california innovation index - university of...

TRANSCRIPT

C A L I F O R N I A

I N N O V A T I O N I N D E X2 0 0 8 I N A U G U R A L I S S U E

desig

n –

3x3

| p

alo

alto

Next 10 is an independent, nonpartisan organization that educates,engages and empowers Californians to improve the State’s future.California was founded by pioneers driven by big dreams and unafraid to face difficult challenges. Like many of us, theycame to California to create a better life for themselves and their families. While this legacy of the California dreamcontinues today, many of us are concerned that the future will not be as bright as our children deserve.

Next 10 is focused on innovation and the intersection between the economy, the environment, and quality of life issuesfor our state. We create tools and provide information that fosters a deeper understanding of the critical issues affectingall Californians. Through education and civic engagement, we hope Californians will become empowered to affect change.

We call ourselves Next 10 because we are not here for the quick fix. Our sights are set on joining with others to improvethe state over the next ten years, and the ten years after that. The decisions we make together will affect California’seconomy, environment and quality of life for years to come. Together, we can create the brighter future we all want forourselves and our children.

ADVISORS TO THE CALIFORNIA GREEN INNOVATION INDEXNext 10 thanks the following expert Advisors for their generous time and guidance on this project:

Ralph Cavanagh Natural Resources Defense Council

Michael Hanemann California Climate Change Center, Goldman School of Public Policy, U.C. Berkeley

Hal Harvey The William and Flora Hewlett Foundation

Elliot Hoffman New Voice of Business

Van Jones Ella Baker Center

Dan Kammen Class of 1935 Distinguished Professor of EnergyDirector, Renewable & Appropriate Energy Laboratory, U.C. Berkeley

Bruce Klafter Applied Materials

Joel Makower Executive Editor, GreenBiz.com

Walter McGuire McGuire & Co., Inc./ Flex Your Power

Joe Nation Former State Assemblyman, District 6Lecturer in Public Policy, Stanford University

Manuel Pastor Professor of Geography and American Studies & Ethnicity, University of Southern California

Fran Pavley Assemblymember (2000-2006), Author AB 32: California Global Warming Solutions ActSenior Climate Advisor, NRDC

Wendy Pulling Pacific Gas & Electric Company

Carol Whiteside Great Valley Center

Tim Woodward Nth Power

PREPARED BY SURVEY CONDUCTED BY PRODUCED BYCollaborative Economics Field Research Corporation Next 10Doug Henton Deborah Jay F. Noel PerryJohn Melville Mark DiCamillo Sarah HenryTracey Grose Marcia PerryGabrielle Maor Rishell JordonBridget Gibbons

Dear Californians,

California has long played an international role as an incubator of innovation. From the integrated circuit to Web 2.0,recombinant DNA to genomics, world changing ideas and inventions have had their genesis in this state. Lesser known,however, is California’s role in “green” innovation, and the significant impact green innovation can make on the state’seconomic and environmental health.

Next 10, an independent, nonpartisan, nonprofit organization, is launching the California Green Innovation Indexto track the state’s green innovation as well as economic and environmental performance within the context of thelandmark California Global Warming Solutions Act (AB 32). The Index analyzes key indicators including energyconsumption and efficiency, economic growth and carbon emissions, to better understand the role green innovationplays in achieving two goals critical to California’s future: 1) reducing the absolute level of the greenhouse gas emissions thatcause global warming, and 2) increasing the state’s gross domestic product, which is the basis for our economic vitality.

This inaugural issue contains several important findings:• As a result of the first wave of green innovation, which began in the 1970s, California has become a world leader

in energy efficiency. In relative terms, California is more energy efficient and emits fewer greenhouse gas emissionsper person than the rest of the United States, Germany, the United Kingdom or Japan.

• California’s economy has grown as a result of this first wave of green innovation. • California may be at an inflection point between the first and second waves of green innovation driven by factors

similar to those that drove the first wave: policy, demand and investment.• While California has made enormous progress, the state’s rate of population growth requires that the next wave of

innovation be larger, faster and more powerful than the last to meet the mandate of AB 32.

Working with leading experts, Next 10 produced the California Green Innovation Index in support of our missionto educate and engage Californians on issues important to the state’s future. There is no more important issue todaythan addressing global warming while growing a vibrant economy.

Sincerely,

F. Noel PerryFounder, Next 10

575 High Street, Suite 310 | Palo Alto, California 94301 | tel: 650.321.5417 | www.next10.org

California’s PopulationPopulation Average Annual Growth Population Projections

2006 2000-2006 2020

37,195,240 2% 43,695,240

Source: California Department of Finance

California’s EconomyGross Domestic Product (GDP) is a way of measuring the size of an economy, and is calculated by summing the valueadded from all industries in the economy. This measure can be used for a country as well as a state, in which case it canalso be expressed as gross state product (GSP).

Total GDP Average Annual Growth Per Capita GDP GDP Projections

2006 2000-2006 2006 2020

$ 1,727,355,000,000 2% $46,440 $ 2,604,898,000,000

Inflation adjusted dollars (2006) Inflation adjusted dollars (2006)Sources: Bureau of Economic Analysis;California Department of Finance Source: Moody's Economy.com

Assembly Bill 32, the “California Global Warming Solutions Act of 2006”Assembly Bill 32 (AB 32) was signed into California law in 2006, mandating the first ever statewide cap on global warmingpollution. AB 32 has put California at the forefront of the fight against global warming by requiring the state to reduceits greenhouse gas (GHG) emissions to 1990 levels by 2020.

California’s Greenhouse Gas EmissionsGreenhouse gases include carbon dioxide, methane, nitrous oxide and various high global warming potential (GWP) gasesincluding perfluorocarbons, hydrofluorocarbons and sulfur hexafluoride (SF6).

AB 32 TargetsTotal GHG Emissions Average Annual Growth Per Capita GHG Emissions Total GHG Emissions (Million Metric Tons of CO2 Equivalent) (Metric Tons of CO2 Equivalent) (Million Metric Tons of CO2 Equivalent)

1990 2004 2000-2004 2004 2020411 479 1% 12.9 411

Sources: California Energy Commission, revision February 2, 2007 to "Inventory of California Greenhouse Gas Emissions and Sinks" Report (December 2006); California Department of Finance

California’s Carbon EconomyThe ratio of GHG emissions to GDP

Meeting AB 32 Targets1990 2004 20200.45 0.35 0.18Sources: California Energy Commission; Bureau of Economic Analysis

California Facts

Table of Contents CORE FINDINGS 4

1 INNOVATION IS THE DRIVER OF CALIFORNIA'S ECONOMIC AND ENVIRONMENTAL PROGRESS 81. California has relied on its innovative economy to provide growing economic, social,

and environmental benefits to its people 8

2. California has a history of policy innovation, which has helped stimulate technological innovation, producing economic and environmental benefits 10

3. California will need to build on its tradition of innovation if it is to reduce its absolute amount of carbon emissions and produce economic benefits in the years ahead 12

California's Story of Recycling 14

2 THE FIRST WAVE OF GREEN INNOVATION 161. California has one of the lowest per capita greenhouse gas emissions and highest

gross domestic products in the nation 16

2. California's economic growth has become less dependent on greenhouse gas emissions over time 17

3. California demonstrates that energy efficiency can translate into economic gain 20

4. Californians have experienced substantial and growing energy savings as a direct result of efficiency programs 22

3 TRACKING SIGNS OF THE NEXT WAVE OF GREEN INNOVATION 24ENVIRONMENT FOR CHANGE 251. Californians recognize the urgency of the problem-and believe a lot can be done about it 25

2. Californians believe that reducing emissions and growing the economy is both possible and desirable-and believe that new technologies will help solve the problem 25

ADOPTION OF GREEN PRODUCTS AND PRACTICES 261. Californians are accelerating their adoption of green products and practices to reduce electricity consumption 27

2. The commercial business sector-the largest consumer of electricity in California-has become more energy efficient in recent years 30

3. Gasoline sales and vehicle miles traveled have leveled off 31

4. Water consumption and pumping-responsible for about 20% of California's gross electricity use-are using less electricity than in the past 34

5. Californians are increasing their use of cleaner energy to reduce greenhouse gas emissions both at home and on the road 35

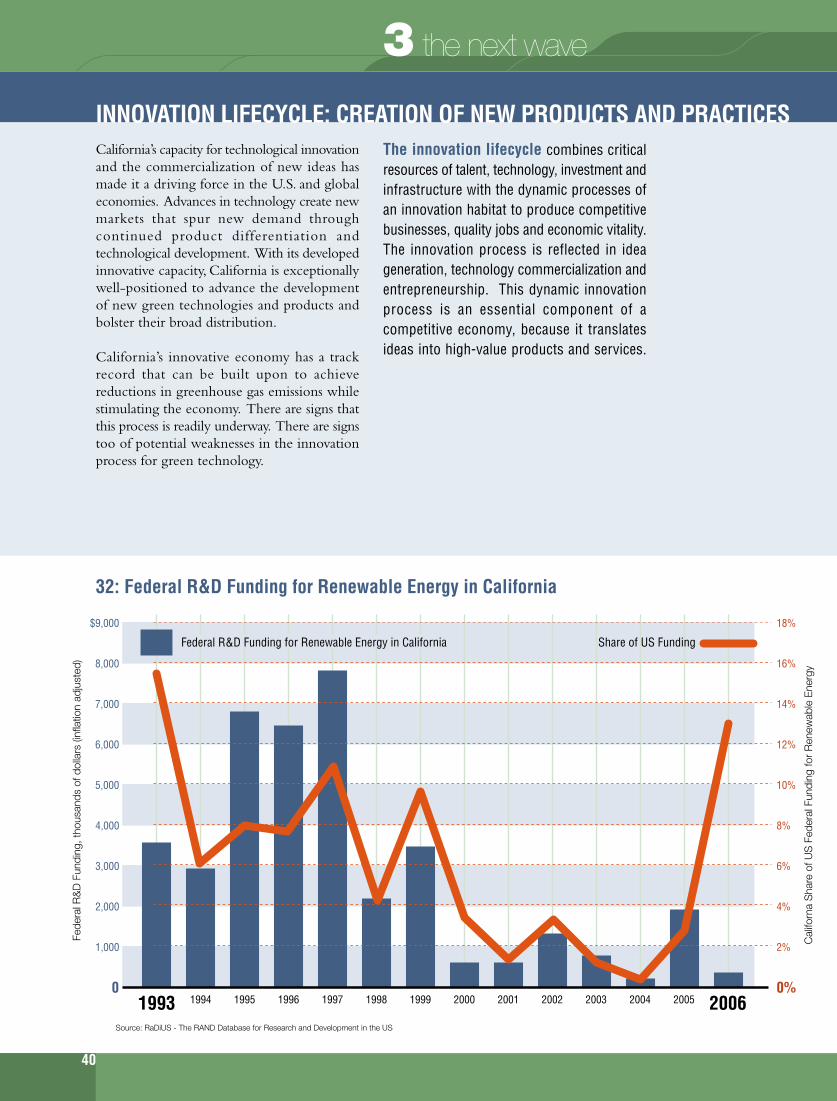

INNOVATION LIFECYCLE: CREATION OF NEW PRODUCTS AND PRACTICES 401. California is drawing increasing R&D investment for clean energy from a variety of public

and private sources 41

2. California is a leader in green technology innovation as measured by patents 42

3. California is top state for U.S. venture capital investment in green technology 43

4. California is home to a growing green industry, which is creating thousands of new companies, jobs, and products to help reduce emissions 46

4 THE CHALLENGE & PROSPECTS FOR THE FUTURE 51

CORE FINDINGSThe inaugural California Green Innovation Index

produced by Next 10 provides a comprehensive

look at the role of innovation in reducing greenhouse

gas emissions while growing the economy. The

Index measures progress toward green innovation—

green in the sense that it generates both

environmenta l and economic benef i t s .

California has been driven by waves of innovation

in information technology, biotechnology and now

energy. Building on a first wave of innovation based

on energy efficiency, the Index identifies a next wave

of innovation that could bring new breakthroughs

in both energy efficiency and clean energy.

4

Emissions and Gross Domestic ProductCarbon emissions per million people - Inflation adjusted GDP dollars per million people; Relative Trends since 1990

Inde

xed

to 1

990

1990 2004

90

95

100

105

110

115

120

125

Source: Energy Information Administration; Population Division, U.S. Census Bureau; Bureau of Economic Analysis; U.S. Department of Commerce

CA per capita emissions

CA per capita GDP

The growing separation illustrates thedeclining dependence of California's economicgrowth on environmental degradation

the first wave

THE FIRST WAVE OF GREEN INNOVATION

California has benefited both economically and environmentally from a first wave of green innovationas a result of increasing energy efficiency since the 1970s.

1. California has become a world leader in addressing global warming. In relative terms, California is more energyefficient and has lower greenhouse gas emissions than the United States as a whole and leads Germany, the United Kingdomand Japan (Chart 2).

2. California has one of the lowest per capita greenhouse gas emissions and highest gross domestic products inthe nation. California’s per capita emissions are less than one-half of the rest of the nation and are lower than they were15 years ago (Chart 1). Among states, California has the second lowest emissions per capita while generating the tenthhighest gross domestic product per capita in the nation.

3. California is more energy efficient than the nation and other comparable states resulting in significant savingsto consumers. Since 1970, California has greatly reduced its total energy consumption per capita (Chart 6). Averagemonthly residential bills for electricity are lower in California than Texas, Florida, and the nation (Chart 8). Moreover,California’s total annual electricity bill as a fraction of GDP is lower than Texas, Florida and the nation (Chart 7). Whatdoes this mean? If California’s annual statewide electricity bill was the same fraction of GDP as Texas, for example,Californians would be paying almost $25 billion more for electricity. Instead, these billions are available for investmentin other areas, generating economic benefits for California.

4. California utility programs and efficiency standards yield billions of dollars in savings and have reduced the needto build additional power plants. California utility efficiency programs and Title 20 and Title 24 (appliance and buildingstandards) have yielded tens of billions of dollars in savings and reduced the need for 24 power plants between 1975 and2003 (Chart 10). The net benefits of these programs continue to improve (Chart 11). The California Energy Commissionestimates that building and appliance standards alone have saved residents and businesses $56 billion through 2003 andare projected to save another $23 billion by 2013.

5

TRACKING SIGNS OF THE NEXT WAVE OF GREEN INNOVATION

Signs that California may be beginning the next wave of green innovation include continued progress inincreasing energy efficiency and the adoption and creation of clean energy.

5. Californians are at the forefront in recognizing that global warming is an urgent challenge that can be addressedby citizens and business as well as government. They also believe that California can reduce greenhouse gases andexpand jobs and prosperity at the same time, and that new technologies can help solve the challenge (Survey Results,pages 22 and 23).

6. Adoption of existing green products and practices is accelerating in California. Californians are adopting andplanning to adopt specific electricity-saving products and practices in homes and businesses (Page 28 and Charts 14, 15,16, 17 on CLF bulbs, appliances and buildings). Californians are also installing solar systems (Chart 28) and purchasinghybrid vehicles (Charts 30-35) at an increasing rate.

7. Creation of new green products and services is increasing in California. California is escalating its share of U.S.patents in solar energy, wind and battery technology (Chart 36). Venture capital investment in California clean energytechnology is growing rapidly (Charts 37, 38, 39). Green establishments and jobs are also increasing, especially in energygeneration and energy efficiency (Charts 41-43).

Milli

ons

of d

olla

rs in

vest

ed in

Cal

iforn

ia c

ompa

nies

1996 2006

900

Source: Nth Power

700

$1,000

0

800

600

Venture Capital Investment in Energy TechnologyInvestment in California companies

500

400

300

200

100

the next wave

6

THE CHALLENGE AND PROSPECTS FOR THE FUTURE

Much more green innovation will be needed if California is to meet the goal of AB 32 (California’s GlobalWarming Solutions Act of 2006 calls for reducing greenhouse gas emissions to the 1990 level by 2020) whilealso growing the economy.

8. California will need to rapidly increase its pace of change with breakthroughs in energy efficiency and the adoptionof clean energy alternatives. This requires significantly accelerating the adoption of clean energy by reducing coststhrough technological innovation (See solar energy cost curve, page 54). It means substantially reducing transportation-generated emissions, which currently make up 41% of total greenhouse gas emissions. Methods to reduce transportation-generated emissions include reducing vehicle miles traveled (Charts 21 & 22) and adopting clean transportation alternatives(Charts 23, 24, 30, 31).

9. California will need to continue to invest in research and commercialization that promotes the creation and adoptionof clean energy. Although federal investment is lagging, California is drawing increasing R&D investment for cleantechnology from a variety of public and private sources. The State has been investing its own resources in clean energythrough various avenues including the PIER program (page 41). The United States government, however, could do muchmore to support green innovation. While California’s share of U.S. patents in clean energy has been increasing, the UnitedStates may no longer be a leader in early stage development of green innovation: since 1998, foreign inventors haveregistered for more green technology patents than U.S. inventors (Chart 35).

10. California is taking steps to achieve the goals of AB 32 and the public supports taking action to address globalwarming. The California Climate Action Team has begun to identify strategies to meet the AB 32 goals (See ClimateAction Team Strategies, page 46), and an increasing number of California businesses are members of the California ClimateAction Registry (Chart 52). The public is very supportive of action to address global warming (Survey Results 55-57).

Milli

on M

etric

Ton

s of

CO

2 E

quiv

alen

t

Source: California Energy Commission

500

0

600

400

History of California Emissions and Future AB 32 Target

300

200

100

20202004

WithoutInnovation

1990

AB32 Emissions Limit

WithInnovation

the future

7

Num

ber

of tr

ansi

stor

s on

an

inte

grat

ed c

ircui

t

NUMBER OF TRANSITORS DOUBLING EVERY 24 MONTHS

Moore’s Law describes an important trend inthe history of information technology: thenumber of transistors that can be placed on anintegrated circuit increases exponentially,doubling approximately every two years.

This observation about continuing innovationin information technology was first made byIntel co-founder Gordon E. Moore in 1965.Moore’s Law has been a driving force oftechnological and social change throughoutthe late 20th century and early 21st century—not only in information technology, but alsoin biotechnology, nanotechnology and energytechnology.

Intel, Excerpts from a conversation with GordonMoore: Moore's Law, Video Transcript, 2005.

1971 1980 1980 2000 2004

10,000,000,000

2,300

10,000

1,000,000,000

100,000,000

10,000,000

1,000,000

500,000

Growth of transitor counts for Intel Processors (dots) and Moore's Law

innovation1

California has helped ignite innovation in areasas diverse as information technology (e.g.,integrated circuits), biotechnology (e.g.,recombinant DNA), agriculture (e.g., waterflow technology), entertainment (e.g., digitalmedia), and communications (e.g., wirelessinternet). Innovation improves efficiency inour economy and creates new sources of value.1

Gordon Moore, the co-founder of IntelCorporation, famously described the exponentialpower of innovation to drive efficiency in theinformation technology industry (see box).

Innovation happens incrementally, but alsocomes in bursts, producing breakthroughs thatrapidly increase efficiencies and value. As theillustration shows, California helped drive wavesof innovation in information technology—from defense to the integrated circuit to thepersonal computer to the internet and now to

Web 2.0. A similar series of waves is evidentwith biotechnology, from recombinant DNAto genomics and now to personalized medicine(i.e., translational genomics). Energy is nodifferent: California has helped drive a first waveof green innovation in energy efficiency thatbegan in the 1970s and continues to this day.

Today, a new wave of innovation that buildson the first wave of improvement in energyefficiency may be underway—one that isbeginning to focus growing dollars and talenton clean energy. This next wave may beemerging even as the first wave of greeninnovation continues delivering benefits toCalifornia. What could this next wave looklike? It could bring new breakthroughs in bothenergy efficiency and clean energy, reducingthe absolute amount of greenhouse gas emissionswhile g rowing the State’s economy.

INNOVATION IS THE DRIVER OF CALIFORNIA’S ECONOMIC AND ENVIRONMENTAL PROGRESS

California hasrelied on itsinnovativeeconomy toprovide growingeconomic,social, andenvironmentalbenefits toits people

MOORE’S LAW

8

1950 2000

PER

FOR

MAN

CE

1960 1970 1980 1990

DEFENSE

INTEGRATEDCIRCUIT

PERSONALCOMPUTER

INTERNET

WEB 2.0

RECOMBINANTDNA

GENOMICS

PERSONALIZEDMEDICINE

ENERGY EFFICIENCY

ENERGY EFFICIENCY &CLEAN ENERGY

TIME

“One of the most important lessons from California’s history of leadership in energy efficiencyis that innovation—technological, economic, and political—can take place at levels far beyondwhat is initially forecast if a strong commitment is made to advancing the sector.”2

Daniel Kammen, Founding Director, Renewable and Appropr iate Energy Laboratory,University of California, Berkeley

“Properly designed environmental standards can trigger innovations that lower the total cost ofa product or improve its value. Such innovations allow companies to use a range of inputs moreproductively—from raw materials to energy to labor—thus offsetting the costs of improvingenvironmental impact and ending the stalemate. Ultimately, this enhanced resource productivitymakes companies more competitive, not less.” 3

Michael Porter, Harvard Business School

“Rather than requiring subsidies, energy-productivity opportunities provide a positive rate ofreturn, freeing up resources that could be consumed elsewhere or invested for faster growth.”4

Diane Farrell, McKinsey Global Institute

OBSERVATIONS ABOUT INNOVATION, EFFICIENCY & THE ENVIRONMENT

WAVES OF INNOVATION

First Wave• Breakthroughs primarily in energy efficiency; growth in renewable energy

• Increasing energy efficiency and reducing emissions per capita while growing the economy

• Most progress in electricity efficiency in homes and workplaces; little progress in transportation

• California is the leader in adoption of innovative green practices

Next Wave• New breakthroughs in both energy efficiency and clean energyalternatives, an alignment of markets, policies, and technology

• Reducing absolute amount of emissions to 1990 levels whilegrowing the economy

• Major improvements in all areas, including transportation viabroad-based adoption of alternative fuel technologies and vehicles

• California is the leader in both creation and adoption of green innovations, serving statewide and global markets

9

5

First in United States

For decades California has been a nationalleader in innovative environmental policy.States have long been seen as the laboratoriesfor new policies, and in the realm ofenvironmental policy, California’s innovativeapproaches are replicated in other states and usedas a model for federal legislation as well as forother countries. According to the CongressionalResearch Service, “California has served as alaboratory for the demonstration of cutting-edge emission control technologies, which,after successfully demonstrated there, wereadopted in similar form at the national level.”5

Since the 1970s the State has boldly set standards,designed incentives, enforced disincentives, andreadjusted major drivers of market dynamicstoward improving energy efficiency andprotecting natural resources and public health.These policy innovations have been the productof combined efforts by public leaders, businessleaders, grassroots organizations, and the State’scutting-edge technology innovation community.

The OPEC oil embargo in 1973 served as amajor force in spurring policy and technologyinnovation relating to energy efficiency. Thenext year, the State established the CaliforniaEnergy Commission to implement energypolicy and planning, and Lawrence Berkeley

National Laboratory established the Center forBuilding Science to research means forimproving energy efficiency. In an earlycontribution to the cause, the Center developeda computer program that modeled the energyperformance of buildings. This programestablished the basis for the path-breakinglegislation on energy efficiency standards forappliances and buildings (Title 20 and Title24). Enactment in California was followed bythe enactment of similar standards across theUnited States and other countries. By 1987,a uniform national standard for efficiency inappliances was in place.

A pioneering effort led by a bold group ofefficiency advocates, utilities, and enlightenedleaders led to the realignment of investor-owned utilities’ financial incentives fromexpanding consumption to investing inefficiency. This was made possible through theimplementation of a decoupling mechanism ofelectricity and natural gas providers in 1982.This policy innovation removes the financialdisincentive for utilities to encourage energyefficiency and conservation by making theirprofits independent of their sales.6 FollowingCalifornia’s lead, other states and countries arepursuing similar mechanisms to unlink economicincentives from environmental degradation.

California hasa history ofpolicy innovation,which has helpedstimulatetechnologicalinnovation,producingeconomic andenvironmentalbenefits

innovation1

California Policy Innovations Over Time (Regulatory, Investment, Incetives)Set in Context with U.S. Policy Innovations and Other Historical Events

1977Clean Water Act

1986Emergency Planning andCommunity Right-to-KnowAct (EPCRKA)

1987National Appliance EnergyConservationAct (NAECA)

1980Comprehensive EnvironmentalResponse, Compensation, andLiability Act (CERCLA) createdthe Superfund program

1974Lawrence Berkeley Laboratory’s Centerfor Building Science Established

1976Statistical model illustratingenergy-savings potential throughbuilding efficiency is releasedto public

1978Efficiency Standardsfor new buildings(Title 24)

1982California PUCorders removalof financial barriersto utilities andenergy efficiencyinvestments

1977Efficiency Standardsfor appliances(Title 20)

1947Los Angeles Air PollutionControl District created;first air pollution agencyin the US.

1959California Motor VehiclePollution Control Boardcreated to test automobileemissions and set standards.

1955National Air PollutionControl Act

8/1973 - 9/1974OPEC Oil Embargo

1963Clean Air Act

1965National EmissionsStandards Act

1967Air Quality Act

1967California Air ResourcesBoard established

1980 - 1983Efficiency Standardsfor appliances - Florida,Kansas and New York

1986Efficiency Standardsfor appliances- Massachusetts

1974CA Energy Commissionis created

10

The energy crisis in 2000 and 2001 providedanother major force in spurring policy andtechnology innovation relating to energyefficiency. A result of the failed attempt atutility market deregulation, rolling black-outscharacterized the two-year period. As in 1973,this crisis provided a fresh impetus for policyand technology innovation targeting improvedenergy efficiency in California. Ensuing policyinnovations include broad-based energyefficiency campaigns, incentives for renewableenergy sources, investment in technologyresearch, and standards that reduce greenhousegas emissions. Recent novel approaches includethe following:

• Flex Your Power, the statewide energy conservationcampaign, was launched in 2001, funded primarilyby a Public Goods Charge of one percent added toinvestor-owned utility bills. This outreach effort aimsto inform residents, businesses, industry and public entitiesof methods for reducing energy use and of financialincentives that encourage adoption of such methods.

• California’s Renewable Portfolio StandardProgram was established with the goal of increasingthe percentage of renewable energy in the State'selectricity mix of investor-owned utilities (IOUs) to20% by 2017. This goal has since been acceleratedto be achieved by 2010.

• California’s Clean Cars Law of 2002 (AB 1493)requires carmakers to reduce global warming emissionsfrom new passenger cars and light trucks beginningin 2009. First in the world to reduce global warmingpollution from cars, this law has now been adoptedby 11 other states. Affecting nearly one-third of theU.S. market, global warming emissions in 2020 willbe reduced by more than 64 million tons of carbondioxide a year.

• The California Global Warming SolutionsAct of 2006 (AB 32) is the first law tocomprehensively limit greenhouse gas (GHG)emissions at the state level. Five Western states(Washington, Oregon, Utah, Arizona, New Mexico)have joined California to combine efforts towardreducing greenhouse gas emissions with the WesternRegional Climate Action Initiative.

California has the creative capacity through itsample assets of innovative technology, policy,and public outreach to make meaningful progresstoward reducing greenhouse gas emissions. Ashistory shows, the investment and risk-takingin innovation pays off beyond the State’s borders.

1990Clean Air Act Amendments of 1990 set newautomobile emissions standards, low-sulfur gas,required Best Available Control Technology (BACT)for toxins, reduction in CFCs.

5/2000- 9/2001California Energy Crisis

1989California Integrated WasteManagement Act (AB939)

1997California Energy Commission'sPublic Interest Energy Research(PIER) Program Established

1989Montreal Protocolon ozone-depletingchemicals implemented

1996Electric IndustryDeregulation Law

2003Governor's West CoastGlobal Warming Initiative(CA, OR, WA)

2006Film release:Who killed the electric car?An Inconvenient Truth

2007Commonwealthof Massachusetts v.EnvironmentalProtection Agency

2/2007Utah, Manitoba &British Columbiajoin Governor'sWest Coast GlobalWarming Initiative

2005Governor's ExecutiveOrder S-3-05 setgreenhouse gasemission reductiontargets

2007Western RegionalClimate Action Initiative

9/2007California PUCapproves incentivesfor investor-owned

energy savings goals

2004Governor’s GreenBuilding InitiativeExecutive Order(S-20-04)

9/2000CA Climate Action Registryestablished (SB1771)

9/2000Legislature approves 10-year,$7 billion utility sectorinvestments in energy

2006California Global WarmingSolutions Act of 2006 (AB 32)

2006California Greenhouse GasPerformance Standards forPower Plants (SB 1368)

8/2006California Solar Initiative

2001Flex Your Powerinitiated

2004Adopted by Idaho

2002California ClimateAction Registry ismandated (SB 812)

CA Renewable PortfolioStandard (RPS)

California AB 1493sets standards foremissions of CO2 andother greenhouse gasesfrom automobiles andlight duty trucks.

2001Adopted by Oregon

2007Adopted by Maryland

efficiency, renewables,technology R&D

utilities in meeting

11

If the past is a guide, California’s tradition ofinnovation could flow in both familiar andunpredictable ways—from breakthroughs inenergy efficiency to adoption of clean energyalternatives. It will need to be “greeninnovation”—green in the sense that it generatesboth environmental and economic benefits.

Green innovation is a shared responsibility. Itis the product of government, private sector,and individual actions. There are actions thatall these parties can take that can lead to positiveresults, but it is the result of the process ofinteractions among these parties that creates afar greater impact on reducing greenhouse gasemissions and generating economic benefits.As this process of action and reaction progresses,patterns of adoption (e.g. purchase of upgradedappliance) and creation (e.g. commercializationof new technology) continue and build uponeach other thereby increasing the speed ofinnovation and increasing the impact onreducing emissions and stimulating the economy.

The diagram below illustrates the three parties:People, Public Sector and Private Sector. Thecurved arrows represent the interaction betweeneach party, and this is where innovation takesplace. This interaction generates the exchangeof ideas, adoption of new behaviors and thecreation of new products and finally results ina larger impact on reducing emissions by eachof the parties.

Green innovation is a two-way street.Government plays a critical role in setting thepolicy environment, and the private sector andindividuals respond to mandates and incentives.However, the private sector and individuals canprovide catalysts for green innovation as well.

Government adopts policy innovations, whichcreates an environment that encourages bothprivate sector and individual innovation. At thesame time, government policy is influenced bythe emergence of new technologies, products,and business practices in the marketplace,which demonstrate what could be possible ona larger scale. Elected officials also pursuepolicy innovations in response to growingconcerns from the public—interests shaped bythe media, consumer experience, and personalvalues, as much as by government informationand incentives.

Private sector businesses respond togovernment mandates and incentives, but alsoto global market forces (like the price of oil).Businesses pursue innovations to meetemerging industry and consumer demand fornew green products and practices. Theseinnovations not only help the bottom line ofCalifornia businesses, but also create jobs, helpinform policy, and change individual behaviorby offering tangible applications of greeninnovation.

The private sector also includes a diverse mixof non-profit groups that promote changes ingovernment policy, business practices, andindividual behaviors. This “independent sector”of organizations is an important catalyst forgreen innovation.

Individuals not only respond to governmentincentives and availability of new products, butalso influence the direction of policy throughthe political process and generate demand fornew green products in the marketplace.

California will needto build on itstradition ofinnovation if it is toreduce its absoluteamount of carbonemissions toaddress globalwarming andproduce economicbenefits in theyears ahead

innovation1

12

INN

OV

AT

ION

I N

NO

VA

TIO

N

I N N O V A T I O N

STANDARDS

POLICYI N C E N T I V E S

GreenhouseGas Emissions

PERFORMANCEEconomy:

Jobs, Income

DYNAMICS OF GREEN INNOVATION

INVESTMENT

PRIVATESECTOR

B U S I N E S S

AT T I T U D E S

PEOPLEB E H AV I O R S

13

A government mandate with significant coordination with businesses and consumersSpecial Analysis prepared by Howard Chong, U.C. Berkeley

In the span of 20 years, California transformedrecycling from an industry of waste to one ofefficacy. California’s story of recycling—usinginnovation to turn waste into prosperity—mirrors the current challenges presented bygreenhouse gas emissions levels and meetingthe goals of AB 32.

In 1989, the waste diversion rate in Californiawas stuck at 10%, and California was runningout of places to put its trash. Recyclingrequirements were born out of the perceptionof a landfill crisis. Within 20 years, Californiadeveloped a new recycling infrastructure andmoved from a 10% diversion rate to a 50%diversion rate. This was not just a matter ofmandating reduction; success required significantcoordination with business consumers to create

“Buy Recycled” markets to integrate recycledmaterials into manufacturing processes andconsumer choices. Furthermore, there was aconcurrent effort to address regulation of landfillsand the pollution that they create despite theconventional wisdom that “more garbage equalseconomic prosperity.”

Recycling has similarities to, and offers potentiallessons on dealing with, the current issue ofclimate change. Energy use has historicallybeen linked to economic prosperity but is nowidentified as having environmental consequencesthat require public action. By combining policywith private industry and individual action,California has the opportunity to reduce theimpact of global warming, while simultaneouslystrengthening the economy.

MORE

CALIFORNIANS

RECYCLE

THAN VOTE

1989 2005

60%

Source: California Integrated Waste Management Board

0%

50%

California Statewide Diversion Rates

40%

30%

20%

10%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

C A L I F O R N I A ’ S S T O R Y

14

Similiarities and Potential Lessons between Recycling and Climate Change

O F R E C Y C L I N G

Recycling

More waste = more “stuff” = prosperity

Pollution from landfills,running out of landfill space

Generate less waste

AB 939 in 1989:Target of 50% diversion by 2000

Significant improvements in characterizingthe waste stream, including mandatoryreporting requirements

Did not sacrifice economic development;evidence shows that recycling hada positive impact on job creation andeconomic growth

Increased disposal costs;voluntary participation in sortingrecyclables from garbage

Extremely positive attitude to recycling,evidenced by high public participation

Climate Change

More energy use = prosperity

Global warming,energy shortages

Consume less energy

AB 32 in 2006: Target of reductionto 1990 levels by 2020(29.5% reduction from business as usual)

Significant improvements in characterizingGHG emissions, including mandatoryreporting requirements

Official State and private forecasts predicta net positive impact on job creation andeconomic growth, though some industriesmay suffer while others gain

Predicted increased energy costs,possibly mitigated or offset by a shifttoward less energy-intensive consumption;voluntary action otherwise

Concern about global warming and willingnessto make adjustments to decrease GHGemissions

Criteria

Conventional Wisdom

Impending Crisis

CorrectiveAction Needed

Government Action

Early Innovations

Effect onEconomicGrowth

Impact on Individuals

Public Attitude

15

1990 1992 1994 1996 1998 2000 2002 20040

5

10

15

20

25

30

35

40

1: GHG Emissions in California and Other StatesCO2 emissions from fossil fuel combustion – metric tons CO2 (MTCO2) per Capita

Met

ric T

ons

CO

2 pe

r C

apita

California

Florida

US w/o CA

Texas

Source: Energy Information Administration; Population Division, U.S. Census Bureau; Bureau of Economic Analysis; U.S. Department of Commerce

2004 National RankingLowest GHG Highest GDP GDP in Billions Share of Total

Emissions Per Capita Per Capita ($2004) U.S. GDP

California 2 10 $ 1,540 13%Texas 40 18 886 8%Florida 11 37 601 5%

34.5

21.4

14.5

12.2

30.6

21.5

14.7

11.0

Source: Energy Information Administration; Population Division, U.S. Census Bureau; Bureau of Economic Analysis; U.S. Department of Commerce

the first wave2

California has been at the forefront of the firstwave of green innovation that began in the1970s and continues to this day. This first waveproved that California could increase its energyefficiency and reduce its greenhouse gas emissionsper capita, while also growing its economy.

The first wave of green innovation was drivenby a confluence of many forces—includingrising oil prices, supportive state policies (asoutlined earlier), shifting attitudes and behaviorsabout energy and water conservation; andtechnological innovation in green building,materials, appliances, lighting, and other areas.It produced breakthroughs in energy efficiencyand stimulated growth in renewable energy inCalifornia. While it is difficult to discern howmuch each of the many different factorscontributed to this first wave, it is clear thatCalifornia today has one of the lowest per capitagreenhouse gas emissions and highest per capitagross domestic products in the nation.

On a per capita basis, the State’s economy hasbecome less dependent on emissions and hasused less energy to produce more economicgrowth over time. California’s situation moreclosely resembles that of Germany, the UnitedKingdom, and Japan than the rest of the UnitedStates—especially other large states with diverseeconomies like Texas and Florida.

California has one of the lowest per capitagreenhouse gas emissions and highestgross domestic products in the nation

California has some of the lowest per capitaGHG emissions in the U.S. In fact, per capitaCO2 emissions in Texas are double those ofCalifornia. Per capita emissions levels inCalifornia today are slightly lower than theywere 15 years ago, dropping from 12.2 to 11MMTCO2E7 (Chart 1).

THE FIRST WAVE OF GREEN INNOVATION

16

GOAL

25.0

20.0

15.0

10.0

5.0

00 0.5 1.0 1.5 2.0 2.5 3.0 3.5

25.0

0

20.0

15.0

10.0

5.0

GOAL0 1.00.5

California’seconomic growthhas becomeless dependenton greenhousegas emissionsover time

2: Global Fossil Fuel Combustion*

California

France

Japan

U.K.

Germany

U.S. w/o CA

United States

India

China

California

France

Japan U.K. Germany

U.S. w/o CA

United States

EFF

ICIE

NC

YE

mis

sion

s pe

r C

apita

(Met

ric T

ons

CO

2 E

quiv

alen

t per

Per

son)

INTENSITYEmissions per GDP Dollar

(Metric Tons CO2 Equivalent per Thousand, inflation adjusted U.S. Dollars GDP

*The combustion of fossil fuels accountsfor roughly 72% of total GHG emissions.

Sources: Energy Information Administration,International Energy Annual 2004;California Energy Commission;Bureau of Economic Analysis,U.S. Department of Commerce

Compared to other countries, California isamong the most advanced and efficienteconomies, which sets it apart from the rest ofthe U.S. Mainly due to structural changes inthe economy, the global economy is becomingless carbon intensive in terms of emissions pergross domestic product (GDP). Greaterdisparities exist in terms of efficiency, oremissions per capita. Resulting primarily fromelectricity generation and transportation, fossilfuel combustion (petroleum, natural gas & coal)makes up the largest category of carbon emissionsin the world. As economies such as China andIndia continue their rapid growth, absolute

emissions and emissions per capita will climb.In view of both emissions per dollar of GDPand emissions per capita, California is comparablewith Japan. Per capita emissions in the rest ofthe U.S. are twice California’s (Chart 2).

California is an example of how an innovativeeconomy can thr ive and grow whilesimultaneously reducing the environmentaldamage associated with growth. Breaking thelink between “environmental bads” and“economic goods” occurs when the growth rateof an environmental pressure is less than that ofeconomic expansion over a period of time.8

17

3: Emissions and Gross Domestic ProductCarbon emissions per million people - Inflation adjusted GDP dollars per million peopleRelative trends since 1990

Inde

xed

to 1

990

California’s GDP is a measurement of the State’seconomic output. Examining the growth inGDP alongside the growth in carbon emissionsillustrates the changing relationship betweenthe two over time. (Carbon emissions accountfor roughly 72% of all greenhouse gas emissions.)Chart 3 depicts the growth rates per capita ofGDP and emissions for California relative to

1990. The growing distance between the trendlines of GDP rising and emissions droppingrepresent the delinking of GHG emissions fromeconomic growth. (Per capita emissions representedhere are based on the California Energy Commission’sGHG Inventory and vary slightly from the federalGHG data represented in Chart 1.)

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 20 03 2004

90

95

100

105

110

115

120

125

Source: Energy Information Administration; Population Division, U.S. Census Bureau; Bureau of Economic Analysis; U.S. Department of Commerce

CA per capita emissions

CA per capita GDP

The growing separation illustratesthe dec lining dependence ofCalifornia's economic growth onenvi ronmenta l degradat ion

the first wave2

18

1990 1992 1994 1996 1998 2000 2002 2004100

150

200

250

300

350

400

450

500

5: Total GHG Emissions in CaliforniaAnnual Emissions

Milli

on M

etric

Ton

s C

O2

Equ

ival

ent

1990 1992 1994 1996 1998 2000 2002 2004 Carbon Free Economy = 0

.02

.04

.06

.08

.10

4: The Carbon EconomyEmissions relative to GDP: California

Em

issi

ons/

GD

P

Illustrated as a ratio of emissions to GDP,Chart 4 depicts California’s carbon economyand its gradually decreasing carbon character.While improvements are evident, in order tomeet the requirements of AB 32, this decreasewill need to be steeper in the future. Asrepresented in Chart 5, the State’s absoluteemissions continue to rise.

*Gross GHG emissions including electricity importsSource: California Energy Commission; Bureau of Economic Analysis; U.S. Department of Commerce

Source: California Energy Commission

Note: Total Baseline greenhouse gas emissionsincludes fossil fuel CO2, with electric imports andinternational fuels (carbon dioxide only) and non-carbon ghg emissions (in CO2 equivalents). Non-carbon ghg emissions are made up of Agriculture(CH4 and N2O). Soils and Forests Carbon Sinks,ODS substitutes, Semi-conductor manufacture(PFCs), Electric Utilities (SF6). Cement, OtherIndustrial Processes, Solid Waste Management,Landfill Gas, and Wastewater, Methane from oiland gas systems, Methane and N2O from FossilFuel Combustion.

19

6: Total Energy Consumption Relative to 1970California and the Rest of the U.S.

Inde

xed

to 1

970

While California’s economy has grownsubstantially over the past several decades, theState has consistently improved its efficiencyin energy consumption (See pages 22-23).Since 1970, California has greatly reduced itstotal energy consumption per capita (Chart6); however, in absolute terms, the State’s totalenergy consumption continues to rise as itspopulation grows, underscoring the need forcontinued efforts to increase efficiency. Totalenergy consumption includes all of the following

sources: petroleum, natural gas, electricity retailsales, nuclear, coal and coal coke, wood, waste,ethanol, hydroelectric, geothermal, solar andwind energy.

The State has shown that it is possible to havelower electricity bills through greater energyefficiency than most states. This meansCalifornians have more to spend on otheruses—money that their counterparts in otherstates spend on energy.

Californiademonstrates thatenergy efficiencycan translate intoeconomic gain

1970 1975 1980 2004

100

120

Source: Energy Information Administration; U.S. Census

CA Per Capita

Rest of U.S. per Capita

1985 1990 1995 2000

110

130

140

150

160

90

80

CA Total Consumption

Rest of U.S. Total Consumption

Although total energy consumption relative to 1970 levelshas increased similarly in California and the rest of theUS, trends in per capita consumption (a measure ofefficiency) have taken very different paths. Since 1980,per capita consumption in California has continuedto decrease relative to 1970 levels.

the first wave2

20

7: Statewide Electricity Bill as a Fraction of GDP

Per

cent

age

of G

DP

8: Average Monthly Residential Gas & Electrical Bills2005

$49

$74

California

$43

$118

Florida

$50

$135

Texas

$84

$86

US w/o CA

In Chart 7, the state electricity bill is representedas a fraction of state GDP. As a fraction of thestate economy, the Texas electricity bill is almostdouble the California bill.

Looking at the most recent year, 2005,California’s bill represents 1.79% of GDP –about half the Texas bill which equates to 3.24%of GDP.8 The difference between the two statesof 1.45%, when put into terms of California’sGDP, translates into $24.7 billion thatCalifornians do not spend on electricity.

Since 1999, there has been little variation yearto year in California’s average residential electricbills. In 2005, the average monthly residentialelectricity bill in California was almost half thatof Texas and two-thirds the average bill inFlorida (Chart 8). In view of natural gas, whilesimilar to bills in Florida and Texas, California’saverage monthly residential bill is roughly half ashigh as bills in the rest of the country (Chart 9).

Recent work by researchers at U.C. Berkeleyconcludes that California's residential low energyuse is real. “From 1970 to 2004, Californiadecreased its annual residential energyconsumption by 35% while other statesincreased. Alternative explanations includingweather, income, prices and economic structureaccount for at most 15%.”10

1990 1991 2005

3.5%

Source: Energy Information Agency, U.S. Department of Energy; Bureau of Economic Analysis, U.S. Department of Commerce

2.0%

4.0%

4.5%

1.0%

0%1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

California

US without CA

Texas

Florida

1.79%

2.97%

2.54%

3.24%

3.0%

2.5%

1.5%

0

20

40

60

80

100

120

$160

140

Natural Gas

Electricity

Source: Energy Information Agency, U.S. Department of Energy

0.5%

21

10: Annual Energy Savings from Efficiency Programs and StandardsGigawatt-hours per year

Investor-OwnedUtility Efficiency

Programs

BuildingStandards

ApplianceStandards

GW

h/ye

ar

California has implemented efficiency programsand standards that have yielded increasingelectricity savings. In 2003, the State saved40,000 Gigawatt-hours through utility efficiencyprograms which equated to 15% of annualelectricity use in California that year (Chart10). Since 1975, this energy savings has supplantedthe need for 24 new, large-scale (500-megawatt)power plants.11 Although Chart 10 only includesprograms of investor-owned utilities, California'spublicly owned utilities have more than tripled

their energy savings targets, which cumulativelynow total about 120 MW per year (comparedto 500 MW for the three major investor-ownedutilities).

In addition, projected savings associated withrecently adopted updates to California’s energyefficiency standards for buildings and appliancesare expected to avoid the need for five giantpower plants in the next 10 years.12 (See page29 for description of Title 20 Appliance EfficiencyStandards and Title 24 Building Efficiency Standards.)

Californians haveexperiencedsubstantial andgrowing energysavings as a directresult of efficiencyprograms

1975 1977 2003

30,000

Source: California Energy CommissionNote: This dataset is part of a demand forecast output. As of October 2007, the CEC does not have 2004 and 2005 data available yet,as data for more recent years have not been normalized to this particular set of data.

20,000

40,000

50,000

10,000

01979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

~15% of Annual Electricity Usein California in 2003

the first wave2

22

Net

Dol

lar

Sav

ings

(Billi

ons

of In

flatio

n A

djus

ted

Dol

lars

)

Firs

t Yea

r N

et A

nnua

l Sav

ings

(GW

h)

First Year Net AnnualEnergy Savings (GWh)Net Dollar Savings

Source: Pacific Gas and Electric Company, Southern California Edison, and San Diego Gas & Electric, “Energy Efficiency Annual Reports,”May 1999–2005, filed at the California Public Utilities Commission.

*Note: Net benefits & energy savings includes Electricity & Natural Gas

1998 1999 2005

1.0B

.6B

1.4B

$1.6B

.2B

02000 2001 2002 2003 2004

.8B

.4B

1.2B2,500

1,500

3,500

500

0

2,000

1,000

3,000

11: Net Dollar Savings and GWh Saved from Utility Efficiency ProgramsInvestor-owned utility efficiency programs

Result of CPUC reinstating utilitymarket decoupling mechanism.

Utility efficiency programs are now generatingmore return on investment—electricity savingsare growing while the cost of funding theseprograms is getting lower (Chart 11). In termsof dollars saved, the California EnergyCommission estimates that building andappliance standards alone have saved residentsand businesses $56 billion through 2003 andare to save another $23 billion by 2013.13

Additionally, projected savings resulting fromnew appliance efficiency standards adopted in2004 are expected to reduce consumer utilitybills by $3.3 billion during the first 15 yearsthey are in effect.14

During the failed electricity deregulation periodin the late 1990s, the California Public UtilitiesCommission (CPUC) did away with“decoupling,” the regulatory mechanism thatenables the State’s investor-owned utilities(IOUs) to promote and provide energyefficiency programs to their customers, withoutcutting into utility profits. The elimination ofdecoupling accounts for the significant drop-off in energy savings from 1998-2000. Theup-tick in 2001 occurred once the CPUCreinstated decoupling.

23

California may be in the early stage of the nextwave of green innovation. A similar confluenceof forces from the first wave may be at work,ushering in this next wave—including risingoil prices, state policies promoting energyefficiency and emission reductions, shiftingattitudes and behaviors regarding global warmingand new technologies such as alternative fuelvehicles, and increasing innovation in energytechnology areas.

There are signs that in recent years the adoptionof existing green products and practices inCalifornia has accelerated. There are also signsthat much higher levels of investment arepouring into energy technology innovation inCalifornia, that the State is producing a growingshare of patents in areas such as solar andwind technology, and that a conservativeestimate of green jobs in California now tops20,000—reflecting growth by about 50%over the last decade.

While it is too early to tell what this new wavemight ultimately look like, the California GreenInnovation Index intends to track signs ofchange in three key areas.

The environment for change.The next wave of green innovation will need asupportive environment if it is to buildmomentum. At its most basic, this means thatlarge numbers of Californians will need torecognize the nature and urgency of the problemof global warming—and to be receptive toinnovation as a way to solve the problem andbring economic benefits to the State.

The adoption of existing greenproducts and practices.Green innovation takes place when residents,businesses, and governments adopt existingproducts and practices to improve energyefficiency or increase energy alternatives inways that reduce greenhouse gas emissionsand generate economic benefits (e.g., financialsavings available for re-investment in moreproductive activities).

The creation of new greenproducts and services.Green innovation also takes place whenbusinesses create new products and servicesthat improve energy efficiency or increaseenergy alternatives in ways that reducegreenhouse gas emissions and generateeconomic gains (e.g., new companies, newjobs, public revenues). This kind of innovationcan serve the needs not only of the Californiamarket, but also those of the globalmarketplace, generating additional economicbenefits for the State.

the next wave3TRACKING SIGNS OF THE NEXT WAVE OF GREEN INNOVATION

24

RECOGNITION OF THE PROBLEM AND RECEPTIVITY TO INNOVATION

Californians recognize the urgency of the problem—and believe a lot can be done about it

As a component of the inaugural California Green InnovationIndex, Next 10 commissioned the 2007 Field/Next 10 GlobalWarming Survey of Californians - a survey of Californiaresidents on their understanding of global warming and thesteps they are taking and willing to take for the purpose ofstemming the impacts of climate change.

More so than Americans in general, Californians recognizethat global warming is very real, urgent, and is having or willhave serious negative impacts—including environmentalimpacts (coastlines, snow pack), economic impacts (agriculture,the broader California economy), and social impacts (health,overall quality of life). But Californians also believe that thegeneral public, industry, and others can do a lot to successfullyaddress the problem.

SURVEY RESULTS:Californians’ Views on Global Warming

51% of Californians have heard “a great deal” aboutglobal warming, compared with 42% of Americans overall.14

70% of Californians say that the issue of global warmingis “extremely” or “very” important to them, compared with52% of Americans overall.15

75% of Californians agree that some action should betaken to combat global warming, compared with 61% ofAmericans overall.16 Moreover, 43% of Californians agreethat “global warming has been established as a serious problemand immediate action is necessary”, compared with 28% ofAmericans overall.17

ENVIRONMENT FOR CHANGE

Large percentages of Californians believe global warmingis a “very serious” threat to the State’s economy (41%),overall quality of life (49%), coastal communities (51%),farmers in the Central Valley (53%), the State’s snowpackand water supply (63%), and the health of Californiansliving where air quality is poor, such as near freeways,ports and industrial sites (66%).

Large percentages of Californians believe that the followinggroups can do “a lot” to reduce global warming: majorcorporations (67%), gas and electric utility companies(63%), government (U.S. 56%, other countries 51%,state and local 49%), and clean energy companies (52%).

57% also believe that the general public (“peoplelike you”) can do a lot about reducing global warming,compared with 27% of Amer icans overall. 1 8

Californians believe that reducing emissionsand growing the economy is both possibleand desirable—and believe that new technologieswill help solve the problem

SURVEY RESULTS:Californians Believe We Can Reduce Emissionsand Grow the Economy at the Same Time

85% agree that California can reduce greenhousegases that contribute to global warming and expand jobsand economic prosperity at the same time. More thanhalf (54%) agree “strongly” with this statement.

77% agree that firms and government researcherswill develop new technologies to solve the problem ofglobal warming; 39% agree “strongly” with this statement.

25

12: GHG Emissions by Source – 2004Includes electricity imports and excludes international bunker fuels

41%

22%

21%

8%8% Transportation

Electrical Power

Industrial

Agriculture& Forestry

Others

Source: California Energy Commission, Inventory of California Greenhouse Gas Emissions and Sinks: 1990-2004. Staff Final Report. CEC-600-2006-013-SF. December 2006.

the next wave3ADOPTION OF GREEN PRODUCTS AND PRACTICESThe combination of actions by individuals,businesses and government leaders that comprisegreen innovation in the forms of technology,preferences and policy, has a compoundingeffect. To measure green innovation in termsof the adoption of green products and practices,we focus on vehicles, homes, and workplaces—the major users of energy and, directly orindirectly, the major drivers of greenhouse gasemissions. As illustrated in Chart 12,

transportation accounts for the highestpercentage of gross greenhouse gas emissions(41%). Businesses and residences, by virtue oftheir electricity use, also drive needs for bothin-state electricity generation and electricityimports—which together account for 22% ofgross emissions. In addition, industrial activitiesproduce 21% of gross GHG emissions. Thus,adoption of green products and practices inhomes, workplaces, and vehicles is critical tothe reduction of greenhouse gas emissions.

26

Californians areaccelerating theiradoption of greenproducts andpractices to reduceelectricityconsumption

13: Electricity Consumption in CaliforniaTrends relative to 1990

Inde

xed

to 1

990

Electricity Consumption by Sector2005

There are signs that Californians have begunto adopt a less energy-intensive lifestyle.Throughout the past 15 years, per capitaelectricity consumption has not increased inCalifornia. In fact, electricity consumption percapita has consistently been lower than 1990levels, with the exception of a spike in 2000(Chart 13).

1990 1991 1992 2005

100

110

Source: California Energy Commission; U.S. Census Bureau

Total

Per Capita

1993 1994 1995 1996

100

115

120

125

130

95

90

1997 1998 1999 2000 2001 2002 2003 2004

While electricity consumption relativeto 1990 levels continues to rise, percapita consumption (except for 2000)has remained below 1990 levels.

40%

34%

18%

8%Commercial

Residential

Industrial

Agriculture

Source: California Energy Commission

27

Our survey results show that the majority ofhomeowners in California are already adoptingor are planning to adopt specific electricitysaving products and practices. Data shows thatan increasing number of Californians arepurchasing energy efficient light bulbs—evenmore so than in the rest of the country. Since2002, the share of Compact Fluorescent Lamps(CFLs) purchased in California has been steadilyon the rise. Although in 1999, the share of CFLspurchased was less than 1% in both Californiaas well as the rest of the U.S., in 2005, the shareof these energy efficient light bulbs purchasedin California was over double that of the restof the U.S. (Chart 14).

Energy Star Appliances are becomingincreasingly more pervasive in the Californiamarket. In 2005, approximately 90% of thedishwashers purchased in California were EnergyStar qualified. The adoption of green productsis helping Californians to reduce electricityconsumption, thereby also contributing to areduction in electricity bills (Chart 15).

the next wave3

SURVEY RESULTS:Large Percentages of Californians are adopting and planningto adopt specific electricity saving products and practices.

Already Likely in ConsideringBehavior Doing Coming Year For Future

Turn off computers, etc. 93% 3% 2%

Adjust heating/AC to save energy 84% 3% 2%

Buy/use CFL or LED bulbs 76% 10% 7%

Buy/use Energy Star appliances* 84% 6% 9%

Install water-saving devices* 76% 5% 12%

Insulate home, water heater, etc.* 75% 6% 12%

(* Share of homeowners only)

28

1999 2000 2001 2002 2003 2004 20050%

2%

4%

6%

8%

14: Market Share of CFL Light BulbsShare of CFLs purchased as a percent of all medium screw-based lamps

1998 2000 2001 2002 2003 2004 20050%

20%

40%

60%

100%

15: California Market Share of Energy Star Appliances

1999

80%

Title 20Appliance Efficiency StandardsIn 1980, the California Energy Commissionwas granted the right to adopt efficiencystandards for appliances. These standards, underthe California Code of Regulations, coverrefrigerators, freezers, washing machines, airconditioners and lighting.

Title 24California Building StandardsThe Energy Efficiency Standards for Residentialand Nonresidential Buildings were establishedin 1978 in response to a legislative mandate toreduce California's energy consumption.Periodically updated to allow for new energyefficiency technologies and methods, thesestandards include minimum requirements forbuilding insulation as well as heating, ventilating,air conditioning, and water heating equipment.California Energy Commission

Source: California Measurement Advisory Council (CALMAC)

California

Source: California Measurement Advisory Council (CALMAC)

Rest of US

Dishwashers

Refrigerators

Clothes Washers

29

29

1980 20030

0.4

0.8

1.2

2.4

16: Office Building Electricity ConsumptionConsumption per Square Foot

1.6

2.0

1990 2000 2001

0

30%

17: Commercial Office Building Electricity Consumption By Industry

-15%

25%

20%

15%

10%

5%

-10%

-5%

1980-1990

1990-2003

SURVEY RESULTS:Californians are reporting that theiremployer encourages specific behaviorsto improve energy efficiency

25% of working Californians say theiremployer provides incentives to employees totake public transit, work from home, or purchasehybrid, electric, or alternative fuel vehicles.

35% of working Californians say theiremployer has provided information about waysto conserve energy and reduce greenhouse gasemissions at the workplace.

Although the electricity intensity of thecommercial business sector increased between1980 and 1990, over the course of the followingdecade it has made gradual progress in becomingmore energy efficient (Chart 16). Overall,commercial electricity consumption per squarefoot declined slightly from 1990-2003 (Chart16). Looking at commercial sector electricity

consumption by industry shows that specificindustries have been making considerable stridesin reducing electricity use (Chart 17). Whilekey industry sectors such as retail, restaurants,food stores, and large offices experiencedsubstantial reductions in energy consumption,the commercial sector still has much potentialto become more energy efficient, as other keysectors continue to consume more electricity.

The commercialbusiness sector–the largestconsumer ofelectricity inCalifornia–has become moreenergy efficient inrecent years

Source: California Energy Commission

GW

h pe

r S

quar

e Fo

otP

erce

nt C

hang

e in

Ele

ctric

ity C

onsu

mpt

ion

per S

quar

e Fo

ot

Source: California Energy Commission

LargeOffices

1,075

All OtherBuildings

1,052

Retail

948

Warehouses

779

Schools

457

SmallOffices

354

Colleges

287

Hospitals

285

Hotels/Motels

284

FoodStores

247

Restaurants

163

RefrigeratedWarehouses

47TotalSq. Feet

(millions ofsquare feet)

the next wave3

30

1970100

90

120

130

18: Petroleum Consumption in CaliforniaTrends relative to 1970

1975

160

80

110

140

150

20041980 1985 1990 1995 2000

2000100

98

104

106

19: Gas Sales in CaliforniaTrends relative to 2000

2001

110

102

108

20062002 2003 2004 2005

199710M

20M

25M

20: Registered Vehicles and Emissions – California

1998

30M

15M

20051999 2000 2001 2002 2003 2004

600

0

500

400

300

200

100

To meet the needs of a rapidly growingpopulation in California, total consumption ofmany resources, including petroleum, has beengrowing accordingly. While there has been anincrease in total petroleum consumption, since

Gasoline salesand vehicle milestraveled haveleveled off

the 1980s per capita consumption has droppedbelow 1970 levels (Chart 18). Other observabletrends include the leveling off of gas sales since2004 relative to 2000 (Chart 19) and thecontinued increase in total CO2 emissions andnumber of vehicles (Chart 20).

While total petroleum consumption relativeto 1970 has continued to rise, per capitaconsumption since the 1980s has remainedbelow levels in 1970.

Total Consumption

per Capita Consumption

Inde

xed

to 1

970

Inde

xed

to 2

000

Total Gas Sales

Gas Sales per Capita

Source: Energy Information Administration, U.S. Census Bureau

Source: California Board of Equalization; U.S. Census Bureau

CO2 Emissions

CA Entire Vehicle Fleet

Tota

l Num

ber

of V

ehic

les

– in

Milli

ons

Source: California Air Resources Board

Thou

sand

s of

tons

of C

O2

emis

sion

s pe

r da

y

31

1995 1996 1997 1998 1999 2000 200598

102

104

106

114

21: Vehicle-Miles TraveledCalifornia & Rest of U.S., Per Capita trends relative to 1995

108

110

112

2001 2002 2003 2004

100

1995 1996 1997 1998 1999 2000 200580

100

110

120

160

22: California VMT & Gas PricesPer Capita trends relative to 1995

130

140

150

2001 2002 2003 2004

90

Source: U.S. Department of Transportation, Federal Highway Administration, Highway Statistics;California Department of Transportation Califorrnia Motor Vehicle Stock, Travel and Fuel Forecast

California

Rest of U.S.

Inde

xed

to 1

995

Vehicle-miles traveled (VMT) per capita havebegun to decrease since 2002, showing thatCalifornians are driving shorter distances onaverage. In the rest of the U.S., however, VMTper capita has grown much faster (Chart 21).

While there are signs that rising gas prices canimpact gas consumption, Chart 22 illustratesthe relative inelasticity of demand for gas inthe State as the rate of price increases far outpacethe drop in consumption. Gas prices alonehave not brought about change in behaviors.

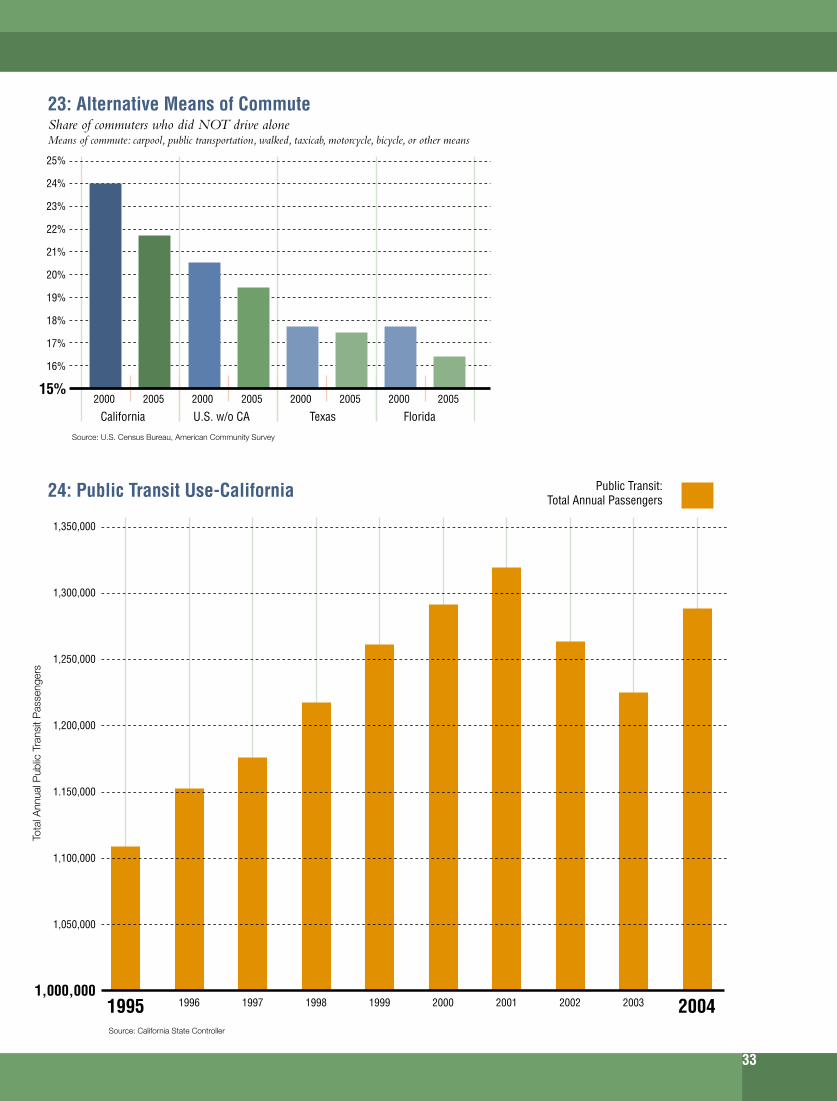

Although the share of the population usingalternative means of commute has beendecreasing in California and the rest of the U.S.alike (Chart 23), Californians are less likely todrive alone than other Americans. Over thepast decade, there has been a long-term trendof growing public transit use. Though dippingwith the economic contraction in 2002 and2003, transit ridership in 2004 was back tolevels seen in 2000 (Chart 24).

* Inflation adjusted to 2005 dollarsSource: U.S. Department of Transportation, Federal Highway Administration, Highway Statistics;

Enegy Information Administration, Petroleum Marketing Annual; California Department of Transportation,Califorrnia Motor Vehicle Stock, Travel and Fuel Forecast

Inde

xed

to 1

995

California VMT

CA Gas Prices

the next wave3

32

Tota

l Ann

ual P

ublic

Tra

nsit

Pas

seng

ers

200015%

19%

20%

21%

25%

23: Alternative Means of CommuteShare of commuters who did NOT drive aloneMeans of commute: carpool, public transportation, walked, taxicab, motorcycle, bicycle, or other means

22%

23%

24%

18%

17%

16%

2005 2000 2005 2000 2005 2000 2005

1,250,000

1.150,000

1,350,000

1,050,000

1,000,000

1,200,000

1,100,000

1,300,000

1995 1999 2004Source: California State Controller

2000 2001 2002 2003

24: Public Transit Use-California Public Transit:Total Annual Passengers

199819971996

Source: U.S. Census Bureau, American Community Survey

California U.S. w/o CA Texas Florida

33

California Energy Commission. 2005. California’s Water-Energy Relationship,Final Staff Report. Publication CEC-700-2005-011-SF (November 2005),Page 8.

California Electricity Use, 2001

Electricity (GWh)Total Water Pumping Electricity Use*5,500Total Water Related Electricity Use**48,012Total Electricity Use**250,494* See Chart 26, for year 2001.

California Energy Commission. 2005. California’sWater-Energy Relationship, Final Staff Report.Publication CEC-700-2005-011-SF (November2005), Page 9.

0

40,000

25: Water Consumption by SectorCalifornia

35,000

30,000

25,000

20,000

15,000

10,000

5,000

Thou

sand

Acr

e Fe

et

Water Consumptionin California - 2003Share of Water Use by Sector

Agricultural

Residential

Commercial 3%Landscape 3%

Industrial 1%

Source: California Department of Water Resources

1998 1999 2000 2001 2002 2003Agricultural Residential Commercial Industrial Landscape

16%

77%

the next wave3California’s water system accounts forapproximately 20% of the State’s gross electricityuse.20 Depicted in Chart 25, agricultural wateruse makes up almost 80% and residential 16%of total water use in California. In 2003(the most recent year available), total waterconsumption was lower than in the threepreceding years.

Conveyance of water across the state in 2001accounted for 11% of total electricity use relatedto water.21 Water use in California is particularly

energy-intensive because much of the State’swater demand is located far away from availablesources, and the process of moving the water(pumping) results in high energy costs.According to the Energy Commission, “Nearly70 percent of the state’s total stream runoff isnorth of Sacramento, but 80 percent of thewater demand is south of Sacramento.”21

Reducing consumption and improving theefficiency of California’s water-use system wouldyield high energy savings and thereby reducegreenhouse gas emissions.

Water consumptionand pumping—responsible forabout 20% ofCalifornia’s grosselectricity use—are using lesselectricity thanin the past

34

California Energy Commission. 2005. California’sWater-Energy Relationship, Final Staff Report.Publication CEC-700-2005-011-SF (November2005), Page 9.

1990 1996 1997 1998 1999 2000 20050

2500

3000

4500

3500

4000

2001 2002 2003 2004

2000

26: Energy Use Through Water PumpingCalifornia

1500

1000

500

19951994199319921991

Source: California Energy Commission

GW

h

Agricultural Water Pumping

Urban Water Pumping

Los Angeles’s Water Conservation SuccessPrompted by the drought of 1987-1992, the City of Los Angeles hasinvested over $100 million in conservation measures over the last decade.Even with steady population growth, these measures have slowed annualaverage demand growth from 2.1% in the pre-conservation period to1.3% projected over the next 20 years. Conservation efforts include apublic awareness program and education campaign that have resultedin the widespread installation of low-flow hardware devices (e.g. toiletsand showerheads) and change in use habits. Additionally, the City isimplementing water recycling for non-potable uses such as landscapingand industrial uses.Los Angeles Department of Water & Power

From 2004-2005, California reduced electricityuse attributed to water pumping, for both urbanand agricultural uses (Chart 26). In addition,public sector initiatives have been establishedto improve water efficiency through fundingprojects and research for new technology, suchas water recapture.

35

0

50,000

28: California Renewable Portfolio StandardActual and Forecasted RPS Generation from Investor-Owned Utilities (IOUs)

40,000

20,000

GW

h

10,000

30,000

0

35,000

27: Renewable Energy Generation in CaliforniaGigawatt hours by source

30,000

15,000

25,000

20,000

GW

h

10,000

5,000

In recent years, many steps have been taken toincrease the generation and procurement ofrenewable energy. From 2002 to 2006, totalrenewable energy generation in the State grewby 8%, with growth primarily in windgeneration23 (Chart 27). Over this period,electricity generation from renewable sourceshas accounted for 11% of California’s totalelectricity generation.

In 2002, the Renewable Portfolio Standard(RPS) was established to ensure that Californiansuse cleaner energy. Since the RPS wasintroduced, investor-owned utilities (IOUs)have been procuring a larger share of renewableenergy (Chart 28). As old contracts expire,the IOUs have new renewable energy contractsin the pipeline to help them attain the RPS targetof 20% renewable energy generation by 2010.

Californians areincreasing theiruse of cleanerenergy to reducegreenhouse gasemissions bothat home andon the road

*Note: Review of the 2007 bids is ongoing at each IOU, with sellers due to be notified in late June or early July as to whether their bids have been short-listed. The IOUs will then enter into negotiations withthose short-lived bidders who agree to post a deposit and withdraw any conflicting offers they had made to other solicitors. Negotiations will continue through 2007, and any resulting RPS contract should befilled with the CPUC for approval by the end of the year. Some of the short-listed bids may not receive contracts, but many represent viable projects that may receive contracts and contribute to the 2010 goal.Source: California Energy Commission

2003Pre-2002 Contracts

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Target:20% of ExpectedIOU Retail Sales

2002 Contracts

2003 Contracts

2004 Contracts

2005 Contracts