capital market expectations 01/12/09. 2 capital market expectations questions to be answered: what...

Post on 22-Dec-2015

216 views

TRANSCRIPT

Capital Market Expectations

01/12/09

2

Capital Market Expectations

Questions to be answered:• What are capital market expectations (CME)?• How does CMEs fit into to the bigger portfolio

management picture?• What is an appropriate framework for

developing CME?• What are some key issues that analysts face

or must recognize while developing CME?• What are some common tools for formulating

CME?

3

Capital Market Expectations

• Capital Market Expectations (CME) represent the investor’s expectations concerning the risk and return prospects of asset classes.

• These are different from micro expectations, which are expectations concerning individual assets.

4

CME within the larger picture

• Developing CME allow portfolio managers to:• Develop return and risk expectations for broad

asset classes.• Ensure that return and risk objectives are

consistent with investor expectations.• Construct efficient portfolios• Develop a basis for the first step in the top-down

approach of constructing portfolios• Broad asset class analyses, industry analyses, individual

security analyses

5

Framework for Developing CME

• Specify the final set of expectations that are needed, including time horizon.

• Research the historical record.

6

Framework for Developing CME

• Specify the methods that will be used to formulate CME and the information required.

• Determine the best sources for information needed.

7

Framework for Developing CME

• Interpret the current investment environment using the selected data and methods.

• Provide the set of expectations required.

• Monitor actual outcomes to provide feedback to improve the CME development process.

8

Framework for Developing CME

• Good forecasts should generally be:• Unbiased, objective and well researched• Efficient (minimizing forecast errors)• Internally consistent

9

Challenges in Forecasting

• Limitations of economic data – lagged, revised, changes in definitions and calculation methods.

• Data measurement errors and biases – transcription errors, survivorship bias, appraisal (smoothed) data.

10

Challenges in Forecasting

• Limitations of historical estimates• Risk/return relationships can be changed if

there is a change in regime.

• Using historical estimates (without correcting for changing regimes) assumes stationarity, i.e., the statistical properties of the forecasted variables remain the same.

11

Challenges in Forecasting

• Limitations of historical estimates• Data-mining bias. Does the variable have

economic rationale?

• Time-period bias.

12

Challenges in Forecasting

• Psychological traps• Anchoring trap – tendency to give

disproportionate weight to the first information received

• Status quo trap – tendency for forecasts to perpetuate recent observations

13

Challenges in Forecasting

• Psychological traps• Confirming evidence trap – bias that leads

individuals to give greater weight to information that supports a preferred point of view

• Overconfidence trap – tendency to overestimate the accuracy of forecasts

14

Challenges in Forecasting

• Psychological traps• Prudence trap – tendency to temper

forecasts so that they do not appear extreme.

• Recallability trap – tendency of forecasts to be overly influenced by events that have left a strong impression.

15

Tools for Formulating CME

• Historical Statistical Approach• Historical statistical characteristics (mean,

variance, correlation) can be used to estimate future returns.

• Shrinkage Estimators• This involves taking a weighted average of

a historical estimate of a parameter and some other parameter estimate (from, for example, CAPM).

16

Tools for Formulating CME

• Financial Market Equilibrium Models• These models describe relationships between

return and risk in which returns are correctly estimated if the equilibrium model is correct and investments are properly priced based on their risk levels.

• The CAPM is one example of such a model.

• Limitations of the CAPM as we know it:• It is difficult to define an appropriate market • Other variables appear to explain returns• The model assumes that markets are perfectly integrated

17

Tools for Formulating CME

• Financial Market Equilibrium Models• ICAPM – International Capital Asset Pricing Model

(Singer and Terhaar, 1997)

• The basic model is the same:

Where

FMiFi RRERRE )()(

)(/),( MMii RVarRRCov

18

Tools for Formulating CME

• Financial Market Equilibrium Models• ICAPM

• An appropriate proxy for the world market portfolio is the global investable market (GIM). This market should include traditional and alternative asset classes.

• We can rearrange the ICAPM equation to the following equation:

where the term in the brackets (GIM Sharpe Ratio) represents the expected risk premium per unit of standard deviation for the GIM.

M

FMMiiFi

RRERRE

)(

)( ,

19

Tools for Formulating CME

• Financial Market Equilibrium Models• ICAPM

• Based on research, a good estimate of this GIM Sharpe ratio is 0.28.

• The ICAPM has the ability to incorporate market imperfections. We consider market segmentation.

• Market segmentation means that there are impediments to capital market movements.

• The more the market is segmented, the more it is dominated by local investors

• With segmented markets, two identical assets (with the same risk characteristics) can have different expected returns.

20

Tools for Formulating CME

• Financial Market Equilibrium Models• ICAPM

• Calculating expected return with market segmentation:• Assume that the market is completely segmented. Then

the risk premium of that market is:

• With the degree of integration of that market, we can estimate the final risk premium:

M

FMiFi

RRERRE

)(

)(

premium)risk segmented*n)integratio of degree1(( )integratedfully if premiumrisk asset *n integratio of deg()( Fi RRE

21

Tools for Formulating CME

• Financial Market Equilibrium Models• ICAPM

• Degree of integration:• Developed equity and bond markets: 80%• US real estate: 70%• Emerging market equities and bonds: 65%

22

Tools for Formulating CME

• Multifactor models • Multifactor models explain the returns to an asset

in terms of a set of factors and are based on the Arbitrage Pricing Theory (APT).

F1t is the period t return to the first designated risk factor and Rit

can be measured as either a nominal or excess return to security i.

itKtiKtitiiit eFbFbFbaR ...2211

23

Tools for Formulating CME

• Multifactor models • To determine a specific asset return and risk

characteristics, we use the factor covariance matrix (which contains the covariances for the factors that drive the return) and factor sensitivities (or betas) for the asset.

24

Tools for Formulating CME

ttt FbFbR 2121111

)()()()() , ( 2,11221222111 FFCovbbbbFVarbbFVarbbasset jiassetCov jijijiji

• Multifactor models• So, for a two-factor model, two-asset model (M),

for example,

and the asset variances and covariances are calculated as:

)(2)()() ( 2,1212221

21 FFCovbbFVarbFVarbiAssetVar iiii

25

Tools for Formulating CME

• Multifactor models• These models can be used to develop expectations

about broader asset classes or to develop expectations about individual securities.

• The following two models are the three-factor and four-factor models used for individual securities.

• They can also be used to determine the style of a particular stock, mutual fund or ETF.

26

Tools for Formulating CME

• Multifactor models• Fama and French three-factor model:

tititmtiitit HMLbSMBbRFRRbaRFRR 321 )()(

where SMB (i.e. small minus big) is the return to a portfolio of small capitalization stocks less the return to a portfolio of large capitalization stocks

HML (i.e. high minus low) is the return to a portfolio of stocks with high ratios of book-to-market values less the return to a portfolio of low book-to-market value stocks

27

Tools for Formulating CME

• Multifactor models• Carhart (1997) extends the Fama-French three

factor model by including a fourth common risk factor that accounts for the tendency for firms with positive past return to produce positive future return. This is referred to as the momentum factor.

where PR1YR is the average return to a set of stocks with the best performance over a year minus that of the of a set of stocks with the worst performance.

YRPRbHMLbSMBbRFRRbaRFRR itititmtiitit 1)()( 4321

28

Tools for Formulating CME

• Multifactor models• Estimating Expected Returns for Individual Stocks

• A Specific set of K common risk factors must be identified

• The risk premia for the factors must be estimated• Sensitivities (or betas) of the ith stock to each of those K

factors must be estimated• The expected returns can be calculated by combining

the results of the previous steps in the appropriate way

29

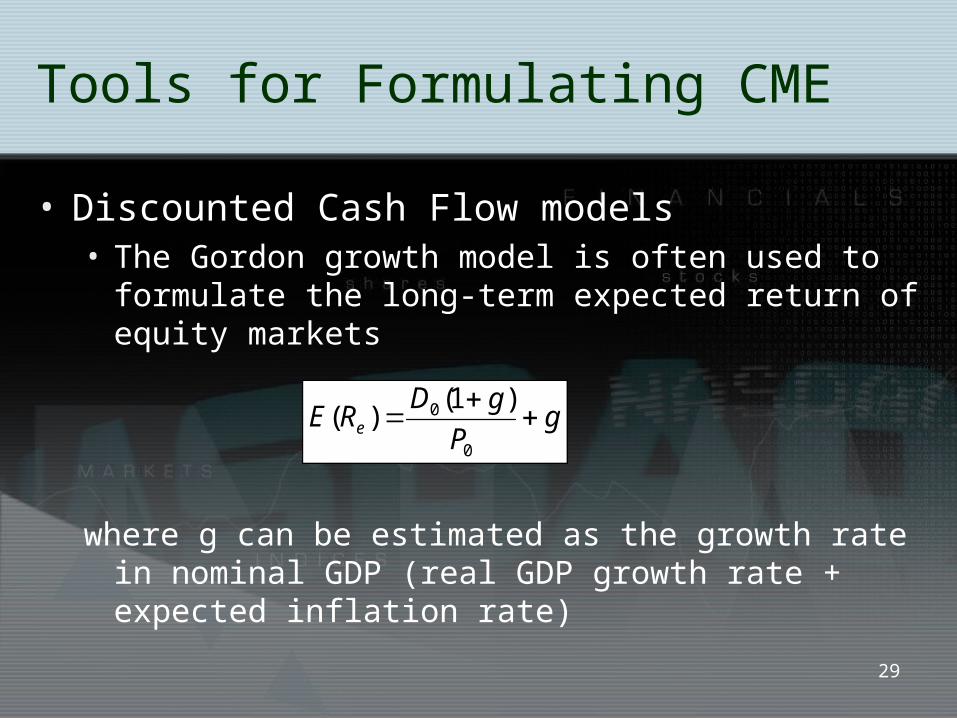

Tools for Formulating CME

• Discounted Cash Flow models• The Gordon growth model is often used to

formulate the long-term expected return of equity markets

where g can be estimated as the growth rate in nominal GDP (real GDP growth rate + expected inflation rate)

gP

gDRE e

0

0 )1()(

30

Tools for Formulating CME

• Risk Premium Approach• The risk premium approach expresses the

expected return on a risky asset as the risk-free rate plus risk premiums to compensate investors for the sources of risk for that asset.

31

Tools for Formulating CME

• Risk Premium Approach• For Fixed-income:

premiumtax

premiummaturity premiumy illiquidit premiumrisk default

premiuminflation rateinterest freerisk real)(

bRE

32

Tools for Formulating CME

• Risk Premium Approach• Inflation premium reflects the average inflation

rate expected over maturity of debt• Illiquidity premium represents the risk of loss

relative to an investment value if it needs to be converted to cash quickly

• Tax premium may be applicable to certain classes of stocks.

33

Tools for Formulating CME

• Risk Premium Approach• For equity, we can use a historical risk premium

estimate to proxy for the equity risk premium:

premiumrisk equity rate bond-Tyr 30)( eRE

34

Tools for Formulating CME

• Survey Method• The survey method involves asking a group of

experts for their CMEs.

• The Livingston Survey (managed by the Fed of Philadelphia) provides expectations on macro-economic variables

35

Readings

• RB 8 (pgs. 239 – 246 – review of CAPM)• RB 9 (pgs. 279 – 291), • RM 2 (up to section 4, we do not cover

the Grinold-Kroner model or Time Series Estimators)