capturing growth opportunities in bc - bcbc.siraza.netbcbc.siraza.net/pdfs/barton presentation -...

TRANSCRIPT

McKinsey & Company |

Looking toward the future:Capturing growth opportunities in BC

May 28, 2013

Business Council of British Columbia

Dominic BartonGlobal Managing Director, McKinsey & Company

McKinsey & Company | 1

LNG – Accelerate development of export capacity to Asia (from 6 Mtpa to at least 18 Mtpa by 2018) before new US and Australian sources come online 22

Gateway economy – Increase share of Asian trade from 5% to 10+% of NA total with Prince Rupert expansion. Build up broader economy with regional HQs of Asian companies, Asia-focused professional services (e.g., law, accounting),and transport services

11

Natural resources (e.g., forestry, coal, copper) – Invest in critical areas to ensure BC at least maintains share as Asia grows, despite recovery in US exports33

Direct engagement – Create cabinet-level position on Asia to signal focus, establish business exchange programs, and convene a tri-sector task force on Asia77

Agrifood – Develop global champions in high-demand protein crops (e.g., beef, seafood, dairy) and processed food to establish BC as net food exporter. Emphasize brand – food safety, quality, and luxury items

44

Education – Establish as top 3 export industry (from 4% to 9% of total exports). Convert at least 60% of language and vocational students to university/college students

55

Tourism – Establish BC as top 3 Western destination for Chinese tourists(70% increase to 375k visits per year). Simplify visa requirement (i.e., faster, less costly, and less complex) for short stays from target markets

66

Seven priorities for BC to pursue

McKinsey & Company | 2

Overview

Five global trends

Opportunities in Asia

BC strengths and opportunities

1

2

3

Lessons from other cities and countries4

McKinsey & Company | 3

Five mega-trends reshaping the global economy

Pricing the planet

The productivity imperative

The market state

The great rebalancing

The global grid

McKinsey & Company | 4

Massive urbanization is underway—old Shanghai

SOURCE: skylander.net

McKinsey & Company | 5

Massive urbanization is underway—new Shanghai

McKinsey & Company | 6

Unprecedented infrastructure development is anticipated over nexttwo decades

SOURCE: OECD Development Center; McKinsey Global Institute analysis; United Nations; McKinsey Global Institute

New large-scale railwaysAs many as 170

large-scale railway systems; currently only 70

in Europe

More big citiesOver 200 cities with population over 1 million;

currently only 35 in Europe

Huge city population 350 million additional

people; more than entire US

population

Thousands of skyscrapers

As many as 50,000;

equivalent to building 10 New

York cities

New large-scale railwaysAs many as 170

large-scale railway systems; currently only 70

in Europe

More big citiesOver 200 cities with population over 1 million;

currently only 35 in Europe

Huge city population 350 million additional

people; more than entire US

population

Thousands of skyscrapers

As many as 50,000;

equivalent to building 10 New

York cities

McKinsey & Company | 7

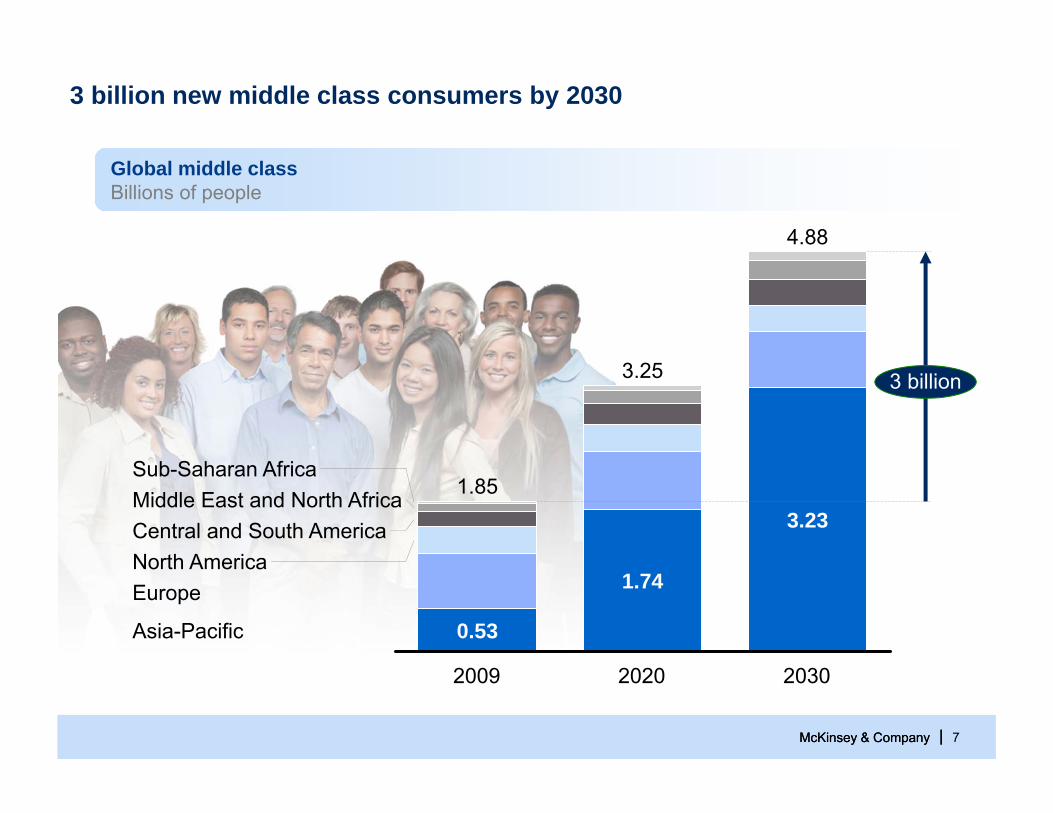

3 billion new middle class consumers by 2030

Global middle classBillions of people

4.88

3 billion

Asia-Pacific

EuropeNorth AmericaCentral and South AmericaMiddle East and North AfricaSub-Saharan Africa

2030

3.23

2020

3.25

1.74

2009

1.85

0.53

McKinsey & Company |

McKinsey & Company | 8

Incomes are rising in developing economies faster, and at a greater scale, than at any previous point in history

SOURCE: Angus Maddison; University of Groningen; Resource Revolution: Meeting the world’s energy, materials, food, and water needs, McKinsey Global Institute, 2011

9

840

1,023

27

48

28

10

Country

154

53

65

33

1700 1800 1900 2000

India

12

16

China

South Korea 10

Japan

Germany

United States

United Kingdom

Year

Population at start of growth period

Years to double GDP per capita

Million

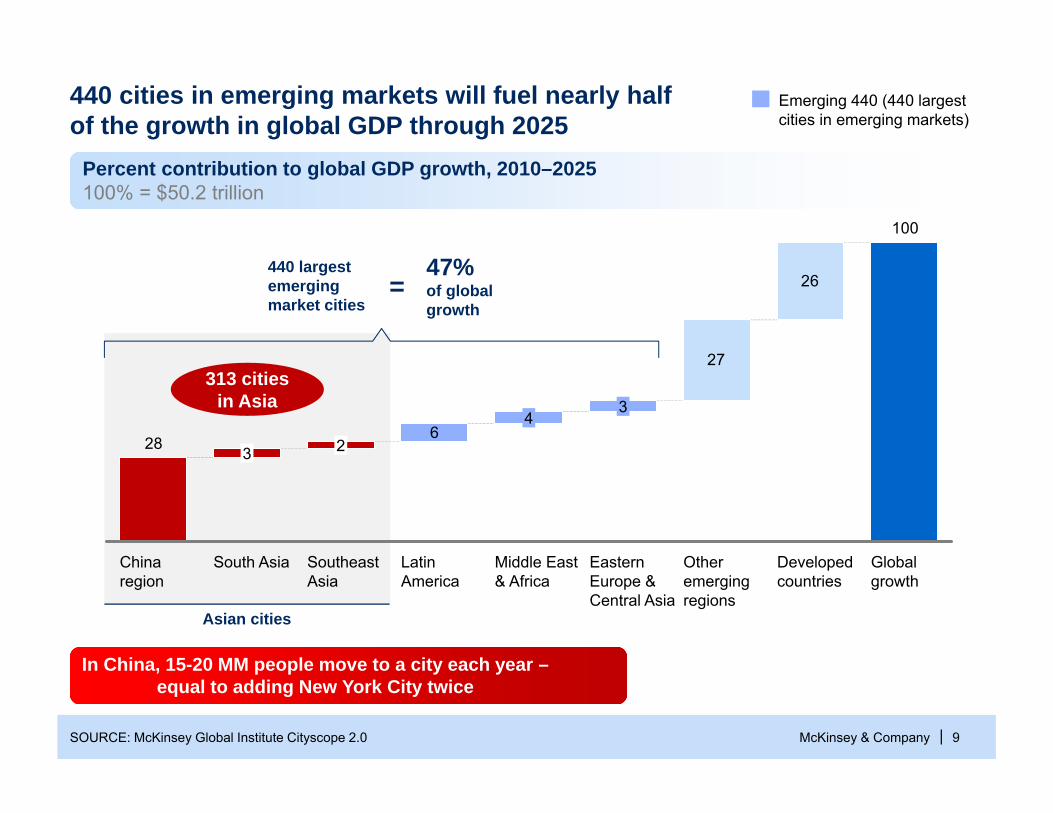

McKinsey & Company | 9SOURCE: McKinsey Global Institute Cityscope 2.0

Percent contribution to global GDP growth, 2010–2025100% = $50.2 trillion

6

27

26

100

28

Global growth

Eastern Europe & Central Asia

Developed countries

Other emerging regions

2

3

Middle East & Africa

4

Latin America

SoutheastAsia

South Asia

3

China region

Asian cities

Emerging 440 (440 largestcities in emerging markets)

440 cities in emerging markets will fuel nearly half of the growth in global GDP through 2025

47%of global growth

440 largest emerging market cities

=

In China, 15-20 MM people move to a city each year –equal to adding New York City twice

313 cities in Asia

McKinsey & Company | 10

Emerging market cities will become the leading consumer markets globally

EmergingAdvanced

2025Rank

1

2

345

678

9

10

11

12

1314

15

Elderly, higher-income consumersShanghaiBeijingTokyoTianjinMumbaiSão PauloOsakaChongqingDelhiNanjingGuangzhouNew York

SeoulHong KongWuhan

xxxx

Municipal water demandMumbaiDelhiShanghaiGuangzhouBeijingBuenos AiresKolkataKhartoumDhakaIstanbulDallas

PuneLas VegasKarachiSão Paulo

Young entry-level consumersLagosDar es SalaamDhakaOuagadougouKhartoumGhaziabadSanaaNairobiLuandaBaghdadKampalaIbadanLusakaKinshasaKano

Laundry care productsSão Paulo Beijing Rio de Janeiro ShanghaiMexico City Moscow Bangkok Istanbul Manila Johannesburg Belo Horizonte Porto AlegreBuenos AiresTianjinTehran

SOURCE: McKinsey Global Institute

McKinsey & Company | 11

Disruptive technology will have enormouseconomic impact by 2025

SOURCE: McKinsey Global Institute analysis

Range of sized potential economic impacts

Impact from other potential applications (not sized)Low High

X–Y$ trillion, annual

Renewable energy 0.2–0.3

Advanced oil and gasexploration and recovery 0.1–0.5

Advanced materials 0.2–0.5

3D printing 0.2–0.6

Energy storage 0.1–0.6

Next-generationgenomics 0.7–1.6

Autonomous and near-autonomous vehicles 0.2–1.9

Advanced robotics 1.7–4.5

Cloud technology 1.7–6.2

Internet of Things 2.7–6.2

Automation ofknowledge work 5.2–6.7

Mobile Internet 3.7–10.8

McKinsey & Company | 12

100

1,000

10,000

100,000

100 1,000 10,000Potential economic impact across sized applications

$ billion (log scale)

A small number of technologies will have disproportionate impact

SOURCE: Factiva; McKinsey Global Institute analysis

Mobile Internet

Internet ofThingsAdvanced

robotics

Autonomous and near-autonomous vehicles Cloud

technology

Automation of knowledge work

High impact technologies

Next-generation genomics

Energy storage

3DprintingAdvanced

materials

Advanced oil and gas exploration and recovery

Renewable energy

Media attentionNumber of relevant articles in major general interest and business publications over 1 year (log scale)

McKinsey & Company | 1313

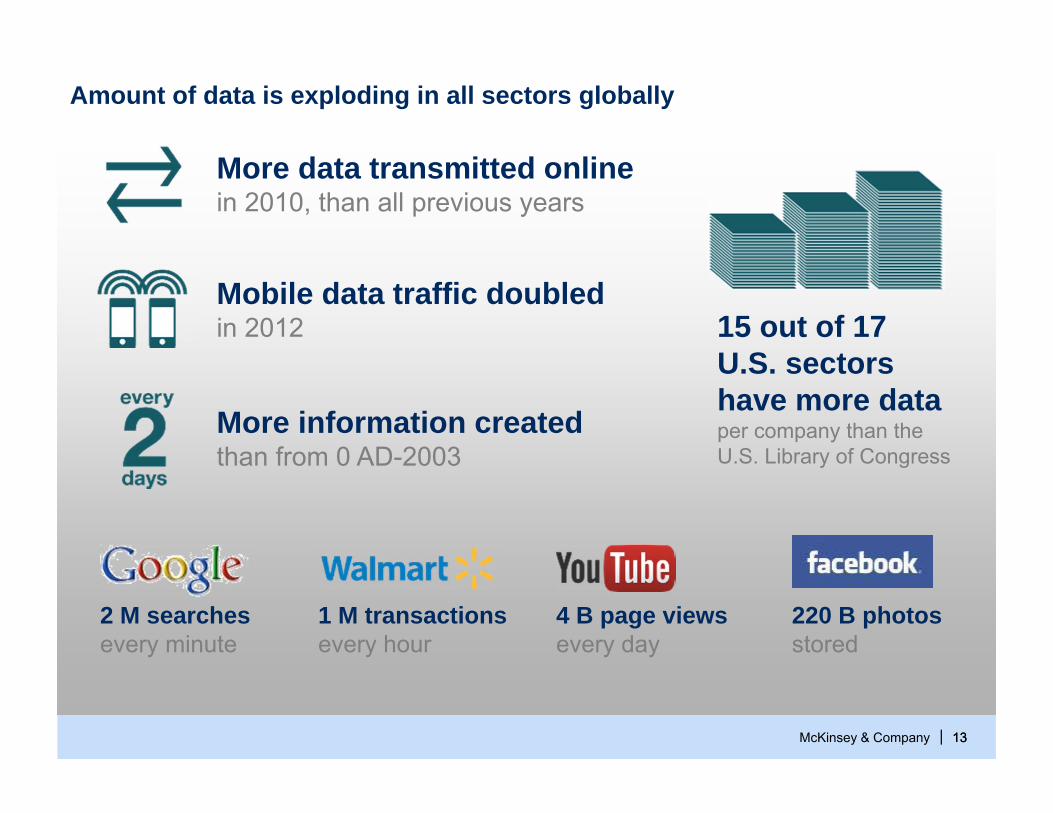

Amount of data is exploding in all sectors globally

220 B photosstored

1 M transactionsevery hour

2 M searchesevery minute

4 B page viewsevery day

Mobile data traffic doubled in 2012

More data transmitted online in 2010, than all previous years

More information created than from 0 AD-2003

15 out of 17 U.S. sectorshave more data per company than the U.S. Library of Congress

McKinsey & Company | 1414

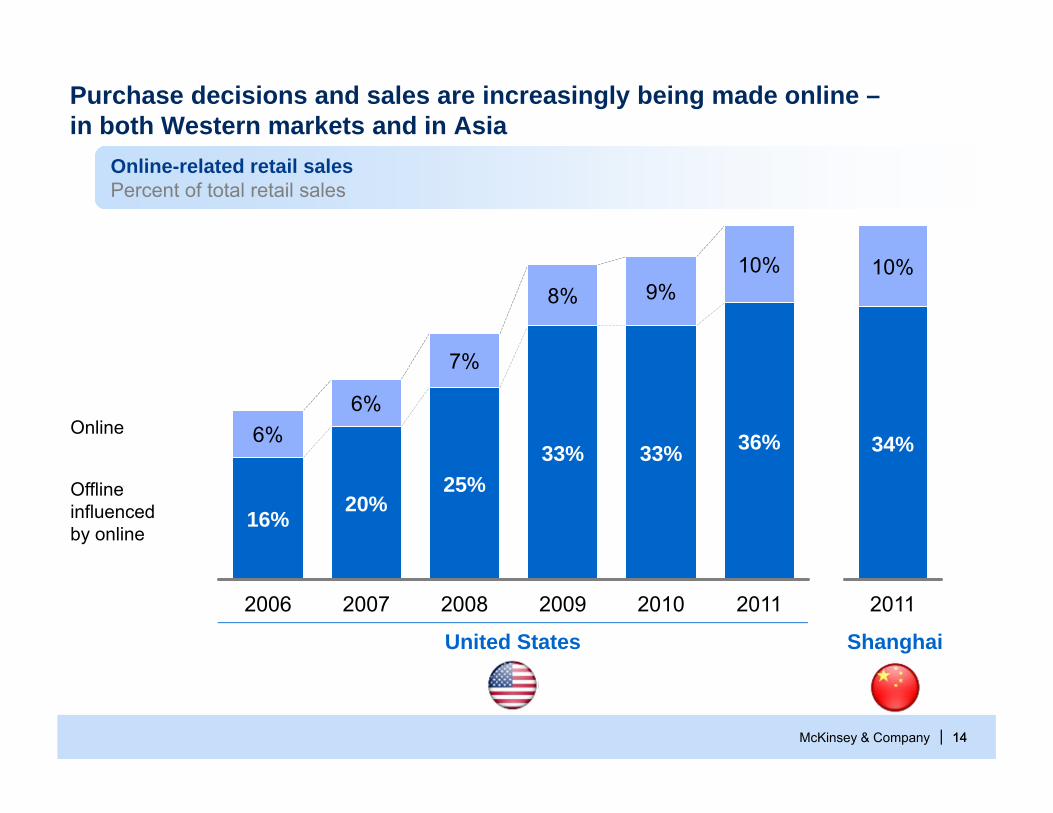

33%

8%

6%

2006

10%

2010

33%

9%

2009

36%

2011

16%

6%

2007

7%

25%

2008

20%

2011

34%

10%

Purchase decisions and sales are increasingly being made online –in both Western markets and in Asia

Online

Offline influenced by online

United States Shanghai

Online-related retail salesPercent of total retail sales

McKinsey & Company | 15

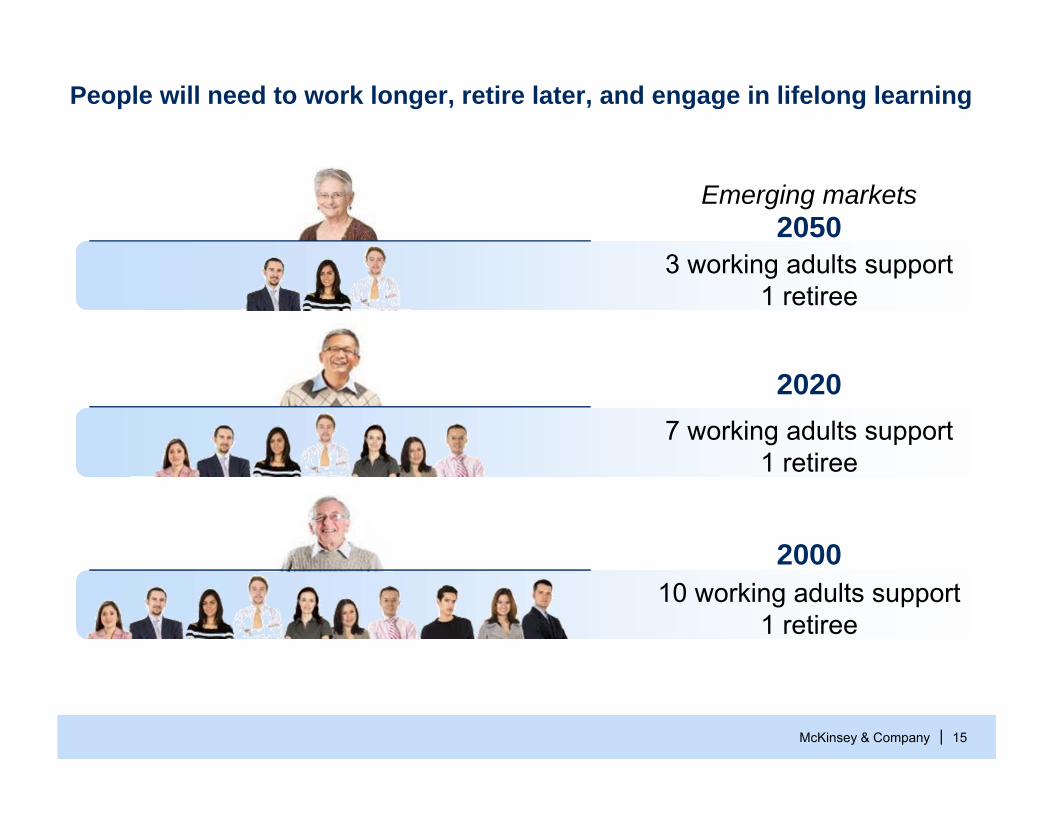

People will need to work longer, retire later, and engage in lifelong learning

10 working adults support 1 retiree

2000

7 working adults support 1 retiree

2020

3 working adults support 1 retiree

2050Emerging markets

McKinsey & Company | 16

We will also face a global shortage of skilled workersand a surplus of low-skilled workers

94

-45-41

Low-skillMedium-skillHigh-skill

Global balance of workers, 2020EMillion workers

McKinsey & Company | 17

The continuing rise of emerging markets will further strain global resources to an unprecedented level

Water FoodEnergy

Increasing gap between demand and supply of fossil fuels; e.g., by 2030 ▪ 25% gap for oil ▪ 30% gap for gas

10,000 years of historical food production thatmust be matchedin the next 50 years

~40% gap between supply and demand by 2030

McKinsey & Company | 18

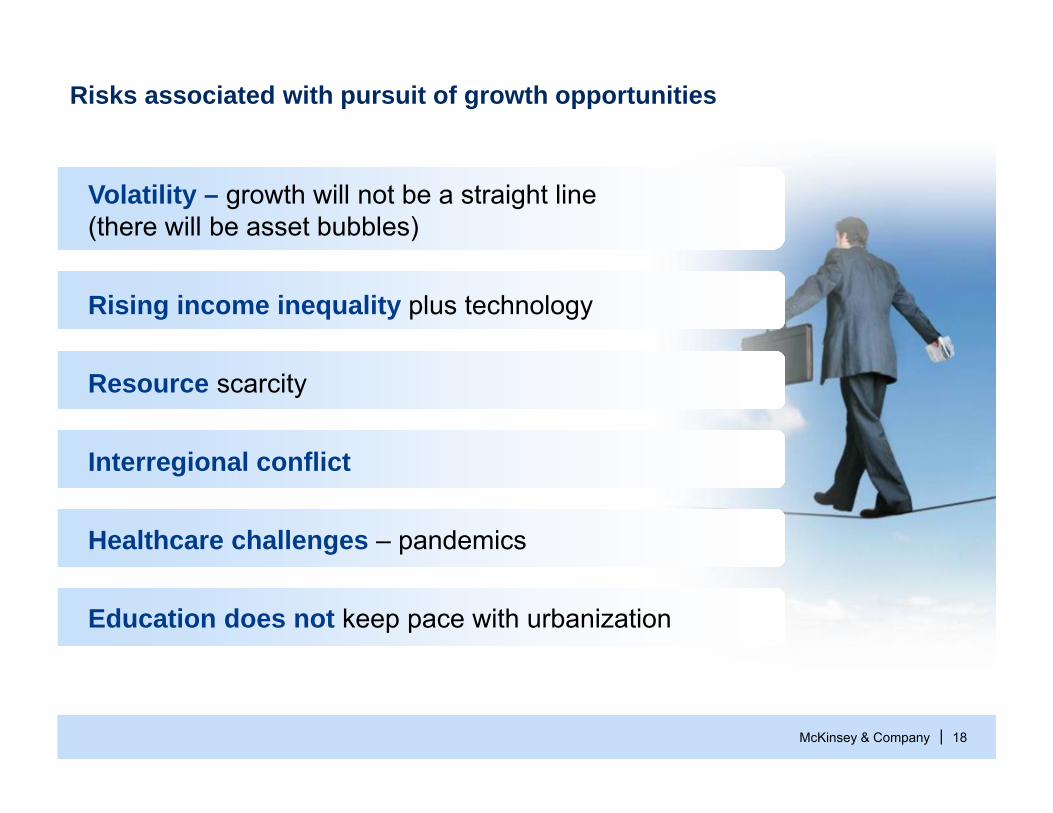

Volatility – growth will not be a straight line(there will be asset bubbles)

Rising income inequality plus technology

Resource scarcity

Interregional conflict

Healthcare challenges – pandemics

Education does not keep pace with urbanization

Risks associated with pursuit of growth opportunities

McKinsey & Company | 19

The lifespan for companies is decreasingEstimated lifespan of S&P 500 companies, years

1822

30

45

90

20111995197519551935

McKinsey & Company | 20

Overview

Five global trends

Opportunities in Asia

BC strengths and opportunities

1

2

3

Lessons from other cities and countries4

McKinsey & Company | 2121

Six significant opportunities in Asia

▪ Consumers – $22 T consumption in emerging markets in 2025 and 2.7 B new middle class consumers by 2030

▪ Education – 1 B Asian youth to educate in any given year and a 36 M shortage of skilled workers in China and India by 2020

▪ Infrastructure – $57 T global demand over next 18 years, with $27 T expected spend in emerging Asia

▪ Tourism – approximately 80 million outbound Chinese travelers in 2012, growing to over 110 million in 2015

▪ Agriculture & food – 2x global increase in meat demand by 2050 due to rise of emerging markets, anticipated 60+% rise in meat consumption in China

▪ Natural resources – 30% increase in global energy needs and 80% in steel needs by 2030

McKinsey & Company | 22

Emerging market consumption will be $30 trillion by 2025,nearly half of global total

$ Trillions

2634

12

30

Developed

Emerging

2025

64

2010

38 Brazil 3

India

10

China 8

Total 30

1

Other

Poland 1

Turkey 1

Indonesia 1

Mexico

Russia 2

3

SOURCE: McKinsey Global Institute

World consumption Emerging market consumption in 2025

McKinsey & Company | 23SOURCE: McKinsey analysis; Global Insight; Economist Intelligence Unit

2,823

2000

1,858

1990

817

2010

+245%

Asian consumers’ disposable incomes have been rapidly increasingover the last 2 decades

+165%

1990

N/A

20102000

381

1,010

1990

+133%446

2000

465

1,040

2010

Indonesia

+204%

20102000

2,464

7,480

2,989

1990

80247

522

201020001990

+553%

India

Turkey Vietnam

Urban China

Per capita disposable incomeUSD (2010 real terms)

McKinsey & Company | 24

The Chinese market is already rivals Western markets in regards to consumption

2nd largest digital camera marketafter the US – more units than Japan, South Korea, and Singapore combined

Flat-screen TV sales of 50 million– 42 M sold in the US and Canada

Largest retail market for laptop computers(27 M units vs. 22 M units in the US in 2012)

Laundry softener sales have grown 20% annually for the past 5 years– surpassing sales in Germany and France

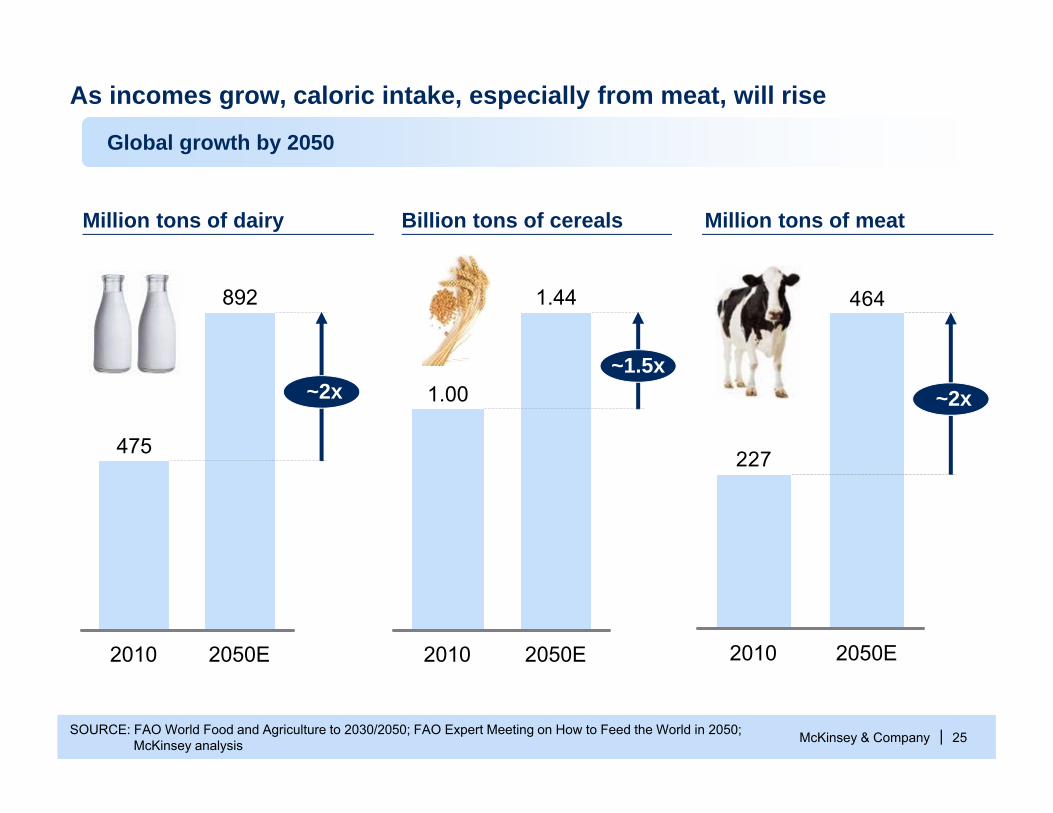

McKinsey & Company | 25SOURCE: FAO World Food and Agriculture to 2030/2050; FAO Expert Meeting on How to Feed the World in 2050; McKinsey analysis

Global growth by 2050

As incomes grow, caloric intake, especially from meat, will rise

892

~2x

475

2050E2010

Million tons of dairy

1.44

~1.5x1.00

2050E2010

Billion tons of cereals

464

227

~2x

2050E2010

Million tons of meat

McKinsey & Company | 26

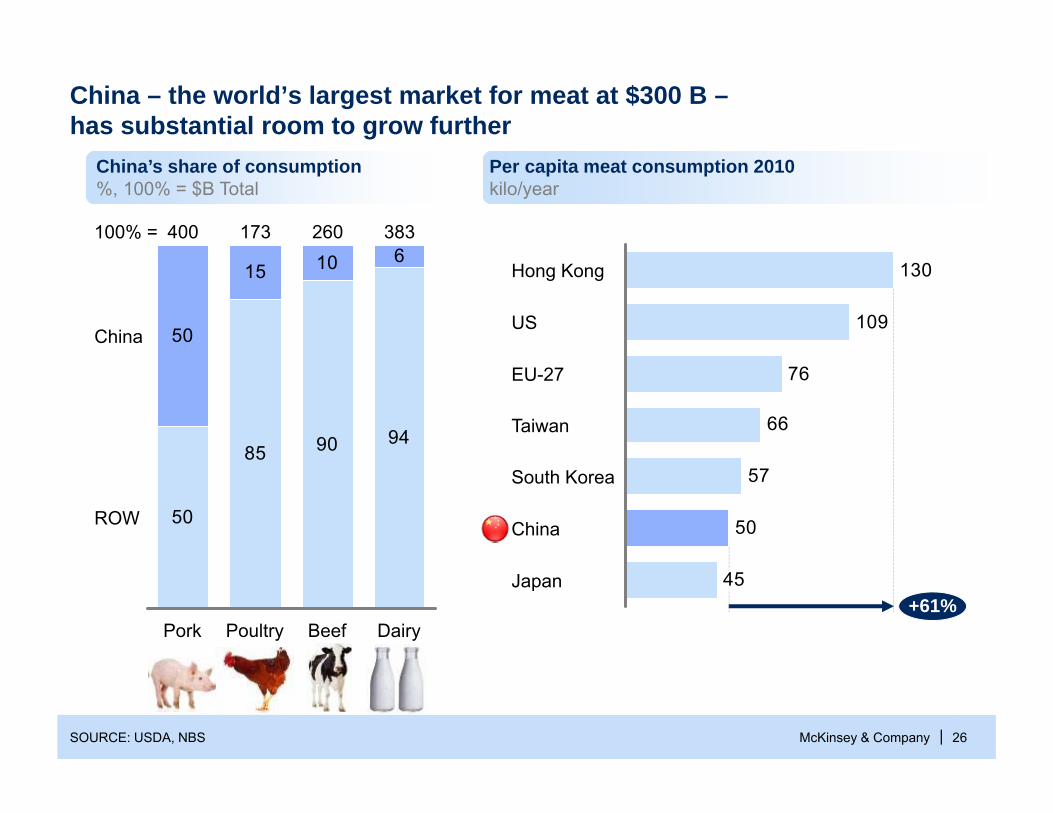

China – the world’s largest market for meat at $300 B –has substantial room to grow further

45

50

57

66

76

109

130

+61%Japan

China

South Korea

Taiwan

EU-27

US

Hong Kong

Per capita meat consumption 2010kilo/year

50

85 90 94

50

15 10 6100% =

ROW

China

Dairy

383

Beef

260

Poultry

173

Pork

400

SOURCE: USDA, NBS

China’s share of consumption%, 100% = $B Total

McKinsey & Company | 27

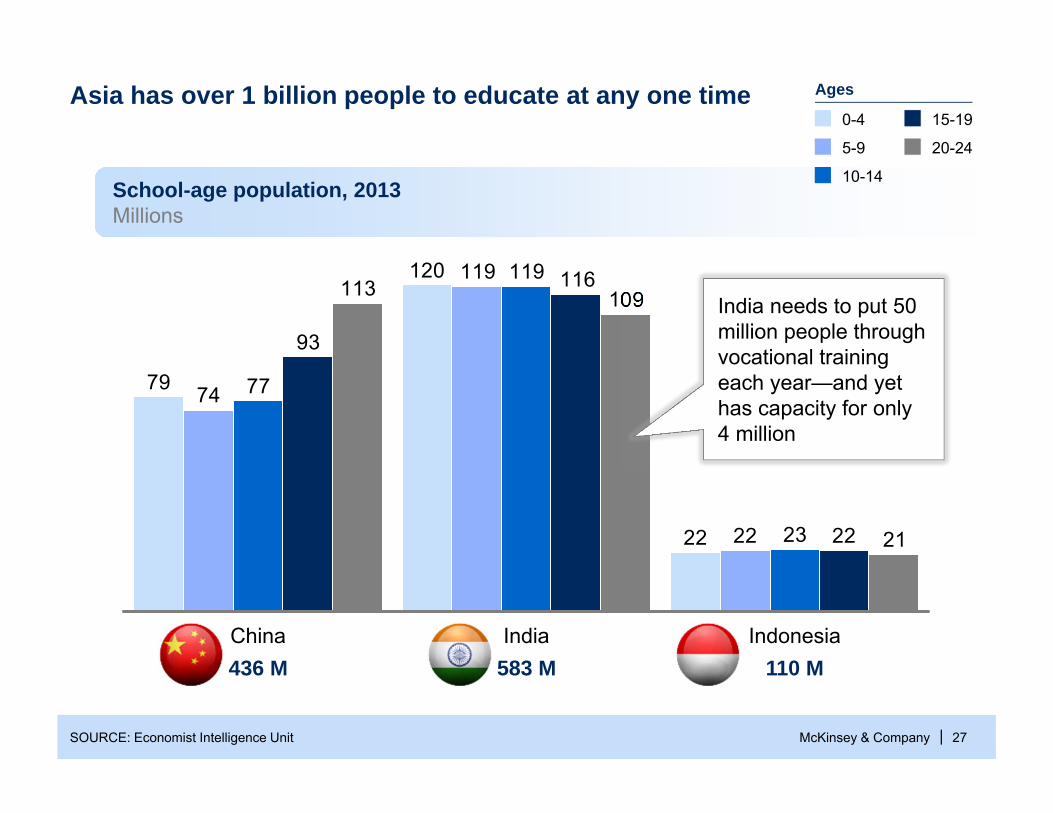

22

120

79

22

119

74

23

119

77

22

116

93

21

109113

IndonesiaIndiaChina

20-24

15-19

10-14

5-9

0-4

School-age population, 2013Millions

AgesAsia has over 1 billion people to educate at any one time

436 M 583 M 110 M

India needs to put 50 million people through vocational training each year—and yet has capacity for only 4 million

SOURCE: Economist Intelligence Unit

McKinsey & Company | 28

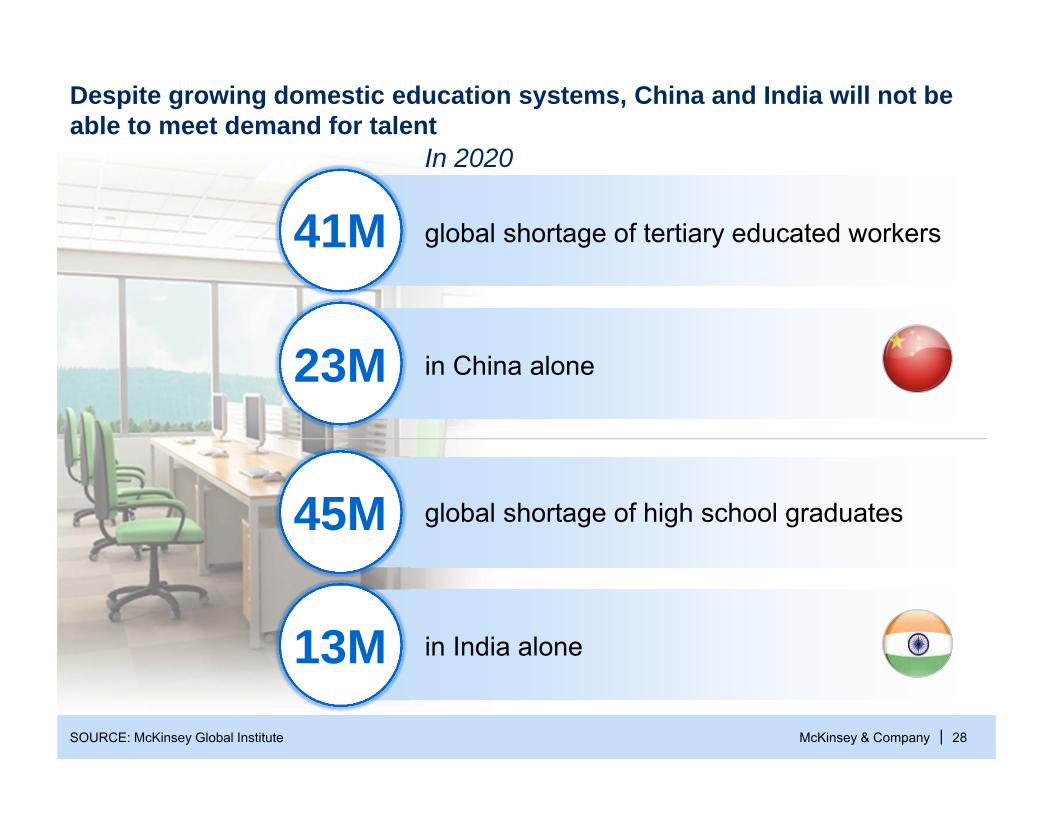

Despite growing domestic education systems, China and India will not be able to meet demand for talent

SOURCE: McKinsey Global Institute

In 2020

41M

23M

45M

13M

global shortage of tertiary educated workers

in China alone

global shortage of high school graduates

in India alone

McKinsey & Company | 29

0

50,000

100,000

150,000

200,000

2011-122010-112009-102008-092007-08

International students in the United States

China is sending more students abroad – while other countries stagnate

SOURCE: Institute of International Education

Turkey

Mexico

Vietnam

Japan

Canada

Taiwan

Saudi Arabia

South Korea

India

China

McKinsey & Company | 30

112

7870

57

31

+15% p.a.

+26% p.a.

2012201120102005 2015E

Overseas tourism has soared in China and is expected to grow further

SOURCE: CEIC, China tourism yearbook, Euromonitor

China outbound travelersMillions

McKinsey & Company | 3131

% of total respondents

SOURCE: Insights China; 2010 China Consumer Survey, focus groups; team analysis

Relieving pressure and escaping to nature are Chinese travellers’top motivators

63

11

19

Increase foreign exposure

Learn knowledge and culture

Relieve work pressure & relax 10

44

8

14

Other (e.g., visit family)Shopping

Entertainment(e.g., karaoke)

Folk culture

Historic sites

Natural landscape(e.g., sea, mountains)

59

% of respondents

The first thing that we seek is natural landscape, especially things that we can’t see here such as the sea

Wuhan participant

Primary purpose for travelTop 3 motivations for travel

McKinsey & Company | 32

Canada has an opportunity to capture a much higher shareof Chinese travelers

Mongolia 0.3

Canada

0.3

0.3Germany0.40.4

Indonesia 0.6United Kingdom

1.1Cambodia

Thailand

Australia

Singapore

1.5

1.2

1.0

USA

Russia0.7

0.8

Vietnam

1.4

France

South Korea

1.6

2.41.8

1.7Taiwan

JapanMalaysia

SOURCE: CEIC, China tourism yearbook, Euromonitor (2011)

China international travellers by destination Millions, 2011

McKinsey & Company | 33SOURCE: McKinsey Insights China; McKinsey Global Economic Growth Database; McKinsey Global Institute

1 Stock of net fixed assets at the end of the year, assuming 5% depreciation rate for all the assets

Demand for infrastructure rises as income increases

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000

Capital stock per capita1

140

120

100

80

60

40

20

0

GDP per capita

Urban China

ChinaIndia

Germany

South Korea

Japan

Italy

UK

US

Capital stock vs. GDP per capita by country and year, 1980–2008$ Thousands, sample of selected countries, constant 2005 prices and exchange rates

McKinsey & Company | 3434

Length of expresswaysThousand km

Length of railwaysThousand km

AirportsNumber of airports

Capacity of container terminalsM TEU (20-foot equivalent units)

12090

78

+33%

202020102007

China plans to rapidly expand infrastructure

100

6554

+54%

202020102007

244192

152

+27%

202020102007

240

13695

+76%

202020102007

SOURCE: CIA factbook; S&P; World Bank; IWG; Difu; Yearbook of China Transportation and Communications; team analysis

McKinsey & Company | 35

Pudong District, Shanghai

$27 trillionAsia infrastructureinvestment need2013-2030

SOURCE: Lujiazui Road, Pudong District, Shanghai

$57 trillionglobal infrastructureinvestment need2013-2030

McKinsey & Company | 36

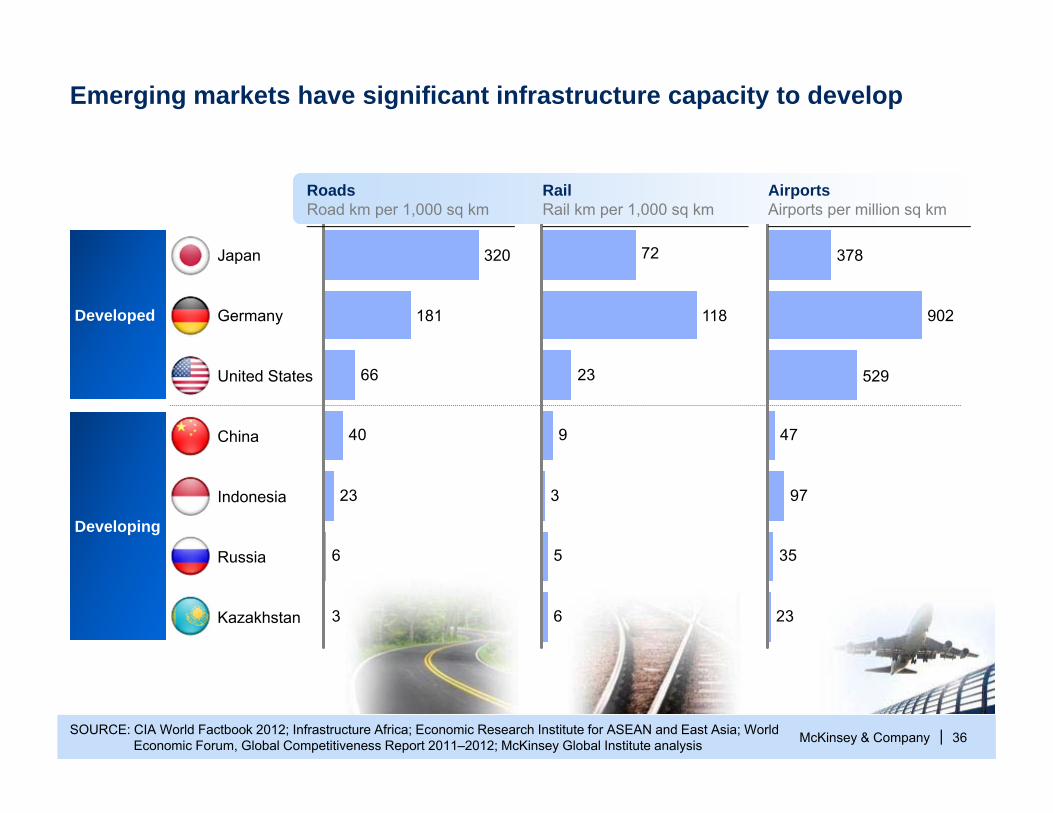

Emerging markets have significant infrastructure capacity to develop

SOURCE: CIA World Factbook 2012; Infrastructure Africa; Economic Research Institute for ASEAN and East Asia; World Economic Forum, Global Competitiveness Report 2011–2012; McKinsey Global Institute analysis

3

6

23

40

66

Kazakhstan

Russia

Indonesia

China

United States

Germany 181

Japan 320

6

5

3

9

23

72

118

23

35

97

47

529

902

378

Developing

Developed

AirportsAirports per million sq km

RailRail km per 1,000 sq km

RoadsRoad km per 1,000 sq km

McKinsey & Company | 37SOURCE: Global Insight; IEA; UN Environment Program (UNEP); FAO; World Steel Association; McKinsey analysis

398

654

+33%

2030

4922010

2000

5682020

+80%

1,847

2,290

1,271

761

6,350

+41%

5,500

4,500

4,000

234

191

137

287

+50%

Rising middle class, urbanization, and infrastructure build-up will drive strong global resource demand

FertilizerMillion tonnes

WaterCubic kilometers

SteelMillion tonnes

Primary energyQuadrillion BTU1

1 British Thermal Units

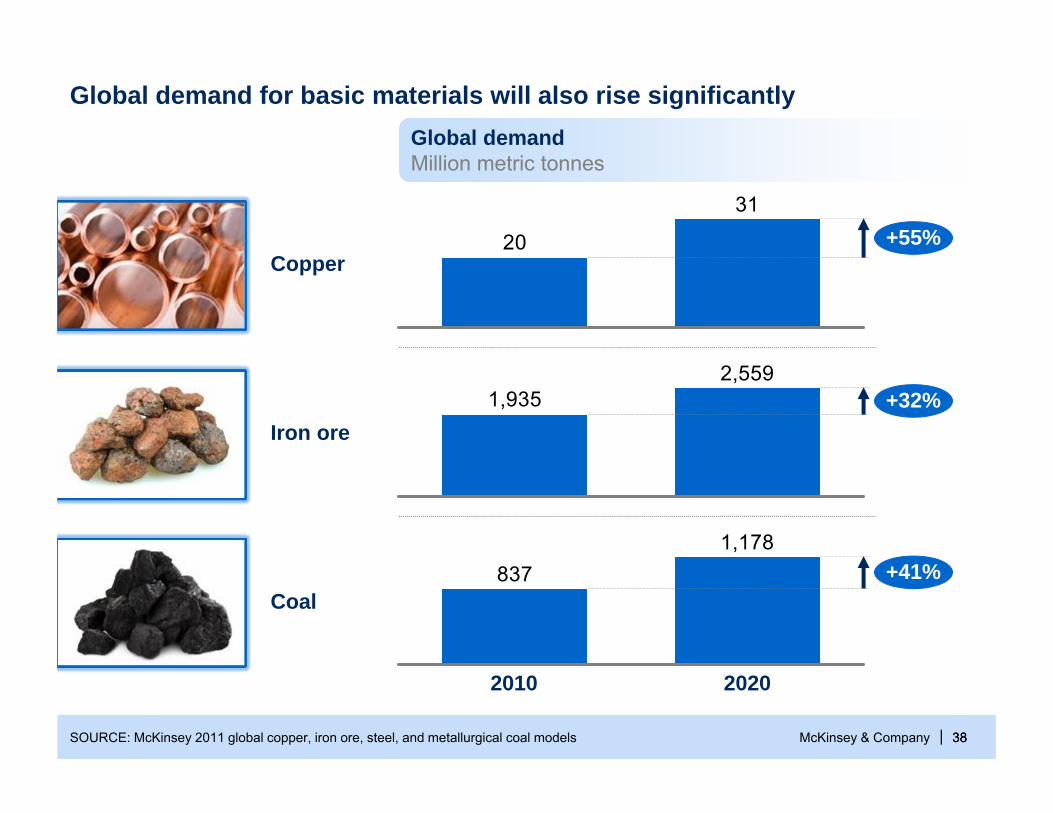

McKinsey & Company | 3838SOURCE: McKinsey 2011 global copper, iron ore, steel, and metallurgical coal models

31

20 +55%

2,5591,935 +32%

1,178837 +41%

Global demand for basic materials will also rise significantlyGlobal demandMillion metric tonnes

Coal

Iron ore

Copper

2010 2020

McKinsey & Company | 3939

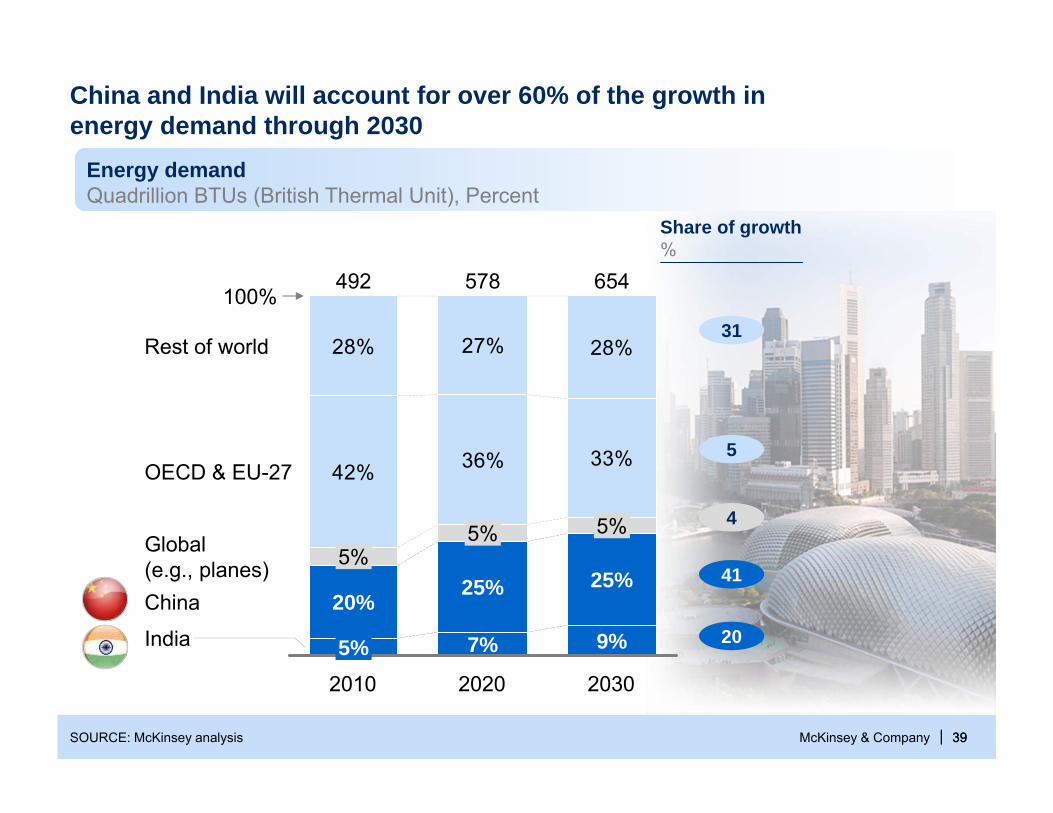

China and India will account for over 60% of the growth in energy demand through 2030

Energy demandQuadrillion BTUs (British Thermal Unit), Percent

41

20

5

31

Share of growth%

4

SOURCE: McKinsey analysis

42% 36% 33%

28% 27% 28%

2030

654

9%

100%

5%

2020

578

India

China

Global(e.g., planes)

OECD & EU-27

7%

25%

5%

2010

492

5%

20%

5%

Rest of world

25%

McKinsey & Company | 40

Overview

Five global trends

Opportunities in Asia

BC strengths and opportunities

1

2

3

Lessons from other cities and countries4

McKinsey & Company | 41

▪ Distinctive geographic positioning

▪ Competitive tax and regulatory environment – attracts businesses and enables them to thrive

▪ Strong education system – highly respected schools and educated workforce

▪ Natural tourist appeal – attracts over 4 MM visitors annually

▪ “Ready to work” with Asia – large immigrant population with relevant language skills and cultural awareness

▪ Abundant natural resources – e.g., shale gas and timber products to support the build-up of Asia

1

▪ Robust existing infrastructure – North America’s 5th busiest port and Canada’s 2nd busiest airport

3

4

2

5

6

7

BC is well positioned to capture these trends

McKinsey & Company | 42

BC has grown the share of its exports to Asia, however Australia demonstrates how much stronger these relationships can be

82%

44%43%40%36%32%

27%27%24%24%23%23%21%

10 1211

+7% p.a.

Australia0403022001 05 06 090807

Trade with AsiaPercent of total annual exports

British Columbia

McKinsey & Company | 43

BC is closer to Asia than any other Western economy

Travel time

Beijing, Asia’s busiest airportHours

14.2

13.7

13.0

11.6

11.1

10.8

New York

London

Los Angeles

Sydney

Vancouver

Prince Rupert

Shanghai, world’sbusiest portDays

34.0

33.9

25.4

23.5

24.1

23.4

McKinsey & Company | 44

Metro Vancouver Port is the 5th largest port in North America

Los Angeles, CA 7.9

Prince Rupert, BC

6.1

Vancouver, BC

5.5

Savannah, GA 2.9

New York/New Jersey

2.5

Long Beach, CA

0.4

1

2

3

4

5

26

Top ports in North America by container traffic, 2010Million TEUs (20-foot equivalent units)

SOURCE: American Association of Port Authorities

McKinsey & Company | 45

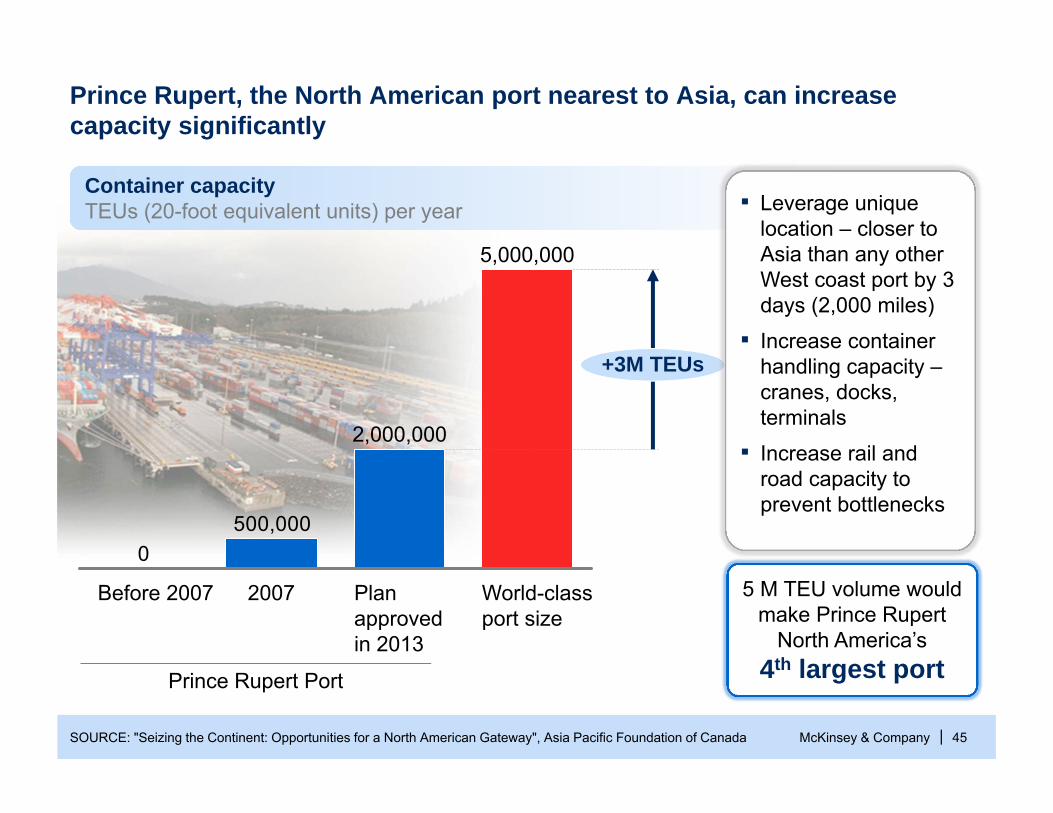

Prince Rupert, the North American port nearest to Asia, can increase capacity significantly

500,0000

Before 2007

+3M TEUs

5,000,000

World-class port size

Plan approved in 2013

2,000,000

2007

Prince Rupert Port

Container capacityTEUs (20-foot equivalent units) per year

SOURCE: "Seizing the Continent: Opportunities for a North American Gateway", Asia Pacific Foundation of Canada

▪ Leverage unique location – closer to Asia than any other West coast port by 3 days (2,000 miles)

▪ Increase container handling capacity –cranes, docks, terminals

▪ Increase rail and road capacity to prevent bottlenecks

5 M TEU volume would make Prince Rupert

North America’s4th largest port

McKinsey & Company | 46

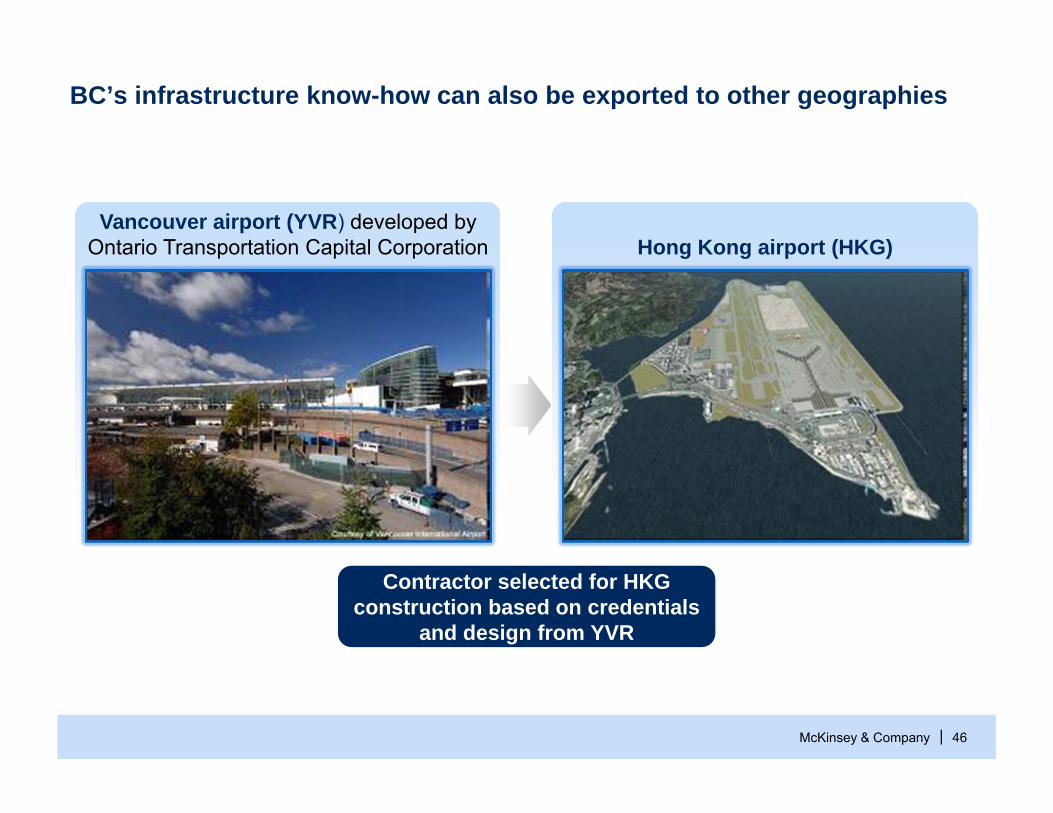

BC’s infrastructure know-how can also be exported to other geographies

Contractor selected for HKGconstruction based on credentials

and design from YVR

Vancouver airport (YVR) developed by Ontario Transportation Capital Corporation Hong Kong airport (HKG)

McKinsey & Company | 47

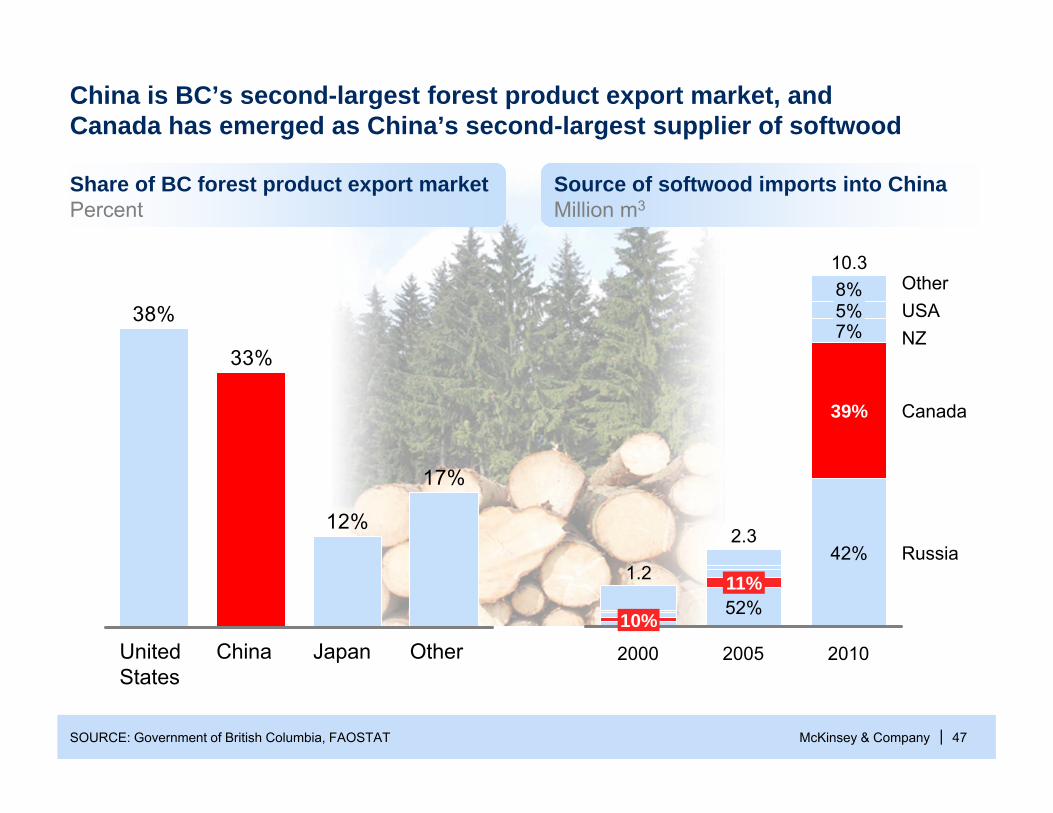

China is BC’s second-largest forest product export market, andCanada has emerged as China’s second-largest supplier of softwood

SOURCE: Government of British Columbia, FAOSTAT

17%

12%

33%

38%

OtherJapanChinaUnited States

Share of BC forest product export marketPercent

Russia

Canada

NZUSAOther

2010

10.3

42%

39%

7%5%8%

2005

2.3

52%11%

2000

1.2

10%

Source of softwood imports into ChinaMillion m3

McKinsey & Company | 48

Planned LNG export projects

Project name and sponsors

Initial liquefaction capacityMtpa1 Expected startup date

2020

2015

2014

2019

Several LNG projects have been proposed, but only 14% of proposed capacity is expected to come online within the next 5 years

1

5

12

12

14Prince RupertLNG

LNG Canada

Pacific Northwest LNG

BC LNG

Kitimat LNG

SOURCE: Company websites, Government of British Columbia

2021

Startup date >5 years

Startup within 3 years

38 Mtpa

6 Mtpa

1 Million tonnes per annum

McKinsey & Company | 49

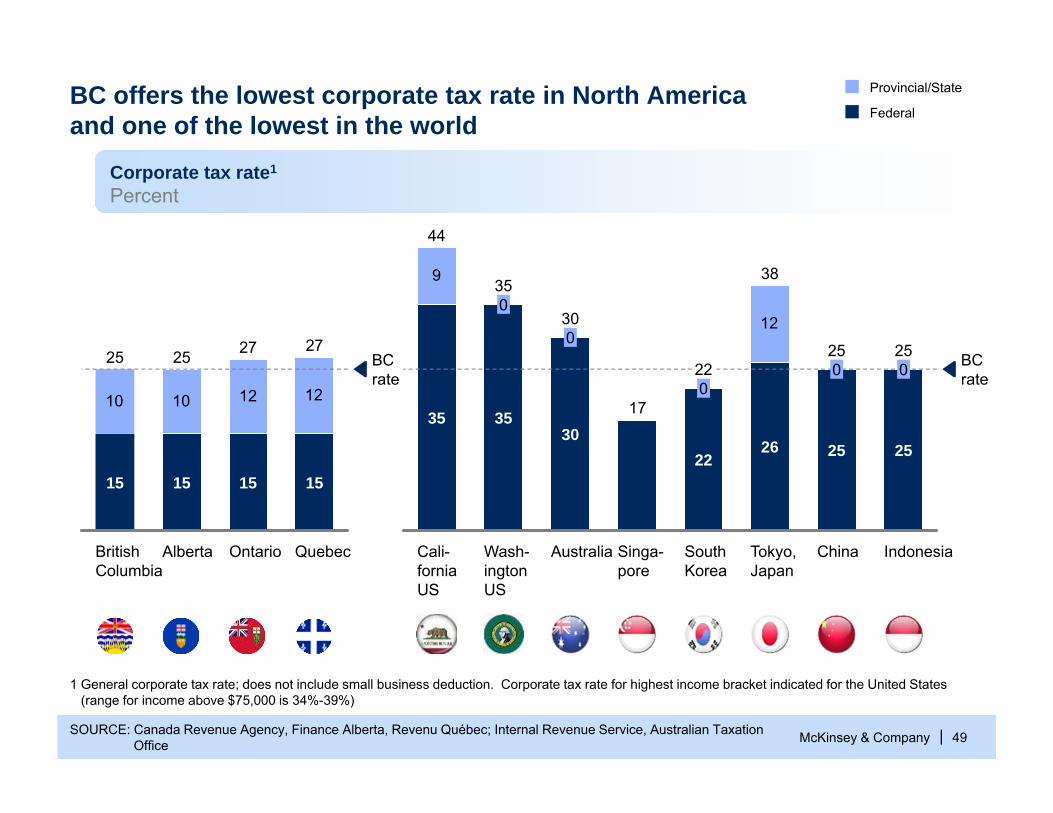

BC offers the lowest corporate tax rate in North Americaand one of the lowest in the world

SOURCE: Canada Revenue Agency, Finance Alberta, Revenu Québec; Internal Revenue Service, Australian Taxation Office

10 10 12 12

BCrate

Quebec

27

15

Ontario

27

15

Alberta

25

15

British Columbia

25

15

1 General corporate tax rate; does not include small business deduction. Corporate tax rate for highest income bracket indicated for the United States (range for income above $75,000 is 34%-39%)

Federal

Provincial/State

17

12

9

30

0

Wash-ingtonUS

35

35

0

Cali-forniaUS

44

35

BCrate

Indonesia

25

25

0

China

25

25

0

Tokyo, Japan

38

26

South Korea

22

22

0

Singa-pore

Australia

30

Corporate tax rate1

Percent

McKinsey & Company | 50

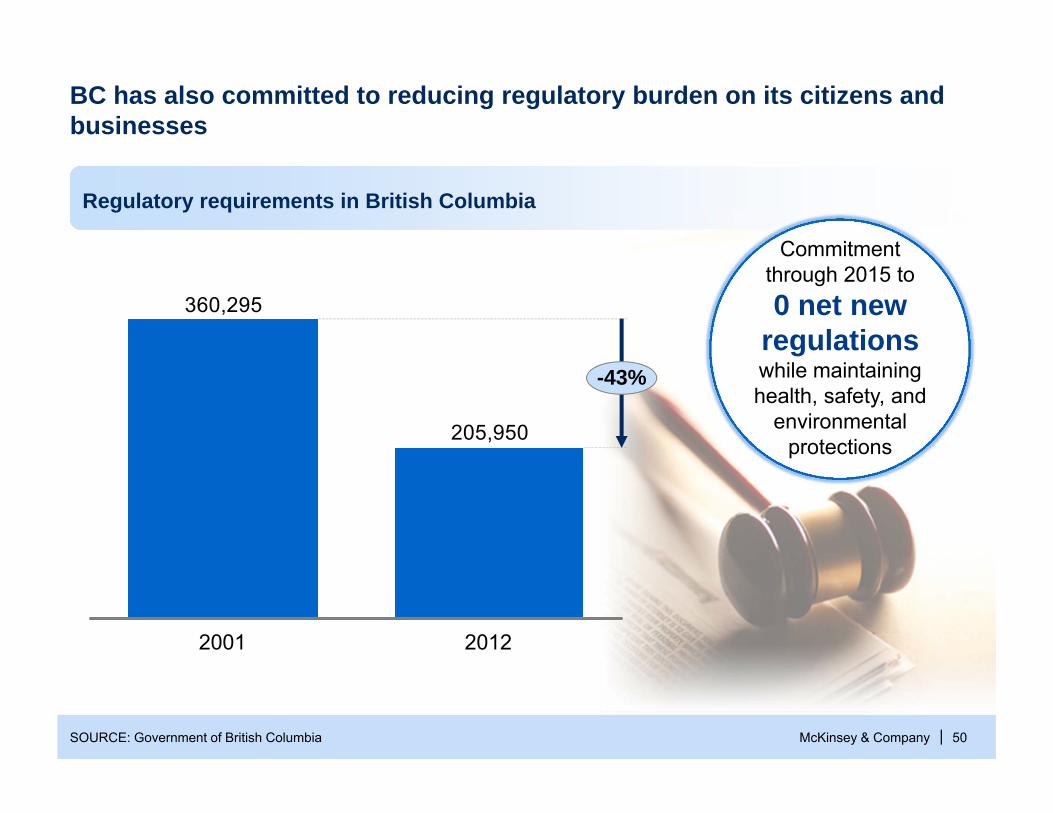

BC has also committed to reducing regulatory burden on its citizens and businesses

SOURCE: Government of British Columbia

205,950

360,295

-43%

2001 2012

Regulatory requirements in British Columbia

Commitmentthrough 2015 to0 net new

regulationswhile maintaining health, safety, and

environmental protections

McKinsey & Company | 51

BC has set an ambitious goal to attract 50% more international students by 2015

51SOURCE: Government of British Columbia

▪ Aims to attract students to meet BC’s future labour needs

▪ Maintains current mix of students –46% of students in language schools

12

31

18

17

65

42

58

28

43

11

12

34

13

13

103113

9438

126

141

15

52

2014-15

150

2013-14

50

2012-13

100

0

11.0%12.0%

9.7%10.0%

2015-162011-12

47

14 16

Private post-secondary

Language schools

K-12

Public post-secondaryBC international student populationThousands

McKinsey & Company | 52SOURCE: Kevin Rudd speaking at the Business Council of British Columbia

Across developing Asia there is a premium opportunity and demand for what these universities offer in terms of globally accredited and credible academic qualifications and [there is an opportunity] to build on … the networks of alumni that come through them intelligently, creatively,and for the future

- Kevin Rudd, former PM of Australia, April 2013

The Asian student opportunity has been widely recognised

Ranked 30th

in the world

McKinsey & Company | 53

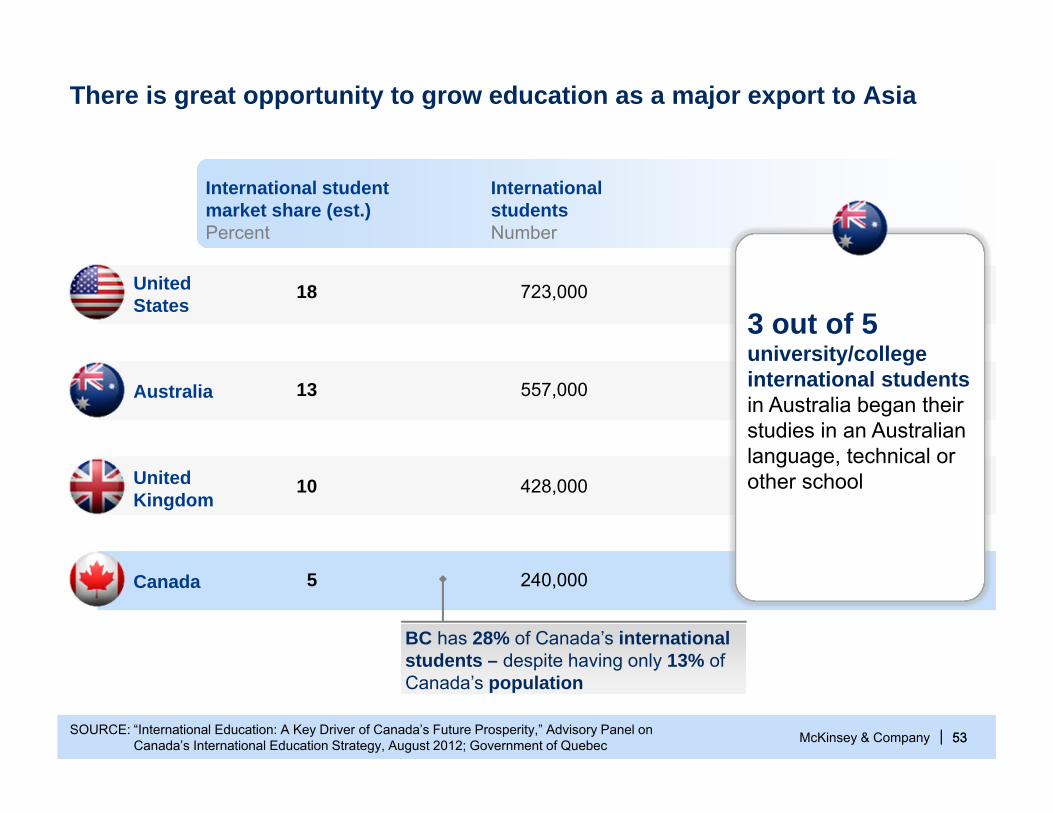

There is great opportunity to grow education as a major export to Asia

SOURCE: “International Education: A Key Driver of Canada’s Future Prosperity,” Advisory Panel onCanada’s International Education Strategy, August 2012; Government of Quebec 53

UnitedKingdom

UnitedStates

Canada

Australia

International student market share (est.)Percent

10

18

5

13

International studentsNumber

428,000

723,000

240,000

557,000

BC has 28% of Canada’s international students – despite having only 13% of Canada’s population

3 out of 5university/college international studentsin Australia began their studies in an Australian language, technical or other school

McKinsey & Company | 54

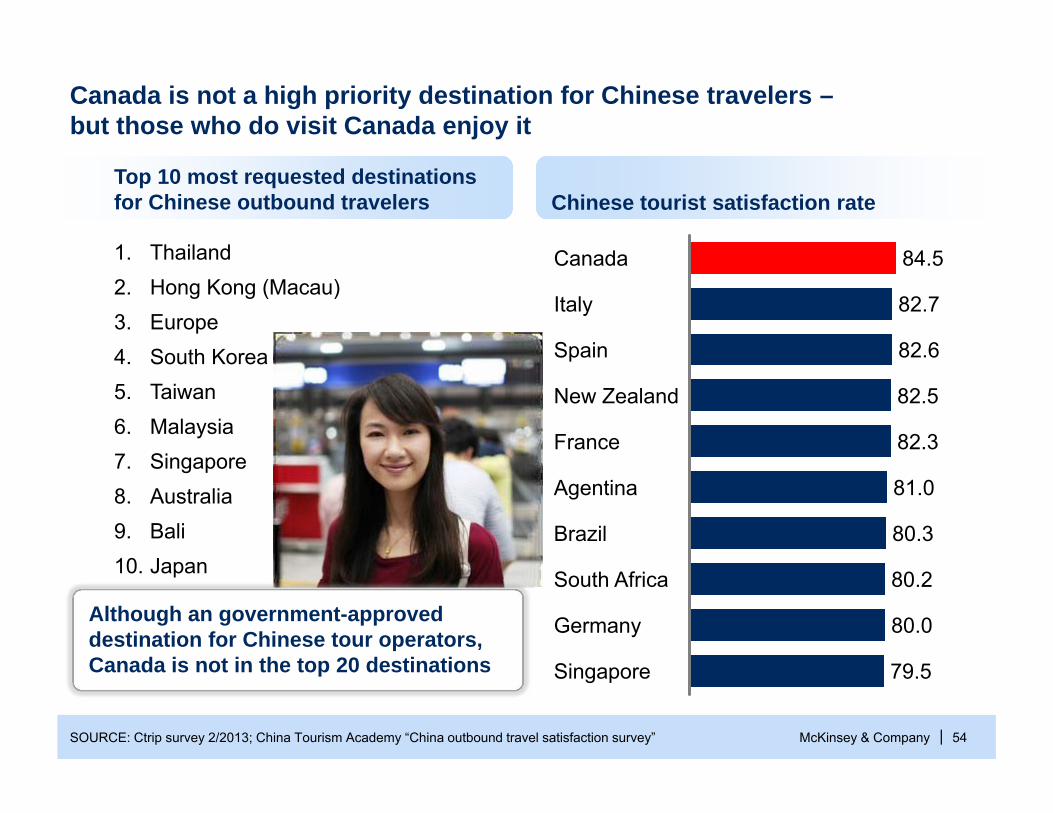

1. Thailand2. Hong Kong (Macau)3. Europe4. South Korea5. Taiwan6. Malaysia7. Singapore8. Australia9. Bali10. Japan

SOURCE: Ctrip survey 2/2013; China Tourism Academy “China outbound travel satisfaction survey”

Singapore 79.5

Germany 80.0

South Africa 80.2

Brazil 80.3

Agentina 81.0

France 82.3

New Zealand 82.5

Spain 82.6

Italy 82.7

Canada 84.5

Canada is not a high priority destination for Chinese travelers –but those who do visit Canada enjoy it

Chinese tourist satisfaction rateTop 10 most requested destinations for Chinese outbound travelers

Although an government-approved destination for Chinese tour operators, Canada is not in the top 20 destinations

McKinsey & Company | 55SOURCE: Kevin Rudd speaking at the Business Council of British Columbia

We’re going to have a 100 M Chinese tourists travelling the world in the next couple of decades. Where are they going to go? Countries where they are met and greeted in the language they are familiar with.

The assumption that English will be the global lingua franca at the end of this century is itself an arrogant assumption – English has only been the lingua franca since English speaking countries triumphed in WWII

- Kevin Rudd, former PM of Australia, April 2013

McKinsey & Company | 56

Three-quarters of new immigrants to British Columbia are from Asia

SOURCE: Citizenship and Immigration Canada

3

11

7Middle East/Africa

Europe

73Asia

6North America

South America

Country of origin for immigrants arriving in 2012, N = 36,164

McKinsey & Company | 57

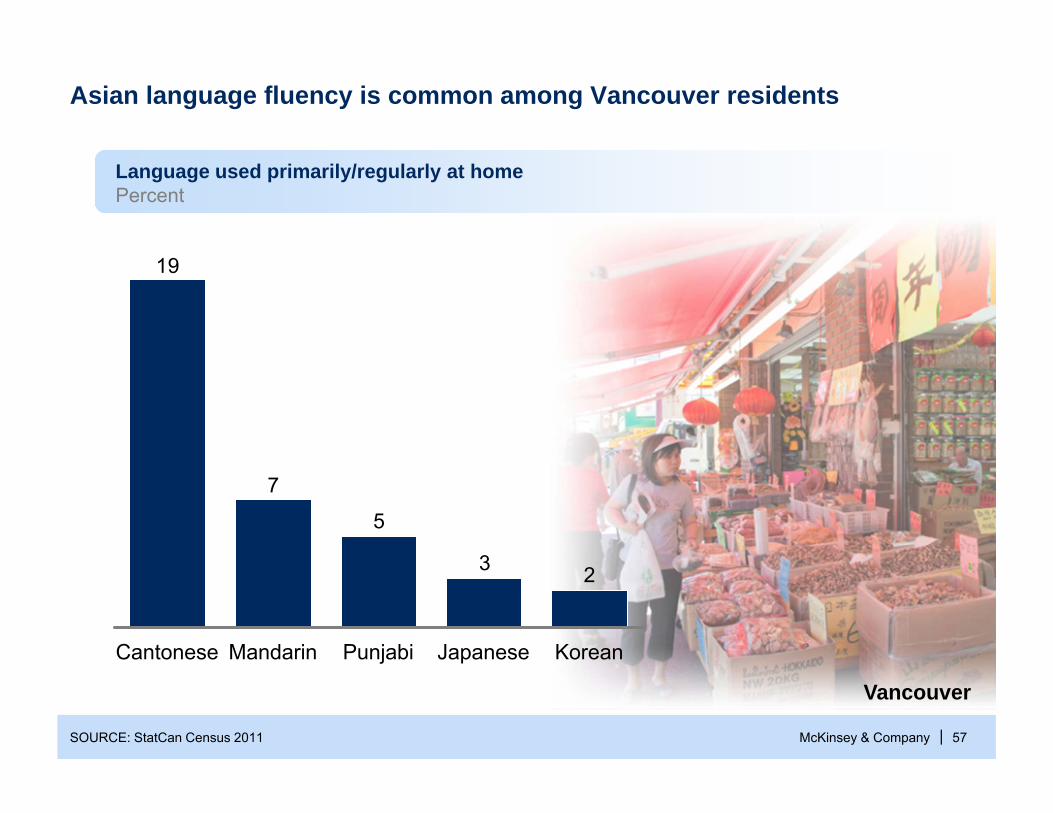

Asian language fluency is common among Vancouver residents

SOURCE: StatCan Census 2011

23

5

7

19

KoreanJapanesePunjabiMandarinCantonese

Language used primarily/regularly at homePercent

Vancouver

McKinsey & Company | 58

LNG – Accelerate development of export capacity to Asia (from 6 Mtpa to at least 18 Mtpa by 2018) before new US and Australian sources come online 22

Gateway economy – Increase share of Asian trade from 5% to 10+% of NA total with Prince Rupert expansion. Build up broader economy with regional HQs of Asian companies, Asia-focused professional services (e.g., law, accounting),and transport services

11

Natural resources (e.g., forestry, coal, copper) – Invest in critical areas to ensure BC at least maintains share as Asia grows, despite recovery in US exports33

Direct engagement – Create cabinet-level position on Asia to signal focus, establish business exchange programs, and convene a tri-sector task force on Asia77

Agrifood – Develop global champions in high-demand protein crops (e.g., beef, seafood, dairy) and processed food to establish BC as net food exporter. Emphasize brand – food safety, quality, and luxury items

44

Education – Establish as top 3 export industry (from 4% to 9% of total exports). Convert at least 60% of language and vocational students to university/college students

55

Tourism – Establish BC as top 3 Western destination for Chinese tourists(70% increase to 375k visits per year). Simplify visa requirement (i.e., faster, less costly, and less complex) for short stays from target markets

66

Seven priorities for BC to pursue

McKinsey & Company | 59

Overview

Five global trends

Opportunities in Asia

BC strengths and opportunities

1

2

3

Lessons from other cities and countries4

McKinsey & Company | 60

▪ Set an explicit and ambitious growth target (e.g., additional 2-3% of GDP growth)

▪ Determine how growth target will be reached at a granular level (i.e., which cities, which industries will deliver and how much)

▪ Establish formal government roles (e.g., cabinet-level ministry) and groups (e.g., Premier’s Delivery Unit) to ensured increased focus on Asia and capture of opportunities

▪ Create joint government-business organizations to enable collaborative pursuit of opportunities (e.g., Malaysia economic transformation labs , Singapore Economic Development Board)

▪ Establish both a physical (e.g., NZ in Shanghai) and virtual presence (e.g., tourism website in Mandarin)

▪ Be willing to make significant, protected investments and invest for the long term (i.e., pay off may take 5+ years)

▪ Leverage both existing and potential diaspora (i.e., both Asians in Canada and Canadians in Asia) as unofficial ambassadors (e.g., Committee of 100, Mexico Talent Abroad)

▪ Engage stakeholders early (i.e., at the planning stage, not only at the approval stage) and allow transparency into objectives and risks

1

2

3

4

5

6

8

Lessons from around the world

7

McKinsey & Company | 61

Examples of where we have helped to drive economic development

Tanzania

Turkey

UK

Georgia

MalaysiaNigeria

Dubai

Brazil

USA

GermanyUkraine

Morocco

EthiopiaColumbia

McKinsey & Company | 62

▪ Be in the top 3 most competitive countries in Latin America

▪ Cultivate a business environment that attracts local and foreign investment (30% of GDP)

▪ Raise the proportion of high value-added goods and services to 60% of exports (19% in 2006)

▪ Quadruple GDP per capita, from $5,000 to $18,000 –become a mid-high income country

▪ Substantially improve quality of life and decrease poverty level to <15% (45% in 2006)

Colombia set an ambitious set of goals to improve its attractiveness to foreign businesses and consumers

Productivity Transformation Program

McKinsey & Company | 63

Leverage creative methods to co-create solutionswith private and public sector

SOURCE: GTP, ETP

Malaysia Economic Transformation Programme

Intensive capability building

Co-creation with the private sector

Private sectorparticipants

Public sectorparticipants150

350 New Jobs3.3 M

15,OOO

92%

▪ 131 entry point projects with detailed plans and modeling

▪ Clear targets and milestonesoutlined

Increased GDP per capita

Private sector funding (>RM1 trillion)

USD / Capita

8 week intense lab environment

Delivery unit to monitor programme

McKinsey & Company | 64

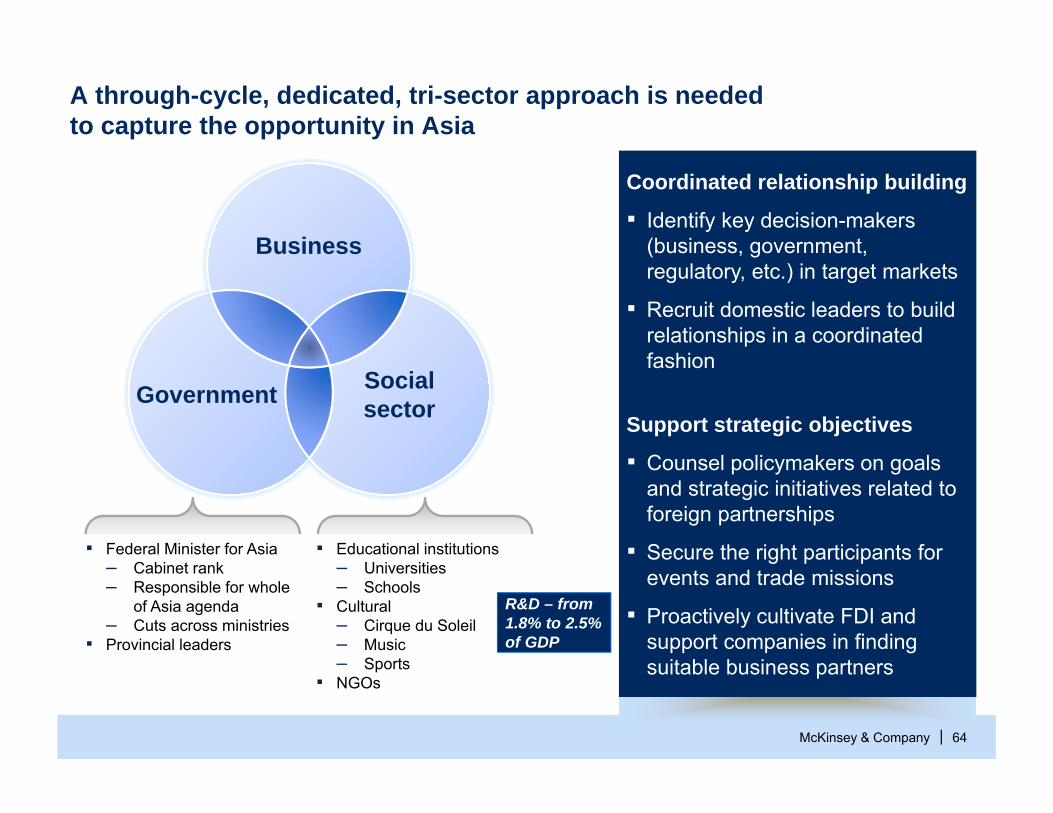

A through-cycle, dedicated, tri-sector approach is neededto capture the opportunity in Asia

Coordinated relationship building

▪ Identify key decision-makers (business, government, regulatory, etc.) in target markets

▪ Recruit domestic leaders to build relationships in a coordinated fashion

Support strategic objectives

▪ Counsel policymakers on goals and strategic initiatives related to foreign partnerships

▪ Secure the right participants for events and trade missions

▪ Proactively cultivate FDI and support companies in finding suitable business partners

▪ Federal Minister for Asia– Cabinet rank– Responsible for whole

of Asia agenda– Cuts across ministries

▪ Provincial leaders

▪ Educational institutions– Universities– Schools

▪ Cultural– Cirque du Soleil– Music– Sports

▪ NGOs

R&D – from 1.8% to 2.5% of GDP

Business

Government Socialsector

McKinsey & Company | 6565

Many countries are developing one-stop government centres

Provides venue and business services for trade events held by NZ businesses

New Zealand Central in Shanghai

▪ Consolidates multiple NZ government bodies in one location

▪ Centre set-up embodies “look and feel” of NZ

McKinsey & Company | 66

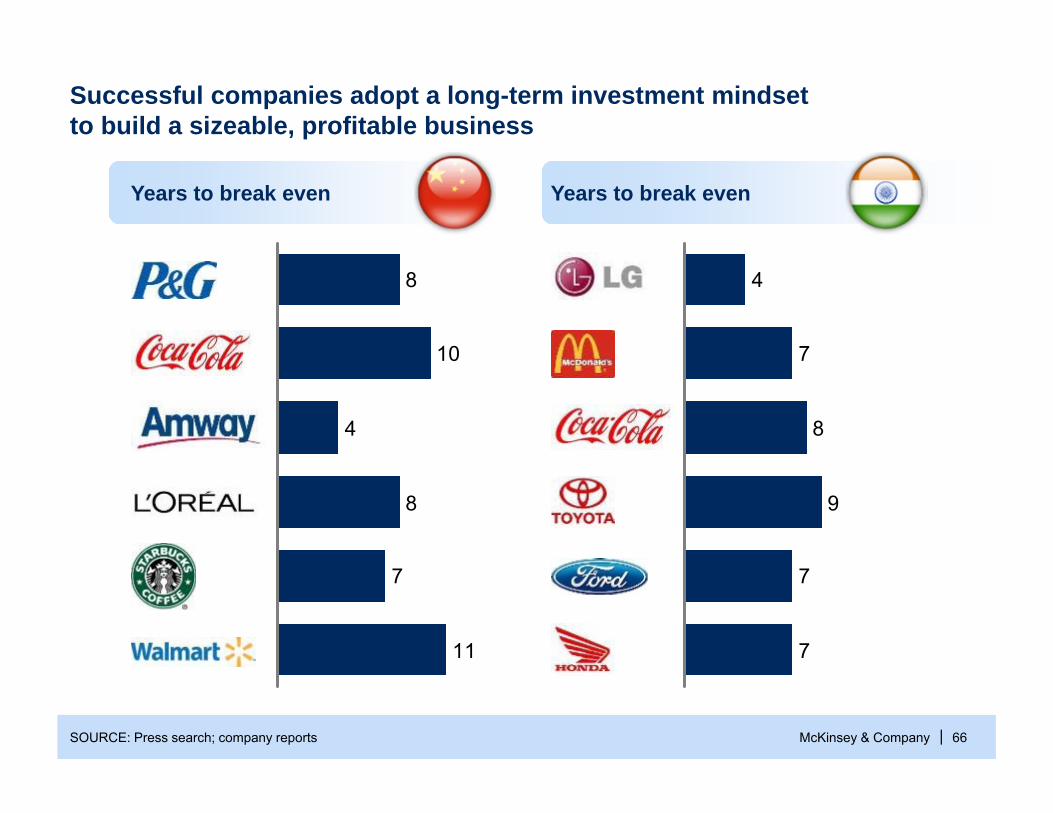

Years to break even Years to break even

11

7

8

4

10

8

Successful companies adopt a long-term investment mindsetto build a sizeable, profitable business

SOURCE: Press search; company reports

7

7

9

8

7

4

McKinsey & Company | 67

New Zealand proactively cultivates long-term government and business relationships in China

SOURCE: New Zealand Ministry of Foreign Affairs, Press Search

PM John Key during visit to ChinaApril 2013

▪ Attended by New Zealand’s Prime Minister John Key and 50 top New Zealand business leaders

New Zealand-China PartnershipForum

“The visit is an opportunity to support New Zealand companies in China through business support activities and major tourism and education promotional events being held in the three Chinese cities the delegation will visit – Guangzhou, Shanghai and Beijing”

New Zealand has "a clear message for China: your investment is welcome”

“It was great to meet with President Xi again and reaffirm the strong relationship between our two countries”

McKinsey & Company | 68SOURCE: Literature search; press releases

Domestically, Australia is pursuing a number of initiatives to strengthen its ties with Asia

New direct currency trading agreement between AUD and RMBlowers cost and speeds up transactions – only 3 countries have direct currency trading with China (US, Brazil, Australia)

Expanded curricula coverage of Asia to build next generation of ties with Asia (e.g., cross-subject curriculum to build cultural understanding, including offering Asian languages in course offerings, exchanges)

Government offers training programs for individuals doing trade in China – covers processes involved in doing business in China and how to mitigate risk

Strengthening of military ties through bilateral defense links between the Australian Defense Force and the People’s Liberation Army to build trust, confidence and transparency for the future

McKinsey & Company | 69

Leverage the two-way diaspora

SOURCE: World Bank, Statscan, World wide webs: diasporas and the international system Lowy Institute

Mexico’s Network of Talent Abroad convenes high-skilled Mexicans abroad in a target set of cities

▪ Promote country’s image abroad

▪ Improve access to foreign capital, information and contacts for those back in Mexico

▪ Irish president Mary Robinson identified ‘important’ members of the Irish diaspora, proactively reached out to them with a request for activities they could do on behalf of Ireland

▪ Create organizations (e.g., Committee of 100) that engages members of diaspora in the receiving country in building relationships with their home country

Treat migrants as well-placed, unofficial ambassadors

Ask leaving citizens to remain connected

Examples from other countries

Looking toward the futureBusiness Council of British ColumbiaDominic Barton, Global Managing DirectorMcKinsey & CompanyMay 28, 2013