by grace joy gakii

TRANSCRIPT

EFFECT OF WORKING CAPITAL MANAGEMENT IN THE

PROFITABILITY OF SMALL AND MEDIUM ENTERPRISES:

A CASE STUDY OF RETAIL OUTLETS AT TWO RIVERS MALL

BY

GRACE JOY GAKII

UNITED STATES INTERNATIONAL UNIVERSITY-AFRICA

SUMMER 2020

THE EFFECT OF WORKING CAPITAL MANAGEMENT IN THE

PROFITABILITY OF SMALL AND MEDIUM ENTERPRISES:

A CASE STUDY OF RETAIL OUTLETS AT TWO RIVERS MALL

BY

GRACE JOY GAKII

A Research Project Report Submitted to the Chandaria School of Business in Partial

Fulfilment of the Requirement for the Degree of Masters in Business Administration

(MBA)

UNITED STATES INTERNATIONAL UNIVERSITY-AFRICA

SUMMER 2020

ii

STUDENT’S DECLARATION

I, the undersigned, declare that this is my original work and has not been submitted to any

other college, institution, or university other than the United States International

University Africa for academic credit.

Signed ____________________________ Date _________________________

Grace Joy Gakii (ID No: 655885)

This research project report has been presented for examination with my approval as the

appointed supervisor.

Signed ____________________________ Date _________________________

Dr. George Achoki

Signed ____________________________ Date _________________________

Dean, Chandaria School of Business

iii

COPYRIGHT

Copyright © Grace Joy Gakii, 2020

All Rights Reserved

iv

ABSTRACT

The purpose of the study was to determine the effect of working capital management on

the profitability of Small and Medium Enterprises (SMEs). The study sought to answer

the following research questions; How does inventory management practices affect

profitability of SMEs at Two Rivers Mall? What is the effect of receivables management

practices on the profitability of SMEs at Two Rivers Mall? and, How does payables

management practices affect profitability of SMEs at Two Rivers Mall?

The research design applied in this study was descriptive research design. This research

design was used so as to cast light on the working capital practices employed by the

SMEs through a process of data collection. It involved observing and describing the

behaviour of the population without influencing it in any way. The population in the

study was composed of all the 45 SMEs that were at the Two Rivers Mall. The sample

frame for this study was composed of all the trading tenants at the Two Rivers Mall, and a

census sampling technique was applied due to the size of the population. This gave the

study a sample size of 45 SMEs. Self-administered questionnaires were used to collect the

study data, and the drop and pick method of data collection was used in the study.

Quantitative data analysis was used in the study where the data obtained was coded and

analysed using Statistical Package for the Social Sciences (SPSS). Descriptive analysis

that included percentage frequencies, means and standard deviations, as well as

inferential statistics composed of correlation analysis as well as simple regressions were

used, and data was presented in the form of diagrams and tables.

The study revealed that a single unit increase in inventory management practices could

result in the SMEs’ profitability increase by a mean index of 0.660 or 66%. It revealed

that a single unit increase in receivables management practices could result in the SMEs’

profitability increase by a mean index of 0.489 or 48.9%. The study also revealed that a

single unit increase in payables management practices could result in the SMEs’

profitability increase by a mean index of 0.462 or 46.2%.

v

The study concluded that the SMEs have installed inventory control systems which

facilitate their ability to keep accurate inventory records. Good inventory management

practices have led to increased profit margins for the firms. The SMEs have aged

accounts receivables report to help in management of accounts receivable, thus

minimizing the experience of bad debt losses. This and other receivables practices has led

to increased profitability of the firms. These SMEs understand that payables management

policy affects their profitability and have employed optimal payables practices to increase

their profitability.

The study recommended that the managers and owners of the SMEs at Two Rivers Mall

develop effective strategic policies that will provide a guideline on inventory, receivable

and payables management. This would be used to train and guide the staff members and

ensure that the SMEs hold onto optimal inventory, receivable and payables levels that

will minimize costs, and maximize their profitability and operating cash flows.

vi

ACKNOWLEDGEMENT

I would like to acknowledge my supervisor Dr. George Achoki who has been patient with

me and guided me throughout this process. His constant support and guidance steered me

through this study, and I am very grateful.

To my family and friends, as well as my colleagues at work, your support in my pursuit

of education has been tremendous and has really pushed me to do my best. I would like to

sincerely thank you and appreciate you all for the support. May the Almighty God bless

all of you and thank you.

vii

DEDICATION

This research project report is dedicated to my Mum for her wise counsel.

You are the best!

viii

TABLE OF CONTENTS

STUDENT’S DECLARATION ....................................................................................... ii

COPYRIGHT ................................................................................................................... iii

ABSTRACT ...................................................................................................................... iv

ACKNOWLEDGEMENT ............................................................................................... vi

DEDICATION................................................................................................................. vii

TABLE OF CONTENTS .............................................................................................. viii

LIST OF FIGURES ...........................................................................................................x

LIST OF TABLES ........................................................................................................... xi

LIST OF ABBREVIATIONS ........................................................................................ xii

CHAPTER ONE ................................................................................................................1

1.0 INTRODUCTION........................................................................................................1

1.1 Background of the Study ...............................................................................................1

1.2 Statement of the Problem ...............................................................................................4

1.3 Purpose of the Study ......................................................................................................5

1.4 Research Questions ........................................................................................................5

1.5 Justification of the Study ...............................................................................................6

1.6 Scope of the Study .........................................................................................................6

1.7 Definition of Terms........................................................................................................7

1.8 Chapter Summary ..........................................................................................................7

CHAPTER TWO ...............................................................................................................8

2.0 LITERATURE REVIEW ...........................................................................................8

2.1 Introduction ....................................................................................................................8

2.2 Inventory Management Practices and Profitability ........................................................8

2.3 Receivables Management Practices and Profitability ..................................................12

2.4 Payables Management Practices and Profitability .......................................................18

2.5 Chapter Summary ........................................................................................................23

CHAPTER THREE .........................................................................................................24

3.0 RESEARCH METHODOLOGY .............................................................................24

3.1 Introduction ..................................................................................................................24

3.2 Research Design...........................................................................................................24

ix

3.3 Population and Sampling Design .................................................................................24

3.4 Data Collection Methods .............................................................................................26

3.5 Research Procedure ......................................................................................................26

3.6 Data Analysis Methods ................................................................................................27

3.7 Chapter Summary ........................................................................................................27

CHAPTER FOUR ............................................................................................................28

4.0 RESULTS AND FINDINGS .....................................................................................28

4.1 Introduction ..................................................................................................................28

4.2 General Information and Response Rate .....................................................................28

4.3 Inventory Management Practices and Profitability ......................................................31

4.4 Receivables Management Practices and Profitability ..................................................36

4.5 Payables Management Practices and Profitability .......................................................43

4.6 Chapter Summary ........................................................................................................48

CHAPTER FIVE .............................................................................................................49

5.0 DISCUSSIONS, CONCLUSIONS AND RECOMMENDATIONS ......................49

5.1 Introduction ..................................................................................................................49

5.2 Summary ......................................................................................................................49

5.3 Discussions ..................................................................................................................50

5.4 Conclusions ..................................................................................................................57

5.5 Recommendations ........................................................................................................58

REFERENCES .................................................................................................................60

APPENDICES ..................................................................................................................68

APPENDIX I: RESEARCH AUTHORIZATION LETTER .......................................68

APPENDIX II: NACOSTI RESEARCH PERMIT ......................................................69

APPENDIX III: QUESTIONNAIRE .............................................................................70

x

LIST OF TABLES

Table 3.1 Target Population ...............................................................................................25

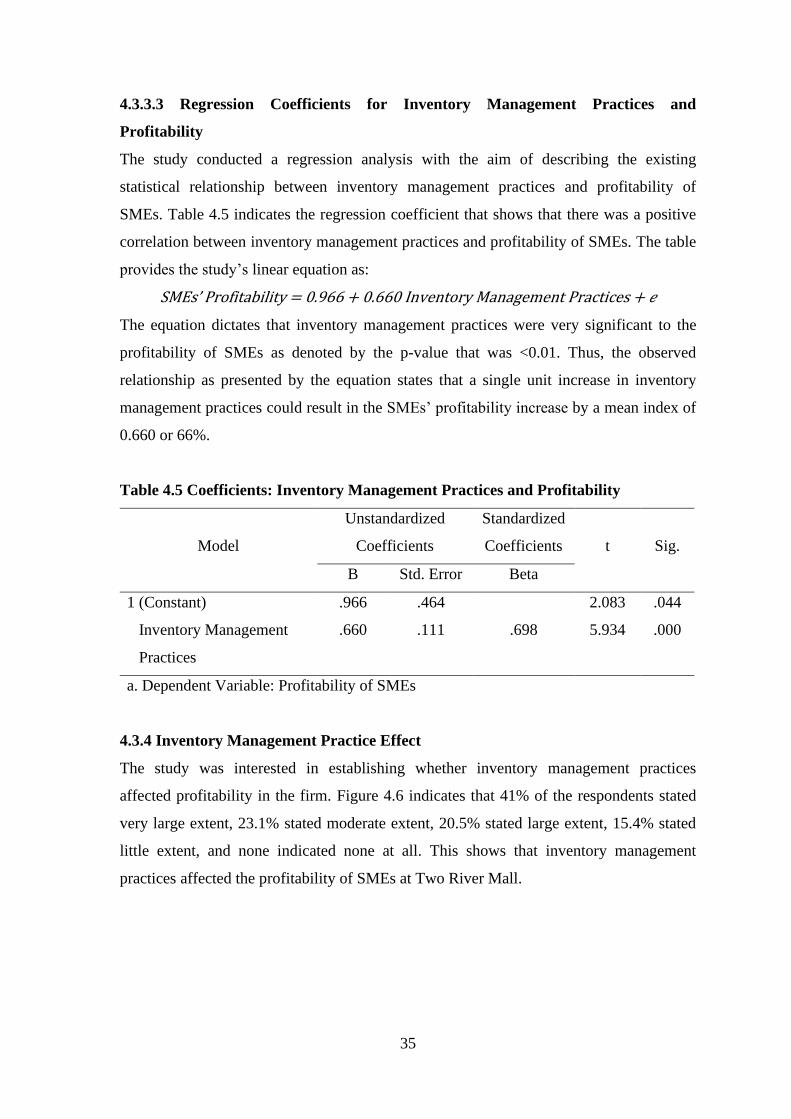

Table 4.1 Descriptive Analysis: Inventory Management Practices and Profitability ........32

Table 4.2 Correlation Analysis: Inventory Management Practices and Profitability ........33

Table 4.3 Model Summary: Inventory Management Practices and Profitability ..............34

Table 4.4 ANOVA: Inventory Management Practices and Profitability ...........................34

Table 4.5 Coefficients: Inventory Management Practices and Profitability ......................35

Table 4.6 Descriptive Analysis: Receivables Management Practices and Profitability ....38

Table 4.7 Correlation Analysis: Receivables Management Practices and Profitability ....40

Table 4.8 Model Summary: Receivables Management Practices and Profitability ...........40

Table 4.9 ANOVA: Receivables Management Practices and Profitability .......................41

Table 4.10 Coefficients: Receivables Management Practices and Profitability ................41

Table 4.11 Descriptive Analysis: Payables Management Practices and Profitability .......44

Table 4.12 Correlation Analysis: Payables Management Practices and Profitability .......45

Table 4.13 Model Summary: Payables Management Practices and Profitability ..............45

Table 4.14 ANOVA: Payables Management Practices and Profitability ..........................46

Table 4.15 Coefficients: Payables Management Practices and Profitability .....................46

xi

LIST OF FIGURES

Figure 4.1 Response Rate ..................................................................................................28

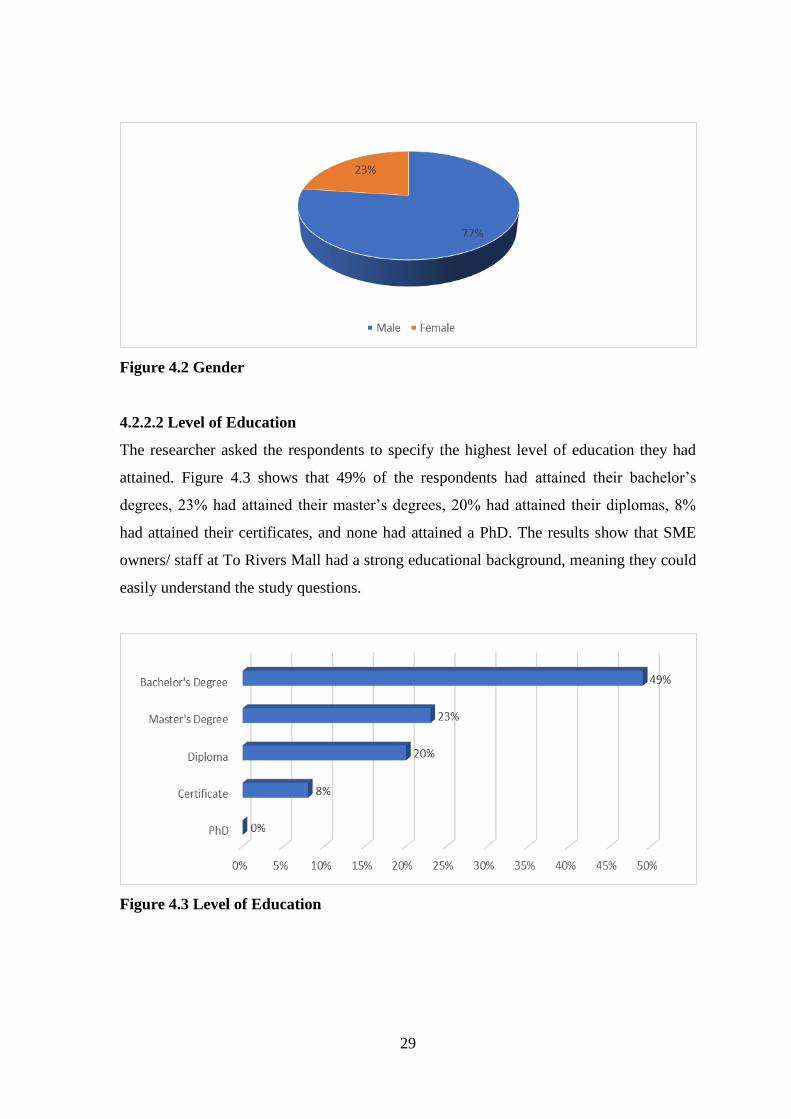

Figure 4.2 Gender ..............................................................................................................29

Figure 4.3 Level of Education ...........................................................................................29

Figure 4.4 Years Worked ...................................................................................................30

Figure 4.5 Position in the SMEs ........................................................................................30

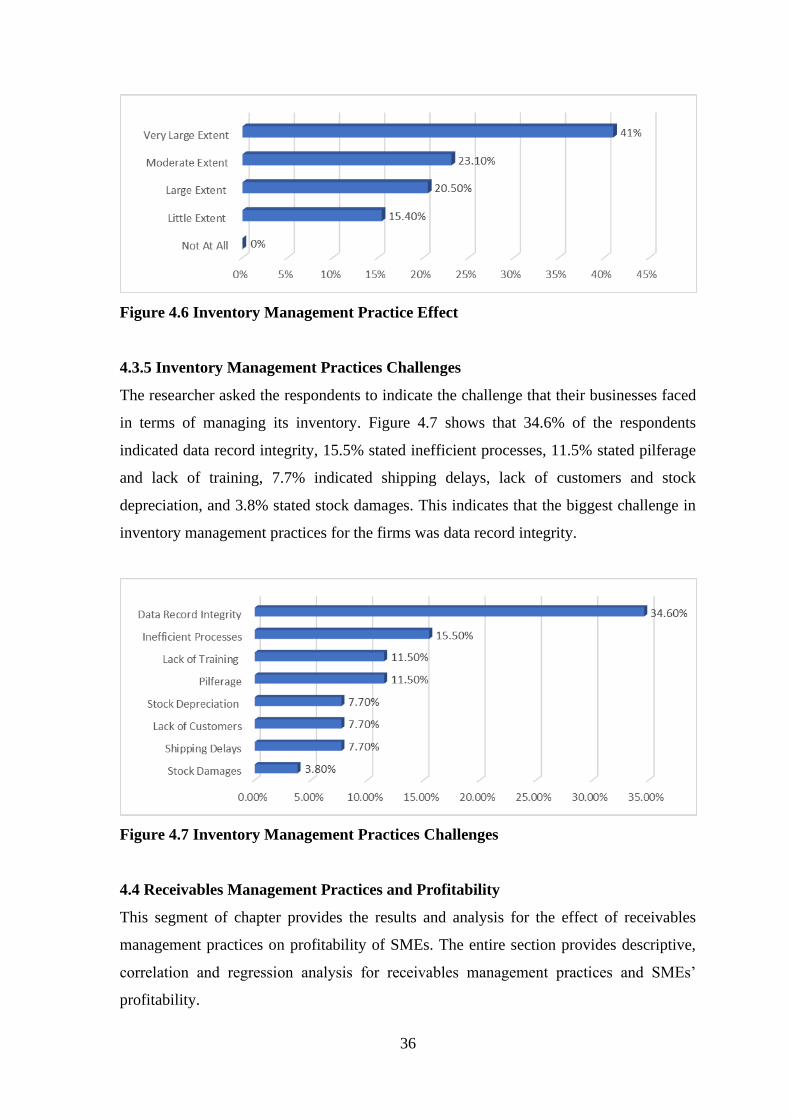

Figure 4.6 Inventory Management Practice Effect ............................................................36

Figure 4.7 Inventory Management Practices Challenges ..................................................36

Figure 4.8 Receivables Management Practice Effect ........................................................42

Figure 4.9 Receivables Management Practices Challenges ...............................................42

Figure 4.10 Payables Management Practice Effect ...........................................................47

Figure 4.11 Payables Management Practices Challenges ..................................................47

xii

LIST OF ABBREVIATIONS

AR: Accounts Receivable

AP: Accounts Payable

ANOVA: Analysis of Variance

CBK: Central Bank of Kenya

CCC: Cash Conversion Cycle

EOQ: Economic Order Quantity

GDP: Gross Domestic Product

GLS: Generalized Least Squares

GWCL: Ghana Water Company Ltd

KNBS: Kenya National Bureau of Statistics

NACOSTI National Commission for Science, Technology and Innovation

NWC: Net Working Capital

NSE: Nairobi Securities Exchange

NYSE: New York Stock Exchange

OLS: Ordinary Least Squares

SMEs: Small and Medium Enterprises

SPSS: Statistical Package for the Social Sciences

UK: United Kingdom

US: United States

WC: Working Capital

WCM: Working Capital Management

ROA: Return on Asset

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Study

Working capital is an important element in corporate financial management. It is

considered so primarily because it directly affects the profitability of the firm (Ullah,

Zahid, Khan, and Islam, 2018). Corporate finance traditionally focuses on the role that

long-term financing decisions play in the functioning of a business. In fact, researchers

have particularly offered empirical findings analysing capital investments, capital

structure, dividend policies or company value, among other topics. Yet, a significant

portion of a firm’s capital structure is represented by short-term assets and other resources

that mature in less than a year. This implies that the financial management of a business

hinges on the management of its short-term operations which then drive to the long-term

goals (Kasozi, 2017). According to Aktas, Croci and Petmezas (2015), Efficient Working

Capital Management (WCM) translates into superior performance because it allows firms

to redeploy underutilised corporate resources to high-value use. According to Singh and

Kumar (2017) a firm has to maintain a proper level of investment in working capital to

avoid the uncertain cash inflow and outflow situation. Suitable liquidity and profitability

scenarios are the main two objectives of WCM but not at the cost of one another. Thus,

each enterprise should make a trade-off between these two objectives to enhance the

efficiency of WCM (Singh and Kumar, 2017).

The management of working capital and the role it plays in advancing financial

performance continues to steer debate among scholars and practitioners alike. The current

thrust of empirical study on the relationship between working capital management and

financial performance is directed towards informing policy on the appropriate current

asset-liability mix which maximizes a firm’s profitability while minimizing its risk

(Jajongo and Makori, 2013). Further, it is notable that a significant portion of the existing

research concentrates on developed rather than on developing economies (Qurashi and

Zahoor, 2017; Samiloglu and Akgun, 2016). The question then arises on whether the

working capital methodologies used on firms in the developed economies apply to firms

within the developing economies whose contrasting economic conditions affect them in

distinct ways.

2

At the same time, there is a massive debate in the existing literature as to which level of

working capital is good for the firm. Arguments exist on supporting both for holding high

and low amount of working capital. One study established that the nature of the

relationship between working capital level and firm profitability depends on the particular

WCM approach preferred by a firm (Afrifa and Padachi, 2016). The consensus is that low

investment in working capital (aggressive policies) may result in outcomes such as loss of

sales and disruptions in the production process, leading to lower profitability. A firm can

apply aggressive policy of WCM by decreasing investment in both the accounts

receivable and inventory. Reducing inventory cost leads to higher firm profitability

because of a decrease in inventory holding costs (Afrifa and Padachi, 2016).

In contrast, a conservative WCM strategy (signifying higher investment in working

capital) may lead to boosting sales by increasing both inventories and trade receivables in

order to increase profitability (Afrifa and Padachi, 2016). Majority of the empirical

studies relating WCM with profitability support the fact that aggressive policy enhances

profitability. One study investigating 65 Pakistani companies for the period between 2005

– 2009 found significant correlation with market value and firm profitability and the

various components of working capital (Alam, Ali, Rehman and Akram, 2011). Another

study analyzing the relationship between WCM and profitability documented a positive

coefficient with Cash Conversion Cycle (CCC), using of a sample of 88 New York Stock

Exchange (NYSE) listed United States (US) manufacturing firms for the period of 2005

to 2007 (Gill, Biger and Mathur, 2010). From their standpoint, the higher the CCC, the

higher the profitability of the firm.

Banos-Cabellero, Garcia-Teruel and Martinez-Solano (2014), focuses on Spanish SMEs

and documents a concave relationship between Net Working Capital (NWC) and firm

performance. Afrifa, Tauringana and Tingbani (2015) investigate the relationship

between Cash Conversion Cycle (CCC) and the profitability of United Kingdom (UK)

Small and Medium-Sized Enterprises (SMEs). Evidence from the study reveals an inverse

U-shape relationship between CCC and Return on Assets (ROA). Tauringana and Afrifa

(2013) examined a relationship to inspect the relative significance of WCM, measured by

cash conversion cycle and its components that are inventory, Account Receivable (AR),

and Account Payable (AP) to the profitability of listed SMEs. By applying the panel data

regression analysis, they concluded that AP and AR are important for the profitability of

3

SMEs (Tauringana & Afrifa, 2013). Likewise, Wasiuzzaman (2015) also documented the

relationship between working capital investment and firm value based on Malaysia by

using data from 192 firms over a period of 8 years (from year 2000 to 2007). Results of

multiple regression analysis indicate that firm value is considerably increased by

progresses in WCM and specifically factual for financially constrained firms. Hence, this

study also suggests, to evaluate a firm, investors should not only focus on firm’s capital

structure, dividend and investment policies but also their working capital strategy in order

to pick the suitable investment alternatives (Wasiuzzaman, 2015).

In Kenya, recent literature on working capital is by Mathuva (2015), whose findings were

that profitable firms on the Kenyan market were found to take less time in collecting cash

from their customers, thereby enforcing low average collection period. Profitability is the

primary goal of all business ventures. A company’s profitability is the ability of a

business to make gains from operations. Profit is a company’s revenue net the expenses

involved in the revenue generation (Hofstrand, 2013). Without profitability a business

will not survive for a long time. It is therefore important that any business keeps track of

both the current and past profitability.

Profitability is measured using the income and expenses from the business. Income

represents money generated from the various activities of the business. One of the ratios

that is used in measuring profitability of a business or company’s performance is the

gross profit margin (Hofstrand, 2013). Gross profit margin measures company's

manufacturing and distribution efficiency during the production process. It is a

measurement of how much of each dollar of a company's revenue is available to cover

overhead, other expenses and profits. The ideal level of gross profit margin depends on

the type of industries, the length of time the business has been in operation and other

factors. A high gross profit margin indicates that the company can make a reasonable

profit, so long as the company or business keeps the overhead cost in control.

On the other hand, a low gross margin indicates that the business is unable to control its

production cost (Hofstrand, 2013). Measuring profitability is the most important step to

measure the success of a business. A business which is not profitable cannot survive for

long. Conversely, a business that is highly profitable will always have a reasonable

turnover and is able to reward its owners with a large return on their investment.

4

Increasing profitability should therefore be one of the most important tasks of the

business managers. Managers should constantly look for ways to improve running of the

business so that profitability can be improved. SMEs play key roles in various economies

worldwide. SMEs are the backbone of all economies and their importance as an impetus

to economic development especially in developing economies cannot be over-

emphasized. They serve as dynamic forces and agents of change as they stimulate

economic growth.

1.2 Statement of the Problem

Working capital is an important component in the financial decision of the company. An

optimal working capital management is reached through a trade- off between profitability

and liquidity. This study aimed to provide empirical evidence about the effects of

working capital management on the profitability of SMEs at Two Rivers Mall.

Traditionally, the corporate finance literature has studied long-term financial decisions

like investments, capital structure, company valuation or dividends. However,

management of short-term assets and liabilities deserves a careful analysis since working

capital management has an important effect on the firm’s profitability as well as its risk.

Consequently, to minimize risk and to improve the overall performance, financial

executives must monitor continuously each of working capital components, i.e.,

receivables, inventories, and payables. An optimal level of working capital management

would be reached by achieving a balance between liquidity and profitability. In fact, if the

company adopts a working capital management policy with an excessive level of current

assets, the risk of liquidity may be reduced. Conversely, the company bears the

opportunity cost of funds that may have been invested in long term assets. Though the

effect of working capital management on profitability is important, only a few empirical

studies have been conducted to observe this relationship.

In the Kenya government blueprint for 2020, the government acknowledged the need for

SMEs to be strengthened to move to a middle- income country (Republic of Kenya,

2010). According to a national survey done by Kenya National Bureau of Statistics

(KNBS) in 2016 SMEs contributed 33.8 percent to national Gross Domestic Product

(GDP) in 2015 and 81.1 percent of employment. The survey established that there were

1.56 million SMEs licensed by county governments while the unlicensed business

5

identified from the households were 5.85 million. A total of 2.2 million SMEs was closed

in the last five years, 2016 inclusive. The closed businesses consisted of majority of

SMEs which accounted for 73.5 percent. On average the businesses closed at 3.8 years.

A survey by the Kenya National Bureau of Statistics released in 2018 indicated that

approximately 400,000 micro small and medium enterprises do not celebrate their second

birthday and very few SMEs reach their fifth birthday, leading to concerns of

sustainability in this critical sector. While opening the SME Financing Africa Forum

2018 in May last year, Central Bank of Kenya (CBK) Governor Patrick Njoroge pointed

out that 46% of Kenya’s SMEs close within a year of founding. This being the case, the

study intends to investigate whether these closures could be attributed to poor working

capital management, with a focus on the SMEs that are located at the Two Rivers Mall.

Therefore, this research investigated enterprises in Two Rivers Mall in order to find out

the best working capital practices that were in use, with a view of identifying capital

management gaps and proposing the best practices to be adopted to ensure business

growth, profitability, expansion and longevity.

1.3 Purpose of the Study

The purpose of the study was to examine the effects of management of working capital on

the profitability of SMEs.

1.4 Research Questions

This study sought to answer the following research questions:

1.4.1 How does inventory management practices affect profitability of SMEs at Two

Rivers Mall?

1.4.2 What is the effect of receivables management practices on the profitability of SMEs

at Two Rivers Mall?

1.4.3 How does payables management practices affect profitability of SMEs at Two

Rivers Mall?

1.5 Justification of the Study

This study attempts to highlight the role of working capital management in the

profitability of SMEs in Kenya. This study may be of use to the following parties:

6

1.5.1 Small and Medium Enterprises

The recommendations and findings of this study may help SMEs understand the effects of

working capital management on profitability so as to enhance growth and success.

1.5.2 Business Advisors

The financial sector is a dynamic industry that is characterised by a highly changing

environment. Information that was gathered during the study may be used by business

advisors in their work as it cuts across a broad spectrum of businesses. Equally, the study

may be used by other firms such as microfinance institutions.

1.5.3 Makers of Policy

One of the pillars of Vision 3030 is the economic pillar. SMEs play a vital role in the

realization of this pillar. The study may provide findings that could be used by

policymakers to propose government interventions and policies that could promote

economic growth and achievement of vision 2030.

1.5.4 Researchers and Scholars

Other scholars and researchers may find this study important because it may be used as a

basis for empirical review. Additionally, the study offers suggestions for further studies

that may be conducted in this area.

1.6 Scope of the Study

The target population of the study was the 45 SMEs who were at the time trading at the

Two Rivers Mall. The study aimed at examining financial data from the retail outlets for

the period 2018 to 2019. The study involved the administration of questionnaires

personally. The study was carried out in a span of three months in the first half of 2020.

1.7 Definition of Terms

1.7.1 Working Capital Management

Management of working capital is defined as all management actions and decisions that

ordinarily influence the size and effectiveness of the working capital. Therefore, the aim

of working capital is to optimally manage current assets and current liabilities such that

7

an acceptable level of net-working capital can be achieved (Umoren and Udo, 2015).

AlShubiri (2011) defined working capital as the amount of a business current assets that

are being financed by long-term debts and/or equity.

1.7.2 Profitability

An enterprise must make profit from all its business activities. Profitability shows how

efficiently the management uses all the resources available in the market. Profitability in

the words of Onyam, Usang and Enyisi (2015) means the ability to make profit from all

the business activities of an organization, company, firm, or an enterprise.

1.7.3 Small and Medium Enterprises

Small and medium-sized enterprises are non-subsidiary, independent firms which employ

fewer than a given number of employees. This number varies across countries. The most

frequent upper limit designating an SME is 250 employees, as in the European Union.

However, some countries set the limit at 200 employees, while the United States

considers SMEs to include firms with fewer than 500 employees. Small firms are

generally those with fewer than 50 employees, while micro-enterprises have at most 10,

or in some cases 5, workers (OECD, 2005).

1.8 Chapter Summary

This chapter presents a background on working capital management and its role in the

profitability of SMEs. The chapter entails the background of the study, statement of the

problem, purpose of the study, research questions, justification of the study, scope of the

study and a definition of key terms. Chapter two presents literature reviewed based on

research questions. Chapter three is the research methodology. Chapter four presents the

results and figures of the study, and chapter five is the discussions, conclusions, and

recommendations of the study.

8

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

This chapter presents the empirical review of the independent and dependent variables.

The subsequent sections examine international and local studies on this. This study has

three independent variables: inventory management, receivables management and

payables management. It aims to determine the impact of these variables on the

profitability of SMEs. Sound working capital management is crucial to the survival of an

organization. It is also imperative for the growth of an organization. The management of

inventory, receivables and payables is a significant component of a firm’s working capital

management. This present study empirically examines the effect of efficiency of working

capital management on the firm’s profitability of SMEs. The study examines one key

indicator of the profitability of SMEs, the gross profit margin.

2.2 Inventory Management Practices and Profitability

2.2.1 Inventory Management Practices

Deveshwara and Dhawal (2013) proposed that inventory management is a method that

companies use to organize, store, and replace inventory, to keep an adequate supply of

goods at the same time minimizing cost. According to Stevenson (2010), Inventory

Management is defined as a framework employed in firms in controlling its interest in

inventory. It includes the recording and observing of stock level, estimating future

request, and settling on when and how to arrange. An effective and efficient management

inventory flow across the value chain is one of the key factors for success of large and

small enterprises. The challenge in managing inventory is to balance the trade-off

between the supplies of inventory with demand. Ideally a company wants to have enough

inventories to satisfy the demands of its customers no lost sales due to inventory stock-

outs. On the other hand, the company does not want to have too much inventory staying

on hand because of the cost of carrying inventory. Inventory decisions are high risk and

high impact for the supply chain management of an organization.

Excessive inventories are one of the most important problems faced by many companies

all over the world. Inventories are engaged funds, and when unproductive, freeze high

capital of the company. Inventories also cause an increase in costs associated with their

maintenance and service. This is especially important today, when the rising cost of

9

operations and increase competition in the market eliminate companies which are not

effective in costs reduction (Ganas and Hyz, 2015). However, the question of whether

inventory reduction has been achieved and whether it has been beneficial to firm’s

performance have not been subject to systematic investigation. One study by Ganas and

Hyz (2015) in Greece examines Greek inventories using data from the SME sector in the

region of Epirus in Greece. The study selected a selection of small and medium

enterprises because these companies are the basis of the economy of Greece in general. It

assumed that improper management of inventories is one of the main reasons behind

failure or poor financial performance of many Greek SMEs. This study hypothesized that

there is a positive relationship between inventory management and firm performance.

This study was conducted on a sample of financial data for 612 firms over the ten years

period. By employing correlation and regression techniques the impact of inventory

management and firm’s profitability was found to be significantly negative. This led to

the conclusion that less profitable firms have worst inventory management measures.

Therefore, managers can create profits for their companies by managing efficiently the

inventories and their components’ measures, leading to an optimum level.

Ashok (2013) investigated the existence of relationship between stock management and

how profitable an enterprise is, in the context of organizations under cement sector in

India. The independent variable in the investigation, earnings prior to interest as well as

tax was employed as a proxy for profitability and the existence of any significant

relationship between stock management and how profitable a company becomes was

conducted using five leading cement manufacturing organizations in India. The

investigation applied regression analysis in ascertaining the effect of stock conversion

period on profit before interest and tax. The results indicated the existence of a

statistically significant but negative linear relationship between stock conversion period

and profit before interest and tax. The investigation revealed that how profitable an

organization becomes has a statistically negative relationship with stock management.

Another study by Atnafu and Balda (2018) examined the impact of inventory

management practice on firms’ competitiveness and organizational performance from

micro and small enterprises in Ethiopia. The finding of this study implies that enhanced

competitive advantage and increased organizational performance could have improved

the levels of inventory management practice. The increased competitiveness of a firm

10

may enable a firm to implement a higher level of inventory management practice due to

the need to outperform its competitors constantly and keep its competitive position. On

the other hand, enhanced organizational performance provides a firm increased capital to

implement various scientific inventory management techniques. To this end, the study

provided empirical evidence to support the literature regarding the impact of inventory

management practices.

The impact of working capital management on profitability was investigated by Agha,

Mba and Mhil (2014). The authors used data collected from Glaxo Smith Kline listed

pharmaceutical company in Karachi Stock Exchange for the years 1996-2011. Return on

assets ratio had been used for the measurement of profitability, while accounts receivable

turnover, creditors turnover, inventory turnover, and current ratio for the measurement of

working capital. The study found that the Working Capital (WC) significantly affects

firm's profitability, and profitability can be enhanced through minimizing inventory

turnover, accounts receivable ratio, and through reducing creditors' turnover ratio. In

addition, the study found that no significant effect of current ratio on the profitability of

firms.

Akinyomi (2014) examined the association between inventory management and the

profitability of Nigerian manufacturing firms. Information for the study was obtained

from secondary sources, specifically the audited financial statements of the

manufacturing companies for the period 2008 to 2012. Return on equity was used as a

proxy for profitability, while inventory conversion period was used as a proxy for

inventory management. Findings from the analysis revealed the existence of statistically

no significant relationship between stock management and the profitability of

manufacturing companies.

Kung’u (2016) studied the effects of inventory control on the profitability of industrial

and allied firms in Kenya. The results of the study showed that when firms maintain good

inventory control systems, the firms’ profits are high. The firms should install modern

inventory control systems such as economic order quantity and just in time. These

inventory control systems help firms maintain optimal inventory levels. Maintaining

optimal inventory levels reduces cost of possible interruptions or loss of business due to

scarcity of products at the same time it reduces high cost of maintaining stock. Cost of

11

high stock includes stock theft, expiry, insurance, and storage. In light of Economic Order

Quantity (EOQ) model, costs must be maintained at minimal level between stock holding

and ordering. The firms should also be able to put in place an effective stock management

system that ensures reliable sales forecast to be used in order purposes. The findings of

inventory control on profitability of manufacturing firms in Kenya showed that finance

managers of manufacturing firms take precautions to ensure that their firms maintain

ideal levels of inventories of both raw materials and finished goods. This may have led to

increased profitability of manufacturing firms in Kenya and therefore it can be concluded

that there exists a positive and significant relationship between inventory control and

profitability.

A study carried out by Mathuva (2010) on the influence of working capital management

components on corporate profitability found that there exists a highly significant positive

relationship between the period taken to convert inventories into sales and profitability.

This meant that firms maintained sufficiently high inventory levels which reduced costs

of possible interruptions in the production process and loss of business due to scarcity of

products.

Mwaura (2017) carried out a study on the effect of inventory turnover on the financial

performance of medium and large retail supermarkets in Kenya. The study adopted

descriptive cross-sectional research design. The data to be collected included sales, cost

of goods, current assets and liabilities, total assets, total liabilities, profit before interest

and tax, closing inventory balance and net profit for each year. The results were analysed

using stata software. The data collected covered the years 2012 - 2016. From the results

of correlation analysis, there is a strong positive and statistically significant correlation

between inventory turnover and financial performance of medium and large retail

supermarkets in Kenya.

2.2.2 Profitability

Anser and Malik (2013) study investigated how cash conversion cycle affects the firms’

profitability of listed manufacturing companies of Pakistan. The study took into

consideration 5 years financial statements data starting from 2007 to 2011. Results

12

showed that manufacturing companies are having low average return on asset and high

average return on equity with reasonable average cash conversion cycle. Regression

results after adjusting for heteroskedasticity of data to minimize the effects of outliers,

showed that cash conversion cycle having significantly inverse association with both

return on assets and equity indicating that the lesser the cash conversion cycle the greater

would be the profitability, measured through return on assets and equity.

Muturi (2015) investigated the effects of cash conversion cycle on profitability of Tea

Factories in Meru. A census method was used to collect primary data from all the seven

tea factories in the county for a period of five years starting from 2009 to 2013. The

correlation and regression analyses were used to analyse and describe the nature of the

relationship between CCC and the firm’s profitability. A lot of literature has pointed out

that efficient management of cash has significantly influenced the firm’s profitability.

This study found out that the CCC significantly negatively affects the tea firm’s

profitability.

Mohamed (2013) studied the effect of cash conversion cycle on the profitability of firms

listed on the Nairobi Securities Exchange. The relation between the firm’s cash

conversion cycle and its profitability is examined using dynamic panel data analysis for a

sample of firms listed on The NSE for the period from 2008 to 2012. The analysis is

applied at the levels of the full sample and divisions of the sample by industry and by

size. The results indicated that there is a significant and negative relationship between the

cash conversion cycle and return on asset. The firms with shorter cash conversion cycles

are more likely to be profitable than firms with longer cash conversion cycles.

2.3 Receivables Management Practices and Profitability

2.3.1 Receivables Management Practices

Accounts receivable represents money owed to a business in return for goods already

delivered or services already rendered. Proper maintenance of accounts receivable helps

an organization maintain customer loyalty, track customer credit and uncollected profits.

However, many organizations nowadays encounter numerous challenges regarding their

invoicing and accounts receivable process (Munene and Tibbs, 2018)

13

Receivable management is an important fact of financial management, this is because

excessive level of current assets and low level of current assets may lead to negative

effect on a firm’s profitability and difficulties in mediating smooth operation (Duru,

Ekwe and Okpe, 2014).

According to Deloof (2013) management of accounts receivables which aims at

maintaining an optimal balance between each of the accounts receivables components,

that is, cash, receivables, inventory and payables is a fundamental part of the overall

corporate strategy to create value and is an important source of competitive advantage in

businesses. The management of accounts receivable is largely influenced by the credit

policy and collection procedure of a firm. Accounts receivable represents the rate at

which the firm collects payments from its customers (Sharma and Kumar 2011).

The key principles of accounts receivable management that a firm should adhere to are

ageing of accounts receivable, evaluating the potential customers ability to pay using

criteria such as integrity of the customer, financial soundness, collateral to be pledged and

current economic conditions should be analysed, establishment of credit terms and limits,

collection of trade credit, assessment of default risk and responsibility and the financing

of accounts receivable until it has been paid by the purchaser (Schaum, 2011).

Shin and Soenen (2013) observed that a well-managed enterprise normally keeps average

collection period normally lesser than average payment period so as to minimize

investment in receivables and also honour its short time obligations on time minimizing

cost of funds. Average payment period is basic test of the business’s good or bad activity

or operation and its important symbol for making good planning for increase or decrease

working capital efficiently. This is because working capital is more effected from sundry

debtors and sundry creditors.

Pais and Gama (2015) examined the effects of working capital management on the

profitability of Portuguese firms. Panel regressions and instrumental variables were used

to model a sample of 6,063 Portuguese SMEs, covering the period 2002-2009. Results

indicated that a reduction in the inventories held and in the number of days that firms take

to settle their commercial liabilities and to collect payments from its customers are

associated to higher corporate profitability.

14

Ramana, Ramakrishnaiah and Chengalrayulu (2013) studied the impact of managing

receivables on the working capital and profitability of cement companies in India.

Ramana et al. found that selected companies from cement industry were efficient in

managing their receivables and this was reflected in lower collection period. The efficient

receivables management was found to have a positive impact on both working capital and

profitability.

Venkata, Ramakrishnaiah and Chengalrayulu (2013), in their study “impact of receivables

management on working capital and profitability: A study of selected cement companies

in India”, collected their data from the Annual Reports of the selected cement companies

from 2001 -2010. The ratios which highlight the efficiency of receivables management

viz, receivables to current assets ratio, receivable to total assets ratio, receivable to sales

ratio, receivable to turnover ratio, average collection period, working capital ratio,

profitability ratio were analysed using Analysis of Variance (ANOVA) statistical tools to

know the impact of working capital on profitability of the selected cement companies.

The investigation revealed that the receivable management across cement industry is

efficient and showed significant impact of working capital on profitability.

Ksenija (2013), investigated how public companies listed at the regulated market in the

republic of Serbia managed their accounts receivable during recession times. A sample of

108 firms was used. The accounts receivables policies were examined in the crisis period

of 2008- 2011. The short-term effects were tested, and the study showed that between

accounts receivables and two dependent variables on profitability, return on total asset

and operating profit margin, there is a positive but no significant relation. This suggests

that the impact of receivables on firm’s profitability changes in times of crisis.

Kakeeto, Timbirimu, Kiizah and Olutayo (2016) studied the effects of account receivable

management and organizational profitability in Mbale Uganda. By testing the hypothesis:

Accounts Receivable Management has a significant positive effect on organizational

profitability. Using a descriptive research design and a case study strategy, they collected

data from the respondents in terms of the two variables. The findings revealed that

revealed that accounts receivable management positively affected organizational

profitability.

15

Akinleye and Adebowale (2019) examined account receivable management and

performance of manufacturing firms in Nigeria. Specifically, the study analysed the effect

of book value of accounts receivable on return on capital employed of manufacturing

firms in Nigeria. It also examined the effect of anticipated bad debt on profitability of

manufacturing firms in Nigeria and analysed the effect of sales growth on return on

capital employed of manufacturing firms in Nigeria. The study sampled 10 manufacturing

firms from the Nigerian Stock Exchange covering a period of 10 years spanning from

2007 to 2016. The study concluded that, accounts receivable has the capacity to

significantly impede the level of performance of manufacturing firms in Nigeria,

especially when measured in terms of return on capital employed. Also, increase in the

anticipated bad debt does not significantly contribute to improved performance of

manufacturing firms in Nigeria. Finally, the study established that though sales growth

has positive impact on performance of manufacturing firms, such positive impact is not a

significant guarantee for improved return on capital employed.

Oware, Samanhyia and Ampong (2015), demonstrated that when a firm does not invest

well in the collection of account receivable then the probability that a firm will stagnate

as a result of very poor account receivables levels and debt accumulation would be high.

This is clearly shown on how the operations of Ghana Water Company Ltd (GWCL) were

affected. When accounts receivable takes a long time to be collected; it becomes

impossible investing in production for your next order. Uncollected amounts tie up

working capital unreasonably and may lead to long business cycles.

Dirie and Ayuma (2018) studied the effect of accounts receivable management on the

financial performance of Small and medium firm enterprises in Mogadishu city in

Somalia. The specific objectives of the study were to investigate the impact of cash flow

management, credit management and credit policy management on financial performance

which are the vital elements of whole concept of account receivable management. The

results reveal for cash flow management, debt management, credit policy management

and inventory management were found to have positive significant correlations on

financial performance at 5% level of significance. The results imply that cash flow

management, credit policy management, inventory management significantly influenced

financial performance of the SME’s in Mogadishu Somalia.

16

Munene and Tibbs (2018) sought to determine the effects of accounts receivable

management on financial performance of Embu Water and Sanitation Company limited,

Embu County, Kenya. The objective of the study was to examine the effects of inventory

turnover period, average payment period, cash conversion period and average collection

period on financial performance of Embu Water and Sanitation Company Limited. The

study used secondary data which was obtained from the accounts and finance

departments. Inventory turnover period, average payment period, cash conversion period

and average collection period was all found to have a positive effect on financial

performance of Embu Water and Sanitation Company Limited.

Mbula, Memba and Njeru (2016) investigated the effect of accounts receivable on

financial performance of firms funded by Government Venture Capital in Kenya. They

found that there is a positive relationship between accounts receivables and financial

performance of firms funded by government venture capital in Kenya.

Lyani (2017) examined the relationship between Accounts Receivable Management

Practices and organizational growth and revealed that efficient Accounts receivable

management practices, when adopted by SMEs lead to growth. However, the study

focused on SMEs in Kakamega County, Kenya

2.3.2 Profitability

Iyewumi, Remy and Omotayo (2015) investigated the relationship between working

capital management and firm’s profitability in the oil and gas sector in Nigeria. The study

is based on secondary data collected from a sample of two listed oil firms in Nigeria for

the period 1995 to 2011. The results of correlation analysis and Ordinary Least Squares

(OLS) estimation technique provide that firm’s profitability in Nigeria is affected by; the

working capital management components which are; cash conversion cycle, average

days’ receivables, average days payables, average days inventories. Second, size of the

firm is equally another important variable found to affect the profitability of firms.

Sabo, Rabi, Usman, Fatima and Tjjani (2015) examined the impact of working capital

management on corporate profitability of 7 listed firms in Nigeria for the periods of 2008

to 2012. The results of descriptive statistics and Generalized Least Squares (GLS)

17

regression analysis confirmed a positive relationship among average collection period,

current ratio and the size of the firm with profitability and a negative relationship with

inventory turnover period and average payment period.

Nzioki, Kimeli, Abudho and Nthiwa, (2013) analysed the effects of working capital

management on the profitability of 9 manufacturing firms listed on the NSE. The result of

multiple regression and correlation analyses revealed that gross operating profit was

positively correlated with average collection period and average payment period but

negatively correlated with cash conversion cycle. The relationship between inventory

turnover in days and gross operating profit was insignificant.

Rehman, Khan and Khokhar (2014) researched the determinants of profitability of

petrochemical companies in Saudi Arabia. They examined the relationship of net profit

margin with creditors’ velocity, long-term debt to equity ratio, debtors’ turnover ratio,

inventory turnover ratio and total assets turnover ratio. The study found that creditors

velocity, long-term debt to equity ratio, inventory turnover ratio and total assets turnover

ratio have a significant relationship with profitability measured using net profit margin.

However, debtors’ turnover ratio did not show any significant relationship with net profit

margin.

Jindal (2017) established in his empirical study on the commercial vehicle industry in

India, done for the period 2009 to 2016 that there was evidence that an increase in the

debtors’ turnover will increase the profitability of the firm. Thus, the efficient

management of accounts receivables increases profitability.

Quayyum (2012) studied the relationship between corporate profitability and working

capital management. She found a positive relationship between the two variables for all

industries included in her study except for the food and allies’ industries in the Dhaka

Stock Exchanges in Bangladesh.

Afeef (2011) examined the relationship between corporate profitability and working

capital management. The study used a sample of 131 companies listed in the Athens

Stock. The study showed that there were significant returns between profitability,

measured through gross operating profit, and the cash conversion cycle. It is found that

18

the manager should be efficient enough in handling the cash conversion cycle and

keeping optimum level of account receivables, account payables and inventory.

2.4 Payables Management Practices and Profitability

2.4.1 Payables Management Practices

Accounts payable is an account that represents a company's obligation to pay off a short-

term debt to its creditors or suppliers. Accounts payable are suppliers whose invoices for

goods or services have processed but who have not yet been paid. Organizations often

regard the amount owing to creditors as a source of free credit. Accounts payable ratio

represents the rate firms pay to their suppliers. It is one of the major sources of secured

short-term financing (Gitman, 2009). Payables management forms a critical component of

the supply chain, under the area of procurement. As companies have become more aware

of the competitive advantages of supply chain management from cost efficiency, product

differentiation and value-added services so too has the task of managing the relationship

between payables and suppliers become fundamentally important (Ashok, 2013).

Afrifa (2016) used unbalanced panel data regression analysis on 6,926 non-financial

small and medium enterprises in UK from 2004 to 2013. The results suggest that firms

should consider their cash flow when making decision on working capital investment. To

improve performance, firms with limited cash flow should reduce their working capital

investment. However, firms with available cash flow should raise their working capital

investment.

Yahaya (2016) carried out a study on effects of working capital management on the

financial performance of the pharmaceutical firms in Nigeria. The study covered a period

of eight years 2006 to 2013. Data for the study was collected through secondary sources

using annual financial reports and bulletins of Nigeria stock exchange of the various firms

covering the period under study. The study found that average payment period was

significantly and positively related with financial performance.

Kumaraswamy (2016) investigated the impact of working capital on financial

performance of Gulf Cooperation Council Firms for a period of 2008-2014. Four

hypotheses pertaining to average payment period components were investigated using

linear regression models. The study identified positive relationship between average

19

payment period with profitability and a negative relationship amid average collection

period and firm profitability.

Madugba and Ogbonnaya (2016) investigated the effects of average payment period and

financial performance: evidence from manufacturing companies in Nigeria. The study

employed multiple regressions in analysing the data sourced from the published financial

statements of the firms under the study. A significant outcome of the study is that

Average Payment Period impacts on both earnings per share and return on capital

employed. The implication is that efficient management average payment period will

improve the financial performance of the manufacturing firms.

Madishetti and Kibona (2013) investigated the impact of average collection period and

average payment period on SMEs profitability in Tanzania. The study was carried out

using dependent variable as gross operating profit and independent variables as average

collection period and average payment period employing relevant information of 38

Tanzanian SMEs for the period from 2006 to 2011. The study employed regression

analysis to determine the impact of average collection period and average payment period

on gross operating profit taking current ratio, size of the firm, financial debt ratio as

control variables. The results indicated that there was a significant negative relationship

between average collection period and profitability. Positive relationship was observed

between average payment period and gross operating profit.

Igwebuike and Nankwo (2018) determined the impact of average payments period on

profitability of quoted insurance companies in Nigeria. The study was carried out using

Return on Assets as dependent variable and Average Payments Period as explanatory

variable. Return on Assets was used as a measure of profitability Data was collected from

the annual financial reports of 20 sampled insurance companies. For testing the

hypothesis, multiple regression technique was used. Current ratio, fixed financial total

asset ratio, debt asset ratio, growth and size were incorporated in the model as control

variables. The results indicated that Average Payments Period has a significant negative

impact on profitability. Based on the findings, the study recommended that Nigerian

insurance companies should endeavour to reduce their number of days accounts payables

optimally and concentrate on reducing the high variability in the average payables period

to enhance their corporate profits.

20

Nwakaego and Ikechukwu (2016) examined the effect of management of accounts

payable on the financial performance of Industrial domestic manufacturing companies in

Nigeria. They collected data from the financial reports of the companies. The study

showed that the relationship between accounts payable ratio and profitability is

statistically positive and significant. Nwakaego and Ikechukwu (2015) examined the

effect of the management of accounts payable on the profitability of brewery companies

in Nigeria. The variables included, accounts payable, debt ratio and sales growth rate.

Secondary sources of data were used for the period 2000-2011. The hypotheses were

tested using multiple regression analytical tools. The results showed that accounts payable

had negative but non- significant relationship with profitability ratio of the companies

under brewery manufacturing companies in Nigeria. Debt ratio had positive and

significant relationship, while sales growth rate was negative and significant with the

profitability ratio of Brewery companies in Nigeria.

Ullah, Islam and Khair (2017) examined the relationship between working capital

management and profitability of SMEs from Bangladesh. 10 SMEs were selected for the

period of 2013-2015.The study concluded that there is no significant relationship between

Accounts Payable and Return on Assets. Moodley and Muller (2017) examined the

management of payables and the return to investors of listed South African companies

over the period 1986 to 2014. The results of the study indicated that for those companies

in industries that have a significant investment in payables, there is a significant positive

association between changes in payable days and shareholder return.

Muchina and Kiano (2011) analysed the influence of working capital management on

firms’ profitability in Kenya. They used fixed panel data of 232 firms. The result

indicated that the average debtor day, stock turnover period and the cash conversion cycle

are significantly affecting the profitability of the firms. They found out also that the

manufacturing firms are in general facing problems with their collection and payment

policies.

Gakure, Cheluget, Onyango and Keraro (2012) analysed the relationship between

working capital management and performance of 15 manufacturing firms listed at the

NSE from 2006 to 2010. They used secondary data from a sample of 18 companies at the

21

NSE. A regression model was used to establish the relationship between the dependent

variable and the independent variables. Pearson’s correlation and regression analysis were

used for the analysis. The results indicated that there is a strong negative relationship

between firm’s performance and liquidity of the firm. The study found that there is a

negative coefficient relationship between accounts collection period, average payment

period, inventory holding period and profitability while the cash conversion cycle was

found to be positively correlated with profitability. However, the effects of the

independent variables except the average payment period were not statistically significant

though the overall model was statistically significant.

Achode and Rotich (2016) examined the effects of accounts payable on financial

performance of publicly listed manufacturing companies at NSE, Kenya. Census

sampling technique was employed, and the study used secondary data, which was

obtained from the companies’ statistics and journals at the NSE. A multiple regression

model was used to test the relationship between the Accounts payable and firm

performance. The results from this research suggested that in most of the manufacturing

firms listed at the NSE, there was a direct positive relationship between AP and the

dependent variable, Profitability and Liquidity,

2.4.2 Profitability

Tauringana and Afrifa (2013) examined 133 alternative investment market listed SMEs

during 2005-2009 by employing panel data regression analysis and a questionnaire

survey. They find that the management of accounts payable and accounts receivable is

important for SMEs profitability.

Tran, Abbott and Yap (2017) studied the relationship between working capital

management and profitability in Vietnamese small- and medium-sized enterprises and

find an increase in firms’ profitability from decreasing the number of days of accounts

receivable, accounts inventories and accounts payable to an optimal minimum.

Obeidat and Jawabri (2016) investigated whether the management of WC affects the

profitability of listed construction equipment firms in Abu Dhabi Securities Exchange.

Data of all listed construction equipment firms in Abu Dhabi Securities Exchange over

the period 2006-2013, had been used in the analysis. Rate of return on total assets had

22

used as an efficient measure of profitability. Inventory management had been measured

through number of days inventory outstanding, and receivables management had been

measured through the collection period in days. Moreover, number of days payables are

outstanding is used to measure payables management. The study concluded that inventory

management significantly affects the profitability of listed construction equipment firms

which agrees with the findings of prior related researchers. The study did not find a

significant effect of receivables management on the profitability of listed construction

equipment firms in Abu Dhabi Securities Exchange. This conclusion is not in agreement

with the conclusion of some prior research. The disagreement between this conclusion

and the conclusions of some prior similar research may be attributed to the nature of the

construction equipment firms, and to the values of the society, where selling on account

are made to selected good customers. The study also concluded that payables

management has no significant effect on profitability of listed construction firms in Abu

Dhabi Securities Exchange. This conclusion is not in agreement with prior related

research. This disagreement may be attributed to the credit policy, where only few

business organizations deal with credit sales.

Kaur and Singh (2013) carried out a study regarding the improvement of the value of

firms through WC. The objective of the study was to analyse the WC performance and its

impact on the value of firms. The authors analysed 164 Indian manufacturing companies

over the period of 2000-2010. The key finding of this study is that efficient management

of WC significantly affects the profitability of firms. In more details, the study found that

there is a wide opportunity to improve the efficiency and profitability of 145 firms among

the total of 164, through the improvement of working capital management.

Nzioki et al. (2013), investigated the impact of WCM on the profitability of industrial

listed firms on NSE. They claimed that the efficient management of WC is a vital issue

for firms' survival and profitability. The study analysed 9 manufacturing listed firms in

NSE, using correlation and multiple regression methods. The study shows that the gross

operating profit is positively correlated with both of average collection period and

average payment period. The study also found a negative correlation between gross

operating profit and cash conversion cycle. The study did not show a significant

correlation between gross operating profit and inventory turnover in days.

23

2.5 Chapter Summary

This chapter has presented a review of literature regarding the relationship between

inventory management, receivables management, payables management and profitability

of SMEs in various countries. The empirical review has provided measures used and

conclusions of studies. Effective working capital management assists a firm in achieving

improved liquidity through the management of the components of receivables, inventory,

and payables. The next chapter presents the research methodology of the study.

24

CHAPTER THREE

3.0 RESEARCH METHODOLOGY

3.1 Introduction

This chapter focuses on the methodology and approaches that were used to collect data

for this research. First, it discusses the research design. Second, it outlines the target

population. Third, it discusses the sample size and sampling procedure. Fourth, it outlines

the data collection procedure and lastly it discusses the data analysis technique.

3.2 Research Design

According to Kothari (2010), research design is the conceptual structure within which

research is conducted, it constitutes the blueprint for the collection, measurement and

analysis of data, as such the design includes an outline of what the researcher will do.

According to Sekeran (2010), a research design is overall plan that is adopted in

conducting a study in order to meet the objectives. In this respect, a research design aims

at answering the research questions of a given study.

In this study, descriptive research design was applied. As noted by Mugenda and

Mugenda (2008) a descriptive research design is defined a systematic empirical approach

where the researcher has no control of the independent variables of the study. In this

respect, the observations about independent variables are done in their natural settings.

This study therefore viewed that a descriptive research design was the most suitable for

data analysis, in data collection and analysis in order to assess the role of working capital

management on the profitability of SMEs in Kenya.

3.3 Population and Sampling Design

3.3.1 Population

Target population refers to all items that a given study wishes to make inferences about.

In research, a population is defined as the total number of units from which a researcher

seeks to select a sample to carry out a study (Cooper & Schindler, 2014). According to

Mugenda and Mugenda (2008) a target population entails all items, units, elements, or

people that form the analysis of the study. This study had a target population of all the 45

small and medium enterprises that were at the Two Rivers Mall.

25

Table 3.1 Target Population

Population Category-Retail Outlets Number of Outlets Percentage

Food and Beverage 4 9

Fashion 22 49

Footwear 3 6

Electronics 3 6

Home zone 3 6

Healthcare, Hair and Beauty 3 6

Arts/ Crafts Culture 4 9

Jewelers 4 9

Total 45 100

Source: Field Survey (2020)

3.3.2 Sampling Design

A sample design is a definite plan for obtaining a sample from a given population. It

refers to the technique or the procedure the researcher would adopt in selecting items for

the sample (Kothari, 2010). A sample design is therefore the framework that serves as the

basis for the selection of a sample survey.

3.3.2.1 Sampling Frame

For this study, a sample frame is defined as the list of all elements that form a population

from which a sample is drawn (Kothari, 2004). The sampling frame is closely related to

the population. According to Cooper & Schindler, (2014) the sampling frame is the list of

elements from which the sample is drawn. The sample frame for this study was composed

of all the trading tenants at the Two Rivers Mall.

3.3.2.2 Sampling Technique

Sampling technique is defined as the way in which a group of potential respondents are

selected as part of a sample size upon which a study is conducted (Cooper & Schindler,

2014). The sampling technique is used to choose the respondents. According to Kothari

(2004), for a target population of less than 100 elements, a census is most appropriate

technique. Since this study was only composed of only 45 retail outlets, a census study

was conducted. The researcher used purposive sampling procedure to select staff

26

depending on their ability to easily analyse and understand the problem of the study. This

was because the researcher believed it was convenient and time saving.

3.3.2.3 Sample Size

Since a researcher cannot feasibly conduct a research on an entire population, particularly

if the population is too large. As such using a sample to represent the population is the

most desirable scientific way of representing a population in a study. According to

Cooper and Schindler (2014), a sample size should adequately represent the population.

Mugenda and Mugenda (2008) define a sample size as the unit representation of a

population under a study. This means that if a population is large, a researcher can select

a small sample that is scientific and use it to represent the entire population. According to

Mugenda and Mugenda (2008), a sample should comprise between 10-30% of the

population, and a good population sample should be at least 10% and not more than 30%

of the entire population. In this study, the researcher conducted a census study of the

population.

3.4 Data Collection Methods

Drop and pick questionnaires and a checklist of documentary review were the essential

data instruments that the researcher used to collect data. The questionnaire comprised of

two parts. The first part was to collect background information on gender, age, education

and working experience. The second part composed structured questions based on the

research questions to collect data from the respondents.

3.5 Research Procedure

To be able to carry out the above study, the researcher first got a letter of authorization

from United States International University - Africa. Once this had been obtained, the

researcher sought to get letters of authority from the National Commission for Science,

Technology and Innovation (NACOSTI) as well as the Institutional Review Board. Once

the approvals were in place, an introductory letter was sent to all the operational

managers of the sampled retail outlets introducing the researcher and the purpose of the

study, as well as permission and co-operation from the respondents. After this, a research

assistant was hired to go out in the field and collect raw data.

27

3.6 Data Analysis Methods

To obtain primary data, the study used a questionnaire. The quantitative data obtained in