caiib super notes: bank financial management: module d: balance sheet management: asset...

TRANSCRIPT

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Asset Classification and Provisioning Norms

Module D: Balance Sheet Management

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

CAIIB – SUPER NOTES

Bank Financial Management: Asset Classification and Provisioning Norms

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Contents

Coverage:

1. Introduction

2. Asset Classification

3. Provisioning Norms

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

INTRODUCTION

1.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Introduction

• If bank is not able to get/recover interest from the

counterparty within reasonable time, then the income should

not be accounted for or recognised, till it is actually received.

• Accounting for interest is changed from accrual basis to

mercantile one

• Asset is tagged non-performing

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

ASSET CLASSIFICATION

2.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Narsimham Committee

• Committee on the Financial System chaired by M. Narsimham

• August 1991

• Recommendations:

– Bank balance sheets should be transparent and compliant with

international accounting standards

– Uniform accounting practices should be adopted

– Prudential norms for income recognition, asset classification and

provisioning introduced by RBI based on the recommendations

– Income recognition policy should be objective and based on record of

recovery

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Non-Performing Assets: Definition

• Interest and/or installment of principal remain overdue for a period

of more than 90 days in respect of a term loan

• Account remains ‘out of order’ in respect of an Overdraft/Cash

Credit

• Bill remains overdue for a period of more than 90 days in the case

of bills purchased and discounted

• Installment of principal or interest thereon remains overdue for:

– 2 crop seasons for short duration crops

– 1 crop season for long duration crops

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Non-Performing Assets

• Only if interest charged during any quarter is not serviced fully

within 90 days from the end of the quarter

• ‘Out of Order’

– Outstanding balance remains continuously in excess of the sanctioned

limit/drawing power

– No credits continuously for 90 days

– Credits not enough to cover interest debited during the period

• ‘Overdue

– Amount not paid on due date fixed by the bank

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Income Recognition

• Process to be objective and based on record of recovery

• Interest on advances against term deposits, NSCs, IVPs, KVPs and

life policies may be taken to income account on the due date,

provided adequate margin is available

• Fees and commissions earned by the bank as a result of

renegotiations or rescheduling of outstanding debts should be

recognized on accrual basis

• For govt. guaranteed advances also the interest on advances should

not be taken into account unless realised

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Income Recognition contd.

• In case of Funded Interest accounts also income recognition should be on

cash basis. Funding of interest in respect of NPAs, if recognised as income,

should be fully provided for

• In case of conversion into Equity, Debentures or any other instruments:

– If interest amount is converted and income is recognised full provision should be

made

– In case of conversion to quoted equity , such equity must be classified as “available

for sale” category

– In case of conversion of principal/interest to debentures, the debentures should be

treated as NPAs ab initio and provision made. Also applies to 0 Coupon Bonds

• Income should be recognised on realisation basis

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Reversal of Income

• Interest accrued and credited to income account in the

corresponding previous year should year should be reversed

or provided for if same is not realised. For govt. guaranteed

accounts also.

• Fees, commission and similar income shall cease to accrue

and should be reversed or provided for with respect to past

periods if uncollected

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Leased Assets

• Finance charge component of finance income accrued and

credited to income account and remaining unrealised should

be reversed or provided for

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Appropriation of recovery in NPAs

• May be taken to income account provided the credits are not

out of fresh/additional credit facilities

• Uniform and consistent process should be followed by the

bank

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

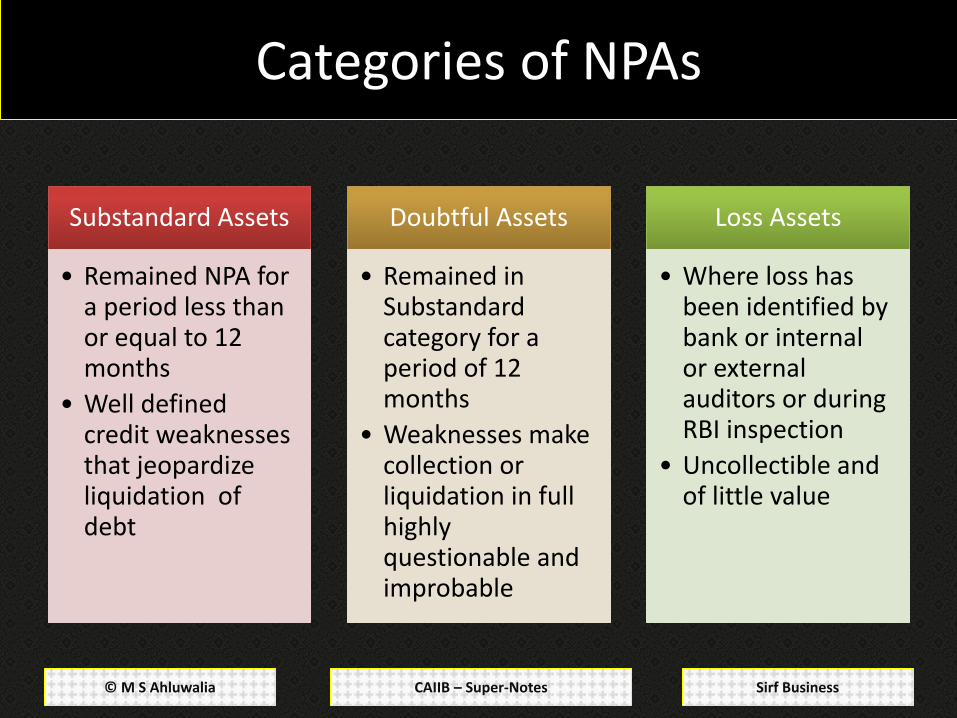

Categories of NPAs

Substandard Assets Substandard Assets

• Remained NPA for a period less than or equal to 12 months

• Well defined credit weaknesses that jeopardize liquidation of debt

Doubtful Assets Doubtful Assets

• Remained in Substandard category for a period of 12 months

• Weaknesses make collection or liquidation in full highly questionable and improbable

Loss Assets Loss Assets

• Where loss has been identified by bank or internal or external auditors or during RBI inspection

• Uncollectible and of little value

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

90 days Out of Order/Overdue: Non-Performing

Asset

90 days Out of Order/Overdue: Non-Performing

Asset

12 Months NPA: Substandard

Asset

12 Months NPA: Substandard

Asset

12 Months Substandard:

Doubtful Asset

12 Months Substandard:

Doubtful Asset

Loss has been identified: Loss

Assets

Loss has been identified: Loss

Assets

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Upgradation of NPA accounts

• If arrears of interest and principal are paid by the borrower

• May be classified as ‘Standard’ account

• When account regularised near the Balance sheet date:

– Should be handled with care

– If account indicates inherent weakness the account should be deemed

NPA

– Other cases bank must furnish to Statutory Auditors/Inspecting

Officers about manner of regularisation of account

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Other Important Points

• Borrower Wise Classification and not account/facility wise

• Advances against Term Deposits, NSCs, KVP/IVP etc need not be

treated as NPAs

• Accounts with potential threats for recovery on account of erosion

in the value of security or non-availability of security or frauds

committed by borrowers – such cases of serious credit impairment

should immediately be classified as doubtful or loss asset

• Accounts with temporary deficiencies should not be classified as

NPA

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

NPA Classification Norms

• Advances under Consortium Arrangements

– Based on record of recovery for the individual member banks

• Loans with Moratorium Period for payment of interest

– Become overdue after due date for payment of interest, if uncollected

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

PROVISIONING NORMS

3.

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Norms Lo

ss A

sset

s Lo

ss A

sset

s Should be written off

If not written off, 100% provision

Should be written off

If not written off, 100% provision

Do

ub

tfu

l Ass

ets

Do

ub

tfu

l Ass

ets 100% of the extent to

which advance is not covered by realisable value of security

For secured portion, depending on period for which advance has remained in doubtful category:

• < 1 yr: 20%

• 1-3 Years: 30%

• > 3 yrs: 100%

100% of the extent to which advance is not covered by realisable value of security

For secured portion, depending on period for which advance has remained in doubtful category:

• < 1 yr: 20%

• 1-3 Years: 30%

• > 3 yrs: 100%

Sub

stan

dar

d A

sset

s Su

bst

and

ard

Ass

ets 10% of Total

outstanding

For ‘unsecured exposures’ additional 10%, i.e., 20%

10% of Total outstanding

For ‘unsecured exposures’ additional 10%, i.e., 20%

CAIIB – Super-Notes © M S Ahluwalia Sirf Business

Do you have any questions or queries or some feedback to give?

Just mark an email to [email protected]

CAIIB – Super-Notes © M S Ahluwalia Sirf Business For more Super-Notes: Click Here

M S Ahluwalia, amongst other things, is a visual artist, blogger,

blog designer and of course an MBA and Banker from New

Delhi, India.

To know more about him you may visit his blog-site: Estudiante De La Vida