canada-united states law institute private financing of entrepreneurships: sources of private...

TRANSCRIPT

CANADA-UNITED STATES LAW INSTITUTE

Private Financing of Entrepreneurships:

Sources of Private Financing

2

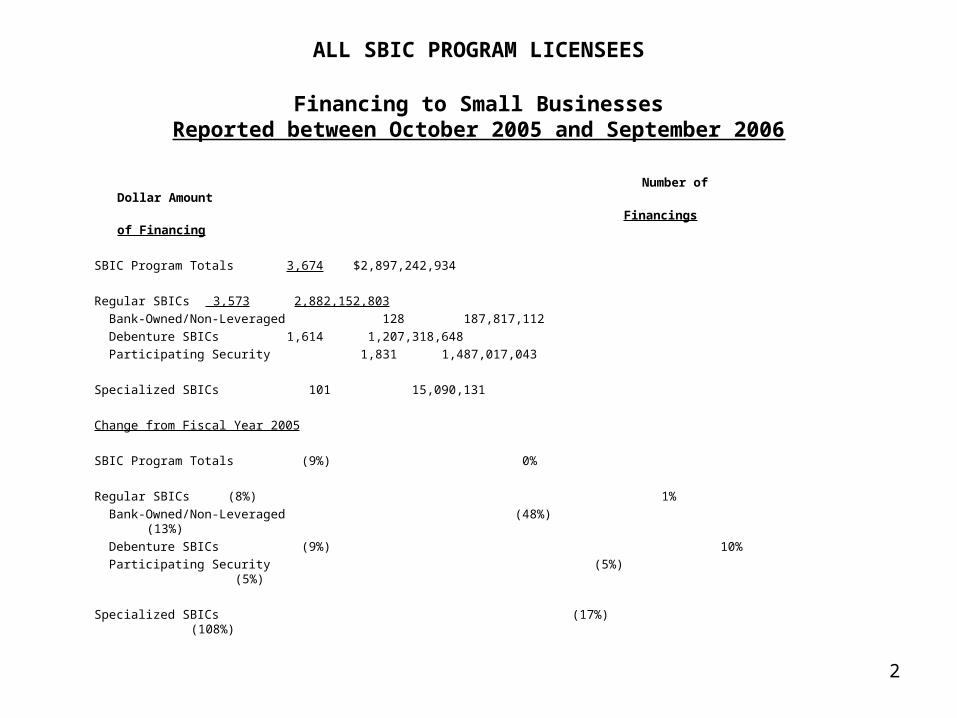

ALL SBIC PROGRAM LICENSEES

Financing to Small BusinessesReported between October 2005 and September 2006

Number of Dollar Amount

Financings of Financing

SBIC Program Totals 3,674 $2,897,242,934

Regular SBICs 3,573 2,882,152,803

Bank-Owned/Non-Leveraged 128 187,817,112

Debenture SBICs 1,614 1,207,318,648

Participating Security 1,831 1,487,017,043

Specialized SBICs 101 15,090,131

Change from Fiscal Year 2005

SBIC Program Totals (9%) 0%

Regular SBICs (8%) 1%

Bank-Owned/Non-Leveraged (48%) (13%)

Debenture SBICs (9%) 10%

Participating Security (5%) (5%)

Specialized SBICs (17%) (108%)

3

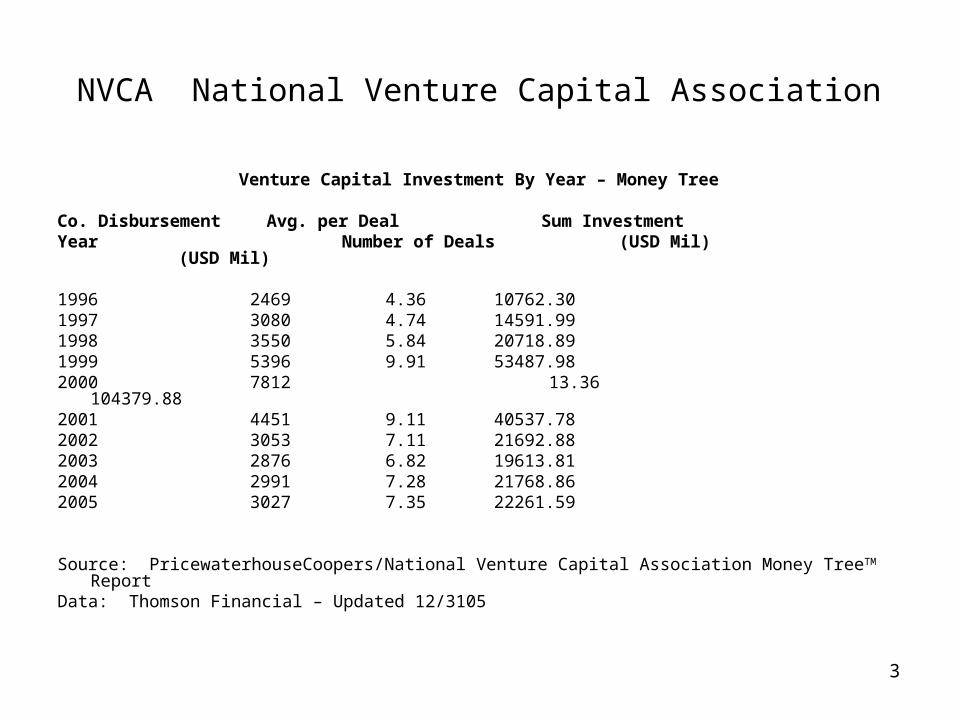

NVCA National Venture Capital Association

Venture Capital Investment By Year – Money Tree

Co. Disbursement Avg. per Deal Sum InvestmentYear Number of Deals (USD Mil) (USD Mil)

1996 2469 4.36 10762.301997 3080 4.74 14591.991998 3550 5.84 20718.891999 5396 9.91 53487.982000 7812 13.36 104379.882001 4451 9.11 40537.782002 3053 7.11 21692.882003 2876 6.82 19613.812004 2991 7.28 21768.862005 3027 7.35 22261.59

Source: PricewaterhouseCoopers/National Venture Capital Association Money TreeTM ReportData: Thomson Financial – Updated 12/3105

4

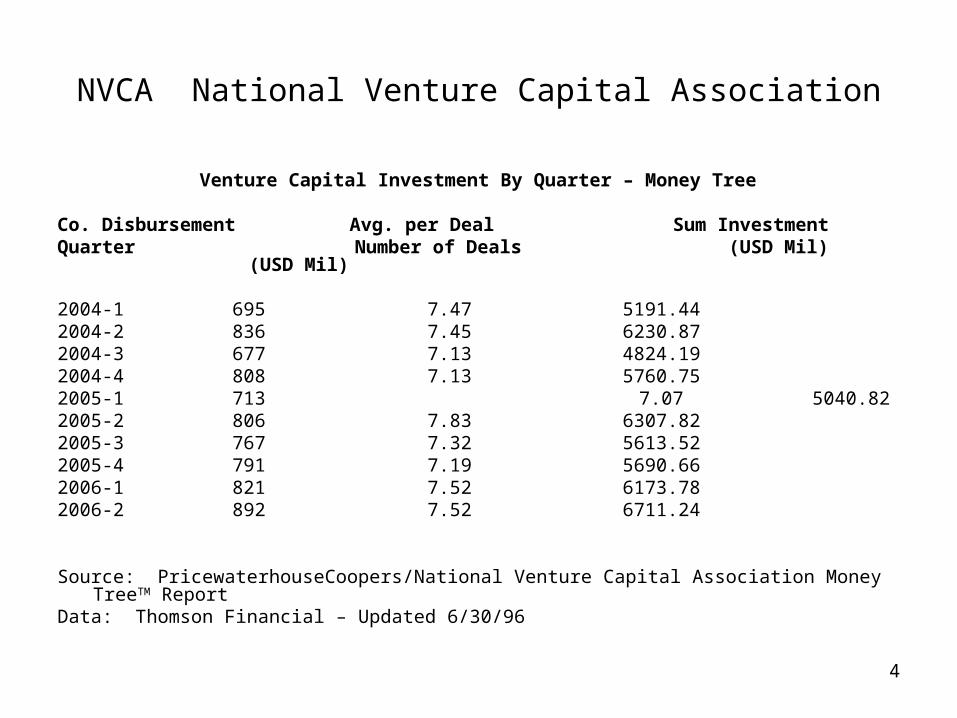

NVCA National Venture Capital Association

Venture Capital Investment By Quarter – Money Tree

Co. Disbursement Avg. per Deal Sum Investment

Quarter Number of Deals (USD Mil) (USD Mil)

2004-1 695 7.47 5191.442004-2 836 7.45 6230.872004-3 677 7.13 4824.192004-4 808 7.13 5760.752005-1 713 7.07 5040.822005-2 806 7.83 6307.822005-3 767 7.32 5613.522005-4 791 7.19 5690.662006-1 821 7.52 6173.782006-2 892 7.52 6711.24

Source: PricewaterhouseCoopers/National Venture Capital Association Money TreeTM ReportData: Thomson Financial – Updated 6/30/96

5

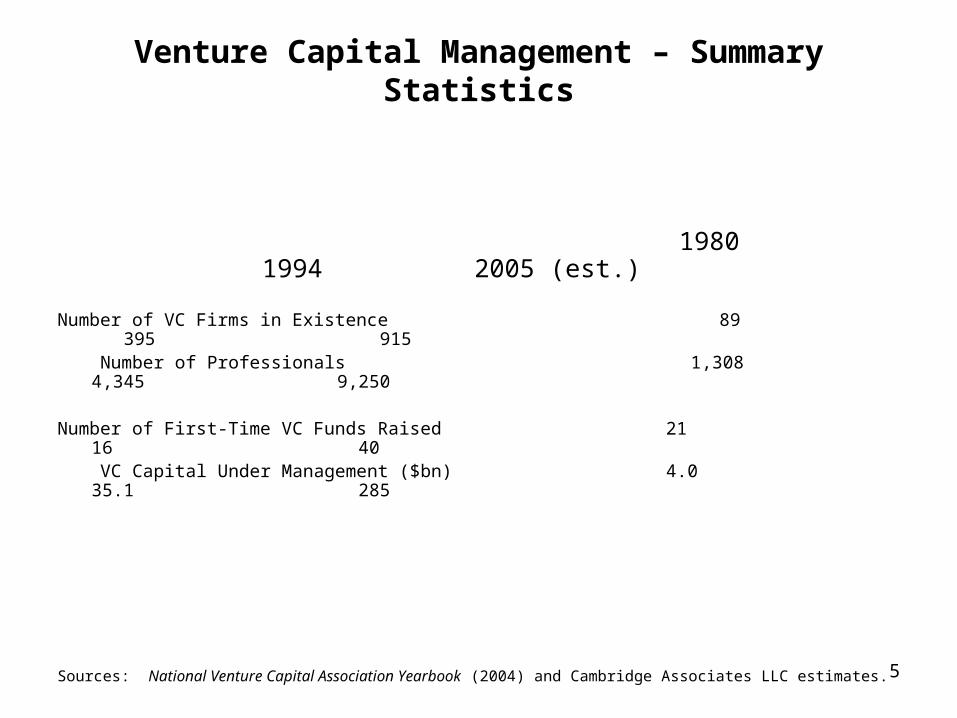

Venture Capital Management – Summary Statistics

1980 1994 2005 (est.)

Number of VC Firms in Existence 89 395 915 Number of Professionals 1,308 4,345 9,250

Number of First-Time VC Funds Raised 21 16 40 VC Capital Under Management ($bn) 4.0 35.1 285

Sources: National Venture Capital Association Yearbook (2004) and Cambridge Associates LLC estimates.

6

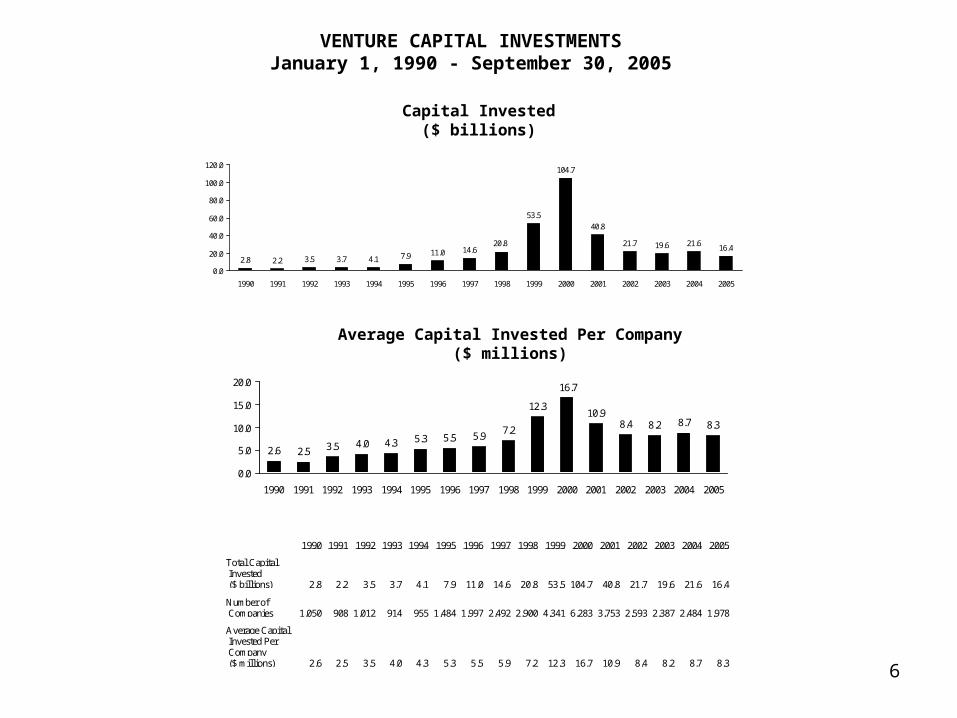

VENTURE CAPITAL INVESTMENTSJanuary 1, 1990 - September 30, 2005

Capital Invested($ billions)

2.8 2.2 3.5 3.7 4.1 7.9 11.0 14.6

53.5

104.7

40.8

21.619.620.816.4

21.7

0.0

20.0

40.0

60.0

80.0

100.0

120.0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

2.6 2.5 3.5 4.0 4.3 5.3 5.5 5.97.2

12.310.9

8.4 8.2 8.7 8.3

16.7

0.0

5.0

10.0

15.0

20.0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Total Capital Invested ($ billions) 2.8 2.2 3.5 3.7 4.1 7.9 11.0 14.6 20.8 53.5 104.7 40.8 21.7 19.6 21.6 16.4

Number of Companies 1,050 908 1,012 914 955 1,484 1,997 2,492 2,900 4,341 6,283 3,753 2,593 2,387 2,484 1,978

Average Capital Invested Per Company ($ millions) 2.6 2.5 3.5 4.0 4.3 5.3 5.5 5.9 7.2 12.3 16.7 10.9 8.4 8.2 8.7 8.3

Sources: MoneyTree Survey, National Venture Capital Association, PricewaterhouseCoopers, and Thomson Venture Economics.

Note: Disbursement data include funds received from corporate co-investment.

Average Capital Invested Per Company($ millions)

7

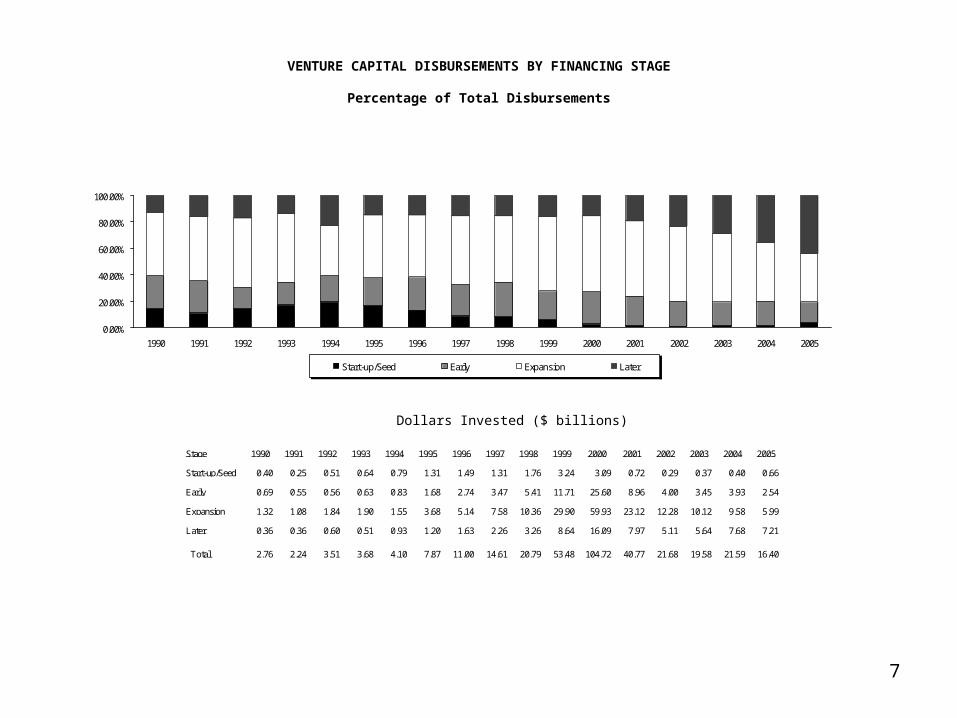

VENTURE CAPITAL DISBURSEMENTS BY FINANCING STAGE

Percentage of Total Disbursements

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Start-up/Seed Early Expansion Later

Dollars Invested ($ billions)

Stage 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Start-up/Seed 0.40 0.25 0.51 0.64 0.79 1.31 1.49 1.31 1.76 3.24 3.09 0.72 0.29 0.37 0.40 0.66

Early 0.69 0.55 0.56 0.63 0.83 1.68 2.74 3.47 5.41 11.71 25.60 8.96 4.00 3.45 3.93 2.54

Expansion 1.32 1.08 1.84 1.90 1.55 3.68 5.14 7.58 10.36 29.90 59.93 23.12 12.28 10.12 9.58 5.99

Later 0.36 0.36 0.60 0.51 0.93 1.20 1.63 2.26 3.26 8.64 16.09 7.97 5.11 5.64 7.68 7.21

Total 2.76 2.24 3.51 3.68 4.10 7.87 11.00 14.61 20.79 53.48 104.72 40.77 21.68 19.58 21.59 16.40

Sources: MoneyTree Survey, National Venture Capital Association, PricewaterhouseCoopers, and Thomson Venture Economics.

Notes: Figures may not total due to rounding. Data for 2005 are through September 30.

8

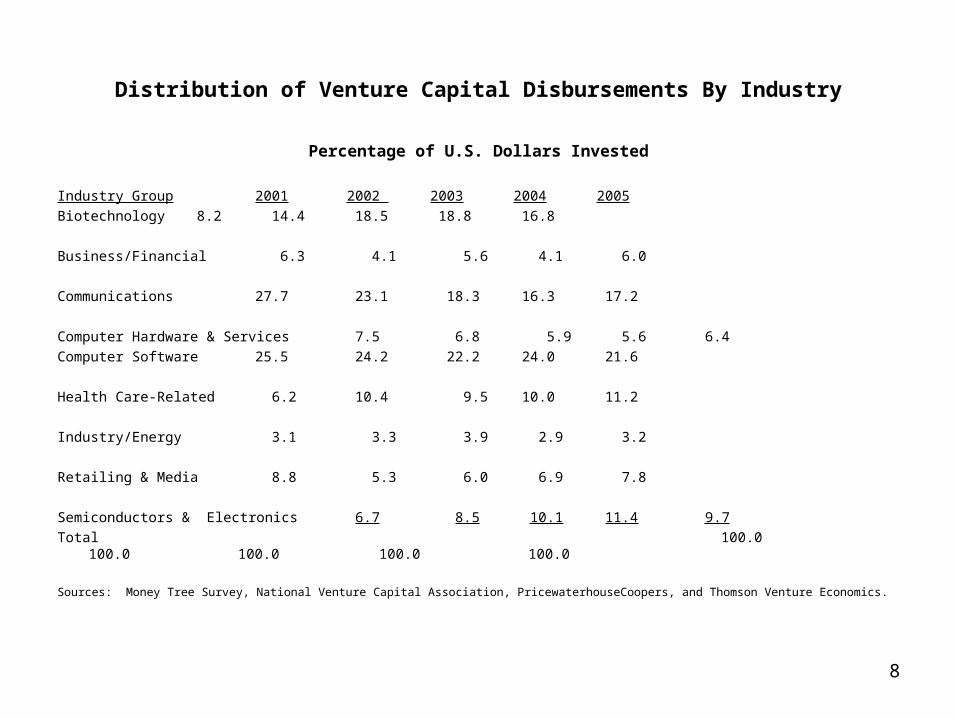

Distribution of Venture Capital Disbursements By Industry

Percentage of U.S. Dollars Invested

Industry Group 2001 2002 2003 2004 2005

Biotechnology 8.2 14.4 18.5 18.8 16.8

Business/Financial 6.3 4.1 5.6 4.1 6.0

Communications 27.7 23.1 18.3 16.3 17.2

Computer Hardware & Services 7.5 6.8 5.9 5.6 6.4

Computer Software 25.5 24.2 22.2 24.0 21.6

Health Care-Related 6.2 10.4 9.5 10.0 11.2

Industry/Energy 3.1 3.3 3.9 2.9 3.2

Retailing & Media 8.8 5.3 6.0 6.9 7.8

Semiconductors & Electronics 6.7 8.5 10.1 11.4 9.7

Total 100.0 100.0 100.0 100.0 100.0

Sources: Money Tree Survey, National Venture Capital Association, PricewaterhouseCoopers, and Thomson Venture Economics.

9

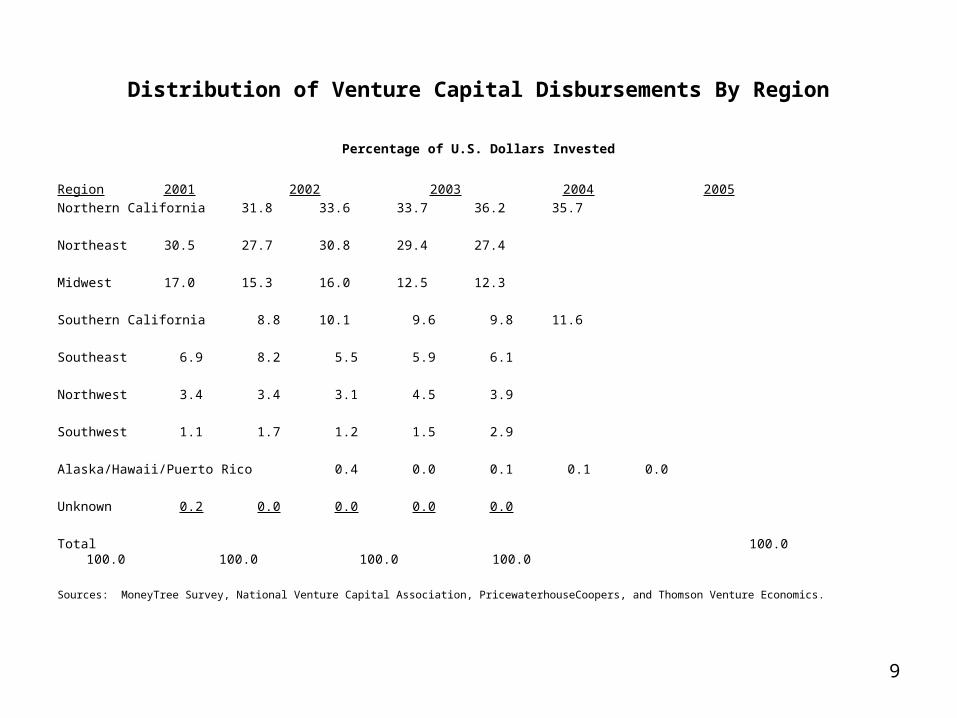

Distribution of Venture Capital Disbursements By Region

Percentage of U.S. Dollars Invested

Region 2001 2002 2003 2004 2005

Northern California 31.8 33.6 33.7 36.2 35.7

Northeast 30.5 27.7 30.8 29.4 27.4

Midwest 17.0 15.3 16.0 12.5 12.3

Southern California 8.8 10.1 9.6 9.8 11.6

Southeast 6.9 8.2 5.5 5.9 6.1

Northwest 3.4 3.4 3.1 4.5 3.9

Southwest 1.1 1.7 1.2 1.5 2.9

Alaska/Hawaii/Puerto Rico 0.4 0.0 0.1 0.1 0.0

Unknown 0.2 0.0 0.0 0.0 0.0

Total 100.0 100.0 100.0 100.0 100.0

Sources: MoneyTree Survey, National Venture Capital Association, PricewaterhouseCoopers, and Thomson Venture Economics.

10

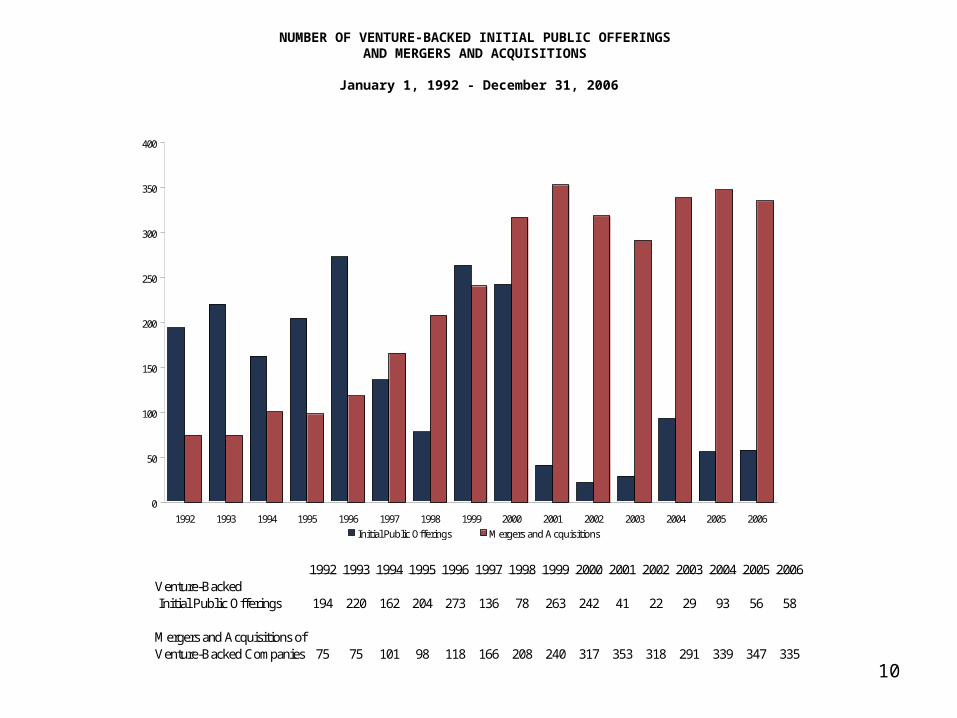

NUMBER OF VENTURE-BACKED INITIAL PUBLIC OFFERINGS AND MERGERS AND ACQUISITIONS

January 1, 1992 - December 31, 2006

0

50

100

150

200

250

300

350

400

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Initial Public Offerings Mergers and Acquisitions

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006Venture-Backed Initial Public Offerings 194 220 162 204 273 136 78 263 242 41 22 29 93 56 58

Mergers and Acquisitions ofVenture-Backed Companies 75 75 101 98 118 166 208 240 317 353 318 291 339 347 335

Sources: National Venture Capital Association Yearbook and Venture Economics.

Note: Data for 2006 are through December 31.213a

11

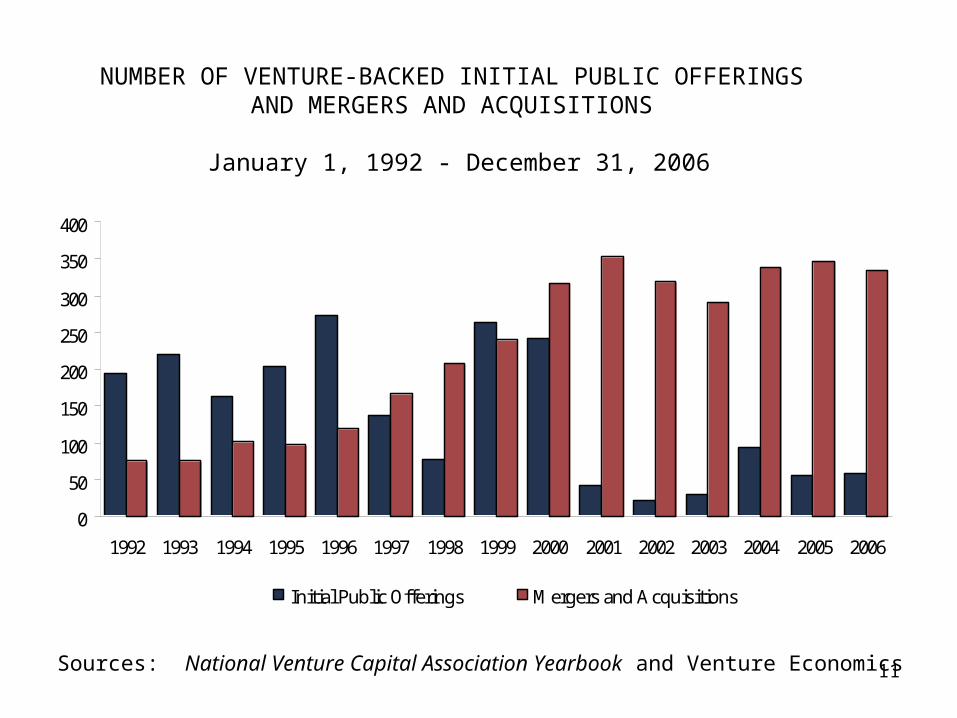

NUMBER OF VENTURE-BACKED INITIAL PUBLIC OFFERINGS AND MERGERS AND ACQUISITIONS

January 1, 1992 - December 31, 2006

0

50

100

150

200

250

300

350

400

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Initial Public Offerings Mergers and Acquisitions

Sources: National Venture Capital Association Yearbook and Venture Economics

12

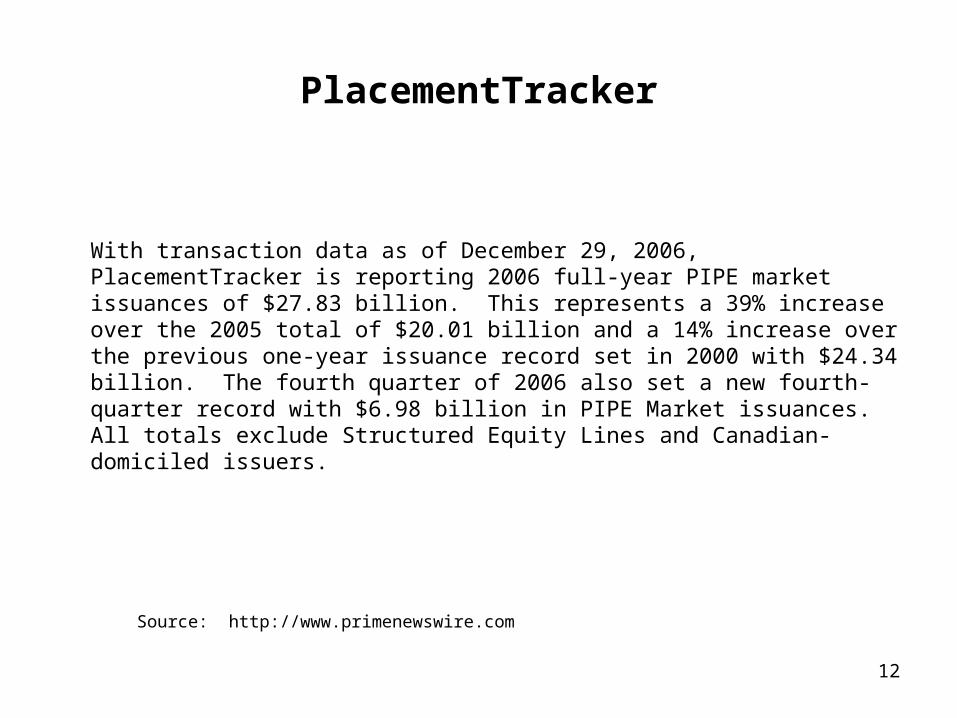

PlacementTracker

With transaction data as of December 29, 2006, PlacementTracker is reporting 2006 full-year PIPE market issuances of $27.83 billion. This represents a 39% increase over the 2005 total of $20.01 billion and a 14% increase over the previous one-year issuance record set in 2000 with $24.34 billion. The fourth quarter of 2006 also set a new fourth-quarter record with $6.98 billion in PIPE Market issuances. All totals exclude Structured Equity Lines and Canadian-domiciled issuers.

Source: http://www.primenewswire.com

13

SPAC’s (Specialized Acquisition Companies)

In all, more than 50 SPAC’s filed to go public in 2005. About half of these, including Cold Spring Capital, have made it to market, raising around $1.2 billion that can be used for acquisitions. By comparison, only 11 deals went public in 2004, and those raised less than $500 million.

Source: http://www.usnews.com

14

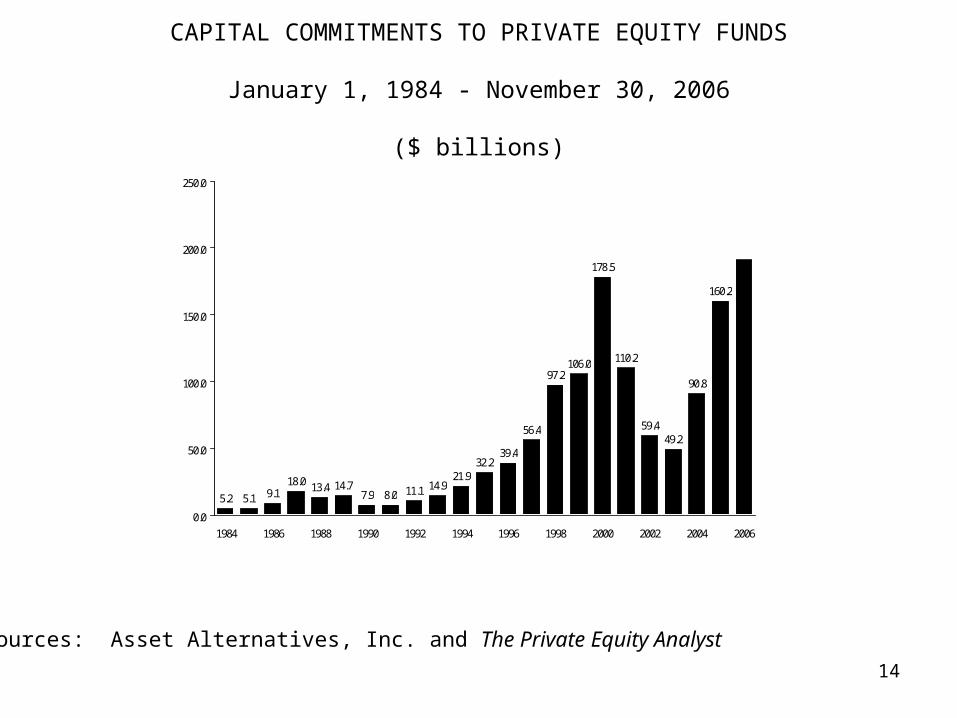

CAPITAL COMMITMENTS TO PRIVATE EQUITY FUNDS

January 1, 1984 - November 30, 2006

($ billions)

32.239.4

97.2

178.5

110.2

59.449.2

90.8

160.2

106.0

5.2 5.1 9.118.0 13.4 14.7

7.9 8.0 11.1 14.921.9

56.4

0.0

50.0

100.0

150.0

200.0

250.0

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Sources: Asset Alternatives, Inc. and The Private Equity Analyst

15

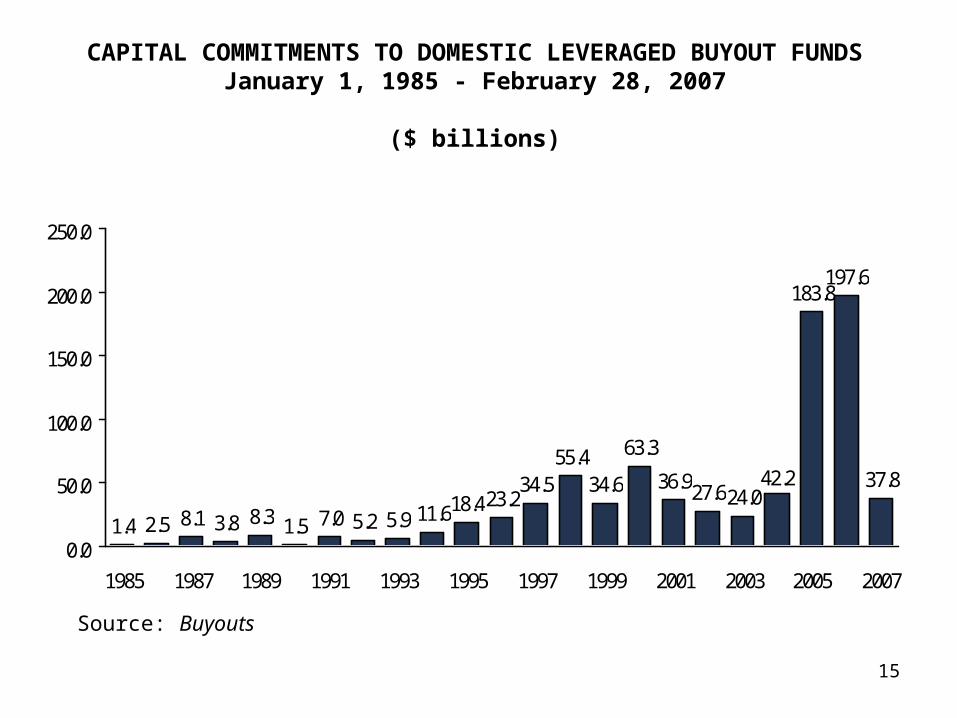

CAPITAL COMMITMENTS TO DOMESTIC LEVERAGED BUYOUT FUNDSJanuary 1, 1985 - February 28, 2007

($ billions)

1.4 2.5 8.1 3.8 8.3 1.5 7.0 5.2 5.9 11.618.423.234.5

55.434.6

63.3

36.927.624.0

183.8197.6

37.842.2

0.0

50.0

100.0

150.0

200.0

250.0

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

Source: Buyouts

16

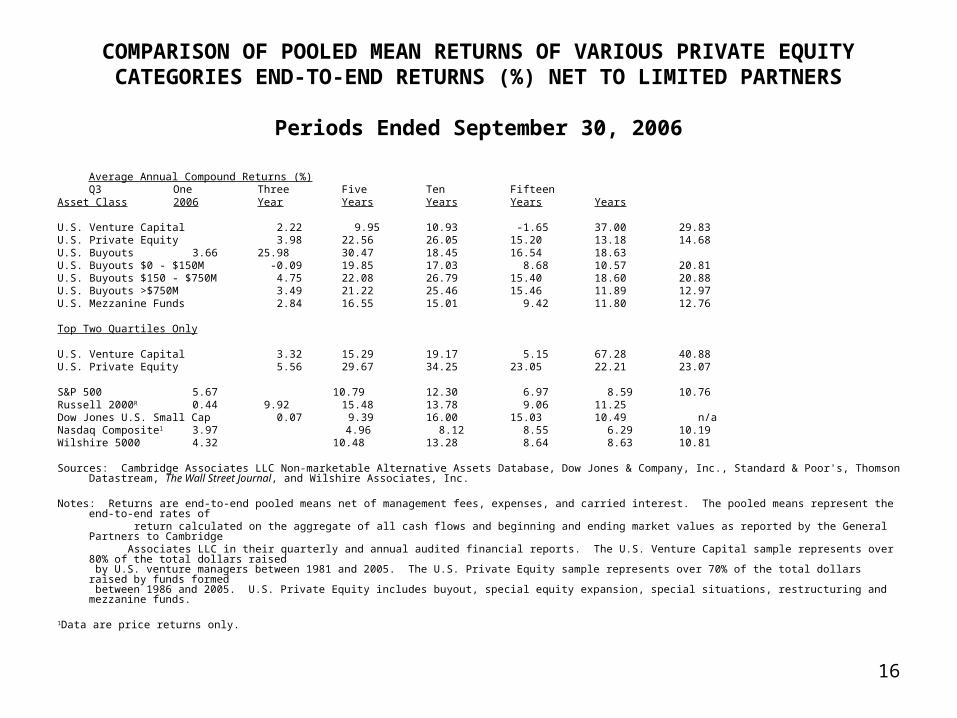

COMPARISON OF POOLED MEAN RETURNS OF VARIOUS PRIVATE EQUITY CATEGORIES END-TO-END RETURNS (%) NET TO LIMITED PARTNERS

Periods Ended September 30, 2006

Average Annual Compound Returns (%) Q3 One Three Five Ten Fifteen

Asset Class 2006 Year Years Years Years Years

U.S. Venture Capital 2.22 9.95 10.93 -1.65 37.00 29.83U.S. Private Equity 3.98 22.56 26.05 15.20 13.18 14.68U.S. Buyouts 3.66 25.98 30.47 18.45 16.54 18.63U.S. Buyouts $0 - $150M -0.09 19.85 17.03 8.68 10.57 20.81U.S. Buyouts $150 - $750M 4.75 22.08 26.79 15.40 18.60 20.88U.S. Buyouts >$750M 3.49 21.22 25.46 15.46 11.89 12.97U.S. Mezzanine Funds 2.84 16.55 15.01 9.42 11.80 12.76

Top Two Quartiles Only

U.S. Venture Capital 3.32 15.29 19.17 5.15 67.28 40.88U.S. Private Equity 5.56 29.67 34.25 23.05 22.21 23.07

S&P 500 5.67 10.79 12.30 6.97 8.59 10.76Russell 2000R 0.44 9.92 15.48 13.78 9.06 11.25Dow Jones U.S. Small Cap 0.07 9.39 16.00 15.03 10.49 n/aNasdaq Composite1 3.97 4.96 8.12 8.55 6.29 10.19Wilshire 5000 4.32 10.48 13.28 8.64 8.63 10.81

Sources: Cambridge Associates LLC Non-marketable Alternative Assets Database, Dow Jones & Company, Inc., Standard & Poor's, Thomson Datastream, The Wall Street Journal, and Wilshire Associates, Inc.

Notes: Returns are end-to-end pooled means net of management fees, expenses, and carried interest. The pooled means represent the end-to-end rates of return calculated on the aggregate of all cash flows and beginning and ending market values as reported by the General Partners to Cambridge Associates LLC in their quarterly and annual audited financial reports. The U.S. Venture Capital sample represents over 80% of the total dollars raised

by U.S. venture managers between 1981 and 2005. The U.S. Private Equity sample represents over 70% of the total dollars raised by funds formed between 1986 and 2005. U.S. Private Equity includes buyout, special equity expansion, special situations, restructuring and mezzanine funds.

1Data are price returns only.