carmen venter workshops for cfp®...

TRANSCRIPT

2015

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 1

TAXATION OF TRUSTS

DISCLAIMER: The information in these notes is for general information purposes only and is not a substitute for professional advice. The presenter will not accept responsibility for any actions taken or not taken on the basis of the information in these notes.

These notes include summaries and case studies of some of the many issues involving Trusts and is therefore by no means exhaustive.

COPYRIGHT: This material is copyright by Carmen Venter and therefore, no part of this material may be reproduced or distributed in any form or means without the Author’s written permission. Reproduction of any of the work that is not authorized, will constitute a copyright infringement and the offender can be liable under the civil and or criminal law.

Where material has been sourced – reference has been made and there are not protected under the copyright notice.

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 2

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 3

TESTAMENTARY TRUST

[ TRUST MORTIS CAUSA]

Comes into being on date of death

INTER VIVOS TRUST

Comes into being during the lifetime of the founder

DISCRETIONARY VESTING TRUST

TRUST {BEWIND }

SPECIAL TRUST

AGE OF 18 & BELOW MENTALLY HANDICAPPED

VESTING :

TERMINOLOGY USED AND MEANING

Beneficiaries have vested rights in the trust assets. Trustees are merely administrators of the assets

DISCRETIONARY: Beneficiaries have no vested rights in the trust assets. Ownership (control) of the assets vest in the Trustees in their fiduciary capacity as a Trustee, who administer the trust assets for the benefit of the beneficiaries.

SPECIAL TRUST: INCOME TAX - (a) minor beneficiaries under the age of 18 stops being a special trust in the year of

assessment that last child becomes 18 or death (b) mentally handicapped / serious physical disability of mentally handicapped

CAPITAL GAIN (a) mentally handicapped/ serious physical disability stops being a special trust at earliest of :-all

assets are disposed of or 2 years from date of death.

VESTS: Beneficiary has a guaranteed/ unconditional right to income/ capital of the trust . If it is an immediate right – then he exchanges it from a vested right/a personal right to a real right. If it is a right sometime in the future – he retains a vested right / a personal right. Vested right includes: income due and payable; income credited to an account in favour of the beneficiary, income capitalized; income dealt with in favour of the beneficiary [ pay support, maintenance, education etc]

CONTINGENT RIGHT The right of the beneficiary to income/ capital of the Trust, is not immediate but rather contingent or conditional upon the occurrence of an uncertain event. This right to income/capital will then only vest in the beneficiary when and if the condition has been filled or the contingency has taken place. Before the ‘vesting’ of income/capital, the beneficiary only has a hope (a spes) and therefore cannot constitute an asset in the beneficiary’s hands.

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 4

TAXATION OF TRUSTS [2015 RATES]

ORDINARY SPECIAL

TRUST TRUST

FOR MENTALLY HANDICAPPED

/ DISABILITY

FOR MINORS

INCOME TAX: 41%

NO REBATES

INCOME TAX: NATURAL PERSON

18% - 41%

NATURAL PERSON

18% - 41%

NO REBATES NO REBATES

CGT : 66.6% INCLUSION RATE CGT : 33.3% INCLUSIVE 33.3% INCLUSIVE

27.31% EFFECTIVE RATE 13.65% EFFECTIVE 13.65% EFFECTIVE

NO ANNUAL EXCLUSION ANNUAL EXCLUSION NO ANNUAL EXCLUSION

NO NATURAL PERSON EXCLUSION NATURAL PERSON EXCLUSIONS

NO NATURAL PERSON EXCLUSIONS

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 5

TAXATION OF TRUSTS

EXEMPTIONS ALLOWED

S 10(1)(k)(i) = local dividend [15% WITHHELD]

S10 B = foreign dividend using the formula = [foreign dividend received x 25/40]

EXEMPTIONS NOT ALLOWED

S10 (1)(i) – local interest exemption only for natural persons

PRIMARY/ SECONDARY / TERTIARY REBATES

Not allowed for a Trust – whether ordinary or a special trust – as these are for natural persons only

Medical credit rebates – whether ordinary or a special trust – as these are for natural persons only

DEDUCTIONS ALLOWED

Expenses incurred in the production of income is allowed – normal tax rules apply.

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 6

Using the above facts, calculate the taxation in each ‘type’ of trust:

An ordinary Trust, receives income totaling R 100 000 and capital gain from the sale of a ‘primary residence’ of R 2 500 000. The income is made of R 50 000 rental, R 25 000 local interest, R10 000 local dividend and R15 000 foreign dividend. Taxable income and tax payable in the trust?

EXAMPLE 1 – ORDINARY TRUST

rental income 50 000 local interest 25 000 local dividend exempt 0 foreign dividend 15 000 Exempt (15 000 x 25/40) (9 375) capital gain at 66.6% 1 665 000 taxable income 1 745 625 000 AT 41% - tax payable of R 715 706

EXAMPLE 2 – SPECIAL TRUST FOR MINOR EXAMPLE 3 – SPECIAL TRUST MENTALLY HANDICAPPED

rental income 50 000 rental income 50 000

local interest 25 000 local interest 25 000 local dividend exempt 0 local dividend exempt 0 foreign dividend 15 000 foreign dividend 15 000 foreign dividend exemption foreign dividend exemption

15 000 x 25/40 (9375) 15 000 x 25/40 (9375) capital gain at 33.3% 832 500 capital gain at 33.3% 156 510 taxable income 913 125 taxable income 237 135

TAX AS PER TABLES OF NATURAL PERSONS FOR BOTH THESE TRUSTS

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 7

HOW DO YOU TRANSFER ASSETS INTO A TRUST ?

1. DONATE

DONATIONS TAX > 100 000 ANNUALY AT 20% CAPITAL GAINS TAX AS A RESULT OF A DISPOSAL TO THE TRUST

[ PORTION OF DONATIONS TAX FORMS PART OF BASE COST FOR CAPITAL GAINS PURPOSES] TRANSFER DUTY WHERE APPLICABLE

2. BEQUEST

ESTATE DUTY ON 20% > R 3 500 000 CAPITAL GAINS TAX AS A RESULT OF THE DISPOSAL TO THE TRUST

3. SELL CAPITAL GAINS TAX AS A RESULT OF A DISPOSAL TO THE TRUST TRANSFER DUTY WHERE APPLICABLE

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 8

NATURE OF INCOME RECEIVED INTO AND DISTRIBUTED BY THE TRUST

INTEREST RENTAL TRADE INCOME

ASSETS SOLD OR DONATED OR BEQUEATHED

TRUST

OWN ASSETS THAT ARE GENERATING THE INCOME ABOVE AND DISTRIBUTES TO THE BENEFICIARIES AS PER THE TRUST DEED OR BY TRUSTEES EXERCISING THEIR DISCRETION

CONDUIT PRINCIPLE FOR

INCOME. NB NOT GAIN!

BENEFICIARY BENEFICIARY BENEFICIARY BENEFICIARY

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 9

DIVIDENDS

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 10

WHO IS ACTUALLY LIABLE FOR THE INCOME AND OR GAIN EARNED BY THE TRUST? INCOME

Section 25B (1) any amount received by or accrued to a trust, will be deemed to accrue to a beneficiary , if that beneficiary has a vested right to it.

Section 25B (2) where beneficiary acquired a vested right as a result of a trustee discretion, deemed to accrue to a beneficiary

ELSE :- THE TRUST

SUBJECT TO SECTION 7 CAPITAL GAIN

Para 80(1) where an ASSET is vested in a beneficiary by a trust – forms part of the aggregate gain / loss of the beneficiary to whom the asset was disposed of.

Para 80 (2) where a GAIN is vested (by the fact that he has an interest in the asset or discretion of the Trustees] – the whole or portion of the gain – forms part of the aggregate gain /loss of the beneficiary to whom the gain so vests.

ELSE:- THE TRUST

SUBJECT TO PARA 68 / 69 / 71 /72

CAPITAL GAINS DISTRIBUTION AND TAXATION TRANSACTION DISCRETIONARY VESTING

ASSET (WITH GAIN) DISTRIBUTED 80 (1) BENEFICIARY IS TAXED GAIN = MV ON DATE OF DISTRIBUTION – BC FOR THE TRUST

ATTRIBUTION = DONOR NON RESIDENT = TRUST

EXCHANGE OF PERSONAL USE FOR REAL RIGHT. THIS EXCHANGE IS BACKDATED TO ORIGINAL VESTING. BC = MV AT DISTRIBUTION GAIN = 0

ASSET (WITH LOSS) DISTRIBUTED 80(1) NOT APPLICABLE LOSS REMAINS IN TRUST = ‘CLOGGED’

AS WITH ABOVE LOSS = 0

ASSET SOLD AND ‘GAIN’ DISTRIBUTED 80(2) BENEFICIARY IS TAXED GAIN = PROCEEDS – BC FOR TRUST

ATTRIBUTION = DONOR NON RESIDENT = TRUST

BENEFICIARY TAXED GAIN = PROCEEDS – BC FOR TRUST X % OF INTEREST.

ATTRIBUTION = DONOR

ASSET SOLD AND ‘GAIN’ STAYS IN TRUST 80(2) NOT APPLICABLE NO VESTED RIGHT TO BENEFICIARY TRUST TAXED: GAIN = PROCEEDS – BC FOR THE TRUST

ATTRIBUTION DONOR

BENEFICIARY TAXED GAIN = PROCEEDS – BC FOR TRUST X % OF INTEREST.

ATTRIBUTION = DONOR

TRUST SELLS ASSETS = LOSS 80(2) NOT APPLICABLE LOSS REMAIN IN TRUST LOSS = PROCEEDS – BC FOR TRUST

LOSS REMAINS IN TRUST

BENEFICIARY SELLS HIS INTEREST IN TRUST 80(1) APPLICABLE BC = NIL BENEFICIARY TAXED ON FULL PROCEEDS

BENEFICIARY TAXED GAIN = PROCEEDS – BE FOR THE BENEFICIARY

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 11

ATTRIBUTION RULES

ONLY APPLICABLE IF THERE WAS A DISPOSITION OF A GRATUITOUS NATURE !! AND THE DONOR IS ALIVE!!!

INCOME CAPITAL S7(2) Income vest with spouse – taxed in the hands of the donor spouse

Para 68 Gain vests in a spouse – gain taxed in the hands of the donor spouse

S7(3) and (4) Income vest with minor – taxed in the hands of the parent of the child

Para 69 Gain vested in a minor – gain taxed in the hands of the donor parent

S7(5) income not vested in a beneficiary due to some condition – taxed in the hands of the donor

Para 70 Gain not vested in beneficiary because it is subject to a condition – gain taxed in the hands of the donor

S7(6) income can be revoked by donor – taxed in hands of the donor whether actually vested/disposed or not

Para 71 Gain vested in beneficiary but can be revoked by donor – gain taxed in the hands of the donor

S7(7) income that has been ceded to another (trust ) which was due to the donor – taxed in the hands of the donor

No corresponding gain attribution as asset still owned by donor

S7(8) income received by a non-resident as a result of a gratuitous disposition by a resident donor – taxed in the hands of the donor

Para 72 asset or gain vested in a non-resident beneficiary – gain taxed in the hands of the donor

Para 73 – where income and capital are attributed to a donor - income attributed first then the gain – limited to the saving enjoyed by the trust

S7(9) – asset sold below market value – the difference is a DONATION for donation tax purposes

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 12

Summary of above

IF THERE IS NO DONATION OR DISPOSITION OF A GRATUITOUS NATURE

If the income / capital VESTS with a beneficiary = Beneficiary taxed

If the income / capital DOES NOT VEST with a beneficiary = Trust is taxed

IF THERE IS A DONATION OR DISPOSITION OF A GRATUITOUS NATURE

THEN: WE ARE GOING TO FIRST TRY: TAX THE DONOR – IF NOT, THEN TAX THE BENEFICIARY – IF NOT, THEN TAX THE TRUST

START!!

WHO ARE THE BENEFICIARIES? DO WE:-

1. HAVE A SPOUSE OF THE DONOR? IF YES THEN S7(2) IS TRIGGERED THEREFORE THE DONOR IS TAXED ON INCOME/CAPITAL VESTED IN SPOUSE. [ Reason must be for tax avoidance only!]

2. HAVE A MINOR (BELOW THE AGE OF 18 AND UNMARRIED)? NO?? THEN EITHER MOVE ON OR, TAX THE BENEFICIARY IF VESTED IN BENEFICIARY OR, TRUST IF THE INCOME HAS BEEN RETAINED IN THE TRUST.

YES?? IS THE DONOR THE PARENT OF THE CHILD??? NO?? MOVE ON YES???S7(3) IS TRIGGERED - THEN TAX THE DONOR IF VESTED IN THE CHILD

3. HAVE A MINOR (BELOW THE AGE OF 18 AND UNMARRIED) WHERE THE DONOR IS THE PARENT OF OTHER CHILDREN IN ANOTHER TRUST

– BUT THERE HAS BEEN A CROSS-DONATION [IE: PARENT A DONATED TO TRUST OF B AND PARENT B DONATED TO TRUST OF A]

IF NO?? THEN MOVE ON

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2013 [email protected] www.futurefinance.co.za Page 13

IF YES?? S7(4) IS TRIGGERED =THEN TAX THE PARENT OF THAT CHILD (NOT THE DONOR)! [IE PARENT A WOULD BE TAXED ON THE DONATION MADE BY B]

4. HAVE A DISCRETIONARY TRUST OR A CONDITION IMPOSED?

NO?? MOVE ON

YES?? S7(5) IS TRIGGERED TAX THE DONOR ONLY ON THE INCOME/ CAPITAL RETAINED IN THE TRUST. IF THE INCOME/CAPITAL HAS BEEN DISTRIBUTED – THEN YOU CANNOT TAX THE DONOR UNLESS OTHER S7’S APPLY *IE LIKE 7(3) FOR INSTANCE].

5. DOES THE TRUST HAVE A CLAUSE WHEREBY THE DONOR CAN REVOKE ANY INCOME /CAPITAL? NO?? MOVE ON YESS?? TRIGGERED S7(6) TAX THE DONOR WHEN IT VESTS IN THE BENEFICIARY ONLY (EVEN IF HE HAS NOT EXERCISED THIS POWER HE IS TAXED JUST FOR THE FACT THAT THE ‘POWER’ EXISTS)

6. HAS THE DONOR ‘DONATED’ INCOME TO THE TRUST (IE BY OWNING A RENT PRODUCING ASSET AND RENTAL PAID TO TRUST)?

NO???? MOVE ON YES?? THEN S7(7) IS TRIGGERED AND WHEN INCOME VESTS IN THE BENEFICIARY THEN TAX THE DONOR.

7. HAVE A NON-RESIDENT BENEFICIARY WHO HAS THE VESTED INCOME OR CAPITAL? NO? MOVE ON.. YES? S 7(8) IS TRIGGERED – TAX THE DONOR WHEN THE INCOME /CAPITAL VESTS IN THE BENEFICIARY.

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 14

TAXATION OF INCOME IN AND DISTRIBUTED FROM A TRUST

1. Discretionary Trust? Yes No

2. Income distributed Yes No See Vested Trust

to / vested in Diagram beneficiaries?

3. Donor alive? Yes No Yes No

4. Beneficiary a Yes No Yes No Yes No Yes No

minor/ spouse or condition/ revoke non resident?

5. Tax = D B B B D T T T

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 15

D = DONOR B= BENEFICIARY T =TRUST

. Vesting Trust? Yes No

2. Income distributed Yes No See Discretionary

to beneficiaries? Trust Diagram

3. Donor alive? Yes No Yes No

4. Beneficiary a Yes No Yes No Yes No Yes No minor/spouse/ revoke/non resident?

5. Tax = D B B B D B B B

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 16

D = DONOR B= BENEFICIARY T =TRUST

CASE STUDIES CASE STUDY 1 The Mars Trust was formed in terms of Mr Senior Mars’ will – who died 5 years ago. The beneficiaries of the Mars Trust nominated were Junior Mars and Herbert Mars, Mr Senior Mars’ son and grandson respectively. It was clear from the Trust Deed that neither beneficiary had any vested right to income or capital – distribution was left to the discretion of the Trustees. The Trust Deed further stipulates that any amount that remains unpaid shall be capitalized and paid out to the ultimate beneficiaries still to be determined by the trustees. A rent producing property was bequeathed to the Mars Trust by the late Senior Mars. In the 2015 year of assessment, Junior Mars donated interest bearing investments to the Mars Trust.

In the 2015 year of assessment the Mars Trust received rental income of R120 000 and interest of R 50 000. The trustees paid out R 45 000 to Herbert Mars (R25 000 rental income and R20 000 interest) and R10 000 rental to Junior Mars – the remainder of R 115 000 was retained in the trust. Herbert Mars is currently 17 years old.

TRUST INCOME RENTAL INTEREST 120 000 50 000 PAID HERBERT {25 000) (20 000) GRANDSON OF FOUNDER PAID JUNIOR MARS (10 000) SON OF FOUNDER RETAINED 85 000 30 000 TAX FOR TRUST RENTAL 85 000 INTEREST 0 ATTRIBUTED TO DONOR BENG JUNIOR MARS 85 000 X 41% TAX FOR HERBERT RENTAL 25 000 INTEREST 0 ATTRIBUTE TO HIS PARENT JUNIOR MARS TAX FOR JUNIOR MARS INTEREST 20 000 ATTRIBUTED FOR MINOR s7(3) Interest 30 000 RETAINED IN THE TRUST S7(5) RENTAL 10 000 INTEREST EXEMPTION (23800) INCOME TO BE TAXED 36 200

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 17

CASE STUDY 2 Chris donated a rent-producing asset and shares to a discretionary trust. Mary (age 15) and Margaret (age 22), his daughters, are the beneficiaries of the Trust. No beneficiary has any vested right. During the 2015 year of assessment, the Trust earned R100 000 rental income and R60 000 from local Dividend. The trustees in exercising their discretion distributed to each beneficiary R25 000 from rental income and R10 000 from dividends. Of the remaining R90 000 retained in the trust, an amount of R 30 000 from rental income had to be accumulated until Mary’s

25th Birthday. TRUST INCOME RENTAL DIVIDEND 100 000 60 000 PAID MARY MINOR (25 000) (10 000) PAID MARGARET (25 000) (10 000) RETAINED IN TRUST 50 000 40 000 TRUST TAX RETAINED IN TUST ATTRIBUTED TO DONOR MARY INCOME RECEIVED ATTRIBUTED TO PARENT S7(3) MARGERET RENTAL 35 000 DIV AFTER EXEMPTION 0 CHRIS ATTRIBUTION 7(3) RENTAL 25 000 DIV AFTER EXEMPTION 0 RETAINED IN TRUST 7(5) RENTAL 50 000 DIV AFTER EXEMPTION 0 TOTAL TAX 75 000

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 18

CASE STUDY 3 Ed created a trust for the benefit of his grandchildren – Adam who is 5 and Brian who is 30. He donated assets to the trust. The deed provides that the trustees have discretionary powers to distribute capital / income as they deem fit. The deed provides further that any remaining annual income, or gain made by the trustees is to be accumulated for the beneficiaries but, they will only be entitled to receive the income and or capital when Ed dies or when the beneficiary turns 30 – whichever is earlier. If any beneficiary dies before their age of 30, the other beneficiaries will proportionally be entitled to that amount. In the 2015 year of assessment, the trust received a taxable income of R 50 000 from the donated assets as well as, selling an asset and making a gain of R200 000. The trustees distributed R 10 000 to each beneficiary out of the income and R50 000 to each beneficiary out of the capital gain.

TRUST

INCOME GAIN 50 000 200 000

TO ADAM (10 000) (50 000) TO BRIAN (10 000) (50 000) RETAINED 30 000 100 000 ADAM TAX – ATTRIBUTED TO DONOR 7(3) BRIAN TAX - INCOME 10 000 TAXABLE GAIN 6 660 (50 000 – 30 000 X 33.3%) 16 660 ED TAX ATTRIBUTED 7(3) INCOME 10 000 GAIN ALSO 50 000 ATTRIBUTED 7(5) RETAINED AND CONDITION INCOME 30 000 GAIN 100 000 TOTAL GAIN 150 000 GAIN 39 960 (150 000 – 30 000 X 33.3%) 79 960

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 19

CASE STUDY 4 Ted creates a trust and donates property. The deed stipulates that rental income must be paid to a PBO. Ownership of the property must be transferred back to Ted if he so notifies the trust in writing.

ATTRIBUTED BACK TO TED S7(7)

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 20

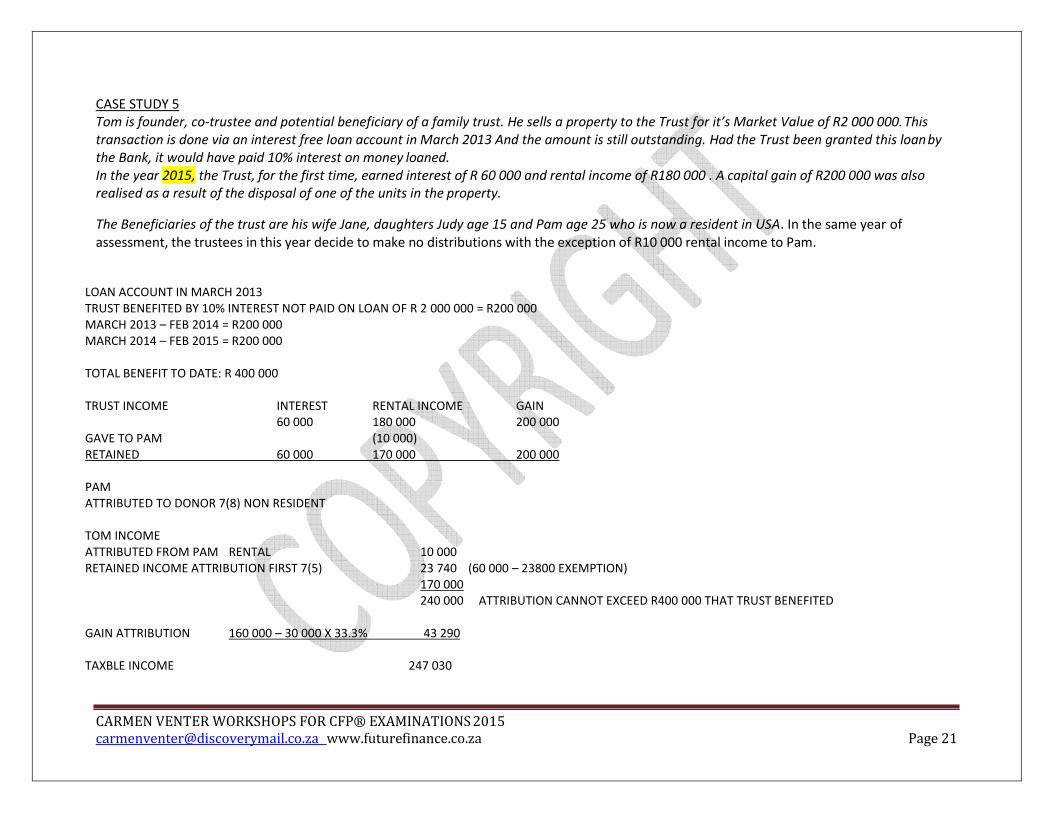

CASE STUDY 5 Tom is founder, co-trustee and potential beneficiary of a family trust. He sells a property to the Trust for it’s Market Value of R2 000 000. This transaction is done via an interest free loan account in March 2013 And the amount is still outstanding. Had the Trust been granted this loan by the Bank, it would have paid 10% interest on money loaned. In the year 2015, the Trust, for the first time, earned interest of R 60 000 and rental income of R180 000 . A capital gain of R200 000 was also realised as a result of the disposal of one of the units in the property.

The Beneficiaries of the trust are his wife Jane, daughters Judy age 15 and Pam age 25 who is now a resident in USA. In the same year of assessment, the trustees in this year decide to make no distributions with the exception of R10 000 rental income to Pam.

LOAN ACCOUNT IN MARCH 2013 TRUST BENEFITED BY 10% INTEREST NOT PAID ON LOAN OF R 2 000 000 = R200 000 MARCH 2013 – FEB 2014 = R200 000 MARCH 2014 – FEB 2015 = R200 000 TOTAL BENEFIT TO DATE: R 400 000 TRUST INCOME INTEREST RENTAL INCOME GAIN 60 000 180 000 200 000 GAVE TO PAM (10 000) RETAINED 60 000 170 000 200 000 PAM ATTRIBUTED TO DONOR 7(8) NON RESIDENT TOM INCOME ATTRIBUTED FROM PAM RENTAL 10 000 RETAINED INCOME ATTRIBUTION FIRST 7(5) 23 740 (60 000 – 23800 EXEMPTION) 170 000 240 000 ATTRIBUTION CANNOT EXCEED R400 000 THAT TRUST BENEFITED GAIN ATTRIBUTION 160 000 – 30 000 X 33.3% 43 290 TAXBLE INCOME 247 030

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 21

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2013 [email protected] www.futurefinance.co.za Page 22

OFFSHORE TRUSTS

DEFINITION OF ‘RESIDENT’ FOR TAX PURPOSES: ‘formed / established & effectively managed in RSA’ = RSA tax resident

a) Remember ! Double Taxation agreement takes precedence! b) If the Offshore Trust is truly a ‘non-resident’ for tax purposes

account to SARS if any income is from a RSA source – this income will attract RSA tax

if a beneficiary is a resident in RSA – the beneficiary is taxed on worldwide income/ capital – unless income previously subject to RSA tax

c) If the offshore trust is ‘resident’ for tax purposes

all amounts received will be subject to tax in RSA

TAX AS PER SECTION 25B OR PARA 80 AND ALL SUBJECT TO ATTRIBUTION RULES

NOTES:

SA Source interest to a non-resident trust – will have 15% withholding interest from 1/1/2013 – unless from GILTS, SA listed debentures and SA bank held deposits

ESTATE DUTY PLANNING

Notes on what to look out for when planning for Estate Planning – in relation to Trusts

NOTE 1

Section 3 (3) ‘ Property which is deemed to be property of the deceased includes:-

(a) ‘ property of which the deceased was immediately prior to his death competent to dispose for his own benefit or for the benefit of his estate.

Section 3 (5) which makes reference to above, we see phrases such as: ‘includes profits of any property’…. ‘has power that would have enabled him to appropriate or dispose of such property as he saw fit’ ……’if under deed of donation, settlement or trust or other disposition…retained the power to revoke or vary provisions..’ ..etc etc

Alter Ego / Sham Trusts eTc Case Law: Jordaan vs Jordaan / Badenhorst vs Badenhorst / Thorpe v Trittenwein / Creighton Trust v CIR

Van der Merwe v Van Der Merwe

NOTE 2

Loan Accounts in Trust

still asset for estate duty purposes although pegged

Bequeathing loan accounts in a Will and Testament to the Trust PARA 12(5) of the 8th Schedule Case law: ITC 1793 / 12399

ANNUAL DONATION BEQUESTS TO REDUCE LOAN ACCOUNT??

CARMEN VENTER WORKSHOPS FOR CFP® EXAMINATIONS 2015 [email protected] www.futurefinance.co.za Page 23