“c t d d h h c“cargo trends and what the cargo …€œc t d d h h c“cargo trends and what the...

TRANSCRIPT

“C T d d h h C“Cargo Trends and what the Cargo Executives think will shape the

revenue recovery in 2010”revenue recovery in 2010

M Nik HMr. Niko Herrmann, Partner, Oliver Wyman

6

S t d bSupported by:

March 2010

“Vi f th T ”“View from the Top”Global Air Cargo CEO Survey

Niko Herrmann, Partner

C O N F I D E N T I A L | www.oliverwyman.com

Survey ParticipantsWe targeted the top 50 cargo-carrying airlines as well as key industry players and got an outstanding 50% response rate

Participants by region Participant characteristics

3%3%Europe

Russia

Participants by regionAfrica

Participant characteristicsStrong coverage of global leaders in air cargo– 60% of top 10

North America

36%16%

6%3%3%

Latin America

– 60% of top 10– 55% of top 20– 36% of top 50– overall more than 30 surveys and

America

17%

– overall, more than 30 surveys and interviews

Even split between16% ll i

19%17%

Asia

Middle East

– 16% all-cargo carriers– 32% belly carriers– 52% combination carriers

8© Oliver Wyman www.oliverwyman.com

Asia

The recovery (1/4)Cautious confidence is the prevailing assessment of early signs of recovery in the cargo market

Confidence: Concerns:“Recovery is still fragile”“Low growth on low base”“While the growth begins, 2010 will be a

“We are out of the worst”

“Upswing will last, but will be modest”

year during which things settle”Unstable economies in some European countries are having a negative effect on an otherwise positive outlook

“Strength of upswing will differ across regions – Asia will lead“

Q4 2009 was strong, short-term on an otherwise positive outlook“Consumer behavior has changed to saving rather than spending, confidence still unstable, as jobless rates soar”

g,inventory replenishment”

“2010 seems to continue as end of 2009 with strong traffic levels”

“Pressure on yields will continue, extremes of Dec 09 unsustainable”“I don’t see any economic reasons for a

b thi ”

9© Oliver Wyman www.oliverwyman.com

cargo boom this year”

The recovery (2/4)Not surprisingly, most CEOs are still somewhat cautious about the recovery for the overall cargo market…

Q: Do you expect a lasting positive trend for the air cargo industry?

39%

55%Percent of replies

39%

6%

Current rebound is No substantial growth, Lasting temporary, relapse into a recession in 2010 is likely

but also no further decline in 2010

upswing for air freight in 2010

“I think the global economy still has to recover; while growth will begin, 2010 will still be a

10© Oliver Wyman www.oliverwyman.com

I think the global economy still has to recover; while growth will begin, 2010 will still be a year during which things settle.”

The recovery (3/4)… but are substantially more bullish when looking at their own business!

Q: How do you see your business developing in 2010? Much betterBetter

Percent of replies

0%

SameWorse

40%23% 16% 10%

0%

86% “better”

43%67%55% 76%

86% better or “much better”

17%26%

10%4%3%0% 10%

Volume Yields Costs Margins

11© Oliver Wyman www.oliverwyman.com

Volume Yields Costs Margins

The recovery (4/4)94% of CEOs expect to reach 2007 revenue levels again before 2013 – much sooner than reported in most of the trade press

Q: When do you expect to reach again revenue levels as in 2007?

48%

Percent of replies

38%

3%3%7%

2010 2011 2012 2013 2014+

12© Oliver Wyman www.oliverwyman.com

94%

Where the volume growth will come fromUnsurprisingly, CEOs expect the highest growth to come from from AsiaMarket growth expectations by region (distribution of answers)

+ ++o---

China & North Asia !

Asia Pacific

Latin America

!

!

Russia / CIS

Africa

!

!

!

MENA

Europe

North America

!

!

!

13© Oliver Wyman www.oliverwyman.com

MENA !

! = expected future sales push= distribution of answers, total = 100%

Yield – a more tepid recoveryFor yield recovery, the expectations are more or less evenly distributed between flat and moderate growthYield growth expectations by region (distribution of answers)

China & North Asia

+ ++o---

Asia Pacific

Latin America

Russia / CIS

Africa

MENA

Europe

North America

14© Oliver Wyman www.oliverwyman.com

MENA

= distribution of answers, total = 100%

Crisis strategies Customer first? Only 1/3 of participants explicitly mentioned customers as the focus of their recovery strategies

Strategies to fight the crisis (as mentioned by: percent of participants)

Productivity improvement

Network management

67%

47%Network management

Fixed cost reduction

47%

43%

40%Capacity reductions

Product portfolio changes

40%

37%

37%Customer initiatives

Pricing/Yield Management

33%

30%

15© Oliver Wyman www.oliverwyman.com

Products Cold Chain and Pharma are widely expected to lead the recovery in both volume and yieldGrowth expectation by product category (average)

+ ++o-

Cold Chain

Express

Pharmaceuticals

Perishables

Electronics / IT

Valuables

General Cargo

Volume

16© Oliver Wyman www.oliverwyman.com

Mail Yield

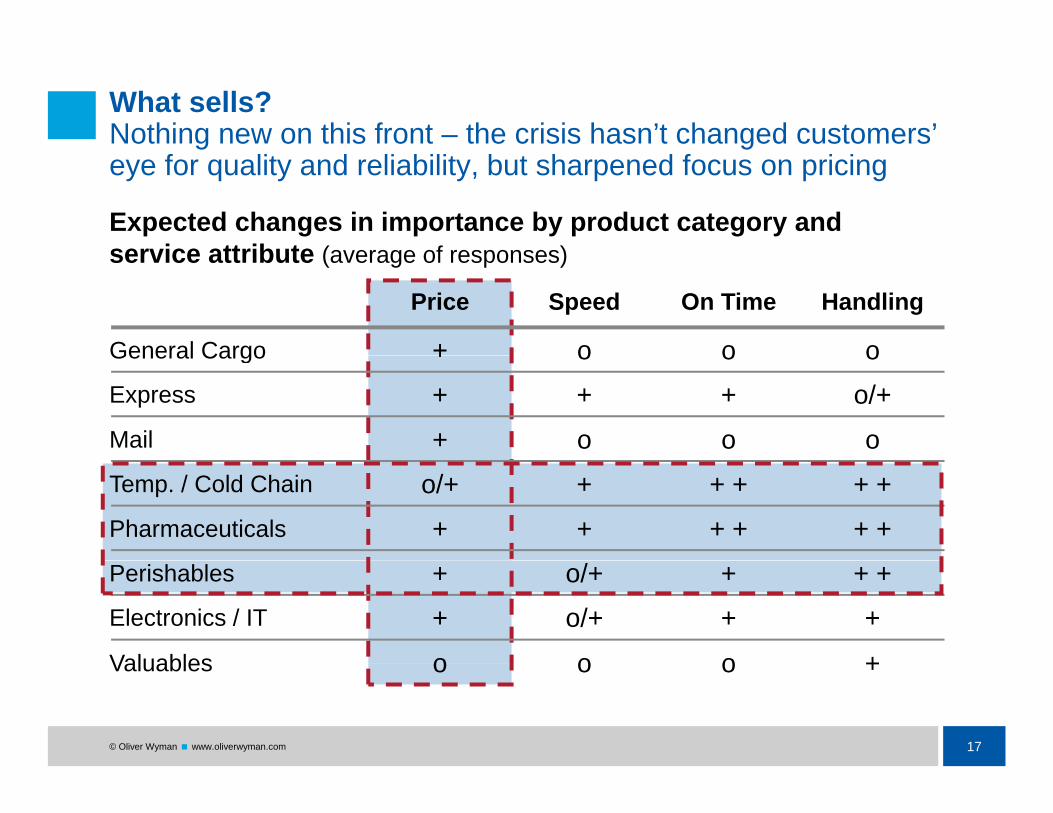

What sells?Nothing new on this front – the crisis hasn’t changed customers’ eye for quality and reliability, but sharpened focus on pricing

Expected changes in importance by product category and service attribute (average of responses)service attribute (average of responses)

General Cargo

Price Speed On Time Handling

+ o o oGeneral Cargo

Express

+

+

+

o

+

o

o

+

o

o

o/+

oTemp. / Cold Chain o/+ + + + + +Pharmaceuticals + + + + + +Perishables + o/+ + + +

Valuables o o o +

Electronics / IT + o/+ + +

17© Oliver Wyman www.oliverwyman.com

Valuables o o o +

Investments E-freight remains the No. 1 investment priority – with Security and Cold Chain capabilities following somewhat closely

Important innovations for competitiveness? Short-term invest focus

E-freight

+++o

67%

Percent of respondents

Security improvements

Cold chain capabilities

40%

43%

Enhanced traceability

CO2 emission reduction

37%

30%

Lightweight containers

Special handling facilities

40%

27%

18© Oliver Wyman www.oliverwyman.com

Green warehouses 20%

Competition from oceanThe slowdown of supply chains has shown viable alternatives to customers – not all of this is likely to reverse again

Q: Do you expect a lasting change in customer decision behavior?

64% 71%

Percent of replies (multiple answers possible)

11%11%

Expect customers to be even more price

Customers will more carefully evaluate the

Customer behavior will be no different than p

sensitive in the future y

benefit of air transport before the crisis

“With the advantages of good speed and reliability, ocean shipping is expected to ti th i l tl titi ith i A id bl ti f t i

19© Oliver Wyman www.oliverwyman.com

continue their relentless competition with air cargo. A considerable portion of current air cargo volume is predicted to go ocean in the future.”

Airline responseThe search continues for lasting high-yield niches

Q: How do you intend to change your product portfolio?

68%61%

Percent of respondents (multiple answers possible)

14%14%

Strengthening of premium products (e g

Increase of value added products (e g time-

Reduction of portfolio complexity purepremium products (e.g.

express / valuables)products (e.g. time-definite, guaranteed)

complexity, pure commodity service

“The air cargo market has matured, and efforts are required to meet customer needs d i th titi Th f th h f hi h fit d t (f

20© Oliver Wyman www.oliverwyman.com

and survive the competition. Therefore, the share of high-profit products (frozen, refrigerated, express, pharmaceuticals, etc.) will expand.”

Forwarder relationshipsSome resentment, some realizations, but mostly the professional partnerships survived the acrimony of the crisis

Relationship quality (distribution of answers)

36%

18%18%

28%

Established new partnerships with different forwarders

Focus on the key forwarders has helped forge

deeper relations

Relations have deteriorated as

forwarders squeezed airlines

Relationships remained

unchanged with our key partners

21© Oliver Wyman www.oliverwyman.com

p qharder

y p

Industry consolidation (1/2)Most CEOs expect a tough consolidation as a result of the crisis, but are actively pursuing partnerships in the near termExpectations of participantsPercent of respondents

Planned activityPercent of respondents

Increased

Percent of respondents (multiple answers possible)

Actively

Percent of respondents

Increased M&A 52% looking for

M&A

Actively

20%

More alliances/ partnerships

39%

Actively looking for alliances/partnerships

48%

Increased vertical integration

32%No activity planned 32%

22© Oliver Wyman www.oliverwyman.com

integration

Industry consolidation (2/2)The industry is further polarizing into fewer, larger carriers that have the financial, network, and experience strength to survive

Opportunities and Threats pp“CX-CA will be mega-deal”

“Most small niche freighter carriers will become extinct, not sustainable through economic cycles”through economic cycles

“Partnerships with integrators are way forward – DHL very active, what about UPS and FedEx?”

“Th i d t i tti f i l ll l ill it“The industry is getting more professional, smaller players will exit as financing gets tougher, customer demand stronger service”

“Alliances are a key component for a smaller airline’s expansion”

23© Oliver Wyman www.oliverwyman.com

Future of freighter operatorsConsolidation will be especially focused in the area of freighters

Q: What does the future for freighter versus belly cargo look like?

81%

Percent of respondents (multiple answers possible)

7%22%

Only a small number of strong, global freighter operators will remain.

More belly carriers will enter into the freighter

business

More small cargo-only airlines will likely evolve along dedicated traffic

lanes

24© Oliver Wyman www.oliverwyman.com

lanes

Larger freightersMore than half the operators intend to focus future fleet decisions on larger aircraft, e.g., B777F or B747-8F

Future fleet decisions (n=20)Future fleet decisions (n 20)

Focus on smaller, midsize freighters 16%

No major

freighters

F l56%

8%

20%changes planned

Focus on large freighters

8%

Reduction of number of f i ht i ft

25© Oliver Wyman www.oliverwyman.com

freighter aircraft

Green cargoETS is perceived primarily as an added cost to be passed on

ETS change to air cargoPercent of respondents

Perceived advantagePercent of respondents

Impact on fleet decisions

p(multiple answers possible)

p

Decreased competitivenessdue to increased cost pressure / fleet disadvantagefleet decisions,

focus on fuel efficiency

Declining

71%13%

g

Declining margins, as carriers can't forward costs

29%87%

Accelerated consolidationdue to rising 19%

Increased competitiveness due to young fleet and already green business model

26© Oliver Wyman www.oliverwyman.com

gcost pressure business model

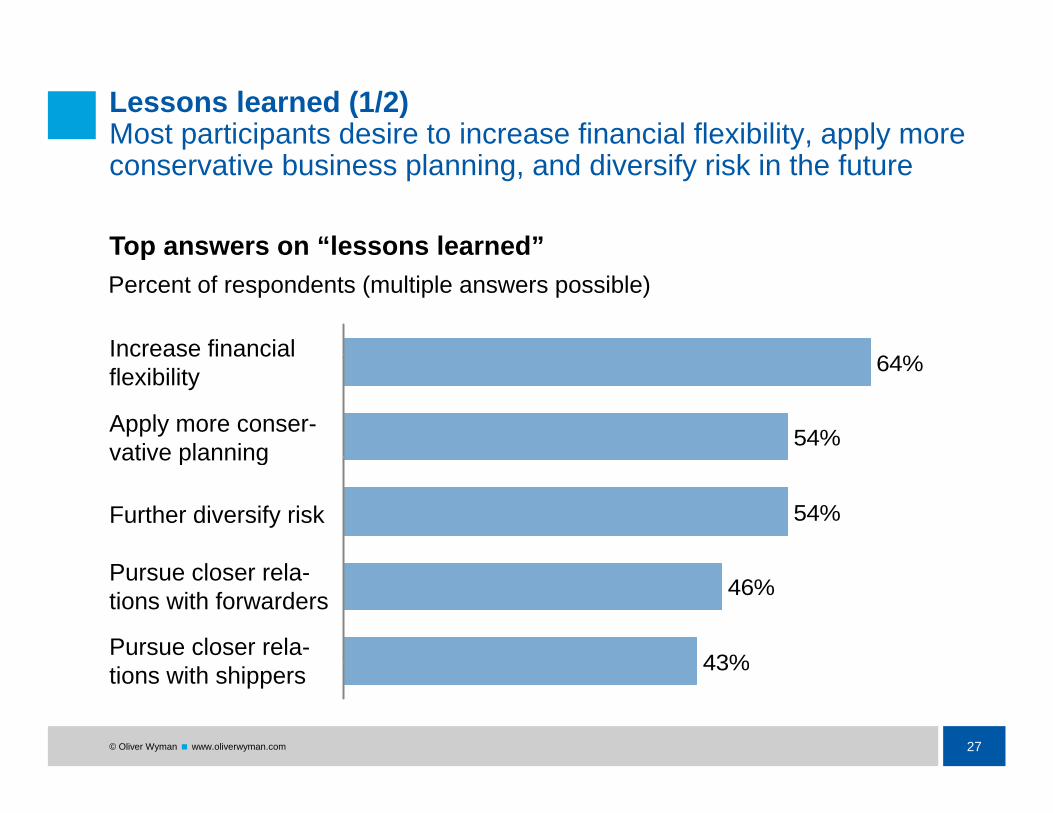

Lessons learned (1/2)Most participants desire to increase financial flexibility, apply more conservative business planning, and diversify risk in the future

Top answers on “lessons learned”Top answers on lessons learned

Increase financial 64%

Percent of respondents (multiple answers possible)

Apply more conser-vative planning

Increase financial flexibility 64%

54%vative planning

Further diversify risk 54%

Pursue closer rela-tions with forwarders 46%

43%Pursue closer rela-

27© Oliver Wyman www.oliverwyman.com

43%tions with shippers

Lessons learned (2/2)Speed is key in reacting to a crisis of such magnitude

Comments“Decisive and fast reaction has been key; opportunistic dithering has cost many carriers millions”

“We're strengthening our risk management practices by setting up processes to perceive danger signs in advance and take prompt action at an appropriate time.

“Creativity and flexibility in internal processes are organizational capacities that need to be acquired – best before the next crisis”

“The industry needs to unite again on key issues; everyone was desperately fighting on their own, need to get more active as a group again”

“In order to add value, express cargo such as door-to-door is going to be important. To make this come true, cooperation between carries will be a significant factor. “

28© Oliver Wyman www.oliverwyman.com

Obstacles Will air cargo achieve a fast return to sustainable industry profitability?

The biggest obstacles in our industry are still…

Commoditization of air freight and 84%

Percent of respondents (multiple answers possible)

air freight and competitive pressure

Increasing cost

84%

55%burden or regulation

Lack of appropriate tools and techniques

55%

42%qto manage margin

Lack of talent in the industry

42%

19%

29© Oliver Wyman www.oliverwyman.com

industry 19%

Conclusion

Industry expects cautious “return to normal”

The environment is getting increasingly tough especially for carriers whoThe environment is getting increasingly tough, especially for carriers who once thought cargo could easily “de-risk” P&L and B/S– How to become more nimble and flexible and responsive ahead of the

next downturn?

More carriers start to think whether they have the critical mass and the market/network strength to get the best out of their capacity– Adam Smith – should you continue to be involved in air cargo?y g

What can you do to escape continued commoditization?– Value-added products become the new commodity – how to differentiate

your product portfolio?your product portfolio?– Specific bilateral partnerships will be increasingly important – who to

work with? Under what economic/operating model?

30© Oliver Wyman www.oliverwyman.com

31© Oliver Wyman www.oliverwyman.com