and Distributes a SPAA

• Assists P.I. with procedural management of active research projects

• Reports instances of non-compliance

Billing the Sponsor

23

Going Forward

• Provide a seamless operation

• Everyone clearly knows what their roles are as well as how they fit into the larger picture

• Nothing gets – passed, – punted or – dropped

• Be Proactive

• Take Responsibility

• Partner with other functional groups

• Ignorance is not bliss

Billing the Sponsor

Invoicing and Collections

Sallie Frainier

25

• Invoicing the Sponsor– Invoices are printed the fifth working day of

the month after the monthly billing run (closing schedule on web).

– Invoices are due upon receipt.

• Collections: In order to ensure the LBNL is not in a vulnerable cash position we are stepping up our collection practices and have documented the cross functional roles:

Invoicing and Collections

26

• Division Analyst Role:–Provide information and prepares documents to

resolve cost overruns–Works with PI, SPO Contracts Officer, and

Accounts Receivable to resolve problems with slow and nonpayment (collection) of invoice payments.

–Close projects in order to suspend work due to nonpayment of invoices at the request of Accounts Receivable and Sponsor Projects Office.

Invoicing and Collections

27

• Accounts Receivable –Assists the Principal Investigator and Division

Analyst with procedural questions regarding invoicing, payments, and collections.

–Prepares invoices and sends to sponsors.–Receives payments from sponsors and applies

them to the invoice.–Works with PI, SPO, and Division Analysts to

resolve problems with slow and nonpayment (collection) of invoices.

–Tracks collection activity in the BAR Conversations

Invoicing and Collections

28

• Sponsored Projects Office–Works with PI, Accounts Receivable, and

Division Analysts to resolve problems with slow and nonpayment (collection) of invoices.

–Works with PI, Division Analysts, Accounts Receivable and the Sponsor regarding potential suspension of work if invoices are not paid in a timely fashion. Will suspend work if Sponsor does not pay invoices.

Invoicing and Collections

29

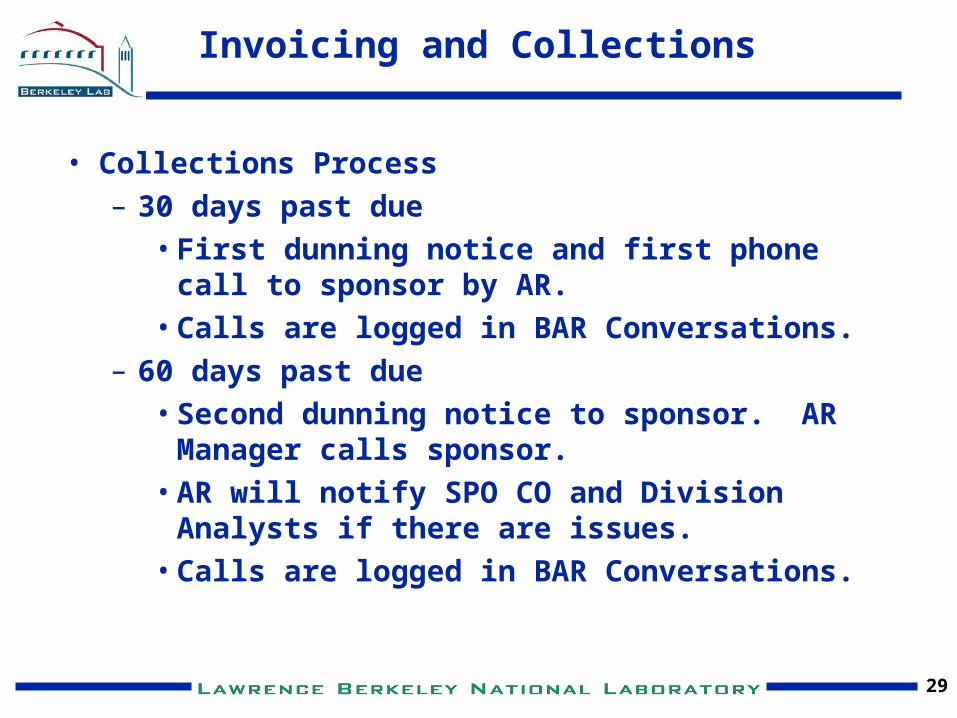

• Collections Process– 30 days past due

• First dunning notice and first phone call to sponsor by AR.

• Calls are logged in BAR Conversations.– 60 days past due

• Second dunning notice to sponsor. AR Manager calls sponsor.

• AR will notify SPO CO and Division Analysts if there are issues.

• Calls are logged in BAR Conversations.

Invoicing and Collections

30

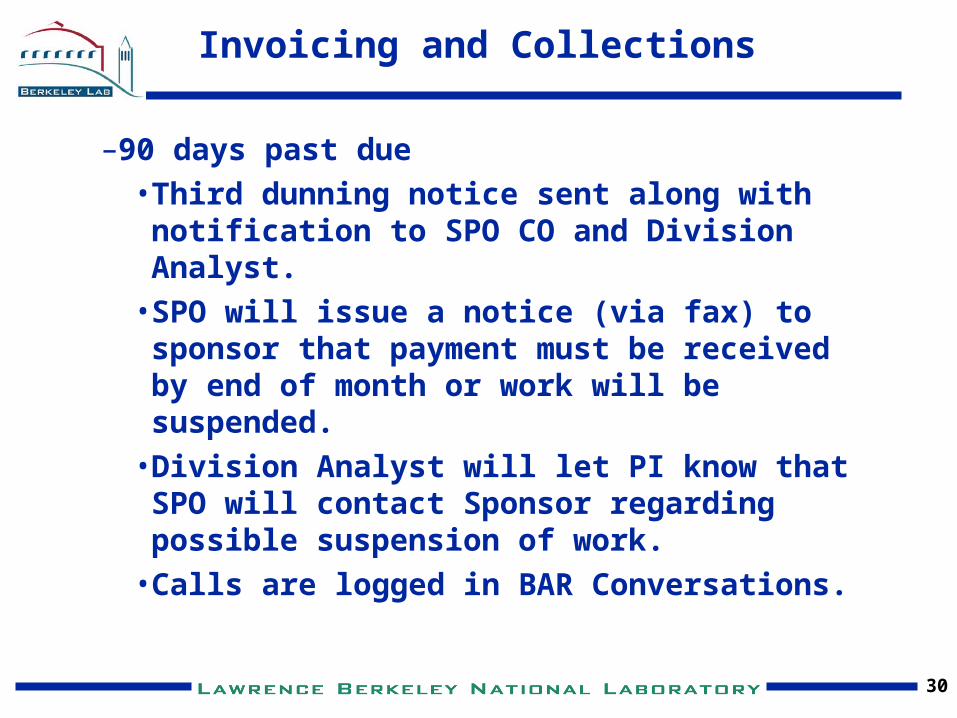

–90 days past due• Third dunning notice sent along with

notification to SPO CO and Division Analyst.• SPO will issue a notice (via fax) to sponsor

that payment must be received by end of month or work will be suspended.

• Division Analyst will let PI know that SPO will contact Sponsor regarding possible suspension of work.

• Calls are logged in BAR Conversations.

Invoicing and Collections

31

– 120 days past due

• AR notifies responsible SPO CO and Division Analyst that work should be suspended and the associated projects need to be closed effective the first day of the following month if payment not received.

• SPO issues written notice via fax to sponsor that work has been suspended and a termination notice will be sent in 30 days if the payment(s) have not been received.

• Division Analyst will let PI know that SPO will contact Sponsor regarding suspension of work and the projects will close in 30 days if payment not received.

• Calls are logged in BAR Conversations.

Invoicing and Collections

32

–150 days past due• AR manager follows up with the sponsor to

collect payment and notifies SPO CO and Division Analyst if Sponsor has not paid.

• If no payment is received, AR notifies SPO and Division Analyst that award will terminate and will be referred to DOE for collections at 180 days past due.

• SPO issues a termination notification via fax to sponsor on 150th day that the award is terminated on the 165th day.

Invoicing and Collections

33

Invoicing and Collections

–180 days past due • AR supervisor notifies SPO CO and Division

Analyst that the collection is being submitted to DOE for collection.

If the Sponsor pays after DOE has begun the collection process, it would have to be decided on a case by case basis to continue research with the sponsor and under what conditions to minimize the financial risk to LBNL.

34

Invoicing and Collections

• When will the new collection process begin?–April 2004

35

Collections Impact

• Impact as of 2/29/04– 355 Invoices are on the aging report.– Based on past history, anywhere from 5-8%

of aged invoices are 120 days or older• Industry standard is 2% allowance for doubtful

accounts

• Under the new Collection procedures, 84 Awards could have qualified for suspension ~ about $400K in outstanding invoiced costs

36

Invoicing and Collections

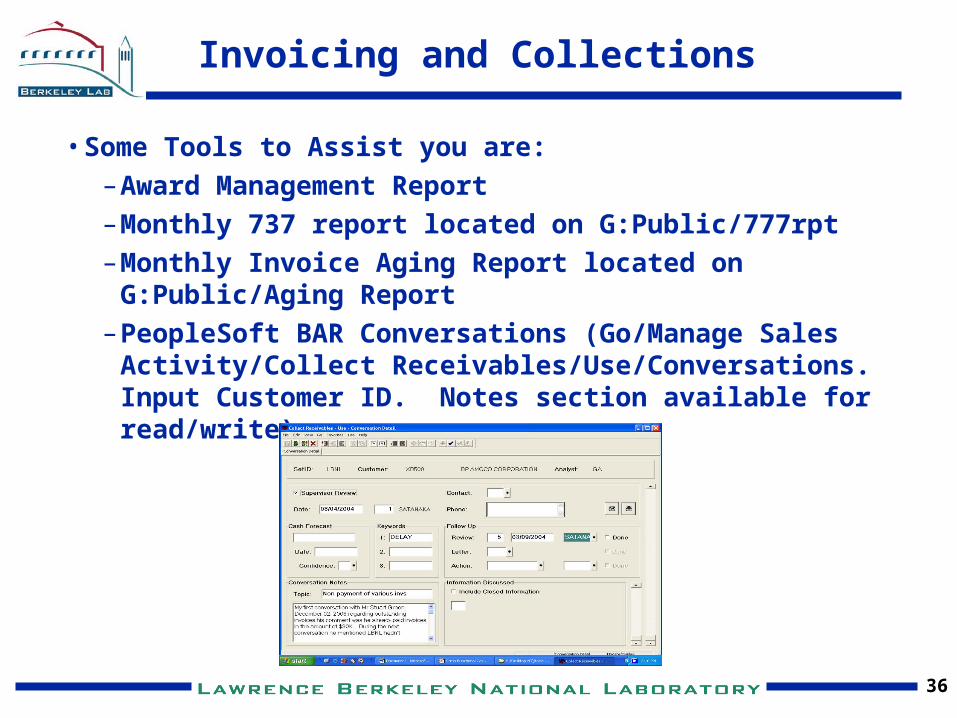

• Some Tools to Assist you are:–Award Management Report–Monthly 737 report located on G:Public/777rpt–Monthly Invoice Aging Report located on G:Public/Aging

Report–PeopleSoft BAR Conversations (Go/Manage Sales

Activity/Collect Receivables/Use/Conversations. Input Customer ID. Notes section available for read/write).

Costs Exceed Award Funding (Contract Value)

orCosts Incurred After

Period of Performance

Sallie Frainier

38

Costs Beyond FundingCosts Beyond Period of Performance

• Reasons for unbilled costs are:–Costs past Period of Performance–Costs in excess of funding

• Both situations require immediate attention by the Division Analyst.

• Division Analysts should coordinate with SPO to obtain no cost extension in the event period of performance expired but funding remains. Notify AR of action.

39

• Division Analyst works with SPO CO and sponsor to obtain additional funding (under terms of award) where costs exceed funding. Notify AR of action.

• Division Analyst works to remove costs if applied to project in error.

• Division Analyst submits a formal request for Bridge Funding in circumstances where additional funding is forthcoming. (must be verifiable)

Costs Beyond FundingCosts Beyond Period of Performance

40

• If the award remains in a negative funding position, the award and project will close on the first of the month following 30 continuous days in a negative position within a one month accounting period.

April May June

4/1/04 5/1/04 6/1/04

Award goes negative 4/15/04

Award remains negative through 5/31/04

Award and Projects Close effective 6/1/04

Costs Beyond FundingCosts Beyond Period of Performance

41

• If the research is complete,–Division Analyst verify the costs are correct to

AR–AR produces Final Invoice (refer to Award

Expiration and Closeout procedures)

• Some Tools to Assist you are:–Cost Browser on IRIS–Award Management Report on IRIS–Monthly 737 report located on G:Public/777rpt–E-Notifications

• 25% of Funding Remaining• Costs have exceed Funding• Award and Projects closure

Costs Beyond FundingCosts Beyond Period of Performance

42

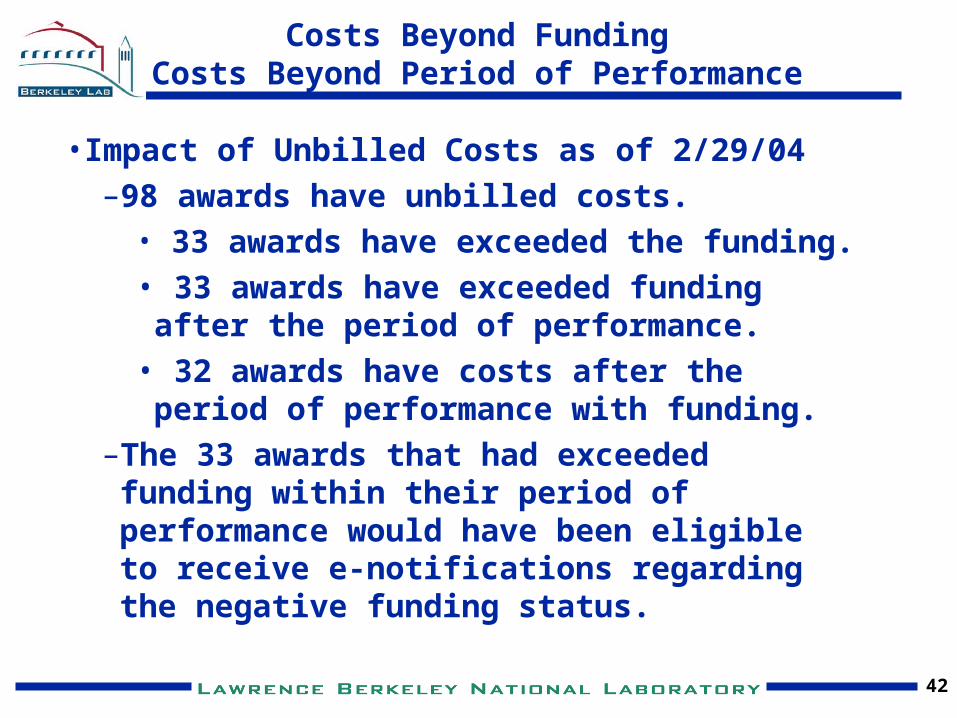

• Impact of Unbilled Costs as of 2/29/04–98 awards have unbilled costs.

• 33 awards have exceeded the funding.• 33 awards have exceeded funding after the

period of performance.• 32 awards have costs after the period of

performance with funding.–The 33 awards that had exceeded funding within

their period of performance would have been eligible to receive e-notifications regarding the negative funding status.

Costs Beyond FundingCosts Beyond Period of Performance

A Word About Cash Management

Sallie Frainier

44

These policies will help ensure compliance with UC, DOE, federal accounting standards, and individual sponsor requirements.

We have focused on funding and cost management to this point, but there is another side to award management and that is “Cash Management”

Cash Management

45

• Cash management means that we manage costs to the cash received to date.

• Cash received = Advance payments + invoice payments

• If costs exceed cash received then the project is in a cash negative position.

• The status of the award’s cash management

Position is detailed on the Award Management Report and the 737 report in the “Available Cash” column.

Cash Management

46

• The requirements around advance payments and prompt invoice payment are designed to alleviate a negative cash position and assure that DOE funds are not used to support sponsored research while waiting for invoice payments.

• Cash management requirements may be implemented in future. If so, we will provide information and training to Division Analysts and PIs.

Cash Management

Award Expiration and Closeout

Andre Bell

48

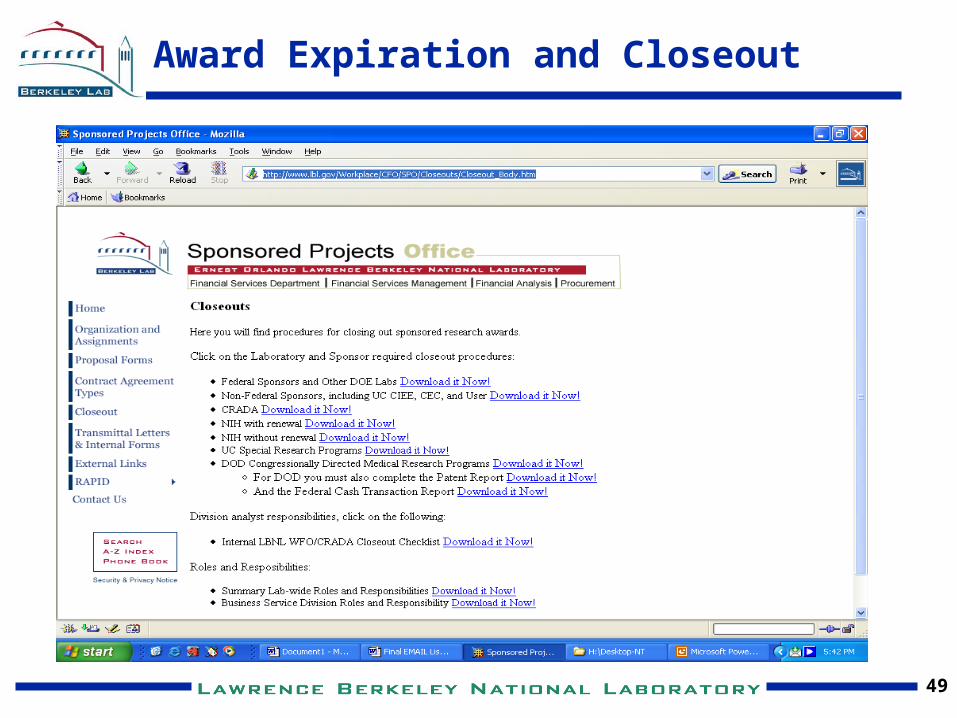

Award Expiration and Closeout

• Managing Award expiration and closeout was reviewed at the RAPID Meeting on 3/19/04.

–The roles and responsibilities and procedures can be accessed at:

http://www.lbl.gov/Workplace/CFO/SPO/Closeouts/Closeout_Body.htm

• Tools to manage award expiration includes–Award Management Report–Monthly 737 report located on G:Public/777rpt–E-Notifications

• E-Notification for Award Expiration at 90, 60, and 30 days prior to end of the period of performance

• E-Notification for Award Closeout at one day after the expiration date

49

Award Expiration and Closeout

Summary of Changes

Phyllis Gale

51

Summary of Changes

• Advances – 4 highest months of costs + equipment + research start up costs.

• Costs and Billing – Expectation that all costs are correct at time of initiation

–Reduces Billing errors–Reduces credit invoices and confusion on the part of

our sponsors.

• Payment Collection – Proactive, Cross-functional collection process.

–Reduces outstanding invoices and avoids suspension of work for nonpayment of invoices.

• Managing Costs within the Contract Value–Problem known immediately and resolved to avoid

closure of award prior to period of performance–Awards and Projects close if Costs have Exceeded

Funding thru a complete accounting cycle –Eliminate unbilled costs.

52

Summary of Changes

• Award Expiration and Closeout – –Awards close the day after expiration–Projects close 30 days after period of

performance.–Coordinate contractual and sponsor closeout

requirements and submission of documentation.

–Final Invoices sent by the target period of 90 days after period of performance eliminates unbilled costs.

E-Notifications

Phyllis Gale

54

E-Notifications

• Costs Exceed Award Funding (Contract Value) or Occur After the Period of Performance

–25% of Funding Remaining.

–Costs have Exceeded Funding.

–Costs have Exceeded Funding thru a complete accounting cycle and Award and Projects close.

• Award Expiration and Closeout

–Award Expiration e-notices sent 90, 60, and 30 days prior to end of the period of performance.

–Email Notification for Award Closeout sent one day after the expiration date.

55

E-Notifications

• When will the E-Notifications start?–May 1, 2004–The E-Notifications for April will be run in the

beginning of April• The e-mails will be captured on a spreadsheet and

sent to Division Analysts for review and action.

• Who will receive E-Notifications?–PIs–Division Analysts (Managed through Smartlists)–SPO CO assigned to the award–AR at the time of Award and Project Closeout

Questions?