case study philippines on microinsurance market development · pdf file ·...

TRANSCRIPT

Case Study: The Philippine experience on Microinsurance Market Development Page 1

Case Study

The Philippine experience on Microinsurance Market Development

For

Training Program of Insurance Supervisors in Asia

Organized by Access to Insurance Initiative, AITRI, GIZ-RFPI and Toronto Center

Manila, Philippines / September 16-20, 2013

Prepared by

Mr. Dante O. Portula

Senior Advisor, GIZ-RFPI Asia

Mr. Reynaldo Vergara

Division Chief, Philippine Insurance Commission

August 2013

Case Study: The Philippine experience on Microinsurance Market Development Page 2

Table of contents

1 Country overview

1.1 Basic demographic and economic data 3

1.2 Financial sector landscape 3

2 The Insurance Industry 4

3 Evolution of Microinsurance development

3.1 Financial inclusion, an overarching goal 4

3.2 Microinsurance policy milestones and circular issuances 5

4 Building capacity and provision of incentives to the private sector 8

5 The approach: Public and Private sector collaboration 10

6 Market Response 10

7 Key Lessons and Challenges 12

8 The way forward 13

9 References 13

Tables

1 Philippine policy reforms on Microinsurance 6

2 Microinsurance circular issuances 7

3 Market response 11

Case Study: The Philippine experience on Microinsurance Market Development Page 3

1. Country overview

1.1 Basic demographic and economic data

The Philippines is an archipelago of 7,107 islands with a total land area, including inland bodies

of water, of approximately 300,000 square kilometers. It is a constitutional republic with a

presidential system. The Philippines is divided into three island groups: Luzon, Visayas, and

Mindanao. As of March 2010, these were divided into 17 regions, 80 provinces, 138 cities, 1,496

municipalities, and 42,025 barangays. Population is around 97.6 Million. Literacy rate is 92.6%.

It is considered a middle income country with a per capita income of $1,790. GDP growth rates

from 2010-2012 were robust at 7.6%, 3.9% and 6.6%, respectively. The economic growth in

2012 was mainly driven by increased investment from the private sector, robust overseas

Filipino remittances and higher government spending. Despite of this however, almost a third

of its population still lives below the poverty line. Latest available data on poverty shows that

on the average, 28 out of 100 Filipinos are living in poverty between the 1st semester of 2006

and 1st semester of 2012.

The 2012 cash operations of the government showed a fiscal deficit of 15.8%, up from 14.5%

revenue deficit in 2011 fiscal year. Borrowings in 2012 were 35.1% of total tax and non-tax

revenues, 87% of which were from domestic sources and 13% from external sources.

1.2 Financial sector landscape

The total resources of the Philippine financial system as of June 2012 reached Php10.45 trillion

(USD254.87 Billion), 8.3% higher than a year ago. The banking industry’s total assets accounted

for 80% of the total resources and 76.2% of the country’s Gross Domestic Product (GDP). Non-

bank financial institutions (which include private and public insurance companies, among

others) contributed for the remaining 20%.

The number of banking institutions (head offices) dropped further to 705 as of end-September

2012 from the year-ago level of 730, denoting the continued consolidation of banks as well as

the exit of weaker players in the banking system. By banking classification, banks (head offices)

consisted of 37 Universal/Commercial Banks, 69 Thrift Banks, and 599 rural banks. Meanwhile,

the operating network (including branches and other offices) of the banking system increased

to 9,301 in September 2012 from 8,965 during the same period the previous year, due mainly

to the increase in the branches/agencies of universal and commercial banks.

The banking system’s asset quality as measured by the Non-Performing Loan (NPL) ratio

sustained its downtrend, easing to 2.6 percent as of end-October 2012 from the 3.2 percent

registered a year ago. Banks’ initiatives to improve asset quality along with prudent lending

regulations helped bring the NPL ratio below pre-Asian crisis levels. Outstanding loans of

Case Study: The Philippine experience on Microinsurance Market Development Page 4

commercial banks, net of banks’ Reverse Repurchase (RRP) placements with the Bangko Sentral

ng Pilipinas (BSP), continued to expand, posting a 16.2 percent y-o-y growth as of end-

December 2012.

The Philippine banking system’s Capital Adequacy Ratio (CAR) on consolidated basis was at

17.6%, which surpassed the 10% domestic regulatory minimum and 8% international norm, was

comparatively higher than those of Indonesia (17.3%), Malaysia (17.3%), Thailand (14.8%) and

South Korea (14.0%).

The Philippines has been lauded globally for its microfinance and financial inclusion initiatives.

For four years in a row (2009-2012), the Economist Intelligence Unit’s global survey has ranked

the Philippines as number one in the world in terms of policy and regulatory framework for

microfinance.

2. The Insurance Industry

As of end of 2012, the Philippine insurance industry is composed of 115 private commercial

companies (including 2 cooperative insurance societies) and 28 Mutual Benefit Associations

(MBAs). The insurance industry is relatively small with assets of Php785.5 Billion (USD19.2

Billion), 79.02% of which was accounted for by the Life sector (33 companies), 16.16% by the

Non-life sector (82 companies) and 4.82% by the Mutual Benefit Association sector (28 MBAs).

Its total assets or resources accounted for only 7.49% of the total resources of the Philippine

financial system and 9.4% of the banking sector’s assets.

Despite a significant numbers of insurance providers, however, the country still has a low

insurance take-up. The insurance penetration or the contribution of the insurance industry to

the country’s national economy is only 1.42% of Gross Domestic Products (GDP). Insurance

density or the average spending of each individual on insurance is only Php1,541 (USD37), of

which Php1,265 (USD31) is spent for Life insurance and Php276 (USD6) is for Non-life insurance.

The market penetration rate or the ratio of individuals with life insurance coverage to

population is only 23%.

3. Evolution of Microinsurance development

3.1 Financial inclusion, an overarching goal

The Philippine Government joined other developing countries in striving towards making

financial services available and accessible to all regardless of income class. This means that the

government shall endeavor to come up with measures that will encourage and allow the

provision of all types of financial services, insurance included, to the whole populace including

Case Study: The Philippine experience on Microinsurance Market Development Page 5

those who belong to the low-income sector. Financial inclusion is clearly articulated in the

Philippine five-year development plan.

In 1997, the Department of Finance (DOF) through the National Credit Council (NCC) adopted,

issued and implemented the National Strategy for Microfinance. This led to the establishment

of a policy and regulatory environment that encouraged private financial institutions to provide

financial services to the poor, thus facilitating the poor’s access to savings and credit services.

From only a handful of financial institutions providing savings and credit services to the low

income sector in 1995, there are now more than 2000 microfinance institutions providing

savings and credit services to more than 7 million low-income clients.

The development of the Philippine Microfinance Industry proved that the provision of formal

financial services, particularly savings and credit, to the poor is a viable and sustainable activity.

A large number of private financial institutions, notably rural, cooperative and thrift banks,

cooperatives and non-government organizations, including commercial banks acting as

wholesaler of microfinance funds, are now actively engaged in providing the poor greater

access to microcredit to finance their livelihood and small business activities. This development

presented a vast opportunity for the poor to improve their lives, increase their income and

build on their assets. However, it has been realized that microcredit does not protect the low-

income from unforeseen and unfortunate events that may adversely affect their livelihood,

lives and families.

The DOF and the Philippine Insurance Commission (PIC) deliberately included in its

development objectives the provision of insurance products and services to the poor. Like those

in the high or middle income classes, the poor should also be protected from unexpected

events such as death, injury and illness, loss of property and other contingent events. This

segment of the population is in fact more vulnerable to risk events. One study conducted in

2008 showed that of the 23.1 million Filipinos living below the poverty line, only about 2.9

million have some kind of risk protection, about half of which are provided informally. Informal

insurance provisions are mostly done by entities and organization (some are MFIs) that provide

self-or in-house insurance. These entities do not have any license from the regulatory authority

and collect premiums and guarantee benefits without any actuarial study, hence posing greater

risk to the low-income client.

3.2 Microinsurance policy milestones and circular issuances

Microinsurance development in the Philippines follows the same path taken for Microfinance

development. The business is driven by the private sector, with government providing only the

enabling environment. The adoption of the various reform measures, policy actions and

Case Study: The Philippine experience on Microinsurance Market Development Page 6

regulatory guidelines identified in the following landmark documents resulted in the growth

and development of the country’s microinsurance industry in a span of 4 years (2009-2012).

Pillar 1: Regulatory Framework for Microinsurance,

Pillar 2: National Strategy for Microinsurance,

Pillar 3: Roadmap to Financial Literacy on Microinsurance, and

Pillar 4: Alternative Dispute Resolution for Microinsurance.

The regulatory framework provides for the regulation of Microinsurance that covers the risk

protection needs of the poor by the private sector. It does not cover social insurance schemes

and risk protection programs administered and implemented by government.

Table 1 summarizes the salient features of the pillars of reforms.

Table 1: Philippine Policy Reforms on Microinsurance

Policy Reforms Features

Regulatory Framework for

Microinsurance (issued in

January 2010)

Outlines the government’s policy thrusts and direction for the establishment of

a policy and regulatory environment that will encourage, enhance and facilitate

the safe and sound provision of microinsurance products and services by the

private sector. It identifies and promotes a system that will protect the rights

and privileges of those who are insured.

National Strategy for

Microfinance (issued in January

2010)

Defines the objective, the roles of the various stakeholders and the key

strategies to be pursued in enhancing access to insurance of the poor. It

encourages complementation of the products of social health insurance by the

private sector. It provides directions towards mainstreaming informal

insurance and insurance-like activities and the promotion of public awareness

and financial literacy.

Roadmap to Financial Literacy

on Microinsurance (issued in

January 2011)

Spells out the key strategies and measures to be adopted for institutionalizing

financial literacy on Microinsurance. Key principles, guidelines, and specific

directions on how to promote and change behavior favorably for the adoption

of Microinsurance among the low- income sector are provided for.

Alternative Dispute Resolution

Framework for Microinsurance

(issued in October 2012)

Requires all insurance entities, agents and brokers who are engaged in

Microinsurance business to follow mediation-conciliation processes of claims

dispute based on parameters offset under the banner, Least cost, Accessible,

Practical, Effective and Timely or LAPET.

The adoption of the policy thrusts and directions embodied in these documents prompted

various financial regulators (e.g. insurance, banking, and non-banking activities) to issue joint

and independent circulars for concerned financial entities under their jurisdiction.

Case Study: The Philippine experience on Microinsurance Market Development Page 7

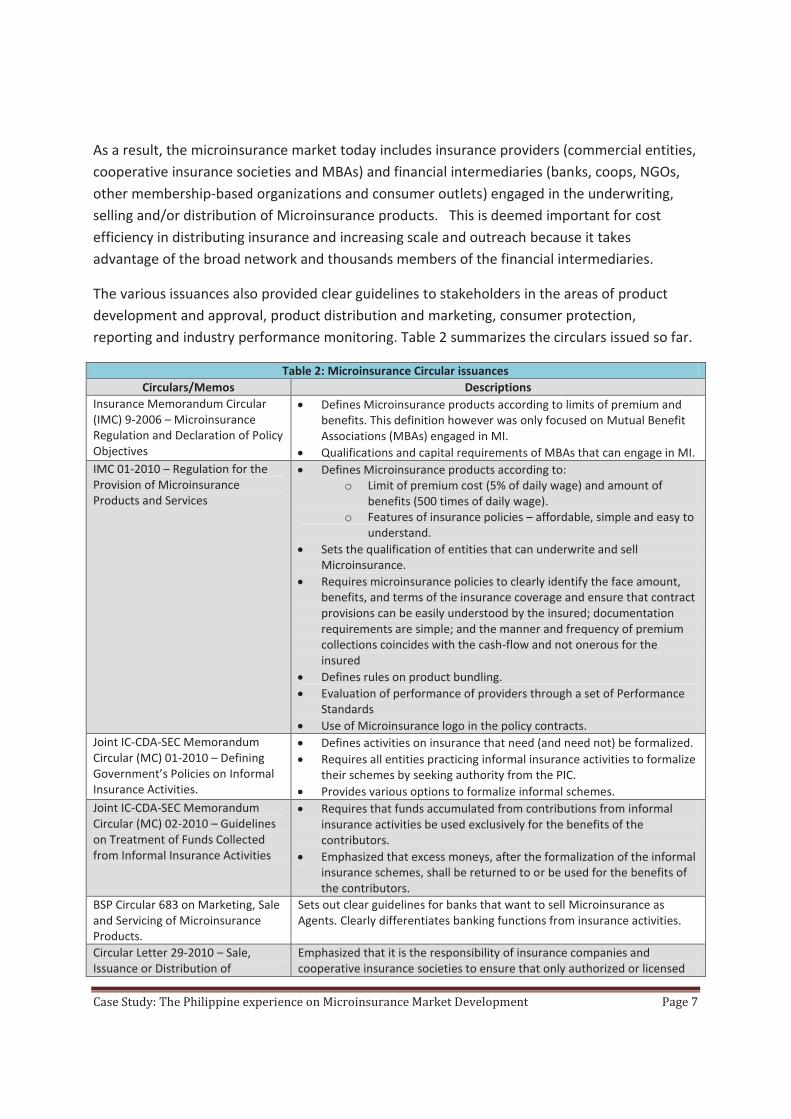

As a result, the microinsurance market today includes insurance providers (commercial entities,

cooperative insurance societies and MBAs) and financial intermediaries (banks, coops, NGOs,

other membership-based organizations and consumer outlets) engaged in the underwriting,

selling and/or distribution of Microinsurance products. This is deemed important for cost

efficiency in distributing insurance and increasing scale and outreach because it takes

advantage of the broad network and thousands members of the financial intermediaries.

The various issuances also provided clear guidelines to stakeholders in the areas of product

development and approval, product distribution and marketing, consumer protection,

reporting and industry performance monitoring. Table 2 summarizes the circulars issued so far.

Table 2: Microinsurance Circular issuances

Circulars/Memos Descriptions

Insurance Memorandum Circular

(IMC) 9-2006 – Microinsurance

Regulation and Declaration of Policy

Objectives

· Defines Microinsurance products according to limits of premium and

benefits. This definition however was only focused on Mutual Benefit

Associations (MBAs) engaged in MI.

· Qualifications and capital requirements of MBAs that can engage in MI.

IMC 01-2010 – Regulation for the

Provision of Microinsurance

Products and Services

· Defines Microinsurance products according to:

o Limit of premium cost (5% of daily wage) and amount of

benefits (500 times of daily wage).

o Features of insurance policies – affordable, simple and easy to

understand.

· Sets the qualification of entities that can underwrite and sell

Microinsurance.

· Requires microinsurance policies to clearly identify the face amount,

benefits, and terms of the insurance coverage and ensure that contract

provisions can be easily understood by the insured; documentation

requirements are simple; and the manner and frequency of premium

collections coincides with the cash-flow and not onerous for the

insured

· Defines rules on product bundling.

· Evaluation of performance of providers through a set of Performance

Standards

· Use of Microinsurance logo in the policy contracts.

Joint IC-CDA-SEC Memorandum

Circular (MC) 01-2010 – Defining

Government’s Policies on Informal

Insurance Activities.

· Defines activities on insurance that need (and need not) be formalized.

· Requires all entities practicing informal insurance activities to formalize

their schemes by seeking authority from the PIC.

· Provides various options to formalize informal schemes.

Joint IC-CDA-SEC Memorandum

Circular (MC) 02-2010 – Guidelines

on Treatment of Funds Collected

from Informal Insurance Activities

· Requires that funds accumulated from contributions from informal

insurance activities be used exclusively for the benefits of the

contributors.

· Emphasized that excess moneys, after the formalization of the informal

insurance schemes, shall be returned to or be used for the benefits of

the contributors.

BSP Circular 683 on Marketing, Sale

and Servicing of Microinsurance

Products.

Sets out clear guidelines for banks that want to sell Microinsurance as

Agents. Clearly differentiates banking functions from insurance activities.

Circular Letter 29-2010 – Sale,

Issuance or Distribution of

Emphasized that it is the responsibility of insurance companies and

cooperative insurance societies to ensure that only authorized or licensed

Case Study: The Philippine experience on Microinsurance Market Development Page 8

Insurance Products intermediaries, i.e., agents and brokers, are engaged to sell insurance/

microinsurance policies. In the case of mutual benefit associations, MBA

insurance products must be issued only to members.

Circular Letter 5-2011 –

Performance Standards for

Microinsurance

Sets guidelines for reporting Microinsurance activities and prescribes the

calculations of prudential and performance ratios according to set of

Performance Standards called SEGURO (Solvency, Efficiency, Governance,

Understanding of Microinsurance, Risk Management and Outreach of

clients).

Circular Letter 6-2011 –Guidelines

for the Approval of Training

Programs and Licensing of

Microinsurance Agents

Outlines the procedures of training and licensing MI agents. Requires the

minimum disclosures such “A Licensed Microinsurance Agent” signage

visible in the premises of the institution.

Circular Letter 39-2011 – Re-

approval of Microinsurance

products

Requires all MI products approved under the IMC No. 9-2006 (the very first

MI circular issued by PIC) to be submitted for re-approval to conform to the

definition of Microinsurance under IMC 1-2010.

Circular Letter 16 to 18-2013 –

Guidelines for the Implementation

of Alternative Dispute Resolution

for Microinsurance (ADReM) by

Commercial Companies,

Cooperatives and MBAs

Describes the principles and procedures of claims-related dispute resolution

mechanisms at least cost, accessible, practical, effective and timely. It

emphasizes consumer protection and also protection of the insurance

industry against illegitimate claims.

Circular Letter 15-2013 –

Procedures for Accreditation of

Mediators-Conciliators in

Alternative Dispute Resolution for

Microinsurance (ADReM)

Sets out the qualifications of mediators-conciliators, training,

responsibilities and code of conduct.

Embedded in the circulars are provisions on transparency and disclosures to ensure consumer

protection. The circulars require all microinsurance policies to clearly identify the face amount,

benefits, and terms of the insurance coverage and ensure that contract provisions can be easily

understood by the insured; documentation requirements are simple; and the manner and

frequency of premium collections coincides with the cash-flow and not onerous for the insured.

4. Building capacity and provision of incentives to the private sector

To achieve the goal of inclusive insurance, the DOF-NCC and PIC deliberately engaged the

private sector. The private sector has an important and significant role in providing viable and

sustainable insurance products and services to the poor because they have the distinctive

competence and comparative advantage when it comes to the provision of needed financial

services. The PIC believes that its role is mainly to provide the appropriate policy and

regulatory environment for encouraging the private sector to participate in the provision of

insurance products and services to the low-income sector. Furthermore, the regulator believes

that its role is to ensure the financial stability of insurance providers and make sure that

consumers are appropriately protected. Thus, licensed private insurance providers were

encouraged to consider the low-income market and cater to their specific insurance needs.

Case Study: The Philippine experience on Microinsurance Market Development Page 9

To further encourage the private sector to participate in microinsurance, PIC has allowed lower

capitalization requirements for providers that are wholly engaged in microinsurance.

Additional admitted assets were also identified for providers engaged in microinsurance. PIC

also created a new category of Microinsurance agents and brokers with relaxed licensing

requirements.

The incentives for private sector participation went beyond the issuance of relevant circulars.

The DOF-NCC, PIC, the insurance associations and with the support of GIZ-MIPSS1 and ADB-

JFPR2 conducted the following capacity building and support activities:

· Conducted market surveys to have a clear understanding of the needs of the low-income

sector. These provided a strong basis in designing the needed policy reforms, product

development and distribution.

· Developed a prototype/standard Microinsurance non-life product tailor-fitted to the needs

of low-income sector using a one-page simplified policy contract. It is a basic cash assistance

policy that provides benefits to the insured and his/her livelihood against perils of personal

accident, fire, flood and earthquake. Insurers offer this voluntary product and compete

among themselves on pricing, benefits, distribution channels and pre/post sale services.

· Simplified the wordings of life policy contracts for easier understanding by the low-income

sector. The contracts include variants of term-life, life policy with cash value and group life.

Similar to the non-life prototype, the simplified life policy contracts enabled the insurers to

efficiently do product development and facilitated the PIC’s approval of MI products within

5 days.

· Conducted Training of Microinsurance Advocates. Training modules tailor-fitted to 9

stakeholders were developed: Macro (policy makers, national government agencies,

regulators, Local Government Units), Meso (insurers, intermediaries, support institutions,

donors), Micro (clients/consumers). Around 660 staff from the macro and meso

stakeholders had been trained as Microinsurance advocates.

· Rolled out a nation-wide Microinsurance awareness campaign. The campaign runs for a

year. It conducted training on MI advocacy, public seminars, MI information exhibits and

1 Deutsche Gesellschaft fur Internationale Zusammenarbeit (GIZ) GmbH – Microinsurance Innovations Project for

Social Security (MIPSS) supported the Microinsurance initiatives of government in 2009-2012. 2 Asian Development Bank (ADB)-Japan Fund for Poverty Reduction (JFPR) supported the Microinsurance initiatives

of government in 2008-2012.

Case Study: The Philippine experience on Microinsurance Market Development Page 10

media briefings. One learning center in Microinsurance was also established in the

Southern part of the Philippines.

· Trained the industry on the understanding, adoption and implementation of set of

indicators for Performance Standards for microinsurance (SEGURO).

5. The approach: Public and Private sector collaboration

Public and private sector collaboration through the Technical Working Groups (TWGs) and

broad based consultations among national and regional stakeholders led to solid ownership of

initiatives and results. The TWGs provided venues for public-private sector participation in the

discussion of policy and regulatory issues and in the formulation of various policy and

regulatory measures addressing the issues. Strong and sustained leadership of the DOF-NCC

and PIC also made the processes effective and efficient. Technical and financial support from

German International Cooperation-Microinsurance Innovations Program for Social Security

(GIZ-MIPSS) and the Asian Development Bank-Japan Fund for Poverty Reduction (ADB JFPR)

Developing Microinsurance Project (MIP) provided inputs from experts. And the excellent

donors’ coordination is the success drivers of Microinsurance market development in the

Philippines.

Public sector includes financial regulators (DOF-NCC, PIC, Bangko Sentral ng Pilipinas,

Cooperative Development Authority, Securities and Exchange Commission) and other national

agencies such as National Anti-Poverty Commission and Philippine Information Agency.

The private sector, on the other hand, includes all associations of insurance providers

(commercial life and non-life companies, cooperative insurance societies and mutual benefit

associations), financial and other institutions engaged in the provision of financial services to

the low-income sector, and associations of agents, brokers, rural banks and MFIs.

Since the private sector was involved in the formulation of policy and regulatory reforms,

adoption and implementation of reform measures were facilitated. In almost all cases,

members of the various working groups serve as advocate for reforms in their own

organization.

The Philippine Government also sought the assistance of development organizations in

promoting and developing the microinsurance industry. Technical assistance from the GIZ and

ADB-JFPR specifically focused on the following areas: developing the appropriate policy and

regulatory environment for increased private sector participation in providing microinsurance

services; building the capacity of regulators in supervising microinsurance providers; developing

prototype product; and increasing awareness on microinsurance among key stakeholders.

Case Study: The Philippine experience on Microinsurance Market Development Page 11

6. Market Response

The implementation of policy reforms on Microinsurance have effectively contributed to the

development of an inclusive insurance market. Before 2009, only MBAs were providing

insurance to the low-income sector. As of end-2012, 35 commercial insurance companies are

voluntarily selling MI products, 17 are life and 18 are non-life. The PIC has already approved 80

MI products, 54 are life and 26 are non-life MI products. Also, there are now 17 licensed MI-

MBAs.

Before 2009, Microinsurance products catering to the clients of MFIs are mostly credit life

protecting the Microfinance provider more than the clients. Today, products that provide

benefits against flood, crop loss, fire, hospitalization and earthquake are already available.

Prior to 2009, there was no MI agent category. At that time, there were only about 3.1 million

individuals covered by MI-MBAs. As of end-2012, PIC has already licensed 124 MI agents, 34 of

whom are rural banks. About 7.8 million have been insured.

As a result of the various initiatives on microinsurance, there is now greater awareness and

interest in microinsurance from both the government and the private sector. There is also an

increased interest among technology providers to provide the necessary backroom support to

insurance providers engaged in MI.

The measures undertaken also resulted in increased risk protection to the low-income sector.

Simplified policy contracts for microinsurance were issued allowing the poor to have a greater

understanding of what insurance is, its benefits and their rights and obligations as insured.

Table 3 shows a comparative performance of the industry.

Table 3: Market Response

Status, before 2009 Status, End-of-2012

MI products mostly credit life except for MBA MI

products

80 MI products approved (54 life and 26 non-life)

6 licensed MI-MBA 17 licensed MI-MBAs

Very few commercial insurance companies with MI 35 insurance companies (17 life and 18 non-life)

voluntarily selling MI products

No MI agent category 124 licensed as MI agents (34 Rural Banks and 90

individuals)

3.1 million individuals covered under MI About 7.8 million insured including dependents are

covered under MI

Insurance penetration was only 1.02 % of GDP Insurance penetration was 1.42% of GDP

Insurance density Php 878 ($19) �Life insurance Php 654

($14)�Non-life insurance Php 224 ($5)

Insurance density Php 1541 ($37). Life insurance Php

1265 ($31), Non-life insurance Php276 ($6)

Estimated life insurance coverage was 13.90% of 91 M

population

Estimated life insurance coverage was 23% of 97.6 M

population

Case Study: The Philippine experience on Microinsurance Market Development Page 12

7. Key Lessons and Challenges

Lessons:

7.1 Government should own and champion the reform measures. It is important to ensure that

concerned government agencies are convinced of and own the policy and regulatory reform

agenda. It is important to have key officials within the concerned government agencies who

support and champion the reform agenda. Having an advocate in government signals

sustainability of reforms, which is important when encouraging private sector participation.

7.2 The private sector should be engaged in formulating policy and regulatory reforms. As key

market participants, they should be consulted on what will work best for them without

sacrificing financial stability and consumer protection.

7.3 Donor assistance should be coordinated and synchronized to maximize returns and avoid

waste of resources.

7.4 Government alone cannot meet the goals of inclusive insurance. A strong partnership

between the government and the private sector is needed to move the agenda forward.

The private sector has a significant and important role in delivering the right products using

appropriate and tailor-fitted processes and distribution mechanisms. The government on

the other hand, should facilitate market innovation and ensure that market conduct

protects both the insurer and the insured.

7.5 Small gains lead to bigger milestones. A common trap to the process of making policy

change is when the discussion is dragged on by the ticklish issue of changing or creating

new laws which could only happen through then intervention of congress. If this happens,

the industry loses sight of (e.g. the adoption and issuance of the Regulatory Framework and

the National Strategy for Microinsurance).

Challenges:

7.6 Low insurance take up in the country primarily stems from a lack of a strong insurance

culture among the populace. A large majority of the population do not appreciate the

benefits and importance of insurance. Very few are willing to part with their hard earned

money in anticipation of getting some guaranteed benefits when a contingent event

happens. The Filipino culture of living everything to fate makes insurance a hard sell

product in the country. To increase insurance penetration in the country, the low-income

market segment should be tapped. Aside from providing the needed huge numbers,

catering to the risk protection needs of this market segment will also help in meeting the

Case Study: The Philippine experience on Microinsurance Market Development Page 13

development objectives and in supporting the poverty alleviation thrusts of the

government.

7.7 Reaching bigger scale requires innovations in product development, distribution and claims

administration. Available success stories (such as in pawnshops) need to be documented to

inspire other players on the profitability of Microinsurance.

8. The way forward:

8.1 Strengthening consumer protection through the adoption, issuance and implementation of

appropriate market conduct guidelines. Support the PIC and the industry in the

implementation of ADReM.

8.2 Adoption of thematic regulations such as on index-based/parametric insurance and

technology-based insurance.

8.3 Conduct studies on impact of regulations and case studies of business successes so far.

9. References

Information used in this case study took reference and recognition from the following sources:

a. Bangko Sentral ng Pilipinas, Annual Report, 2012

b. Dante Portula, power point material “Philippines Model of Microinsurance Inclusion: Process

and Success Factors of Public-Private Collaboration”, 5th Asia Microinsurance Conference,

July 2011.

c. MIPSS website www.microinsurancephil.com

d. National Statistics and Coordination Board website www.nscb.gov.ph

e. Philippine Insurance Commission, Microinsurance circulars,

www.insurancecommission.gov.ph

f. Philippine Insurance Commission, power point presentation “Developing an Inclusive

Insurance Market: The Path Taken by the Philippine Government”, July 2013, prepared for

RFPI Asia.

g. Philippine Insurance Commission, power point presentation “Engaging the Private Sector for

Inclusive Insurance: The Path Taken by the Philippine Government”, July 2013, prepared for

RFPI Asia.

h. Technical Working Group, Regulatory Framework for Microinsurance, Philippines, January

2010

i. Technical Working Group, National Strategy for Microfinance, Philippines, January 2010

Case Study: The Philippine experience on Microinsurance Market Development Page 14

j. Technical Working Group, Roadmap to Financial Literacy on Microinsurance, Philippines,

January 2011

k. Technical Working Group, Alternative Dispute Resolution Framework for Microinsurance,

Philippines, October 2012

Other useful resource:

www.microinsurancephil.blogspot.com (contents compiled by Director Joselito Almario, DOF-

NCC)

Microinsurance Training Program

for Insurance Supervisors in Asia

16-20 September 2013

Taal Vista Hotel / Tagaytay, Philippines

Philippine Approach to Developing Inclusive

Insurance Market (Part 1)

Reynaldo Vergara, Philippine Insurance Commission (PIC)

Dante Portula, German International Cooperation (GIZ)

Outline

1. Philippine financial system landscape

2. Microinsurance key indicators

3. Regulatory Framework on Microinsurance

4. National Strategy on Microinsurance

5. Lessons and Challenges

Philippine Financial Landscape

Total Resources, 2012

(USD254.9 Billions)

Banks NBFIs Insurance, private

203.9 (80.0%)

31.8 (12.5%)

19.2 (7.5%)

Philippine Financial Landscape

Total Resources, 2012

(USD254.9 Billions)

Banks NBFIs Insurance, private

203.9 (80.0%)

31.8 (12.5%)

19.2 (7.5%)

Insurance Sector: • 115 private commercial

companies

• 33 Life (79%)

• 82 Non-life (16.2%)

• 28 MBAs (4.8%)

Banking Sector: • 705 head offices

• 37 Universal/Commercial Banks

• 69 Thrift Banks

• 599 Rural and Coop Banks

• 9,301 operating network (branches)

Insurance Market (As of end-2012)

Insurance penetration was 1.42% of GDP

Insurance density Php1541 ($37):Life Php1265 ($31), Non-life Php276 ($6)

Estimated life insurance coverage was 23% of 97.6 M population

Philippine Financial Landscape

Microinsurance key indicators

As of end-2012

80 MI products approved (54 life and 26 non-life)

17 licensed MI-MBAs

35 insurance companies (17 life and 18 non-life)

124 licensed as MI agents (34 Rural Banks and 90 individuals)

Definition of Microinsurance

Insurance Memorandum Circular (IMC) 1-2010

A financial product or service that meets the risk protection needs of the poor

Daily Contribution/premium not more than 5 percent of the current daily minimum wage rate

(P23.30 or USD 0.53)

Guaranteed benefits not more than 500 times the daily minimum wage rate.

(P233,000.00 or USD 5,295)

MI Regulatory Framework

MI Regulatory Framework Key distinctions : Traditional and MI

Common Provisions for

Individual/Group

Insurance Plans

Traditional

Insurance Products

Microinsurance

Products

(IMC 1-2010)

Ø Maximum

Premium

Depending on the

company

5% of the current daily

minimum wage rate in

Metro Manila

Ø Maximum

Benefit

Depending on the

company

500 times the daily

minimum wage rate in

Metro Manila

Ø Policy Contract Full of complex

conditions

Simple and easy to

understand

Ø Frequency of Premium

Collection

Monthly, Quarterly,

Semi-Annual, Annual

Daily, Weekly, Monthly,

Quarterly, Semi-

Annual, Annual

MI Regulatory Framework

Key distinctions : Traditional and MI

Common Provisions

for Individual/Group

Insurance Plans

Traditional

Insurance Products

Microinsurance

Products

Ø Grace Period 31 days from

premium due date

45 days from

premium due date

Ø Contestability

Period

Maximum of

2 years from date

of issue or last

reinstatement of

the policy

Maximum of

1 year from date of

issue or last

reinstatement of the

policy

MI Regulatory Framework

Key distinctions : Traditional and MI

Common Provisions for

Individual/Group

Insurance Plans

Traditional

Insurance Products

Microinsurance Products

Ø Suicide Clause Maximum of

2 years from date of

issue or last

reinstatement of the

policy

Maximum of 1 year from

date of issue or last

reinstatement of the

policy

Ø Claims

Settlement

Within 60 days after

submission of

complete documents

Within 10 days after

submission of complete

documents

MI Regulatory Framework Increasing SUPPLY

PROVIDERS

Commercial Insurers

Coop Insurance Societies

Mutual Benefit Associations

DELIVERY MECHANISMS

Non-traditional mechanisms (e.g.

pawnshops, e-commerce)

Partnerships and Tie-ups with community-based organizations

Entities as Microinsurance agents/brokers

REGULATORY SPACE

Lower capitalization requirements

Additional admitted assets

Relaxed licensing requirements for MI

agents

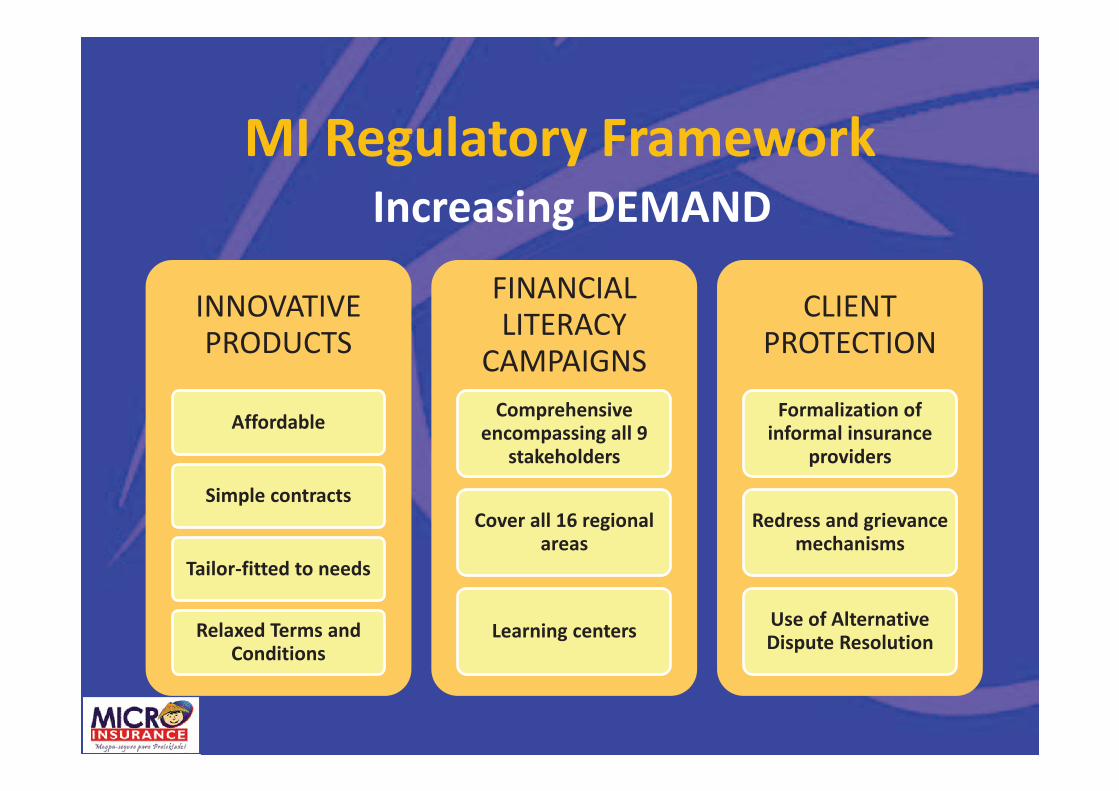

MI Regulatory Framework Increasing DEMAND

INNOVATIVE PRODUCTS

Affordable

Simple contracts

Tailor-fitted to needs

Relaxed Terms and Conditions

FINANCIAL LITERACY

CAMPAIGNS

Comprehensive encompassing all 9

stakeholders

Cover all 16 regional areas

Learning centers

CLIENT PROTECTION

Formalization of informal insurance

providers

Redress and grievance mechanisms

Use of Alternative Dispute Resolution

MI National Strategy Role of the Government

Policy and Regulatory Agencies

• Enabling policy and regulatory environment

• Measures supportive of financial inclusion

• Guidelines for mainstreaming informal insurance

Other National Agencies and

Instrumentalities

• Networks and linkages with Microinsurance providers

• Inclusion of Microinsurance in programs

• Basic support services

Local Government Units (LGUs)

• Collaboration with private sector providers

• Institutionalization of Redress Mechanisms

• Public awareness and education

MI National Strategy

Role of the Private Sector

PRODUCT INNOVATION

• Design and provide simple, affordable and accessible innovative Microinsurance products

MARKET DEEPENING

• Expand channels for the safe, efficient and effective delivery with fast claims payments

FINANCIAL LITERACY

• Educate the masses on the importance of risk protection and build trust among the general public

Developing MI Regulatory

Framework and Strategy

The Process

Mapping of gaps and inefficiencies

Drafting of policy papers – TWG series

Industry and public consultations

Launching and adoption

Value to MI Inclusion

Clear definition of MI, target sectors, roles of

various players

Strategies for mainstreaming informal

insurance, Finlit

Opened up the MI supply market beyond

MBAs

Opened up delivery channels beyond traditional agents

Results so far…

Issued JOINT circulars on formalization and

delivery channels

Set up MI committee in respective association of

insurers

80 new MI products from 35 companies approved

by IC since 2010

About 7.8 million insured under MI

Lessons and Challenges

1. Government should own and champion

the reform measures.

2. The private sector should be engaged in

formulating policy and regulatory

reforms.

3. Small gains lead to bigger milestones.

-- Acknowledgement --many of the slides used in this presentation

were adapted from files of power point

presentations prepared by the Philippine

Department of Finance – National Credit

Council and the Insurance Commission

Maraming Salamat!!

(Thank You)

Microinsurance Training Program

for Insurance Supervisors in Asia

16-20 September 2013

Taal Vista Hotel / Tagaytay, Philippines

Philippine Approach to Developing Inclusive

Insurance Market (Part 2)

Reynaldo Vergara, Philippine Insurance Commission (PIC)

Dante Portula, German International Cooperation (GIZ)

Outline

1. Developing Microinsurance prototype product

2. Roadmap to Financial Literacy on MI

3. Tools for consumer protection

• Formalizing the informal

• SEGURO Performance Standards

• Alternative Dispute Resolution (ADR) scheme

4. Market Response

5. Lessons and Challenges

MI Product Prototype

Buhay Bahay Kabuhayan (BBK)

§Microinsurance Policy that pays the

insured or his beneficiary the sum

assured in case a covered peril results in

loss or damage to life and property

MI Product Prototype

BBK Overview

§Non life Property Insurance with Personal Accident

§One-year term coverage

§One claim on any one peril terminates the policy

§Claim Settlement within ten (10) days upon

submission of complete claim requirements

§Php10,000 per unit. Maximum of 3 units per family

MI Product Prototype

BBK named perils

§Fire,

§Lightning,

§Typhoon,

§Floods,

§Earthquake,

§or Accidental death (PA), Total &

Permanent Disability (TPD)

MI Product Prototype

Acceptable Proof of Loss & Proof of Claims

Minimum requirements:

§Barangay/Village or Local Government

Certification

§Death Certificate (for Personal Accident)

MI Product Prototype

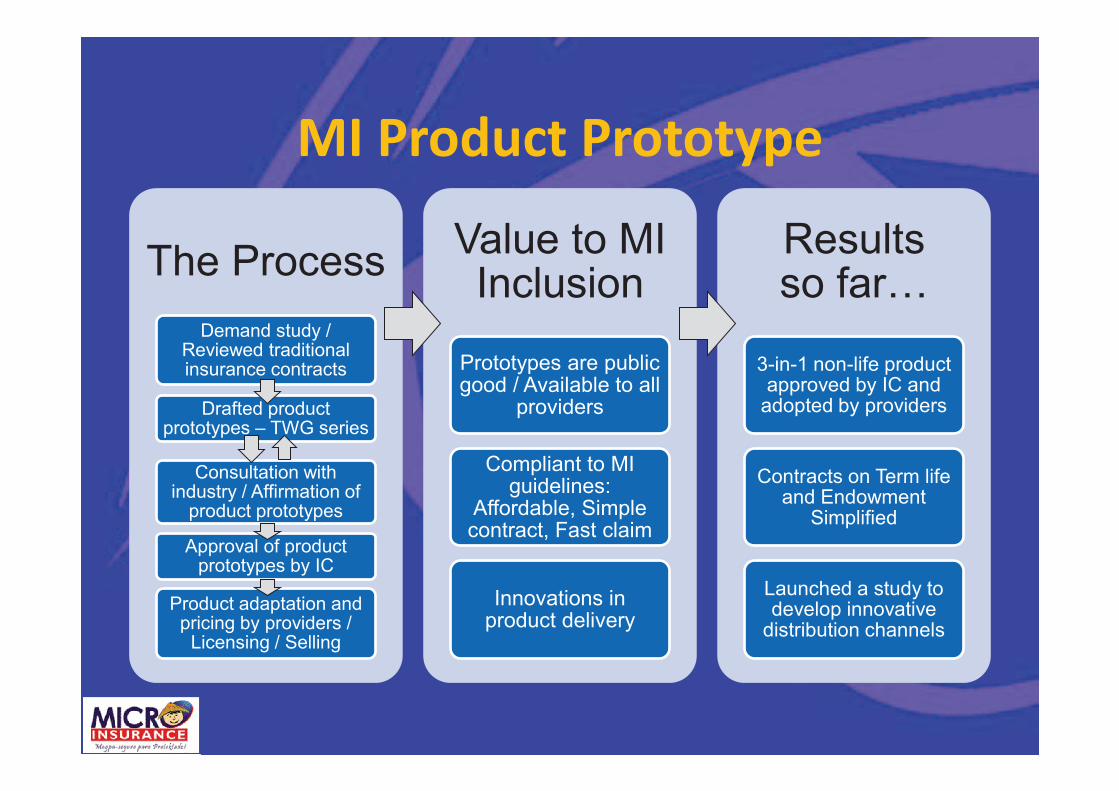

The Process

Demand study / Reviewed traditional insurance contracts

Drafted product prototypes – TWG series

Consultation with industry / Affirmation of

product prototypes

Approval of product prototypes by IC

Product adaptation and pricing by providers /

Licensing / Selling

Value to MI Inclusion

Prototypes are public good / Available to all

providers

Compliant to MI guidelines:

Affordable, Simple contract, Fast claim

Innovations in product delivery

Results so far…

3-in-1 non-life product approved by IC and

adopted by providers

Contracts on Term life and Endowment

Simplified

Launched a study to develop innovative

distribution channels

Financial

Literacy (FinLit)

on

Microinsurance

Finlit – Vision

Adequate risk protection for the

low-income sector through a strong

insurance culture among the

Filipinos

• protect their financial assets

• manage their resources for risk and social protection

To help the low-income

sector

• become proactive in the provision and promotion of Microinsurance

•To build

capacities of stakeholders

Finlit – Objectives

MI Advocacy – Strategies

Target stakeholders

1. Legislators

2. Regulators

3. National Government

Agencies

4. LGUs

5. Insurance Providers

6. Intermediaries

7. Support Institutions

8. Donors

9. Clients

Training of MI Speakers’ Bureau

Training of MI Advocates (TOMA)

MI Seminars for public and private entities

MI seminars for clients by respective stakeholders

Financial Literacy on MI

MI Advocacy – Tools

Financial Literacy on MI

Training modules

Audio Visual Presentations (AVPs)

Jingles

Flip chart

Poster

Brochures

Frequently Asked Questions (FAQs)

FINLIT ROADSHOWS

Cagayan Valley – Tuguegarao

(May 21-26, 2012)

CAR - Baguio City (July 16-21, 2012)

Ilocos - San Fernando

(April 16-20, 2012)

Central Luzon – San Fernando,

Pampanga (June 18-23, 2012)

NCR (January 23-25

& 31, 2012)

Southern Luzon – Calamba, Laguna

(June 4-9, 2012)

Bicol – Legazpi City

(February 6-11, 2012)

Eastern Visayas – Tacloban City

(Sept 19-21, 2011) Western Visayas – Iloilo City

(February 20-25, 2012)

Northern Mindanao – Cagayan de Oro

(April 23-28, 2012)

Zamboanga Peninsula –

Zamboanga City (May 7-12, 2012)

ARMM – Cotabato City (August 2012)

SOCCSKARGEN –

Koronadal City (July 2-7, 2012)

Davao – Davao City

(March 19-24, 2012)

Central Visayas – Cebu City

(March 5-10, 2012)

CARAGA – Butuan City

(Oct 10-14, 2011)

Roadmap to FinLit on MI

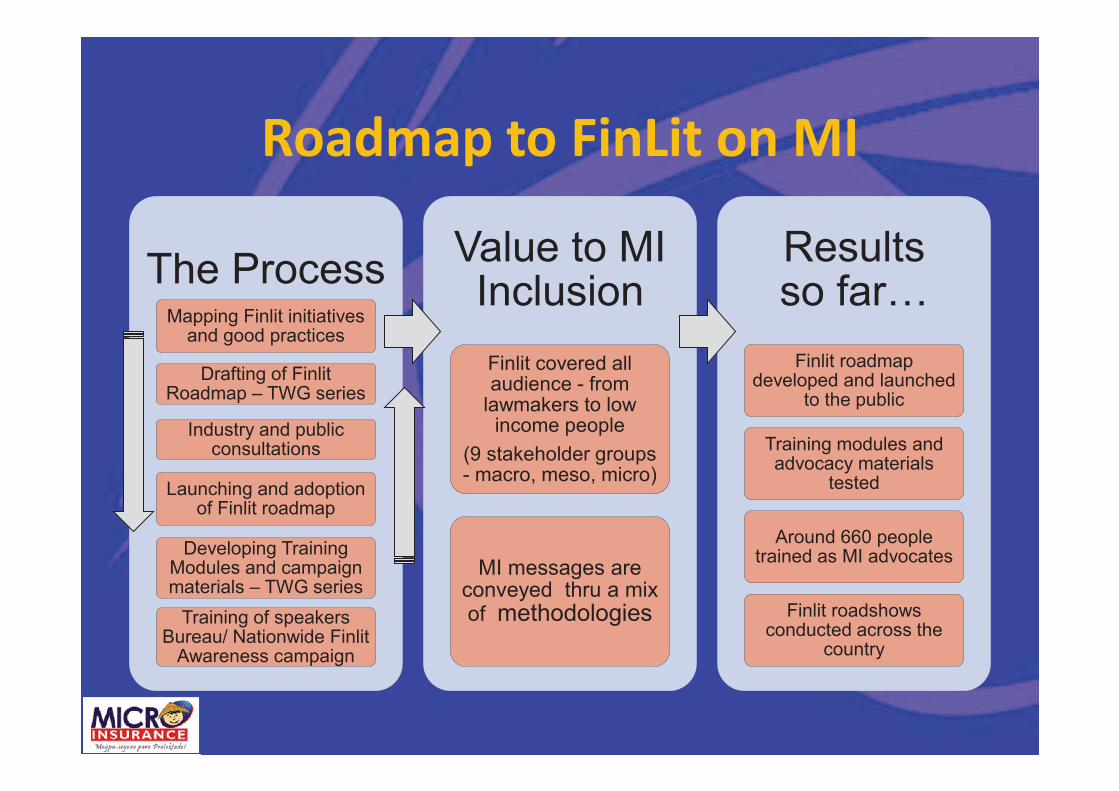

The Process Mapping Finlit initiatives

and good practices

Drafting of Finlit Roadmap – TWG series

Industry and public consultations

Launching and adoption of Finlit roadmap

Developing Training Modules and campaign materials – TWG series

Training of speakers Bureau/ Nationwide Finlit

Awareness campaign

Value to MI Inclusion

Finlit covered all audience - from

lawmakers to low income people

(9 stakeholder groups - macro, meso, micro)

MI messages are conveyed thru a mix of methodologies

Results so far…

Finlit roadmap developed and launched

to the public

Training modules and advocacy materials

tested

Around 660 people trained as MI advocates

Finlit roadshows conducted across the

country

Consumer Protection (CP) Tools

• All entities that will engage or are

engaged in insurance activities are

required to get a Certificate of

Authority from the Philippine

Insurance Commission (PIC).

• All insurance products shall be

approved by PIC.

Government’s Policy

Consumer Protection (CP) Tools

Joint Memo Circular 01-2010 - Who should be regulated

WITH REGULATION

• Contributions/premiums are regularly collected prior to the occurrence of a contingent event; and

• Guaranteed benefits are provided upon the occurrence of a contingent event.

NO REGULATION

• Individuals voluntarily pledge and contribute a certain amount of money to a fund.

• Benefits are not pre-determined but are contingent to the amounts collected. (e.g. Damayan/ Abuluyan Scheme)

Consumer Protection (CP) Tools Joint Memo Circular 01-2010 – Options for Formalization

WITHIN 1 YEAR

• Partner with commercial insurance companies that will provide approved insurance products, either:

• Group policies

• Individual policies

• Have members/clients join:

• A Mutual Benefit Association

• A cooperative insurance provider

• Enter into formal arrangements with authorized insurance providers/Microinsurance agent/broker

WITHIN 2 YEARS

• Organize into an insurance provider and seek appropriate authority from the Insurance Commission

• Life or non-life insurance company

• Mutual Benefit Association

• Cooperative Insurance Provider

Consumer Protection (CP) Tools

SEGURO – Performance Standards for MI (Insurance Circular 5-2011)

Stability

Efficiency

Governance

Understanding of the Product by the Client

Risk-Based Capital

Outreach

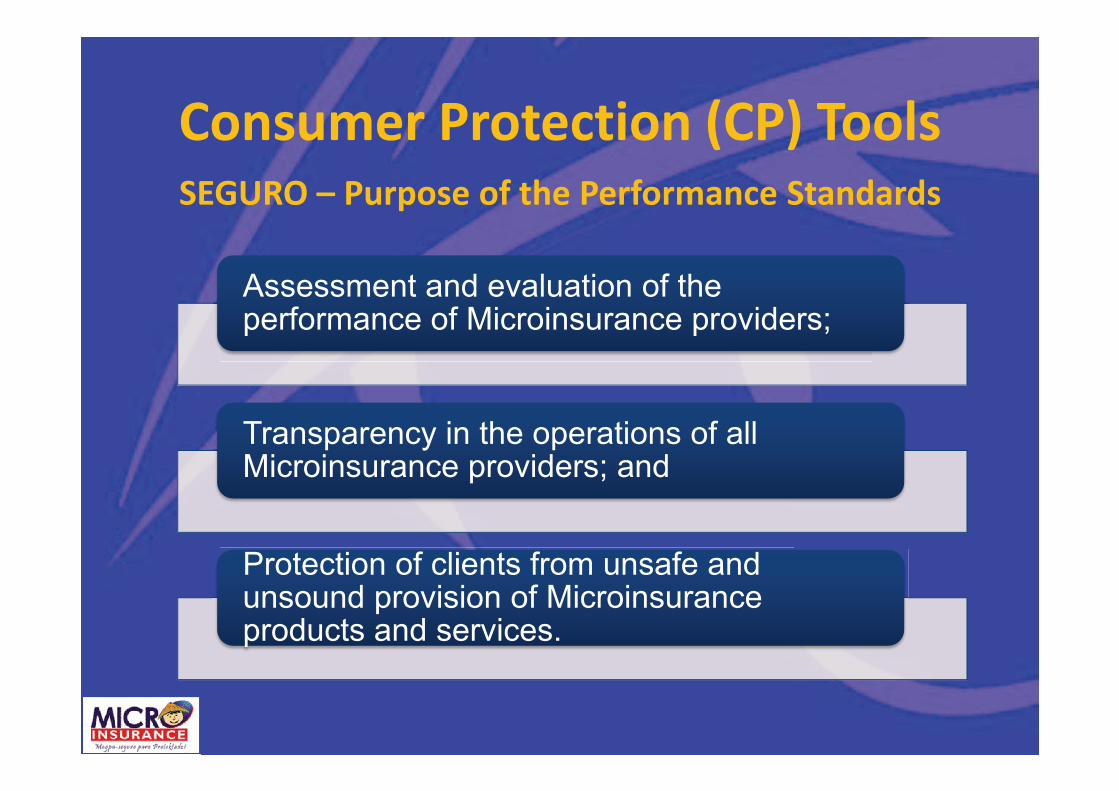

Consumer Protection (CP) Tools

SEGURO – Purpose of the Performance Standards

Assessment and evaluation of the performance of Microinsurance providers;

Transparency in the operations of all Microinsurance providers; and

Protection of clients from unsafe and unsound provision of Microinsurance products and services.

Consumer Protection (CP) Tools

SEGURO – Users of the Performance Standards

Insurance Commission

Management of Microinsurance providers

Agents and brokers (particularly the MFIs)

Donor agencies

Domestic and international private investors

General public (existing and potential clients of Microinsurance)

Consumer Protection (CP) Tools

SEGURO – Obligation of Insurance Companies

Submit to the Insurance Commission on or before April

30 the resulting SEGURO indicators covering previous

year’s operations

Consumer Protection (CP) Tools

SEGURO – PIC utilization of PS results

Publish aggregate status report on the Microinsurance industry

Create early warning system

Recommend appropriate remedial measures, when warranted

Review SEGURO at least once in every three (3) years

Consumer Protection (CP) Tools

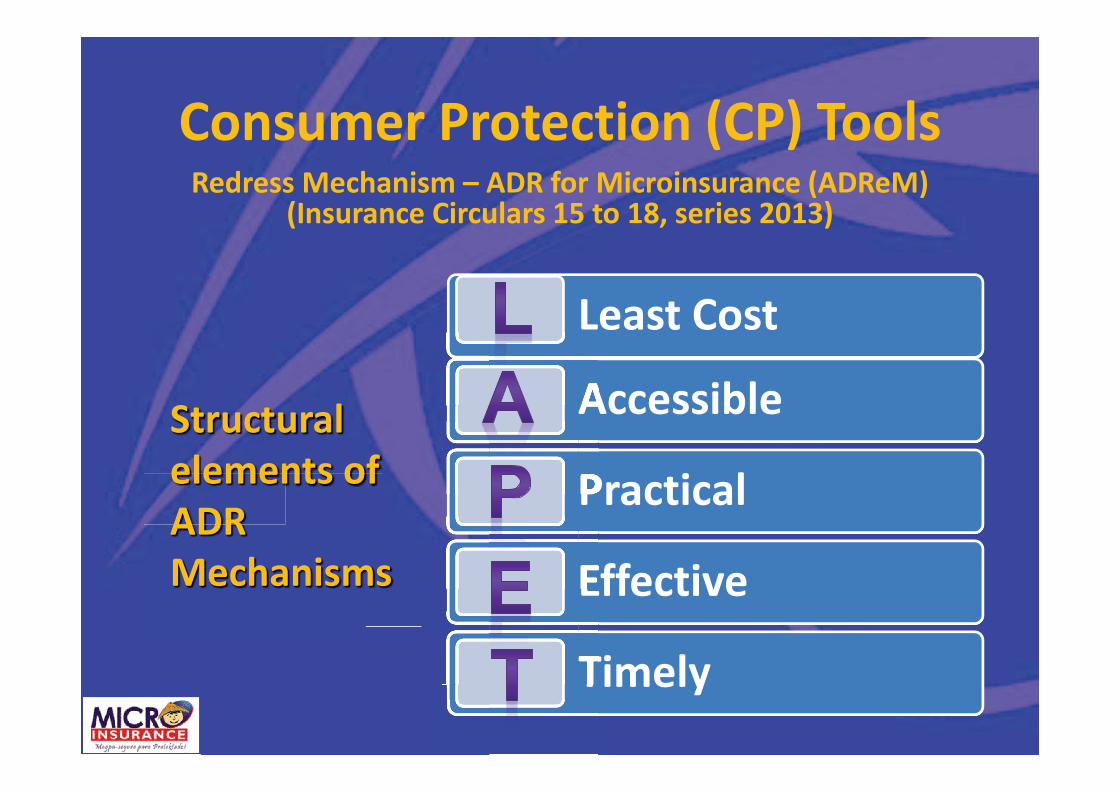

Redress Mechanism – ADR for Microinsurance (ADReM) (Insurance Circulars 15 to 18, series 2013)

• Alternative Dispute Resolution (ADR)

reduces

• cost

• time and

• complexity of any subsequent

litigation.

• ADR provides options to stakeholders

• for resolving disputes outside the

courtroom.

Consumer Protection (CP) Tools

Redress Mechanism – ADR for Microinsurance (ADReM) (Insurance Circulars 15 to 18, series 2013)

To provide avenues to settle Microinsurance disputes through the swiftest and most accessible means.

ADR Objective

Consumer Protection (CP) Tools Redress Mechanism – ADR for Microinsurance (ADReM)

(Insurance Circulars 15 to 18, series 2013)

Structural

elements of

ADR

Mechanisms

Least Cost

Accessible

Practical

Effective

Timely

Consumer Protection (CP) Tools

Redress Mechanism – ADR for Microinsurance (ADReM) (Insurance Circulars 15 to 18, series 2013)

Reporting Information Campaign

Information on the outcome of cases referred to ADR

processes shall be incorporated in the

Annual Reports submitted by insurance

providers to the PIC.

Microinsurance providers and delivery channels shall promote

the use of mediation and conciliation as a recourse mechanism available to

all policyholders to address any dispute.

Market Response

Before 2009

MI products mostly credit life except for MBA MI products

6 licensed MI-MBA

Very few commercial insurance companies with MI

No MI agent category

End-2012

80 MI products approved (54 life and 26 non-life)

17 licensed MI-MBAs

35 insurance companies (17 life and 18 non-life)

124 licensed as MI agents (34 Rural Banks and 90

individuals)

Market Response

Before 2009

3.1 million individuals covered under MI

Insurance penetration was only 1.02 % of GDP

Insurance density Php878 ($19): Life Php654 ($14), Non-life

Php224 ($5)

Estimated life insurance coverage was 13.90% of 91 M population

End-2012

About 12 million insured including dependents are

covered under MI

Insurance penetration was 1.42% of GDP

Insurance density Php1541 ($37):Life Php1265 ($31), Non-

life Php276 ($6)

Estimated life insurance coverage was 23% of 97.6 M population

Lessons and Challenges

1. Government alone cannot meet

the goals of inclusive insurance.

2. Donor assistance should be

coordinated and synchronized.

-- Acknowledgement --many of the slides and contents used in this

presentation were adapted from files of power

point presentations prepared by the Philippine

Department of Finance – National Credit

Council and the Insurance Commission

Maraming Salamat!!

(Thank You)